Analysis of Costing, Budgeting, and Financial Performance Metrics

VerifiedAdded on 2023/06/15

|12

|2666

|90

Report

AI Summary

This assignment solution covers key aspects of managing financial resources, including cost sheet calculations, variance analysis, and performance metrics. The cost sheet details prime cost, production cost, and other costs related to sales, distribution, and administration. Variance analysis explains adverse and favorable variances with real-world examples from companies like Tesco and Morrison. The report also discusses flexible budgets and direct labor variance. Furthermore, it explains and illustrates performance metrics such as Average Daily Rate (ADR), Revenue per Available Room (RevPAR), Average Rate Index (ARI), Market Penetration Index (MPI), and Average Length of Stay (ALOS) with examples from the hospitality industry, particularly Premier Inn hotel. Desklib offers this solved assignment and many other resources to support students in their studies.

MANAGING FINANCIAL

RESOURCES

RESOURCES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

SECTION A.....................................................................................................................................3

Question 1....................................................................................................................................3

SECTION B.....................................................................................................................................5

Question 4....................................................................................................................................5

Question 5....................................................................................................................................7

REFERENCES................................................................................................................................1

SECTION A.....................................................................................................................................3

Question 1....................................................................................................................................3

SECTION B.....................................................................................................................................5

Question 4....................................................................................................................................5

Question 5....................................................................................................................................7

REFERENCES................................................................................................................................1

