Financial Analysis and Performance Report for Bellovida Ltd

VerifiedAdded on 2020/06/06

|16

|4462

|374

Report

AI Summary

This report provides a comprehensive financial analysis of Bellovida Ltd, evaluating its performance using ratio analysis, including profitability, liquidity, efficiency, and gearing ratios. The analysis extends to non-financial aspects impacting business performance, such as customer retention and employee turnover. Furthermore, the report delves into break-even point analysis, calculating the break-even point in units and value, along with margin of safety. Investment appraisal techniques, including payback period, ARR, and NPV are applied to evaluate investment decisions. The report also examines working capital management, pricing strategies, and budgeting methods, providing a holistic view of the company's financial health and strategic planning.

MANAGING FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION 1...................................................................................................................................1

(i) Calculation of ratios...........................................................................................................1

(ii) Analysis of ratios..............................................................................................................2

iii) Explanation of four non-financial aspects which are used for improving business

performance............................................................................................................................3

QUESTION 2...................................................................................................................................3

A) Significance of BEP analysis............................................................................................3

B) BEP point in units and value.............................................................................................4

C) Margin of safety in units and value...................................................................................5

D) Profit and loss at sales of 8000 units.................................................................................5

E) P&L when selling price declines to $42............................................................................5

QUESTION 3...................................................................................................................................5

I) Comparing payback period (PP) and NPV.........................................................................5

ii) Evaluating and suggesting firm for investment decisions.................................................6

QUESTION 4...................................................................................................................................8

i) Listing out key functions and activities of a bank..............................................................8

ii) Explaining three terms.......................................................................................................8

iii) Significance of WC management for manufacturing company........................................8

QUESTION 5...................................................................................................................................9

i) Various pricing methods and suggesting the best strategy.................................................9

ii) Calculating unit selling price and advising the management...........................................10

QUESTION 6.................................................................................................................................10

i) Comparing Fixed and Flexible Budgets............................................................................10

ii) Importance of budgetary planning system.......................................................................11

iii) Calculating profit and loss..............................................................................................11

QUESTION 7.................................................................................................................................12

i) Discussing given statement of budgeting..........................................................................12

ii) Preparing different budgets..............................................................................................12

REFERENCES..............................................................................................................................14

QUESTION 1...................................................................................................................................1

(i) Calculation of ratios...........................................................................................................1

(ii) Analysis of ratios..............................................................................................................2

iii) Explanation of four non-financial aspects which are used for improving business

performance............................................................................................................................3

QUESTION 2...................................................................................................................................3

A) Significance of BEP analysis............................................................................................3

B) BEP point in units and value.............................................................................................4

C) Margin of safety in units and value...................................................................................5

D) Profit and loss at sales of 8000 units.................................................................................5

E) P&L when selling price declines to $42............................................................................5

QUESTION 3...................................................................................................................................5

I) Comparing payback period (PP) and NPV.........................................................................5

ii) Evaluating and suggesting firm for investment decisions.................................................6

QUESTION 4...................................................................................................................................8

i) Listing out key functions and activities of a bank..............................................................8

ii) Explaining three terms.......................................................................................................8

iii) Significance of WC management for manufacturing company........................................8

QUESTION 5...................................................................................................................................9

i) Various pricing methods and suggesting the best strategy.................................................9

ii) Calculating unit selling price and advising the management...........................................10

QUESTION 6.................................................................................................................................10

i) Comparing Fixed and Flexible Budgets............................................................................10

ii) Importance of budgetary planning system.......................................................................11

iii) Calculating profit and loss..............................................................................................11

QUESTION 7.................................................................................................................................12

i) Discussing given statement of budgeting..........................................................................12

ii) Preparing different budgets..............................................................................................12

