Comprehensive Management Accounting and Financial Performance Review

VerifiedAdded on 2021/06/17

|13

|1936

|27

Homework Assignment

AI Summary

This management accounting assignment analyzes a company's financial performance using ratio analysis, trend analysis, and cash flow budgeting. The solution examines profitability, financial stability, and asset utilization ratios, comparing performance over multiple years. It includes calculations for key financial metrics such as operating profit margin, return on assets, and debt-to-equity ratio. Furthermore, the assignment covers cash budgeting, forecasting cash receipts and payments, and creating sales and purchase budgets. The document also discusses variance analysis, highlighting its role in monitoring and controlling costs. Finally, it offers insights into the limitations of ratio analysis and variance analysis while providing a comprehensive overview of the company's financial health and future cash needs.

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Solution 1:..................................................................................................................................3

Solution 1.1:...........................................................................................................................3

Solution 1.2:...........................................................................................................................5

Solution 1.3:...........................................................................................................................7

Solution 2:..................................................................................................................................9

Solution 2.1:...........................................................................................................................9

Solution 2.2:.........................................................................................................................11

Solution 1:..................................................................................................................................3

Solution 1.1:...........................................................................................................................3

Solution 1.2:...........................................................................................................................5

Solution 1.3:...........................................................................................................................7

Solution 2:..................................................................................................................................9

Solution 2.1:...........................................................................................................................9

Solution 2.2:.........................................................................................................................11

Solution 1:

Solution 1.1:

a. Ratio analysis helps provide an insight into the financial performance of the company.

In the given case we are provided with some ratios of company for two financial

years, from which we need to determine the credit worthiness of the company. From

the ratio analysis of two years we can see that the company has earned lower profits in

the current year, nut the liquidity position of the company is in a good state. The

benchmark for current ratio is 2 and the company has the ratio of 2.1. This shows high

liquidity and availability of funds for repayment of loan. The ratios paint a kind of

favourable picture for the credit worthiness of the company, but taking the decision

solely based on ratios will not be correct. it is important that we consider qualitative

information regarding company also, in order to have a complete picture. It is

important we also see other aspects of the business so that its real position can be

understood.

b. The above ratios give us an idea of the liquidity and profitability of the company.

there are few other ratios too which will help us analyse the company’s worth:

- Debt to equity ratio: this ratio helps us calculate the ratio of debt and equity

involved in the capital structure. This gives us the idea on how much debt is

already used by the company. Taking the general capital structure of the industry

to which company belongs we can see if more debt would be suitable for the

company or not. Based on the existing debt history of the company, the repayment

history can be analysed for future performance of the company.

- Interest coverage ratio: the interest coverage ratio helps us analyse the earnings

of the company. It helps us evaluate the company’s ability to earn eng profits to

pay back the interest accrued. This ratio calculates the number of times is the

earnings of the interest expense. Higher the ratio better it is. It is important to

check the company’s profitability before sanctioning of any loan. The company

should have a secure financial health so that it can secure the lenders of the

repayment of loan and interest expense. (Atkinson, 2012)

- Debtor turnover ratio: this is a kind of efficiency ratio that will help us

understand the cash flow of the company from its debtor. Higher turnover ratios

indicate that the company will have its fund stuck with the debtors for higher

Solution 1.1:

a. Ratio analysis helps provide an insight into the financial performance of the company.

In the given case we are provided with some ratios of company for two financial

years, from which we need to determine the credit worthiness of the company. From

the ratio analysis of two years we can see that the company has earned lower profits in

the current year, nut the liquidity position of the company is in a good state. The

benchmark for current ratio is 2 and the company has the ratio of 2.1. This shows high

liquidity and availability of funds for repayment of loan. The ratios paint a kind of

favourable picture for the credit worthiness of the company, but taking the decision

solely based on ratios will not be correct. it is important that we consider qualitative

information regarding company also, in order to have a complete picture. It is

important we also see other aspects of the business so that its real position can be

understood.

b. The above ratios give us an idea of the liquidity and profitability of the company.

there are few other ratios too which will help us analyse the company’s worth:

- Debt to equity ratio: this ratio helps us calculate the ratio of debt and equity

involved in the capital structure. This gives us the idea on how much debt is

already used by the company. Taking the general capital structure of the industry

to which company belongs we can see if more debt would be suitable for the

company or not. Based on the existing debt history of the company, the repayment

history can be analysed for future performance of the company.

- Interest coverage ratio: the interest coverage ratio helps us analyse the earnings

of the company. It helps us evaluate the company’s ability to earn eng profits to

pay back the interest accrued. This ratio calculates the number of times is the

earnings of the interest expense. Higher the ratio better it is. It is important to

check the company’s profitability before sanctioning of any loan. The company

should have a secure financial health so that it can secure the lenders of the

repayment of loan and interest expense. (Atkinson, 2012)

- Debtor turnover ratio: this is a kind of efficiency ratio that will help us

understand the cash flow of the company from its debtor. Higher turnover ratios

indicate that the company will have its fund stuck with the debtors for higher

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

period. Company needs to make policies in order to ensure regular flow of funds

from debtors in order to ensure liquidity.

c. Though ratio analysis is a very essential tool which helps in taking financial decisions,

it also has a few limitations:

- Ratio analysis is based on past performance, it s not necessary that the past

performance will be continued by the company in the near future

- The figures of the financial statement fail to incorporate the inflation rates, which

will affect the future financial status of the company.

