HI5002 Finance for Business: Caltex Australia Financial Report

VerifiedAdded on 2023/04/03

|22

|4550

|450

Report

AI Summary

This report analyzes the financial performance of Caltex Australia to provide investment recommendations. It includes a detailed financial analysis using profitability ratios, operating efficiency ratios, and cash management techniques. The report also performs sensitivity analysis, identifies systematic and unsystematic risks, and evaluates the company's dividend policy. The analysis covers the period from 2015 to 2018, providing a comprehensive view of Caltex Australia's financial health. The report concludes with a recommendation to a potential investor, based on the overall evaluation of the company's financial position and future prospects. The assignment follows the guidelines of HI5002 Finance for Business, a group assignment, and aims to examine key financial concepts and performance measures.

1

Unit Code: HI5002

Unit Title: Finance for Business

Group Assignment

Unit Code: HI5002

Unit Title: Finance for Business

Group Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Abstract

The report has evaluated the financial performance of Caltex Australia for proving

recommendation to a potential investors regarding investment within the company. The financial

performance has been analyzed with the use of ratio analysis, cash management, and sensitivity

analysis and dividend payout ratio. It is recommended to an investor to hold back the share and

not to invest within the company due to its weak financial position as depicted with ratio

analysis.

Abstract

The report has evaluated the financial performance of Caltex Australia for proving

recommendation to a potential investors regarding investment within the company. The financial

performance has been analyzed with the use of ratio analysis, cash management, and sensitivity

analysis and dividend payout ratio. It is recommended to an investor to hold back the share and

not to invest within the company due to its weak financial position as depicted with ratio

analysis.

3

Contents

Abstract............................................................................................................................................2

Section I: Introduction.....................................................................................................................4

Section II: Detailed financial analysis of Caltex Australia..............................................................4

Section 2.1: Brief description of Caltex Australia...........................................................................4

Section 2.2: Use of ratios to evaluate the performance of Caltex Australia....................................4

Profitability Ratios of Caltex Australia........................................................................................4

Operating Efficiency Ratio..........................................................................................................7

Section 2.3: Use of marketable securities for cash management.....................................................9

Section 2.4: Sensitivity Analysis through using the given data.....................................................10

Section 2.5: Identification and discussion on systematic risk and Unsystematic risk that impacts

the performance of Caltex Australia..............................................................................................16

Systematic Risks associated with Caltex Australia....................................................................16

Unsystematic Risks associated with the Caltex Australia.........................................................16

Section 2.6: Calculation of dividend payout of Caltex Australia for last three years and

interpretation of dividend policy used by Caltex...........................................................................17

Dividend Payout Ratio of Caltex Australia................................................................................17

Section III: Letter of Recommendation to the client.....................................................................19

Section IV: Conclusion..................................................................................................................19

References......................................................................................................................................20

Contents

Abstract............................................................................................................................................2

Section I: Introduction.....................................................................................................................4

Section II: Detailed financial analysis of Caltex Australia..............................................................4

Section 2.1: Brief description of Caltex Australia...........................................................................4

Section 2.2: Use of ratios to evaluate the performance of Caltex Australia....................................4

Profitability Ratios of Caltex Australia........................................................................................4

Operating Efficiency Ratio..........................................................................................................7

Section 2.3: Use of marketable securities for cash management.....................................................9

Section 2.4: Sensitivity Analysis through using the given data.....................................................10

Section 2.5: Identification and discussion on systematic risk and Unsystematic risk that impacts

the performance of Caltex Australia..............................................................................................16

Systematic Risks associated with Caltex Australia....................................................................16

Unsystematic Risks associated with the Caltex Australia.........................................................16

Section 2.6: Calculation of dividend payout of Caltex Australia for last three years and

interpretation of dividend policy used by Caltex...........................................................................17

Dividend Payout Ratio of Caltex Australia................................................................................17

Section III: Letter of Recommendation to the client.....................................................................19

Section IV: Conclusion..................................................................................................................19

References......................................................................................................................................20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Section I: Introduction

The purpose of the assignment is to provide recommendation to an institutional investor

aiming to invest within Australian market by undertaking an analysis of the financial

performance of an ASX listed entity. The ASX listed entity selected for the purpose of

conducting financial evaluation is Caltex Australia, a supplier of transport fuel and convenience

retailing products. The financial evaluation of the selected company has been done by analysis of

its performance ratios such as profitability and operational efficiency. This is followed by

analyzing its cash management and performing sensitivity analysis on the data provided. Also, it

has outlined the systematic and unsystematic risks related with the company and also evaluated

its dividend policy. Lastly, it provides recommendation to a potential investor regarding the

financial health of the company to support the investment decisions on the basis of overall

evaluation carried out. It also includes a conclusions section in the last to summarize the overall

findings generated through the report.