REFERENCES..............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

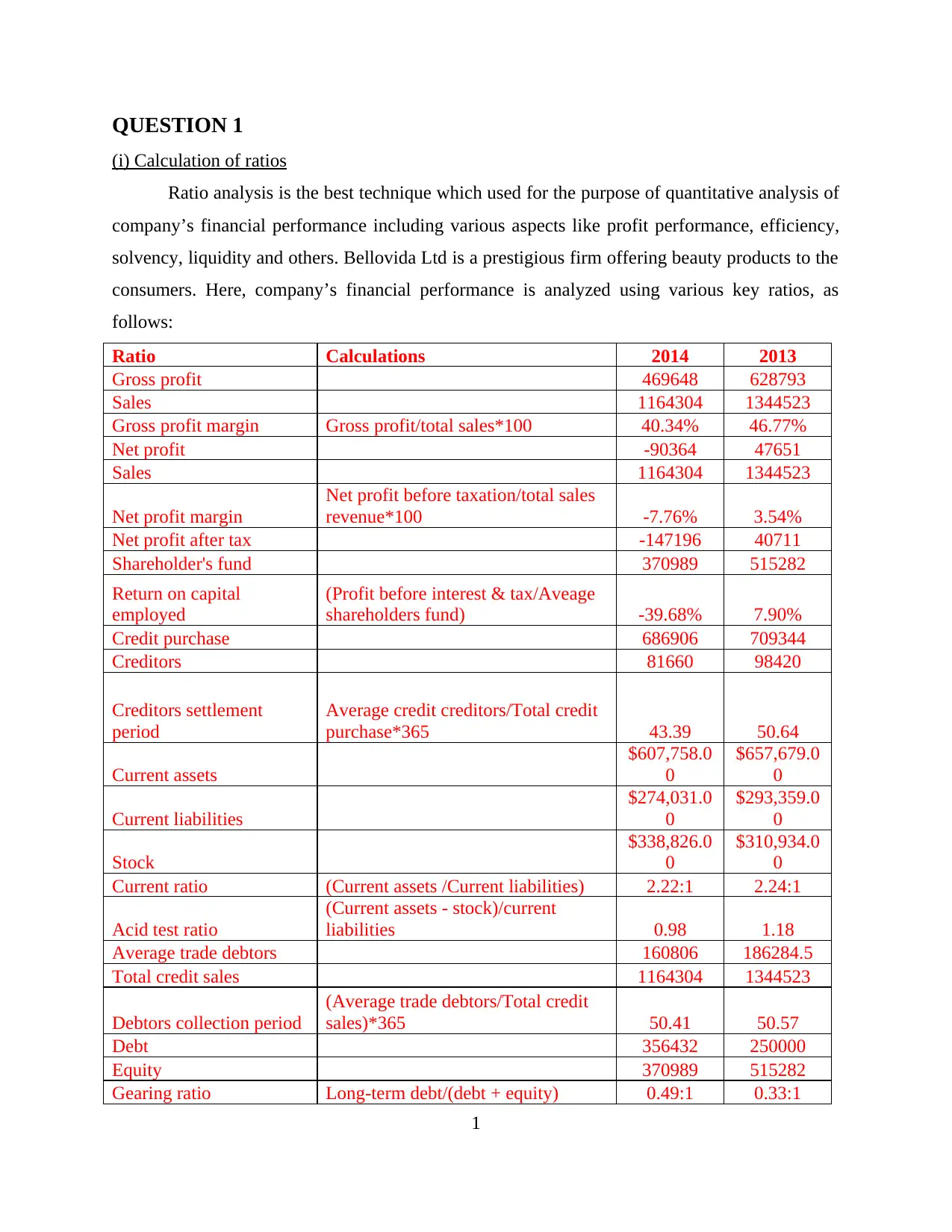

QUESTION 1

(i) Calculation of ratios

Ratio analysis is the best technique which used for the purpose of quantitative analysis of

company’s financial performance including various aspects like profit performance, efficiency,

solvency, liquidity and others. Bellovida Ltd is a prestigious firm offering beauty products to the

consumers. Here, company’s financial performance is analyzed using various key ratios, as

follows:

Ratio Calculations 2014 2013

Gross profit 469648 628793

Sales 1164304 1344523

Gross profit margin Gross profit/total sales*100 40.34% 46.77%

Net profit -90364 47651

Sales 1164304 1344523

Net profit margin

Net profit before taxation/total sales

revenue*100 -7.76% 3.54%

Net profit after tax -147196 40711

Shareholder's fund 370989 515282

Return on capital

employed

(Profit before interest & tax/Aveage

shareholders fund) -39.68% 7.90%

Credit purchase 686906 709344

Creditors 81660 98420

Creditors settlement

period

Average credit creditors/Total credit

purchase*365 43.39 50.64

Current assets

$607,758.0

0

$657,679.0

0

Current liabilities

$274,031.0

0

$293,359.0

0

Stock

$338,826.0

0

$310,934.0

0

Current ratio (Current assets /Current liabilities) 2.22:1 2.24:1

Acid test ratio

(Current assets - stock)/current

liabilities 0.98 1.18

Average trade debtors 160806 186284.5

Total credit sales 1164304 1344523

Debtors collection period

(Average trade debtors/Total credit

sales)*365 50.41 50.57

Debt 356432 250000

Equity 370989 515282

Gearing ratio Long-term debt/(debt + equity) 0.49:1 0.33:1

1

(i) Calculation of ratios

Ratio analysis is the best technique which used for the purpose of quantitative analysis of

company’s financial performance including various aspects like profit performance, efficiency,

solvency, liquidity and others. Bellovida Ltd is a prestigious firm offering beauty products to the

consumers. Here, company’s financial performance is analyzed using various key ratios, as

follows:

Ratio Calculations 2014 2013

Gross profit 469648 628793

Sales 1164304 1344523

Gross profit margin Gross profit/total sales*100 40.34% 46.77%

Net profit -90364 47651

Sales 1164304 1344523

Net profit margin

Net profit before taxation/total sales

revenue*100 -7.76% 3.54%

Net profit after tax -147196 40711

Shareholder's fund 370989 515282

Return on capital

employed

(Profit before interest & tax/Aveage

shareholders fund) -39.68% 7.90%

Credit purchase 686906 709344

Creditors 81660 98420

Creditors settlement

period

Average credit creditors/Total credit

purchase*365 43.39 50.64

Current assets

$607,758.0

0

$657,679.0

0

Current liabilities

$274,031.0

0

$293,359.0

0

Stock

$338,826.0

0

$310,934.0

0

Current ratio (Current assets /Current liabilities) 2.22:1 2.24:1

Acid test ratio

(Current assets - stock)/current

liabilities 0.98 1.18

Average trade debtors 160806 186284.5

Total credit sales 1164304 1344523

Debtors collection period

(Average trade debtors/Total credit

sales)*365 50.41 50.57

Debt 356432 250000

Equity 370989 515282

Gearing ratio Long-term debt/(debt + equity) 0.49:1 0.33:1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(ii) Analysis of ratios

Profitability performance

Bellovida Ltd’s gross profit came down from 46.77% to 40.34% in FY 2016 due to

huge decline in the total sales by 13.40% due to lack of market demand, poor quality products,

availability of organic beauty products by competitors at economical charges and others. In

despite of this, as company operates worldwide, therefore, at international presence, firm also

suffered issues like inflation, currency exchange rate and political landscape in different nations.

Besides this, although selling, general and administration expenses were under the control of

manger, still, high depreciation and rising cost of borrowing resultant fall in net profit. It has

resultant net loss of 7.76% on total sales indicates that firm had not performed strongly in the

market. Despite this, as company had made a provision of income tax worth 56832 which tends

to decline net profit, as a result, return on capital employed came downward from 7.90% to

39.68% loss.

Liquidity performance:

Current ratio fallen from 2.24:1 to 2.22:1, still, it is above ideal ratio of 2:1 which state

that liquidity is properly managed by the firm to pay-off timely all of its deferred payment to

suppliers and other short-term debt. Due to high availability of stock at the end of the financial

year, acid test ratio came down from 1.18:1 to 0.98:1 which is closer to the benchmark of 1:1.

Thus, the results presents that there is a sound management of liquidity status in the business.

