Accounting for Managers: Performance and Overhead Analysis

VerifiedAdded on 2022/08/20

|11

|1749

|12

Homework Assignment

AI Summary

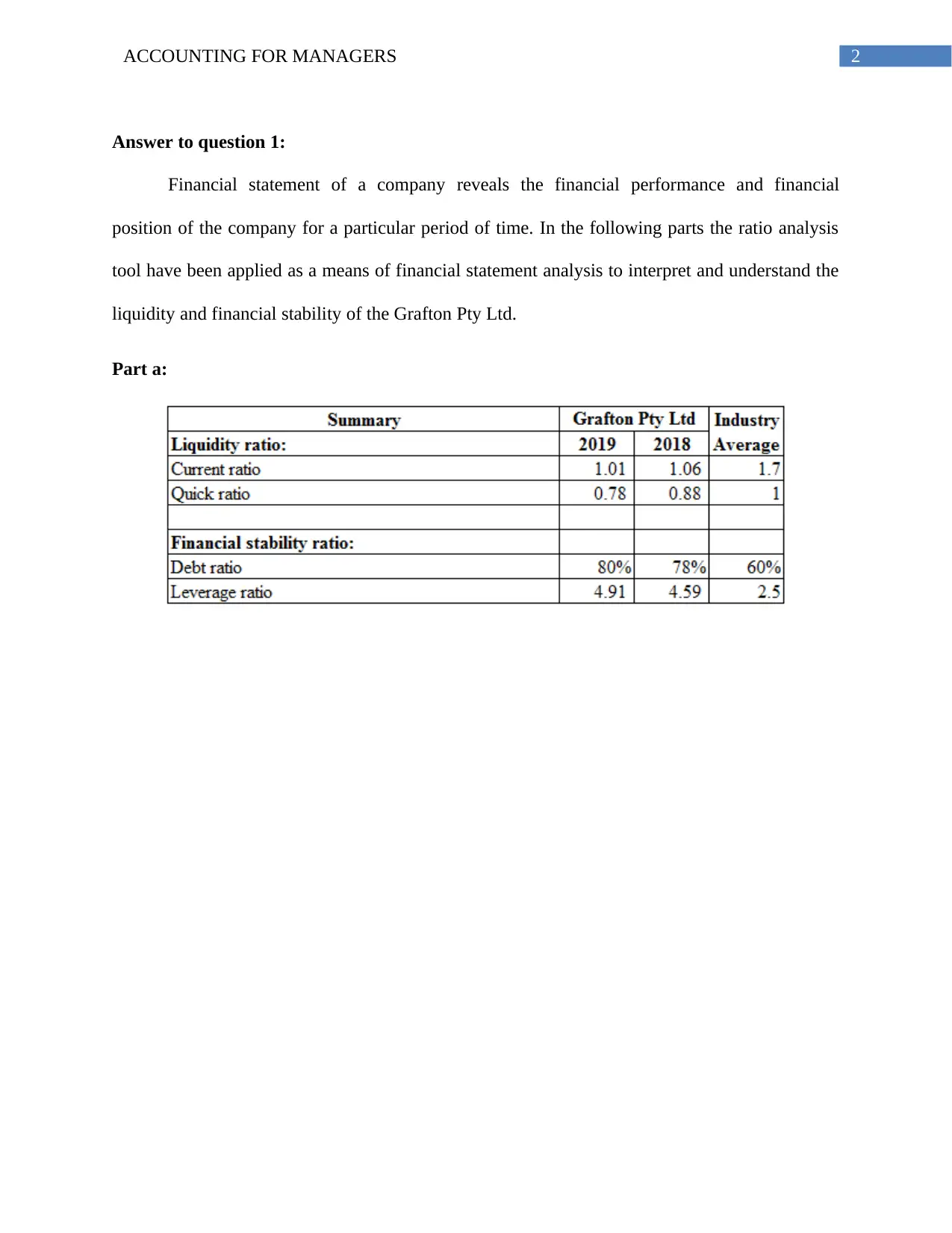

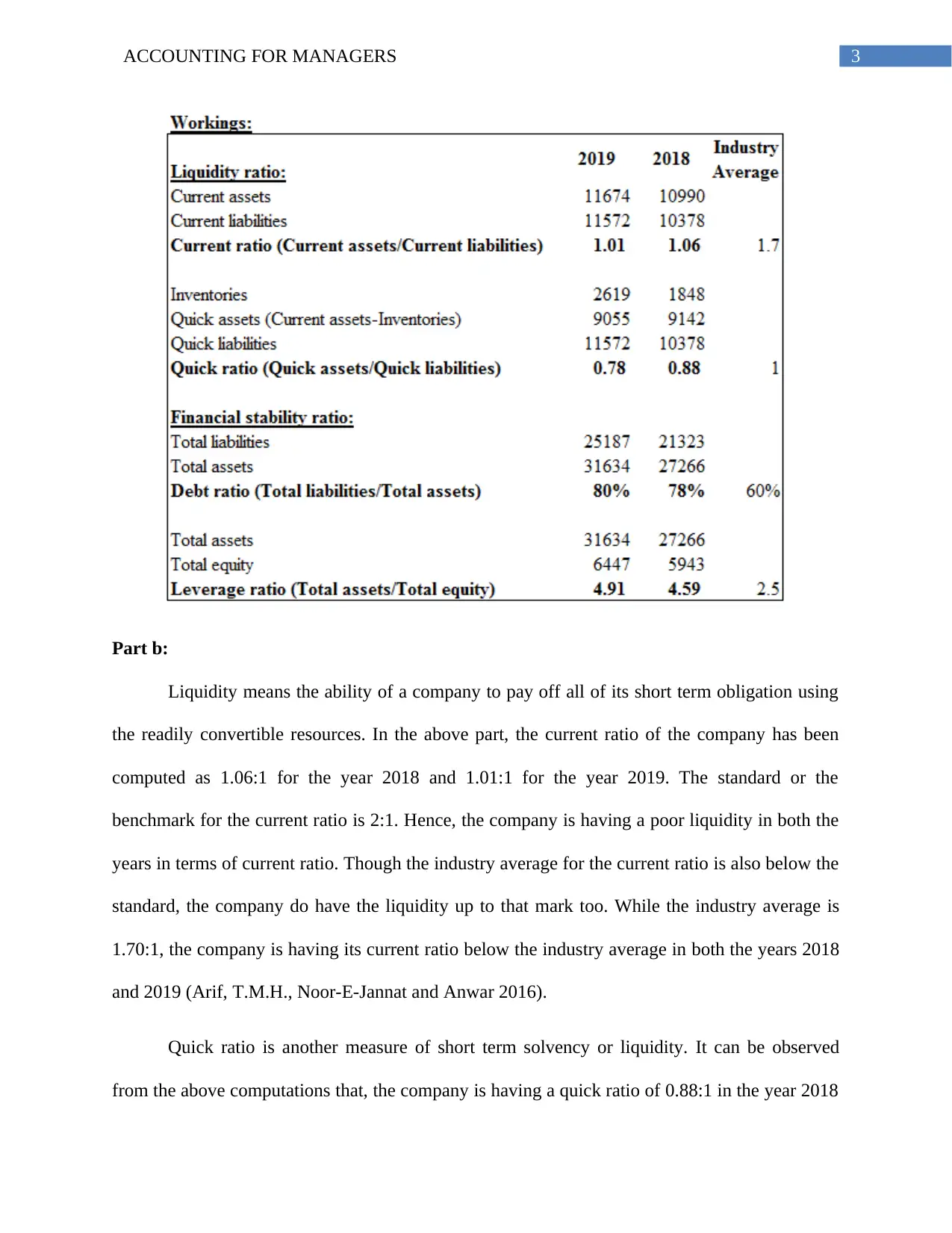

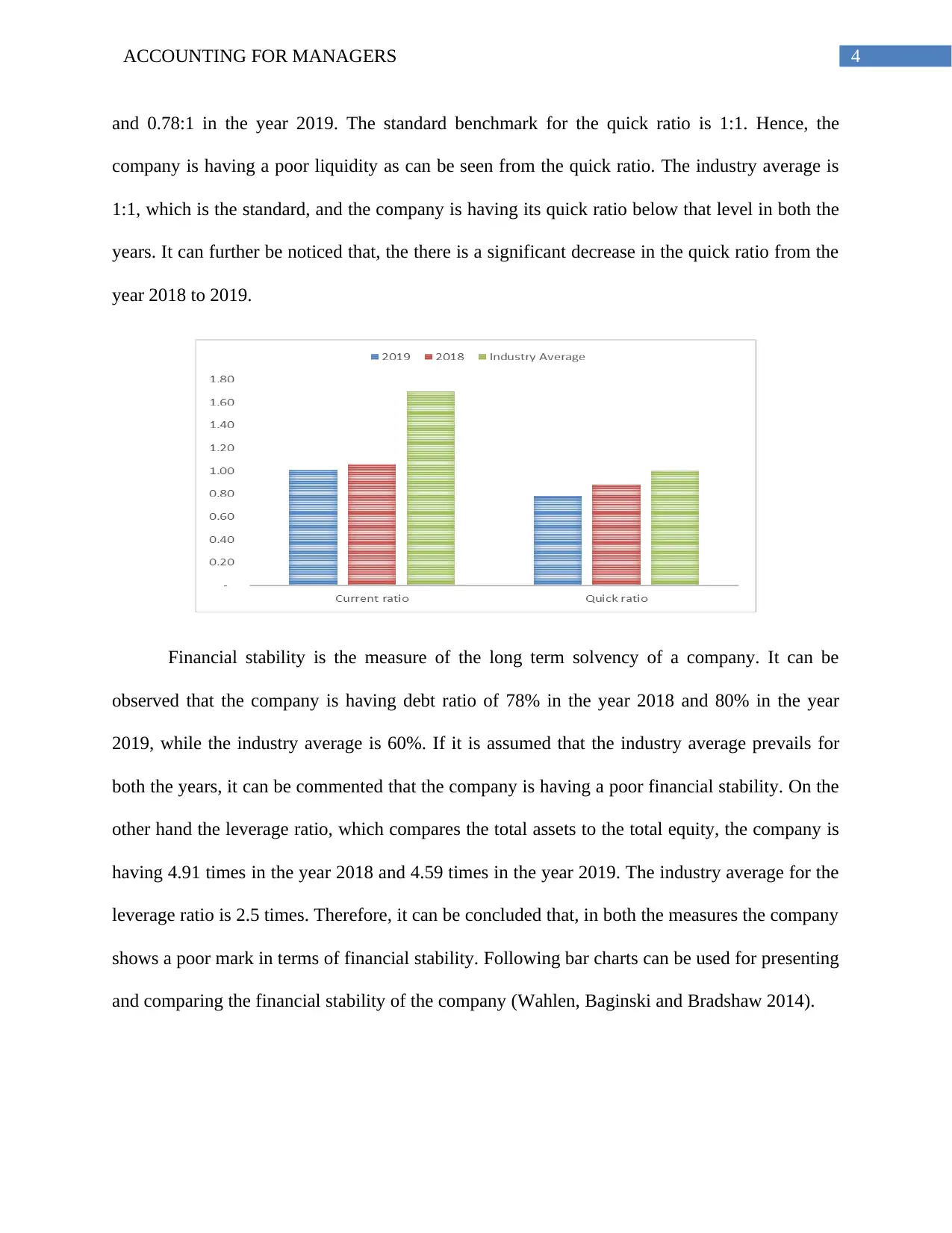

