Accounting and Finance Report: APN Outdoor Group Financial Analysis

VerifiedAdded on 2020/04/01

|11

|2693

|31

Report

AI Summary

This report provides a detailed financial analysis of APN Outdoor Group, an ASX-listed outdoor advertising company. It examines the company's capital structure, including a comparison of its bonds with government bonds and an analysis of its debt and equity components. The report calculates the weighted average cost of capital (WACC) and compares APN's capital structure with that of Investa Office Funds. Furthermore, it analyzes key financial ratios, including profitability, liquidity, leverage, and asset turnover ratios, to evaluate the company's wealth maximization strategies over the past three years. The report also discusses the importance of minimizing the cost of capital and recommends strategies for APN Outdoor Group to lower its cost of capital, such as managing interest rates, capital structure policy, tax rates, and investment policy. The analysis concludes with insights into the company's financial performance and recommendations for future financial strategies.

Running head: ACCOUNTING AND FINANCE

ACCOUNTING AND FINANCE

ACCOUNTING AND FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCE 2

Executive summary

In this study, the researcher has made critical analysis on the financial performance of APN

Outdoor Group. The researcher has also demonstrated the capital structure of APN outdoor

group and its wealth maximization strategy, with the help of different financial instruments like

financial ratios and comparative analysis. However, the study does not end here, further analysis

on the cost of capital of the company also been done with the help of examples.

Executive summary

In this study, the researcher has made critical analysis on the financial performance of APN

Outdoor Group. The researcher has also demonstrated the capital structure of APN outdoor

group and its wealth maximization strategy, with the help of different financial instruments like

financial ratios and comparative analysis. However, the study does not end here, further analysis

on the cost of capital of the company also been done with the help of examples.

ACCOUNTING AND FINANCE 3

Table of contents

Introduction......................................................................................................................................4

Discussing the capital structure of APN Outdoor Group................................................................4

Critically analyzing the wealth maximization strategy of APN Outdoor Group.............................6

Conclusion.....................................................................................................................................10

References......................................................................................................................................12

Table of contents

Introduction......................................................................................................................................4

Discussing the capital structure of APN Outdoor Group................................................................4

Critically analyzing the wealth maximization strategy of APN Outdoor Group.............................6

Conclusion.....................................................................................................................................10

References......................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING AND FINANCE 4

Introduction

APN Outdoor group Limited (APO) is one of the greatest outdoor advertising operator in

Australia and in New Zealand. It is an ASX listed company which offers many advertising

services. These advertising includes digital billboards, static roadside billboards, advertisement

of rails and advertisement of airport in Australia and New Zealand. This study aims to

demonstrate the capital structure of APN outdoor group and its wealth maximization strategy,

with the help of different financial instruments like financial ratios and comparative analysis.

The researchers have also aimed to recommend the company for lowering its cost of capital.

Discussing the capital structure of APN Outdoor Group

Every business raises funds for financing its projects. It may raise funds either internally or

externally. If a firm raises funds internally it may use reserves and surpluses, retained earnings or

it may have to sell its assets. However, if the company needs huge funds, it has to raise funds by

issuing either equity shares or preference shares. Moreover, it may also borrow funds from

financial institutions or banks (Hope & Myllylahti, 2013). Thus, the capital structure is said to be

the mixture of short-term and long-term debt or equity.

a) Comparing the bonds of the company with government bonds

According to Wayne Castle, the CFO of APN Outdoor Group, the bonds of the company

distributed in the market proved to be the beneficial factor for the business. The rate of the bonds

was low as compared to the government, but the return on such bonds were reasonable. Thus, in

the year 2014, the company sold bonds in large distribution. This not only helped the parent

company to grow their business, but it's subsidiaries like iOM Pty Ltd, has largely gained benefit

in promoting them in the international market. On the counterpart, government bonds took

dominating position since 2015, due to its low risk, regular income and easy to buy and sell

factor (www.quotes.wsj.com, 2017).

b) Categorizing and calculating current capital structure and after tax weighted average

cost of capital

From the annual report of 2016, it has been found that the company APN outdoor group limited

has taken more borrowings in the year 2016 for its current project. It has been found that

company has not raised its funds from internal sources but it has raised its funds from external

sources like borrowings of $ 102,677 from bank and issued equity shares to the public, which is

fully paid up (Becker & Ivashina, 2015). The structure of equity debts is described below.

Introduction

APN Outdoor group Limited (APO) is one of the greatest outdoor advertising operator in

Australia and in New Zealand. It is an ASX listed company which offers many advertising

services. These advertising includes digital billboards, static roadside billboards, advertisement

of rails and advertisement of airport in Australia and New Zealand. This study aims to

demonstrate the capital structure of APN outdoor group and its wealth maximization strategy,

with the help of different financial instruments like financial ratios and comparative analysis.