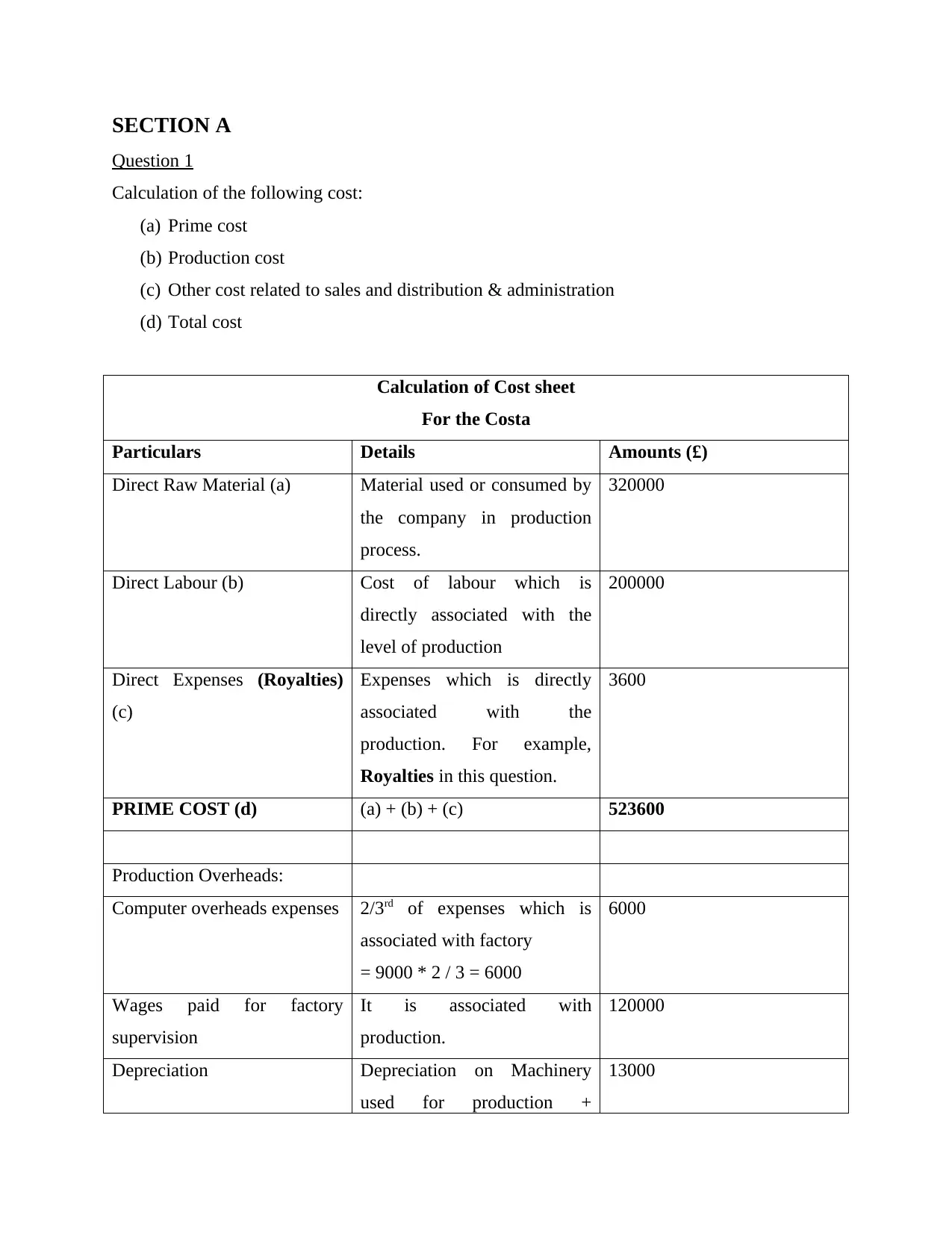

SECTION A

Question 1

Calculation of the following cost:

(a) Prime cost

(b) Production cost

(c) Other cost related to sales and distribution & administration

(d) Total cost

Calculation of Cost sheet

For the Costa

Particulars Details Amounts (£)

Direct Raw Material (a) Material used or consumed by

the company in production

process.

320000

Direct Labour (b) Cost of labour which is

directly associated with the

level of production

200000

Direct Expenses (Royalties)

(c)

Expenses which is directly

associated with the

production. For example,

Royalties in this question.

3600

PRIME COST (d) (a) + (b) + (c) 523600

Production Overheads:

Computer overheads expenses 2/3rd of expenses which is

associated with factory

= 9000 * 2 / 3 = 6000

6000

Wages paid for factory

supervision

It is associated with

production.

120000

Depreciation Depreciation on Machinery

used for production +

13000

Question 1

Calculation of the following cost:

(a) Prime cost

(b) Production cost

(c) Other cost related to sales and distribution & administration

(d) Total cost

Calculation of Cost sheet

For the Costa

Particulars Details Amounts (£)

Direct Raw Material (a) Material used or consumed by

the company in production

process.

320000

Direct Labour (b) Cost of labour which is

directly associated with the

level of production

200000

Direct Expenses (Royalties)

(c)

Expenses which is directly

associated with the

production. For example,

Royalties in this question.

3600

PRIME COST (d) (a) + (b) + (c) 523600

Production Overheads:

Computer overheads expenses 2/3rd of expenses which is

associated with factory

= 9000 * 2 / 3 = 6000

6000

Wages paid for factory

supervision

It is associated with

production.

