University: Financial Management and Control Report on Bitmap plc

VerifiedAdded on 2023/01/23

|33

|7137

|62

Report

AI Summary

This report presents a comprehensive financial analysis of Bitmap plc, a London-based furniture manufacturer, evaluating its performance over two years. Part A assesses profitability, liquidity, gearing, asset utilization, and investor potential through ratio analysis of the income statement and balance sheet. It also includes an evaluation of the working capital cycle. Part B delves into capital budgeting, applying techniques such as payback period, NPV, and IRR, followed by an evaluation of suitable financing sources. Finally, Part C examines the budgeting process and the interlinking of various budgets within a business. The report provides a detailed assessment of Bitmap plc's financial health and strategic decisions, supported by relevant financial data and calculations.

Running Head: Financial Management and Control

FINANCIAL MANAGEMENT AND

CONTROL

STUDENT NAME

UNIVERSITY NAME

FINANCIAL MANAGEMENT AND

CONTROL

STUDENT NAME

UNIVERSITY NAME

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management and Control

Contents

Part A..........................................................................................................................................................2

Introduction.............................................................................................................................................2

Evaluation of the financial performance of Bitmap plc on the basis of past two year’s financial

statements...............................................................................................................................................3

Asset utilisation:......................................................................................................................................9

Investor’s potential:...............................................................................................................................11

A brief evaluation of Bitmap plc’s working capital cycle........................................................................12

Conclusion:............................................................................................................................................14

Part B.........................................................................................................................................................15

Capital Budgeting Analysis:....................................................................................................................15

Cash-flow details:..............................................................................................................................15

1) The Payback Period...................................................................................................................17

2) The Discounted Payback Period................................................................................................18

3) The Accounting Rate of Return.................................................................................................19

4) The Net Present Value...............................................................................................................21

5) The Internal Rate of Return.......................................................................................................22

Evaluation of different investment appraisal techniques:.....................................................................23

Evaluation of two suitable sources of finance to fund this investment:................................................25

Part C.........................................................................................................................................................27

Budgeting..............................................................................................................................................27

Evaluation of the budgeting process and the interlinking of various budgets used within a business.. 28

References:................................................................................................................................................31

1

Contents

Part A..........................................................................................................................................................2

Introduction.............................................................................................................................................2

Evaluation of the financial performance of Bitmap plc on the basis of past two year’s financial

statements...............................................................................................................................................3

Asset utilisation:......................................................................................................................................9

Investor’s potential:...............................................................................................................................11

A brief evaluation of Bitmap plc’s working capital cycle........................................................................12

Conclusion:............................................................................................................................................14

Part B.........................................................................................................................................................15

Capital Budgeting Analysis:....................................................................................................................15

Cash-flow details:..............................................................................................................................15

1) The Payback Period...................................................................................................................17

2) The Discounted Payback Period................................................................................................18

3) The Accounting Rate of Return.................................................................................................19

4) The Net Present Value...............................................................................................................21

5) The Internal Rate of Return.......................................................................................................22

Evaluation of different investment appraisal techniques:.....................................................................23

Evaluation of two suitable sources of finance to fund this investment:................................................25

Part C.........................................................................................................................................................27

Budgeting..............................................................................................................................................27

Evaluation of the budgeting process and the interlinking of various budgets used within a business.. 28

References:................................................................................................................................................31

1

Financial Management and Control

Part A

Introduction

Bitmap plc is a recognised furniture manufacturer based in London. This report evaluates its

financial performance on the basis of the financial results which the company has posted over the

past two years. Various changes in the key elements of the two most important financial

statements: income statement and balance sheet, will be analysed to evaluate Bitmap’s

performance in relation to profitability, liquidity, gearing, asset utilisation and investors

potential. This evaluation will be done by calculating important financial ratios for the company

and then interpreting the results (Bragg, 2012). This report also includes the calculation and brief

evaluation of the working capital cycle for Bitmap plc.

2

Part A

Introduction

Bitmap plc is a recognised furniture manufacturer based in London. This report evaluates its

financial performance on the basis of the financial results which the company has posted over the

past two years. Various changes in the key elements of the two most important financial

statements: income statement and balance sheet, will be analysed to evaluate Bitmap’s

performance in relation to profitability, liquidity, gearing, asset utilisation and investors

potential. This evaluation will be done by calculating important financial ratios for the company

and then interpreting the results (Bragg, 2012). This report also includes the calculation and brief

evaluation of the working capital cycle for Bitmap plc.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Management and Control

