Financial Performance Analysis: Accounting Concepts and Statements

VerifiedAdded on 2022/12/27

|14

|3454

|83

Homework Assignment

AI Summary

This assignment delves into the analysis of financial performance, covering various aspects of accounting and financial statements. It begins by exploring considerations when purchasing an apartment, highlighting relevant accounting information. The assignment then differentiates between accounting and management systems, emphasizing their distinct purposes and users. It further examines the fundamental differences between a sole trader, a partnership, and a company, outlining factors to consider when choosing the right business design. The core of the assignment focuses on financial statements, including the balance sheet, income statement, and cash flow statement, explaining their key features and how they reflect a company's financial health. It includes example journal entries, and explores accrual and cash accounting methods, along with the owner's equity accounts. The assignment covers topics from initial purchase considerations to the accounting treatment of revenue and expenses, providing a comprehensive overview of financial performance analysis.

Financial Performance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Topic 1

Question 1

Considerations when buying an apartment include factors such as location, type (studio, one

bedroom, two or three bedrooms), size (bigger rooms, additional bathroom, balcony), age of the

apartment, and available funds. Information to assist the purchase decision includes whether the

apartment is for residential or investment purpose, personal taste (e.g. interior design, view),

distance to workplace or train stations, funds to meet ongoing costs like repairs and maintenance

required after purchase, body corporate fees, council rates, and insurance. Initial purchase

considerations include whether the apartment is to be purchased outright or through a home loan

taken with a financial institution, stamp duty to be paid, and the eligibility of obtaining first-

home buyer grant from the federal/state government. Purchase considerations and ongoing costs

represent accounting information relevant to the decision-making process.

Question 2

Accounting and management systems have different purposes, different user centers, and

vary in the level of control that can be reported by outside business entities. Management Funds

for construction to produce external user reports, e.g. commercial lenders. These reports are

standard financial reports for reporting entities, and should therefore comply with accounting

standards. all levels of management. Reports are specific objective reports, designed to meet the

specific needs of users of those reports, and the format as well.

The content of the reports depends on who the report is for, and the purpose for which the

report is prepared. While financial accounting, reports can be annual and semi-annual,

management accounting reports are usually requested daily, weekly, monthly, or on demand.

Department The question of whether two separate systems are required depends largely on the

cost of both the financial and financial management systems are based on the accounting

framework, most of its common features. Therefore, a single account system can be used to meet

the requirements of both accounting methods.

Explain the fundamental differences between a single trader (or a single patent), a

partnership with a company. What factors need to be considered in choosing the right design for

Darren's lawn mower business? The three basic elements of a business are: Craftsmen where

1

Topic 1

Question 1

Considerations when buying an apartment include factors such as location, type (studio, one

bedroom, two or three bedrooms), size (bigger rooms, additional bathroom, balcony), age of the

apartment, and available funds. Information to assist the purchase decision includes whether the

apartment is for residential or investment purpose, personal taste (e.g. interior design, view),

distance to workplace or train stations, funds to meet ongoing costs like repairs and maintenance

required after purchase, body corporate fees, council rates, and insurance. Initial purchase

considerations include whether the apartment is to be purchased outright or through a home loan

taken with a financial institution, stamp duty to be paid, and the eligibility of obtaining first-

home buyer grant from the federal/state government. Purchase considerations and ongoing costs

represent accounting information relevant to the decision-making process.

Question 2

Accounting and management systems have different purposes, different user centers, and

vary in the level of control that can be reported by outside business entities. Management Funds

for construction to produce external user reports, e.g. commercial lenders. These reports are

standard financial reports for reporting entities, and should therefore comply with accounting

standards. all levels of management. Reports are specific objective reports, designed to meet the

specific needs of users of those reports, and the format as well.

The content of the reports depends on who the report is for, and the purpose for which the

report is prepared. While financial accounting, reports can be annual and semi-annual,

management accounting reports are usually requested daily, weekly, monthly, or on demand.

Department The question of whether two separate systems are required depends largely on the

cost of both the financial and financial management systems are based on the accounting

framework, most of its common features. Therefore, a single account system can be used to meet

the requirements of both accounting methods.

Explain the fundamental differences between a single trader (or a single patent), a

partnership with a company. What factors need to be considered in choosing the right design for

Darren's lawn mower business? The three basic elements of a business are: Craftsmen where

1

people run their own business. They would be donating their cash or equity to the business and

they would be lending money in the name of the business in their own name. They will be able to

pay off the outstanding balance of the business and, if they are unable to pay, the bank will be

able to access their assets to pay off the outstanding debt. This business building is suitable for

small jobs with small staff and income. The The sole Trader is solely responsible for the overall

operation of the business and operations. The building works for small businesses that require a

small investment to be set up and have relatively low running costs. Management Partnerships

are two or more people in a business together, operating under a partnership agreement that is

likely to be a formal written agreement. they are more profitable than individual traders because

they have a larger base of marital divorce contributions and are able to share the risks and

obligations associated with starting a business. The partnership is treated as a separate

accounting entity but not a separate legal entity. This means that the underlying assets and

liabilities of the partnership belong to the individual partners in the agreed portion as part of the

partnership agreement. Therefore, if the business is unsuccessful, lenders are entitled to receive

individual assets from their partners in the event that the entity is unable to repay any outstanding

debt. For this reason, a partnership structure is often used where there is a low level of risk to the

business or where the law stipulates that the business should be managed by service providers.

For example, professional work includes accountants and lawyers. A company is a separate law

firm that owns a company called to shares. The owners of the company are known as

shareholders. The beauty of a business structure is that, as a separate legal entity, assets and

liabilities belong to a company. In the event that a business fails to repay its debt, lenders may

only have access to the company's assets to repay the debt. Investments in a company by its

shareholders are limited to shareholder contributions, which means that the shareholder pays the

shares. This business structure is more specific to businesses that need large sums of money has

a large number of executives and employees and has a high business risk. Disadvantages include

high set-up and ongoing costs and a decrease in uncontrolled control over the operation of the

business where shareholders are not directly involved in the activities of the business which

helps for better performance which helps for higher profitability for the businesses.

