BBA Thesis: Financial Performance of Bank Asia Limited

VerifiedAdded on 2022/02/19

|27

|4179

|19

Report

AI Summary

This thesis report presents a comprehensive analysis of the financial performance of Bank Asia Limited, a leading private commercial bank in Bangladesh. The report, submitted to the University of Development Alternative (UODA), covers the period from 2014 to 2018 and examines various financial aspects, including export & import, capital structure, assets, loans, investments, and non-performing loans. Key financial ratios such as Return on Assets (ROA), Return on Equity (ROE), Debt to Equity Ratio, and Earnings per Share (EPS) are analyzed to assess the bank's profitability, efficiency, and financial health. The report also includes an overview of the banking sector in Bangladesh, the objectives of the study, and findings based on the analysis of the bank's financial data. The report concludes with an overview of the bank's performance and provides valuable insights into its financial standing.

1 | P a g e

UNIVERSITY OF DEVELOPMENT ALTERNATIVE (UODA)

THESIS REPORT

A STUDY ON

Financial Performance of Bank Asia Limited

SUBMITTED TO:

THE DEAN

FACULTY OF BUSINESS ADMINISTRATION

SUPERVISED BY:

MR. SIDDIQUE HAYAT KHAN

ASSOCIATE PROFESSOR

SUBMITTED BY:

RAKIB HOSSAIN

BBA 53 BATCH, MAJOR FINANCE

STUDENT ID: 021163034

FACULTY OF BUSINESS ADMINISTRATION

BBA PROGRAM

UNIVERSITY OF DEVELOPMENT ALTERNATIVE (UODA)

DATE:

SEPTEMBER 12, 2020

UNIVERSITY OF DEVELOPMENT ALTERNATIVE (UODA)

THESIS REPORT

A STUDY ON

Financial Performance of Bank Asia Limited

SUBMITTED TO:

THE DEAN

FACULTY OF BUSINESS ADMINISTRATION

SUPERVISED BY:

MR. SIDDIQUE HAYAT KHAN

ASSOCIATE PROFESSOR

SUBMITTED BY:

RAKIB HOSSAIN

BBA 53 BATCH, MAJOR FINANCE

STUDENT ID: 021163034

FACULTY OF BUSINESS ADMINISTRATION

BBA PROGRAM

UNIVERSITY OF DEVELOPMENT ALTERNATIVE (UODA)

DATE:

SEPTEMBER 12, 2020

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2 | P a g e

Letter of Transmittal

12-sep-2020

The Dean

Faculty of Business Administration

University of Development Alternative (UODA)

Subject: Submission of thesis on “Financial Performance of Bank Asia Limited”.

Dear Sir,

With due respect, I would like to state that I have completed a thesis with my honest and maximum effort

that fulfills partial requirements of Bachelor of Business Administration Degree. I have prepared this

report on the basis of my on Bank Asia Limited. It is a great pleasure for me to present you this report

under the heading of “Financial performance”. I enjoy preparing this report, which enriched my partial

knowledge of the theoretical concept. Under the supervision of Mr. Siddique Hayat Khan.

I would like to thanks you for giving me such a great job and opportunity like this to prove my ability in

making a quality report. Therefore, I sincerely hope that you would be kind enough to accept my report for

assessment and oblige thereby.

Thanking you for your kind supervisions.

Sincerely yours,

Rakib Hossain

Batch # 53rd

Std. ID # 021163034

University of Development Alternative

Letter of Transmittal

12-sep-2020

The Dean

Faculty of Business Administration

University of Development Alternative (UODA)

Subject: Submission of thesis on “Financial Performance of Bank Asia Limited”.

Dear Sir,

With due respect, I would like to state that I have completed a thesis with my honest and maximum effort

that fulfills partial requirements of Bachelor of Business Administration Degree. I have prepared this

report on the basis of my on Bank Asia Limited. It is a great pleasure for me to present you this report

under the heading of “Financial performance”. I enjoy preparing this report, which enriched my partial

knowledge of the theoretical concept. Under the supervision of Mr. Siddique Hayat Khan.

I would like to thanks you for giving me such a great job and opportunity like this to prove my ability in

making a quality report. Therefore, I sincerely hope that you would be kind enough to accept my report for

assessment and oblige thereby.

Thanking you for your kind supervisions.

Sincerely yours,

Rakib Hossain

Batch # 53rd

Std. ID # 021163034

University of Development Alternative

3 | P a g e

Declaration

I am Rakib Hossain, hereby declare that the thesis titled “Financial Performance of Bank Asia

Limited” is uniquely prepared by my own efforts after the completion of three months works on

Bank Asia Limited. This report is a record of extensive research work under the supervision and

guidance of Mr. Siddique Hayat Khan, University of Development Alternative (UODA) .