The researchers have also aimed to recommend the company for lowering its cost of capital.

Discussing the capital structure of APN Outdoor Group

Every business raises funds for financing its projects. It may raise funds either internally or

externally. If a firm raises funds internally it may use reserves and surpluses, retained earnings or

it may have to sell its assets. However, if the company needs huge funds, it has to raise funds by

issuing either equity shares or preference shares. Moreover, it may also borrow funds from

financial institutions or banks (Hope & Myllylahti, 2013). Thus, the capital structure is said to be

the mixture of short-term and long-term debt or equity.

a) Comparing the bonds of the company with government bonds

According to Wayne Castle, the CFO of APN Outdoor Group, the bonds of the company

distributed in the market proved to be the beneficial factor for the business. The rate of the bonds

was low as compared to the government, but the return on such bonds were reasonable. Thus, in

the year 2014, the company sold bonds in large distribution. This not only helped the parent

company to grow their business, but it's subsidiaries like iOM Pty Ltd, has largely gained benefit

in promoting them in the international market. On the counterpart, government bonds took

dominating position since 2015, due to its low risk, regular income and easy to buy and sell

factor (www.quotes.wsj.com, 2017).

b) Categorizing and calculating current capital structure and after tax weighted average

cost of capital

From the annual report of 2016, it has been found that the company APN outdoor group limited

has taken more borrowings in the year 2016 for its current project. It has been found that

company has not raised its funds from internal sources but it has raised its funds from external

sources like borrowings of $ 102,677 from bank and issued equity shares to the public, which is

fully paid up (Becker & Ivashina, 2015). The structure of equity debts is described below.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCE 5

Number of issued capital is 166,614,509 and the paid-up capital is $ 222,334

Basic earnings per share is 0.29*166,614,509= $48,318,208

Dividend paid is $29,158.

Computation of after tax weighted average cost of capital

APO issued 166,6144,509 shares of common stock @ $7.50 per share. The shares are currently

trading at $ 9.90 per share. Current risk-free rate is 2.4%, market risk premium is 7% and the

company has a beta coefficient of 1.3 (www.au.finance.yahoo.com, 2017).

The tax rate is 28.5%.

Current Market Value of Equity = 1666144509 × $9.90 = $16494820640

Current Market Value of Debt = 1666144509 × $25 = $41653612725

Total Market Value of Debt and Equity = $ 58148433365

Weight of Equity = $16494820640/ $41653612725= 39.59%

Weight of Debt = $41653612725/ $58148433365= 71.63%, or

Weight of Debt = 100% minus cost of equity = 100% − 39.59% = 61.41%

Cost of Equity = Risk Free Rate + Beta × Market Risk Premium = 2.4% + 1.3× 7% = 11.5%

After-tax cost of debt is 7.586% [= 10.61% * (1 – 28.5%)].

WACC = (weight of equity * cost of equity) + (weight of debt * after tax cost of debt)

WACC = (39.59% * 11.5%) + (61.41% * 7.586%) = 9.317%

c) Comparing firm’s capital structure with Investa Office Funds

Capital structure of APO includes long-term borrowings, issued capital, reserves and surpluses

and retained earnings. Similarly, the capital structure of IOF also includes borrowings, issued

capital, reserves and surplus, but IOF also has issued debentures at the rate of 8%. Based on the

comparison of financial statements of both the companies for the year 2016, it can be said that

APO has issued more equity capital as compared to equities issued by IOF. However, there is an

interesting fact in the comparison of issued capital between both the companies (Baur &

Miyakawa, 2014). APO at one hand had similar pattern of issuing equities and IOF on the other

hand had issued different number of equities in different years. This indicates that IOF is

relatively dependent on the equities to raise funds for its business projects.

d) Outlining significant changes in the capital structure of the firm in the past three years

Based on the review of annual reports of past three years, it can be seen that the APO has not

gone through a big rollercoaster in its capital structure. Its long-term borrowings had increased

Number of issued capital is 166,614,509 and the paid-up capital is $ 222,334

Basic earnings per share is 0.29*166,614,509= $48,318,208

Dividend paid is $29,158.

Computation of after tax weighted average cost of capital

APO issued 166,6144,509 shares of common stock @ $7.50 per share. The shares are currently

trading at $ 9.90 per share. Current risk-free rate is 2.4%, market risk premium is 7% and the

company has a beta coefficient of 1.3 (www.au.finance.yahoo.com, 2017).

The tax rate is 28.5%.

Current Market Value of Equity = 1666144509 × $9.90 = $16494820640

Current Market Value of Debt = 1666144509 × $25 = $41653612725

Total Market Value of Debt and Equity = $ 58148433365

Weight of Equity = $16494820640/ $41653612725= 39.59%

Weight of Debt = $41653612725/ $58148433365= 71.63%, or

Weight of Debt = 100% minus cost of equity = 100% − 39.59% = 61.41%

Cost of Equity = Risk Free Rate + Beta × Market Risk Premium = 2.4% + 1.3× 7% = 11.5%

After-tax cost of debt is 7.586% [= 10.61% * (1 – 28.5%)].