Question 3

Financial statements are written records that transfer business functions and financial

performance of a company. Financial statements are often audited by government agencies,

2

they would be lending money in the name of the business in their own name. They will be able to

pay off the outstanding balance of the business and, if they are unable to pay, the bank will be

able to access their assets to pay off the outstanding debt. This business building is suitable for

small jobs with small staff and income. The The sole Trader is solely responsible for the overall

operation of the business and operations. The building works for small businesses that require a

small investment to be set up and have relatively low running costs. Management Partnerships

are two or more people in a business together, operating under a partnership agreement that is

likely to be a formal written agreement. they are more profitable than individual traders because

they have a larger base of marital divorce contributions and are able to share the risks and

obligations associated with starting a business. The partnership is treated as a separate

accounting entity but not a separate legal entity. This means that the underlying assets and

liabilities of the partnership belong to the individual partners in the agreed portion as part of the

partnership agreement. Therefore, if the business is unsuccessful, lenders are entitled to receive

individual assets from their partners in the event that the entity is unable to repay any outstanding

debt. For this reason, a partnership structure is often used where there is a low level of risk to the

business or where the law stipulates that the business should be managed by service providers.

For example, professional work includes accountants and lawyers. A company is a separate law

firm that owns a company called to shares. The owners of the company are known as

shareholders. The beauty of a business structure is that, as a separate legal entity, assets and

liabilities belong to a company. In the event that a business fails to repay its debt, lenders may

only have access to the company's assets to repay the debt. Investments in a company by its

shareholders are limited to shareholder contributions, which means that the shareholder pays the

shares. This business structure is more specific to businesses that need large sums of money has

a large number of executives and employees and has a high business risk. Disadvantages include

high set-up and ongoing costs and a decrease in uncontrolled control over the operation of the

business where shareholders are not directly involved in the activities of the business which

helps for better performance which helps for higher profitability for the businesses.

Question 3

Financial statements are written records that transfer business functions and financial

performance of a company. Financial statements are often audited by government agencies,

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

accountants, firms, etc. to ensure accuracy and tax revenue, financing, or for investment

purposes. The financial statements include:

Balance Sheet: It includes the liabilities, assets for the company for knowing its funds which

helps company for better performance which helps for higher profitability for the businesses.

Income statement: It views the expenses, income for the company’s for knowing the profits

which helps company for better performance which helps for higher profitability for the

businesses.

Cash flow statement

1 Income statement

Usually, the first place an investor or analyst will look at is the income statement. The income

statement shows the performance of the business in each period, indicating a very high sales

revenue. The statement then deducts the cost of the goods sold (COGS) for the full benefit. From

there, total profit is affected by other operating costs and revenue, depending on the type of

business, access to lower income - the “basic” business.

Key features:

It shows the income and expenses of the business

Indicated at a specific time (e.g., 1 year, 1 quarter, year and day, etc.)

Uses accounting principles such as matching and accumulating representations (not provided in

cash)

Used for profit testing

# 2 Balance Sheet

The balance reflects the company's assets, liabilities, and equity of shareholders over a period of

time. As is well known, assets should be equal to debt and equity. The asset class starts with cash

and equity, which should be equal to the balance found at the end of the cash flow statement. The

balance then reflects the changes in each major account from time to time. Revenue from income

statement into balance as a change in earnings (for dividends)

3

purposes. The financial statements include:

Balance Sheet: It includes the liabilities, assets for the company for knowing its funds which

helps company for better performance which helps for higher profitability for the businesses.

Income statement: It views the expenses, income for the company’s for knowing the profits

which helps company for better performance which helps for higher profitability for the

businesses.

Cash flow statement

1 Income statement

Usually, the first place an investor or analyst will look at is the income statement. The income

statement shows the performance of the business in each period, indicating a very high sales

revenue. The statement then deducts the cost of the goods sold (COGS) for the full benefit. From

there, total profit is affected by other operating costs and revenue, depending on the type of

business, access to lower income - the “basic” business.

Key features:

It shows the income and expenses of the business

Indicated at a specific time (e.g., 1 year, 1 quarter, year and day, etc.)

Uses accounting principles such as matching and accumulating representations (not provided in

cash)

Used for profit testing

# 2 Balance Sheet

The balance reflects the company's assets, liabilities, and equity of shareholders over a period of

time. As is well known, assets should be equal to debt and equity. The asset class starts with cash

and equity, which should be equal to the balance found at the end of the cash flow statement. The

balance then reflects the changes in each major account from time to time. Revenue from income

statement into balance as a change in earnings (for dividends)

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Key features:

Indicates the financial status of the business

Revealed as a "summary" or company financial image for a period of time (e.g., as of December

31, 2017)

It has three categories: assets, liabilities, and equity of shareholders

Assets = Liabilities + Shareholder Equity

# 3 Cash flow statement

Cash flow statement then take the income and adjust it to any non-cash expenses. After that, with

the changes in the balance sheet, the use and acquisition of funds are available. The cash flow

statement shows the currency change for each period, as well as the initial balance and end

balance of the cash.

Key features:

It shows an increase and decrease in cash

Indicated at a specific time, accounting period (e.g., 1 year, 1 quarter, year and day, etc.)

It reverses all accounting principles to reflect pure cash flow

It has three categories: operating income, capital investment, and cash flow

It shows the change in value in the balance of money from the beginning to the end of the period.