I confirm that, the report is only prepared for only my academic requirement not for other purpose. I also

assure that this internship report is not submitted anywhere of Bangladesh before me.

Batch # 53rd

Std.ID # 021162034

University of Development Alternative (UODA)

Declaration

I am Rakib Hossain, hereby declare that the thesis titled “Financial Performance of Bank Asia

Limited” is uniquely prepared by my own efforts after the completion of three months works on

Bank Asia Limited. This report is a record of extensive research work under the supervision and

guidance of Mr. Siddique Hayat Khan, University of Development Alternative (UODA) .

I confirm that, the report is only prepared for only my academic requirement not for other purpose. I also

assure that this internship report is not submitted anywhere of Bangladesh before me.

Batch # 53rd

Std.ID # 021162034

University of Development Alternative (UODA)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4 | P a g e

Executive Summary

In this report the financial performance of Bank Asia Ltd. has been analyzed. It has been one of the

leading private commercial banks in Bangladesh and also doing really well over past few years. At the

beginning of the report, a precise. At the beginning of the report, a precise Introduction, Objective of

report and Fact/ Summaries Information. In addition, the ratio analysis has been done of last five years

performance which will help to understand the current as well as past performance of Bank Asia Ltd. .

After that I want to show that export & Import , Authorized capital, Paid-up capital, Core (Tier 1) capital,

Supplementary (Tier 2) capital, Total capital (Tier 1 and Tier 2), Total risk weighted assets, Tier 1 capital

to risk-weighted asset ratio (%),Tier 2 capital to risk-weighted asset ratio (%),Number of share

outstanding, Deposits, Assets, Loans and Advances, Investments, Non-performing loans/assets

(NPL/NPA),Provisions, Classified loan. I have mentioned about some findings of this Bank.

Executive Summary

In this report the financial performance of Bank Asia Ltd. has been analyzed. It has been one of the

leading private commercial banks in Bangladesh and also doing really well over past few years. At the

beginning of the report, a precise. At the beginning of the report, a precise Introduction, Objective of

report and Fact/ Summaries Information. In addition, the ratio analysis has been done of last five years

performance which will help to understand the current as well as past performance of Bank Asia Ltd. .

After that I want to show that export & Import , Authorized capital, Paid-up capital, Core (Tier 1) capital,

Supplementary (Tier 2) capital, Total capital (Tier 1 and Tier 2), Total risk weighted assets, Tier 1 capital

to risk-weighted asset ratio (%),Tier 2 capital to risk-weighted asset ratio (%),Number of share

outstanding, Deposits, Assets, Loans and Advances, Investments, Non-performing loans/assets

(NPL/NPA),Provisions, Classified loan. I have mentioned about some findings of this Bank.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5 | P a g e