Section II: Detailed financial analysis of Caltex Australia

Section 2.1: Brief description of Caltex Australia

Caltex Australia is a publicly listed ASX company involved in supplying of transport fuel

and also operates as a convenient retailer within Australian market. The core segments of the

company includes purchasing, refining,, distributing and marketing of petroleum based products

and also having its own convenience stores in the country. It has established in period of 1990s

and is regarded to be only fuel based company of Australia that is listed on the ASX. It has

presently attained a distinctive position within the oil and gas sector of the country owing to its

leading position in transporting fuels. It is known to supply about one third of transport fuel

needs within Australian market. The leading position has been attained by the company owning

to its agile supply chain that enables it in providing safe and high quality fuel based products to

its diverse customers such as retail, mining, aviation, agriculture, automotive sector and the

government. It has developed its unique position among all the refiner and marketers in Australia

by conducting its operations in an independent manner and all the decisions are taken by the

management and Board members as it is only publicly listed company. It has the presence of

about 3,500 employees working across the country and is known to be one of the biggest

companies developing attractive job opportunities and supporting the development of

employment sector within the country (Caltex Australia: Our Company, 2018).

Section 2.2: Use of ratios to evaluate the performance of Caltex Australia

Profitability Ratios of Caltex Australia

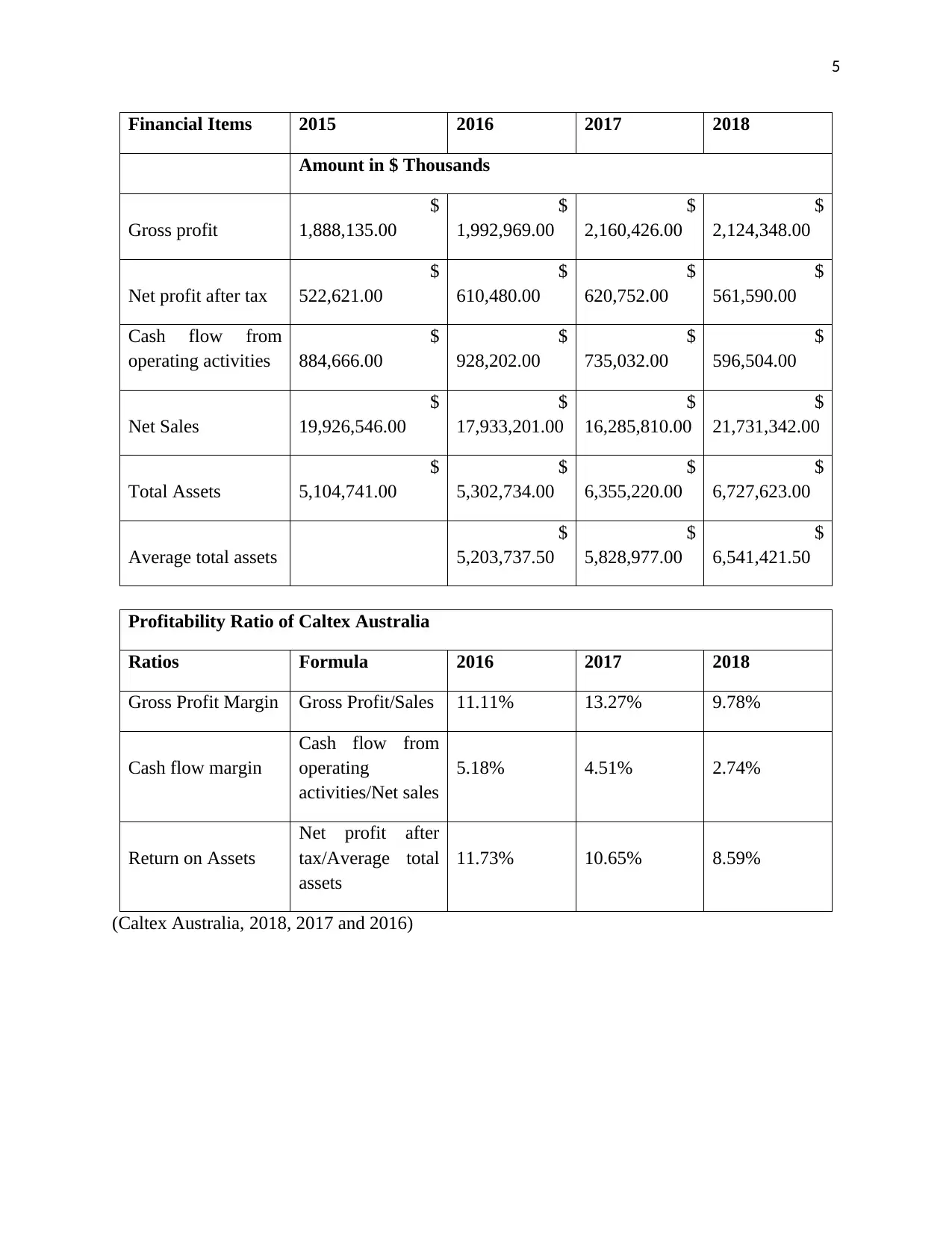

Financial Data of Caltex Australia for calculation of Profitability Ratio

Section I: Introduction

The purpose of the assignment is to provide recommendation to an institutional investor

aiming to invest within Australian market by undertaking an analysis of the financial

performance of an ASX listed entity. The ASX listed entity selected for the purpose of

conducting financial evaluation is Caltex Australia, a supplier of transport fuel and convenience

retailing products. The financial evaluation of the selected company has been done by analysis of

its performance ratios such as profitability and operational efficiency. This is followed by

analyzing its cash management and performing sensitivity analysis on the data provided. Also, it

has outlined the systematic and unsystematic risks related with the company and also evaluated

its dividend policy. Lastly, it provides recommendation to a potential investor regarding the

financial health of the company to support the investment decisions on the basis of overall

evaluation carried out. It also includes a conclusions section in the last to summarize the overall

findings generated through the report.

Section II: Detailed financial analysis of Caltex Australia

Section 2.1: Brief description of Caltex Australia

Caltex Australia is a publicly listed ASX company involved in supplying of transport fuel

and also operates as a convenient retailer within Australian market. The core segments of the

company includes purchasing, refining,, distributing and marketing of petroleum based products