TOPIC 2

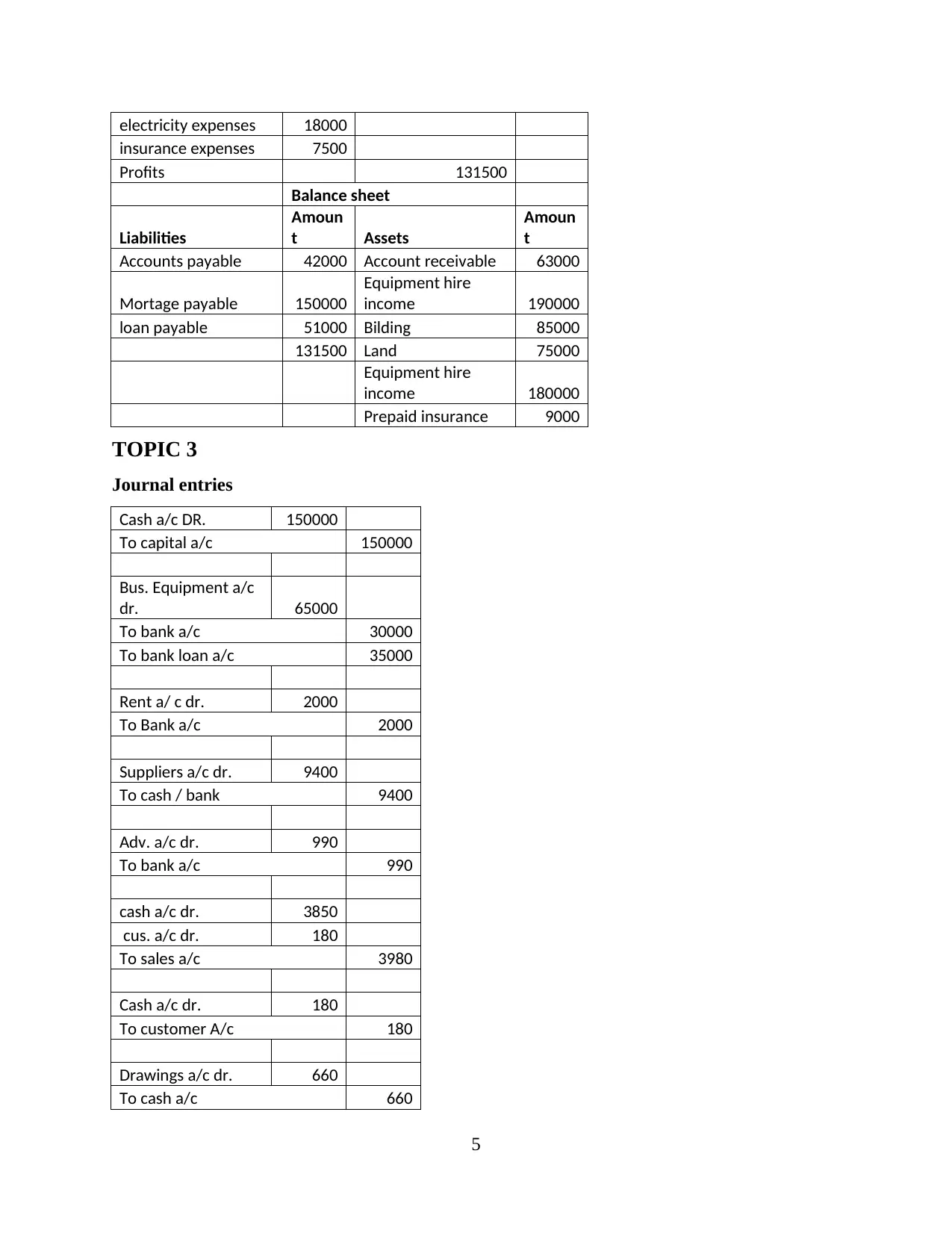

Question 1

Income statement

Particulars Debit Credit

Interest revenue 8000

Wages 75000

Advertising expenses 30000

prepaid insurance 9000

4

Indicates the financial status of the business

Revealed as a "summary" or company financial image for a period of time (e.g., as of December

31, 2017)

It has three categories: assets, liabilities, and equity of shareholders

Assets = Liabilities + Shareholder Equity

# 3 Cash flow statement

Cash flow statement then take the income and adjust it to any non-cash expenses. After that, with

the changes in the balance sheet, the use and acquisition of funds are available. The cash flow

statement shows the currency change for each period, as well as the initial balance and end

balance of the cash.

Key features:

It shows an increase and decrease in cash

Indicated at a specific time, accounting period (e.g., 1 year, 1 quarter, year and day, etc.)

It reverses all accounting principles to reflect pure cash flow

It has three categories: operating income, capital investment, and cash flow

It shows the change in value in the balance of money from the beginning to the end of the period.