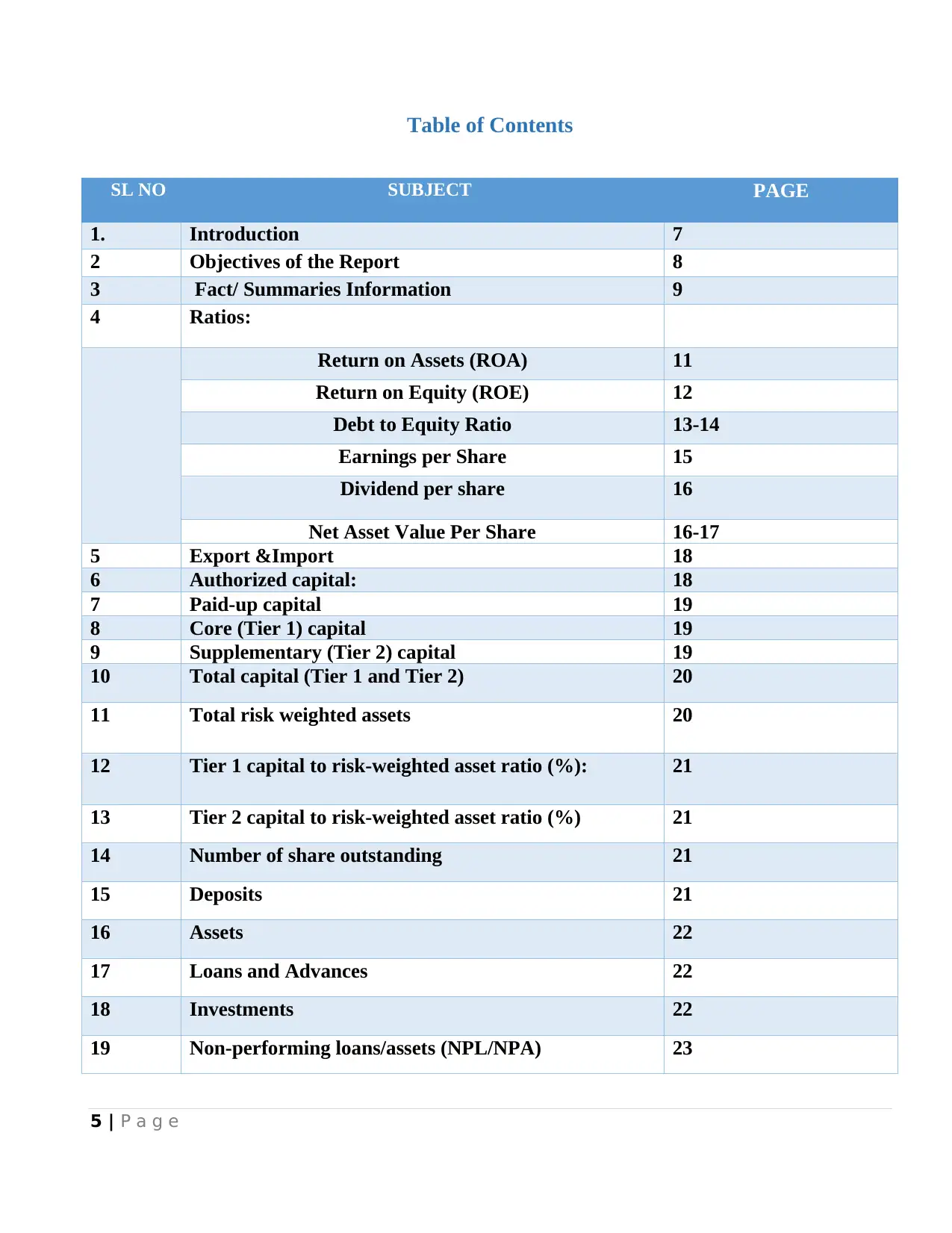

Table of Contents

SL NO SUBJECT PAGE

1. Introduction 7

2 Objectives of the Report 8

3 Fact/ Summaries Information 9

4 Ratios:

Return on Assets (ROA) 11

Return on Equity (ROE) 12

Debt to Equity Ratio 13-14

Earnings per Share 15

Dividend per share 16

Net Asset Value Per Share 16-17

5 Export &Import 18

6 Authorized capital: 18

7 Paid-up capital 19

8 Core (Tier 1) capital 19

9 Supplementary (Tier 2) capital 19

10 Total capital (Tier 1 and Tier 2) 20

11 Total risk weighted assets 20

12 Tier 1 capital to risk-weighted asset ratio (%): 21

13 Tier 2 capital to risk-weighted asset ratio (%) 21

14 Number of share outstanding 21

15 Deposits 21

16 Assets 22

17 Loans and Advances 22

18 Investments 22

19 Non-performing loans/assets (NPL/NPA) 23

Table of Contents

SL NO SUBJECT PAGE

1. Introduction 7

2 Objectives of the Report 8

3 Fact/ Summaries Information 9

4 Ratios:

Return on Assets (ROA) 11

Return on Equity (ROE) 12

Debt to Equity Ratio 13-14

Earnings per Share 15

Dividend per share 16

Net Asset Value Per Share 16-17

5 Export &Import 18

6 Authorized capital: 18

7 Paid-up capital 19

8 Core (Tier 1) capital 19

9 Supplementary (Tier 2) capital 19

10 Total capital (Tier 1 and Tier 2) 20

11 Total risk weighted assets 20

12 Tier 1 capital to risk-weighted asset ratio (%): 21

13 Tier 2 capital to risk-weighted asset ratio (%) 21

14 Number of share outstanding 21

15 Deposits 21

16 Assets 22

17 Loans and Advances 22

18 Investments 22

19 Non-performing loans/assets (NPL/NPA) 23

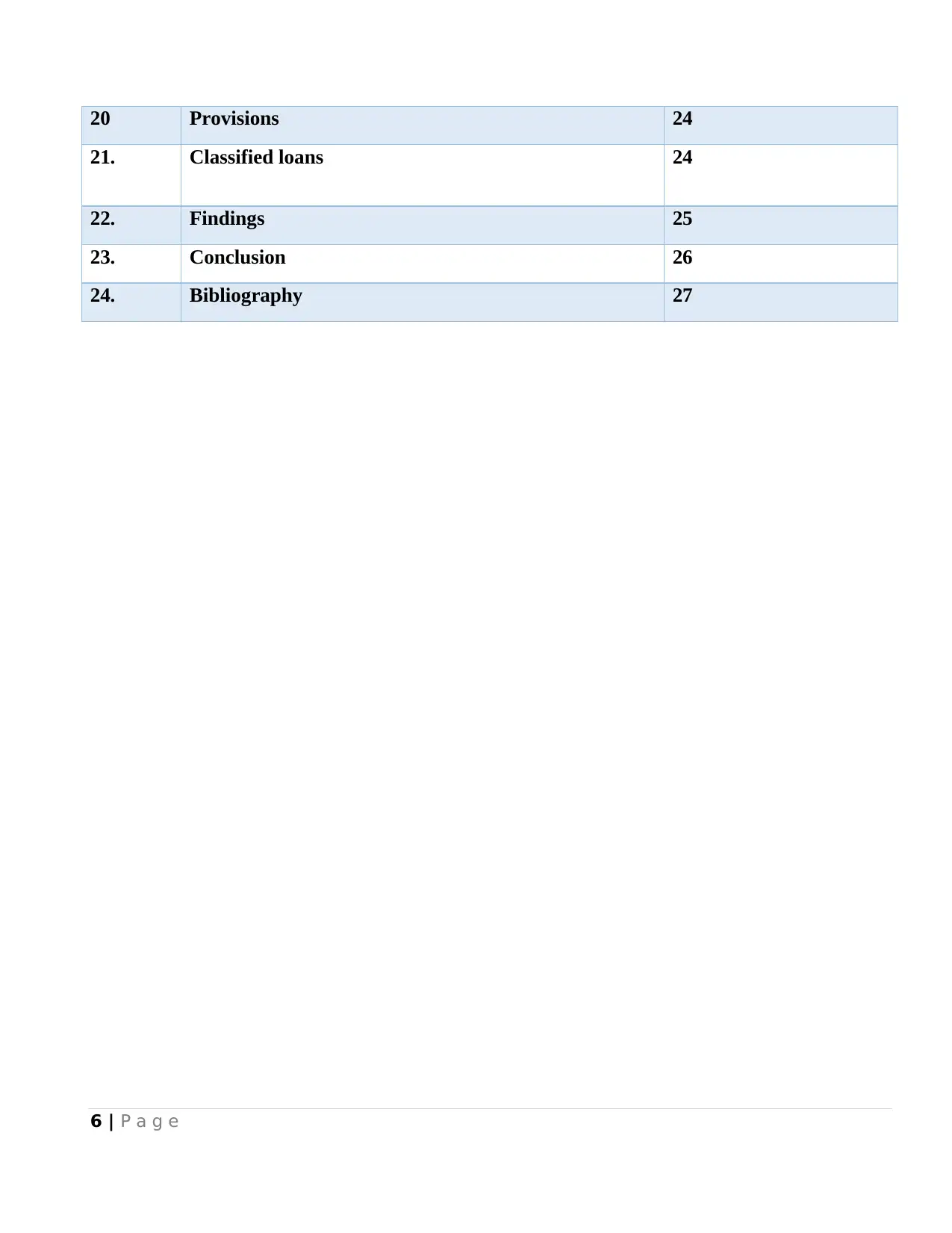

6 | P a g e

20 Provisions 24

21. Classified loans 24

22. Findings 25

23. Conclusion 26

24. Bibliography 27

20 Provisions 24

21. Classified loans 24

22. Findings 25

23. Conclusion 26

24. Bibliography 27

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7 | P a g e