and also having its own convenience stores in the country. It has established in period of 1990s

and is regarded to be only fuel based company of Australia that is listed on the ASX. It has

presently attained a distinctive position within the oil and gas sector of the country owing to its

leading position in transporting fuels. It is known to supply about one third of transport fuel

needs within Australian market. The leading position has been attained by the company owning

to its agile supply chain that enables it in providing safe and high quality fuel based products to

its diverse customers such as retail, mining, aviation, agriculture, automotive sector and the

government. It has developed its unique position among all the refiner and marketers in Australia

by conducting its operations in an independent manner and all the decisions are taken by the

management and Board members as it is only publicly listed company. It has the presence of

about 3,500 employees working across the country and is known to be one of the biggest

companies developing attractive job opportunities and supporting the development of

employment sector within the country (Caltex Australia: Our Company, 2018).

Section 2.2: Use of ratios to evaluate the performance of Caltex Australia

Profitability Ratios of Caltex Australia

Financial Data of Caltex Australia for calculation of Profitability Ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

Financial Items 2015 2016 2017 2018

Amount in $ Thousands

Gross profit

$

1,888,135.00

$

1,992,969.00

$

2,160,426.00

$

2,124,348.00

Net profit after tax

$

522,621.00

$

610,480.00

$

620,752.00

$

561,590.00

Cash flow from

operating activities

$

884,666.00

$

928,202.00

$

735,032.00

$

596,504.00

Net Sales

$

19,926,546.00

$

17,933,201.00

$

16,285,810.00

$

21,731,342.00

Total Assets

$

5,104,741.00

$

5,302,734.00

$

6,355,220.00

$

6,727,623.00

Average total assets

$

5,203,737.50

$

5,828,977.00

$

6,541,421.50

Profitability Ratio of Caltex Australia

Ratios Formula 2016 2017 2018

Gross Profit Margin Gross Profit/Sales 11.11% 13.27% 9.78%

Cash flow margin

Cash flow from

operating

activities/Net sales

5.18% 4.51% 2.74%

Return on Assets

Net profit after

tax/Average total

assets

11.73% 10.65% 8.59%

(Caltex Australia, 2018, 2017 and 2016)

Financial Items 2015 2016 2017 2018

Amount in $ Thousands

Gross profit

$

1,888,135.00

$

1,992,969.00

$

2,160,426.00

$

2,124,348.00

Net profit after tax

$

522,621.00

$

610,480.00

$

620,752.00

$

561,590.00

Cash flow from

operating activities

$

884,666.00

$

928,202.00

$

735,032.00

$

596,504.00

Net Sales

$

19,926,546.00

$

17,933,201.00

$

16,285,810.00

$

21,731,342.00

Total Assets

$

5,104,741.00

$

5,302,734.00

$

6,355,220.00

$

6,727,623.00

Average total assets

$

5,203,737.50

$

5,828,977.00

$

6,541,421.50

Profitability Ratio of Caltex Australia

Ratios Formula 2016 2017 2018

Gross Profit Margin Gross Profit/Sales 11.11% 13.27% 9.78%

Cash flow margin

Cash flow from

operating

activities/Net sales

5.18% 4.51% 2.74%

Return on Assets

Net profit after

tax/Average total

assets

11.73% 10.65% 8.59%

(Caltex Australia, 2018, 2017 and 2016)