TOPIC 2

Question 1

Income statement

Particulars Debit Credit

Interest revenue 8000

Wages 75000

Advertising expenses 30000

prepaid insurance 9000

4

electricity expenses 18000

insurance expenses 7500

Profits 131500

Balance sheet

Liabilities

Amoun

t Assets

Amoun

t

Accounts payable 42000 Account receivable 63000

Mortage payable 150000

Equipment hire

income 190000

loan payable 51000 Bilding 85000

131500 Land 75000

Equipment hire

income 180000

Prepaid insurance 9000

TOPIC 3

Journal entries

Cash a/c DR. 150000

To capital a/c 150000

Bus. Equipment a/c

dr. 65000

To bank a/c 30000

To bank loan a/c 35000

Rent a/ c dr. 2000

To Bank a/c 2000

Suppliers a/c dr. 9400

To cash / bank 9400

Adv. a/c dr. 990

To bank a/c 990

cash a/c dr. 3850

cus. a/c dr. 180

To sales a/c 3980

Cash a/c dr. 180

To customer A/c 180

Drawings a/c dr. 660

To cash a/c 660

5

insurance expenses 7500

Profits 131500

Balance sheet

Liabilities

Amoun

t Assets

Amoun

t

Accounts payable 42000 Account receivable 63000

Mortage payable 150000

Equipment hire

income 190000

loan payable 51000 Bilding 85000

131500 Land 75000

Equipment hire

income 180000

Prepaid insurance 9000

TOPIC 3

Journal entries

Cash a/c DR. 150000

To capital a/c 150000

Bus. Equipment a/c

dr. 65000

To bank a/c 30000

To bank loan a/c 35000

Rent a/ c dr. 2000

To Bank a/c 2000

Suppliers a/c dr. 9400

To cash / bank 9400

Adv. a/c dr. 990

To bank a/c 990

cash a/c dr. 3850

cus. a/c dr. 180

To sales a/c 3980

Cash a/c dr. 180

To customer A/c 180

Drawings a/c dr. 660

To cash a/c 660

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

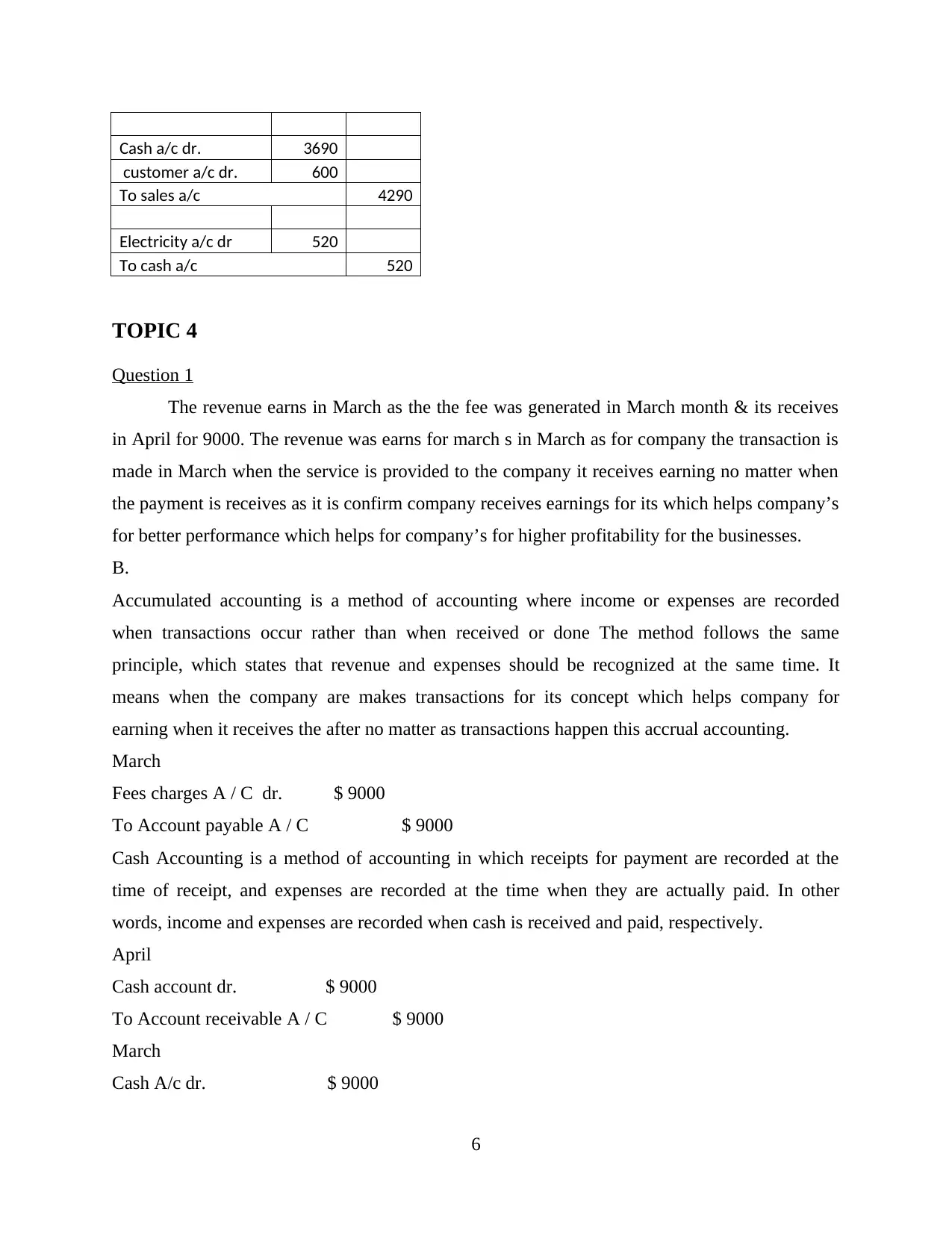

Cash a/c dr. 3690

customer a/c dr. 600

To sales a/c 4290

Electricity a/c dr 520

To cash a/c 520

TOPIC 4

Question 1

The revenue earns in March as the the fee was generated in March month & its receives

in April for 9000. The revenue was earns for march s in March as for company the transaction is

made in March when the service is provided to the company it receives earning no matter when

the payment is receives as it is confirm company receives earnings for its which helps company’s

for better performance which helps for company’s for higher profitability for the businesses.

B.

Accumulated accounting is a method of accounting where income or expenses are recorded

when transactions occur rather than when received or done The method follows the same

principle, which states that revenue and expenses should be recognized at the same time. It

means when the company are makes transactions for its concept which helps company for

earning when it receives the after no matter as transactions happen this accrual accounting.

March

Fees charges A / C dr. $ 9000

To Account payable A / C $ 9000

Cash Accounting is a method of accounting in which receipts for payment are recorded at the

time of receipt, and expenses are recorded at the time when they are actually paid. In other

words, income and expenses are recorded when cash is received and paid, respectively.

April

Cash account dr. $ 9000

To Account receivable A / C $ 9000

March

Cash A/c dr. $ 9000

6

customer a/c dr. 600

To sales a/c 4290

Electricity a/c dr 520

To cash a/c 520

TOPIC 4

Question 1

The revenue earns in March as the the fee was generated in March month & its receives

in April for 9000. The revenue was earns for march s in March as for company the transaction is

made in March when the service is provided to the company it receives earning no matter when

the payment is receives as it is confirm company receives earnings for its which helps company’s

for better performance which helps for company’s for higher profitability for the businesses.

B.

Accumulated accounting is a method of accounting where income or expenses are recorded

when transactions occur rather than when received or done The method follows the same

principle, which states that revenue and expenses should be recognized at the same time. It

means when the company are makes transactions for its concept which helps company for

earning when it receives the after no matter as transactions happen this accrual accounting.

March

Fees charges A / C dr. $ 9000

To Account payable A / C $ 9000

Cash Accounting is a method of accounting in which receipts for payment are recorded at the

time of receipt, and expenses are recorded at the time when they are actually paid. In other

words, income and expenses are recorded when cash is received and paid, respectively.

April

Cash account dr. $ 9000

To Account receivable A / C $ 9000

March

Cash A/c dr. $ 9000

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To Fees charges A / C dr. $ 9000

TOPIC 5

Question 1

The draw or withdrawal account for a patent is a temporary owner’s account that is closed at the

end of the accounting year. The drawing account is also an account that is in conflict with the

equity of the owner, because the debit balance of the drawing account conflicts with the normal

credit balance of the owner's account.

At the end of the accounting year, the drawing account is closed directly to the primary account

with an entry that removes the principal account and includes the draw account of the owner.

Please note that the drawing owner account is not a cost and is therefore not closed to the Income

Summary account and the money will not appear on the company's income statement.

Question 2

Equity accounts are financial representations of business ownership. Money can come from

payments to the business by its owners, or from residual income generated by the business. Due

to the different sources of equity funds, equity is maintained in different types of accounts.

All financial accounts, with the exception of the accountant's account, have natural rates of debt.

If the savings account has a debit balance, this means that it is possible that the entity has

experienced a loss, or that the entity has issued more shares than it would have earned on

savings. The following accounts are mostly used by companies.

Normal Stock

Ordinary stock A limited amount of stock sold directly to investors. Par value is usually very

small or non-existent, so the balance in this account may be small.

Preferred Stock

Preferred stock A limited amount of preferred stock. These shares have special rights and

privileges beyond those granted on ordinary stock. Some organizations have never issued a

7

TOPIC 5

Question 1

The draw or withdrawal account for a patent is a temporary owner’s account that is closed at the

end of the accounting year. The drawing account is also an account that is in conflict with the

equity of the owner, because the debit balance of the drawing account conflicts with the normal

credit balance of the owner's account.

At the end of the accounting year, the drawing account is closed directly to the primary account

with an entry that removes the principal account and includes the draw account of the owner.

Please note that the drawing owner account is not a cost and is therefore not closed to the Income

Summary account and the money will not appear on the company's income statement.

Question 2

Equity accounts are financial representations of business ownership. Money can come from

payments to the business by its owners, or from residual income generated by the business. Due

to the different sources of equity funds, equity is maintained in different types of accounts.