INTRODUCTION

Banks are very old form of financial institution that channel excess funds from surplus unit to

deficit unit in consideration of a price called Interest. The banking sector is dominating the financial

sector of Bangladesh that mobilizes resources for productive investments in a country which in turn

contributes to economic development. Like other countries, banking sector plays a vital role in the

economic development of Bangladesh. To achieve economic development, a sound and efficient

banking systems’ importance can’t be denied. In Bangladesh, this sector has reached to another

level during the last three decades or so, as a result of increased demand of the growing economy.

But in the recent times, the banking sector has been going through several uncertainties which is

very alarming for the economy. Non-performing loan or default loan is the most concerned issues of

the banking sector. Day by day the rate of NPL has been increasing which made the banks very

conscious about granting loans to the customers. Furthermore, siphoning money to other foreign

countries is also a very alarming issue regarding this sector.

INTRODUCTION

Banks are very old form of financial institution that channel excess funds from surplus unit to

deficit unit in consideration of a price called Interest. The banking sector is dominating the financial

sector of Bangladesh that mobilizes resources for productive investments in a country which in turn

contributes to economic development. Like other countries, banking sector plays a vital role in the

economic development of Bangladesh. To achieve economic development, a sound and efficient

banking systems’ importance can’t be denied. In Bangladesh, this sector has reached to another

level during the last three decades or so, as a result of increased demand of the growing economy.