120000

Depreciation Depreciation on Machinery

used for production +

13000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

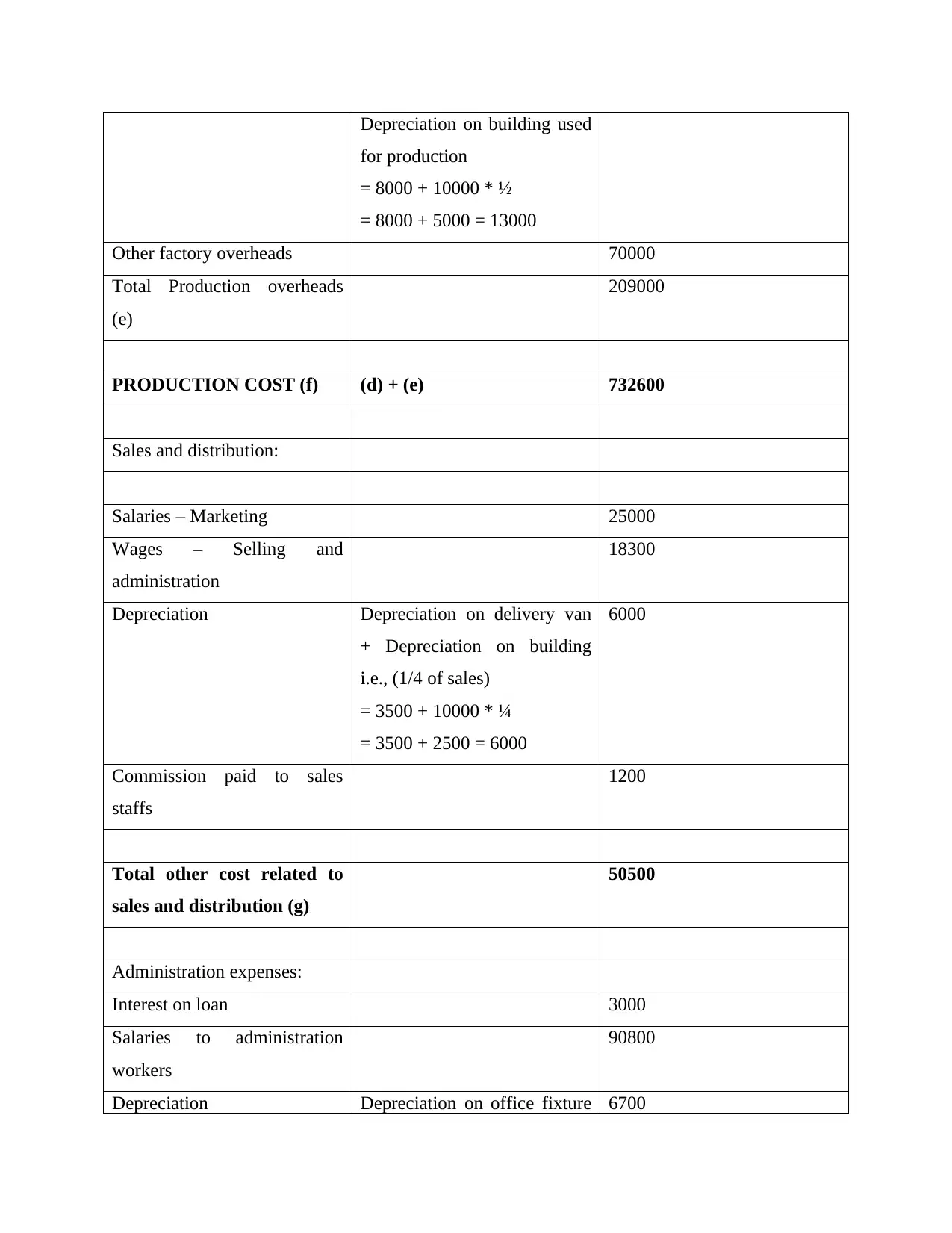

Depreciation on building used

for production

= 8000 + 10000 * ½

= 8000 + 5000 = 13000

Other factory overheads 70000

Total Production overheads

(e)

209000

PRODUCTION COST (f) (d) + (e) 732600

Sales and distribution:

Salaries – Marketing 25000

Wages – Selling and

administration

18300

Depreciation Depreciation on delivery van

+ Depreciation on building

i.e., (1/4 of sales)

= 3500 + 10000 * ¼

= 3500 + 2500 = 6000

6000

Commission paid to sales

staffs

1200

Total other cost related to

sales and distribution (g)

50500

Administration expenses:

Interest on loan 3000

Salaries to administration

workers

90800

Depreciation Depreciation on office fixture 6700

for production

= 8000 + 10000 * ½

= 8000 + 5000 = 13000

Other factory overheads 70000

Total Production overheads

(e)

209000

PRODUCTION COST (f) (d) + (e) 732600

Sales and distribution:

Salaries – Marketing 25000

Wages – Selling and

administration

18300

Depreciation Depreciation on delivery van

+ Depreciation on building

i.e., (1/4 of sales)

= 3500 + 10000 * ¼

= 3500 + 2500 = 6000

6000

Commission paid to sales

staffs

1200

Total other cost related to

sales and distribution (g)

50500

Administration expenses:

Interest on loan 3000

Salaries to administration

workers

90800

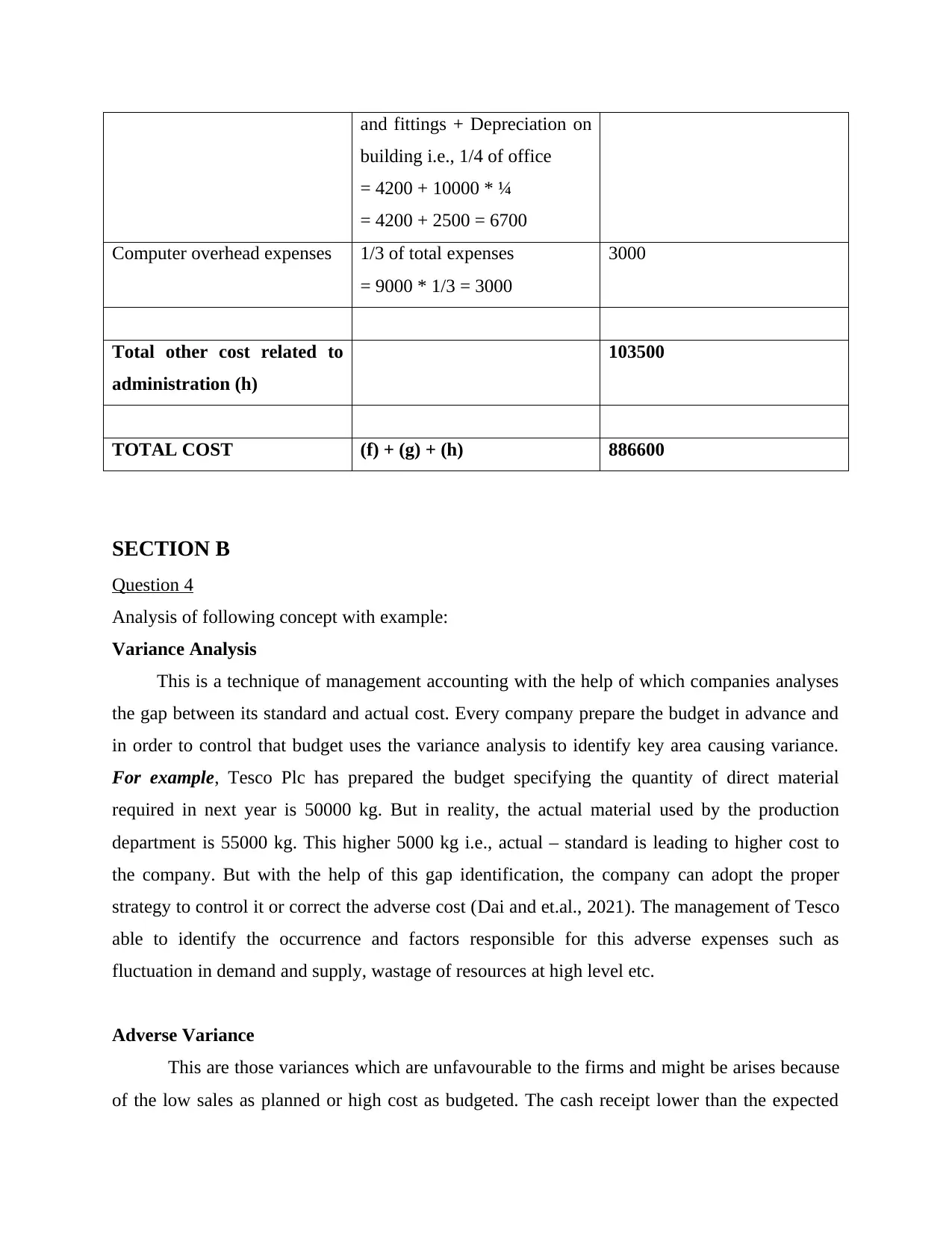

Depreciation Depreciation on office fixture 6700

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and fittings + Depreciation on

building i.e., 1/4 of office

= 4200 + 10000 * ¼

= 4200 + 2500 = 6700

Computer overhead expenses 1/3 of total expenses

= 9000 * 1/3 = 3000

3000

Total other cost related to

administration (h)

103500

TOTAL COST (f) + (g) + (h) 886600

SECTION B

Question 4

Analysis of following concept with example:

Variance Analysis

This is a technique of management accounting with the help of which companies analyses

the gap between its standard and actual cost. Every company prepare the budget in advance and

in order to control that budget uses the variance analysis to identify key area causing variance.

For example, Tesco Plc has prepared the budget specifying the quantity of direct material

required in next year is 50000 kg. But in reality, the actual material used by the production

department is 55000 kg. This higher 5000 kg i.e., actual – standard is leading to higher cost to

the company. But with the help of this gap identification, the company can adopt the proper

strategy to control it or correct the adverse cost (Dai and et.al., 2021). The management of Tesco

able to identify the occurrence and factors responsible for this adverse expenses such as

fluctuation in demand and supply, wastage of resources at high level etc.

Adverse Variance

This are those variances which are unfavourable to the firms and might be arises because

of the low sales as planned or high cost as budgeted. The cash receipt lower than the expected

building i.e., 1/4 of office

= 4200 + 10000 * ¼

= 4200 + 2500 = 6700

Computer overhead expenses 1/3 of total expenses

= 9000 * 1/3 = 3000

3000

Total other cost related to

administration (h)

103500

TOTAL COST (f) + (g) + (h) 886600

SECTION B

Question 4

Analysis of following concept with example:

Variance Analysis

This is a technique of management accounting with the help of which companies analyses

the gap between its standard and actual cost. Every company prepare the budget in advance and

in order to control that budget uses the variance analysis to identify key area causing variance.