All financial accounts, with the exception of the accountant's account, have natural rates of debt.

If the savings account has a debit balance, this means that it is possible that the entity has

experienced a loss, or that the entity has issued more shares than it would have earned on

savings. The following accounts are mostly used by companies.

Normal Stock

Ordinary stock A limited amount of stock sold directly to investors. Par value is usually very

small or non-existent, so the balance in this account may be small.

Preferred Stock

Preferred stock A limited amount of preferred stock. These shares have special rights and

privileges beyond those granted on ordinary stock. Some organizations have never issued a

7

preferred stock, while others may have issued certain portions of it. A key feature of popular

stock is the payment of fixed dividends, which makes this a safe investment for investors.

Additional Paid Capital

The overpayment is the amount paid to the investors in excess of the estimated amount of stock

sold directly to them by the issuer. The balance in this account can be quite high, especially

considering the small number of stocks that have been awarded multiple stock certificates.

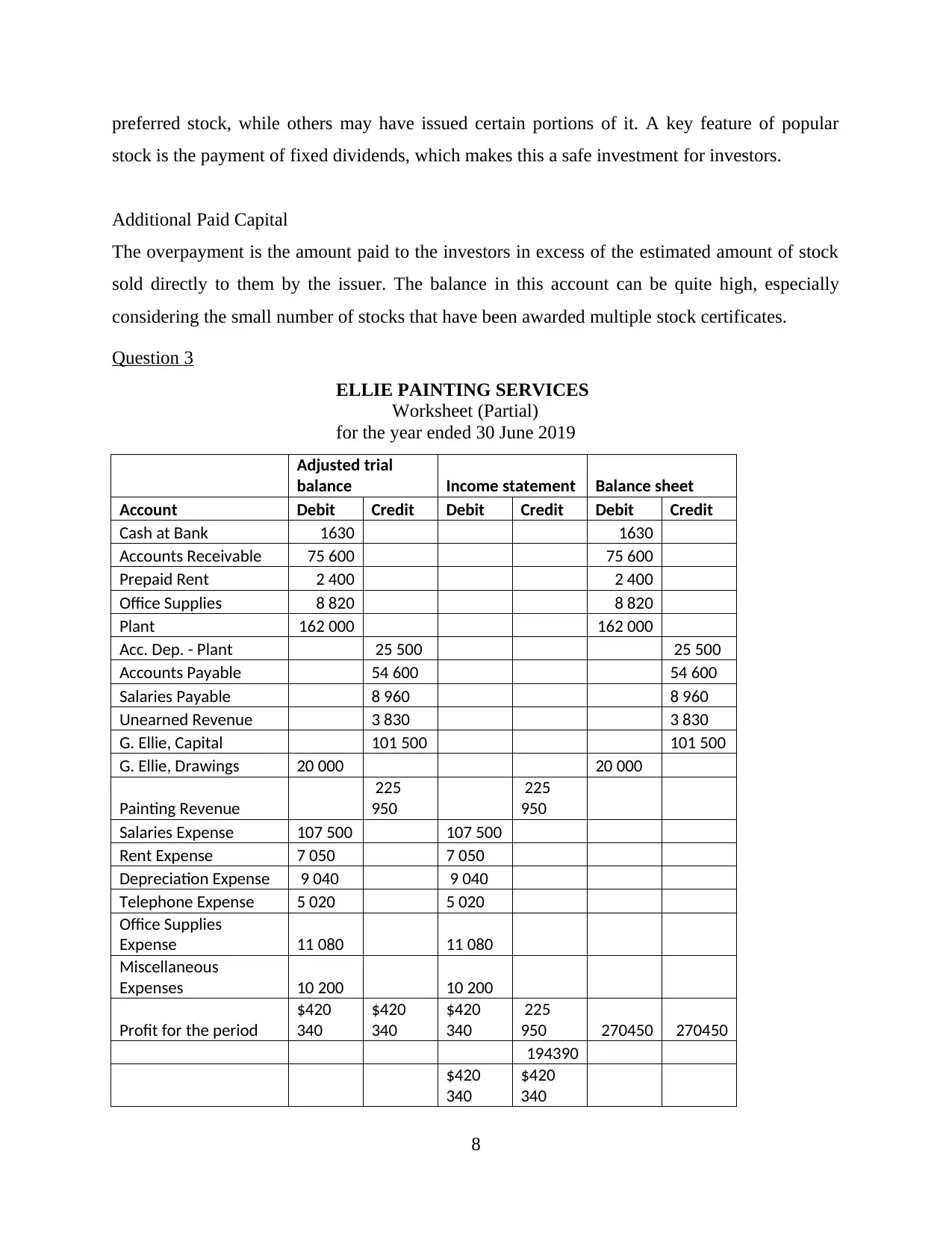

Question 3

ELLIE PAINTING SERVICES

Worksheet (Partial)

for the year ended 30 June 2019

Adjusted trial

balance Income statement Balance sheet

Account Debit Credit Debit Credit Debit Credit

Cash at Bank 1630 1630

Accounts Receivable 75 600 75 600

Prepaid Rent 2 400 2 400

Office Supplies 8 820 8 820

Plant 162 000 162 000

Acc. Dep. - Plant 25 500 25 500

Accounts Payable 54 600 54 600

Salaries Payable 8 960 8 960

Unearned Revenue 3 830 3 830

G. Ellie, Capital 101 500 101 500

G. Ellie, Drawings 20 000 20 000

Painting Revenue

225

950

225

950

Salaries Expense 107 500 107 500

Rent Expense 7 050 7 050

Depreciation Expense 9 040 9 040

Telephone Expense 5 020 5 020

Office Supplies

Expense 11 080 11 080

Miscellaneous

Expenses 10 200 10 200

Profit for the period

$420

340

$420

340

$420

340

225

950 270450 270450

194390

$420

340

$420

340

8

stock is the payment of fixed dividends, which makes this a safe investment for investors.

Additional Paid Capital

The overpayment is the amount paid to the investors in excess of the estimated amount of stock

sold directly to them by the issuer. The balance in this account can be quite high, especially

considering the small number of stocks that have been awarded multiple stock certificates.

