Financial Analysis and Performance of Glow Sheets Limited

VerifiedAdded on 2020/10/22

|10

|1952

|203

Report

AI Summary

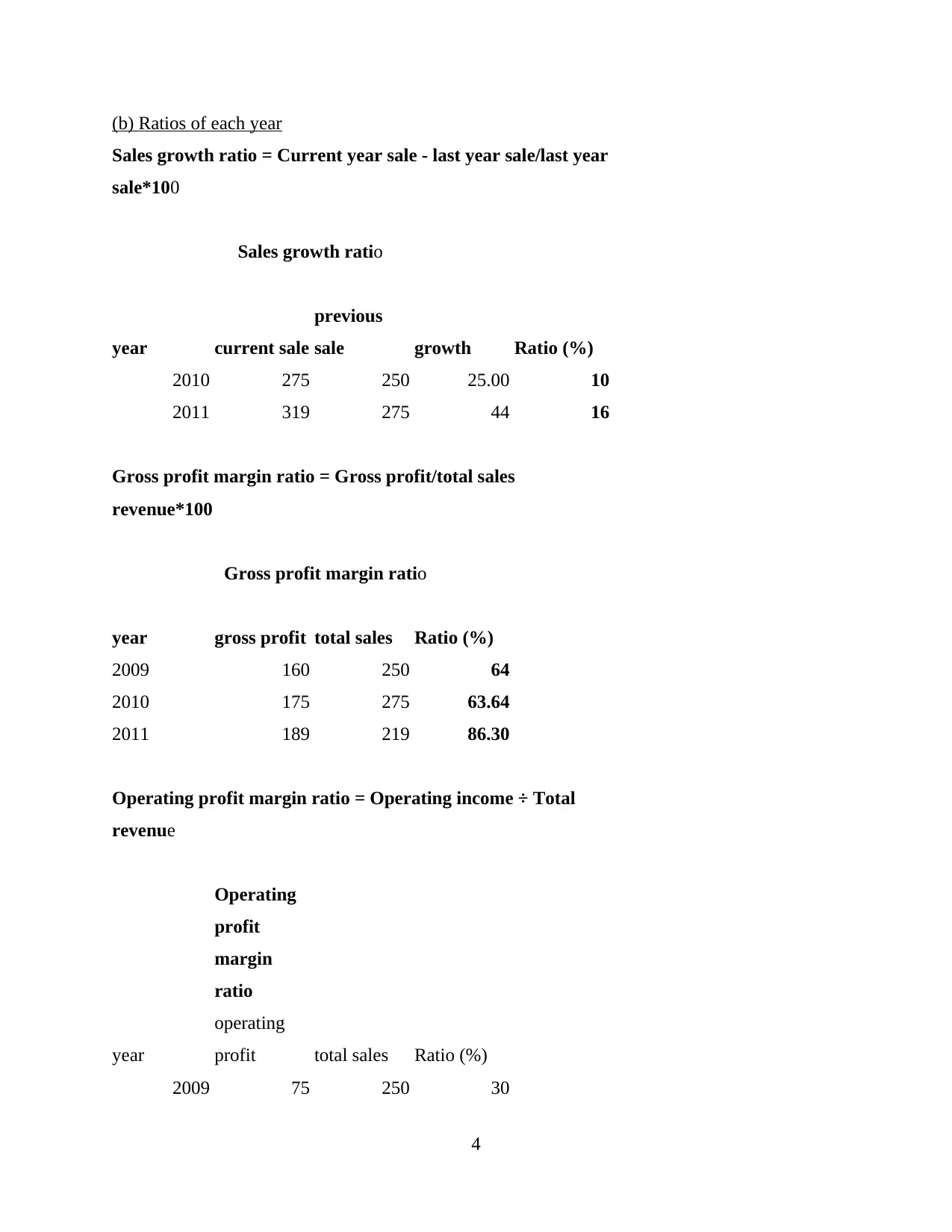

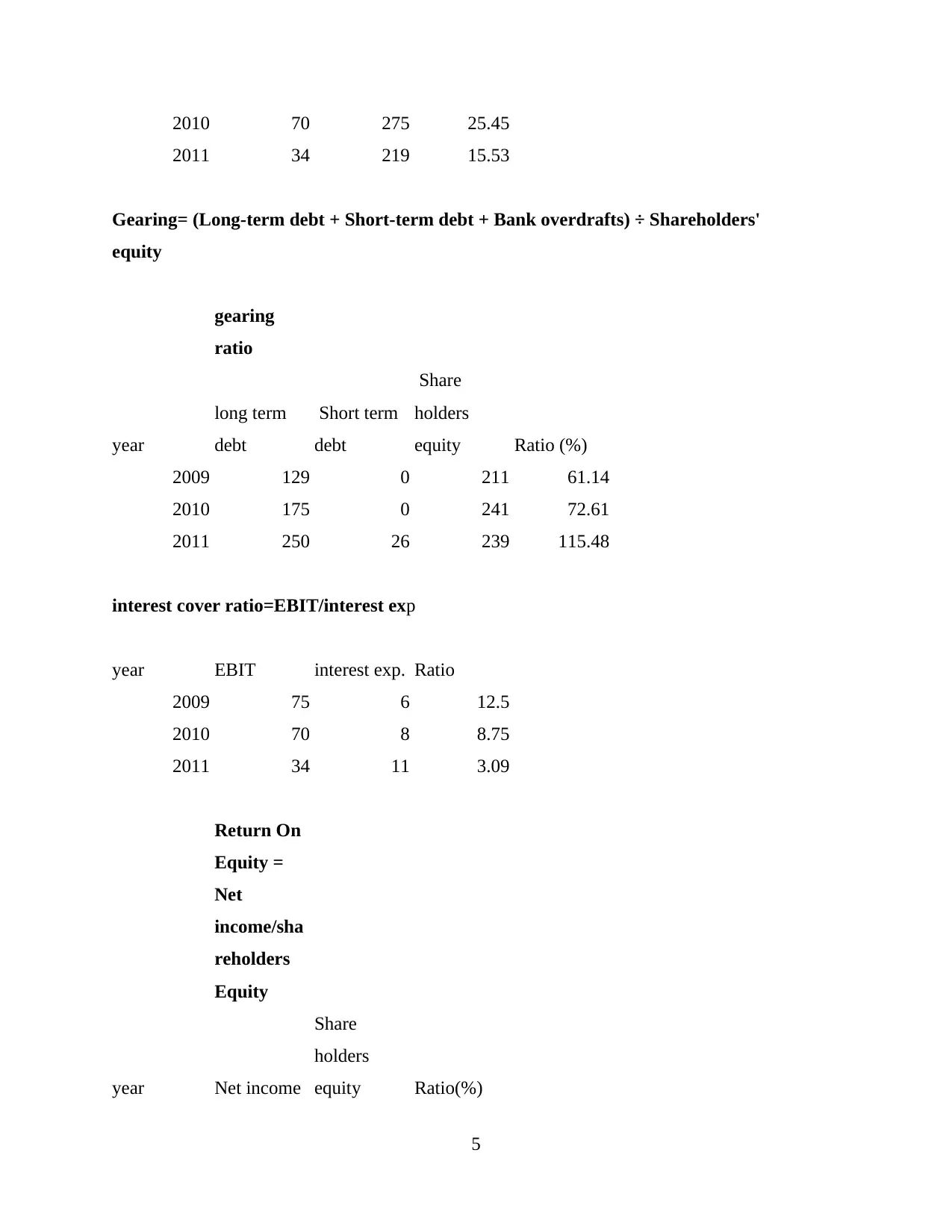

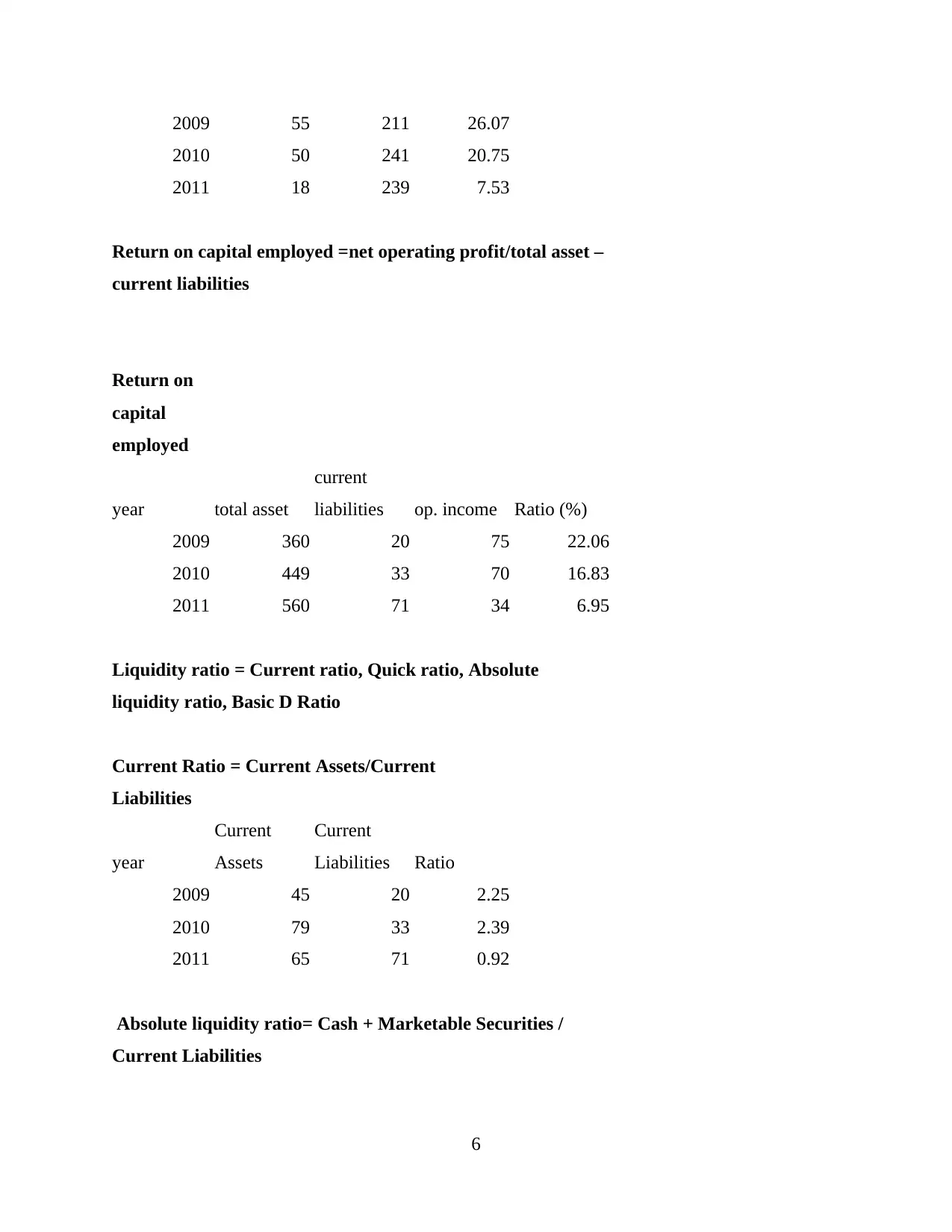

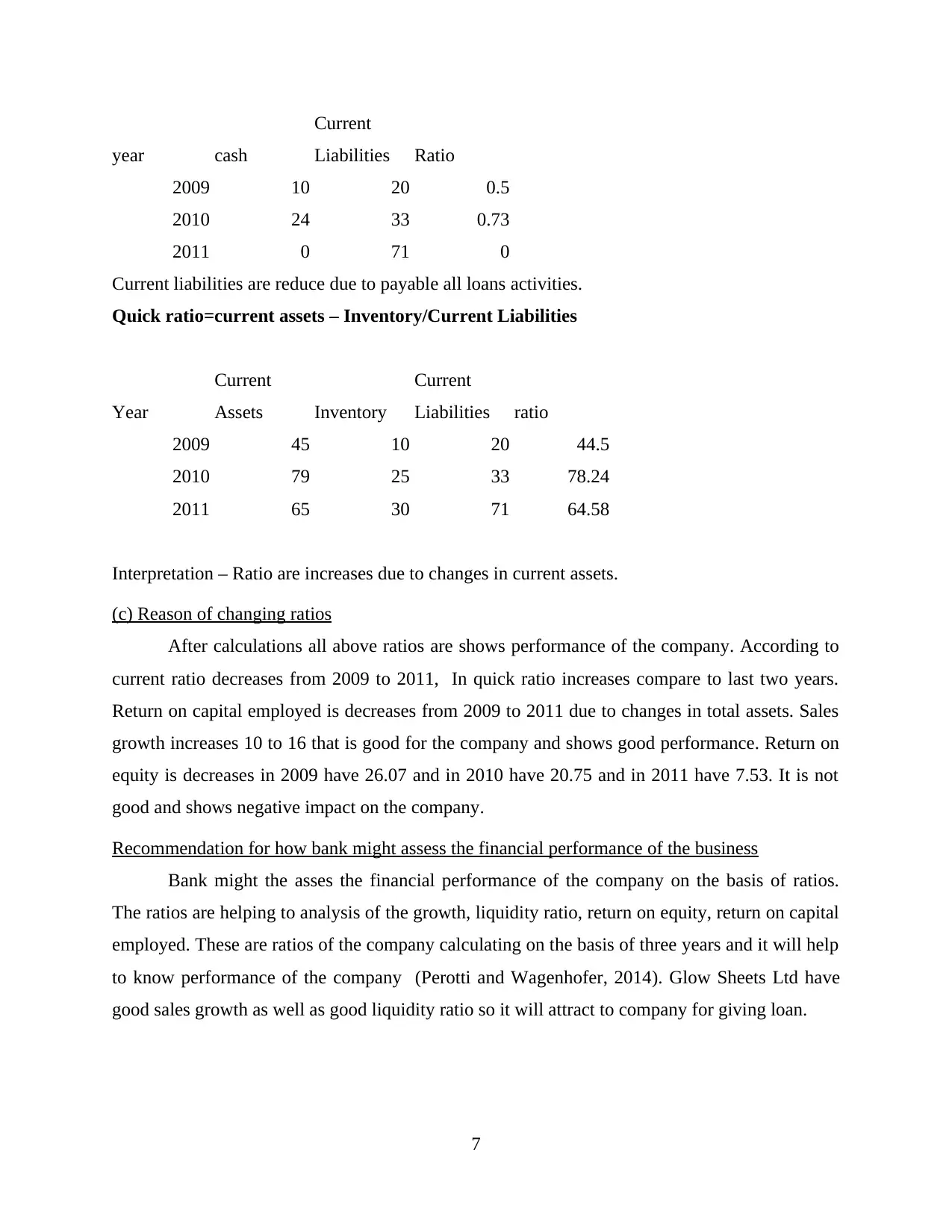

This report provides a financial performance analysis of Glow Sheets Ltd, focusing on key financial ratios from 2009 to 2011. The analysis includes calculations and interpretations of sales growth, gross profit margin, operating profit margin, gearing, interest cover, liquidity ratios (current and quick), return on equity, and return on capital employed. The report identifies the elements of financial performance, such as assets and liabilities, and examines how these ratios changed over the three-year period. The analysis highlights the company's strengths and weaknesses, recommending how a bank might assess the company's financial health based on these ratios. The conclusion summarizes the findings, emphasizing the importance of ratio analysis in understanding the company's financial position and performance. The report references various financial accounting principles and relevant academic sources.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.