6

2016 2017 2018

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

11.11%

13.27%

9.78%

5.18%

4.51%

2.74%

11.73%

10.65%

8.59%

Profitability Ratio of Caltex Australia

Percentage

The profitability of Caltex Australia can be analyzed by using the following ratios.

Gross profit margin: Gross profit margin reveals the money left after paying cost of

goods sold. Gross profit margin indicates financial success and viability of products and

services of the company. It can be said from analyzing the trend of the ratio for the

company over the past three years that gross profit has been improved over the period of

time. Net sales of the company have been decreased in 2015, 2016 and 2017 but in 2018

a boost can be noticed in net sales. In 2017 nets sales was $ 16,285,810.00 that have

increased to $ 21,731,342.00 resulting a decline in the gross profit margin of 3.49%.

Cash flow margin: Operating cash flow margin is a profitability ratio that measures net

operating cash flow from operating activities as a percentage of net sales in a particular

period. Cash flow margin states how efficiently a company is converting its sales in to

cash. A downward trend is noticed on analyzing the last three years data that shows a

drastic fall down in cash flow margin from 5.18% to 2.74%. The reason for such decline

is increase in operating cash outflow as compared to operating cash inflow and increase

in denominator, net sales (Brigham and Michael, 2013).

Return on Assets (ROA): This ratio reveals the percentage of net profit realized by the

company over the use of its assets. It indicates the efficiency of the company in using it

resources to realize net profit. This ratio has stated a downward trend over the past three

2016 2017 2018

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

11.11%

13.27%

9.78%

5.18%

4.51%

2.74%

11.73%

10.65%

8.59%

Profitability Ratio of Caltex Australia

Percentage

The profitability of Caltex Australia can be analyzed by using the following ratios.

Gross profit margin: Gross profit margin reveals the money left after paying cost of

goods sold. Gross profit margin indicates financial success and viability of products and

services of the company. It can be said from analyzing the trend of the ratio for the

company over the past three years that gross profit has been improved over the period of

time. Net sales of the company have been decreased in 2015, 2016 and 2017 but in 2018

a boost can be noticed in net sales. In 2017 nets sales was $ 16,285,810.00 that have

increased to $ 21,731,342.00 resulting a decline in the gross profit margin of 3.49%.

Cash flow margin: Operating cash flow margin is a profitability ratio that measures net

operating cash flow from operating activities as a percentage of net sales in a particular

period. Cash flow margin states how efficiently a company is converting its sales in to

cash. A downward trend is noticed on analyzing the last three years data that shows a

drastic fall down in cash flow margin from 5.18% to 2.74%. The reason for such decline

is increase in operating cash outflow as compared to operating cash inflow and increase

in denominator, net sales (Brigham and Michael, 2013).

Return on Assets (ROA): This ratio reveals the percentage of net profit realized by the

company over the use of its assets. It indicates the efficiency of the company in using it

resources to realize net profit. This ratio has stated a downward trend over the past three

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

years. Return on assets has been declined from 11.73% to 8.59% that shows company has

not been able to use it resources properly. The reason for the same is decreasing profit

and an increase in net sales in the year 2018 (Damodaran, 2011).