For example, Tesco Plc has prepared the budget specifying the quantity of direct material

required in next year is 50000 kg. But in reality, the actual material used by the production

department is 55000 kg. This higher 5000 kg i.e., actual – standard is leading to higher cost to

the company. But with the help of this gap identification, the company can adopt the proper

strategy to control it or correct the adverse cost (Dai and et.al., 2021). The management of Tesco

able to identify the occurrence and factors responsible for this adverse expenses such as

fluctuation in demand and supply, wastage of resources at high level etc.

Adverse Variance

This are those variances which are unfavourable to the firms and might be arises because

of the low sales as planned or high cost as budgeted. The cash receipt lower than the expected

and high payments more than the forecasted is also one of the reason behind the adverse

variance. The real life example of adverse variance is as follows: Morrison is a UK based retail

company that projected that in the year 2021 they will make a total sale of £200000 but in actual

they have only generated £170000 from the sales. This will cause them unfavourable and adverse

variance of £30000 i.e., £170000 - £200000. Another example of adverse variance is that the

company expected the total cost of production in the same year will be only £120000 but in

reality the company actual cost is £140000 which means an increase in the cost by £20000. This

is known an adverse variance or gap (Salles, Rocha and Goncalves, 2021).

Favourable Variance

Favourable variance is just opposite of adverse variance in which the actual income of the

company is higher than the standard one and actual expenses of the company is lower than the

projected expense. With the help of this positive results, the company and its staffs get the

motivation towards their work. For example, Eagle eye is a technology company which prepare

flexible budget every year and expect the next year expenses. The total expenses they are

expecting in the next year from its business is around £100000 but in actual they only incur

£75000. This means that actual – expected = £100000 - £75000 = £25000 favourable is a surplus

for the company which helps them in further expansion of the business (da Silva Alves and da

Rocha, 2021). Thus, every company have to use the variance analysis as a budgetary control

technique.

Flexible Budget

The flexible budgets are the budgets which is prepare by the company along with the

proper adjustment as per change in the level of activity. The flexible budget is totally different

from the static or fixed budget because it gets change over the period of time with the change in

the business internal and external environment. In order to prepare the flexible budget, the

company first need to identify its fixed and variable cost. It is because variable cost changes in

flexible budget and fixed cost remain the same at all level of activity. For example, Mark and

Spenser company has a budgeted revenue of £10 million and the cost of goods sold is £5 million.

In this total cost of goods sold the variable cost is only £3 million which changes over the change

in sales revenue (Fenny and et.al., 2021).

variance. The real life example of adverse variance is as follows: Morrison is a UK based retail

company that projected that in the year 2021 they will make a total sale of £200000 but in actual

they have only generated £170000 from the sales. This will cause them unfavourable and adverse

variance of £30000 i.e., £170000 - £200000. Another example of adverse variance is that the

company expected the total cost of production in the same year will be only £120000 but in

reality the company actual cost is £140000 which means an increase in the cost by £20000. This

is known an adverse variance or gap (Salles, Rocha and Goncalves, 2021).

Favourable Variance

Favourable variance is just opposite of adverse variance in which the actual income of the

company is higher than the standard one and actual expenses of the company is lower than the

projected expense. With the help of this positive results, the company and its staffs get the

motivation towards their work. For example, Eagle eye is a technology company which prepare

flexible budget every year and expect the next year expenses. The total expenses they are

expecting in the next year from its business is around £100000 but in actual they only incur

£75000. This means that actual – expected = £100000 - £75000 = £25000 favourable is a surplus

for the company which helps them in further expansion of the business (da Silva Alves and da

Rocha, 2021). Thus, every company have to use the variance analysis as a budgetary control

technique.

Flexible Budget

The flexible budgets are the budgets which is prepare by the company along with the

proper adjustment as per change in the level of activity. The flexible budget is totally different

from the static or fixed budget because it gets change over the period of time with the change in

the business internal and external environment. In order to prepare the flexible budget, the

company first need to identify its fixed and variable cost. It is because variable cost changes in

flexible budget and fixed cost remain the same at all level of activity. For example, Mark and

Spenser company has a budgeted revenue of £10 million and the cost of goods sold is £5 million.

In this total cost of goods sold the variable cost is only £3 million which changes over the change

in sales revenue (Fenny and et.al., 2021).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

But the remaining of £2 million does not changes because this are fixed in nature. In this

way, the company able to manage and control its budgets and enjoy the higher revenue and

profitability. The benefit of flexible budget to the M&S company is that it helps the manager to

pursue the new opportunities and mitigate the risk. In simple term, the flexible budget reflects

the state of finance more accurately.