Efficiency performance:

Creditor’s settlement period came down from 50.64 to 43.39 days shows that in this year,

firm decided to pay their suppliers quickly by arranging required liquidity. However,, debtors

collection period remain constant to 50 days which shows that firm did not change its credit

collection policy considering their current liquidity status.

Gearing ratio:

The ratio reveals that this year, firm increased its leverage in its capital structure through

more borrowings as in the earlier period, debt was just used in 33% out of total capital, which

grown up to 49% this year. It may be to get tax benefit through interest deduction. Despite this,

as due to loss, company may suffer issues to attract investors to put money in the business. The

2

Profitability performance

Bellovida Ltd’s gross profit came down from 46.77% to 40.34% in FY 2016 due to

huge decline in the total sales by 13.40% due to lack of market demand, poor quality products,

availability of organic beauty products by competitors at economical charges and others. In

despite of this, as company operates worldwide, therefore, at international presence, firm also

suffered issues like inflation, currency exchange rate and political landscape in different nations.

Besides this, although selling, general and administration expenses were under the control of

manger, still, high depreciation and rising cost of borrowing resultant fall in net profit. It has

resultant net loss of 7.76% on total sales indicates that firm had not performed strongly in the

market. Despite this, as company had made a provision of income tax worth 56832 which tends

to decline net profit, as a result, return on capital employed came downward from 7.90% to

39.68% loss.

Liquidity performance:

Current ratio fallen from 2.24:1 to 2.22:1, still, it is above ideal ratio of 2:1 which state

that liquidity is properly managed by the firm to pay-off timely all of its deferred payment to

suppliers and other short-term debt. Due to high availability of stock at the end of the financial

year, acid test ratio came down from 1.18:1 to 0.98:1 which is closer to the benchmark of 1:1.

Thus, the results presents that there is a sound management of liquidity status in the business.

Efficiency performance:

Creditor’s settlement period came down from 50.64 to 43.39 days shows that in this year,

firm decided to pay their suppliers quickly by arranging required liquidity. However,, debtors

collection period remain constant to 50 days which shows that firm did not change its credit

collection policy considering their current liquidity status.

Gearing ratio:

The ratio reveals that this year, firm increased its leverage in its capital structure through

more borrowings as in the earlier period, debt was just used in 33% out of total capital, which

grown up to 49% this year. It may be to get tax benefit through interest deduction. Despite this,

as due to loss, company may suffer issues to attract investors to put money in the business. The

2

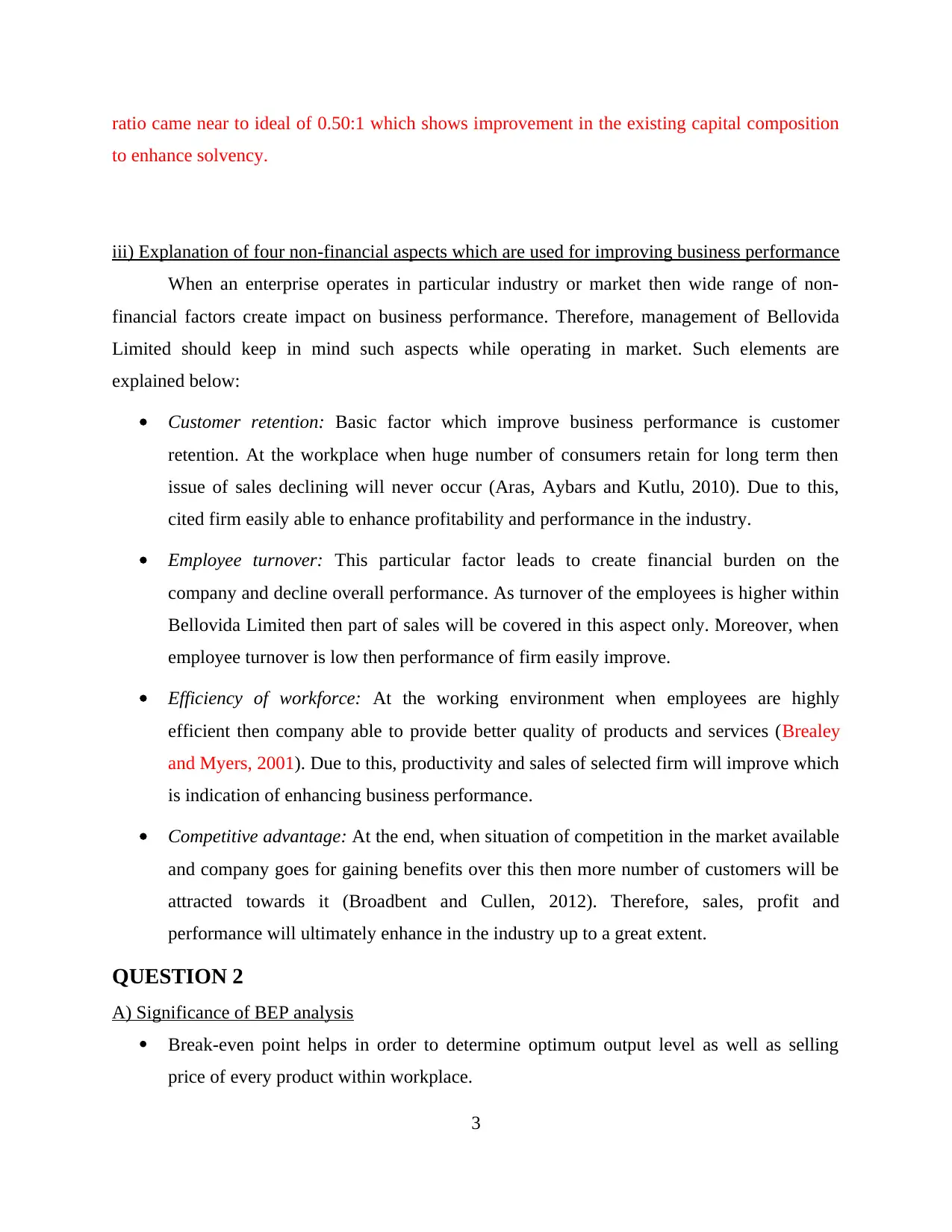

ratio came near to ideal of 0.50:1 which shows improvement in the existing capital composition

to enhance solvency.

iii) Explanation of four non-financial aspects which are used for improving business performance

When an enterprise operates in particular industry or market then wide range of non-

financial factors create impact on business performance. Therefore, management of Bellovida

Limited should keep in mind such aspects while operating in market. Such elements are

explained below:

Customer retention: Basic factor which improve business performance is customer

retention. At the workplace when huge number of consumers retain for long term then

issue of sales declining will never occur (Aras, Aybars and Kutlu, 2010). Due to this,

cited firm easily able to enhance profitability and performance in the industry.