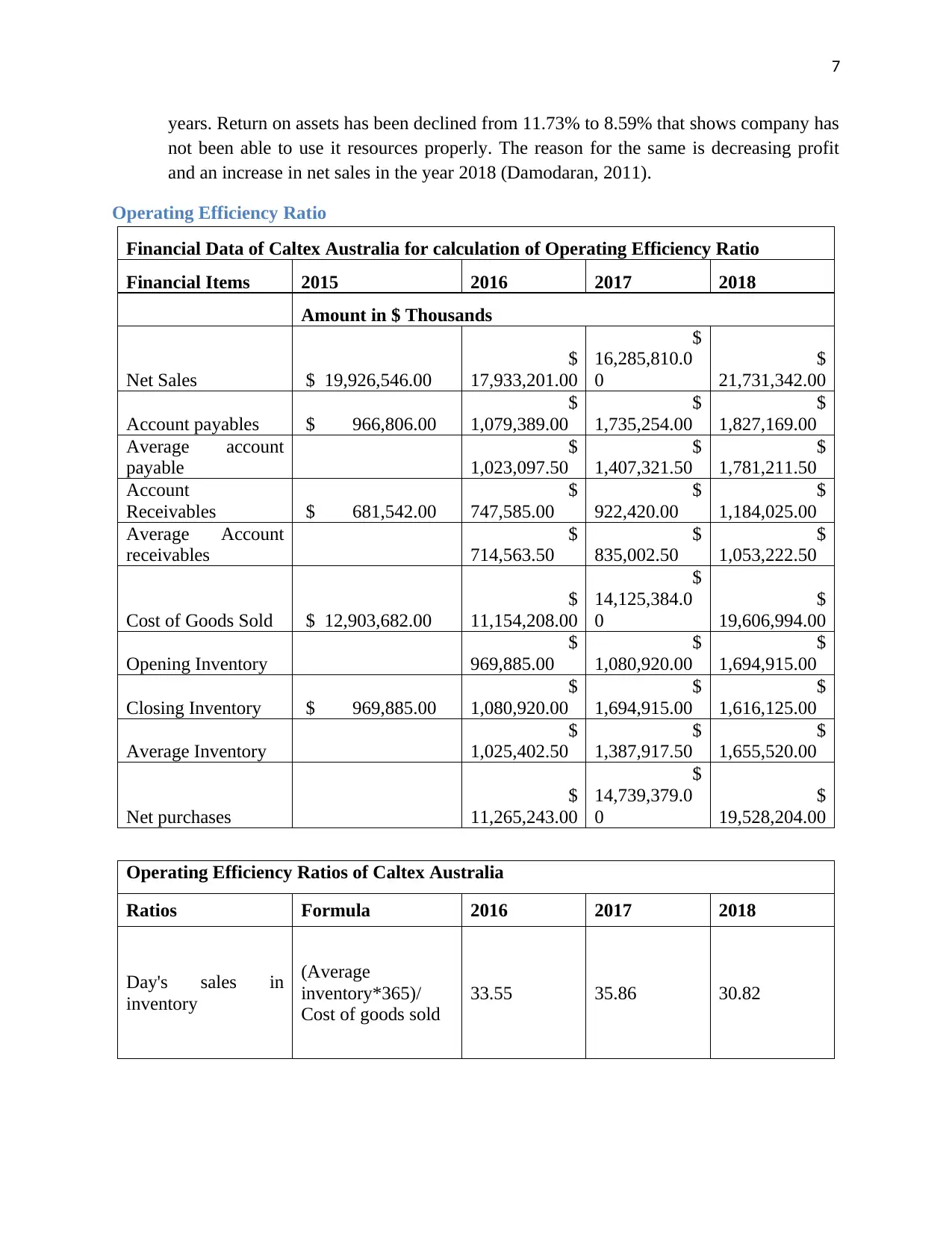

Operating Efficiency Ratio

Financial Data of Caltex Australia for calculation of Operating Efficiency Ratio

Financial Items 2015 2016 2017 2018

Amount in $ Thousands

Net Sales $ 19,926,546.00

$

17,933,201.00

$

16,285,810.0

0

$

21,731,342.00

Account payables $ 966,806.00

$

1,079,389.00

$

1,735,254.00

$

1,827,169.00

Average account

payable

$

1,023,097.50

$

1,407,321.50

$

1,781,211.50

Account

Receivables $ 681,542.00

$

747,585.00

$

922,420.00

$

1,184,025.00

Average Account

receivables

$

714,563.50

$

835,002.50

$

1,053,222.50

Cost of Goods Sold $ 12,903,682.00

$

11,154,208.00

$

14,125,384.0

0

$

19,606,994.00

Opening Inventory

$

969,885.00

$

1,080,920.00

$

1,694,915.00

Closing Inventory $ 969,885.00

$

1,080,920.00

$

1,694,915.00

$

1,616,125.00

Average Inventory

$

1,025,402.50

$

1,387,917.50

$

1,655,520.00

Net purchases

$

11,265,243.00

$

14,739,379.0

0

$

19,528,204.00

Operating Efficiency Ratios of Caltex Australia

Ratios Formula 2016 2017 2018

Day's sales in

inventory

(Average

inventory*365)/

Cost of goods sold

33.55 35.86 30.82

years. Return on assets has been declined from 11.73% to 8.59% that shows company has

not been able to use it resources properly. The reason for the same is decreasing profit

and an increase in net sales in the year 2018 (Damodaran, 2011).