Direct Labour Variance

This is a type of variance with the help of which the company can identify the gap

between the standard and actual direct labour cost. Formula of calculating the direct labour

variance is = (standard hours * standard rate) – (actual hours * actual rate). For example, Tesco

company has the following information regarding its direct labour and that they expected

standard hours require for 1 unit is 3 hours and actual hours the company worker takes is 200

hours for the total production of 50 units (Fernando, Samita and Peiris, 2021). The standard rate

of direct labour per hour is £20 and actual is £15 so the direct labour variance is as follows:

(50 * 3 * 20) – (200 * 16) = £200 adverse.

This means that the actual direct labour cost incurred by company is higher than the

expected one which need to be reduce. It might be because of the laziness of the worker and for

improving it the company have to motivate its employees.

Question 5

Explanation of the following using the formula and example:

Average Daily Rate (ADR)

This is basically a metric which is largely and widely used by the hospitality industry in

order to calculate the average revenue earned from an occupied room in a day. With the help of

this measure, the hotel and other loading company determine their operating performance and

make decision accordingly.

Formula of average daily rate = Rooms revenue earned / Number of rooms sold

way, the company able to manage and control its budgets and enjoy the higher revenue and

profitability. The benefit of flexible budget to the M&S company is that it helps the manager to

pursue the new opportunities and mitigate the risk. In simple term, the flexible budget reflects

the state of finance more accurately.

Direct Labour Variance

This is a type of variance with the help of which the company can identify the gap

between the standard and actual direct labour cost. Formula of calculating the direct labour

variance is = (standard hours * standard rate) – (actual hours * actual rate). For example, Tesco

company has the following information regarding its direct labour and that they expected

standard hours require for 1 unit is 3 hours and actual hours the company worker takes is 200

hours for the total production of 50 units (Fernando, Samita and Peiris, 2021). The standard rate

of direct labour per hour is £20 and actual is £15 so the direct labour variance is as follows:

(50 * 3 * 20) – (200 * 16) = £200 adverse.

This means that the actual direct labour cost incurred by company is higher than the

expected one which need to be reduce. It might be because of the laziness of the worker and for

improving it the company have to motivate its employees.

Question 5

Explanation of the following using the formula and example:

Average Daily Rate (ADR)

This is basically a metric which is largely and widely used by the hospitality industry in

order to calculate the average revenue earned from an occupied room in a day. With the help of

this measure, the hotel and other loading company determine their operating performance and

make decision accordingly.

Formula of average daily rate = Rooms revenue earned / Number of rooms sold

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Example: Premier Inn hotel of UK has around 72000 rooms in their total 800 hotels and the total

amount of revenue the company earn from its 800 hotel is £1440000. So, the average daily rates

of Premier Inn hotel are £1440000 / 72000 rooms = 20 per room

But on the other side, it is also noted that company does not consider the complimentary

rooms and rooms occupied by staff in the calculation of ADR. The benefit, the company are

enjoying with this measure is that its reduces their stress level and they able to increase the

money. In case if ADR is high, the company get to know that they are moving on a right track

(Rovella, 2017).

Revenue per available room (RevPAR)

This is another measure which help the hospitality sector companies in identifying the

revenue generated per available room. This helps them in measuring their revenue generation

performance.

Formula of revenue per available room = Average daily room rates * occupancy rate

The occupancy rate represents the rate of the rooms which are occupied by the customers.

Example; In the above case, the average daily rate of Premier Inn hotel is £20 per room from

total 72000 rooms. But the occupancy rate of the rooms is only 80% than the revenue per

available room is as follows:

£20 * 80% = £16 per room

So, on this basis it can be said that the total revenue Premier Inn hotel generated from its

one available room is £16. It is benefit for the company to use this measure also along with the

ADR measure because it provides more accurate result (Kuang, 2021). It is not possible that all

the time, all the rooms of the hotel is occupied by someone. So, it is important for company to

keep in mind this fact.

Average Rate Index (ARI)

This measure helps the hospitality industry and companies in identifying their own

average daily rate as compared with the competitors ADR. With the help of this, the company

such as hotels can determine whether they can exist or raise in the competitive market or not.

Formula of average rate index = Own ADR / Competitors average ADR

amount of revenue the company earn from its 800 hotel is £1440000. So, the average daily rates

of Premier Inn hotel are £1440000 / 72000 rooms = 20 per room

But on the other side, it is also noted that company does not consider the complimentary

rooms and rooms occupied by staff in the calculation of ADR. The benefit, the company are

enjoying with this measure is that its reduces their stress level and they able to increase the

money. In case if ADR is high, the company get to know that they are moving on a right track

(Rovella, 2017).

