Financial Performance and Valuation Analysis Report - BABS4 Module

VerifiedAdded on 2022/12/17

|16

|3639

|23

Report

AI Summary

This report, prepared for a Financial Management and Analysis module, provides a comprehensive analysis of a company's financial performance. It begins with a detailed profitability, liquidity, solvency, efficiency, and investment ratio analysis, comparing data over two years and interpreting the trends. The report then addresses the limitations of ratio analysis and offers recommendations for improvement. Furthermore, it delves into investment appraisal techniques, calculating payback periods, net present values (NPV), and internal rates of return (IRR) for different investment choices, ultimately recommending the best option. The report continues with a discussion of rights issues, calculating theoretical ex-rights prices, values of rights, and their impact on shareholder wealth. It also covers company valuation, using market capitalization, net asset value, and price-earnings ratios, alongside an analysis of dividend growth. Finally, the report examines systematic and unsystematic risk and their impact on businesses, and concludes with a recommendation to acquire a company based on price-earnings ratio. The assignment provides a detailed financial analysis and valuation, offering insights into various financial concepts.

FINANCIAL MANAGEMENT AND ANALYSIS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Content

INTRODUCTION ..........................................................................................................................4

TASK 1............................................................................................................................................5

2. Limitation of ratio analysis.....................................................................................................7

3. Recommendations...................................................................................................................7

TASK 2............................................................................................................................................7

a. Payback period .......................................................................................................................7

b. Assessment of NPV ................................................................................................................8

c. Computation of IRR................................................................................................................9

d. Recommending the best choice out of several alternatives available by applying investment

appraisal tools............................................................................................................................10

TASK 3..........................................................................................................................................10

a) Theoretical ex-rights price of Dusseldorf plc.......................................................................10

b) Values of rights attached to each existing share...................................................................10

c) Effect on wealth of Lukas.....................................................................................................11

TASK 4..........................................................................................................................................12

a) value of Amsterdam plc through market capitalization........................................................12

B) value of Amsterdam plc using the net asset value...............................................................12

c) Value through Price earnings ratio........................................................................................12

d) average historic dividend growth rate ..................................................................................13

e) Advise...................................................................................................................................13

TASK 5..........................................................................................................................................13

CONCLUSION..............................................................................................................................15

REFRENCES.................................................................................................................................16

INTRODUCTION ..........................................................................................................................4

TASK 1............................................................................................................................................5

2. Limitation of ratio analysis.....................................................................................................7

3. Recommendations...................................................................................................................7

TASK 2............................................................................................................................................7

a. Payback period .......................................................................................................................7

b. Assessment of NPV ................................................................................................................8

c. Computation of IRR................................................................................................................9

d. Recommending the best choice out of several alternatives available by applying investment

appraisal tools............................................................................................................................10

TASK 3..........................................................................................................................................10

a) Theoretical ex-rights price of Dusseldorf plc.......................................................................10

b) Values of rights attached to each existing share...................................................................10

c) Effect on wealth of Lukas.....................................................................................................11

TASK 4..........................................................................................................................................12

a) value of Amsterdam plc through market capitalization........................................................12

B) value of Amsterdam plc using the net asset value...............................................................12

c) Value through Price earnings ratio........................................................................................12

d) average historic dividend growth rate ..................................................................................13

e) Advise...................................................................................................................................13

TASK 5..........................................................................................................................................13

CONCLUSION..............................................................................................................................15

REFRENCES.................................................................................................................................16

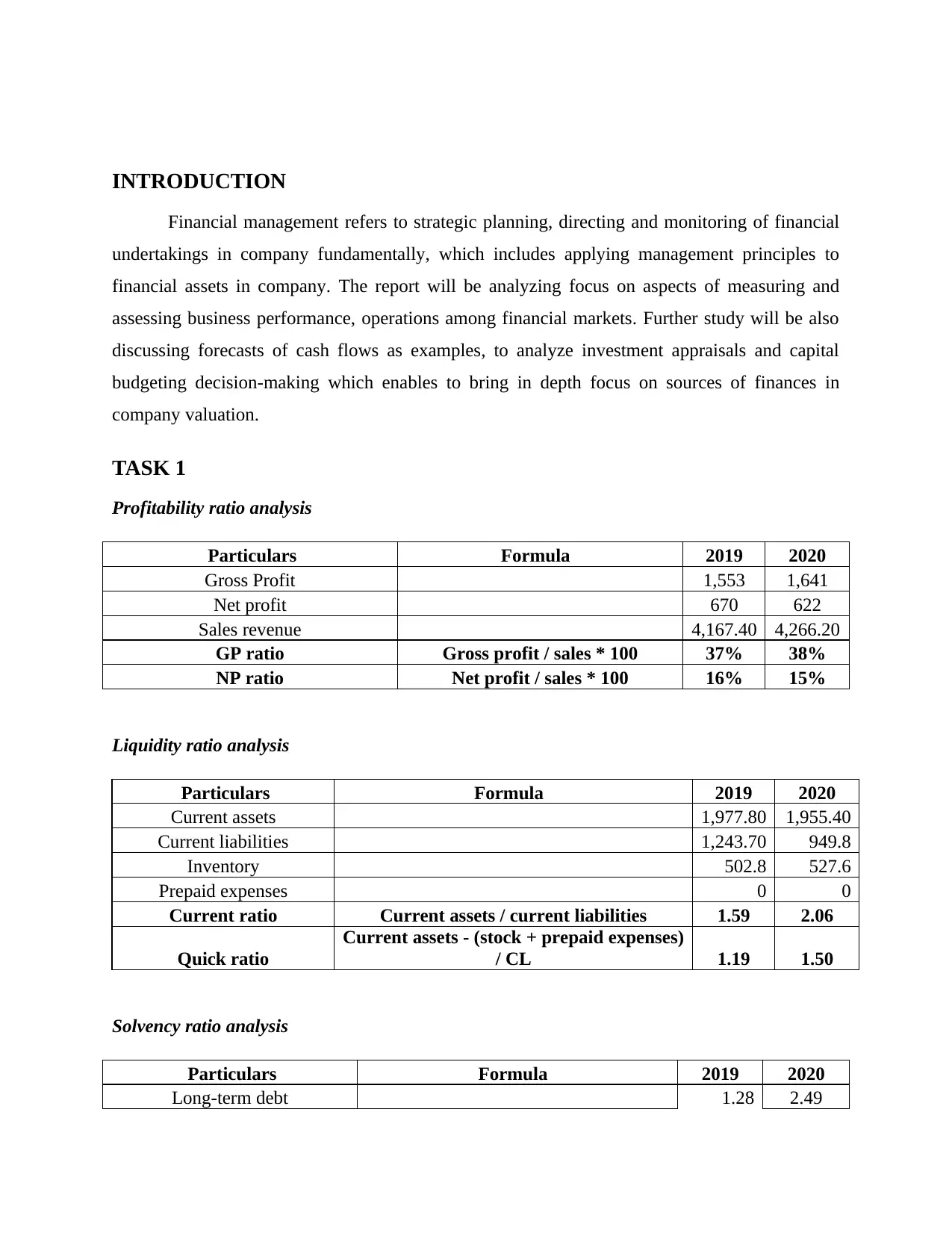

INTRODUCTION

Financial management refers to strategic planning, directing and monitoring of financial

undertakings in company fundamentally, which includes applying management principles to

financial assets in company. The report will be analyzing focus on aspects of measuring and

assessing business performance, operations among financial markets. Further study will be also

discussing forecasts of cash flows as examples, to analyze investment appraisals and capital

budgeting decision-making which enables to bring in depth focus on sources of finances in

company valuation.