But in the recent times, the banking sector has been going through several uncertainties which is

very alarming for the economy. Non-performing loan or default loan is the most concerned issues of

the banking sector. Day by day the rate of NPL has been increasing which made the banks very

conscious about granting loans to the customers. Furthermore, siphoning money to other foreign

countries is also a very alarming issue regarding this sector.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8 | P a g e

OBJECTIVE OF REPORT

The objectives of the report can be divided into two levels. One is primary objective and the other is

secondary objectives.

The primary objectives of the report are:

• To fulfill one of the requirements of achieving BBA degree.

• To secure good marks on internship report.

• To adapt with the corporate world.

The secondary objectives of the report are:

• To identify their key financial performances for acquiring the knowledge of

operational efficiency of Bank Asia Ltd.

• To obtain a clear concept of banking sector in Bangladesh.

• To get acquainted with the ratios which indicate and measure the performance of

a bank.

OBJECTIVE OF REPORT

The objectives of the report can be divided into two levels. One is primary objective and the other is

secondary objectives.

The primary objectives of the report are:

• To fulfill one of the requirements of achieving BBA degree.

• To secure good marks on internship report.

• To adapt with the corporate world.

The secondary objectives of the report are:

• To identify their key financial performances for acquiring the knowledge of

operational efficiency of Bank Asia Ltd.

• To obtain a clear concept of banking sector in Bangladesh.

• To get acquainted with the ratios which indicate and measure the performance of

a bank.