Question 3

ELLIE PAINTING SERVICES

Worksheet (Partial)

for the year ended 30 June 2019

Adjusted trial

balance Income statement Balance sheet

Account Debit Credit Debit Credit Debit Credit

Cash at Bank 1630 1630

Accounts Receivable 75 600 75 600

Prepaid Rent 2 400 2 400

Office Supplies 8 820 8 820

Plant 162 000 162 000

Acc. Dep. - Plant 25 500 25 500

Accounts Payable 54 600 54 600

Salaries Payable 8 960 8 960

Unearned Revenue 3 830 3 830

G. Ellie, Capital 101 500 101 500

G. Ellie, Drawings 20 000 20 000

Painting Revenue

225

950

225

950

Salaries Expense 107 500 107 500

Rent Expense 7 050 7 050

Depreciation Expense 9 040 9 040

Telephone Expense 5 020 5 020

Office Supplies

Expense 11 080 11 080

Miscellaneous

Expenses 10 200 10 200

Profit for the period

$420

340

$420

340

$420

340

225

950 270450 270450

194390

$420

340

$420

340

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TOPIC 6

Question 1

Internal control is a process or process put in place to protect assets, promote efficiency,

and ensure accurate accounting and record keeping. An operating system can prevent and detect

errors and malfunctions. Although the gold standard for disaster risk management and internal

control systems is represented by the Sarbanes-Oxley law and the chairmanship of the Charitable

Organizations Committee (COSO), not all regulatory functions are feasible. In practice the size

and type of internal control will depend on the size and size of the business.

The internal control process can be as simple as getting a training procedures manual (e.g.,

submitting cost reports), requiring a username and password to log in to the system, or

performing a monthly bank reconciliation.

Limitations: The absolute limit of internal control is the idea that in all well-designed

internal systems, there will be limitations. Controls may cease to operate or not function as

intended if the employee does not understand the internal control procedures, or if the employee

has good intentions but misjudges the value of the control and then passes it on. The employee

may also allow the employee to go beyond control or be transported to the cutting rooms to meet

deadlines. For example, in order to meet pay cuts, employee pay rates and hours may not be

subject to due diligence and pre-pay evaluation.

In addition, overuse of control systems can cause damage and lead to poor performance,

indicating that they are expensive over time. If the controls have too much control and make

daily tasks too difficult, employees may ignore them or try to escape control.

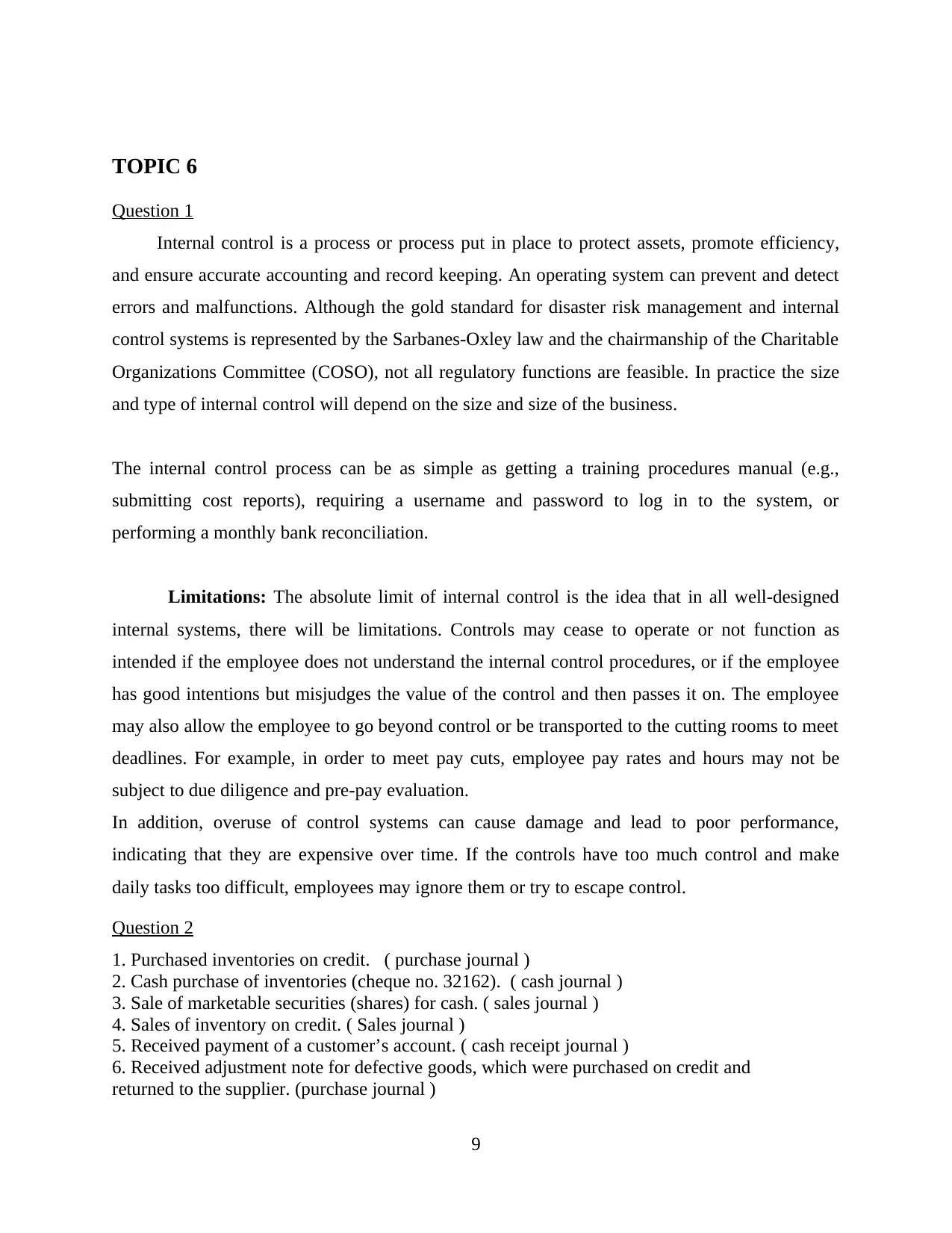

Question 2

1. Purchased inventories on credit. ( purchase journal )

2. Cash purchase of inventories (cheque no. 32162). ( cash journal )

3. Sale of marketable securities (shares) for cash. ( sales journal )

4. Sales of inventory on credit. ( Sales journal )

5. Received payment of a customer’s account. ( cash receipt journal )

6. Received adjustment note for defective goods, which were purchased on credit and

returned to the supplier. (purchase journal )

9

Question 1

Internal control is a process or process put in place to protect assets, promote efficiency,

and ensure accurate accounting and record keeping. An operating system can prevent and detect

errors and malfunctions. Although the gold standard for disaster risk management and internal

control systems is represented by the Sarbanes-Oxley law and the chairmanship of the Charitable

Organizations Committee (COSO), not all regulatory functions are feasible. In practice the size

and type of internal control will depend on the size and size of the business.