TASK 1

Profitability ratio analysis

Particulars Formula 2019 2020

Gross Profit 1,553 1,641

Net profit 670 622

Sales revenue 4,167.40 4,266.20

GP ratio Gross profit / sales * 100 37% 38%

NP ratio Net profit / sales * 100 16% 15%

Liquidity ratio analysis

Particulars Formula 2019 2020

Current assets 1,977.80 1,955.40

Current liabilities 1,243.70 949.8

Inventory 502.8 527.6

Prepaid expenses 0 0

Current ratio Current assets / current liabilities 1.59 2.06

Quick ratio

Current assets - (stock + prepaid expenses)

/ CL 1.19 1.50

Solvency ratio analysis

Particulars Formula 2019 2020

Long-term debt 1.28 2.49

Financial management refers to strategic planning, directing and monitoring of financial

undertakings in company fundamentally, which includes applying management principles to

financial assets in company. The report will be analyzing focus on aspects of measuring and

assessing business performance, operations among financial markets. Further study will be also

discussing forecasts of cash flows as examples, to analyze investment appraisals and capital

budgeting decision-making which enables to bring in depth focus on sources of finances in

company valuation.

TASK 1

Profitability ratio analysis

Particulars Formula 2019 2020

Gross Profit 1,553 1,641

Net profit 670 622

Sales revenue 4,167.40 4,266.20

GP ratio Gross profit / sales * 100 37% 38%

NP ratio Net profit / sales * 100 16% 15%

Liquidity ratio analysis

Particulars Formula 2019 2020

Current assets 1,977.80 1,955.40

Current liabilities 1,243.70 949.8

Inventory 502.8 527.6

Prepaid expenses 0 0

Current ratio Current assets / current liabilities 1.59 2.06

Quick ratio

Current assets - (stock + prepaid expenses)

/ CL 1.19 1.50

Solvency ratio analysis

Particulars Formula 2019 2020

Long-term debt 1.28 2.49

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Shareholder's equity 0.55 0.44

Debt-equity ratio Long-term debt / shareholders’ equity 2.33 5.66

Efficiency ratios

Particulars Formula 2019 2020

Turnover or sales revenue 4,167.40 4,266.20

Average total assets 3,742.60 3,673.30

Average fixed assets 1,764.80 1,717.90

Total assets turnover ratio 1.11 1.161

Fixed assets turnover ratio 2.36 2.48

Investment ratios

Particulars Formula 2019 2020

Dividends per share Annual dividends / Number of shares 1.68 0

Price-earnings ratio Market value per share / earnings per share 15.61 27.63

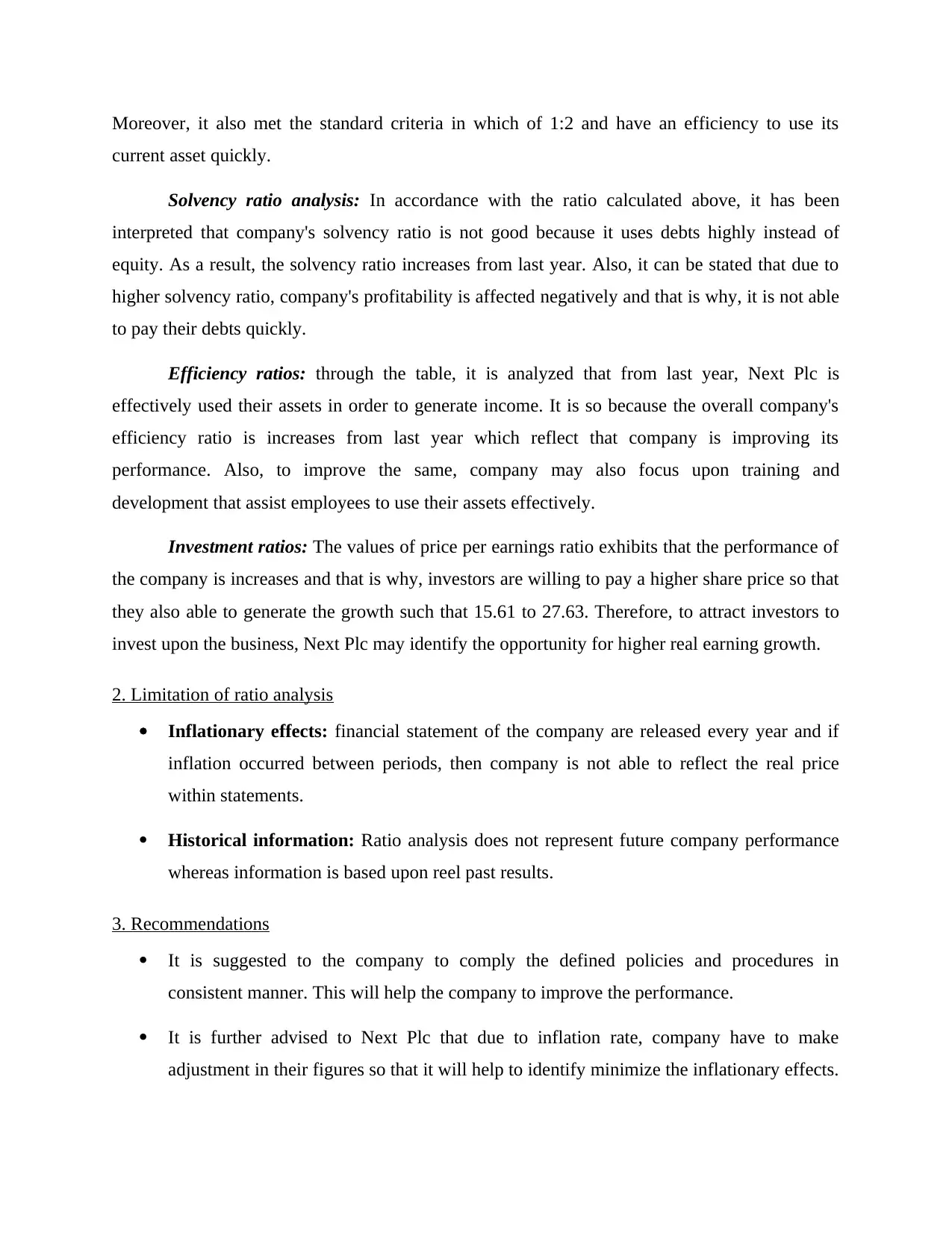

Interpretations

Profitability ratio analysis: Through the table it has been interpreted that GP ratio of the

company is good because it is increases from last year by 1% and it means that company's direct

expenses are controlled and that is why, it is able to increase its Gross profit ratio. Whereas, on

the other side, Net profit ratio is decreases which is not beneficial for the Next Plc because it

does not have any control over the indirect expenses. This in turn leads to affect the overall

image of a company in opposite manner. Therefore, there is a need to control the expenses in

order to improve the net profit of a firm.