WACC = (weight of equity * cost of equity) + (weight of debt * after tax cost of debt)

WACC = (39.59% * 11.5%) + (61.41% * 7.586%) = 9.317%

c) Comparing firm’s capital structure with Investa Office Funds

Capital structure of APO includes long-term borrowings, issued capital, reserves and surpluses

and retained earnings. Similarly, the capital structure of IOF also includes borrowings, issued

capital, reserves and surplus, but IOF also has issued debentures at the rate of 8%. Based on the

comparison of financial statements of both the companies for the year 2016, it can be said that

APO has issued more equity capital as compared to equities issued by IOF. However, there is an

interesting fact in the comparison of issued capital between both the companies (Baur &

Miyakawa, 2014). APO at one hand had similar pattern of issuing equities and IOF on the other

hand had issued different number of equities in different years. This indicates that IOF is

relatively dependent on the equities to raise funds for its business projects.

d) Outlining significant changes in the capital structure of the firm in the past three years

Based on the review of annual reports of past three years, it can be seen that the APO has not

gone through a big rollercoaster in its capital structure. Its long-term borrowings had increased

ACCOUNTING AND FINANCE 6

over three years, but issued and paid up capital remained unchanged. In addition, retained

earnings had significantly rose in every consecutive year, along with the considerable rise in the

reserves and surpluses (Robb & Robinson, 2014). This indicates that the company is wisely

applying wealth maximization strategies. However, the most eye-catching change can be seen,

the company had paid dividend in the year 2016 amounted to $ 29,158, which is more than twice

of previous year that is $ 9,164.

Critically analyzing the wealth maximization strategy of APN Outdoor Group

In every business shareholder value maximization plays a pivotal role in creating profit.

Therefore, wealth maximization balances the interest of shareholders and stakeholders.

Similarly, it becomes necessary to wisely chose the appropriate wealth maximization strategies.

Building credit, wisely investing, building wealth through retained earnings, and boosting stock

prices are the best ways to maximize wealth or shareholders value.