9 | P a g e

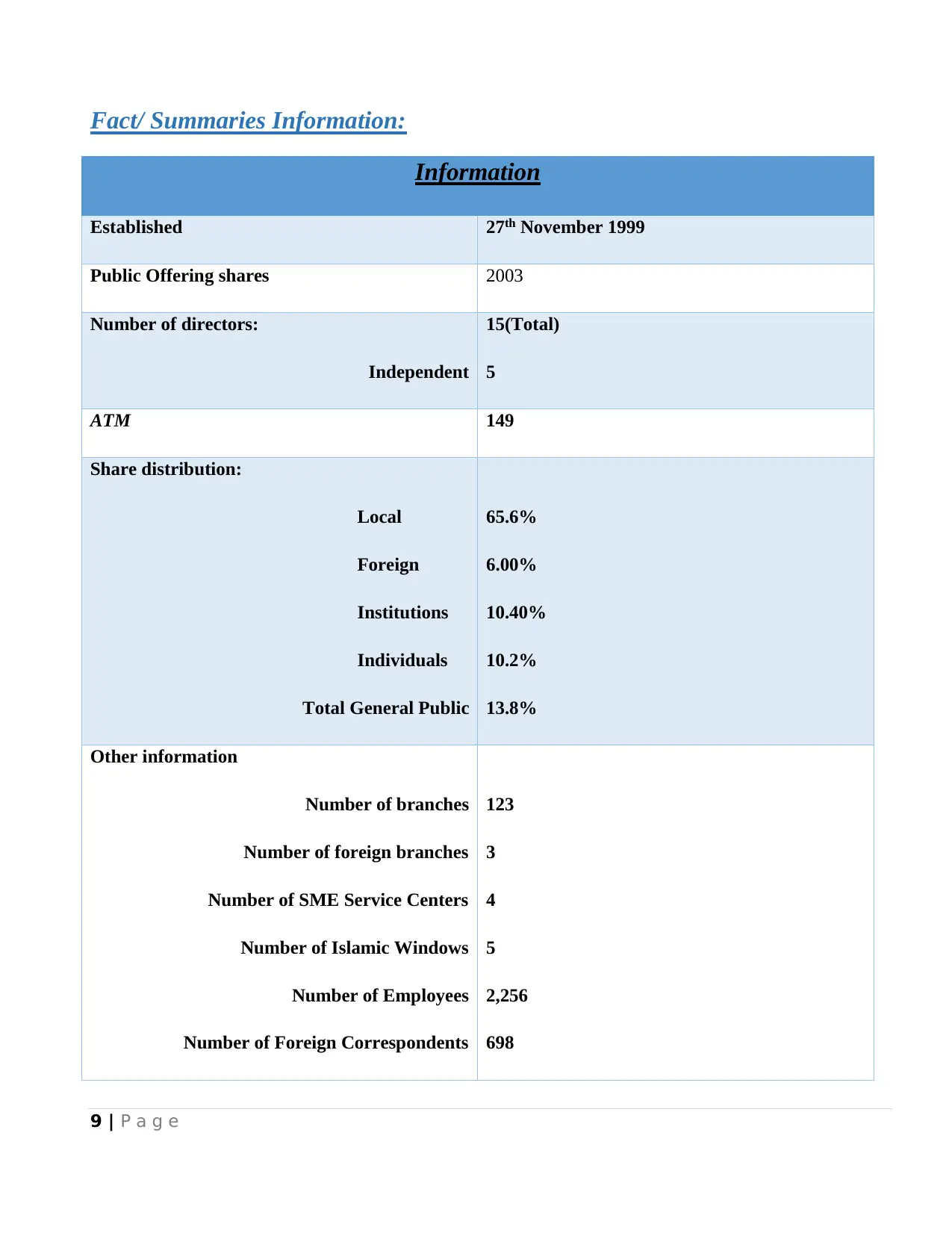

Fact/ Summaries Information:

Information

Established 27th November 1999

Public Offering shares 2003

Number of directors:

Independent

15(Total)

5

ATM 149

Share distribution:

Local

Foreign

Institutions

Individuals

Total General Public

65.6%

6.00%

10.40%

10.2%

13.8%

Other information

Number of branches

Number of foreign branches

Number of SME Service Centers

Number of Islamic Windows

Number of Employees

Number of Foreign Correspondents

123

3

4

5

2,256

698

Fact/ Summaries Information:

Information

Established 27th November 1999

Public Offering shares 2003

Number of directors:

Independent

15(Total)

5

ATM 149

Share distribution:

Local

Foreign

Institutions

Individuals

Total General Public

65.6%

6.00%

10.40%

10.2%

13.8%

Other information

Number of branches

Number of foreign branches

Number of SME Service Centers

Number of Islamic Windows

Number of Employees

Number of Foreign Correspondents

123

3

4

5

2,256

698

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10 | P a g e

Coverage Area District 64

Upazilla 417

SHARES INFORMATION MATRIX:

No. of Shares Outstanding(Million) 1,110.39

Earnings Per Share (Taka) 2.04

Number of Shareholders 10,344.00

Market Value Per Share (Taka) 17.70

Price Earnings Ratio 8.68

Net Asset Value Per Share (Taka) 21.02

Dividend Coverage ratio 2.04

Coverage Area District 64

Upazilla 417

SHARES INFORMATION MATRIX:

No. of Shares Outstanding(Million) 1,110.39

Earnings Per Share (Taka) 2.04

Number of Shareholders 10,344.00

Market Value Per Share (Taka) 17.70

Price Earnings Ratio 8.68

Net Asset Value Per Share (Taka) 21.02

Dividend Coverage ratio 2.04

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11 | P a g e

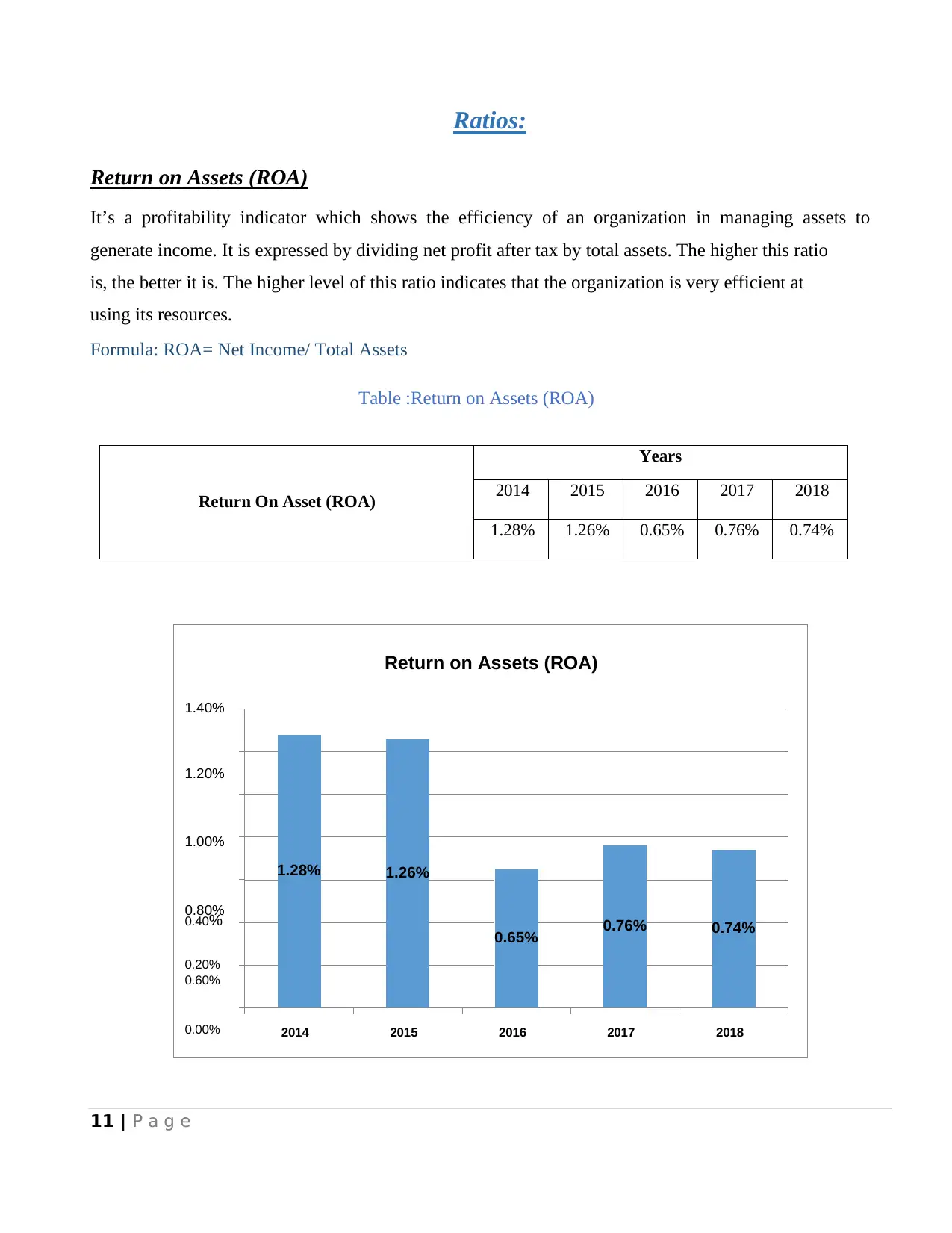

Ratios:

Return on Assets (ROA)

It’s a profitability indicator which shows the efficiency of an organization in managing assets to

generate income. It is expressed by dividing net profit after tax by total assets. The higher this ratio

is, the better it is. The higher level of this ratio indicates that the organization is very efficient at

using its resources.

Formula: ROA= Net Income/ Total Assets

Table :Return on Assets (ROA)

Return On Asset (ROA)

Years

2014 2015 2016 2017 2018

1.28% 1.26% 0.65% 0.76% 0.74%

Return on Assets (ROA)

1.40%

1.20%

1.00%

0.80%

0.60%

1.28% 1.26%

0.40%

0.65% 0.76% 0.74%

0.20%

0.00% 2014 2015 2016 2017 2018

Ratios:

Return on Assets (ROA)

It’s a profitability indicator which shows the efficiency of an organization in managing assets to

generate income. It is expressed by dividing net profit after tax by total assets. The higher this ratio

is, the better it is. The higher level of this ratio indicates that the organization is very efficient at

using its resources.

Formula: ROA= Net Income/ Total Assets

Table :Return on Assets (ROA)

Return On Asset (ROA)

Years

2014 2015 2016 2017 2018

1.28% 1.26% 0.65% 0.76% 0.74%

Return on Assets (ROA)

1.40%

1.20%

1.00%

0.80%

0.60%

1.28% 1.26%

0.40%

0.65% 0.76% 0.74%

0.20%

0.00% 2014 2015 2016 2017 2018

12 | P a g e

Interpretation:

From the above figure we can see that return on asset was in increasing trend from 2014 to 2015.

In 2014 Bank Asia Ltd. Has earned Tk. 1.28 for each taka of assets they have invested. But in

2016 return on asset declines drastically because profit after tax of 2016 was lower than 2014 and

2015 and total asset was higher than 2014 and 2015 and that’s why the return on asset declines. In

2017 it again increased because its profit after tax and total asset increased but in 2018, it slightly

decreased to 0.74% than the previous year.