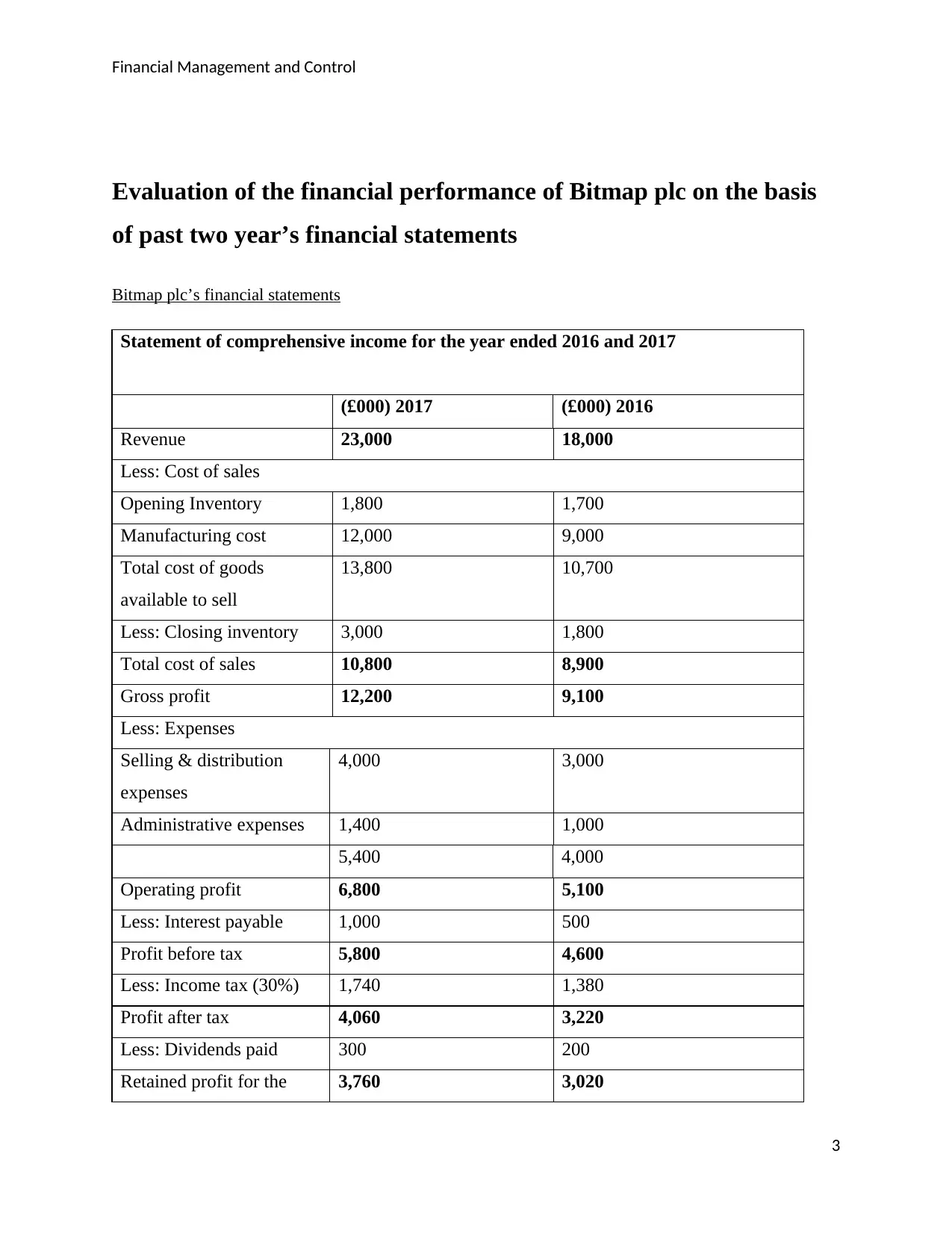

Evaluation of the financial performance of Bitmap plc on the basis

of past two year’s financial statements

Bitmap plc’s financial statements

Statement of comprehensive income for the year ended 2016 and 2017

(£000) 2017 (£000) 2016

Revenue 23,000 18,000

Less: Cost of sales

Opening Inventory 1,800 1,700

Manufacturing cost 12,000 9,000

Total cost of goods

available to sell

13,800 10,700

Less: Closing inventory 3,000 1,800

Total cost of sales 10,800 8,900

Gross profit 12,200 9,100

Less: Expenses

Selling & distribution

expenses

4,000 3,000

Administrative expenses 1,400 1,000

5,400 4,000

Operating profit 6,800 5,100

Less: Interest payable 1,000 500

Profit before tax 5,800 4,600

Less: Income tax (30%) 1,740 1,380

Profit after tax 4,060 3,220

Less: Dividends paid 300 200

Retained profit for the 3,760 3,020

3

Evaluation of the financial performance of Bitmap plc on the basis

of past two year’s financial statements

Bitmap plc’s financial statements

Statement of comprehensive income for the year ended 2016 and 2017

(£000) 2017 (£000) 2016

Revenue 23,000 18,000

Less: Cost of sales

Opening Inventory 1,800 1,700

Manufacturing cost 12,000 9,000

Total cost of goods

available to sell

13,800 10,700

Less: Closing inventory 3,000 1,800

Total cost of sales 10,800 8,900

Gross profit 12,200 9,100

Less: Expenses

Selling & distribution

expenses

4,000 3,000

Administrative expenses 1,400 1,000

5,400 4,000

Operating profit 6,800 5,100

Less: Interest payable 1,000 500

Profit before tax 5,800 4,600

Less: Income tax (30%) 1,740 1,380

Profit after tax 4,060 3,220

Less: Dividends paid 300 200

Retained profit for the 3,760 3,020

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management and Control

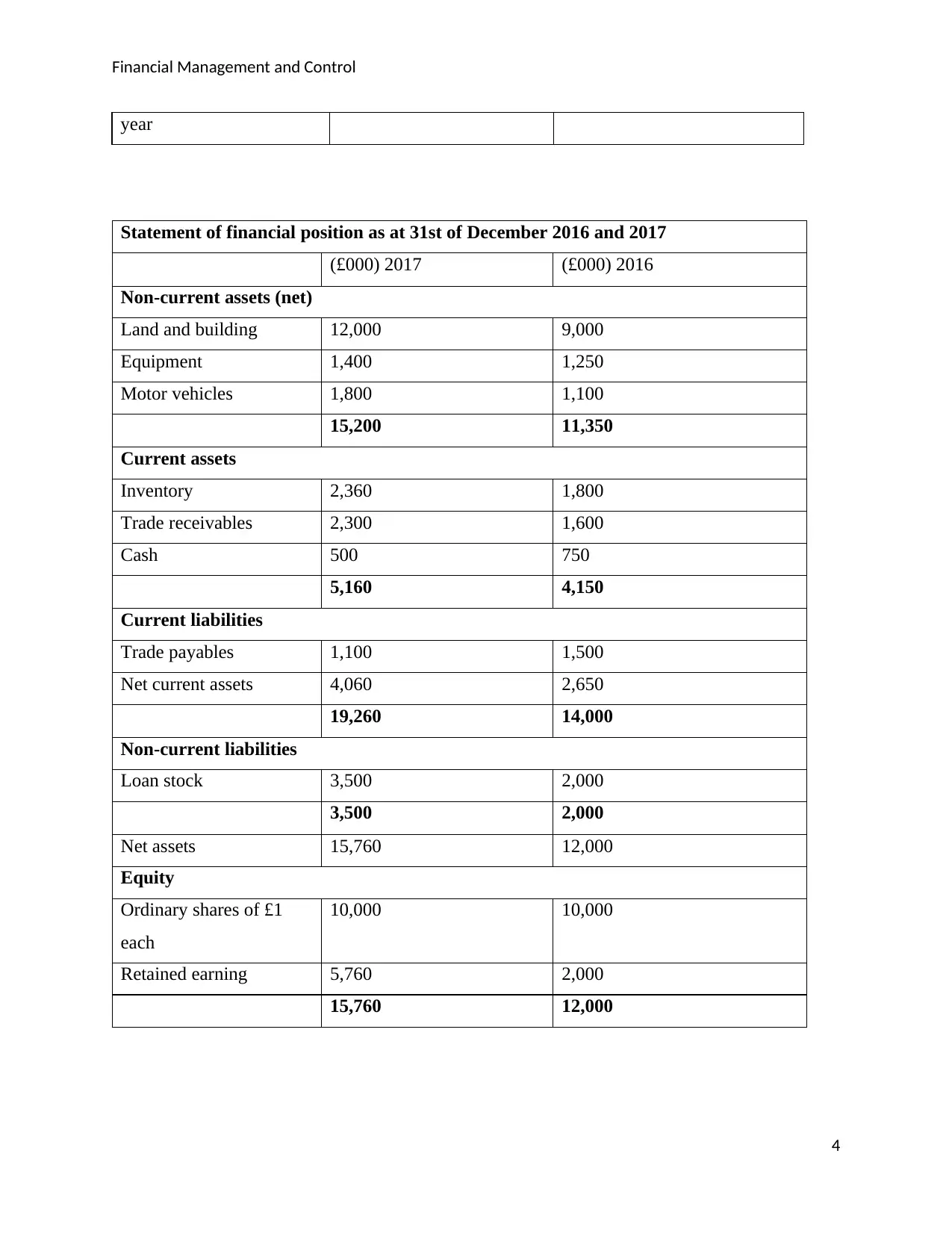

year

Statement of financial position as at 31st of December 2016 and 2017