Revenue per available room (RevPAR)

This is another measure which help the hospitality sector companies in identifying the

revenue generated per available room. This helps them in measuring their revenue generation

performance.

Formula of revenue per available room = Average daily room rates * occupancy rate

The occupancy rate represents the rate of the rooms which are occupied by the customers.

Example; In the above case, the average daily rate of Premier Inn hotel is £20 per room from

total 72000 rooms. But the occupancy rate of the rooms is only 80% than the revenue per

available room is as follows:

£20 * 80% = £16 per room

So, on this basis it can be said that the total revenue Premier Inn hotel generated from its

one available room is £16. It is benefit for the company to use this measure also along with the

ADR measure because it provides more accurate result (Kuang, 2021). It is not possible that all

the time, all the rooms of the hotel is occupied by someone. So, it is important for company to

keep in mind this fact.

Average Rate Index (ARI)

This measure helps the hospitality industry and companies in identifying their own

average daily rate as compared with the competitors ADR. With the help of this, the company

such as hotels can determine whether they can exist or raise in the competitive market or not.

Formula of average rate index = Own ADR / Competitors average ADR

Example; Premier Inn is the largest brand of UK and its main or closet competitor is Gloria hotel

and resort. From the above calculation, it is identified that average daily rate of Premier Inn is

£20, while from the research it is identified that the ADR of Gloria hotel and resort is £15. So, on

this basis the ARI is as follows:

= £20 / £25 = 0.8

On this basis, it is identified that the price of the Premier Inn hotel is lower as compared

to its competitor (Murimi, Wadongo and Olielo, 2021). So, in order to improve it the company

need to increase their marketing for increasing bookings, attracting lower occupancy but on the

same side higher revenue in order to exist in the market.

Market Penetration Index (MPI)

This is also known as occupancy index with the help of which hospitality companies

measure its performance with the aggregate grouping of hotels. The higher MPI i.e., more than

100 is denote that the company’s occupancy performance is better than the aggregate number of

hotels (Caley and et.al., 2021). The occupancy is computed using the formula of rooms sold

divided by rooms available.

Formula of MPI = Subject hotel occupancy rate / aggregate group of hotels occupancy rate * 100

For example, Premier Inn has the occupancy rate of 80% and the aggregate group of hotels

occupancy rate is 70% than MPI is as follows:

= 80 / 70 * 100 = 114 which is more than 100.

So, on this basis it can be said that the overall occupancy performance of Premier Inn

hotel as compared to its aggregate other hotels is high and best. It is because Premier Inn hotel

has captured more than its expected shares.

Average Length of Stay (ALOS)

This is also one of the best measure which is used by hospitality industry in order to

identify the average number of days the tourist or other people spend in the hotels.

Formula = Total room nights / number of reservation checked in

For example, Premier Inn hotel had around 5 guest within a certain period and that five guest

spent 6, 4, 5, 3, 7 days respectively at hotel. So, the average length of stay of 5 guest at Premier

Inn hotel are as follows:

and resort. From the above calculation, it is identified that average daily rate of Premier Inn is

£20, while from the research it is identified that the ADR of Gloria hotel and resort is £15. So, on

this basis the ARI is as follows:

= £20 / £25 = 0.8

On this basis, it is identified that the price of the Premier Inn hotel is lower as compared

to its competitor (Murimi, Wadongo and Olielo, 2021). So, in order to improve it the company

need to increase their marketing for increasing bookings, attracting lower occupancy but on the

same side higher revenue in order to exist in the market.

Market Penetration Index (MPI)

This is also known as occupancy index with the help of which hospitality companies

measure its performance with the aggregate grouping of hotels. The higher MPI i.e., more than

100 is denote that the company’s occupancy performance is better than the aggregate number of

hotels (Caley and et.al., 2021). The occupancy is computed using the formula of rooms sold

divided by rooms available.

Formula of MPI = Subject hotel occupancy rate / aggregate group of hotels occupancy rate * 100

For example, Premier Inn has the occupancy rate of 80% and the aggregate group of hotels

occupancy rate is 70% than MPI is as follows:

= 80 / 70 * 100 = 114 which is more than 100.

So, on this basis it can be said that the overall occupancy performance of Premier Inn

hotel as compared to its aggregate other hotels is high and best. It is because Premier Inn hotel

has captured more than its expected shares.

Average Length of Stay (ALOS)

This is also one of the best measure which is used by hospitality industry in order to

identify the average number of days the tourist or other people spend in the hotels.

