Recording Business Transactions: Financial Analysis Report, Oxford

VerifiedAdded on 2022/12/28

|16

|2518

|85

Report

AI Summary

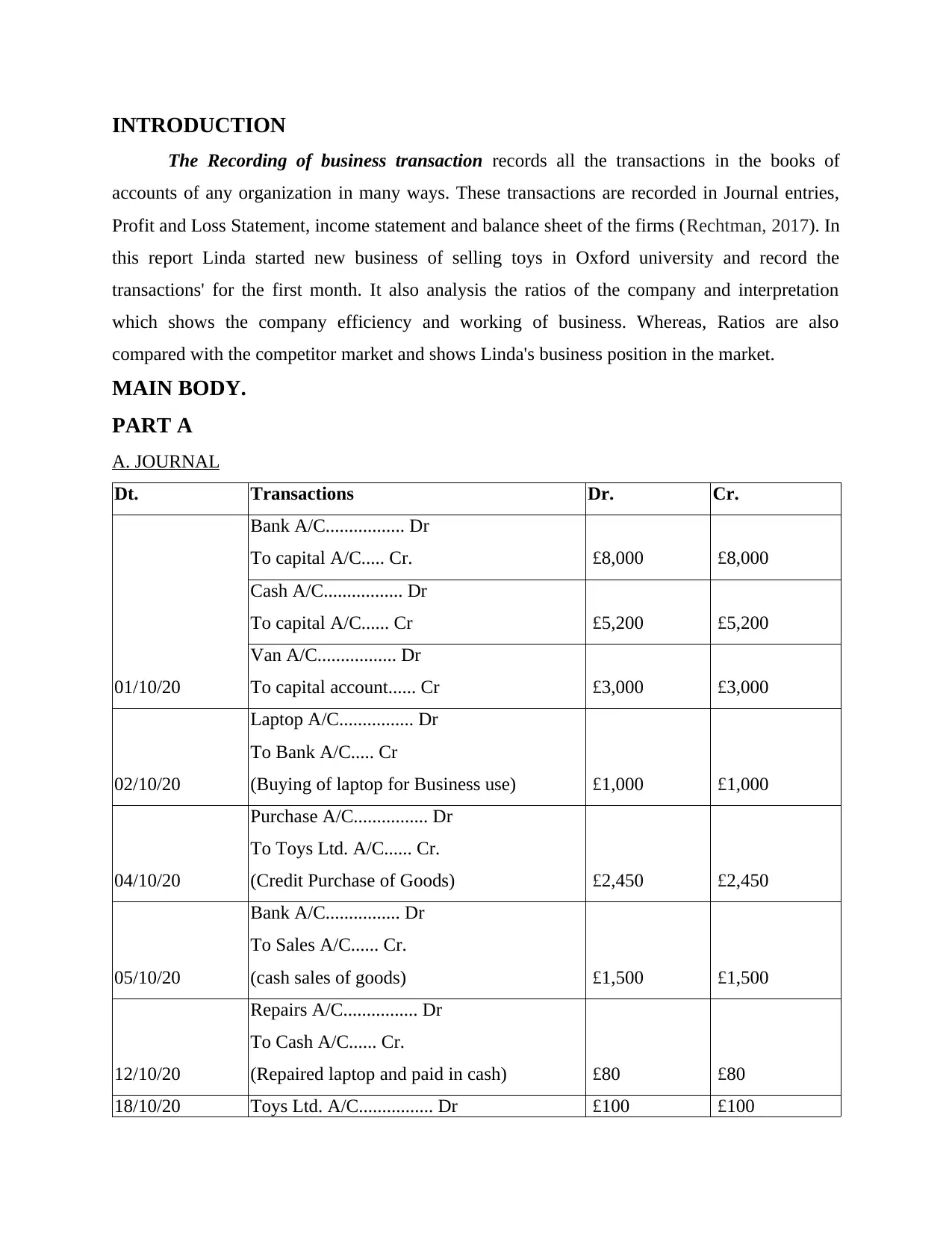

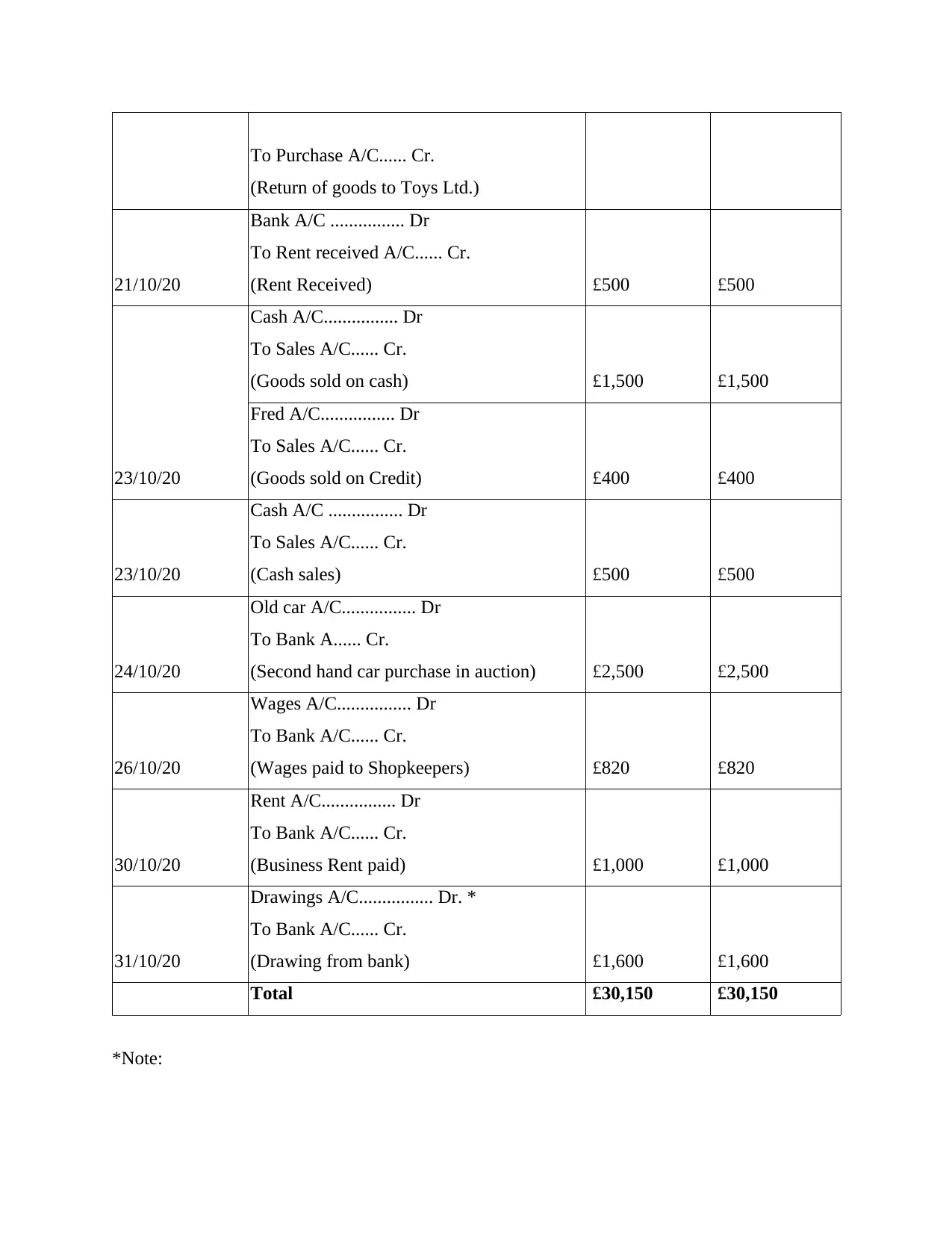