(£000) 2017 (£000) 2016

Non-current assets (net)

Land and building 12,000 9,000

Equipment 1,400 1,250

Motor vehicles 1,800 1,100

15,200 11,350

Current assets

Inventory 2,360 1,800

Trade receivables 2,300 1,600

Cash 500 750

5,160 4,150

Current liabilities

Trade payables 1,100 1,500

Net current assets 4,060 2,650

19,260 14,000

Non-current liabilities

Loan stock 3,500 2,000

3,500 2,000

Net assets 15,760 12,000

Equity

Ordinary shares of £1

each

10,000 10,000

Retained earning 5,760 2,000

15,760 12,000

4

year

Statement of financial position as at 31st of December 2016 and 2017

(£000) 2017 (£000) 2016

Non-current assets (net)

Land and building 12,000 9,000

Equipment 1,400 1,250

Motor vehicles 1,800 1,100

15,200 11,350

Current assets

Inventory 2,360 1,800

Trade receivables 2,300 1,600

Cash 500 750

5,160 4,150

Current liabilities

Trade payables 1,100 1,500

Net current assets 4,060 2,650

19,260 14,000

Non-current liabilities

Loan stock 3,500 2,000

3,500 2,000

Net assets 15,760 12,000

Equity

Ordinary shares of £1

each

10,000 10,000

Retained earning 5,760 2,000

15,760 12,000

4

Financial Management and Control

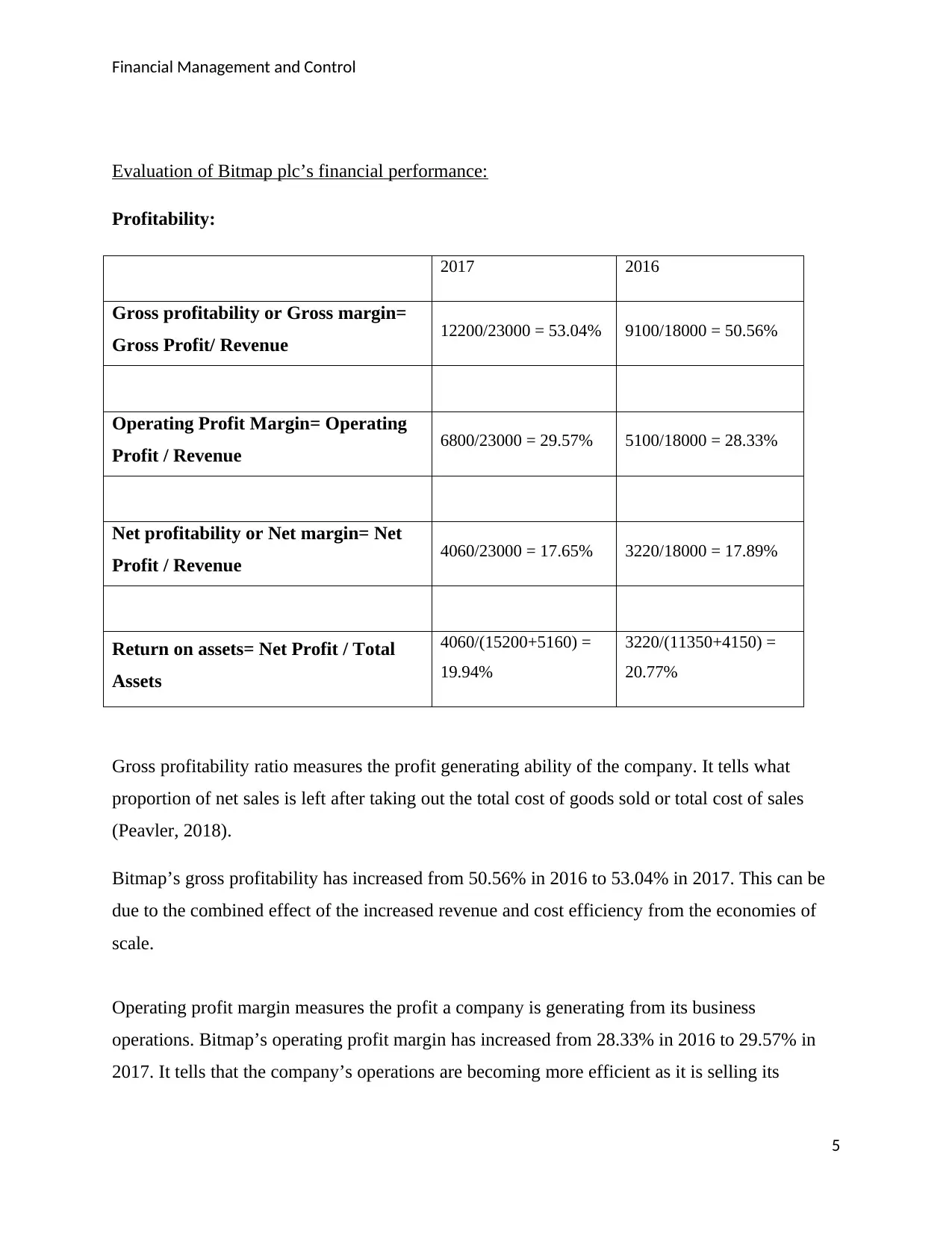

Evaluation of Bitmap plc’s financial performance:

Profitability:

2017 2016

Gross profitability or Gross margin=

Gross Profit/ Revenue 12200/23000 = 53.04% 9100/18000 = 50.56%

Operating Profit Margin= Operating

Profit / Revenue 6800/23000 = 29.57% 5100/18000 = 28.33%

Net profitability or Net margin= Net

Profit / Revenue 4060/23000 = 17.65% 3220/18000 = 17.89%

Return on assets= Net Profit / Total

Assets

4060/(15200+5160) =

19.94%

3220/(11350+4150) =

20.77%

Gross profitability ratio measures the profit generating ability of the company. It tells what

proportion of net sales is left after taking out the total cost of goods sold or total cost of sales

(Peavler, 2018).