Employee turnover: This particular factor leads to create financial burden on the

company and decline overall performance. As turnover of the employees is higher within

Bellovida Limited then part of sales will be covered in this aspect only. Moreover, when

employee turnover is low then performance of firm easily improve.

Efficiency of workforce: At the working environment when employees are highly

efficient then company able to provide better quality of products and services (Brealey

and Myers, 2001). Due to this, productivity and sales of selected firm will improve which

is indication of enhancing business performance.

Competitive advantage: At the end, when situation of competition in the market available

and company goes for gaining benefits over this then more number of customers will be

attracted towards it (Broadbent and Cullen, 2012). Therefore, sales, profit and

performance will ultimately enhance in the industry up to a great extent.

QUESTION 2

A) Significance of BEP analysis

Break-even point helps in order to determine optimum output level as well as selling

price of every product within workplace.

3

to enhance solvency.

iii) Explanation of four non-financial aspects which are used for improving business performance

When an enterprise operates in particular industry or market then wide range of non-

financial factors create impact on business performance. Therefore, management of Bellovida

Limited should keep in mind such aspects while operating in market. Such elements are

explained below:

Customer retention: Basic factor which improve business performance is customer

retention. At the workplace when huge number of consumers retain for long term then

issue of sales declining will never occur (Aras, Aybars and Kutlu, 2010). Due to this,

cited firm easily able to enhance profitability and performance in the industry.

Employee turnover: This particular factor leads to create financial burden on the

company and decline overall performance. As turnover of the employees is higher within

Bellovida Limited then part of sales will be covered in this aspect only. Moreover, when

employee turnover is low then performance of firm easily improve.

Efficiency of workforce: At the working environment when employees are highly

efficient then company able to provide better quality of products and services (Brealey

and Myers, 2001). Due to this, productivity and sales of selected firm will improve which

is indication of enhancing business performance.

Competitive advantage: At the end, when situation of competition in the market available

and company goes for gaining benefits over this then more number of customers will be

attracted towards it (Broadbent and Cullen, 2012). Therefore, sales, profit and

performance will ultimately enhance in the industry up to a great extent.

QUESTION 2

A) Significance of BEP analysis

Break-even point helps in order to determine optimum output level as well as selling

price of every product within workplace.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

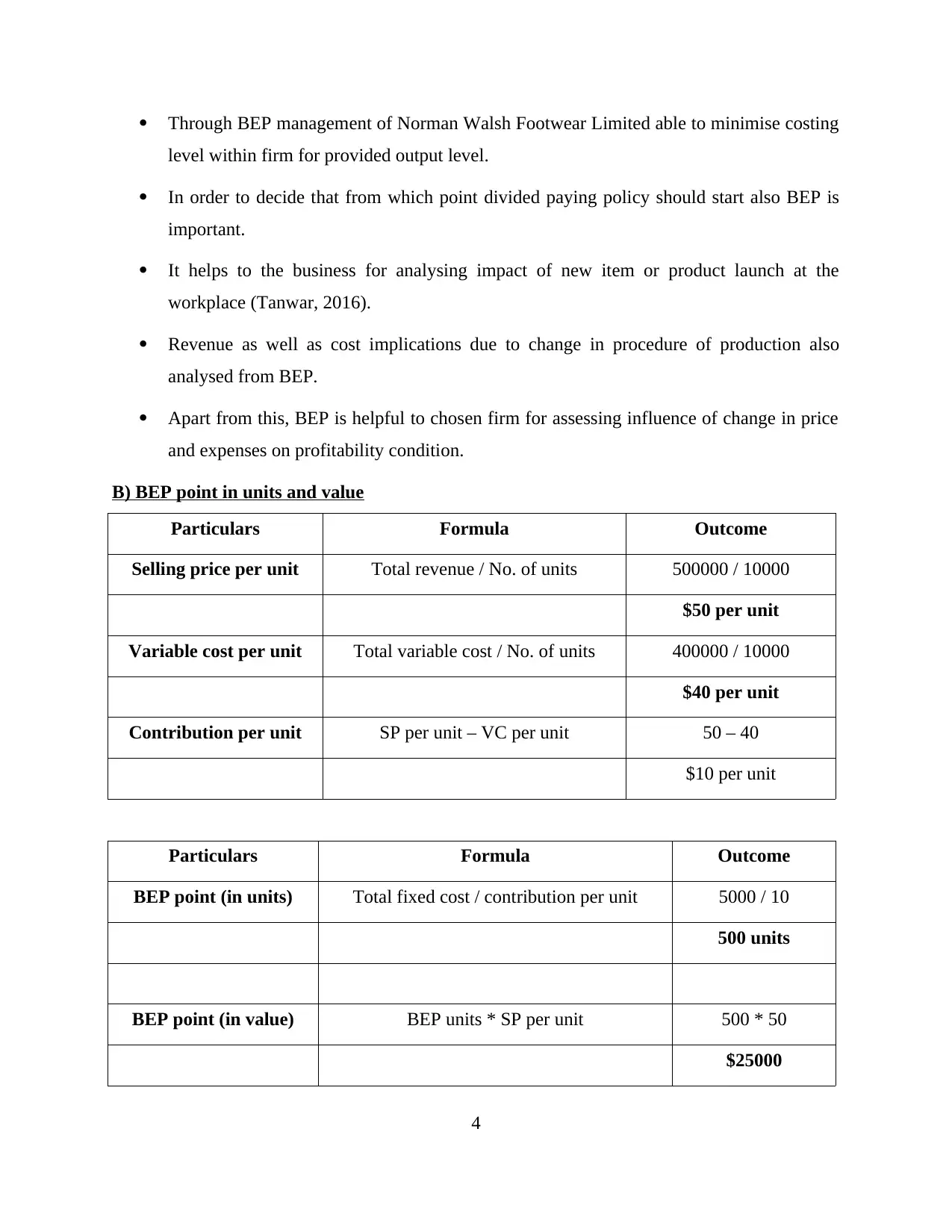

Through BEP management of Norman Walsh Footwear Limited able to minimise costing

level within firm for provided output level.