- There may be changes taking place in the management of the company or in the

shareholding which are likely to affect the operations, ratio analysis fails to

incorporate effects of decision like these on the financial performance of the

company.

- Interpretation of ratio analysis is not a easy task. It is important that the data form

ratio analysis is interpreted properly in order to have correct results.

- Few of the ratios involve figures from the balance sheet. We should keep in mind

that these figures are on the last date of the balance sheet. These figures keep

changing and so does the financial viability of the company.

from debtors in order to ensure liquidity.

c. Though ratio analysis is a very essential tool which helps in taking financial decisions,

it also has a few limitations:

- Ratio analysis is based on past performance, it s not necessary that the past

performance will be continued by the company in the near future

- The figures of the financial statement fail to incorporate the inflation rates, which

will affect the future financial status of the company.

- There may be changes taking place in the management of the company or in the

shareholding which are likely to affect the operations, ratio analysis fails to

incorporate effects of decision like these on the financial performance of the

company.

- Interpretation of ratio analysis is not a easy task. It is important that the data form

ratio analysis is interpreted properly in order to have correct results.

- Few of the ratios involve figures from the balance sheet. We should keep in mind

that these figures are on the last date of the balance sheet. These figures keep

changing and so does the financial viability of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

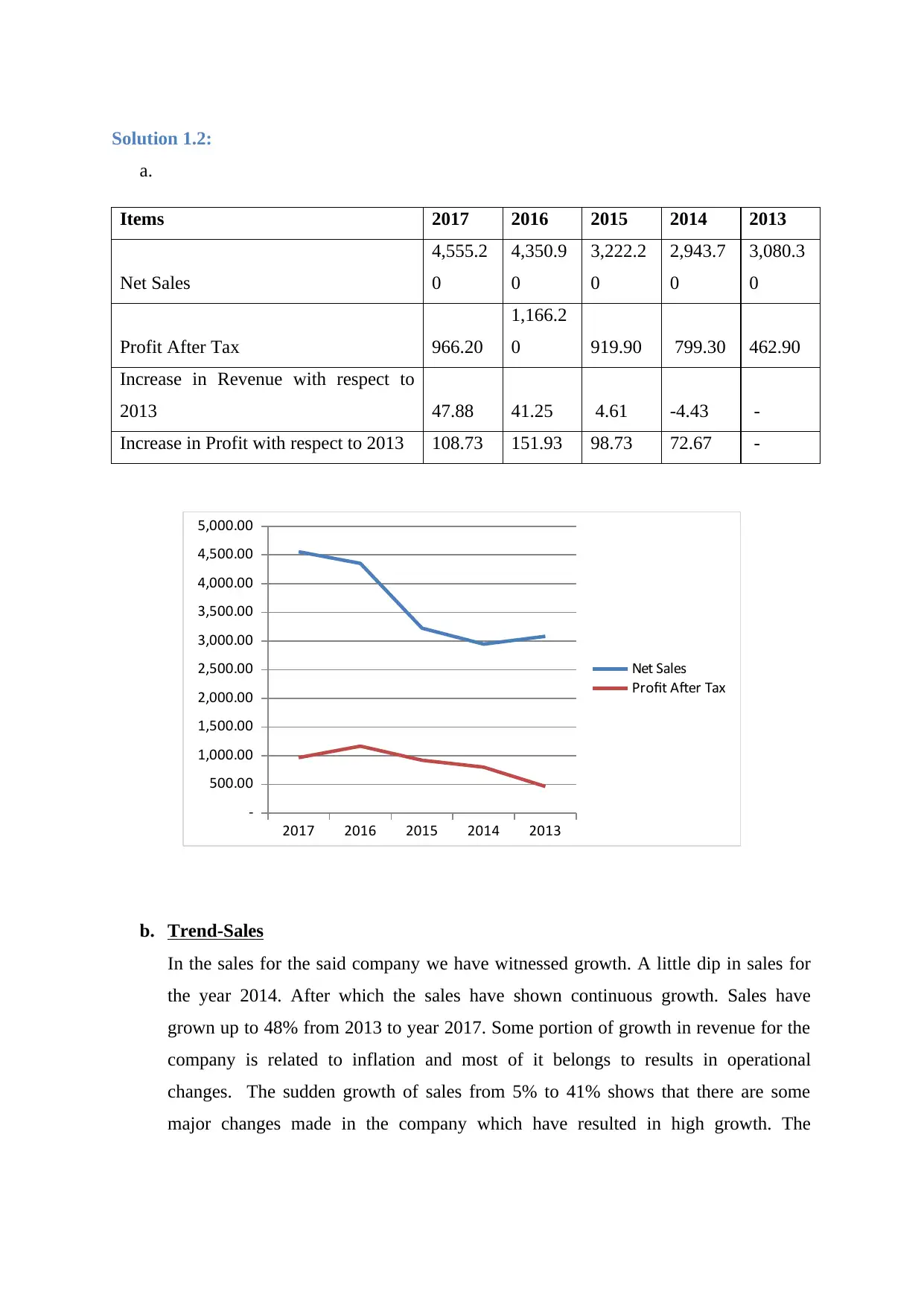

Solution 1.2:

a.

Items 2017 2016 2015 2014 2013

Net Sales

4,555.2

0

4,350.9

0

3,222.2

0

2,943.7

0

3,080.3

0

Profit After Tax 966.20

1,166.2

0 919.90 799.30 462.90

Increase in Revenue with respect to

2013 47.88 41.25 4.61 -4.43 -

Increase in Profit with respect to 2013 108.73 151.93 98.73 72.67 -

2017 2016 2015 2014 2013

-

500.00

1,000.00

1,500.00

2,000.00

2,500.00

3,000.00

3,500.00

4,000.00

4,500.00

5,000.00

Net Sales

Profit After Tax

b. Trend-Sales

In the sales for the said company we have witnessed growth. A little dip in sales for

the year 2014. After which the sales have shown continuous growth. Sales have

grown up to 48% from 2013 to year 2017. Some portion of growth in revenue for the