Bitmap’s gross profitability has increased from 50.56% in 2016 to 53.04% in 2017. This can be

due to the combined effect of the increased revenue and cost efficiency from the economies of

scale.

Operating profit margin measures the profit a company is generating from its business

operations. Bitmap’s operating profit margin has increased from 28.33% in 2016 to 29.57% in

2017. It tells that the company’s operations are becoming more efficient as it is selling its

5

Evaluation of Bitmap plc’s financial performance:

Profitability:

2017 2016

Gross profitability or Gross margin=

Gross Profit/ Revenue 12200/23000 = 53.04% 9100/18000 = 50.56%

Operating Profit Margin= Operating

Profit / Revenue 6800/23000 = 29.57% 5100/18000 = 28.33%

Net profitability or Net margin= Net

Profit / Revenue 4060/23000 = 17.65% 3220/18000 = 17.89%

Return on assets= Net Profit / Total

Assets

4060/(15200+5160) =

19.94%

3220/(11350+4150) =

20.77%

Gross profitability ratio measures the profit generating ability of the company. It tells what

proportion of net sales is left after taking out the total cost of goods sold or total cost of sales

(Peavler, 2018).

Bitmap’s gross profitability has increased from 50.56% in 2016 to 53.04% in 2017. This can be

due to the combined effect of the increased revenue and cost efficiency from the economies of

scale.

Operating profit margin measures the profit a company is generating from its business

operations. Bitmap’s operating profit margin has increased from 28.33% in 2016 to 29.57% in

2017. It tells that the company’s operations are becoming more efficient as it is selling its

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Management and Control

product in more profitable manner after accounting for all operating expenses.

Net profit margin measures overall profitability, profit the company is making as a proportion of

its sales after considering all types of incomes and expenses. Net profit margin of Bitmap has

decreased slightly from 17.89% in 2016 to 17.65% in 2017. This change can be due to the

increased interest cost from the additional debt which the company has taken for its capital

investments.

Return on assets measures the profit generated by the company’s assets. Bitmap’s return on

assets has decreased from 20.77% in 2016 to 19.94% in 2017.

Year on year increase in company’s net profit in 2017 = (4060-3220)/3220 or 26.08%.

Year on year increase in company’s total assets in 2017 = ((15200+5160) - (11350+4150)) /

(11350+4150) = 31.35%.

Even though the company’s net profit has increased by 26% in 2017 as compared to previous

year but its return on assets has decreased because of the higher year on year increase in its total

assets as the company has been making high capital investments.

Bitmap’s core business has generated higher profits in 2017 but its overall profitability as

measured by net profit margin has decreased due to the company’s decision to increase its capital

investments. It shows that Bitmap has good potential to generate future profits as company is

expanding and its business is doing well.

6

product in more profitable manner after accounting for all operating expenses.

Net profit margin measures overall profitability, profit the company is making as a proportion of

its sales after considering all types of incomes and expenses. Net profit margin of Bitmap has

decreased slightly from 17.89% in 2016 to 17.65% in 2017. This change can be due to the

increased interest cost from the additional debt which the company has taken for its capital

investments.

Return on assets measures the profit generated by the company’s assets. Bitmap’s return on

assets has decreased from 20.77% in 2016 to 19.94% in 2017.

Year on year increase in company’s net profit in 2017 = (4060-3220)/3220 or 26.08%.

Year on year increase in company’s total assets in 2017 = ((15200+5160) - (11350+4150)) /

(11350+4150) = 31.35%.

Even though the company’s net profit has increased by 26% in 2017 as compared to previous

year but its return on assets has decreased because of the higher year on year increase in its total

assets as the company has been making high capital investments.

Bitmap’s core business has generated higher profits in 2017 but its overall profitability as

measured by net profit margin has decreased due to the company’s decision to increase its capital

investments. It shows that Bitmap has good potential to generate future profits as company is

expanding and its business is doing well.