In order to decide that from which point divided paying policy should start also BEP is

important.

It helps to the business for analysing impact of new item or product launch at the

workplace (Tanwar, 2016).

Revenue as well as cost implications due to change in procedure of production also

analysed from BEP.

Apart from this, BEP is helpful to chosen firm for assessing influence of change in price

and expenses on profitability condition.

B) BEP point in units and value

Particulars Formula Outcome

Selling price per unit Total revenue / No. of units 500000 / 10000

$50 per unit

Variable cost per unit Total variable cost / No. of units 400000 / 10000

$40 per unit

Contribution per unit SP per unit – VC per unit 50 – 40

$10 per unit

Particulars Formula Outcome

BEP point (in units) Total fixed cost / contribution per unit 5000 / 10

500 units

BEP point (in value) BEP units * SP per unit 500 * 50

$25000

4

level within firm for provided output level.

In order to decide that from which point divided paying policy should start also BEP is

important.

It helps to the business for analysing impact of new item or product launch at the

workplace (Tanwar, 2016).

Revenue as well as cost implications due to change in procedure of production also

analysed from BEP.

Apart from this, BEP is helpful to chosen firm for assessing influence of change in price

and expenses on profitability condition.

B) BEP point in units and value

Particulars Formula Outcome

Selling price per unit Total revenue / No. of units 500000 / 10000

$50 per unit

Variable cost per unit Total variable cost / No. of units 400000 / 10000

$40 per unit

Contribution per unit SP per unit – VC per unit 50 – 40

$10 per unit

Particulars Formula Outcome

BEP point (in units) Total fixed cost / contribution per unit 5000 / 10

500 units

BEP point (in value) BEP units * SP per unit 500 * 50

$25000

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

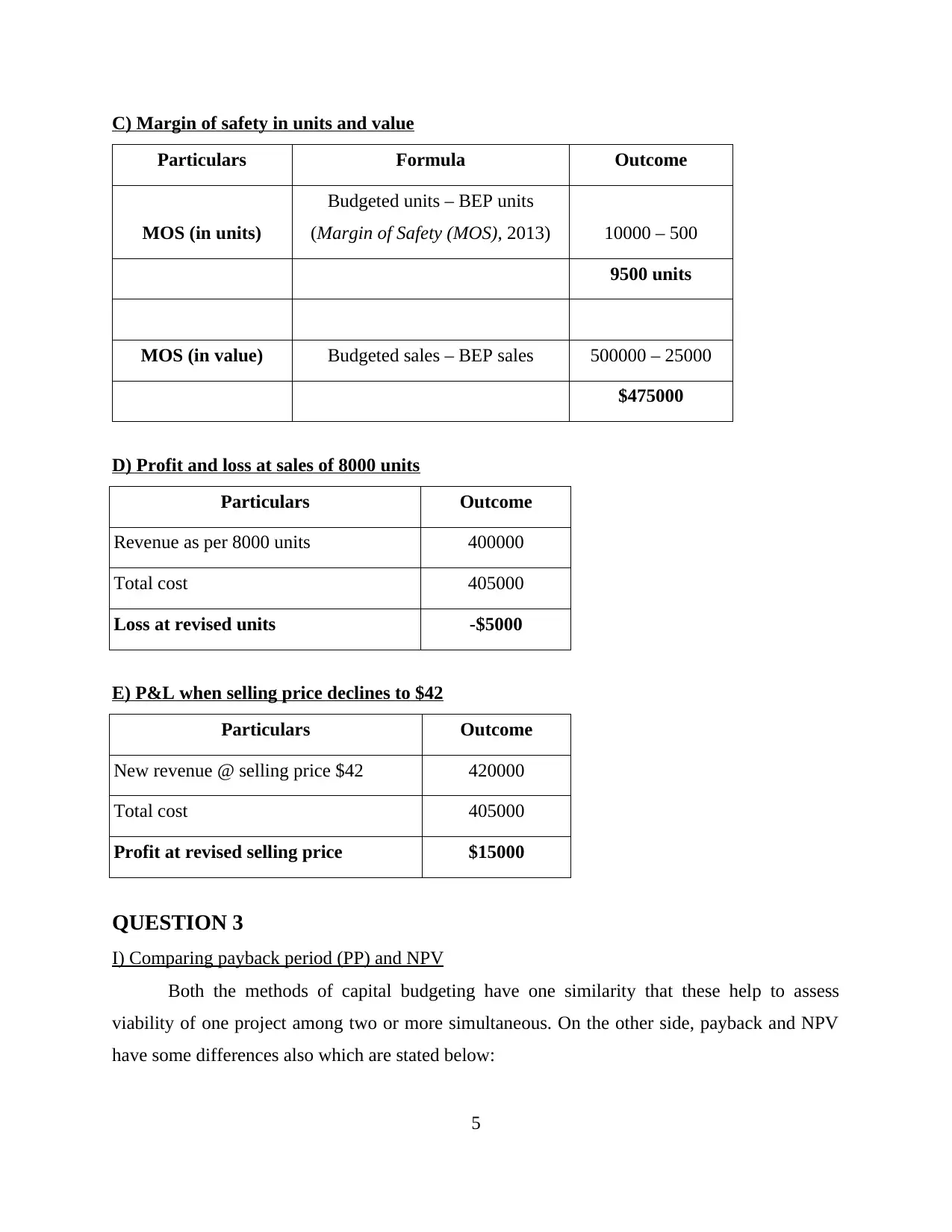

C) Margin of safety in units and value

Particulars Formula Outcome

MOS (in units)