Liquidity ratio analysis: From the able it is interpreted in the context of current ratio that

it measures the company's ability to pay amount within short period within a limited year. It is so

because it is suitable for the standard criteria i.e. 2:1. Thus, Next Plc is able to pay their liability

amount because it has efficiency to manage the asset over each liability. On the other side, quick

ratio of the firm is good and that is why, firm is able to meet its liability with its liquid assets.

Debt-equity ratio Long-term debt / shareholders’ equity 2.33 5.66

Efficiency ratios

Particulars Formula 2019 2020

Turnover or sales revenue 4,167.40 4,266.20

Average total assets 3,742.60 3,673.30

Average fixed assets 1,764.80 1,717.90

Total assets turnover ratio 1.11 1.161

Fixed assets turnover ratio 2.36 2.48

Investment ratios

Particulars Formula 2019 2020

Dividends per share Annual dividends / Number of shares 1.68 0

Price-earnings ratio Market value per share / earnings per share 15.61 27.63

Interpretations

Profitability ratio analysis: Through the table it has been interpreted that GP ratio of the

company is good because it is increases from last year by 1% and it means that company's direct

expenses are controlled and that is why, it is able to increase its Gross profit ratio. Whereas, on

the other side, Net profit ratio is decreases which is not beneficial for the Next Plc because it

does not have any control over the indirect expenses. This in turn leads to affect the overall

image of a company in opposite manner. Therefore, there is a need to control the expenses in

order to improve the net profit of a firm.

Liquidity ratio analysis: From the able it is interpreted in the context of current ratio that

it measures the company's ability to pay amount within short period within a limited year. It is so

because it is suitable for the standard criteria i.e. 2:1. Thus, Next Plc is able to pay their liability

amount because it has efficiency to manage the asset over each liability. On the other side, quick

ratio of the firm is good and that is why, firm is able to meet its liability with its liquid assets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Moreover, it also met the standard criteria in which of 1:2 and have an efficiency to use its

current asset quickly.

Solvency ratio analysis: In accordance with the ratio calculated above, it has been

interpreted that company's solvency ratio is not good because it uses debts highly instead of

equity. As a result, the solvency ratio increases from last year. Also, it can be stated that due to

higher solvency ratio, company's profitability is affected negatively and that is why, it is not able

to pay their debts quickly.

Efficiency ratios: through the table, it is analyzed that from last year, Next Plc is

effectively used their assets in order to generate income. It is so because the overall company's

efficiency ratio is increases from last year which reflect that company is improving its

performance. Also, to improve the same, company may also focus upon training and

development that assist employees to use their assets effectively.

Investment ratios: The values of price per earnings ratio exhibits that the performance of

the company is increases and that is why, investors are willing to pay a higher share price so that

they also able to generate the growth such that 15.61 to 27.63. Therefore, to attract investors to

invest upon the business, Next Plc may identify the opportunity for higher real earning growth.

2. Limitation of ratio analysis

Inflationary effects: financial statement of the company are released every year and if

inflation occurred between periods, then company is not able to reflect the real price

within statements.

Historical information: Ratio analysis does not represent future company performance

whereas information is based upon reel past results.

3. Recommendations

It is suggested to the company to comply the defined policies and procedures in

consistent manner. This will help the company to improve the performance.

It is further advised to Next Plc that due to inflation rate, company have to make

adjustment in their figures so that it will help to identify minimize the inflationary effects.

current asset quickly.

Solvency ratio analysis: In accordance with the ratio calculated above, it has been

interpreted that company's solvency ratio is not good because it uses debts highly instead of

equity. As a result, the solvency ratio increases from last year. Also, it can be stated that due to

higher solvency ratio, company's profitability is affected negatively and that is why, it is not able

to pay their debts quickly.

Efficiency ratios: through the table, it is analyzed that from last year, Next Plc is

effectively used their assets in order to generate income. It is so because the overall company's

efficiency ratio is increases from last year which reflect that company is improving its

performance. Also, to improve the same, company may also focus upon training and

development that assist employees to use their assets effectively.

Investment ratios: The values of price per earnings ratio exhibits that the performance of

the company is increases and that is why, investors are willing to pay a higher share price so that

they also able to generate the growth such that 15.61 to 27.63. Therefore, to attract investors to

invest upon the business, Next Plc may identify the opportunity for higher real earning growth.

2. Limitation of ratio analysis

Inflationary effects: financial statement of the company are released every year and if

inflation occurred between periods, then company is not able to reflect the real price

within statements.

Historical information: Ratio analysis does not represent future company performance

whereas information is based upon reel past results.

3. Recommendations

It is suggested to the company to comply the defined policies and procedures in

consistent manner. This will help the company to improve the performance.

It is further advised to Next Plc that due to inflation rate, company have to make

adjustment in their figures so that it will help to identify minimize the inflationary effects.