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management and Control

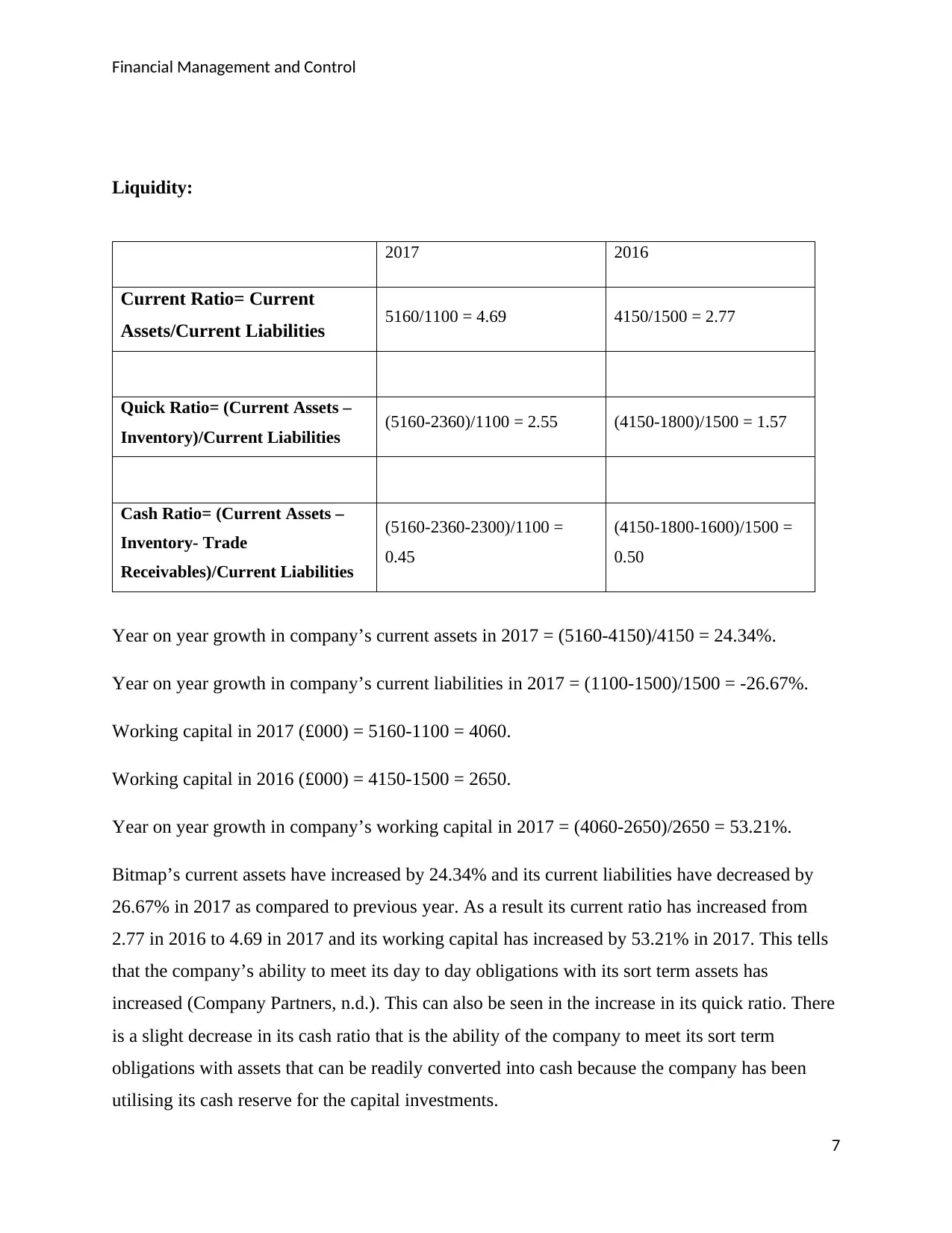

Liquidity:

2017 2016

Current Ratio= Current

Assets/Current Liabilities 5160/1100 = 4.69 4150/1500 = 2.77

Quick Ratio= (Current Assets –

Inventory)/Current Liabilities (5160-2360)/1100 = 2.55 (4150-1800)/1500 = 1.57

Cash Ratio= (Current Assets –

Inventory- Trade

Receivables)/Current Liabilities

(5160-2360-2300)/1100 =

0.45

(4150-1800-1600)/1500 =

0.50

Year on year growth in company’s current assets in 2017 = (5160-4150)/4150 = 24.34%.

Year on year growth in company’s current liabilities in 2017 = (1100-1500)/1500 = -26.67%.

Working capital in 2017 (£000) = 5160-1100 = 4060.

Working capital in 2016 (£000) = 4150-1500 = 2650.

Year on year growth in company’s working capital in 2017 = (4060-2650)/2650 = 53.21%.

Bitmap’s current assets have increased by 24.34% and its current liabilities have decreased by

26.67% in 2017 as compared to previous year. As a result its current ratio has increased from

2.77 in 2016 to 4.69 in 2017 and its working capital has increased by 53.21% in 2017. This tells

that the company’s ability to meet its day to day obligations with its sort term assets has

increased (Company Partners, n.d.). This can also be seen in the increase in its quick ratio. There

is a slight decrease in its cash ratio that is the ability of the company to meet its sort term

obligations with assets that can be readily converted into cash because the company has been

utilising its cash reserve for the capital investments.

7

Liquidity:

2017 2016

Current Ratio= Current

Assets/Current Liabilities 5160/1100 = 4.69 4150/1500 = 2.77

Quick Ratio= (Current Assets –

Inventory)/Current Liabilities (5160-2360)/1100 = 2.55 (4150-1800)/1500 = 1.57

Cash Ratio= (Current Assets –

Inventory- Trade

Receivables)/Current Liabilities

(5160-2360-2300)/1100 =

0.45

(4150-1800-1600)/1500 =

0.50

Year on year growth in company’s current assets in 2017 = (5160-4150)/4150 = 24.34%.

Year on year growth in company’s current liabilities in 2017 = (1100-1500)/1500 = -26.67%.

Working capital in 2017 (£000) = 5160-1100 = 4060.

Working capital in 2016 (£000) = 4150-1500 = 2650.

Year on year growth in company’s working capital in 2017 = (4060-2650)/2650 = 53.21%.

Bitmap’s current assets have increased by 24.34% and its current liabilities have decreased by

26.67% in 2017 as compared to previous year. As a result its current ratio has increased from

2.77 in 2016 to 4.69 in 2017 and its working capital has increased by 53.21% in 2017. This tells

that the company’s ability to meet its day to day obligations with its sort term assets has

increased (Company Partners, n.d.). This can also be seen in the increase in its quick ratio. There

is a slight decrease in its cash ratio that is the ability of the company to meet its sort term

obligations with assets that can be readily converted into cash because the company has been

utilising its cash reserve for the capital investments.