Budgeted units – BEP units

(Margin of Safety (MOS), 2013) 10000 – 500

9500 units

MOS (in value) Budgeted sales – BEP sales 500000 – 25000

$475000

D) Profit and loss at sales of 8000 units

Particulars Outcome

Revenue as per 8000 units 400000

Total cost 405000

Loss at revised units -$5000

E) P&L when selling price declines to $42

Particulars Outcome

New revenue @ selling price $42 420000

Total cost 405000

Profit at revised selling price $15000

QUESTION 3

I) Comparing payback period (PP) and NPV

Both the methods of capital budgeting have one similarity that these help to assess

viability of one project among two or more simultaneous. On the other side, payback and NPV

have some differences also which are stated below:

5

Particulars Formula Outcome

MOS (in units)

Budgeted units – BEP units

(Margin of Safety (MOS), 2013) 10000 – 500

9500 units

MOS (in value) Budgeted sales – BEP sales 500000 – 25000

$475000

D) Profit and loss at sales of 8000 units

Particulars Outcome

Revenue as per 8000 units 400000

Total cost 405000

Loss at revised units -$5000

E) P&L when selling price declines to $42

Particulars Outcome

New revenue @ selling price $42 420000

Total cost 405000

Profit at revised selling price $15000

QUESTION 3

I) Comparing payback period (PP) and NPV

Both the methods of capital budgeting have one similarity that these help to assess

viability of one project among two or more simultaneous. On the other side, payback and NPV

have some differences also which are stated below:

5

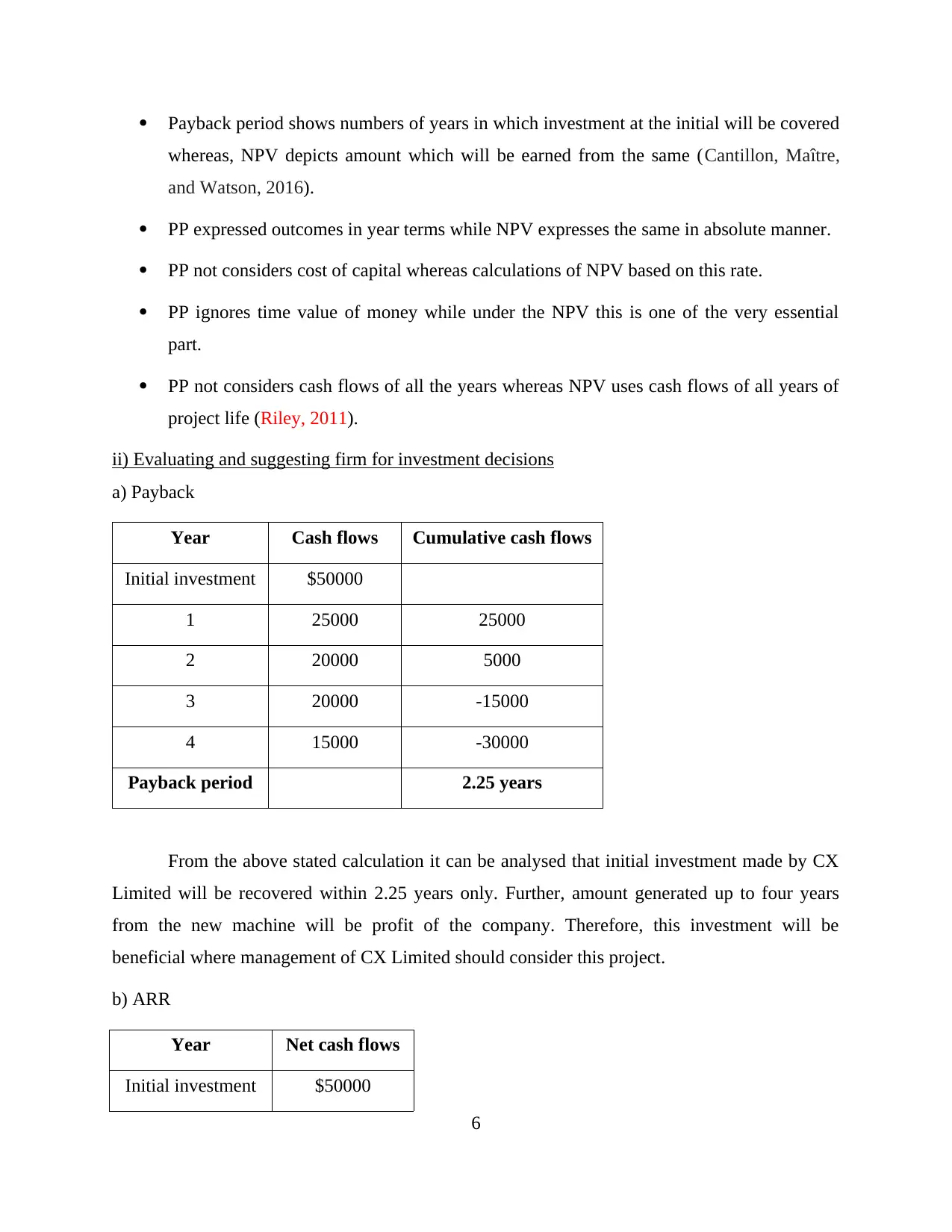

Payback period shows numbers of years in which investment at the initial will be covered

whereas, NPV depicts amount which will be earned from the same (Cantillon, Maître,

and Watson, 2016).

PP expressed outcomes in year terms while NPV expresses the same in absolute manner.

PP not considers cost of capital whereas calculations of NPV based on this rate.

PP ignores time value of money while under the NPV this is one of the very essential

part.