company is related to inflation and most of it belongs to results in operational

changes. The sudden growth of sales from 5% to 41% shows that there are some

major changes made in the company which have resulted in high growth. The

a.

Items 2017 2016 2015 2014 2013

Net Sales

4,555.2

0

4,350.9

0

3,222.2

0

2,943.7

0

3,080.3

0

Profit After Tax 966.20

1,166.2

0 919.90 799.30 462.90

Increase in Revenue with respect to

2013 47.88 41.25 4.61 -4.43 -

Increase in Profit with respect to 2013 108.73 151.93 98.73 72.67 -

2017 2016 2015 2014 2013

-

500.00

1,000.00

1,500.00

2,000.00

2,500.00

3,000.00

3,500.00

4,000.00

4,500.00

5,000.00

Net Sales

Profit After Tax

b. Trend-Sales

In the sales for the said company we have witnessed growth. A little dip in sales for

the year 2014. After which the sales have shown continuous growth. Sales have

grown up to 48% from 2013 to year 2017. Some portion of growth in revenue for the

company is related to inflation and most of it belongs to results in operational

changes. The sudden growth of sales from 5% to 41% shows that there are some

major changes made in the company which have resulted in high growth. The

company has then managed maintained this growth rate in 2017. Highest growth in

revenue was witnessed in with growth of 48% in sales.

Trend-Profit

After the year 2013, a high growth in profit margin was witnessed. Even though

revenue fell by 4%, the net profit margin increased by 73% approximately. The

increase in profit margin may be due to operating efficiency in the organisation. It

seems that the company has implemented methods to make the most out of existing

resources. This has resulted in increase in profit margin by up to 109% in year 2017.

Though the revenue increase was 50%, the profit margin increased by 109%. This

shows some serious development on the part of the company.

revenue was witnessed in with growth of 48% in sales.

Trend-Profit

After the year 2013, a high growth in profit margin was witnessed. Even though

revenue fell by 4%, the net profit margin increased by 73% approximately. The

increase in profit margin may be due to operating efficiency in the organisation. It

seems that the company has implemented methods to make the most out of existing

resources. This has resulted in increase in profit margin by up to 109% in year 2017.

Though the revenue increase was 50%, the profit margin increased by 109%. This

shows some serious development on the part of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