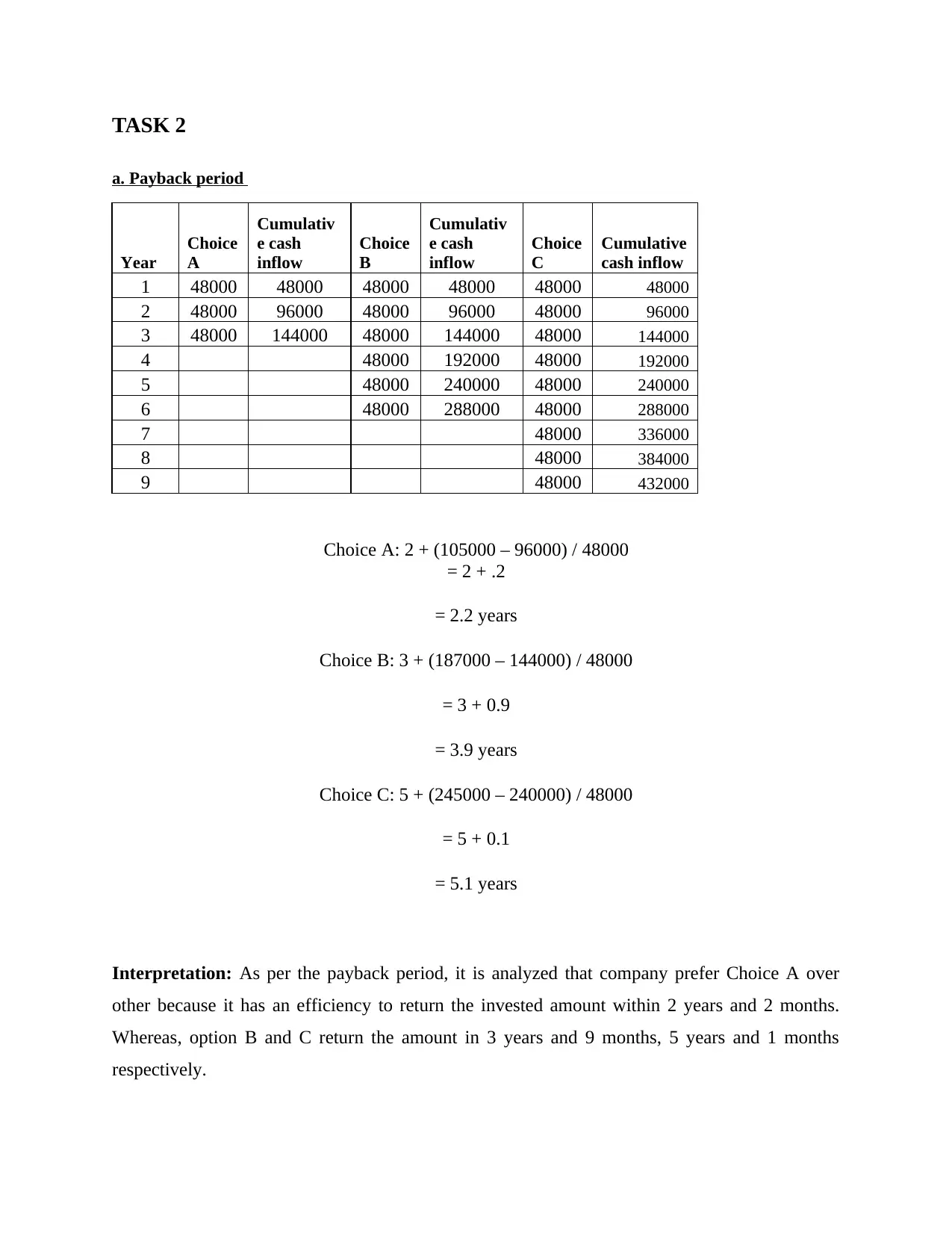

TASK 2

a. Payback period

Year

Choice

A

Cumulativ

e cash

inflow

Choice

B

Cumulativ

e cash

inflow

Choice

C

Cumulative

cash inflow

1 48000 48000 48000 48000 48000 48000

2 48000 96000 48000 96000 48000 96000

3 48000 144000 48000 144000 48000 144000

4 48000 192000 48000 192000

5 48000 240000 48000 240000

6 48000 288000 48000 288000

7 48000 336000

8 48000 384000

9 48000 432000

Choice A: 2 + (105000 – 96000) / 48000

= 2 + .2

= 2.2 years

Choice B: 3 + (187000 – 144000) / 48000

= 3 + 0.9

= 3.9 years

Choice C: 5 + (245000 – 240000) / 48000

= 5 + 0.1

= 5.1 years

Interpretation: As per the payback period, it is analyzed that company prefer Choice A over

other because it has an efficiency to return the invested amount within 2 years and 2 months.

Whereas, option B and C return the amount in 3 years and 9 months, 5 years and 1 months

respectively.

a. Payback period

Year

Choice

A

Cumulativ

e cash

inflow

Choice

B

Cumulativ

e cash

inflow

Choice

C

Cumulative

cash inflow

1 48000 48000 48000 48000 48000 48000

2 48000 96000 48000 96000 48000 96000

3 48000 144000 48000 144000 48000 144000

4 48000 192000 48000 192000

5 48000 240000 48000 240000

6 48000 288000 48000 288000

7 48000 336000

8 48000 384000

9 48000 432000

Choice A: 2 + (105000 – 96000) / 48000

= 2 + .2

= 2.2 years

Choice B: 3 + (187000 – 144000) / 48000

= 3 + 0.9

= 3.9 years

Choice C: 5 + (245000 – 240000) / 48000

= 5 + 0.1

= 5.1 years

Interpretation: As per the payback period, it is analyzed that company prefer Choice A over

other because it has an efficiency to return the invested amount within 2 years and 2 months.

Whereas, option B and C return the amount in 3 years and 9 months, 5 years and 1 months