7

Financial Management and Control

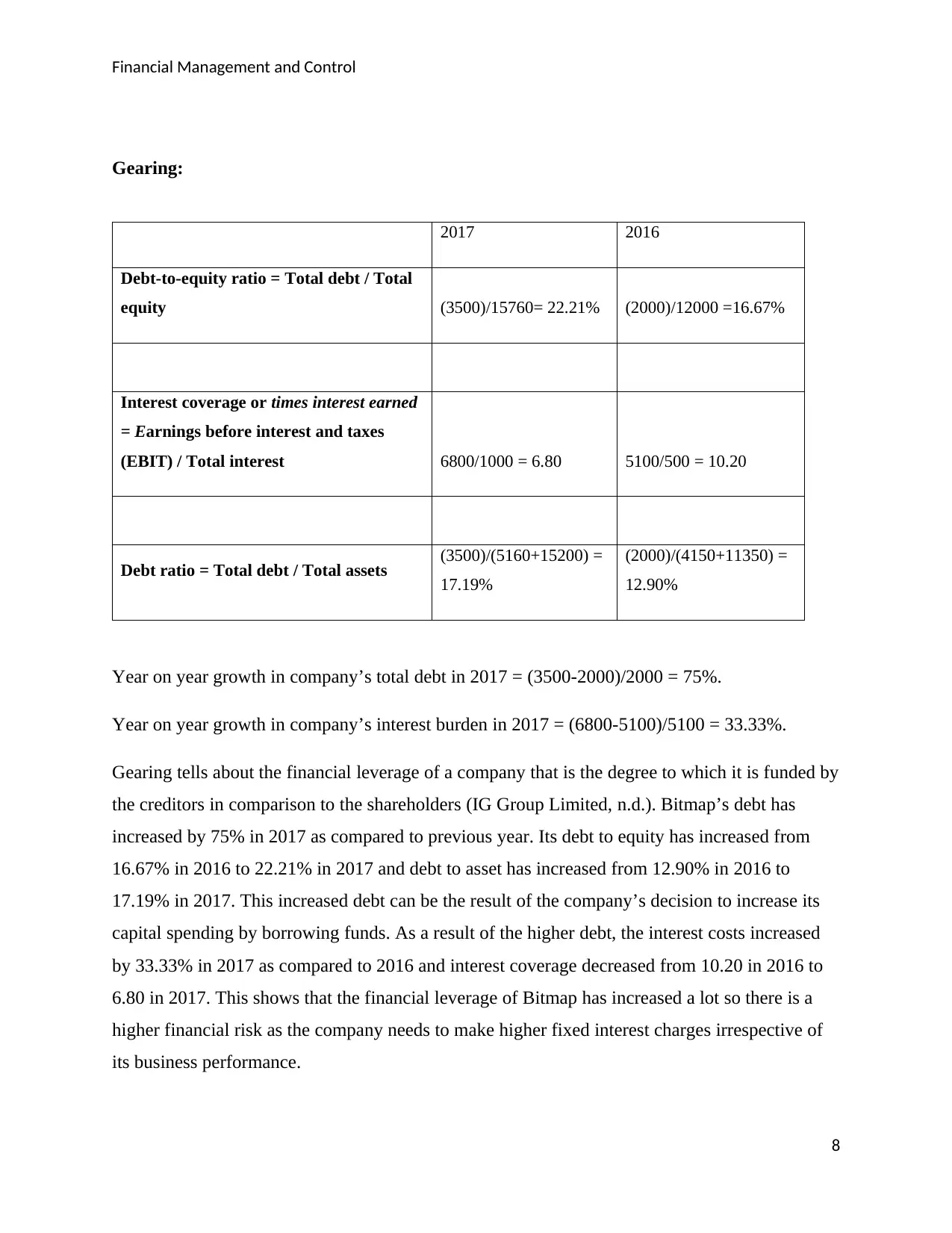

Gearing:

2017 2016

Debt-to-equity ratio = Total debt / Total

equity (3500)/15760= 22.21% (2000)/12000 =16.67%

Interest coverage or times interest earned

= Earnings before interest and taxes

(EBIT) / Total interest 6800/1000 = 6.80 5100/500 = 10.20

Debt ratio = Total debt / Total assets (3500)/(5160+15200) =

17.19%

(2000)/(4150+11350) =

12.90%

Year on year growth in company’s total debt in 2017 = (3500-2000)/2000 = 75%.

Year on year growth in company’s interest burden in 2017 = (6800-5100)/5100 = 33.33%.

Gearing tells about the financial leverage of a company that is the degree to which it is funded by

the creditors in comparison to the shareholders (IG Group Limited, n.d.). Bitmap’s debt has

increased by 75% in 2017 as compared to previous year. Its debt to equity has increased from

16.67% in 2016 to 22.21% in 2017 and debt to asset has increased from 12.90% in 2016 to

17.19% in 2017. This increased debt can be the result of the company’s decision to increase its

capital spending by borrowing funds. As a result of the higher debt, the interest costs increased

by 33.33% in 2017 as compared to 2016 and interest coverage decreased from 10.20 in 2016 to

6.80 in 2017. This shows that the financial leverage of Bitmap has increased a lot so there is a

higher financial risk as the company needs to make higher fixed interest charges irrespective of

its business performance.

8

Gearing:

2017 2016

Debt-to-equity ratio = Total debt / Total

equity (3500)/15760= 22.21% (2000)/12000 =16.67%

Interest coverage or times interest earned

= Earnings before interest and taxes

(EBIT) / Total interest 6800/1000 = 6.80 5100/500 = 10.20

Debt ratio = Total debt / Total assets (3500)/(5160+15200) =

17.19%

(2000)/(4150+11350) =

12.90%

Year on year growth in company’s total debt in 2017 = (3500-2000)/2000 = 75%.

Year on year growth in company’s interest burden in 2017 = (6800-5100)/5100 = 33.33%.

Gearing tells about the financial leverage of a company that is the degree to which it is funded by

the creditors in comparison to the shareholders (IG Group Limited, n.d.). Bitmap’s debt has

increased by 75% in 2017 as compared to previous year. Its debt to equity has increased from

16.67% in 2016 to 22.21% in 2017 and debt to asset has increased from 12.90% in 2016 to

17.19% in 2017. This increased debt can be the result of the company’s decision to increase its

capital spending by borrowing funds. As a result of the higher debt, the interest costs increased

by 33.33% in 2017 as compared to 2016 and interest coverage decreased from 10.20 in 2016 to

6.80 in 2017. This shows that the financial leverage of Bitmap has increased a lot so there is a

higher financial risk as the company needs to make higher fixed interest charges irrespective of

its business performance.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Management and Control

