MG5556 Financial Resources Management: Company Performance Analysis

VerifiedAdded on 2022/10/31

|21

|3412

|211

Report

AI Summary

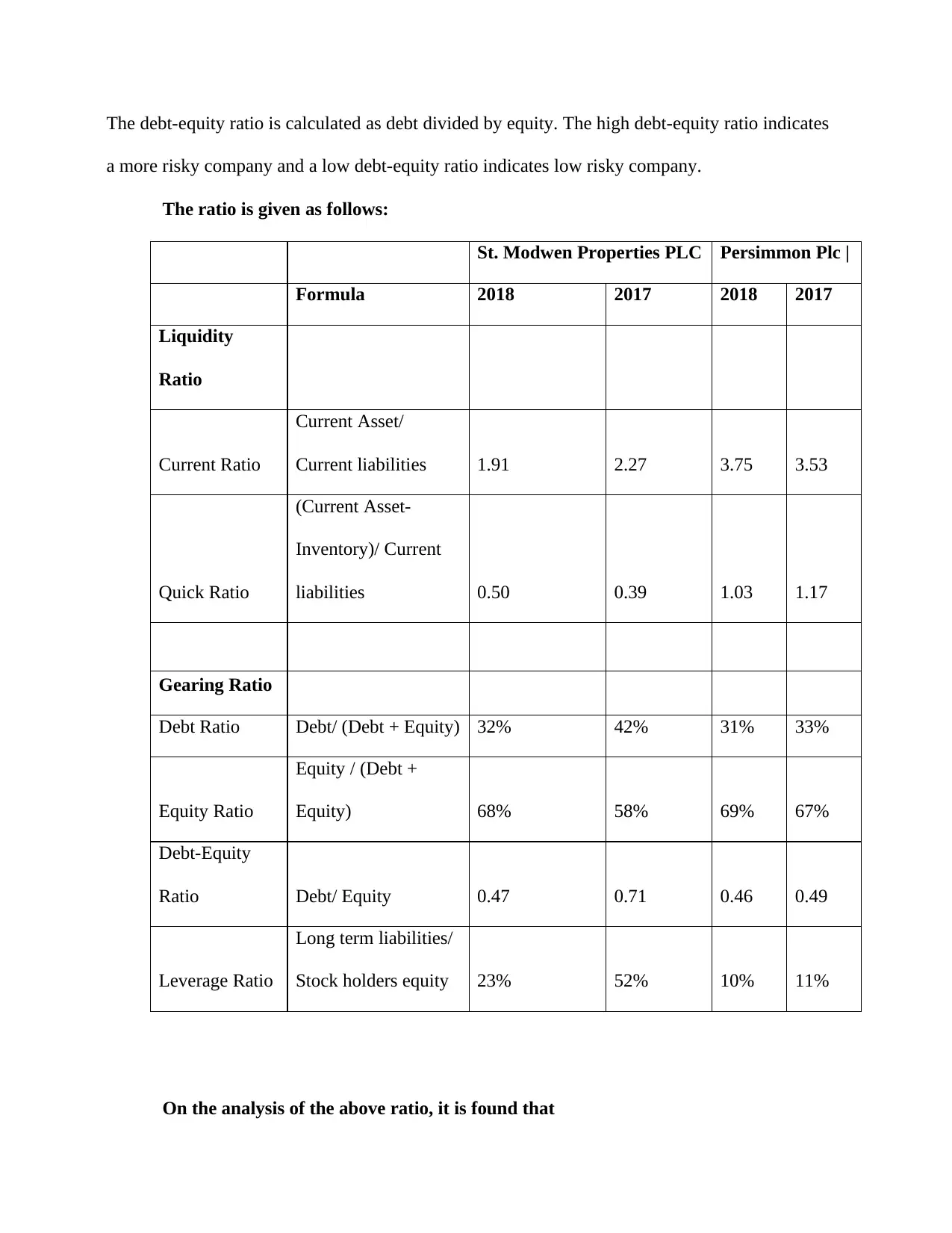

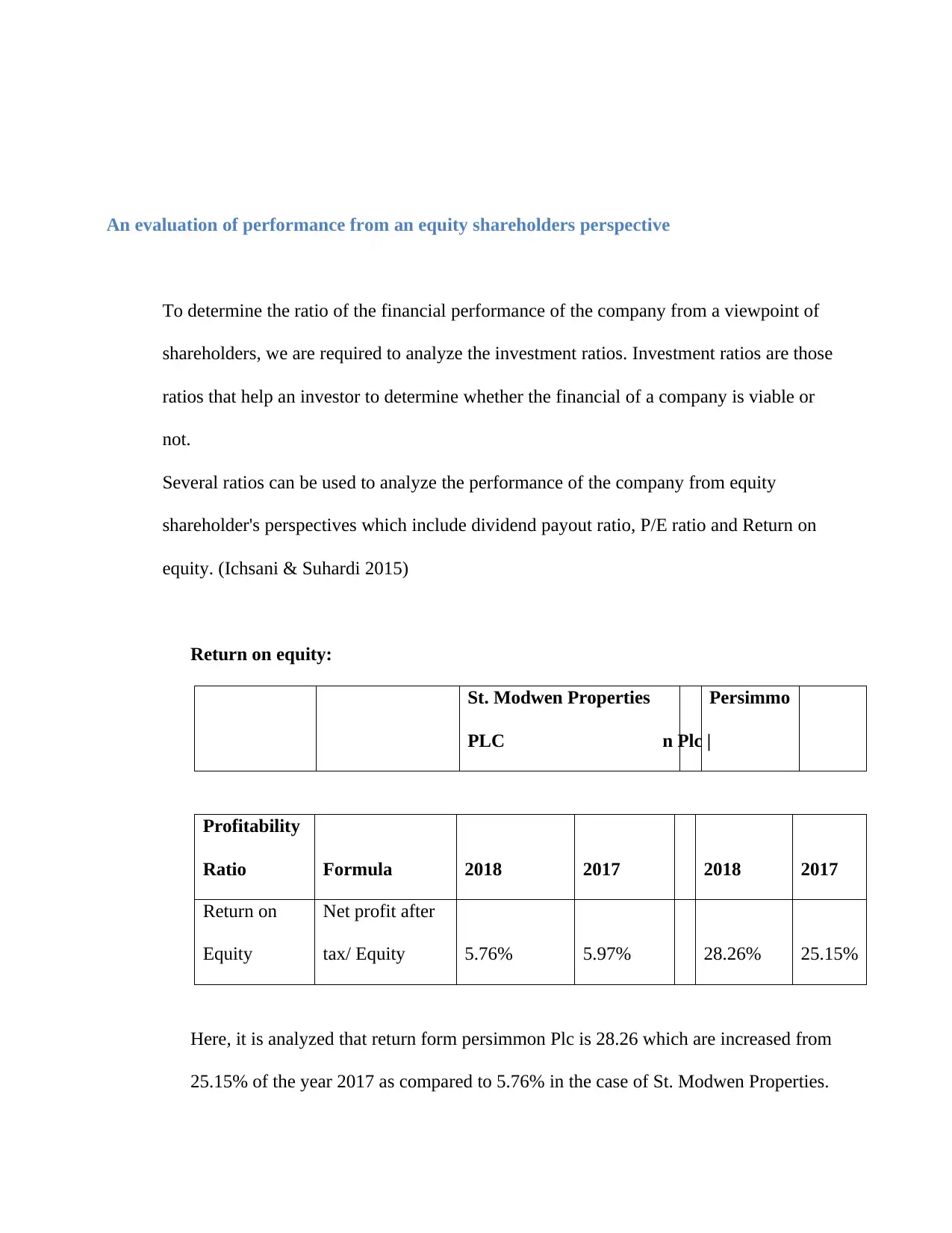

This report provides a comprehensive analysis of the financial performance and valuation of two UK-listed companies, Persimmon Plc and St. Modwen Properties Plc. The analysis begins with an executive summary and introduction, followed by a detailed examination of profitability ratios, including gross profit margin, net profit margin, return on equity, and return on assets. The report then assesses the financial position from both short-term (liquidity) and long-term (gearing) perspectives, utilizing ratios such as the current ratio, quick ratio, debt ratio, and debt-equity ratio. Furthermore, the report evaluates the companies' performance from an equity shareholder's perspective, focusing on return on equity. The study concludes with a comparative analysis of the overall performance and financial position of the businesses, recommending the more suitable company for investment based on the findings. Finally, the valuation of the company is done using the forecast dividend growth model.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.