respectively.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

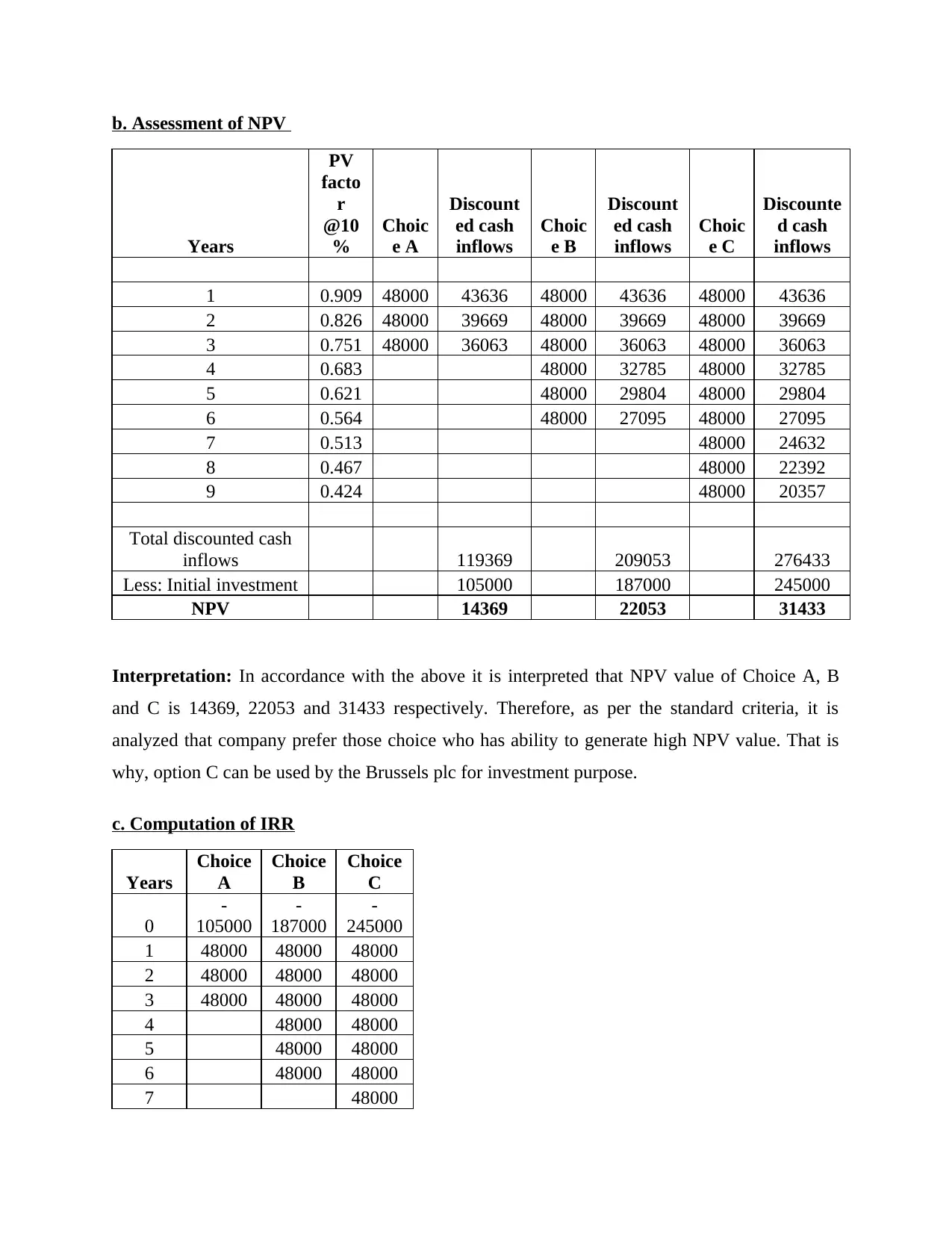

b. Assessment of NPV

Years

PV

facto

r

@10

%

Choic

e A

Discount

ed cash

inflows

Choic

e B

Discount

ed cash

inflows

Choic

e C

Discounte

d cash

inflows

1 0.909 48000 43636 48000 43636 48000 43636

2 0.826 48000 39669 48000 39669 48000 39669

3 0.751 48000 36063 48000 36063 48000 36063

4 0.683 48000 32785 48000 32785

5 0.621 48000 29804 48000 29804

6 0.564 48000 27095 48000 27095

7 0.513 48000 24632

8 0.467 48000 22392

9 0.424 48000 20357

Total discounted cash

inflows 119369 209053 276433

Less: Initial investment 105000 187000 245000

NPV 14369 22053 31433

Interpretation: In accordance with the above it is interpreted that NPV value of Choice A, B

and C is 14369, 22053 and 31433 respectively. Therefore, as per the standard criteria, it is

analyzed that company prefer those choice who has ability to generate high NPV value. That is

why, option C can be used by the Brussels plc for investment purpose.

c. Computation of IRR

Years

Choice

A

Choice

B

Choice

C

0

-

105000

-

187000

-

245000

1 48000 48000 48000

2 48000 48000 48000

3 48000 48000 48000

4 48000 48000

5 48000 48000

6 48000 48000

7 48000

Years

PV

facto

r

@10

%

Choic

e A

Discount

ed cash

inflows

Choic

e B

Discount

ed cash

inflows

Choic

e C

Discounte

d cash

inflows

1 0.909 48000 43636 48000 43636 48000 43636

2 0.826 48000 39669 48000 39669 48000 39669

3 0.751 48000 36063 48000 36063 48000 36063

4 0.683 48000 32785 48000 32785

5 0.621 48000 29804 48000 29804

6 0.564 48000 27095 48000 27095

7 0.513 48000 24632

8 0.467 48000 22392

9 0.424 48000 20357

Total discounted cash

inflows 119369 209053 276433

Less: Initial investment 105000 187000 245000

NPV 14369 22053 31433

Interpretation: In accordance with the above it is interpreted that NPV value of Choice A, B

and C is 14369, 22053 and 31433 respectively. Therefore, as per the standard criteria, it is

analyzed that company prefer those choice who has ability to generate high NPV value. That is

why, option C can be used by the Brussels plc for investment purpose.

c. Computation of IRR

Years

Choice

A

Choice

B

Choice

C

0

-

105000

-

187000

-

245000

1 48000 48000 48000

2 48000 48000 48000

3 48000 48000 48000

4 48000 48000

5 48000 48000

6 48000 48000

7 48000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

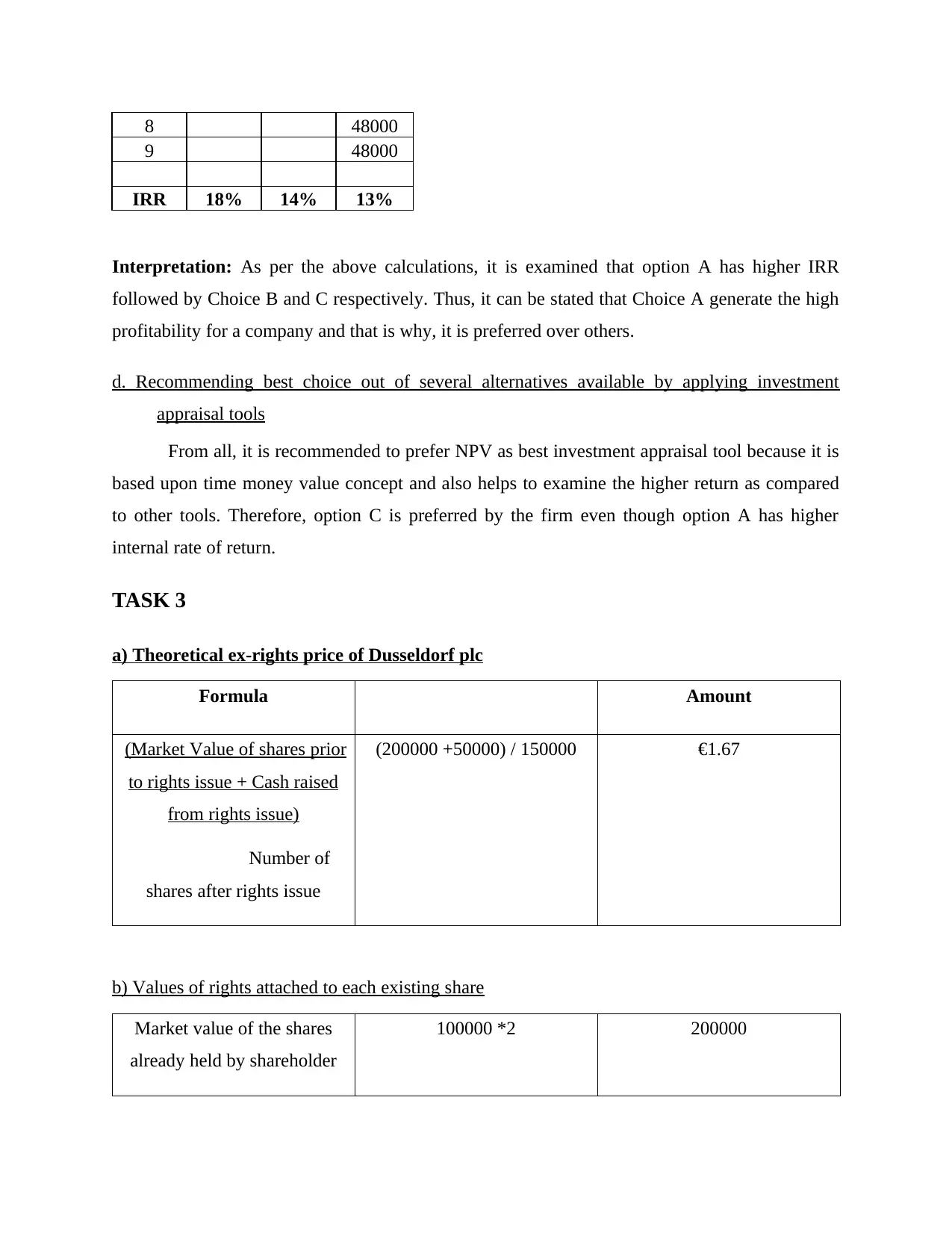

8 48000

9 48000

IRR 18% 14% 13%

Interpretation: As per the above calculations, it is examined that option A has higher IRR

followed by Choice B and C respectively. Thus, it can be stated that Choice A generate the high

profitability for a company and that is why, it is preferred over others.

d. Recommending best choice out of several alternatives available by applying investment

appraisal tools

From all, it is recommended to prefer NPV as best investment appraisal tool because it is

based upon time money value concept and also helps to examine the higher return as compared

to other tools. Therefore, option C is preferred by the firm even though option A has higher

internal rate of return.