Operating Efficiency Ratio

Financial Data of Caltex Australia for calculation of Operating Efficiency Ratio

Financial Items 2015 2016 2017 2018

Amount in $ Thousands

Net Sales $ 19,926,546.00

$

17,933,201.00

$

16,285,810.0

0

$

21,731,342.00

Account payables $ 966,806.00

$

1,079,389.00

$

1,735,254.00

$

1,827,169.00

Average account

payable

$

1,023,097.50

$

1,407,321.50

$

1,781,211.50

Account

Receivables $ 681,542.00

$

747,585.00

$

922,420.00

$

1,184,025.00

Average Account

receivables

$

714,563.50

$

835,002.50

$

1,053,222.50

Cost of Goods Sold $ 12,903,682.00

$

11,154,208.00

$

14,125,384.0

0

$

19,606,994.00

Opening Inventory

$

969,885.00

$

1,080,920.00

$

1,694,915.00

Closing Inventory $ 969,885.00

$

1,080,920.00

$

1,694,915.00

$

1,616,125.00

Average Inventory

$

1,025,402.50

$

1,387,917.50

$

1,655,520.00

Net purchases

$

11,265,243.00

$

14,739,379.0

0

$

19,528,204.00

Operating Efficiency Ratios of Caltex Australia

Ratios Formula 2016 2017 2018

Day's sales in

inventory

(Average

inventory*365)/

Cost of goods sold

33.55 35.86 30.82

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

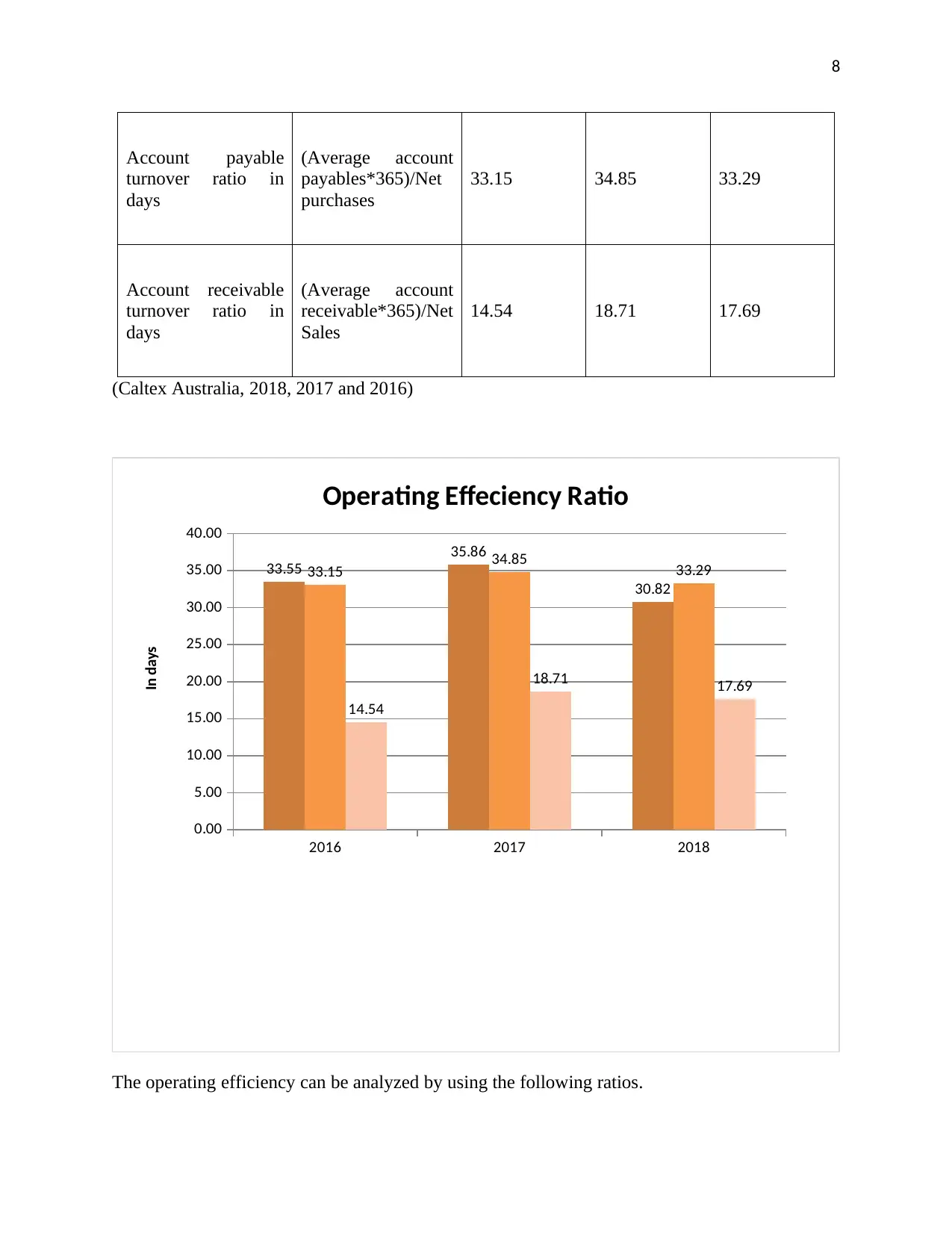

Account payable

turnover ratio in

days

(Average account

payables*365)/Net

purchases

33.15 34.85 33.29

Account receivable

turnover ratio in

days

(Average account

receivable*365)/Net

Sales

14.54 18.71 17.69

(Caltex Australia, 2018, 2017 and 2016)

2016 2017 2018

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

33.55

35.86

30.82

33.15 34.85 33.29

14.54

18.71 17.69

Operating Effeciency Ratio

In days

The operating efficiency can be analyzed by using the following ratios.

Account payable

turnover ratio in

days

(Average account

payables*365)/Net

purchases

33.15 34.85 33.29

Account receivable

turnover ratio in

days

(Average account

receivable*365)/Net

Sales

14.54 18.71 17.69

(Caltex Australia, 2018, 2017 and 2016)

2016 2017 2018

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

33.55

35.86

30.82

33.15 34.85 33.29

14.54

18.71 17.69

Operating Effeciency Ratio

In days

The operating efficiency can be analyzed by using the following ratios.

9

Day’s sales in inventory: This financial ratio depicts the average number of days a

company took to sell its inventory in an accounting year. The less the number of days,

better the ratio is. It shows company is efficiently selling its inventory. The past three

years data of Caltex Australia shows that company has worked upon its efficiency and

made it. Caltex has successfully decreased the number of days to convert its inventory

into sales. In 2016 the ratio was 33.55 days that has decreased to 30.82 days despite

increase in average inventory and net sales.

Account payable turnover ratio in days: This ratio states company’s efficiency in

paying off its creditors for outstanding invoices measured in number of days. Account

payable turnover ratio of Caltex Australia stated a stable trend over the past three years.