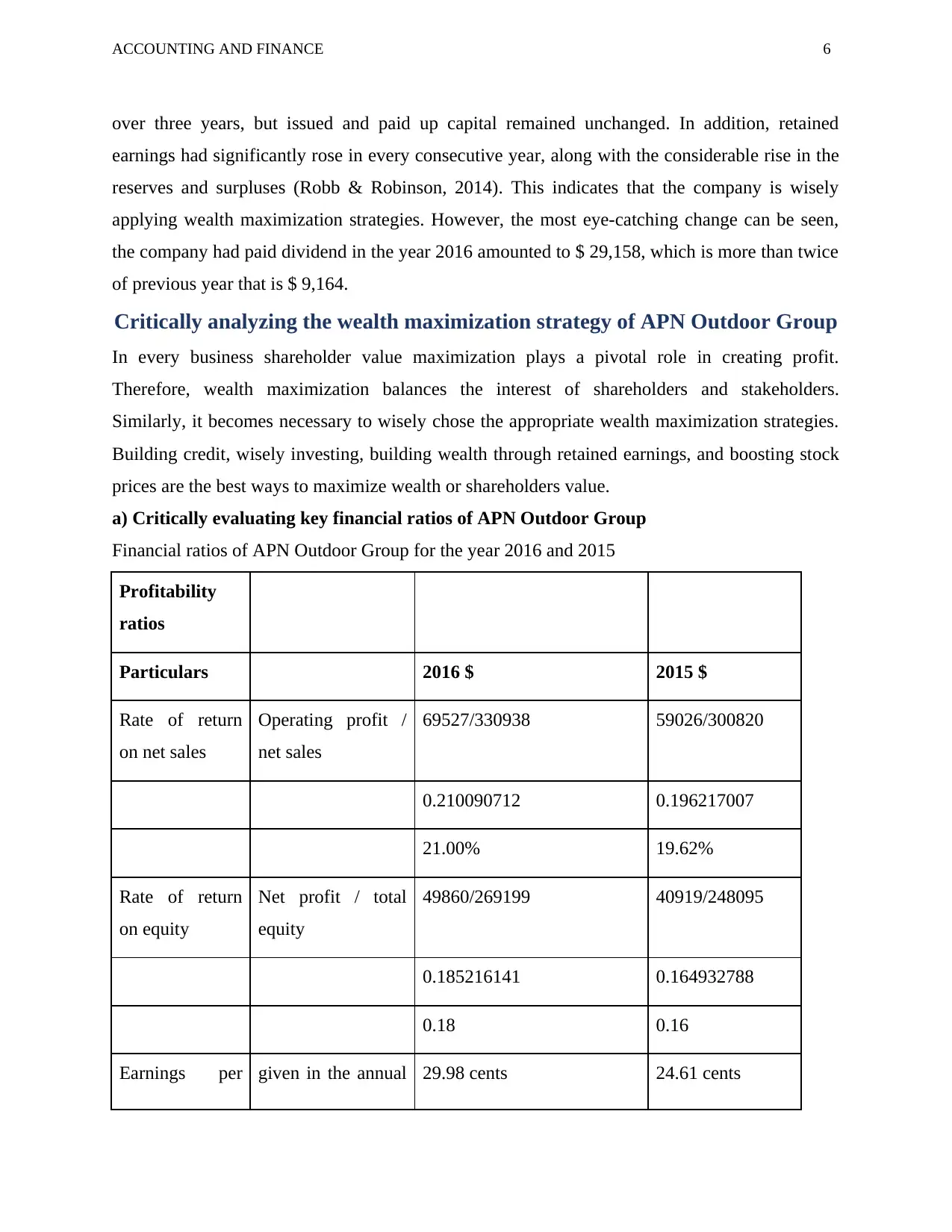

a) Critically evaluating key financial ratios of APN Outdoor Group

Financial ratios of APN Outdoor Group for the year 2016 and 2015

Profitability

ratios

Particulars 2016 $ 2015 $

Rate of return

on net sales

Operating profit /

net sales

69527/330938 59026/300820

0.210090712 0.196217007

21.00% 19.62%

Rate of return

on equity

Net profit / total

equity

49860/269199 40919/248095

0.185216141 0.164932788

0.18 0.16

Earnings per given in the annual 29.98 cents 24.61 cents

over three years, but issued and paid up capital remained unchanged. In addition, retained

earnings had significantly rose in every consecutive year, along with the considerable rise in the

reserves and surpluses (Robb & Robinson, 2014). This indicates that the company is wisely

applying wealth maximization strategies. However, the most eye-catching change can be seen,

the company had paid dividend in the year 2016 amounted to $ 29,158, which is more than twice

of previous year that is $ 9,164.

Critically analyzing the wealth maximization strategy of APN Outdoor Group

In every business shareholder value maximization plays a pivotal role in creating profit.

Therefore, wealth maximization balances the interest of shareholders and stakeholders.

Similarly, it becomes necessary to wisely chose the appropriate wealth maximization strategies.

Building credit, wisely investing, building wealth through retained earnings, and boosting stock

prices are the best ways to maximize wealth or shareholders value.

