Applied Business Finance: Financial Statements & Ratio Analysis Report

VerifiedAdded on 2023/06/17

|13

|2728

|392

Report

AI Summary

This report provides an analysis of applied business finance, focusing on the meaning and significance of financial management, key financial statements, and ratio analysis. It includes an income statement and balance sheet created using Excel, along with calculations of profitability, liquidity, and efficiency ratios based on case study information. The report interprets these ratios, highlighting the company's ability to generate profits and manage its resources. It also describes how business structure can improve financial performance, emphasizing the importance of sales, resource utilization, and cash management strategies. The conclusion emphasizes that effective financial management is crucial for a successful firm, aiding in planning, organizing, and maximizing earnings.

Applied Business

Finance

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

SECTION 1......................................................................................................................................3

Determine the meaning of financial management and its significance..................................3

SECTION 2......................................................................................................................................4

Explain the key financial statements and how ratios are used in financial management.......4

SECTION 3......................................................................................................................................5

(ii) Income statement using Excel.......................................................................................6

(iii) Completed the Balance sheet using excel.......................................................................6

(iv) Using case study information, calculate the Profitability, Liquidity, and Efficiency ratios

based on the company's analysis results .................................................................................7

SECTION 4......................................................................................................................................9

Describe the business structure that is being used to improve financial performance, using

examples from the case study.................................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

APPENDIX....................................................................................................................................11

INTRODUCTION...........................................................................................................................3

SECTION 1......................................................................................................................................3

Determine the meaning of financial management and its significance..................................3

SECTION 2......................................................................................................................................4

Explain the key financial statements and how ratios are used in financial management.......4

SECTION 3......................................................................................................................................5

(ii) Income statement using Excel.......................................................................................6

(iii) Completed the Balance sheet using excel.......................................................................6

(iv) Using case study information, calculate the Profitability, Liquidity, and Efficiency ratios

based on the company's analysis results .................................................................................7

SECTION 4......................................................................................................................................9

Describe the business structure that is being used to improve financial performance, using

examples from the case study.................................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

APPENDIX....................................................................................................................................11

INTRODUCTION

Financial management can be described as the activity of organising and controlling a

company's financial activities in order to assist the organisation earn higher returns. It monitors

the company's performance and the effectiveness of the finance management team using a

variety of accounting statements and procedures (Fang and et. al., 2018). In this report, the

concept and importance of financial management, as well as numerous accounting statements

and ratio analysis is explained. The income statement in the appendix further discusses the

performance of an organisation on the basis of its profitability, liquidity, and efficiency.

SECTION 1

Determine the meaning of financial management and its significance.

Finance is the foundation of any company. It is required to keep the business running

smoothly and efficiently. Financial management refers to the part of an organisation that is

responsible for the planning, arranging, directing, and managing of financial activities. It aids in

addressing the needs of shareholders while also maximising the company's income, profit, and

growth.

Financial Management’s importance:

1. Profitability: It examines the firm's efficiency and growth, which will aid in growing

profitability and providing a long-term strategy for the company.

2. Financial Decisions: It aids in the making of crucial financial decisions inside the firm.

A poor decision can jeopardise the entire company. It informs us of the many dangers and

possibilities, as well as assisting us in determining the percentage of shareholder capital

and borrowed cash.

3. Fund Allocation: The profit can be allocated to the right distribution of monetary

resources and dividends. It improves the functional ratio, lowers the cost of capital, and

raises the firm's economic worth.

4. Capital structure formation: It must be developed in order to estimate the amount of

capital necessary. Every venture is reliant on the amount of capital a company has and

how much it needs to raise from outside sources (Haw and et. al., 2018).

Financial management can be described as the activity of organising and controlling a

company's financial activities in order to assist the organisation earn higher returns. It monitors

the company's performance and the effectiveness of the finance management team using a

variety of accounting statements and procedures (Fang and et. al., 2018). In this report, the

concept and importance of financial management, as well as numerous accounting statements

and ratio analysis is explained. The income statement in the appendix further discusses the

performance of an organisation on the basis of its profitability, liquidity, and efficiency.

SECTION 1

Determine the meaning of financial management and its significance.

Finance is the foundation of any company. It is required to keep the business running

smoothly and efficiently. Financial management refers to the part of an organisation that is

responsible for the planning, arranging, directing, and managing of financial activities. It aids in

addressing the needs of shareholders while also maximising the company's income, profit, and

growth.

Financial Management’s importance:

1. Profitability: It examines the firm's efficiency and growth, which will aid in growing

profitability and providing a long-term strategy for the company.

2. Financial Decisions: It aids in the making of crucial financial decisions inside the firm.

A poor decision can jeopardise the entire company. It informs us of the many dangers and

possibilities, as well as assisting us in determining the percentage of shareholder capital

and borrowed cash.

3. Fund Allocation: The profit can be allocated to the right distribution of monetary

resources and dividends. It improves the functional ratio, lowers the cost of capital, and

raises the firm's economic worth.

4. Capital structure formation: It must be developed in order to estimate the amount of

capital necessary. Every venture is reliant on the amount of capital a company has and

how much it needs to raise from outside sources (Haw and et. al., 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

5. Economic Stability: It gives the business a sense of security since it reflects a stable

financial structure. It can help the company gain more revenues by preventing degrading

activities.

SECTION 2

Explain the key financial statements and how ratios are used in financial management.

Financial Statements are the records that the corporation is required to keep. It depicts the

company's economic activity and status. Government officials, accountants, and firms audit these

both internally and externally to ensure the reliability and validity of the tax and for investment

considerations (Huang and et. al., 2018). The following are some of the most important financial

statements:

Balance Sheet: It shows the assets, liabilities, and shareholder equity of a company

throughout the course of a fiscal year. Both the asset and liability sections should be

equal; if they aren't, there is a problem with the transaction recording. It also displays the

current fiscal year's cash and bank balances.