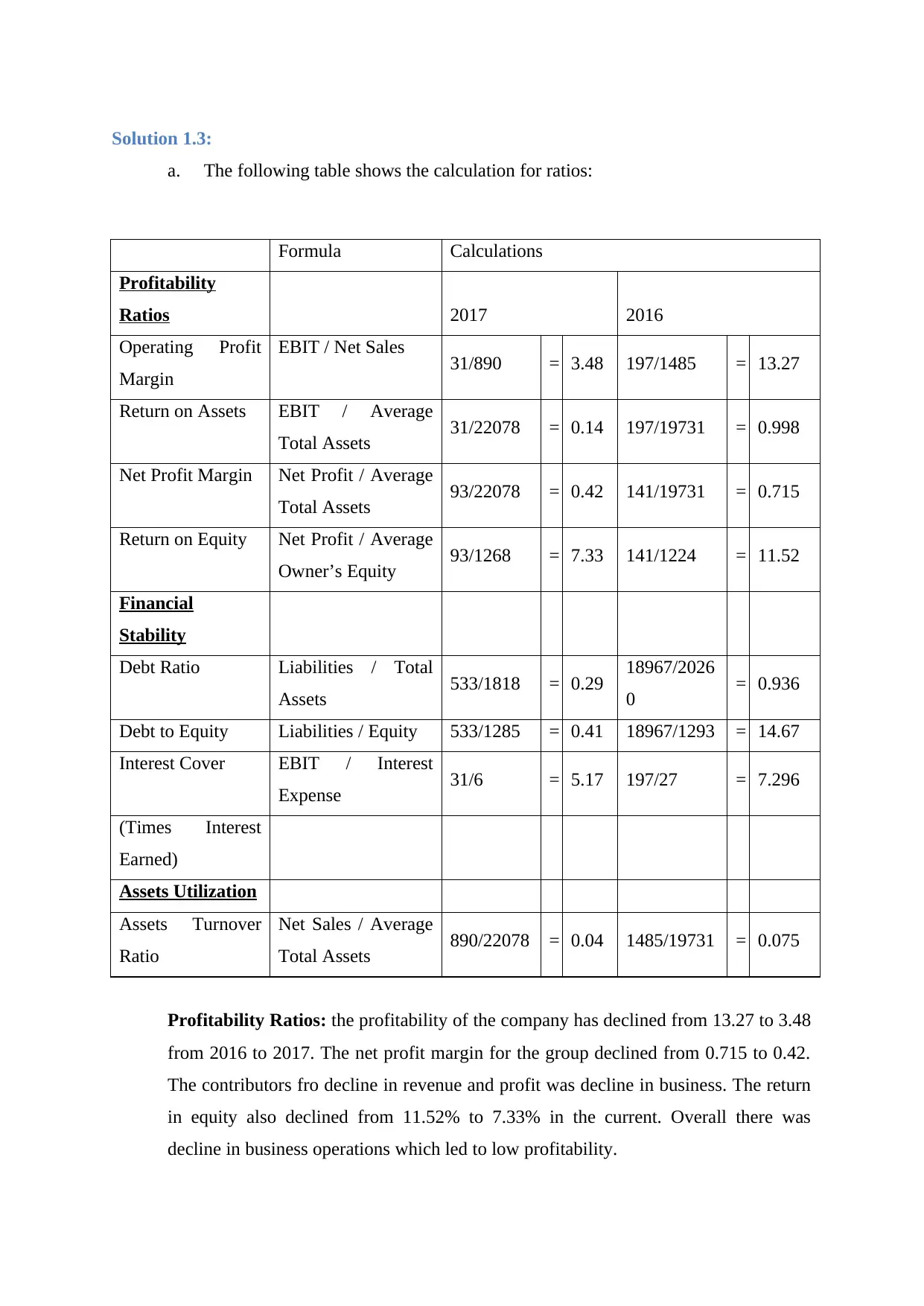

Solution 1.3:

a. The following table shows the calculation for ratios:

Formula Calculations

Profitability

Ratios 2017 2016

Operating Profit

Margin

EBIT / Net Sales 31/890 = 3.48 197/1485 = 13.27

Return on Assets EBIT / Average

Total Assets 31/22078 = 0.14 197/19731 = 0.998

Net Profit Margin Net Profit / Average

Total Assets 93/22078 = 0.42 141/19731 = 0.715

Return on Equity Net Profit / Average

Owner’s Equity 93/1268 = 7.33 141/1224 = 11.52

Financial

Stability

Debt Ratio Liabilities / Total

Assets 533/1818 = 0.29 18967/2026

0 = 0.936

Debt to Equity Liabilities / Equity 533/1285 = 0.41 18967/1293 = 14.67

Interest Cover EBIT / Interest

Expense 31/6 = 5.17 197/27 = 7.296

(Times Interest

Earned)

Assets Utilization

Assets Turnover

Ratio

Net Sales / Average

Total Assets 890/22078 = 0.04 1485/19731 = 0.075

Profitability Ratios: the profitability of the company has declined from 13.27 to 3.48

from 2016 to 2017. The net profit margin for the group declined from 0.715 to 0.42.

The contributors fro decline in revenue and profit was decline in business. The return

in equity also declined from 11.52% to 7.33% in the current. Overall there was

decline in business operations which led to low profitability.

a. The following table shows the calculation for ratios:

Formula Calculations

Profitability

Ratios 2017 2016

Operating Profit

Margin

EBIT / Net Sales 31/890 = 3.48 197/1485 = 13.27

Return on Assets EBIT / Average

Total Assets 31/22078 = 0.14 197/19731 = 0.998

Net Profit Margin Net Profit / Average

Total Assets 93/22078 = 0.42 141/19731 = 0.715

Return on Equity Net Profit / Average

Owner’s Equity 93/1268 = 7.33 141/1224 = 11.52

Financial

Stability

Debt Ratio Liabilities / Total

Assets 533/1818 = 0.29 18967/2026

0 = 0.936

Debt to Equity Liabilities / Equity 533/1285 = 0.41 18967/1293 = 14.67

Interest Cover EBIT / Interest

Expense 31/6 = 5.17 197/27 = 7.296

(Times Interest

Earned)

Assets Utilization

Assets Turnover

Ratio

Net Sales / Average

Total Assets 890/22078 = 0.04 1485/19731 = 0.075

Profitability Ratios: the profitability of the company has declined from 13.27 to 3.48

from 2016 to 2017. The net profit margin for the group declined from 0.715 to 0.42.