a) Critically evaluating key financial ratios of APN Outdoor Group

Financial ratios of APN Outdoor Group for the year 2016 and 2015

Profitability

ratios

Particulars 2016 $ 2015 $

Rate of return

on net sales

Operating profit /

net sales

69527/330938 59026/300820

0.210090712 0.196217007

21.00% 19.62%

Rate of return

on equity

Net profit / total

equity

49860/269199 40919/248095

0.185216141 0.164932788

0.18 0.16

Earnings per given in the annual 29.98 cents 24.61 cents

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

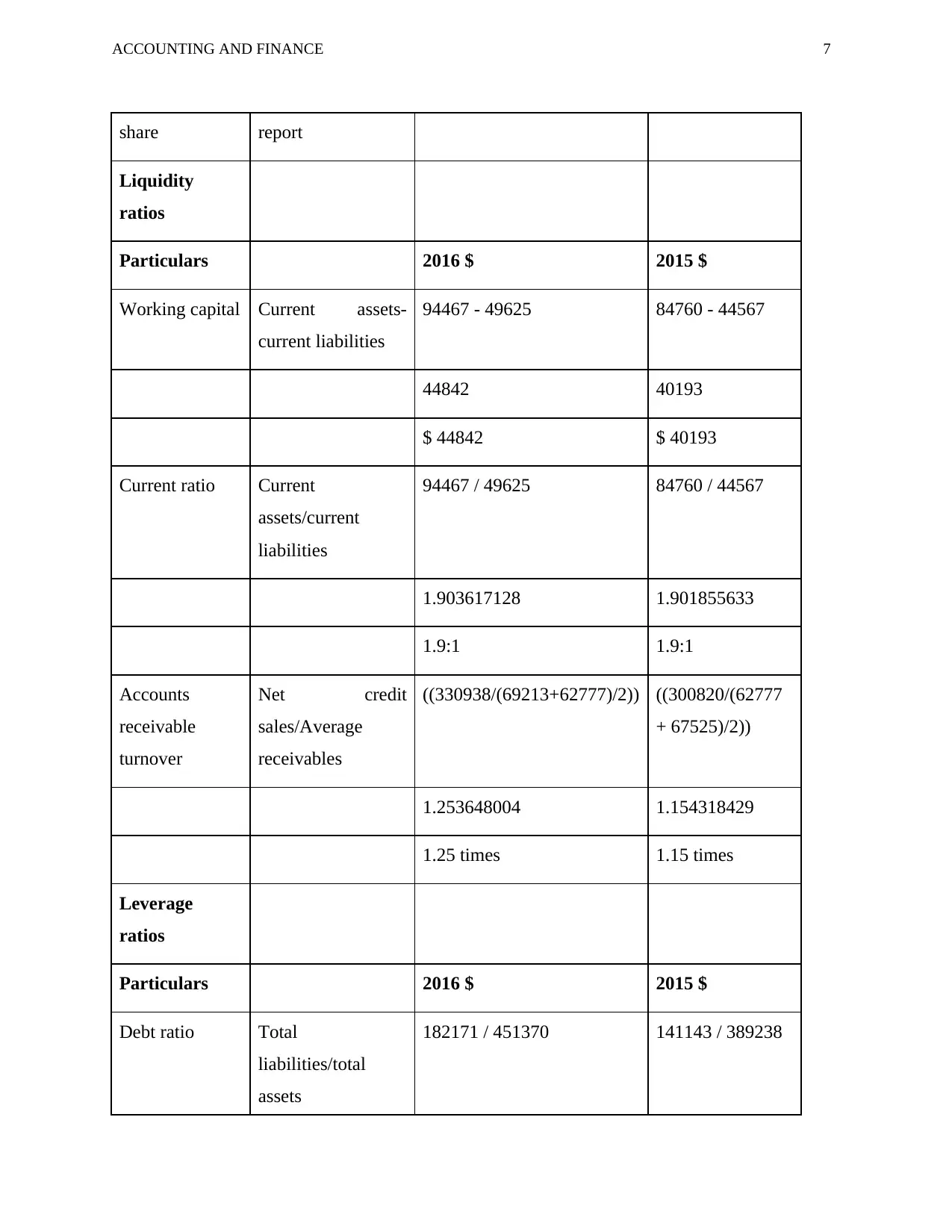

ACCOUNTING AND FINANCE 7

share report

Liquidity

ratios

Particulars 2016 $ 2015 $

Working capital Current assets-

current liabilities

94467 - 49625 84760 - 44567

44842 40193

$ 44842 $ 40193

Current ratio Current

assets/current

liabilities

94467 / 49625 84760 / 44567

1.903617128 1.901855633

1.9:1 1.9:1

Accounts

receivable

turnover

Net credit

sales/Average

receivables

((330938/(69213+62777)/2)) ((300820/(62777

+ 67525)/2))

1.253648004 1.154318429

1.25 times 1.15 times

Leverage

ratios

Particulars 2016 $ 2015 $

Debt ratio Total

liabilities/total

assets

182171 / 451370 141143 / 389238

share report

Liquidity

ratios

Particulars 2016 $ 2015 $

Working capital Current assets-

current liabilities

94467 - 49625 84760 - 44567

44842 40193

$ 44842 $ 40193

Current ratio Current

assets/current

liabilities

94467 / 49625 84760 / 44567

1.903617128 1.901855633

1.9:1 1.9:1

Accounts

receivable

turnover

Net credit

sales/Average

receivables

((330938/(69213+62777)/2)) ((300820/(62777

+ 67525)/2))