Company has taken approx. 33 days to pay off its payables. Company has taken 34.85

days in 2017 to pay off its creditors but in 2018 it covered it up (Davies and Crawford,

2011).

Account receivables turnover ratio in days: This ratio states the number of days a

company took to collect its debtors in an accounting year. The shorter the number of

days, better the ratio is. In the past three years Caltex Australia has not efficiently

collecting its debtors. Caltex Australia has taken 14.54 days in 2016 to collect its debtors

and in 2018 it took 17.69 days to collect the debtors. This is not a good sign for the

company as it is not able to liquidate its credit sales in cash easily (Krantz, 2016).

Section 2.3: Use of marketable securities for cash management

Marketable securities refer to the securities or investments that have been made by the

company to have enough cash and cash equivalents within the year. These investments are used

with the purpose to receive the company within one year. Marketable securities are being listed

under heading the current assets section of the balance sheet and it is valued at current fair value.

On looking at the balance sheet and notes to accounts of Caltex Australia, it has been

found that company has used only cash and cash equivalents and accounts receivables as

marketable securities to have enough cash resources to pay the current liabilities (Caltex

Australia. 2018).

Day’s sales in inventory: This financial ratio depicts the average number of days a

company took to sell its inventory in an accounting year. The less the number of days,

better the ratio is. It shows company is efficiently selling its inventory. The past three

years data of Caltex Australia shows that company has worked upon its efficiency and

made it. Caltex has successfully decreased the number of days to convert its inventory

into sales. In 2016 the ratio was 33.55 days that has decreased to 30.82 days despite

increase in average inventory and net sales.

Account payable turnover ratio in days: This ratio states company’s efficiency in

paying off its creditors for outstanding invoices measured in number of days. Account

payable turnover ratio of Caltex Australia stated a stable trend over the past three years.

Company has taken approx. 33 days to pay off its payables. Company has taken 34.85

days in 2017 to pay off its creditors but in 2018 it covered it up (Davies and Crawford,

2011).

Account receivables turnover ratio in days: This ratio states the number of days a

company took to collect its debtors in an accounting year. The shorter the number of

days, better the ratio is. In the past three years Caltex Australia has not efficiently

collecting its debtors. Caltex Australia has taken 14.54 days in 2016 to collect its debtors

and in 2018 it took 17.69 days to collect the debtors. This is not a good sign for the

company as it is not able to liquidate its credit sales in cash easily (Krantz, 2016).