Formula = Total room nights / number of reservation checked in

For example, Premier Inn hotel had around 5 guest within a certain period and that five guest

spent 6, 4, 5, 3, 7 days respectively at hotel. So, the average length of stay of 5 guest at Premier

Inn hotel are as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= 6 + 4 + 5 + 3 + 7 / 5 guest = 25 days / 5 = 5 days

On this basis, it is state that the average length of stay of a guest in Premier Inn hotel is 5

days (Hoang, 2021). It is because the time spent by each guest in the hotel was different as their

arrival date and departure date are different from each other.

On this basis, it is state that the average length of stay of a guest in Premier Inn hotel is 5

days (Hoang, 2021). It is because the time spent by each guest in the hotel was different as their

arrival date and departure date are different from each other.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Dai, M. and et.al., 2021. A dynamic mean-variance analysis for log returns. Management

Science. 67(2). pp.1093-1108.

Salles, T., Rocha, L. and Goncalves, M., 2021. A bias-variance analysis of state-of-the-art

random forest text classifiers. Advances in Data Analysis and Classification. 15(2).

pp.379-405.

da Silva Alves, L. A. and da Rocha, C. H. M., 2021. The Strategic Variance Analysis of LAN

and TAM airlines merger in the early 2010’s. Transportation Research Procedia. 58.

pp.503-510.

Fernando, D. R., Samita, S. and Peiris, T. U. S., 2021. Identifying Panel Inconsistency in

Sensory Profiles using Multivariate Analysis of Variance (MANOVA) and follow–up

Canonical Variate Analysis (CVA). Tropical Agricultural Research. 33(1).

Rovella, A., 2017. SIGLA: a flexible, portable and reusable ERP System for Research

Management.

Kuang, W., 2021. Conditional covariance matrix forecast using the hybrid exponentially

weighted moving average approach. Journal of Forecasting.

Murimi, M., Wadongo, B. and Olielo, T., 2021. Determinants of revenue management practices

and their impacts on the financial performance of hotels in Kenya: a proposed theoretical

framework. Future Business Journal. 7(1). pp.1-7.

Caley, L. and et.al., 2021. Average rate of lung function decline in adults with cystic fibrosis in

the United Kingdom: Data from the UK CF registry. Journal of Cystic Fibrosis. 20(1).

pp.86-90.

Hoang, A. D., 2021. Influence of culture on French sauna market penetration: case company:

Zenestar.

Fenny, A. P. and et.al., 2021. Costs and Extra Length of Stay because of Neonatal Bloodstream

Infection at a Teaching Hospital in Ghana. PharmacoEconomics-Open. 5(1). pp.111-120.

1

Books and journals

Dai, M. and et.al., 2021. A dynamic mean-variance analysis for log returns. Management

Science. 67(2). pp.1093-1108.

Salles, T., Rocha, L. and Goncalves, M., 2021. A bias-variance analysis of state-of-the-art

random forest text classifiers. Advances in Data Analysis and Classification. 15(2).

pp.379-405.

da Silva Alves, L. A. and da Rocha, C. H. M., 2021. The Strategic Variance Analysis of LAN

and TAM airlines merger in the early 2010’s. Transportation Research Procedia. 58.

pp.503-510.

Fernando, D. R., Samita, S. and Peiris, T. U. S., 2021. Identifying Panel Inconsistency in

Sensory Profiles using Multivariate Analysis of Variance (MANOVA) and follow–up

Canonical Variate Analysis (CVA). Tropical Agricultural Research. 33(1).

Rovella, A., 2017. SIGLA: a flexible, portable and reusable ERP System for Research

Management.

Kuang, W., 2021. Conditional covariance matrix forecast using the hybrid exponentially

weighted moving average approach. Journal of Forecasting.

Murimi, M., Wadongo, B. and Olielo, T., 2021. Determinants of revenue management practices

and their impacts on the financial performance of hotels in Kenya: a proposed theoretical

framework. Future Business Journal. 7(1). pp.1-7.

Caley, L. and et.al., 2021. Average rate of lung function decline in adults with cystic fibrosis in

the United Kingdom: Data from the UK CF registry. Journal of Cystic Fibrosis. 20(1).

pp.86-90.

Hoang, A. D., 2021. Influence of culture on French sauna market penetration: case company:

Zenestar.

Fenny, A. P. and et.al., 2021. Costs and Extra Length of Stay because of Neonatal Bloodstream

Infection at a Teaching Hospital in Ghana. PharmacoEconomics-Open. 5(1). pp.111-120.

1

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.