1.253648004 1.154318429

1.25 times 1.15 times

Leverage

ratios

Particulars 2016 $ 2015 $

Debt ratio Total

liabilities/total

assets

182171 / 451370 141143 / 389238

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCE 8

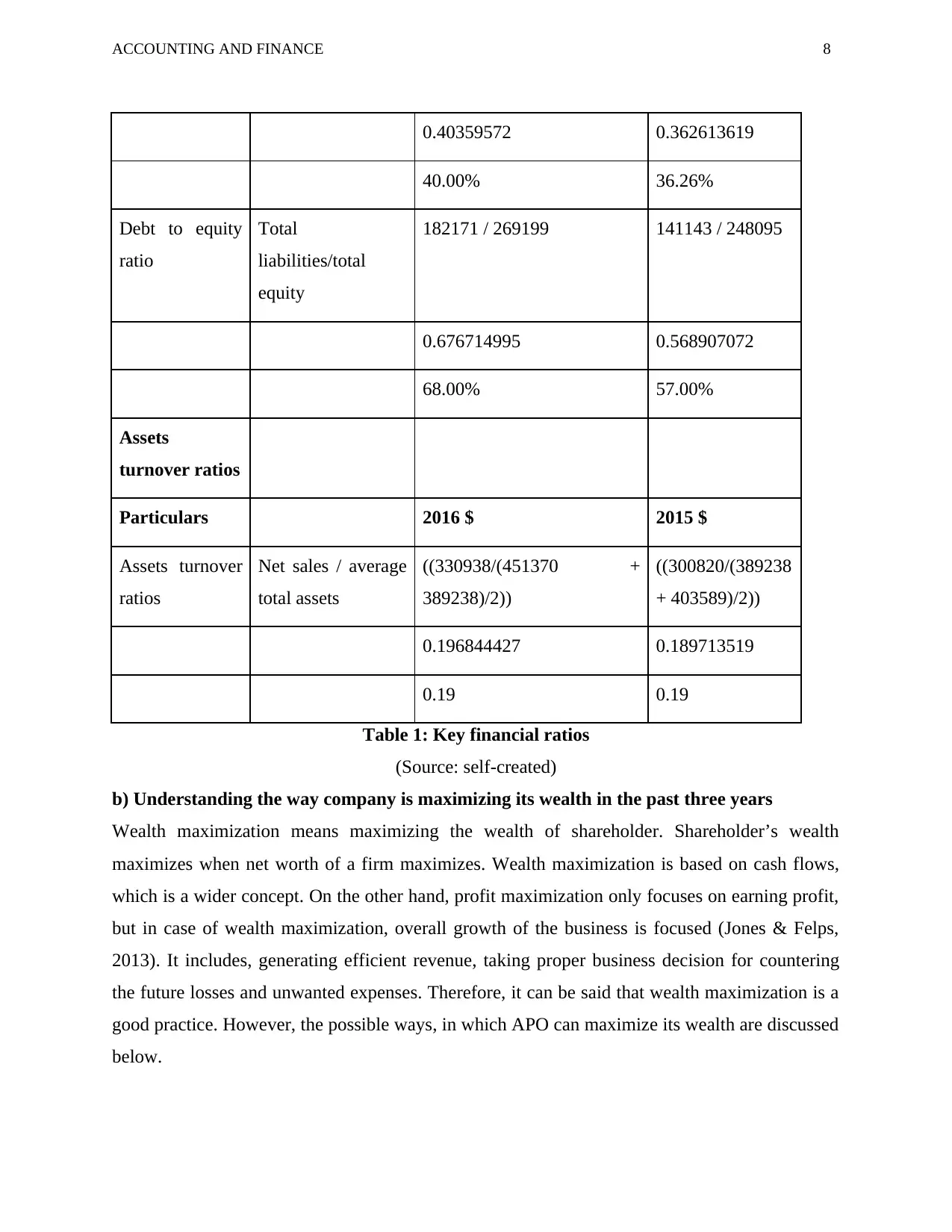

0.40359572 0.362613619

40.00% 36.26%

Debt to equity

ratio

Total

liabilities/total

equity

182171 / 269199 141143 / 248095

0.676714995 0.568907072

68.00% 57.00%

Assets

turnover ratios

Particulars 2016 $ 2015 $

Assets turnover

ratios

Net sales / average

total assets

((330938/(451370 +

389238)/2))

((300820/(389238

+ 403589)/2))

0.196844427 0.189713519

0.19 0.19

Table 1: Key financial ratios

(Source: self-created)

b) Understanding the way company is maximizing its wealth in the past three years

Wealth maximization means maximizing the wealth of shareholder. Shareholder’s wealth

maximizes when net worth of a firm maximizes. Wealth maximization is based on cash flows,

which is a wider concept. On the other hand, profit maximization only focuses on earning profit,

but in case of wealth maximization, overall growth of the business is focused (Jones & Felps,

2013). It includes, generating efficient revenue, taking proper business decision for countering

the future losses and unwanted expenses. Therefore, it can be said that wealth maximization is a

good practice. However, the possible ways, in which APO can maximize its wealth are discussed

below.

0.40359572 0.362613619

40.00% 36.26%

Debt to equity

ratio

Total

liabilities/total

equity

182171 / 269199 141143 / 248095

0.676714995 0.568907072

68.00% 57.00%

Assets

turnover ratios

Particulars 2016 $ 2015 $

Assets turnover

ratios

Net sales / average

total assets

((330938/(451370 +

389238)/2))

((300820/(389238

+ 403589)/2))

0.196844427 0.189713519

0.19 0.19

Table 1: Key financial ratios

(Source: self-created)

b) Understanding the way company is maximizing its wealth in the past three years

Wealth maximization means maximizing the wealth of shareholder. Shareholder’s wealth

maximizes when net worth of a firm maximizes. Wealth maximization is based on cash flows,

which is a wider concept. On the other hand, profit maximization only focuses on earning profit,

but in case of wealth maximization, overall growth of the business is focused (Jones & Felps,

2013). It includes, generating efficient revenue, taking proper business decision for countering

the future losses and unwanted expenses. Therefore, it can be said that wealth maximization is a

good practice. However, the possible ways, in which APO can maximize its wealth are discussed

below.