TASK 3

a) Theoretical ex-rights price of Dusseldorf plc

Formula Amount

(Market Value of shares prior

to rights issue + Cash raised

from rights issue)

Number of

shares after rights issue

(200000 +50000) / 150000 €1.67

b) Values of rights attached to each existing share

Market value of the shares

already held by shareholder

100000 *2 200000

9 48000

IRR 18% 14% 13%

Interpretation: As per the above calculations, it is examined that option A has higher IRR

followed by Choice B and C respectively. Thus, it can be stated that Choice A generate the high

profitability for a company and that is why, it is preferred over others.

d. Recommending best choice out of several alternatives available by applying investment

appraisal tools

From all, it is recommended to prefer NPV as best investment appraisal tool because it is

based upon time money value concept and also helps to examine the higher return as compared

to other tools. Therefore, option C is preferred by the firm even though option A has higher

internal rate of return.

TASK 3

a) Theoretical ex-rights price of Dusseldorf plc

Formula Amount

(Market Value of shares prior

to rights issue + Cash raised

from rights issue)

Number of

shares after rights issue

(200000 +50000) / 150000 €1.67

b) Values of rights attached to each existing share

Market value of the shares

already held by shareholder

100000 *2 200000

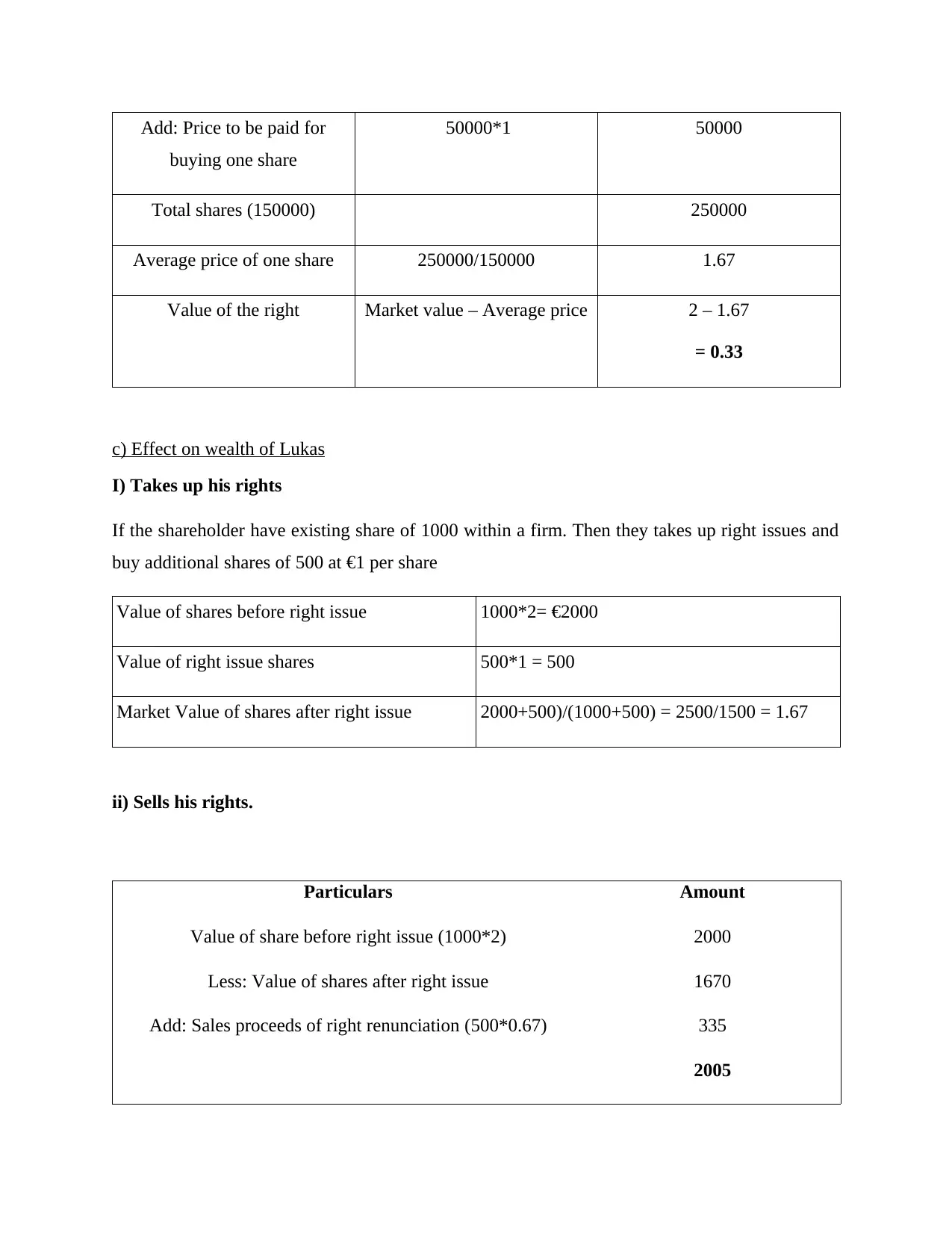

Add: Price to be paid for

buying one share

50000*1 50000

Total shares (150000) 250000

Average price of one share 250000/150000 1.67

Value of the right Market value – Average price 2 – 1.67

= 0.33

c) Effect on wealth of Lukas

I) Takes up his rights

If the shareholder have existing share of 1000 within a firm. Then they takes up right issues and

buy additional shares of 500 at €1 per share

Value of shares before right issue 1000*2= €2000

Value of right issue shares 500*1 = 500

Market Value of shares after right issue 2000+500)/(1000+500) = 2500/1500 = 1.67

ii) Sells his rights.

Particulars Amount

Value of share before right issue (1000*2) 2000

Less: Value of shares after right issue 1670

Add: Sales proceeds of right renunciation (500*0.67) 335

2005

buying one share

50000*1 50000

Total shares (150000) 250000

Average price of one share 250000/150000 1.67

Value of the right Market value – Average price 2 – 1.67

= 0.33

c) Effect on wealth of Lukas

I) Takes up his rights

If the shareholder have existing share of 1000 within a firm. Then they takes up right issues and

buy additional shares of 500 at €1 per share

Value of shares before right issue 1000*2= €2000

Value of right issue shares 500*1 = 500

Market Value of shares after right issue 2000+500)/(1000+500) = 2500/1500 = 1.67

ii) Sells his rights.