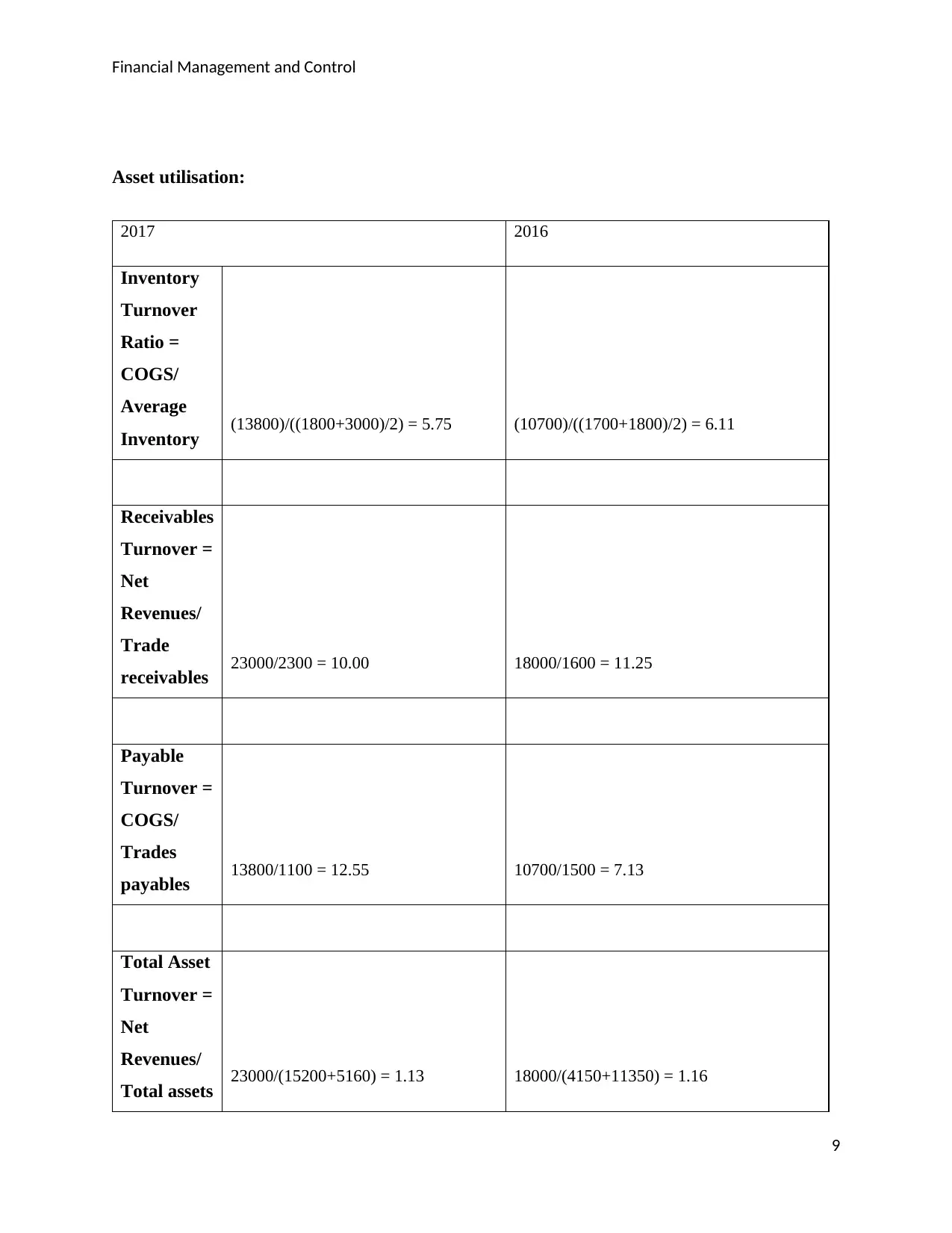

Asset utilisation:

2017 2016

Inventory

Turnover

Ratio =

COGS/

Average

Inventory (13800)/((1800+3000)/2) = 5.75 (10700)/((1700+1800)/2) = 6.11

Receivables

Turnover =

Net

Revenues/

Trade

receivables 23000/2300 = 10.00 18000/1600 = 11.25

Payable

Turnover =

COGS/

Trades

payables 13800/1100 = 12.55 10700/1500 = 7.13

Total Asset

Turnover =

Net

Revenues/

Total assets 23000/(15200+5160) = 1.13 18000/(4150+11350) = 1.16

9

Asset utilisation:

2017 2016

Inventory

Turnover

Ratio =

COGS/

Average

Inventory (13800)/((1800+3000)/2) = 5.75 (10700)/((1700+1800)/2) = 6.11

Receivables

Turnover =

Net

Revenues/

Trade

receivables 23000/2300 = 10.00 18000/1600 = 11.25

Payable

Turnover =

COGS/

Trades

payables 13800/1100 = 12.55 10700/1500 = 7.13

Total Asset

Turnover =

Net

Revenues/

Total assets 23000/(15200+5160) = 1.13 18000/(4150+11350) = 1.16

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management and Control

Year on year growth in company’s trade payables in 2017 = (1100-1500)/1500 = -26.67%.

Year on year growth in company’s trade receivables in 2017 = (2300-1600)/1600 = 43.75%.

Year on year increase in company’s total assets in 2017 = ((15200+5160) - (11350+4150)) /

(11350+4150) = 31.35%.

Year on year growth in company’s revenues in 2017 = (23000-18000)/18000 = 27.78%

Efficiency or asset utilisation ratios tell how efficiently company is using its assets to generate

revenues (Bragg, 2012). Bitmap’s trade receivable turnover ratio decreased from 11.25 in 2016

to 10 in 2017 as its trade receivables have increased a lot in comparison to the increase in the

company’s revenue. This shows that the company is opting for loose credit policies or it is

inefficiently collecting the money from the customers. It can have negative consequences as the

company’s increased revenues might not get converted into cash. Bitmap’s inventory

management can be bit of a problem as its inventory has been increasing at higher pace as

compared to sales, so there is risk of inventory write-down in future. The company’s payables

turnover has increased from 7.13 to 12.55, which can be because of a stricter credit arrangement

from its suppliers and it can cause liquidity issues in future. Bitmap’s total asset turnover has

decreased from 1.16 to 1.13 as the company is expanding and its asset base is rapidly increasing

because of the higher capital investments. Decreasing asset turnover means that the company is

not effectively generating revenues with its assets but this can be because of Bitmap’s decision to

increase its business investment.

10

Year on year growth in company’s trade payables in 2017 = (1100-1500)/1500 = -26.67%.

Year on year growth in company’s trade receivables in 2017 = (2300-1600)/1600 = 43.75%.

Year on year increase in company’s total assets in 2017 = ((15200+5160) - (11350+4150)) /

(11350+4150) = 31.35%.

Year on year growth in company’s revenues in 2017 = (23000-18000)/18000 = 27.78%

Efficiency or asset utilisation ratios tell how efficiently company is using its assets to generate

revenues (Bragg, 2012). Bitmap’s trade receivable turnover ratio decreased from 11.25 in 2016

to 10 in 2017 as its trade receivables have increased a lot in comparison to the increase in the

company’s revenue. This shows that the company is opting for loose credit policies or it is

inefficiently collecting the money from the customers. It can have negative consequences as the

company’s increased revenues might not get converted into cash. Bitmap’s inventory

management can be bit of a problem as its inventory has been increasing at higher pace as

compared to sales, so there is risk of inventory write-down in future. The company’s payables

turnover has increased from 7.13 to 12.55, which can be because of a stricter credit arrangement

from its suppliers and it can cause liquidity issues in future. Bitmap’s total asset turnover has

decreased from 1.16 to 1.13 as the company is expanding and its asset base is rapidly increasing

because of the higher capital investments. Decreasing asset turnover means that the company is

not effectively generating revenues with its assets but this can be because of Bitmap’s decision to

increase its business investment.