The internal control process can be as simple as getting a training procedures manual (e.g.,

submitting cost reports), requiring a username and password to log in to the system, or

performing a monthly bank reconciliation.

Limitations: The absolute limit of internal control is the idea that in all well-designed

internal systems, there will be limitations. Controls may cease to operate or not function as

intended if the employee does not understand the internal control procedures, or if the employee

has good intentions but misjudges the value of the control and then passes it on. The employee

may also allow the employee to go beyond control or be transported to the cutting rooms to meet

deadlines. For example, in order to meet pay cuts, employee pay rates and hours may not be

subject to due diligence and pre-pay evaluation.

In addition, overuse of control systems can cause damage and lead to poor performance,

indicating that they are expensive over time. If the controls have too much control and make

daily tasks too difficult, employees may ignore them or try to escape control.

Question 2

1. Purchased inventories on credit. ( purchase journal )

2. Cash purchase of inventories (cheque no. 32162). ( cash journal )

3. Sale of marketable securities (shares) for cash. ( sales journal )

4. Sales of inventory on credit. ( Sales journal )

5. Received payment of a customer’s account. ( cash receipt journal )

6. Received adjustment note for defective goods, which were purchased on credit and

returned to the supplier. (purchase journal )

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7. Owner withdrew cash. ( cash journal )

8. Payment of monthly rent by cheque. ( general journal )

9. Cash refund to a customer who returned inventory. ( cash journal )

10. Year-end closing entries. ( general journal )

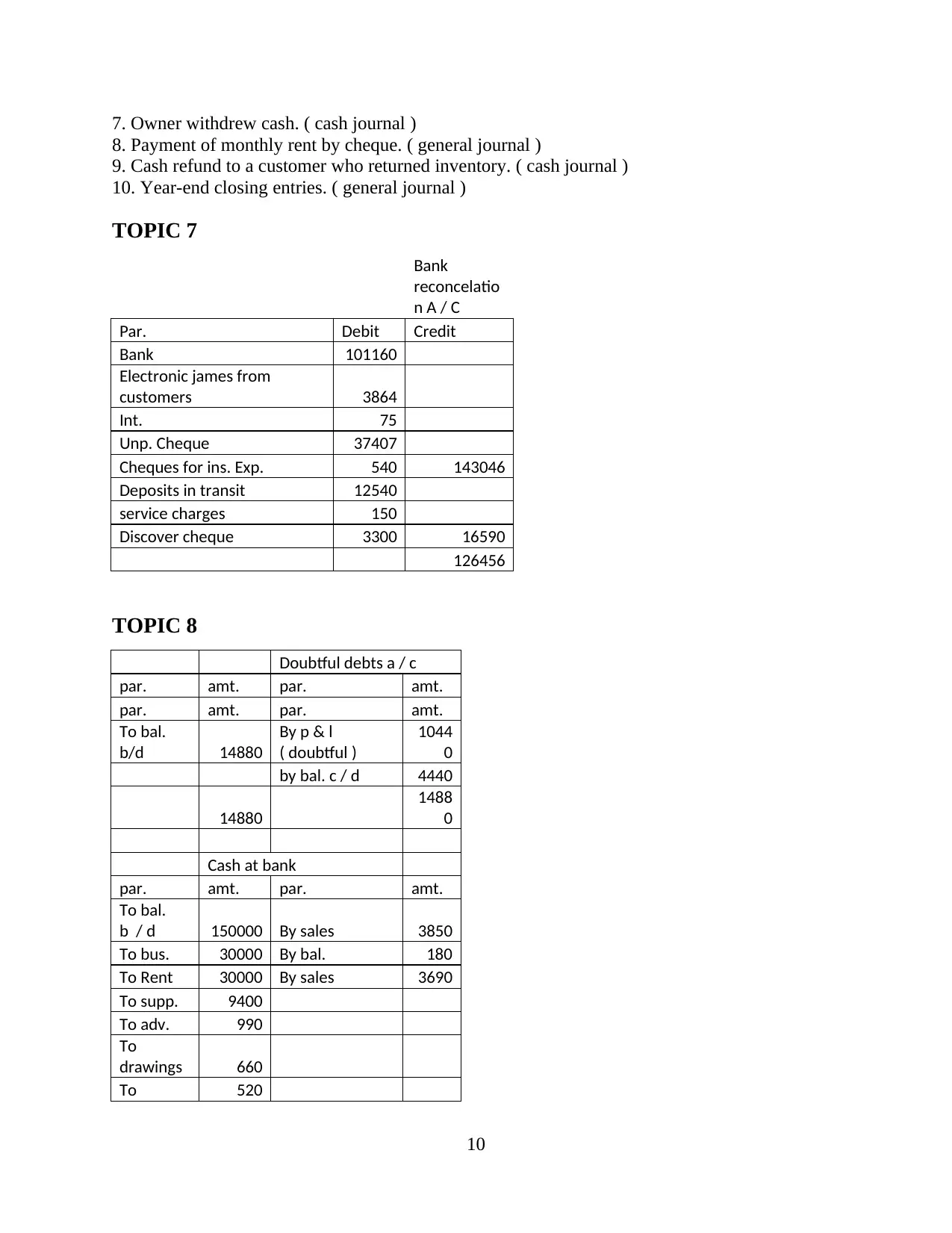

TOPIC 7

Bank

reconcelatio

n A / C

Par. Debit Credit

Bank 101160

Electronic james from

customers 3864

Int. 75

Unp. Cheque 37407

Cheques for ins. Exp. 540 143046

Deposits in transit 12540

service charges 150

Discover cheque 3300 16590

126456

TOPIC 8

Doubtful debts a / c

par. amt. par. amt.

par. amt. par. amt.

To bal.

b/d 14880

By p & l

( doubtful )

1044

0

by bal. c / d 4440

14880

1488

0

Cash at bank

par. amt. par. amt.

To bal.

b / d 150000 By sales 3850

To bus. 30000 By bal. 180

To Rent 30000 By sales 3690

To supp. 9400

To adv. 990

To

drawings 660

To 520

10

8. Payment of monthly rent by cheque. ( general journal )

9. Cash refund to a customer who returned inventory. ( cash journal )

10. Year-end closing entries. ( general journal )

TOPIC 7

Bank

reconcelatio

n A / C

Par. Debit Credit

Bank 101160

Electronic james from

customers 3864

Int. 75

Unp. Cheque 37407

Cheques for ins. Exp. 540 143046

Deposits in transit 12540

service charges 150

Discover cheque 3300 16590

126456

TOPIC 8

Doubtful debts a / c

par. amt. par. amt.

par. amt. par. amt.