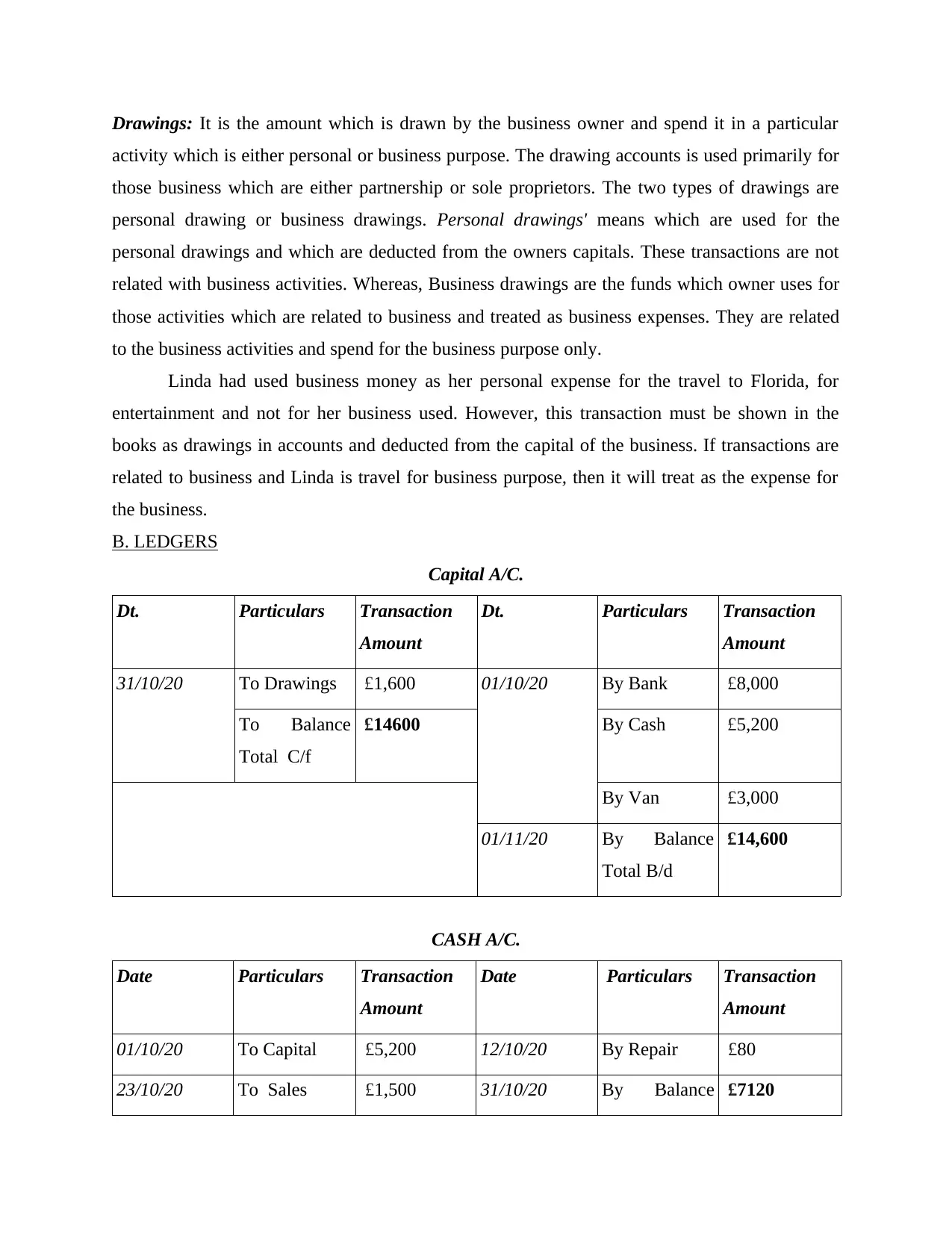

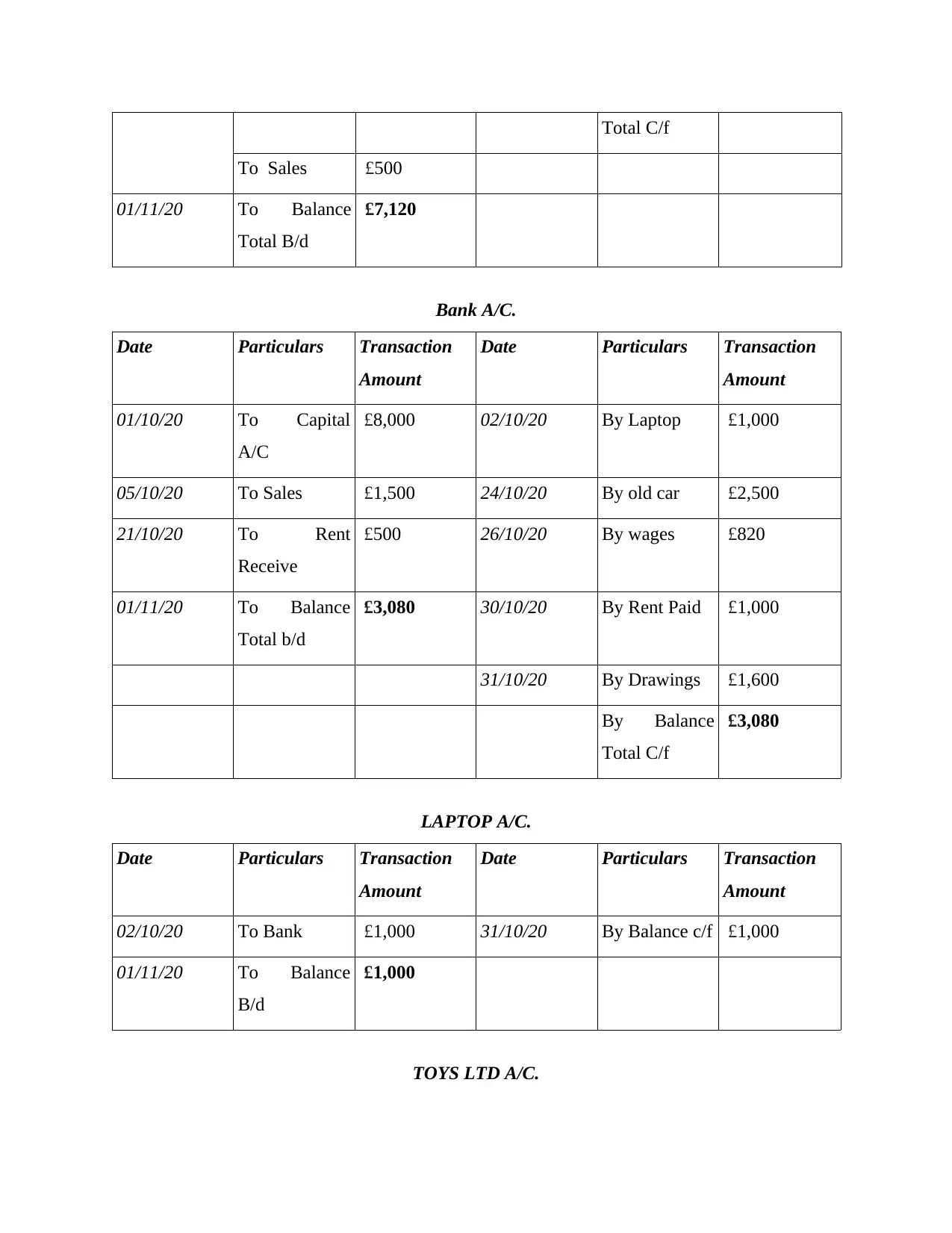

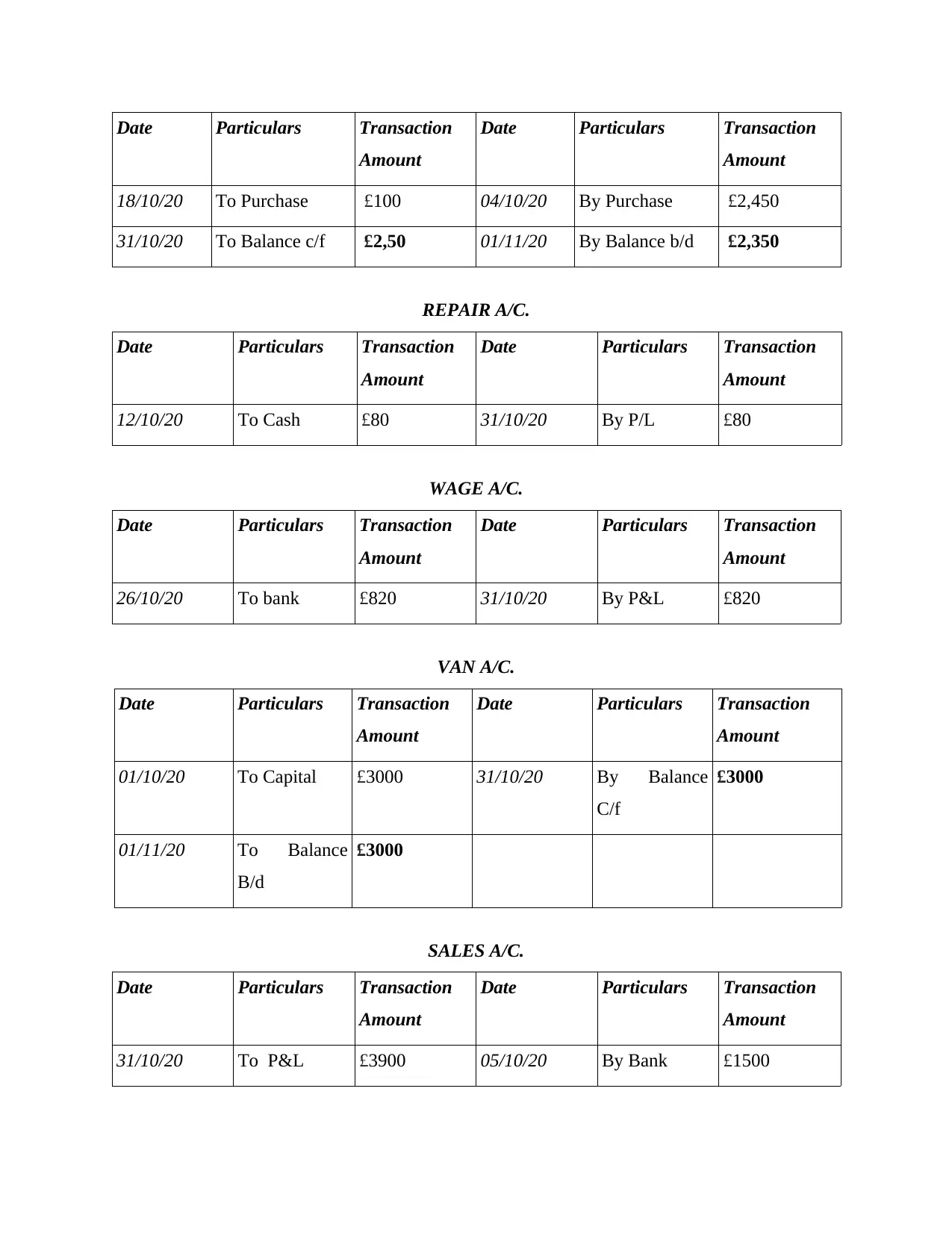

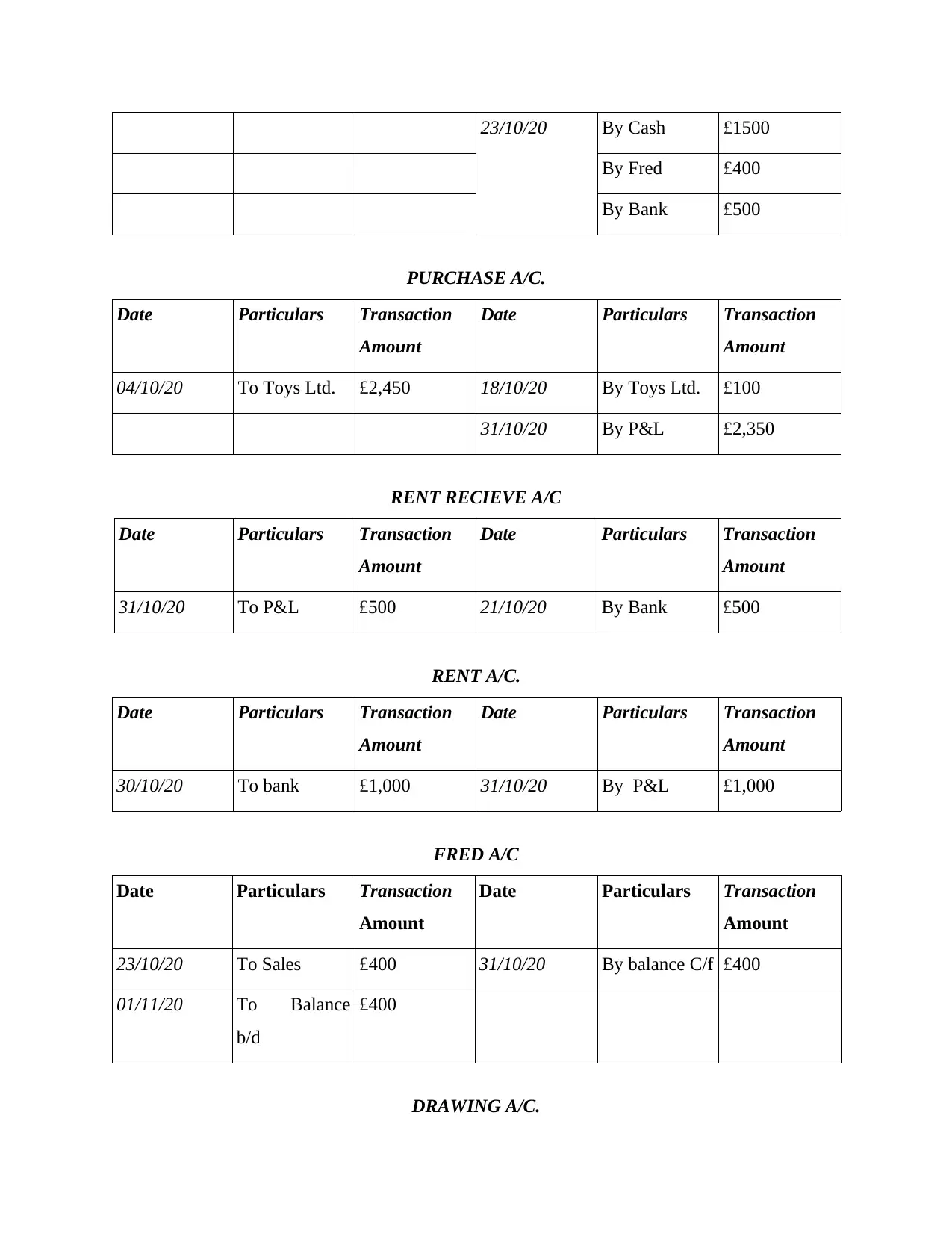