Income Statement: It focuses on the company's revenues and expenses to determine the

profit, which is known as net income. It's kept in order to show how much money the

company makes. It is calculated by summing the revenue and subtracting the expenses

incurred throughout the fiscal year to arrive at the fiscal year's net profit or loss. It is split

into two sections. First, it calculates gross profit based on operating income and expenses.

The net profit is derived by subtracting non-operating expenses and adding non-operating

income.

Cash Flow Statements: It aids in determining the requirement for external funding. It

calculates the cash inflow and outflow for operating, investing, and financing activities.

The changes in current assets and current liabilities, as well as interest and tax payments,

are all part of operating activities. The purchase or sale of fixed assets, as well as any

payment related to the company's merger and acquisition, are all examples of investing

activities. The issuance of equity capital, debentures, loans, and dividend payments are all

examples of financing activities.

Ratios: These are used to assess the state of two or more financial statement parts. It

summarises the financial data seen in the financial statements. It assesses the company's financial

financial structure. It can help the company gain more revenues by preventing degrading

activities.

SECTION 2

Explain the key financial statements and how ratios are used in financial management.

Financial Statements are the records that the corporation is required to keep. It depicts the

company's economic activity and status. Government officials, accountants, and firms audit these

both internally and externally to ensure the reliability and validity of the tax and for investment

considerations (Huang and et. al., 2018). The following are some of the most important financial

statements:

Balance Sheet: It shows the assets, liabilities, and shareholder equity of a company

throughout the course of a fiscal year. Both the asset and liability sections should be

equal; if they aren't, there is a problem with the transaction recording. It also displays the

current fiscal year's cash and bank balances.

Income Statement: It focuses on the company's revenues and expenses to determine the

profit, which is known as net income. It's kept in order to show how much money the

company makes. It is calculated by summing the revenue and subtracting the expenses

incurred throughout the fiscal year to arrive at the fiscal year's net profit or loss. It is split

into two sections. First, it calculates gross profit based on operating income and expenses.

The net profit is derived by subtracting non-operating expenses and adding non-operating

income.

Cash Flow Statements: It aids in determining the requirement for external funding. It

calculates the cash inflow and outflow for operating, investing, and financing activities.

The changes in current assets and current liabilities, as well as interest and tax payments,

are all part of operating activities. The purchase or sale of fixed assets, as well as any

payment related to the company's merger and acquisition, are all examples of investing

activities. The issuance of equity capital, debentures, loans, and dividend payments are all

examples of financing activities.

Ratios: These are used to assess the state of two or more financial statement parts. It

summarises the financial data seen in the financial statements. It assesses the company's financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

performance, allowing the company to be proactive. It assesses both short- and long-term

financial and operational performance, assisting in the identification of company trends

(Mahpour and Mortaheb, 2018). It refers to the relationship or comparison that is established

between the various statistics in the profit and loss account and the balance sheet. These ratios

aid in evaluating a company's performance by comparing it to prior year's results or to the

performance of other companies in the same field. It also aids in detecting the current trend and

forecasting future trends. There are a variety of ratios that businesses can employ to manage their

cash.

Uses of Ratios:

Comparisons: It assesses the financial performance of the company and compares it to

that of other companies in the same industry.

Decision-Making: Gainfulness, trends, paying and borrowing capacity may all be

assessed using financial statements, which aids in making the best selections.

Operational Efficiency: It aids in the determination of a company's liquidity, solvency,

and profitability. And it also shows management's ability to keep costs low while creating

revenue and profit (Mestry, 2018).

Financial Resource Utilization: It provides quantitative information about the company

that aids in evaluating resource overuse and underutilization.