To bal.

b/d 14880

By p & l

( doubtful )

1044

0

by bal. c / d 4440

14880

1488

0

Cash at bank

par. amt. par. amt.

To bal.

b / d 150000 By sales 3850

To bus. 30000 By bal. 180

To Rent 30000 By sales 3690

To supp. 9400

To adv. 990

To

drawings 660

To 520

10

electricity

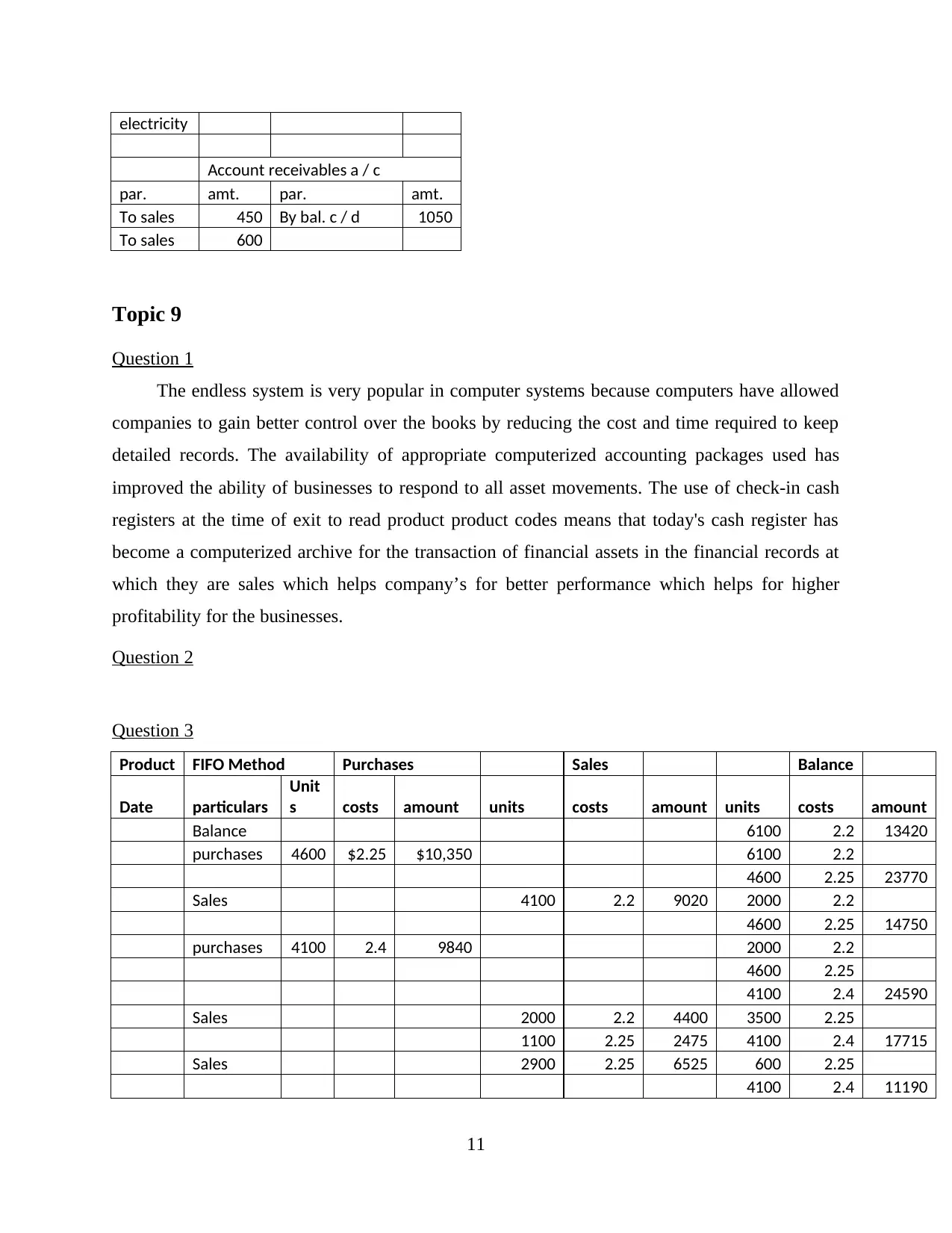

Account receivables a / c

par. amt. par. amt.

To sales 450 By bal. c / d 1050

To sales 600

Topic 9

Question 1

The endless system is very popular in computer systems because computers have allowed

companies to gain better control over the books by reducing the cost and time required to keep

detailed records. The availability of appropriate computerized accounting packages used has

improved the ability of businesses to respond to all asset movements. The use of check-in cash

registers at the time of exit to read product product codes means that today's cash register has

become a computerized archive for the transaction of financial assets in the financial records at

which they are sales which helps company’s for better performance which helps for higher

profitability for the businesses.

Question 2

Question 3

Product FIFO Method Purchases Sales Balance

Date particulars

Unit

s costs amount units costs amount units costs amount

Balance 6100 2.2 13420

purchases 4600 $2.25 $10,350 6100 2.2

4600 2.25 23770

Sales 4100 2.2 9020 2000 2.2

4600 2.25 14750

purchases 4100 2.4 9840 2000 2.2

4600 2.25

4100 2.4 24590

Sales 2000 2.2 4400 3500 2.25

1100 2.25 2475 4100 2.4 17715

Sales 2900 2.25 6525 600 2.25

4100 2.4 11190

11

Account receivables a / c

par. amt. par. amt.

To sales 450 By bal. c / d 1050

To sales 600

Topic 9

Question 1

The endless system is very popular in computer systems because computers have allowed

companies to gain better control over the books by reducing the cost and time required to keep

detailed records. The availability of appropriate computerized accounting packages used has

improved the ability of businesses to respond to all asset movements. The use of check-in cash

registers at the time of exit to read product product codes means that today's cash register has

become a computerized archive for the transaction of financial assets in the financial records at

which they are sales which helps company’s for better performance which helps for higher

profitability for the businesses.

Question 2

Question 3

Product FIFO Method Purchases Sales Balance

Date particulars

Unit

s costs amount units costs amount units costs amount

Balance 6100 2.2 13420

purchases 4600 $2.25 $10,350 6100 2.2

4600 2.25 23770

Sales 4100 2.2 9020 2000 2.2

4600 2.25 14750

purchases 4100 2.4 9840 2000 2.2

4600 2.25

4100 2.4 24590

Sales 2000 2.2 4400 3500 2.25

1100 2.25 2475 4100 2.4 17715

Sales 2900 2.25 6525 600 2.25

4100 2.4 11190

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.