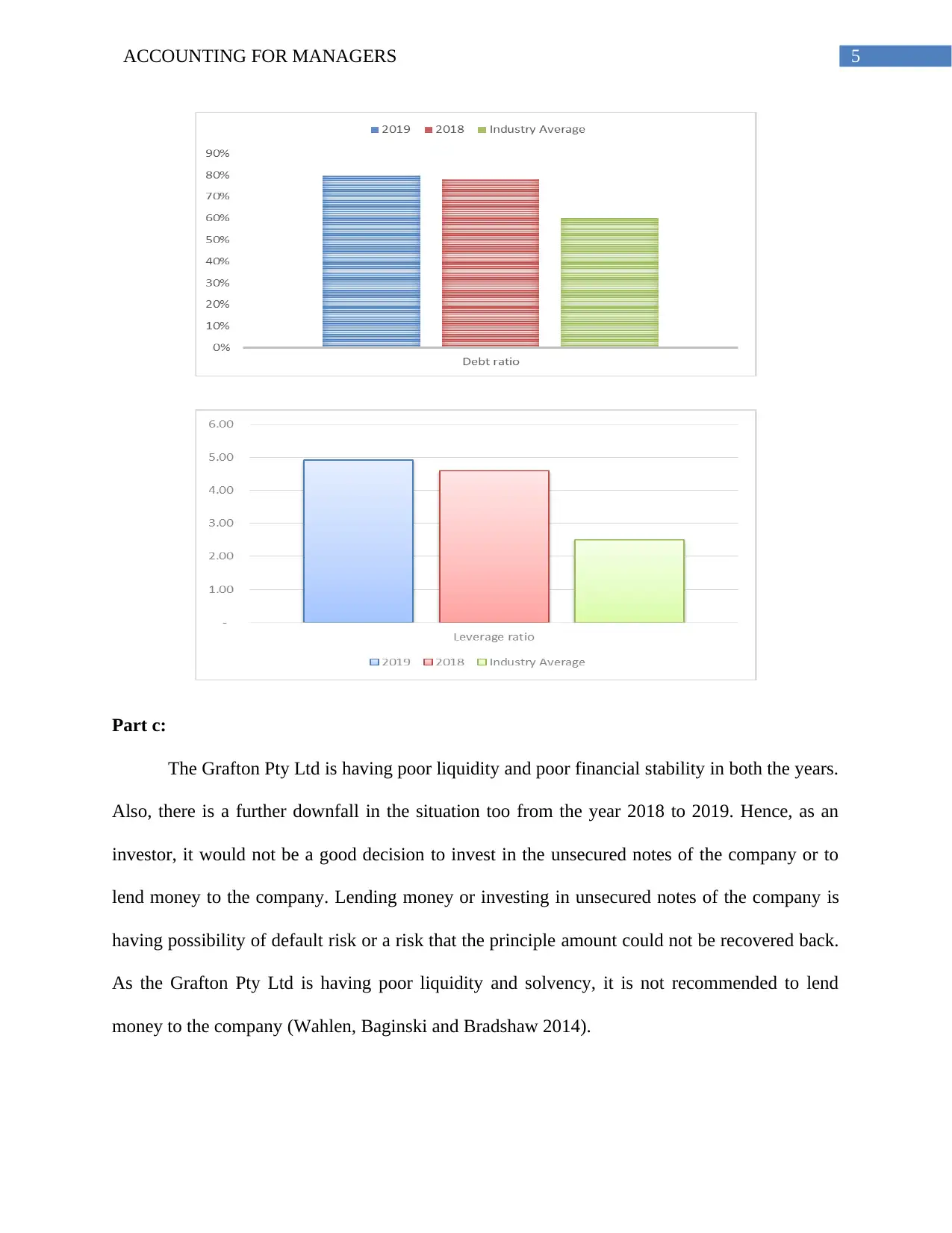

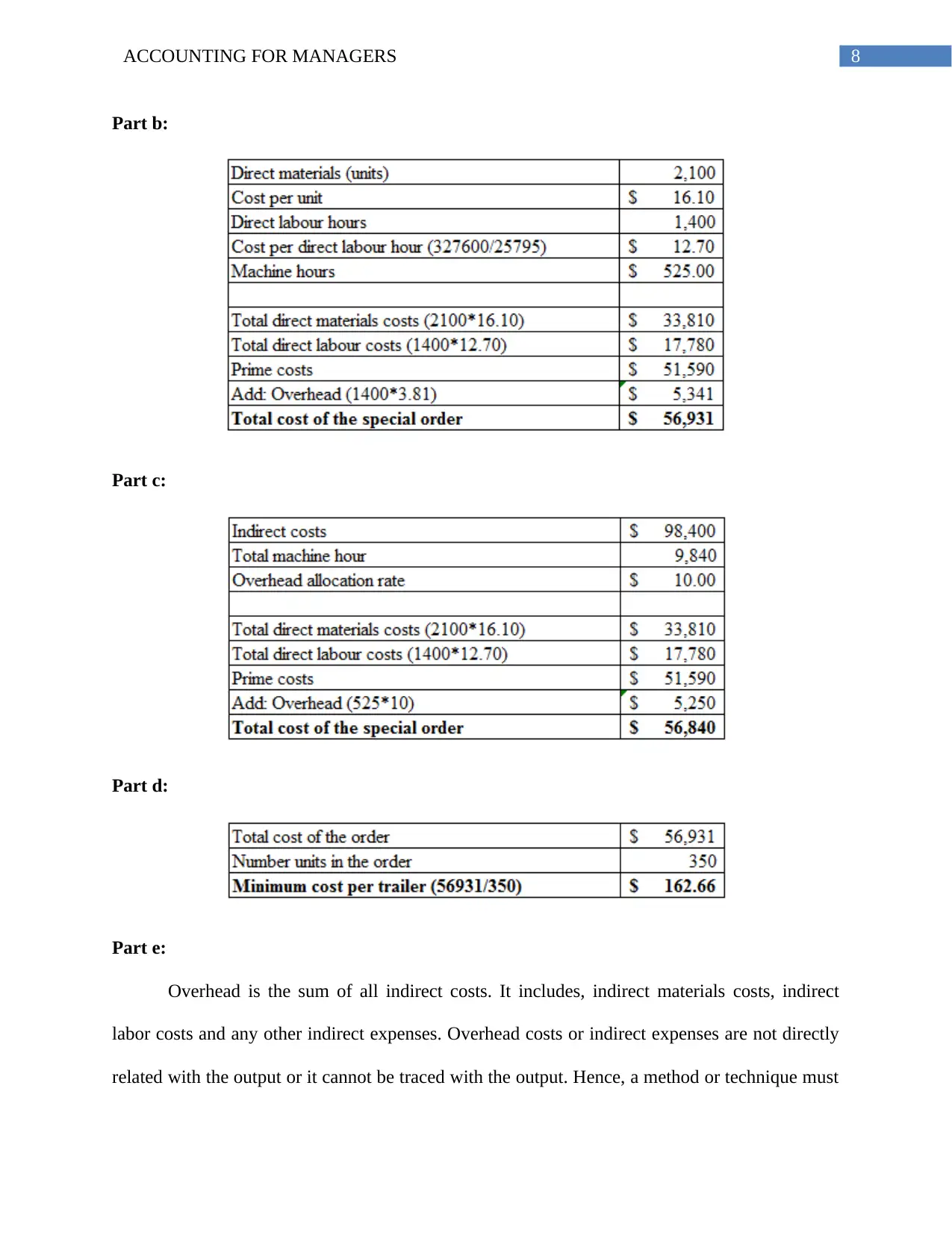

This assignment provides a comprehensive analysis of financial statements, ratio analysis, and managerial accounting principles. The solution begins with an examination of Grafton Pty Ltd's financial performance, including liquidity and financial stability, using ratio analysis to assess its current and quick ratios, debt ratio, and leverage ratio. The analysis offers insights into the company's financial health and provides investment recommendations. The assignment then delves into profitability analysis, comparing marketing strategies proposed by different managers at Dunning Ltd, evaluating their impact on profit and break-even points. Finally, the assignment explores overhead allocation methods, contrasting traditional and activity-based costing systems, highlighting the advantages and disadvantages of each approach. The solution provides a detailed explanation of these concepts with relevant calculations and interpretations.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.