PP not considers cash flows of all the years whereas NPV uses cash flows of all years of

project life (Riley, 2011).

ii) Evaluating and suggesting firm for investment decisions

a) Payback

Year Cash flows Cumulative cash flows

Initial investment $50000

1 25000 25000

2 20000 5000

3 20000 -15000

4 15000 -30000

Payback period 2.25 years

From the above stated calculation it can be analysed that initial investment made by CX

Limited will be recovered within 2.25 years only. Further, amount generated up to four years

from the new machine will be profit of the company. Therefore, this investment will be

beneficial where management of CX Limited should consider this project.

b) ARR

Year Net cash flows

Initial investment $50000

6

whereas, NPV depicts amount which will be earned from the same (Cantillon, Maître,

and Watson, 2016).

PP expressed outcomes in year terms while NPV expresses the same in absolute manner.

PP not considers cost of capital whereas calculations of NPV based on this rate.

PP ignores time value of money while under the NPV this is one of the very essential

part.

PP not considers cash flows of all the years whereas NPV uses cash flows of all years of

project life (Riley, 2011).

ii) Evaluating and suggesting firm for investment decisions

a) Payback

Year Cash flows Cumulative cash flows

Initial investment $50000

1 25000 25000

2 20000 5000

3 20000 -15000

4 15000 -30000

Payback period 2.25 years

From the above stated calculation it can be analysed that initial investment made by CX

Limited will be recovered within 2.25 years only. Further, amount generated up to four years

from the new machine will be profit of the company. Therefore, this investment will be

beneficial where management of CX Limited should consider this project.

b) ARR

Year Net cash flows

Initial investment $50000

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

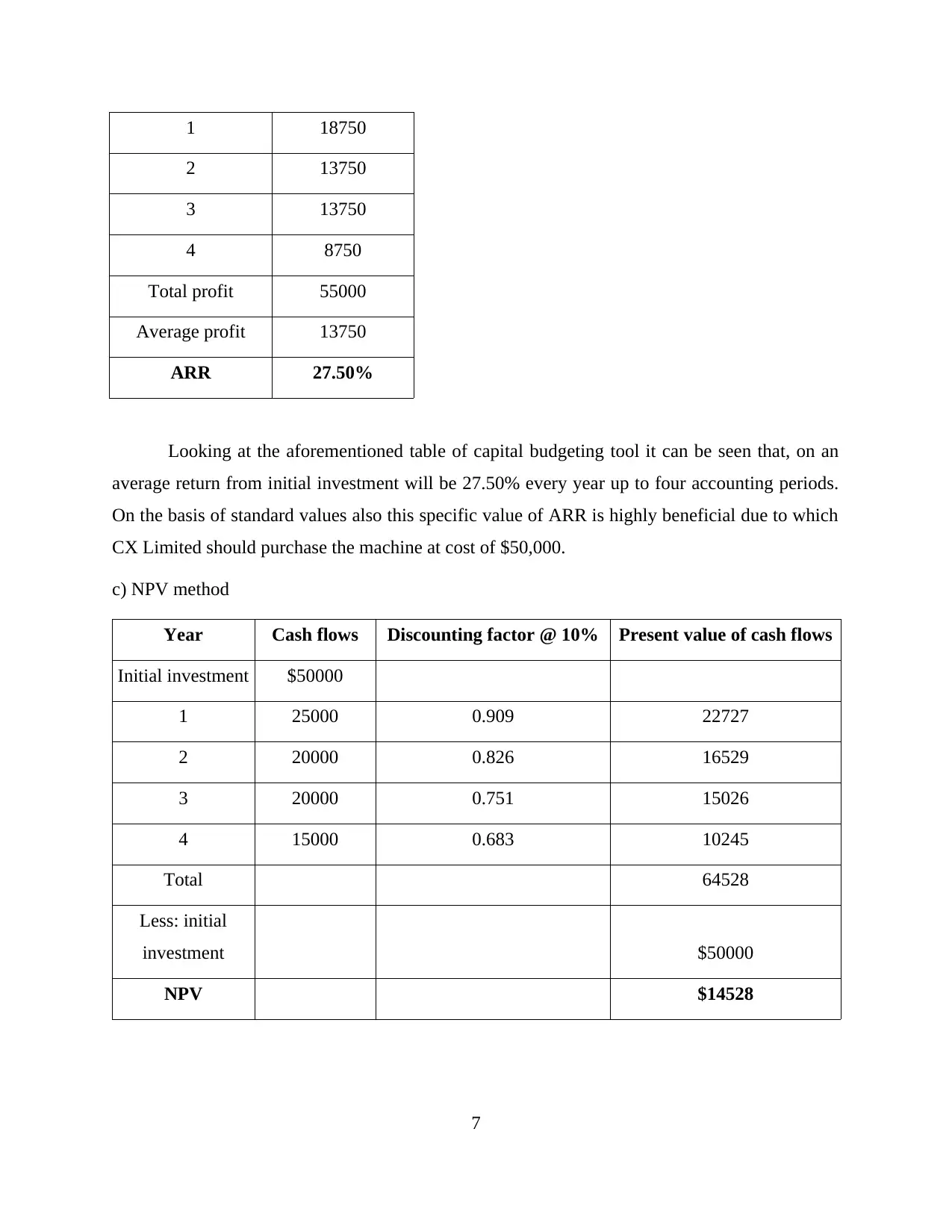

1 18750

2 13750

3 13750

4 8750

Total profit 55000

Average profit 13750

ARR 27.50%

Looking at the aforementioned table of capital budgeting tool it can be seen that, on an

average return from initial investment will be 27.50% every year up to four accounting periods.

On the basis of standard values also this specific value of ARR is highly beneficial due to which

CX Limited should purchase the machine at cost of $50,000.

c) NPV method

Year Cash flows Discounting factor @ 10% Present value of cash flows

Initial investment $50000

1 25000 0.909 22727

2 20000 0.826 16529

3 20000 0.751 15026

4 15000 0.683 10245

Total 64528

Less: initial

investment $50000

NPV $14528

7

2 13750

3 13750

4 8750

Total profit 55000

Average profit 13750

ARR 27.50%

Looking at the aforementioned table of capital budgeting tool it can be seen that, on an

average return from initial investment will be 27.50% every year up to four accounting periods.