SECTION 3

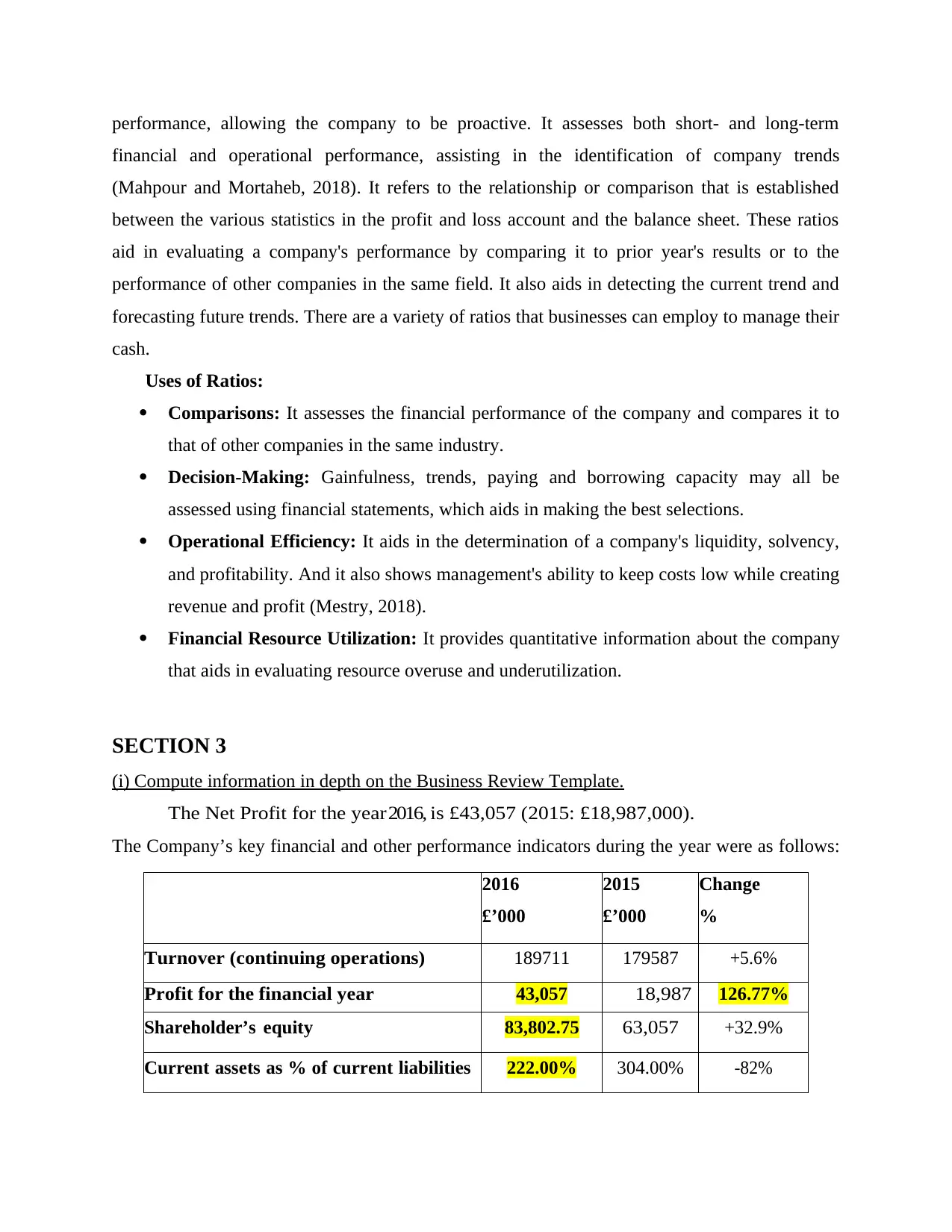

(i) Compute information in depth on the Business Review Template.

The Net Profit for the year 2016, is £43,057 (2015: £18,987,000).

The Company’s key financial and other performance indicators during the year were as follows:

2016

£’000

2015

£’000

Change

%

Turnover (continuing operations) 189711 179587 +5.6%

Profit for the financial year 43,057 18,987 126.77%

Shareholder’s equity 83,802.75 63,057 +32.9%

Current assets as % of current liabilities 222.00% 304.00% -82%

financial and operational performance, assisting in the identification of company trends

(Mahpour and Mortaheb, 2018). It refers to the relationship or comparison that is established

between the various statistics in the profit and loss account and the balance sheet. These ratios

aid in evaluating a company's performance by comparing it to prior year's results or to the

performance of other companies in the same field. It also aids in detecting the current trend and

forecasting future trends. There are a variety of ratios that businesses can employ to manage their

cash.

Uses of Ratios:

Comparisons: It assesses the financial performance of the company and compares it to

that of other companies in the same industry.

Decision-Making: Gainfulness, trends, paying and borrowing capacity may all be

assessed using financial statements, which aids in making the best selections.

Operational Efficiency: It aids in the determination of a company's liquidity, solvency,

and profitability. And it also shows management's ability to keep costs low while creating

revenue and profit (Mestry, 2018).

Financial Resource Utilization: It provides quantitative information about the company

that aids in evaluating resource overuse and underutilization.

SECTION 3

(i) Compute information in depth on the Business Review Template.

The Net Profit for the year 2016, is £43,057 (2015: £18,987,000).

The Company’s key financial and other performance indicators during the year were as follows:

2016

£’000

2015

£’000

Change

%

Turnover (continuing operations) 189711 179587 +5.6%

Profit for the financial year 43,057 18,987 126.77%

Shareholder’s equity 83,802.75 63,057 +32.9%

Current assets as % of current liabilities 222.00% 304.00% -82%

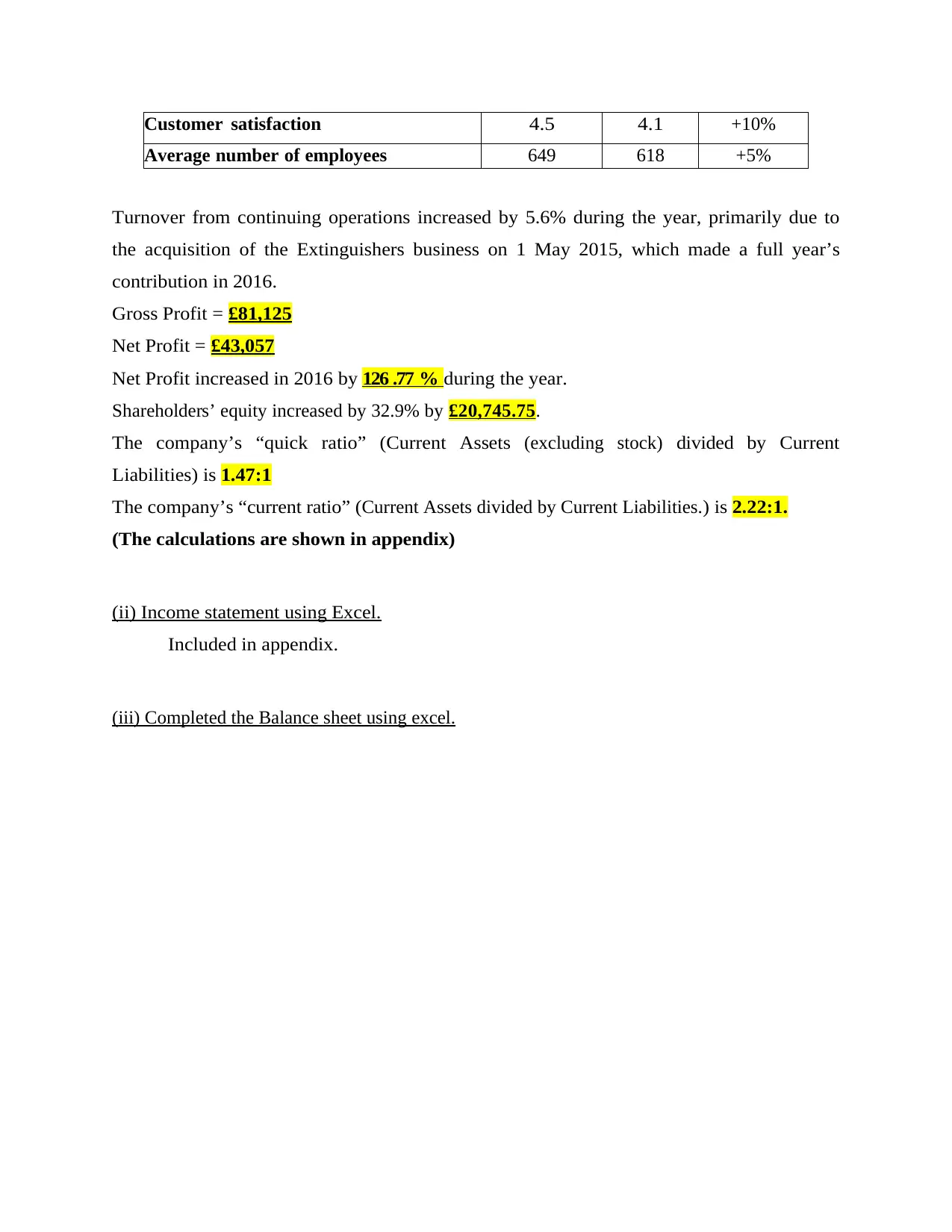

Customer satisfaction 4.5 4.1 +10%

Average number of employees 649 618 +5%

Turnover from continuing operations increased by 5.6% during the year, primarily due to

the acquisition of the Extinguishers business on 1 May 2015, which made a full year’s

contribution in 2016.

Gross Profit = £81,125

Net Profit = £43,057

Net Profit increased in 2016 by 126 .77 % during the year.

Shareholders’ equity increased by 32.9% by £20,745.75.

The company’s “quick ratio” (Current Assets (excluding stock) divided by Current

Liabilities) is 1.47:1

The company’s “current ratio” (Current Assets divided by Current Liabilities. ) is 2.22:1.

(The calculations are shown in appendix)

(ii) Income statement using Excel.

Included in appendix.

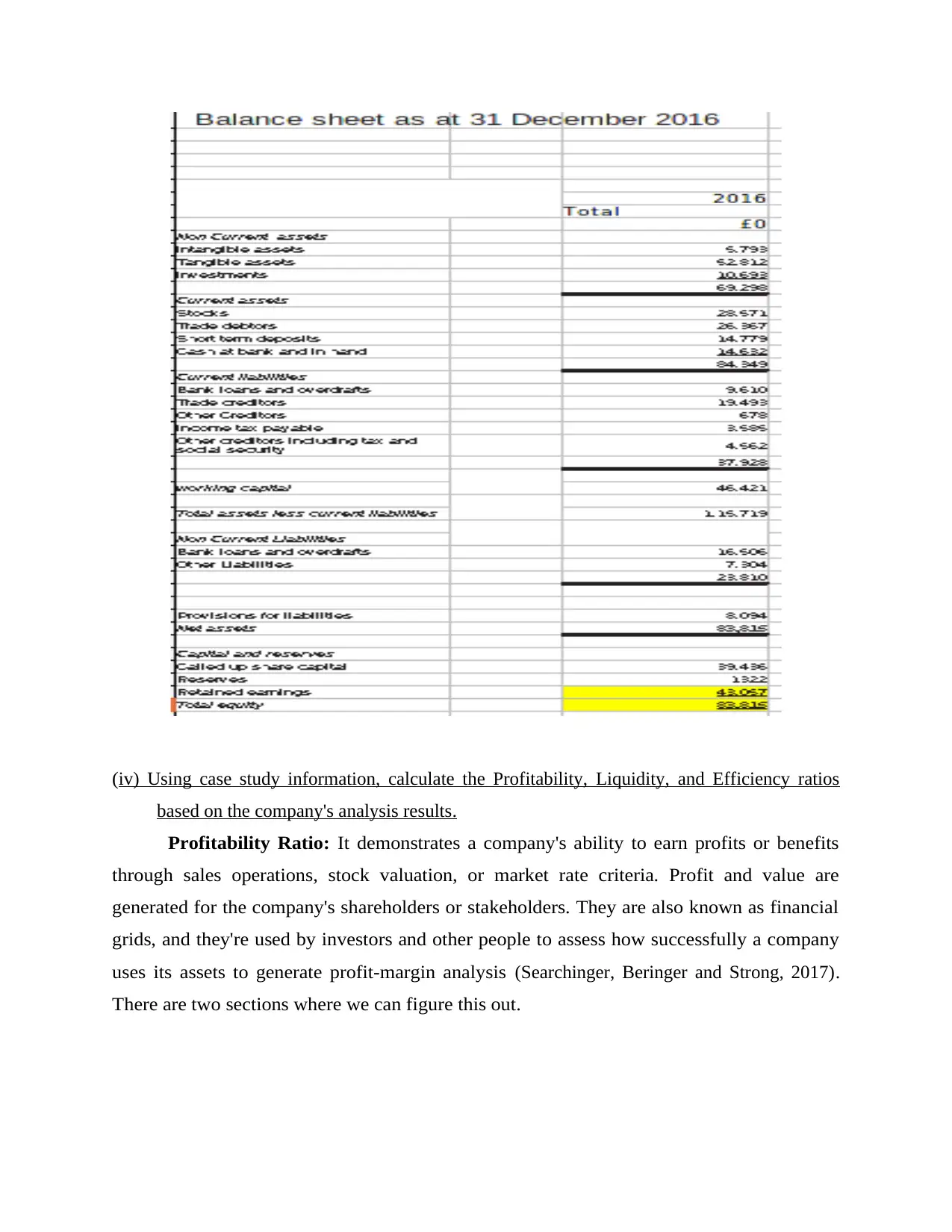

(iii) Completed the Balance sheet using excel.

Average number of employees 649 618 +5%

Turnover from continuing operations increased by 5.6% during the year, primarily due to

the acquisition of the Extinguishers business on 1 May 2015, which made a full year’s

contribution in 2016.