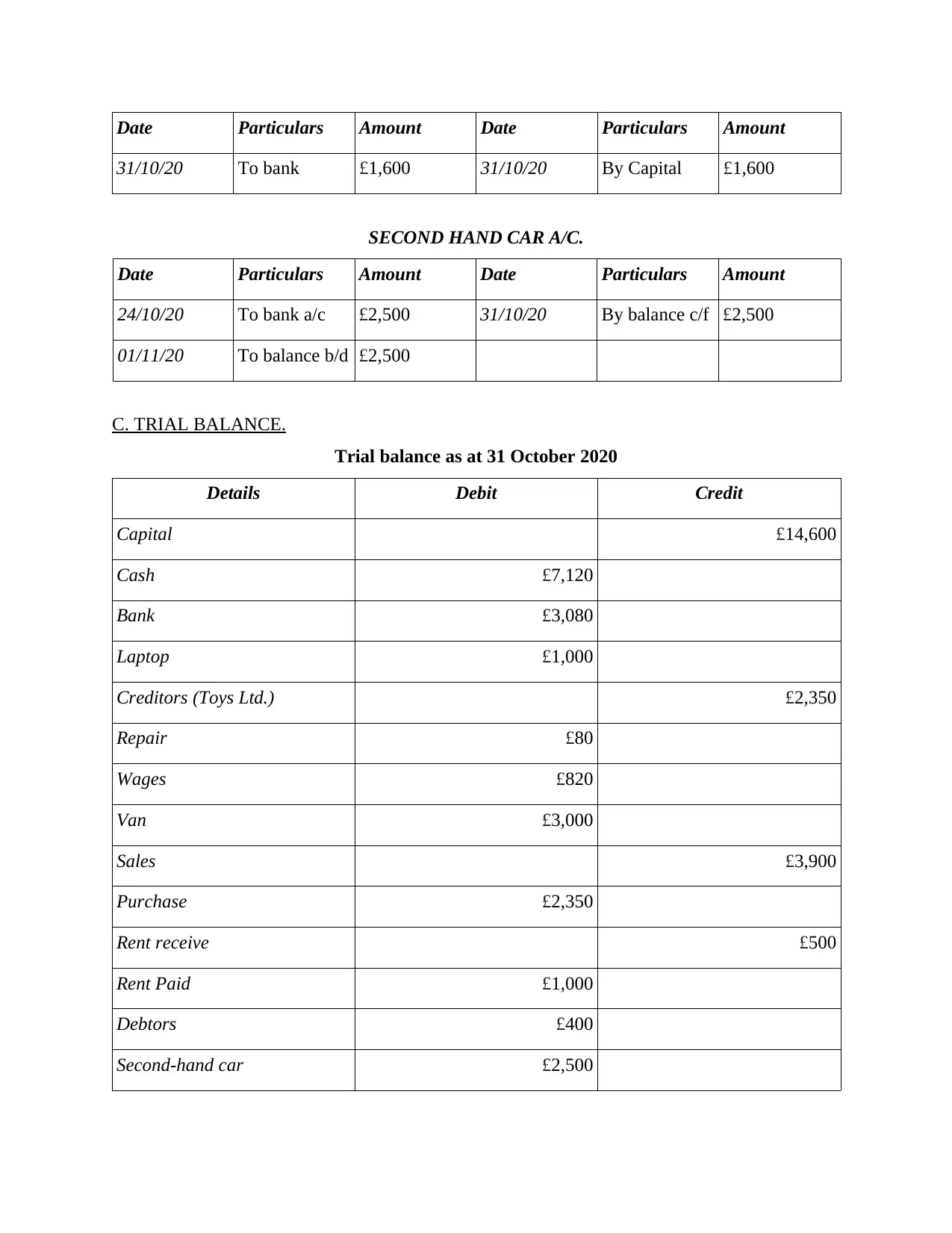

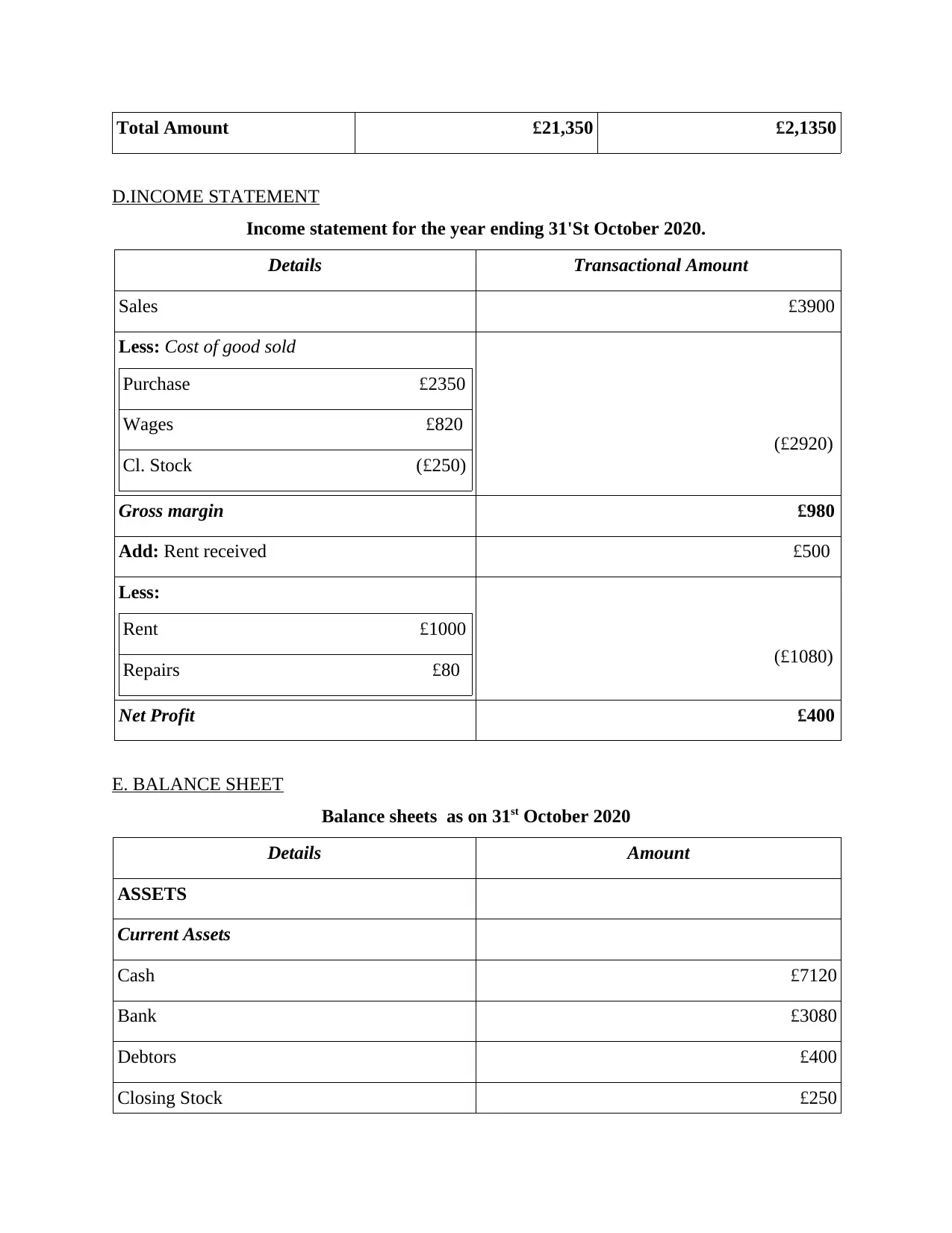

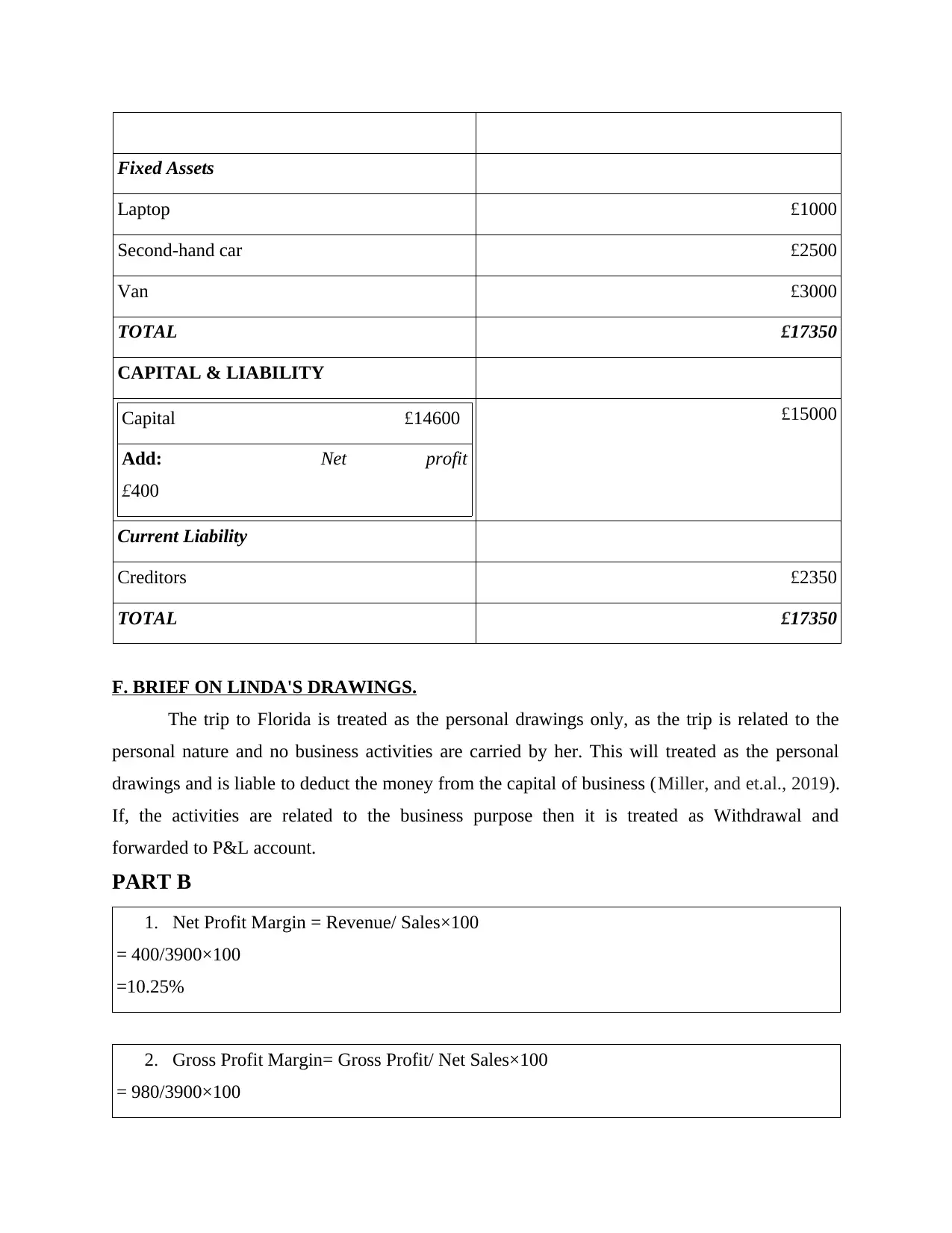

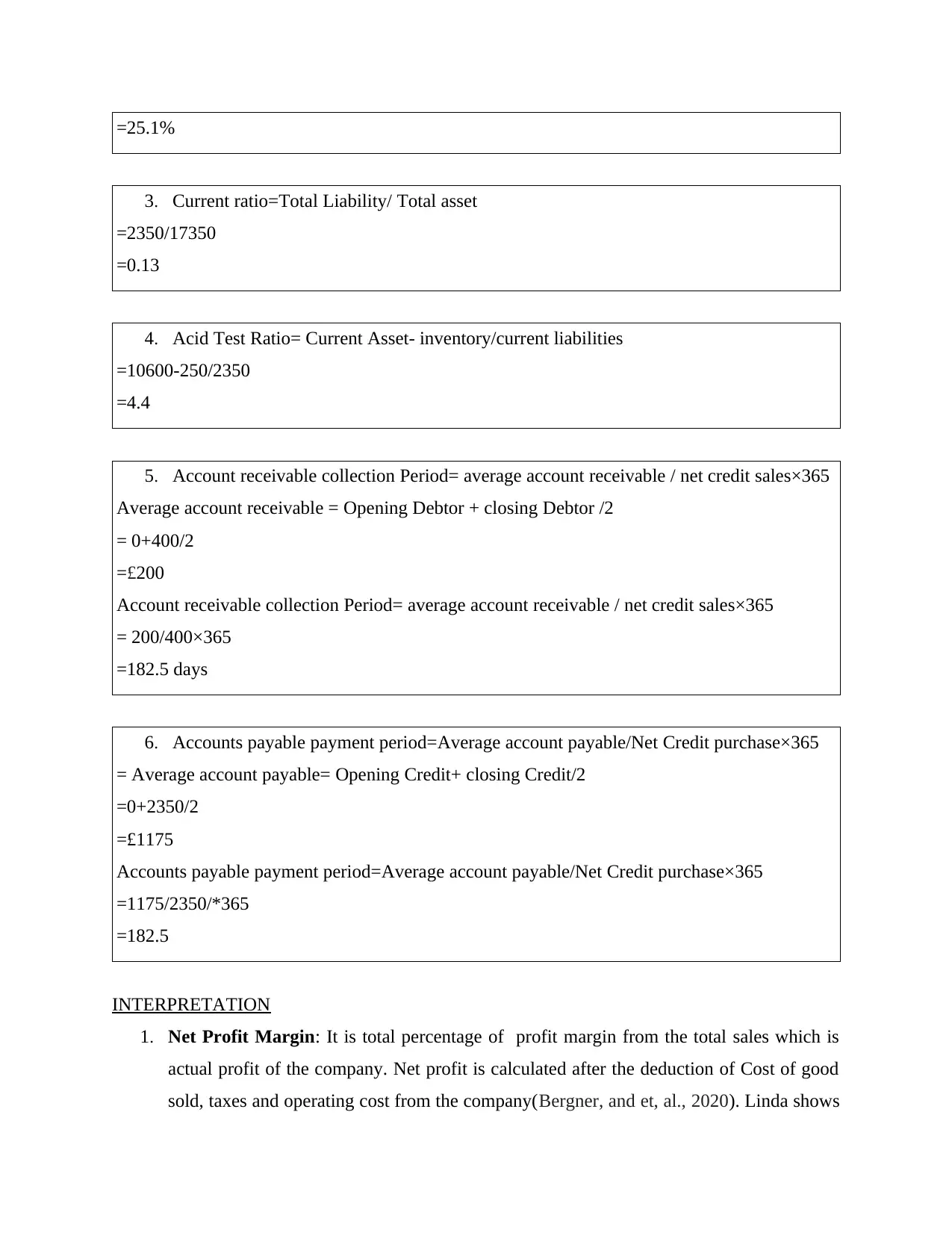

This report provides a comprehensive analysis of recording business transactions for a new toy business started by Linda at Oxford University. The report meticulously details the recording of transactions in journal entries, ledgers, trial balance, income statement, and balance sheet. It includes a thorough analysis of financial ratios, such as net profit margin, gross profit margin, current ratio, acid test ratio, accounts receivable collection period, and accounts payable payment period, comparing Linda's business performance with the average competitor market. The report highlights the company's financial position, interpretations of the ratios, and concludes with recommendations for improvement, particularly in areas like net profit margin, current ratio, and accounts payable payment period to ensure the business's long-term sustainability and competitiveness in the market. It also addresses the handling of owner's drawings, distinguishing between personal and business-related expenses.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.