Particulars Amount

Value of share before right issue (1000*2) 2000

Less: Value of shares after right issue 1670

Add: Sales proceeds of right renunciation (500*0.67) 335

2005

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

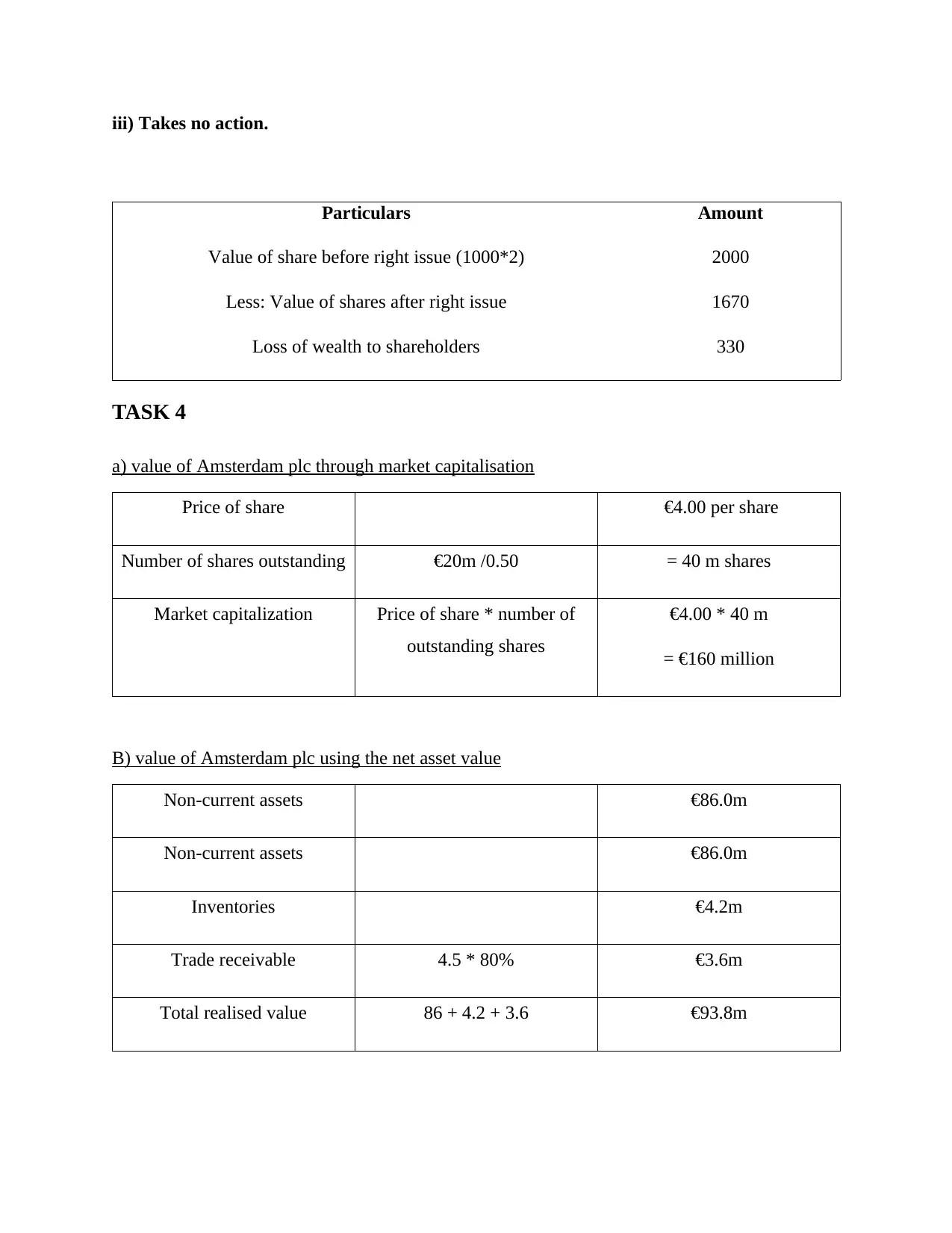

iii) Takes no action.