Gross Profit = £81,125

Net Profit = £43,057

Net Profit increased in 2016 by 126 .77 % during the year.

Shareholders’ equity increased by 32.9% by £20,745.75.

The company’s “quick ratio” (Current Assets (excluding stock) divided by Current

Liabilities) is 1.47:1

The company’s “current ratio” (Current Assets divided by Current Liabilities. ) is 2.22:1.

(The calculations are shown in appendix)

(ii) Income statement using Excel.

Included in appendix.

(iii) Completed the Balance sheet using excel.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(iv) Using case study information, calculate the Profitability, Liquidity, and Efficiency ratios

based on the company's analysis results.

Profitability Ratio: It demonstrates a company's ability to earn profits or benefits

through sales operations, stock valuation, or market rate criteria. Profit and value are

generated for the company's shareholders or stakeholders. They are also known as financial

grids, and they're used by investors and other people to assess how successfully a company

uses its assets to generate profit-margin analysis (Searchinger, Beringer and Strong, 2017) .

There are two sections where we can figure this out.

based on the company's analysis results.

Profitability Ratio: It demonstrates a company's ability to earn profits or benefits

through sales operations, stock valuation, or market rate criteria. Profit and value are

generated for the company's shareholders or stakeholders. They are also known as financial

grids, and they're used by investors and other people to assess how successfully a company

uses its assets to generate profit-margin analysis (Searchinger, Beringer and Strong, 2017) .

There are two sections where we can figure this out.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

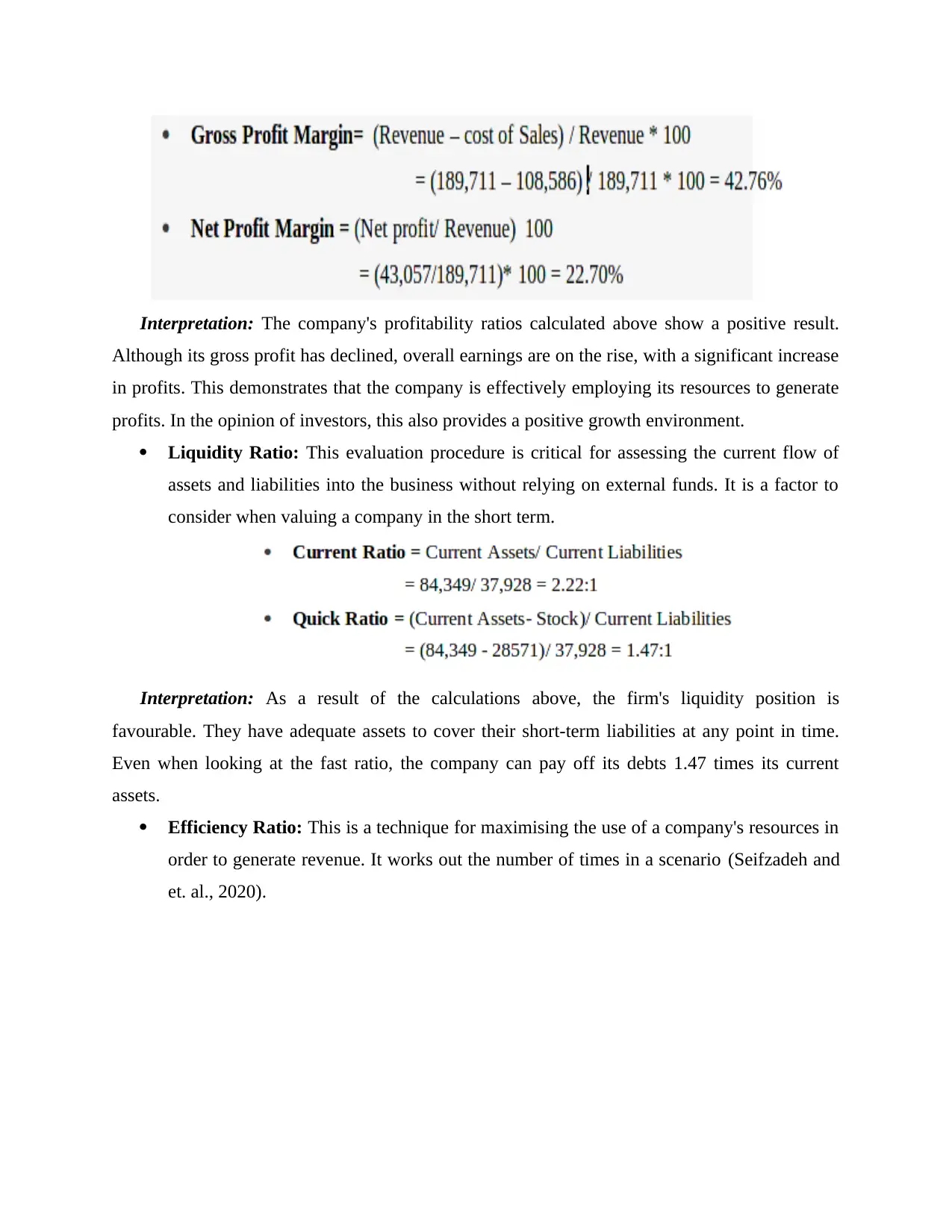

Interpretation: The company's profitability ratios calculated above show a positive result.

Although its gross profit has declined, overall earnings are on the rise, with a significant increase

in profits. This demonstrates that the company is effectively employing its resources to generate

profits. In the opinion of investors, this also provides a positive growth environment.

Liquidity Ratio: This evaluation procedure is critical for assessing the current flow of

assets and liabilities into the business without relying on external funds. It is a factor to

consider when valuing a company in the short term.

Interpretation: As a result of the calculations above, the firm's liquidity position is

favourable. They have adequate assets to cover their short-term liabilities at any point in time.

Even when looking at the fast ratio, the company can pay off its debts 1.47 times its current

assets.