ACCOUNTING AND FINANCE 9

In this case, the company has generated huge revenue as compared to the previous year, which is

the first step of wealth maximization. The company APN outdoor group invested in a project and

get more internal rate of return and its net present value also increased, in this way shareholder’s

wealth increased (Grant, 2016). This company motivated its employee for the purpose of

maximizing its wealth.

The company’s total equity in the year 2016, 2015 and 2014 are $ 269,199, $ 248,095 and $

216274 respectively. However, total debt for the three consecutive years include borrowings,

amounted to $ 102,677, $ 65,926 and $ 85,121. On the other hand, issued and paid up capital

were remained unchanged. Thus, it can be said that the company is not completely dependent on

the raising funds from public. Whatever the funds required, it raises from borrowings.

c) Discussing the importance of minimizing cost of capital

Since cost of capital is that required of return, which is used for capital budgeting project, it

becomes important to minimize cost of capital, because high cost of capital will tend to increase

cost of capital budgeting like rise in cost of making plants, buildings, etc. (Dhaliwal et al. 2014).

However, lower cost of capital will allow only required cost of budgeting, unnecessary cost will

be abandoned. Thus, it is very important to minimize cost of capital. The importance is described

below.

Due to minimizing cost of capital, required rate of return will increase and internal rate of return

will also increase. But due to reduction in the value of 1 dollar every year, rate of dividend will

remain same but net present value will increase in future. For example,

NPV at 10% discount rate = $ 18,372

Since NPV is greater than zero we have to increase discount rate, thus

NPV at 13% discount rate = $ 4,521

But, it is still greater than zero, discount rate must further be increased, thus

NPV at 14% discount rate = $204

NPV at 15% discount rate = ($3,975)

Since NPV is fairly close to zero at 14% value of (r), therefore

In this case, the company has generated huge revenue as compared to the previous year, which is

the first step of wealth maximization. The company APN outdoor group invested in a project and

get more internal rate of return and its net present value also increased, in this way shareholder’s

wealth increased (Grant, 2016). This company motivated its employee for the purpose of

maximizing its wealth.

The company’s total equity in the year 2016, 2015 and 2014 are $ 269,199, $ 248,095 and $

216274 respectively. However, total debt for the three consecutive years include borrowings,

amounted to $ 102,677, $ 65,926 and $ 85,121. On the other hand, issued and paid up capital

were remained unchanged. Thus, it can be said that the company is not completely dependent on

the raising funds from public. Whatever the funds required, it raises from borrowings.

c) Discussing the importance of minimizing cost of capital

Since cost of capital is that required of return, which is used for capital budgeting project, it

becomes important to minimize cost of capital, because high cost of capital will tend to increase

cost of capital budgeting like rise in cost of making plants, buildings, etc. (Dhaliwal et al. 2014).

However, lower cost of capital will allow only required cost of budgeting, unnecessary cost will

be abandoned. Thus, it is very important to minimize cost of capital. The importance is described

below.

Due to minimizing cost of capital, required rate of return will increase and internal rate of return

will also increase. But due to reduction in the value of 1 dollar every year, rate of dividend will

remain same but net present value will increase in future. For example,

NPV at 10% discount rate = $ 18,372

Since NPV is greater than zero we have to increase discount rate, thus

NPV at 13% discount rate = $ 4,521

But, it is still greater than zero, discount rate must further be increased, thus

NPV at 14% discount rate = $204

NPV at 15% discount rate = ($3,975)

Since NPV is fairly close to zero at 14% value of (r), therefore

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING AND FINANCE 10

IRR≈14%

Table 2: Computation of IRR

(Source: self-created)

d) Recommending the firm, the ways in which it can lower its cost of capital and adopt

alternative capital structure

There are many ways for minimizing cost of capital

Level of interest rates: The level of interest rate affects the cost of capital because if interest

rates increase, the cost of capital will also increase so the company APN outdoor group should

borrow loan at very low interest which minimizes the cost of capital.

Capital structure policy: The company APN outdoor group must have control over its capital

structure. If it raises huge funds by issuing preference shares or by borrowing loans, it must pay

dividend if the company earns profit. However, if the company earns losses, it must pay interest.

Thus, the company must make correct decision before raise funds from these sources.

Tax rates: If tax rates increase, cost of capital will also increase. So, for minimizing cost of

capital, company should decrease cost of production.

Investment policy: APN Outdoor group should invest practically, for example, if APO invest in

low cost project, it may save investment cost, but the return will not be satisfactory. On the other

hand, the investment in superior project may attract higher investment cost, but it will give

higher rate of return.

Conclusion

It has been found from above discussion that the company APN outdoor group has taken

borrowing in the year 2016 for its current project. APN Outdoor group Limited(APO) is one of

the greatest outdoor advertising operator in Australia and in New Zealand. Company is

performing well in the last five years. This company mainly focuses on wealth maximization

tools. According to the annual report of 2016, 2015 and 2014 it has been found that, APN

outdoor group has increased its internal rate of return and got positive net present value.