Particulars Amount

Value of share before right issue (1000*2) 2000

Less: Value of shares after right issue 1670

Loss of wealth to shareholders 330

TASK 4

a) value of Amsterdam plc through market capitalisation

Price of share €4.00 per share

Number of shares outstanding €20m /0.50 = 40 m shares

Market capitalization Price of share * number of

outstanding shares

€4.00 * 40 m

= €160 million

B) value of Amsterdam plc using the net asset value

Non-current assets €86.0m

Non-current assets €86.0m

Inventories €4.2m

Trade receivable 4.5 * 80% €3.6m

Total realised value 86 + 4.2 + 3.6 €93.8m

Particulars Amount

Value of share before right issue (1000*2) 2000

Less: Value of shares after right issue 1670

Loss of wealth to shareholders 330

TASK 4

a) value of Amsterdam plc through market capitalisation

Price of share €4.00 per share

Number of shares outstanding €20m /0.50 = 40 m shares

Market capitalization Price of share * number of

outstanding shares

€4.00 * 40 m

= €160 million

B) value of Amsterdam plc using the net asset value

Non-current assets €86.0m

Non-current assets €86.0m

Inventories €4.2m

Trade receivable 4.5 * 80% €3.6m

Total realised value 86 + 4.2 + 3.6 €93.8m

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

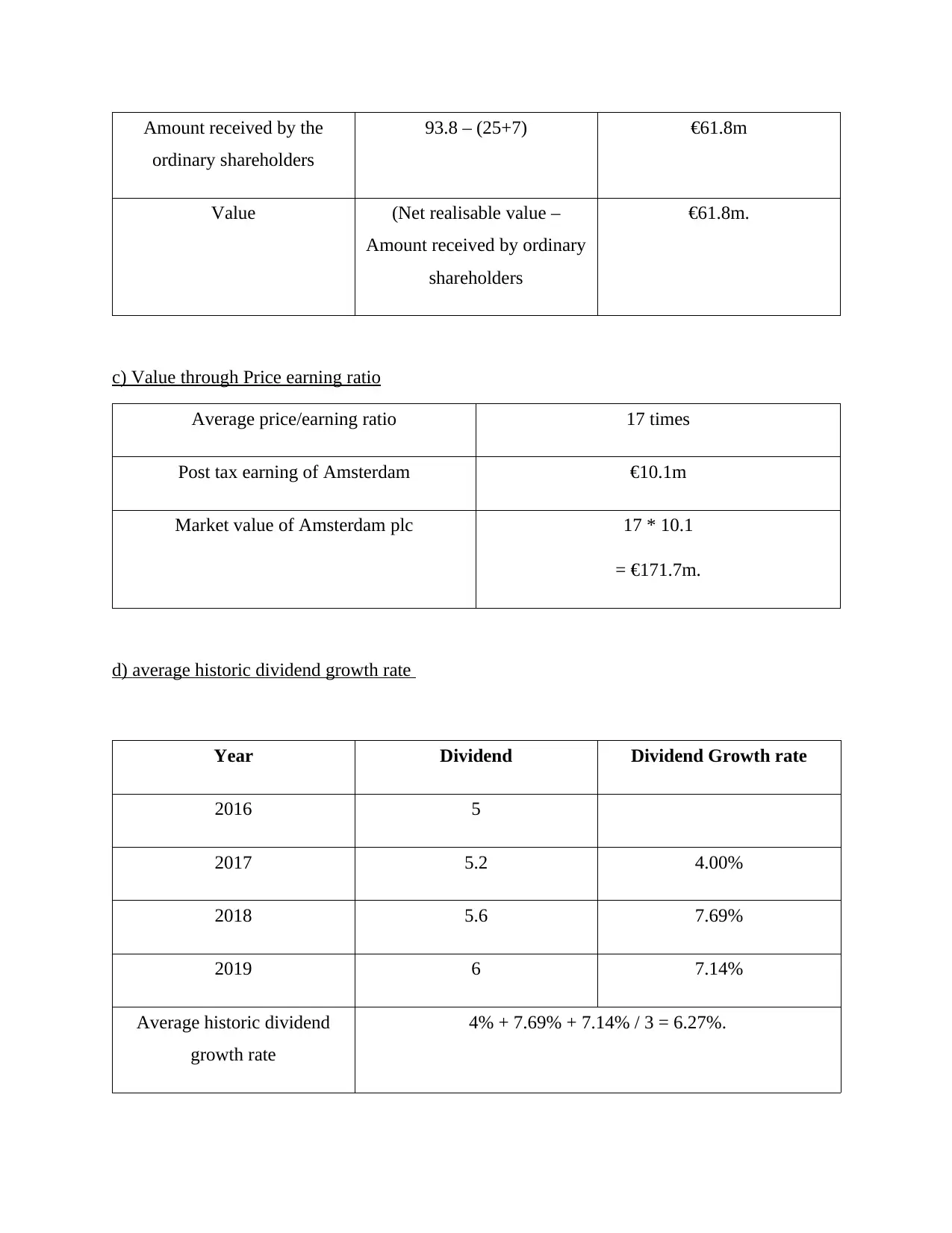

Amount received by the

ordinary shareholders

93.8 – (25+7) €61.8m

Value (Net realisable value –

Amount received by ordinary

shareholders

€61.8m.

c) Value through Price earning ratio

Average price/earning ratio 17 times

Post tax earning of Amsterdam €10.1m

Market value of Amsterdam plc 17 * 10.1

= €171.7m.

d) average historic dividend growth rate

Year Dividend Dividend Growth rate

2016 5

2017 5.2 4.00%

2018 5.6 7.69%

2019 6 7.14%

Average historic dividend

growth rate

4% + 7.69% + 7.14% / 3 = 6.27%.

ordinary shareholders

93.8 – (25+7) €61.8m

Value (Net realisable value –

Amount received by ordinary

shareholders

€61.8m.

c) Value through Price earning ratio

Average price/earning ratio 17 times

Post tax earning of Amsterdam €10.1m

Market value of Amsterdam plc 17 * 10.1

= €171.7m.

d) average historic dividend growth rate

Year Dividend Dividend Growth rate

2016 5

2017 5.2 4.00%

2018 5.6 7.69%

2019 6 7.14%

Average historic dividend

growth rate

4% + 7.69% + 7.14% / 3 = 6.27%.

e) Advise

Through the above, it has been analyzed investors are willing to acquire the company,

and they have to pay €171.7 million as defined in price earning ratio. It is preferred over others

because it popular for valuing business. On contrasting note, value on the basis of net asset value

is low and being a brand image, company is not ready to attract investor at low rates. That is

why, it is advised investor to acquire Amsterdam plc by considering price earnings ratio.

TASK 5

(A) Systematic risk can be understood as market risks that are general perils of investments that

cannot be diversified away where interest rates, recessions are examples of systematic risks.

Unsystematic risk on other hand relates to individual stocks associated with particular industry

referred with unsystematic risks, where impact is often also varied. Systematic risk refers to

profitability of loss linked with whole market segments such as changes in government policies

for specific industry, on other hand unsystematic risks has impact on particular industry

businesses. Beta is statistical measure of volatility of stock versus overall market where it

enables to monitor sensitivity of stock market fundamentally. Systematic risk plays strong role

within business as they are non-divertible, cannot be controlled, minimized or eliminated by

company as whole which has to be focused on for higher scale results among business functional

scale growth. The unsystematic risk on other hand can be easily controlled, minimized and

eliminated towards company on whole organization which can be also synchronized as per wider

targets in functional scenarios. The systematic risk is widely crucial to be monitored among

business avenues, where commercial strength can be identified towards present and future work

growth targets actively. Unsystematic risk on other hand, can be monitored by taking steps to

develop strategic control on risk factors and to identify new varied range of effective targets

imperatively. The difference factors have in depth analyzed varied functional scope segments

accurately, towards operational growth paradigm which enables new range of diversity

paradigms towards new business parameters. This can be analyzed as one of the widely crucial

aspect, which synchronizes diversity within strategic planning for competent diversity aspects

and to leverage larger technical growth actively.

(B) Money markets are used for short term lending aspects usually assets are being held for one

year or less, whereas on other hand capital markets are used for long term securities which has

Through the above, it has been analyzed investors are willing to acquire the company,

and they have to pay €171.7 million as defined in price earning ratio. It is preferred over others

because it popular for valuing business. On contrasting note, value on the basis of net asset value

is low and being a brand image, company is not ready to attract investor at low rates. That is

why, it is advised investor to acquire Amsterdam plc by considering price earnings ratio.

TASK 5

(A) Systematic risk can be understood as market risks that are general perils of investments that

cannot be diversified away where interest rates, recessions are examples of systematic risks.

Unsystematic risk on other hand relates to individual stocks associated with particular industry

referred with unsystematic risks, where impact is often also varied. Systematic risk refers to

profitability of loss linked with whole market segments such as changes in government policies

for specific industry, on other hand unsystematic risks has impact on particular industry

businesses. Beta is statistical measure of volatility of stock versus overall market where it

enables to monitor sensitivity of stock market fundamentally. Systematic risk plays strong role

within business as they are non-divertible, cannot be controlled, minimized or eliminated by

company as whole which has to be focused on for higher scale results among business functional

scale growth. The unsystematic risk on other hand can be easily controlled, minimized and

eliminated towards company on whole organization which can be also synchronized as per wider

targets in functional scenarios. The systematic risk is widely crucial to be monitored among

business avenues, where commercial strength can be identified towards present and future work

growth targets actively. Unsystematic risk on other hand, can be monitored by taking steps to

develop strategic control on risk factors and to identify new varied range of effective targets

imperatively. The difference factors have in depth analyzed varied functional scope segments

accurately, towards operational growth paradigm which enables new range of diversity

paradigms towards new business parameters. This can be analyzed as one of the widely crucial

aspect, which synchronizes diversity within strategic planning for competent diversity aspects

and to leverage larger technical growth actively.

(B) Money markets are used for short term lending aspects usually assets are being held for one

year or less, whereas on other hand capital markets are used for long term securities which has

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.