Efficiency Ratio: This is a technique for maximising the use of a company's resources in

order to generate revenue. It works out the number of times in a scenario (Seifzadeh and

et. al., 2020).

Although its gross profit has declined, overall earnings are on the rise, with a significant increase

in profits. This demonstrates that the company is effectively employing its resources to generate

profits. In the opinion of investors, this also provides a positive growth environment.

Liquidity Ratio: This evaluation procedure is critical for assessing the current flow of

assets and liabilities into the business without relying on external funds. It is a factor to

consider when valuing a company in the short term.

Interpretation: As a result of the calculations above, the firm's liquidity position is

favourable. They have adequate assets to cover their short-term liabilities at any point in time.

Even when looking at the fast ratio, the company can pay off its debts 1.47 times its current

assets.

Efficiency Ratio: This is a technique for maximising the use of a company's resources in

order to generate revenue. It works out the number of times in a scenario (Seifzadeh and

et. al., 2020).

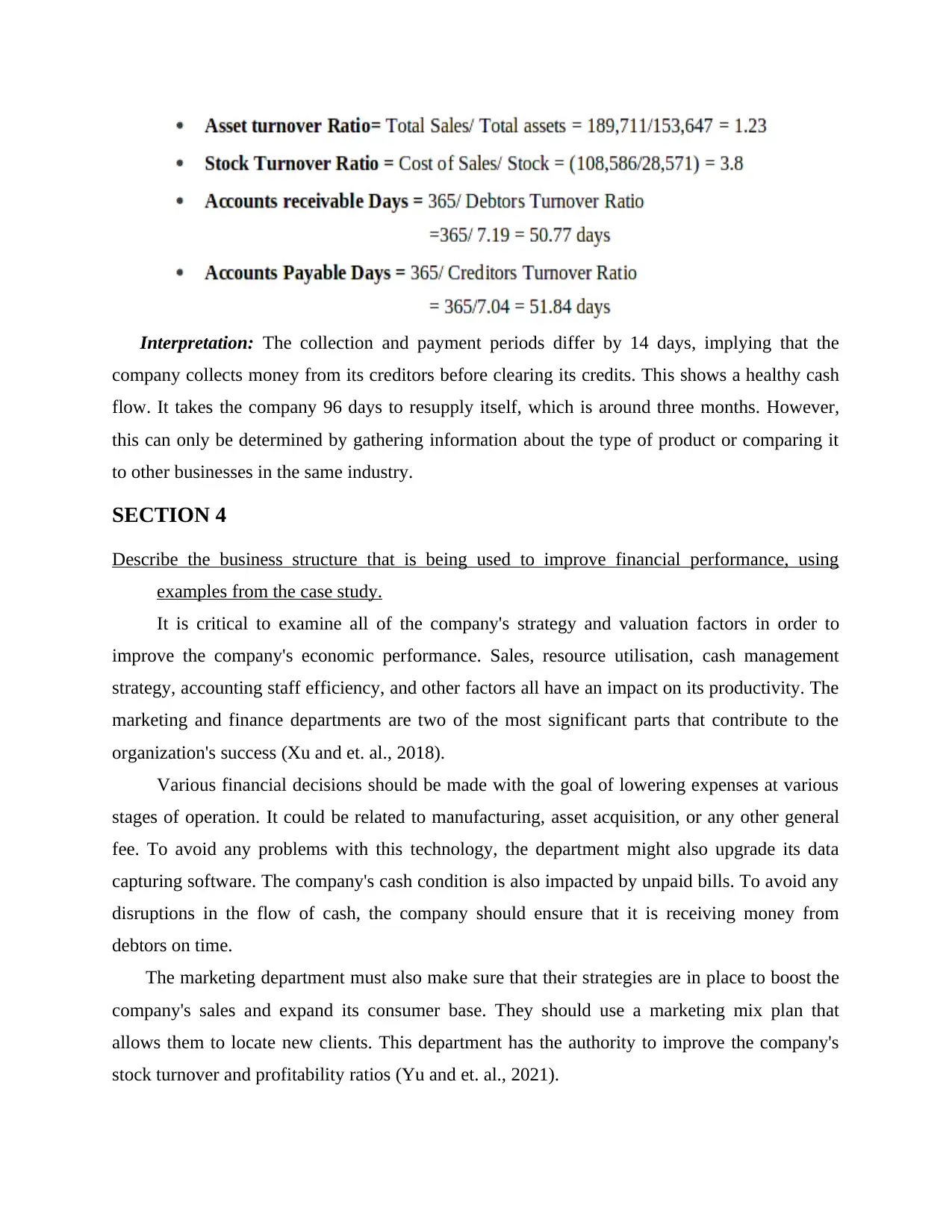

Interpretation: The collection and payment periods differ by 14 days, implying that the

company collects money from its creditors before clearing its credits. This shows a healthy cash

flow. It takes the company 96 days to resupply itself, which is around three months. However,

this can only be determined by gathering information about the type of product or comparing it

to other businesses in the same industry.

SECTION 4

Describe the business structure that is being used to improve financial performance, using

examples from the case study.

It is critical to examine all of the company's strategy and valuation factors in order to

improve the company's economic performance. Sales, resource utilisation, cash management

strategy, accounting staff efficiency, and other factors all have an impact on its productivity. The

marketing and finance departments are two of the most significant parts that contribute to the

organization's success (Xu and et. al., 2018).

Various financial decisions should be made with the goal of lowering expenses at various

stages of operation. It could be related to manufacturing, asset acquisition, or any other general

fee. To avoid any problems with this technology, the department might also upgrade its data

capturing software. The company's cash condition is also impacted by unpaid bills. To avoid any

disruptions in the flow of cash, the company should ensure that it is receiving money from

debtors on time.