The contributors fro decline in revenue and profit was decline in business. The return

in equity also declined from 11.52% to 7.33% in the current. Overall there was

decline in business operations which led to low profitability.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Stability: from the ratios above we can see that the balance sheet size of

the group has decline drastically. The debt ratio of the company which was 0.936

times has now fallen to 0.29 times. The debt to equity ratio has declined from 14.67 to

0.41. The company has paid off its major debts which have led to decline in both debt

and assets. The interest coverage ratio which used to be 7.30 times has now become

5.17 times. This is due to lower profits and lower interest expenses.

Asset utilisation: the company used to have a sale of 0.075 for every dollar spent on

asset, now the company earns 0.04 for every dollar invested in asset.

b. Mr. Ming is of the view that of the cash flow from operating activities is not equal to

the earnings of the company then the company might have serious financial issues, we

agree with the view of Mr. Ming. Cash flow from operating activities represents the

cash flow from major part of the business. If the company does not have sufficient

cash flows from its operating activities and uses most of the funds of investing and

financing activities then it represents a stressful financial status. The company should

have sufficient cash flow from operations, since the major part of the business lies it

its operating activities. If it fails to generate cash then steps to improve operating

efficiency should be taken.

the group has decline drastically. The debt ratio of the company which was 0.936

times has now fallen to 0.29 times. The debt to equity ratio has declined from 14.67 to

0.41. The company has paid off its major debts which have led to decline in both debt

and assets. The interest coverage ratio which used to be 7.30 times has now become

5.17 times. This is due to lower profits and lower interest expenses.

Asset utilisation: the company used to have a sale of 0.075 for every dollar spent on

asset, now the company earns 0.04 for every dollar invested in asset.

b. Mr. Ming is of the view that of the cash flow from operating activities is not equal to

the earnings of the company then the company might have serious financial issues, we

agree with the view of Mr. Ming. Cash flow from operating activities represents the

cash flow from major part of the business. If the company does not have sufficient

cash flows from its operating activities and uses most of the funds of investing and

financing activities then it represents a stressful financial status. The company should

have sufficient cash flow from operations, since the major part of the business lies it

its operating activities. If it fails to generate cash then steps to improve operating

efficiency should be taken.

Solution 2:

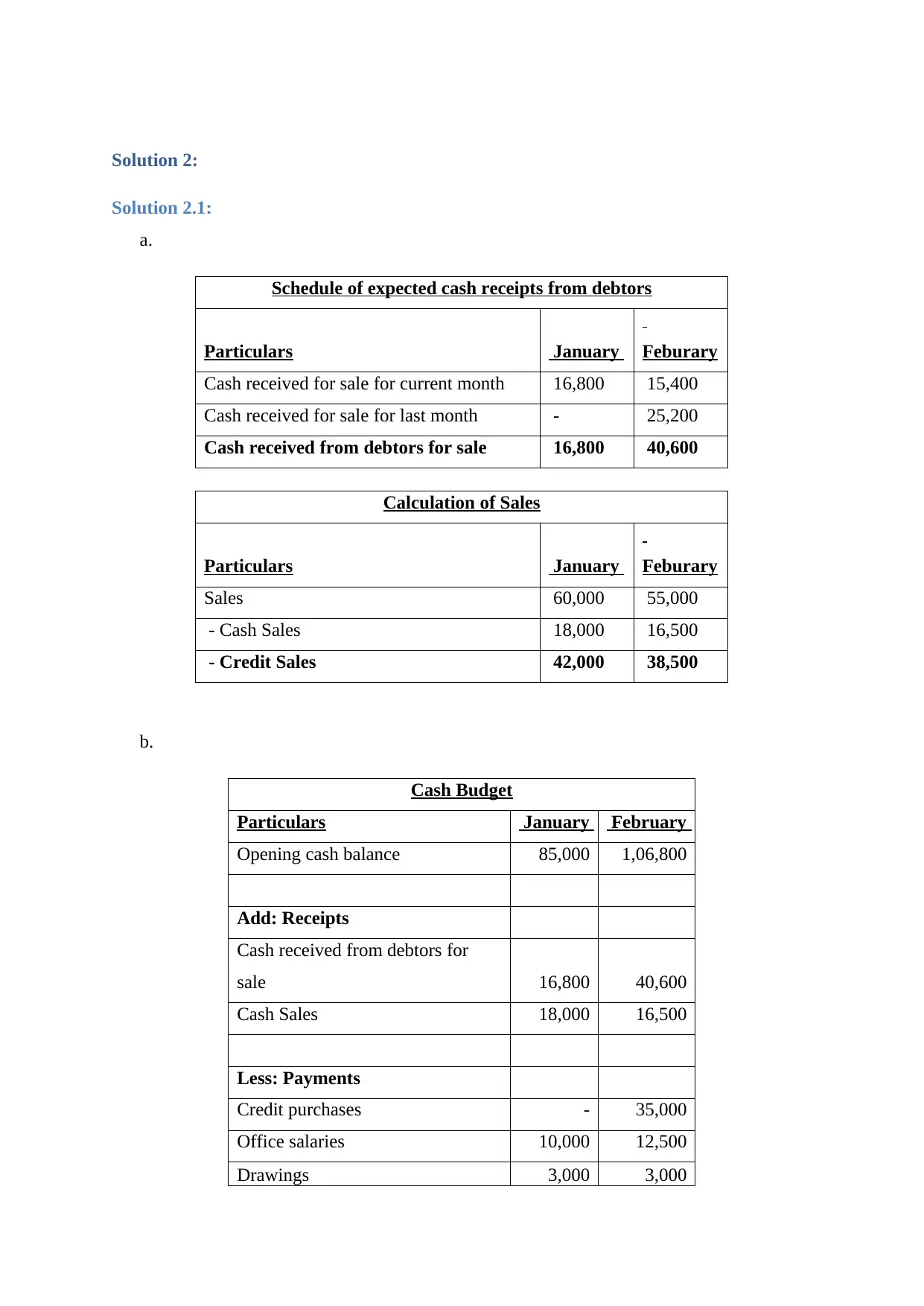

Solution 2.1:

a.

Schedule of expected cash receipts from debtors

Particulars January Feburary

Cash received for sale for current month 16,800 15,400

Cash received for sale for last month - 25,200

Cash received from debtors for sale 16,800 40,600

Calculation of Sales

Particulars January Feburary

Sales 60,000 55,000

- Cash Sales 18,000 16,500

- Credit Sales 42,000 38,500

b.

Cash Budget

Particulars January February

Opening cash balance 85,000 1,06,800

Add: Receipts

Cash received from debtors for

sale 16,800 40,600

Cash Sales 18,000 16,500

Less: Payments

Credit purchases - 35,000

Office salaries 10,000 12,500

Drawings 3,000 3,000

Solution 2.1:

a.

Schedule of expected cash receipts from debtors

Particulars January Feburary

Cash received for sale for current month 16,800 15,400

Cash received for sale for last month - 25,200

Cash received from debtors for sale 16,800 40,600

Calculation of Sales

Particulars January Feburary

Sales 60,000 55,000

- Cash Sales 18,000 16,500

- Credit Sales 42,000 38,500

b.

Cash Budget

Particulars January February

Opening cash balance 85,000 1,06,800

Add: Receipts

Cash received from debtors for

sale 16,800 40,600

Cash Sales 18,000 16,500

Less: Payments

Credit purchases - 35,000

Office salaries 10,000 12,500

Drawings 3,000 3,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Closing Cash balance 1,06,800 1,13,400

c. The company has an instalment of $80000 due at the end of February. From the

calculations above we can see that the company has a cash position of $113400 at the

end of February. Also, the company requires maintaining a cash balance of $15000 in

order to keep its solvency in check. Even if the company pays off its instalment of

$80000, it would still have cash of $33400 left to spare.

In case if the company had shortage of cash, then they should opt for short term

overdraft facilities. Therefore, the company is expected to have sufficient cash

balance at the end of February in order to meet the instalment expense.

c. The company has an instalment of $80000 due at the end of February. From the

calculations above we can see that the company has a cash position of $113400 at the

end of February. Also, the company requires maintaining a cash balance of $15000 in

order to keep its solvency in check. Even if the company pays off its instalment of

$80000, it would still have cash of $33400 left to spare.

In case if the company had shortage of cash, then they should opt for short term

overdraft facilities. Therefore, the company is expected to have sufficient cash

balance at the end of February in order to meet the instalment expense.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