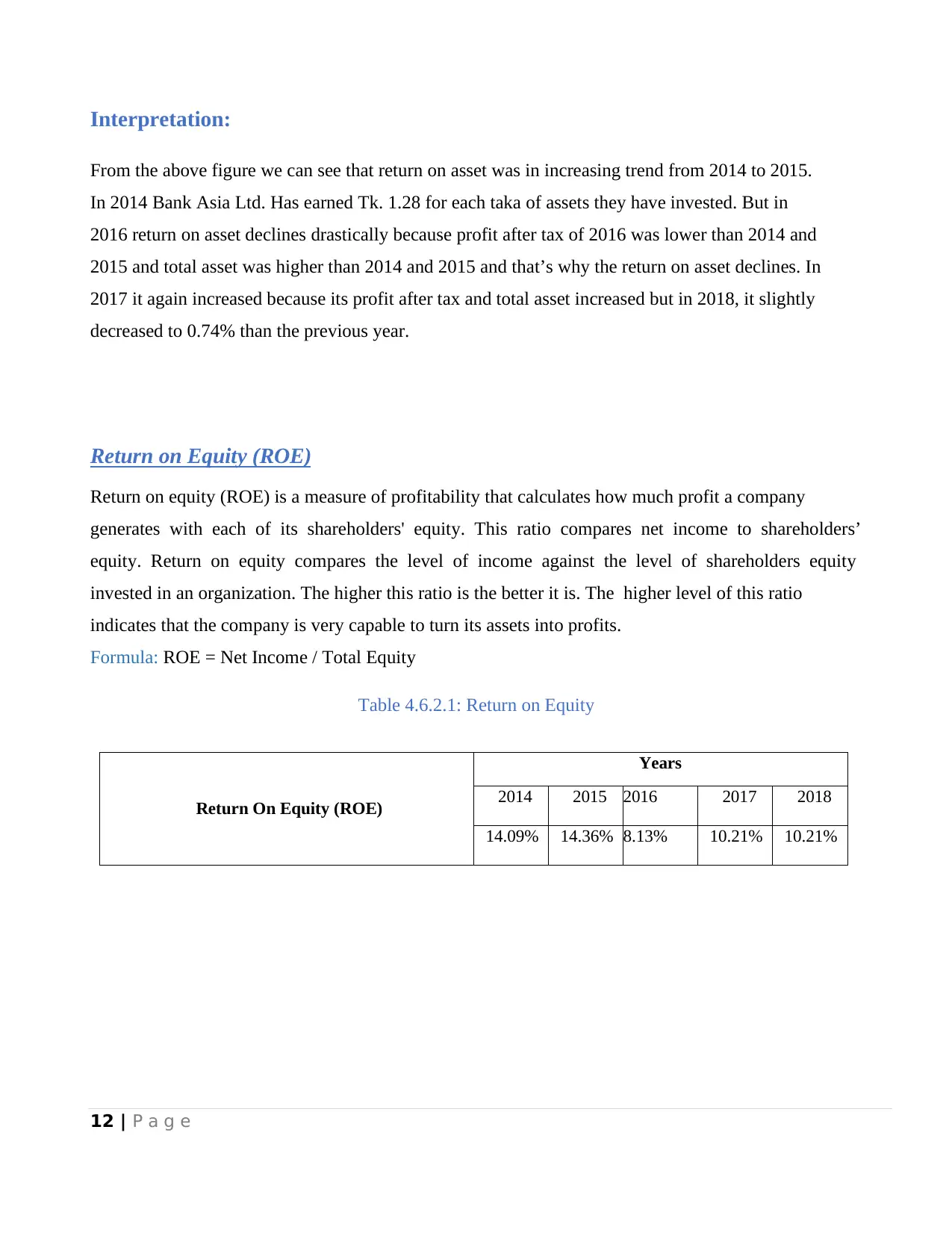

Return on Equity (ROE)

Return on equity (ROE) is a measure of profitability that calculates how much profit a company

generates with each of its shareholders' equity. This ratio compares net income to shareholders’

equity. Return on equity compares the level of income against the level of shareholders equity

invested in an organization. The higher this ratio is the better it is. The higher level of this ratio

indicates that the company is very capable to turn its assets into profits.

Formula: ROE = Net Income / Total Equity

Table 4.6.2.1: Return on Equity

Return On Equity (ROE)

Years

2014 2015 2016 2017 2018

14.09% 14.36% 8.13% 10.21% 10.21%

Interpretation:

From the above figure we can see that return on asset was in increasing trend from 2014 to 2015.

In 2014 Bank Asia Ltd. Has earned Tk. 1.28 for each taka of assets they have invested. But in

2016 return on asset declines drastically because profit after tax of 2016 was lower than 2014 and

2015 and total asset was higher than 2014 and 2015 and that’s why the return on asset declines. In

2017 it again increased because its profit after tax and total asset increased but in 2018, it slightly

decreased to 0.74% than the previous year.

Return on Equity (ROE)

Return on equity (ROE) is a measure of profitability that calculates how much profit a company

generates with each of its shareholders' equity. This ratio compares net income to shareholders’

equity. Return on equity compares the level of income against the level of shareholders equity

invested in an organization. The higher this ratio is the better it is. The higher level of this ratio

indicates that the company is very capable to turn its assets into profits.

Formula: ROE = Net Income / Total Equity

Table 4.6.2.1: Return on Equity

Return On Equity (ROE)

Years

2014 2015 2016 2017 2018

14.09% 14.36% 8.13% 10.21% 10.21%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.