On the basis of standard values also this specific value of ARR is highly beneficial due to which

CX Limited should purchase the machine at cost of $50,000.

c) NPV method

Year Cash flows Discounting factor @ 10% Present value of cash flows

Initial investment $50000

1 25000 0.909 22727

2 20000 0.826 16529

3 20000 0.751 15026

4 15000 0.683 10245

Total 64528

Less: initial

investment $50000

NPV $14528

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Another tool of investment appraisal method is net present value which reflects profit or

return which will be generated at the end of project life from investment made. Positive NPV of

the project is advantageous for the firms. In the current case scenario, value of NPV is worth of

$14528 which is positive and better. Due to this, CX Limited must invest money in this project.

QUESTION 4

i) Listing out key functions and activities of a bank

Key function of the bank is to accept deposits made by the people and corporations. The

deposits are like current account, fixed, recurring as well as savings.

In order to provide loan or required fund to people and firms also bank comes into

consideration.

Apart from this, discounting of bills of exchange is done by banks also which is another

key activity of them (Finkler and et.al., 2016).

Further, bank has some agency functions which include transfer of funds, cheques

collection, periodic payments and collections as well as portfolio management.

ii) Explaining three terms

a) Bank Overdraft: Overdraft is one kind of extension or crossing limit of credit of

borrowing amount from bank when account becomes zero. Generally, it means that bank

provided loan to customers when balance of their account becomes minor.

b) Hire Purchase: A procedure in which one person pays amount to another behind using

asset in an instalment basis for using it is known as hire purchase. Herein, ownership transferred

at the end of agreement period.

c) Venture Capitalist: A person who makes investment in business ventures or any start-

up is referred as venture capitalists. It is one kind of equity financing where company has to give

shareholding of it to venture capitalist as cost of finance (Mao, 2013).

iii) Significance of WC management for manufacturing company

Working capital (WC) is a tool which reflects difference between current assets and

current liabilities of the company. It is very essential and significant part of each and every sector

8

return which will be generated at the end of project life from investment made. Positive NPV of

the project is advantageous for the firms. In the current case scenario, value of NPV is worth of

$14528 which is positive and better. Due to this, CX Limited must invest money in this project.

QUESTION 4

i) Listing out key functions and activities of a bank

Key function of the bank is to accept deposits made by the people and corporations. The

deposits are like current account, fixed, recurring as well as savings.

In order to provide loan or required fund to people and firms also bank comes into

consideration.

Apart from this, discounting of bills of exchange is done by banks also which is another

key activity of them (Finkler and et.al., 2016).

Further, bank has some agency functions which include transfer of funds, cheques

collection, periodic payments and collections as well as portfolio management.

ii) Explaining three terms

a) Bank Overdraft: Overdraft is one kind of extension or crossing limit of credit of

borrowing amount from bank when account becomes zero. Generally, it means that bank

provided loan to customers when balance of their account becomes minor.

b) Hire Purchase: A procedure in which one person pays amount to another behind using

asset in an instalment basis for using it is known as hire purchase. Herein, ownership transferred

at the end of agreement period.

c) Venture Capitalist: A person who makes investment in business ventures or any start-

up is referred as venture capitalists. It is one kind of equity financing where company has to give

shareholding of it to venture capitalist as cost of finance (Mao, 2013).

iii) Significance of WC management for manufacturing company

Working capital (WC) is a tool which reflects difference between current assets and

current liabilities of the company. It is very essential and significant part of each and every sector

8

along with manufacturing. Further, some key importance of WC management for selected

industry is stated below:

Key significance of better WC and proper management is that, it helps to manufacturing

businesses for gaining higher return on capital invested to manufacture products and

services (Walker, 2009).

It helps to utilise available equipments of manufacturing in an optimum direction along

with maintaining them appropriately.

By managing WC in proper way, companies of cited sector able to improve credit profile

among stakeholders as well as manage solvency. When solvency ratio is lower, then

interest burden on business reduces (Importance of Working Capital Management, 2017).

It supports to raise profitability and liquidity position which is indication of improving

business performance.

Through WC management, manufacturing firms can gain competitive benefits in the

industry.

QUESTION 5

i) Various pricing methods and suggesting the best strategy Market based: As per this method, on the basis of quantity demanded in market by

customers price of products is to be determined. Through this, BestCost can charge price

as demand fluctuations in the market of CEREAL6 product. Cost plus pricing: In this kind of pricing technique, at the initial level cost of per unit is

to be determined and then desired percentage of profit added. It is supportive for

recovering all the expenses associated with the production and selling (Arnold, 2013). Competitor led pricing: Herein, pricing level of existing rivals available in the market is

analysed by the management and then charges of own products are determined. Using

this particular method, BestCost Limited able to gain competitive benefits in the industry. Market penetration: At the last, when company introduces it in the market and start

selling products then charges low prices. As start to grow in the market then increase

9

industry is stated below:

Key significance of better WC and proper management is that, it helps to manufacturing

businesses for gaining higher return on capital invested to manufacture products and

services (Walker, 2009).

It helps to utilise available equipments of manufacturing in an optimum direction along

with maintaining them appropriately.

By managing WC in proper way, companies of cited sector able to improve credit profile

among stakeholders as well as manage solvency. When solvency ratio is lower, then

interest burden on business reduces (Importance of Working Capital Management, 2017).

It supports to raise profitability and liquidity position which is indication of improving

business performance.

Through WC management, manufacturing firms can gain competitive benefits in the

industry.

QUESTION 5

i) Various pricing methods and suggesting the best strategy Market based: As per this method, on the basis of quantity demanded in market by

customers price of products is to be determined. Through this, BestCost can charge price

as demand fluctuations in the market of CEREAL6 product. Cost plus pricing: In this kind of pricing technique, at the initial level cost of per unit is

to be determined and then desired percentage of profit added. It is supportive for

recovering all the expenses associated with the production and selling (Arnold, 2013). Competitor led pricing: Herein, pricing level of existing rivals available in the market is

analysed by the management and then charges of own products are determined. Using

this particular method, BestCost Limited able to gain competitive benefits in the industry. Market penetration: At the last, when company introduces it in the market and start

selling products then charges low prices. As start to grow in the market then increase

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.