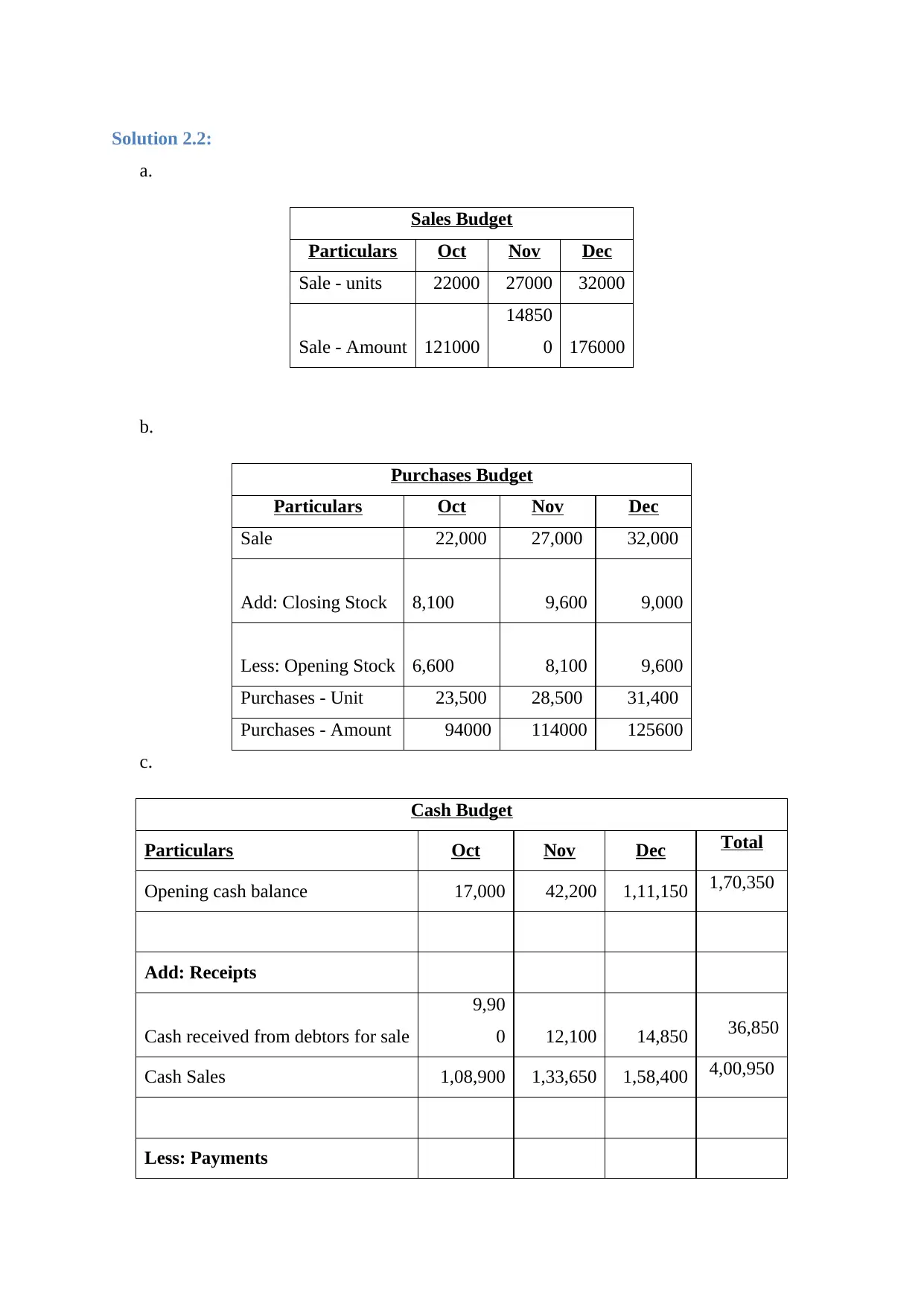

Solution 2.2:

a.

Sales Budget

Particulars Oct Nov Dec

Sale - units 22000 27000 32000

Sale - Amount 121000

14850

0 176000

b.

Purchases Budget

Particulars Oct Nov Dec

Sale 22,000 27,000 32,000

Add: Closing Stock 8,100 9,600 9,000

Less: Opening Stock 6,600 8,100 9,600

Purchases - Unit 23,500 28,500 31,400

Purchases - Amount 94000 114000 125600

c.

Cash Budget

Particulars Oct Nov Dec Total

Opening cash balance 17,000 42,200 1,11,150 1,70,350

Add: Receipts

Cash received from debtors for sale

9,90

0 12,100 14,850 36,850

Cash Sales 1,08,900 1,33,650 1,58,400 4,00,950

Less: Payments

a.

Sales Budget

Particulars Oct Nov Dec

Sale - units 22000 27000 32000

Sale - Amount 121000

14850

0 176000

b.

Purchases Budget

Particulars Oct Nov Dec

Sale 22,000 27,000 32,000

Add: Closing Stock 8,100 9,600 9,000

Less: Opening Stock 6,600 8,100 9,600

Purchases - Unit 23,500 28,500 31,400

Purchases - Amount 94000 114000 125600

c.