10

Financial Management and Control

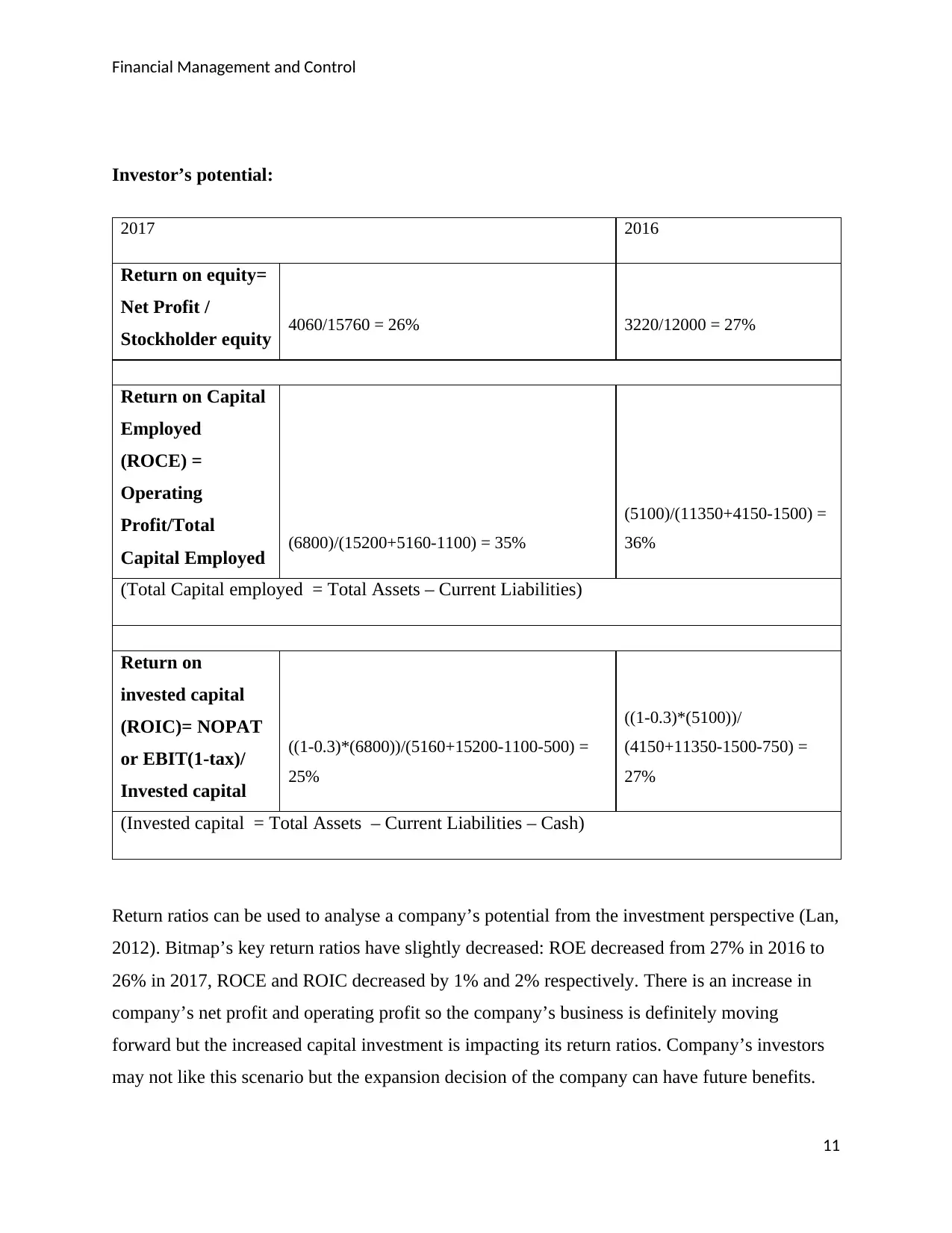

Investor’s potential:

2017 2016

Return on equity=

Net Profit /

Stockholder equity 4060/15760 = 26% 3220/12000 = 27%

Return on Capital

Employed

(ROCE) =

Operating

Profit/Total

Capital Employed (6800)/(15200+5160-1100) = 35%

(5100)/(11350+4150-1500) =

36%

(Total Capital employed = Total Assets – Current Liabilities)

Return on

invested capital

(ROIC)= NOPAT

or EBIT(1-tax)/

Invested capital

((1-0.3)*(6800))/(5160+15200-1100-500) =

25%

((1-0.3)*(5100))/

(4150+11350-1500-750) =

27%

(Invested capital = Total Assets – Current Liabilities – Cash)

Return ratios can be used to analyse a company’s potential from the investment perspective (Lan,

2012). Bitmap’s key return ratios have slightly decreased: ROE decreased from 27% in 2016 to

26% in 2017, ROCE and ROIC decreased by 1% and 2% respectively. There is an increase in

company’s net profit and operating profit so the company’s business is definitely moving

forward but the increased capital investment is impacting its return ratios. Company’s investors

may not like this scenario but the expansion decision of the company can have future benefits.

11

Investor’s potential:

2017 2016

Return on equity=

Net Profit /

Stockholder equity 4060/15760 = 26% 3220/12000 = 27%

Return on Capital

Employed

(ROCE) =

Operating

Profit/Total

Capital Employed (6800)/(15200+5160-1100) = 35%

(5100)/(11350+4150-1500) =

36%

(Total Capital employed = Total Assets – Current Liabilities)

Return on

invested capital

(ROIC)= NOPAT

or EBIT(1-tax)/

Invested capital

((1-0.3)*(6800))/(5160+15200-1100-500) =

25%

((1-0.3)*(5100))/

(4150+11350-1500-750) =

27%

(Invested capital = Total Assets – Current Liabilities – Cash)

Return ratios can be used to analyse a company’s potential from the investment perspective (Lan,

2012). Bitmap’s key return ratios have slightly decreased: ROE decreased from 27% in 2016 to

26% in 2017, ROCE and ROIC decreased by 1% and 2% respectively. There is an increase in

company’s net profit and operating profit so the company’s business is definitely moving

forward but the increased capital investment is impacting its return ratios. Company’s investors

may not like this scenario but the expansion decision of the company can have future benefits.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 33

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.