The marketing department must also make sure that their strategies are in place to boost the

company's sales and expand its consumer base. They should use a marketing mix plan that

allows them to locate new clients. This department has the authority to improve the company's

stock turnover and profitability ratios (Yu and et. al., 2021).

company collects money from its creditors before clearing its credits. This shows a healthy cash

flow. It takes the company 96 days to resupply itself, which is around three months. However,

this can only be determined by gathering information about the type of product or comparing it

to other businesses in the same industry.

SECTION 4

Describe the business structure that is being used to improve financial performance, using

examples from the case study.

It is critical to examine all of the company's strategy and valuation factors in order to

improve the company's economic performance. Sales, resource utilisation, cash management

strategy, accounting staff efficiency, and other factors all have an impact on its productivity. The

marketing and finance departments are two of the most significant parts that contribute to the

organization's success (Xu and et. al., 2018).

Various financial decisions should be made with the goal of lowering expenses at various

stages of operation. It could be related to manufacturing, asset acquisition, or any other general

fee. To avoid any problems with this technology, the department might also upgrade its data

capturing software. The company's cash condition is also impacted by unpaid bills. To avoid any

disruptions in the flow of cash, the company should ensure that it is receiving money from

debtors on time.

The marketing department must also make sure that their strategies are in place to boost the

company's sales and expand its consumer base. They should use a marketing mix plan that

allows them to locate new clients. This department has the authority to improve the company's

stock turnover and profitability ratios (Yu and et. al., 2021).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONCLUSION

From the above report, it can be stated that a successful firm requires an effective

financial management system. It plans and organises all of the finances in order to maximise

earnings and maximise utility. It employs a variety of financial accounts to assess the

performance of a corporation using techniques such as accounting ratios and to identify solutions

for improving the firm's situation. These ratios aid in the interpretation of the company's

profitability, efficiency, and liquidity status by establishing a relationship between the various

figures in the financial statements.

From the above report, it can be stated that a successful firm requires an effective

financial management system. It plans and organises all of the finances in order to maximise

earnings and maximise utility. It employs a variety of financial accounts to assess the

performance of a corporation using techniques such as accounting ratios and to identify solutions

for improving the firm's situation. These ratios aid in the interpretation of the company's

profitability, efficiency, and liquidity status by establishing a relationship between the various

figures in the financial statements.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Fang, W and et. al., 2018. Falls from heights: A computer vision-based approach for safety

harness detection. Automation in Construction. 91. pp.53-61.

Haw, I.M and et. al., 2018. Having a finger in the pie: labor power and corporate payout

policy. Financial Management. 47(4). pp.993-1027.

Huang, J and et. al., 2018. Build financial capability for all. Grand challenges for social work

and society. pp.227-247.

Mahpour, A. and Mortaheb, M.M., 2018. Financial-based incentive plan to reduce construction

waste. Journal of Construction Engineering and Management. 144(5). p.04018029.

Mestry, R., 2018. The role of governing bodies in the management of financial resources in

South African no-fee public schools. Educational Management Administration &

Leadership. 46(3). pp.385-400.

Searchinger, T.D., Beringer, T. and Strong, A., 2017. Does the world have low-carbon bioenergy

potential from the dedicated use of land? Energy Policy. 110. pp.434-446.

Seifzadeh, M and et. al., 2020. The relationship between management characteristics and

financial statement readability. EuroMed Journal of Business.

Xu, H and et. al., 2018. Personal exposure of PM2. 5 emitted from solid fuels combustion for

household heating and cooking in rural Guanzhong Plain, northwestern

China. Atmospheric Environment. 185. pp.196-206.

Yu, H and et. al., 2021. Polycyclic aromatic hydrocarbons in surface waters from the seven main

river basins of China: Spatial distribution, source apportionment, and potential risk

assessment. Science of the Total Environment. 752. p.141764.

Zelenkov, Y., Fedorova, E. and Chekrizov, D., 2017. Two-step classification method based on

genetic algorithm for bankruptcy forecasting. Expert Systems with Applications. 88.

pp.393-401.

Books and Journals

Fang, W and et. al., 2018. Falls from heights: A computer vision-based approach for safety

harness detection. Automation in Construction. 91. pp.53-61.

Haw, I.M and et. al., 2018. Having a finger in the pie: labor power and corporate payout

policy. Financial Management. 47(4). pp.993-1027.

Huang, J and et. al., 2018. Build financial capability for all. Grand challenges for social work

and society. pp.227-247.

Mahpour, A. and Mortaheb, M.M., 2018. Financial-based incentive plan to reduce construction

waste. Journal of Construction Engineering and Management. 144(5). p.04018029.

Mestry, R., 2018. The role of governing bodies in the management of financial resources in

South African no-fee public schools. Educational Management Administration &

Leadership. 46(3). pp.385-400.

Searchinger, T.D., Beringer, T. and Strong, A., 2017. Does the world have low-carbon bioenergy

potential from the dedicated use of land? Energy Policy. 110. pp.434-446.

Seifzadeh, M and et. al., 2020. The relationship between management characteristics and

financial statement readability. EuroMed Journal of Business.

Xu, H and et. al., 2018. Personal exposure of PM2. 5 emitted from solid fuels combustion for

household heating and cooking in rural Guanzhong Plain, northwestern

China. Atmospheric Environment. 185. pp.196-206.

Yu, H and et. al., 2021. Polycyclic aromatic hydrocarbons in surface waters from the seven main

river basins of China: Spatial distribution, source apportionment, and potential risk

assessment. Science of the Total Environment. 752. p.141764.

Zelenkov, Y., Fedorova, E. and Chekrizov, D., 2017. Two-step classification method based on

genetic algorithm for bankruptcy forecasting. Expert Systems with Applications. 88.

pp.393-401.