Cash Budget

Particulars Oct Nov Dec Total

Opening cash balance 17,000 42,200 1,11,150 1,70,350

Add: Receipts

Cash received from debtors for sale

9,90

0 12,100 14,850 36,850

Cash Sales 1,08,900 1,33,650 1,58,400 4,00,950

Less: Payments

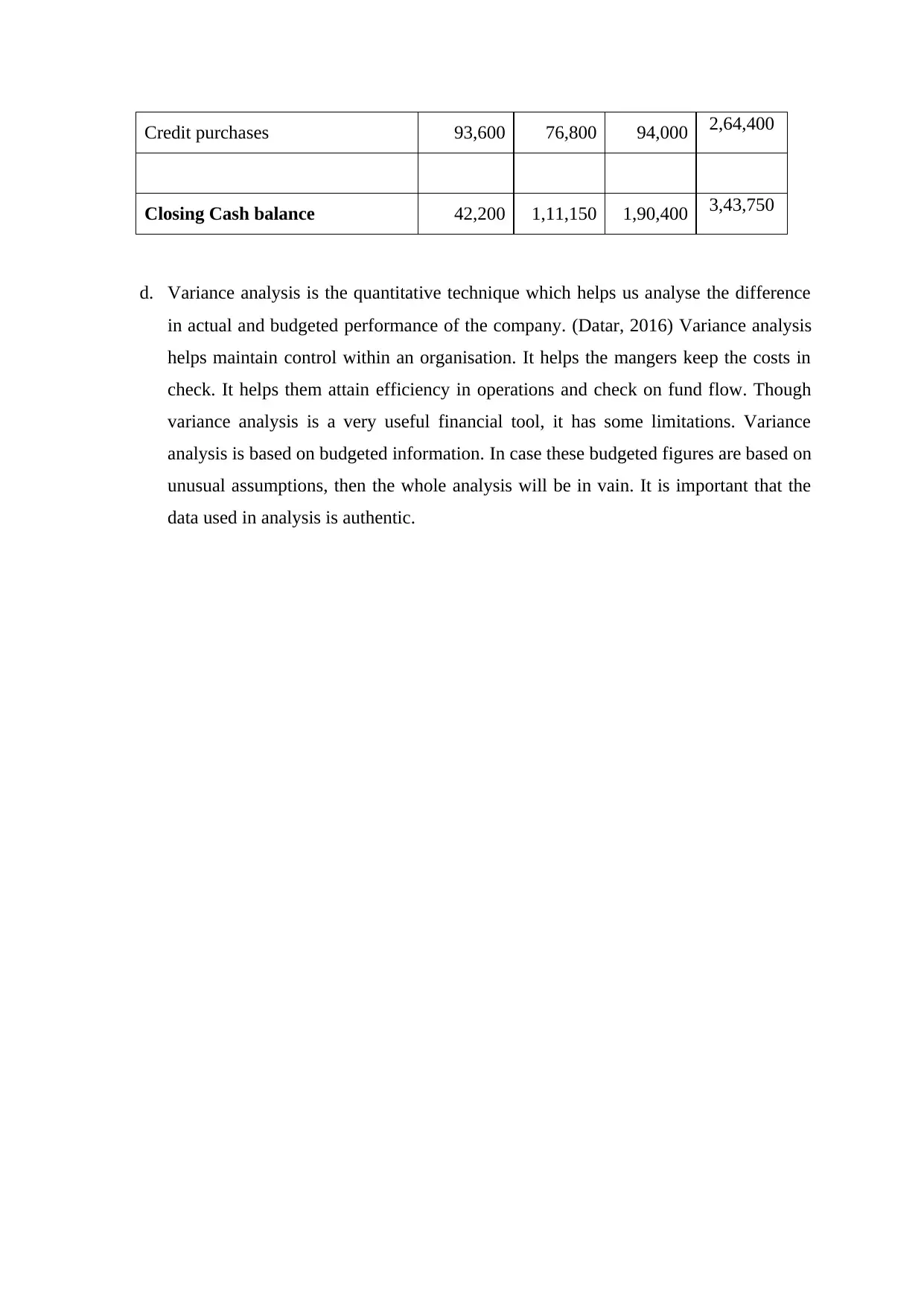

Credit purchases 93,600 76,800 94,000 2,64,400

Closing Cash balance 42,200 1,11,150 1,90,400 3,43,750

d. Variance analysis is the quantitative technique which helps us analyse the difference

in actual and budgeted performance of the company. (Datar, 2016) Variance analysis

helps maintain control within an organisation. It helps the mangers keep the costs in

check. It helps them attain efficiency in operations and check on fund flow. Though

variance analysis is a very useful financial tool, it has some limitations. Variance

analysis is based on budgeted information. In case these budgeted figures are based on

unusual assumptions, then the whole analysis will be in vain. It is important that the

data used in analysis is authentic.

Closing Cash balance 42,200 1,11,150 1,90,400 3,43,750

d. Variance analysis is the quantitative technique which helps us analyse the difference

in actual and budgeted performance of the company. (Datar, 2016) Variance analysis

helps maintain control within an organisation. It helps the mangers keep the costs in

check. It helps them attain efficiency in operations and check on fund flow. Though

variance analysis is a very useful financial tool, it has some limitations. Variance

analysis is based on budgeted information. In case these budgeted figures are based on

unusual assumptions, then the whole analysis will be in vain. It is important that the

data used in analysis is authentic.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.