IRR≈14%

Table 2: Computation of IRR

(Source: self-created)

d) Recommending the firm, the ways in which it can lower its cost of capital and adopt

alternative capital structure

There are many ways for minimizing cost of capital

Level of interest rates: The level of interest rate affects the cost of capital because if interest

rates increase, the cost of capital will also increase so the company APN outdoor group should

borrow loan at very low interest which minimizes the cost of capital.

Capital structure policy: The company APN outdoor group must have control over its capital

structure. If it raises huge funds by issuing preference shares or by borrowing loans, it must pay

dividend if the company earns profit. However, if the company earns losses, it must pay interest.

Thus, the company must make correct decision before raise funds from these sources.

Tax rates: If tax rates increase, cost of capital will also increase. So, for minimizing cost of

capital, company should decrease cost of production.

Investment policy: APN Outdoor group should invest practically, for example, if APO invest in

low cost project, it may save investment cost, but the return will not be satisfactory. On the other

hand, the investment in superior project may attract higher investment cost, but it will give

higher rate of return.

Conclusion

It has been found from above discussion that the company APN outdoor group has taken

borrowing in the year 2016 for its current project. APN Outdoor group Limited(APO) is one of

the greatest outdoor advertising operator in Australia and in New Zealand. Company is

performing well in the last five years. This company mainly focuses on wealth maximization

tools. According to the annual report of 2016, 2015 and 2014 it has been found that, APN

outdoor group has increased its internal rate of return and got positive net present value.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCE 11

References

APO.AU Stock Price & News - APN Outdoor Group Ltd. - Wall Street Journal.

(2017). Quotes.wsj.com. Retrieved on 17 September 2017, from

http://quotes.wsj.com/AU/XASX/APO

APO.AX: Summary for APNOUTDOOR FPO - Yahoo Finance. (2017). Au.finance.yahoo.com.

Retrieved 17 September 2017, from https://au.finance.yahoo.com/quote/APO.AX?

p=APO.AX

Baur, D. G., & Miyakawa, I. (2014). No puzzle: The foreign exchange exposure of Australian

firms. International Review of Financial Analysis, 32, 13-22.

Becker, B., & Ivashina, V. (2015). Reaching for yield in the bond market. The Journal of

Finance, 70(5), 1863-1902.

Dhaliwal, D., Li, O. Z., Tsang, A., & Yang, Y. G. (2014). Corporate social responsibility

disclosure and the cost of equity capital: The roles of stakeholder orientation and

financial transparency. Journal of Accounting and Public Policy, 33(4), 328-355.

Grant, R. M. (2016). Contemporary Strategy Analysis Text Only. John Wiley & Sons.

Hope, W., & Myllylahti, M. (2013). Financialisation of media ownership in New Zealand. New

Zealand Sociology, 28(3), 192.

Jones, T. M., & Felps, W. (2013). Shareholder wealth maximization and social welfare: A

utilitarian critique. Business Ethics Quarterly, 23(2), 207-238.

Robb, A. M., & Robinson, D. T. (2014). The capital structure decisions of new firms. The

Review of Financial Studies, 27(1), 153-179.

References

APO.AU Stock Price & News - APN Outdoor Group Ltd. - Wall Street Journal.

(2017). Quotes.wsj.com. Retrieved on 17 September 2017, from

http://quotes.wsj.com/AU/XASX/APO

APO.AX: Summary for APNOUTDOOR FPO - Yahoo Finance. (2017). Au.finance.yahoo.com.

Retrieved 17 September 2017, from https://au.finance.yahoo.com/quote/APO.AX?

p=APO.AX

Baur, D. G., & Miyakawa, I. (2014). No puzzle: The foreign exchange exposure of Australian

firms. International Review of Financial Analysis, 32, 13-22.

Becker, B., & Ivashina, V. (2015). Reaching for yield in the bond market. The Journal of

Finance, 70(5), 1863-1902.

Dhaliwal, D., Li, O. Z., Tsang, A., & Yang, Y. G. (2014). Corporate social responsibility

disclosure and the cost of equity capital: The roles of stakeholder orientation and

financial transparency. Journal of Accounting and Public Policy, 33(4), 328-355.

Grant, R. M. (2016). Contemporary Strategy Analysis Text Only. John Wiley & Sons.

Hope, W., & Myllylahti, M. (2013). Financialisation of media ownership in New Zealand. New

Zealand Sociology, 28(3), 192.

Jones, T. M., & Felps, W. (2013). Shareholder wealth maximization and social welfare: A

utilitarian critique. Business Ethics Quarterly, 23(2), 207-238.

Robb, A. M., & Robinson, D. T. (2014). The capital structure decisions of new firms. The

Review of Financial Studies, 27(1), 153-179.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.