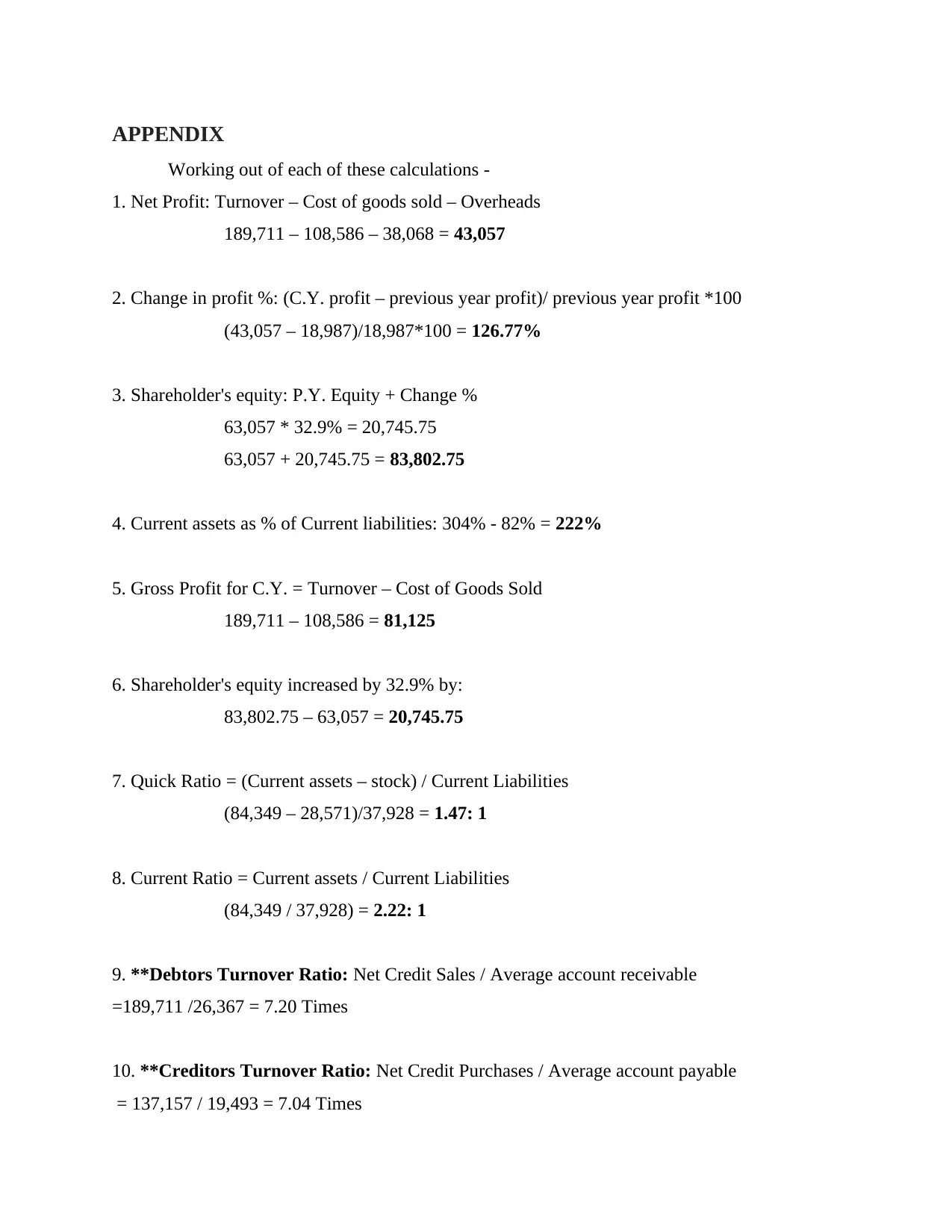

APPENDIX

Working out of each of these calculations -

1. Net Profit: Turnover – Cost of goods sold – Overheads

189,711 – 108,586 – 38,068 = 43,057

2. Change in profit %: (C.Y. profit – previous year profit)/ previous year profit *100

(43,057 – 18,987)/18,987*100 = 126.77%

3. Shareholder's equity: P.Y. Equity + Change %

63,057 * 32.9% = 20,745.75

63,057 + 20,745.75 = 83,802.75

4. Current assets as % of Current liabilities: 304% - 82% = 222%

5. Gross Profit for C.Y. = Turnover – Cost of Goods Sold

189,711 – 108,586 = 81,125

6. Shareholder's equity increased by 32.9% by:

83,802.75 – 63,057 = 20,745.75

7. Quick Ratio = (Current assets – stock) / Current Liabilities

(84,349 – 28,571)/37,928 = 1.47: 1

8. Current Ratio = Current assets / Current Liabilities

(84,349 / 37,928) = 2.22: 1

9. **Debtors Turnover Ratio: Net Credit Sales / Average account receivable

=189,711 /26,367 = 7.20 Times

10. **Creditors Turnover Ratio: Net Credit Purchases / Average account payable

= 137,157 / 19,493 = 7.04 Times

Working out of each of these calculations -

1. Net Profit: Turnover – Cost of goods sold – Overheads

189,711 – 108,586 – 38,068 = 43,057

2. Change in profit %: (C.Y. profit – previous year profit)/ previous year profit *100

(43,057 – 18,987)/18,987*100 = 126.77%

3. Shareholder's equity: P.Y. Equity + Change %

63,057 * 32.9% = 20,745.75

63,057 + 20,745.75 = 83,802.75

4. Current assets as % of Current liabilities: 304% - 82% = 222%

5. Gross Profit for C.Y. = Turnover – Cost of Goods Sold

189,711 – 108,586 = 81,125

6. Shareholder's equity increased by 32.9% by:

83,802.75 – 63,057 = 20,745.75

7. Quick Ratio = (Current assets – stock) / Current Liabilities

(84,349 – 28,571)/37,928 = 1.47: 1

8. Current Ratio = Current assets / Current Liabilities

(84,349 / 37,928) = 2.22: 1

9. **Debtors Turnover Ratio: Net Credit Sales / Average account receivable

=189,711 /26,367 = 7.20 Times

10. **Creditors Turnover Ratio: Net Credit Purchases / Average account payable

= 137,157 / 19,493 = 7.04 Times

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.