Accounting and Finance Report: Case Studies and Financial Analysis

VerifiedAdded on 2021/05/31

|12

|1670

|20

Report

AI Summary

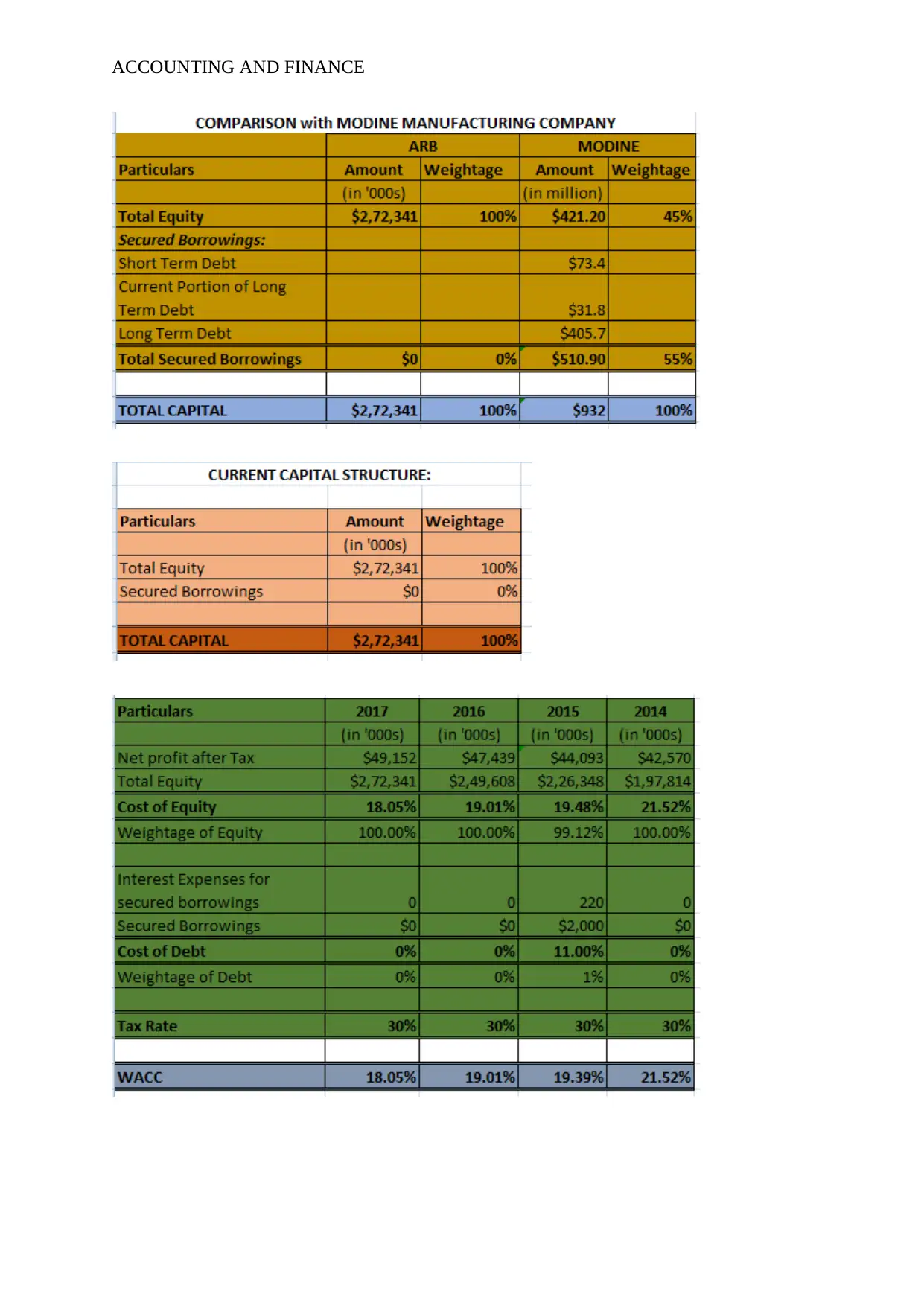

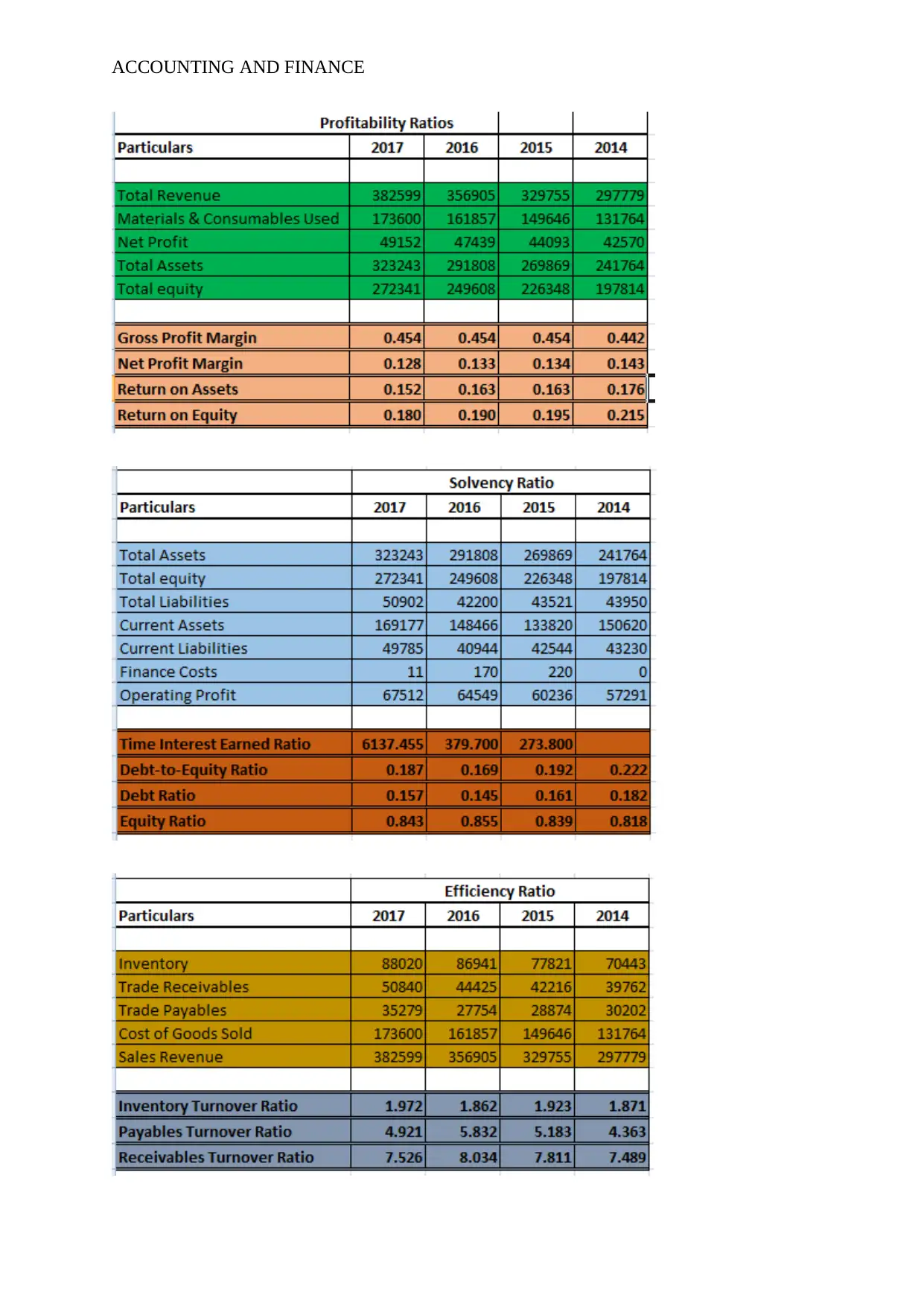

This report presents a comprehensive analysis of accounting and finance principles through two distinct case studies. Part A focuses on Saturn Pet Care, evaluating two projects using capital budgeting techniques such as Net Present Value (NPV), Profitability Index, and Payback Period. It explores product cannibalization and addresses the impact of estimated sales errors and the valuation of a vacant factory. Part B shifts to an evaluation of ARB Limited's financial performance, examining its capital structure, Weighted Average Cost of Capital (WACC), and the application of the Capital Asset Pricing Model (CAPM) to determine the cost of equity. The report compares ARB Limited's capital structure to industry peers, analyzes key financial ratios (profitability, efficiency, and solvency), and identifies changes in capital structure over time. It concludes with recommendations to improve financial performance, focusing on cost reduction and capital structure optimization. The report utilizes financial ratios, capital budgeting tools, and comparative analysis to provide a detailed assessment of the companies' financial positions and strategic decisions.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.