Section 2.3: Use of marketable securities for cash management

Marketable securities refer to the securities or investments that have been made by the

company to have enough cash and cash equivalents within the year. These investments are used

with the purpose to receive the company within one year. Marketable securities are being listed

under heading the current assets section of the balance sheet and it is valued at current fair value.

On looking at the balance sheet and notes to accounts of Caltex Australia, it has been

found that company has used only cash and cash equivalents and accounts receivables as

marketable securities to have enough cash resources to pay the current liabilities (Caltex

Australia. 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Section 2.4: Sensitivity Analysis through using the given data

Life of project consider by the company 4 Years

Cost of Equipment 2,000,000.00$

Reisdual Value 200,000.00$

Depreciation Method Straight Line

Life of Equipment 4 years

Depreciation of Equipment per year 450,000.00$

Working Capital 600,000.00$

Recovery of working capital 600,000.00$

Selling Units per year 300000 per year

Selling Price 20.00$

Variable Cost 12.00$

Fixed Cost 300,000.00$

Discount Rate 10%

Tax Rate 30%

Information given in the question

Section 2.4: Sensitivity Analysis through using the given data

Life of project consider by the company 4 Years

Cost of Equipment 2,000,000.00$

Reisdual Value 200,000.00$

Depreciation Method Straight Line

Life of Equipment 4 years

Depreciation of Equipment per year 450,000.00$

Working Capital 600,000.00$

Recovery of working capital 600,000.00$

Selling Units per year 300000 per year

Selling Price 20.00$

Variable Cost 12.00$

Fixed Cost 300,000.00$

Discount Rate 10%

Tax Rate 30%

Information given in the question

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

0 1 2 3 4

Cash Inflows

Units sold 300000 300000 300000 300000

Selling price 20.00$ 20.00$ 20.00$ 20.00$

Net Cash Inflows 6,000,000.00$ 6,000,000.00$ 6,000,000.00$ 6,000,000.00$

Cash Outflows

Variable Cost 3,600,000.00$ 3,600,000.00$ 3,600,000.00$ 3,600,000.00$

Fixed Cost 300,000.00$ 300,000.00$ 300,000.00$ 300,000.00$

Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Total Cash outflows 4,350,000.00$ 4,350,000.00$ 4,350,000.00$ 4,350,000.00$

Cash flows before tax 1,650,000.00$ 1,650,000.00$ 1,650,000.00$ 1,650,000.00$

Less: Tax @ 30% 495,000.00$ 495,000.00$ 495,000.00$ 495,000.00$

Cash Flows after tax 1,155,000.00$ 1,155,000.00$ 1,155,000.00$ 1,155,000.00$

Add: Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Cash Flows before

depreciation after tax 1,605,000.00$ 1,605,000.00$ 1,605,000.00$ 1,605,000.00$

Initial Equiment Cost (2,000,000.00)$

Salvage Value 200,000.00$

Working Capital

Initial Requirement (600,000.00)$

Recovery 600,000.00$

Net Cash Flows (2,600,000.00)$ 1,605,000.00$ 1,605,000.00$ 1,605,000.00$ 2,405,000.00$

PVF @ 10% 1.000 0.909 0.826 0.751 0.683

(2,600,000.00)$ 1,459,090.91$ 1,326,446.28$ 1,205,860.26$ 1,642,647.36$

Net Present Value 3,034,044.81$

Cash Flows during the life of the project in normal Case

Years

Particulars

(Reilly and Brown, 2011)

0 1 2 3 4

Cash Inflows

Units sold 300000 300000 300000 300000

Selling price 20.00$ 20.00$ 20.00$ 20.00$

Net Cash Inflows 6,000,000.00$ 6,000,000.00$ 6,000,000.00$ 6,000,000.00$

Cash Outflows

Variable Cost 3,600,000.00$ 3,600,000.00$ 3,600,000.00$ 3,600,000.00$

Fixed Cost 300,000.00$ 300,000.00$ 300,000.00$ 300,000.00$

Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Total Cash outflows 4,350,000.00$ 4,350,000.00$ 4,350,000.00$ 4,350,000.00$

Cash flows before tax 1,650,000.00$ 1,650,000.00$ 1,650,000.00$ 1,650,000.00$

Less: Tax @ 30% 495,000.00$ 495,000.00$ 495,000.00$ 495,000.00$

Cash Flows after tax 1,155,000.00$ 1,155,000.00$ 1,155,000.00$ 1,155,000.00$

Add: Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Cash Flows before

depreciation after tax 1,605,000.00$ 1,605,000.00$ 1,605,000.00$ 1,605,000.00$

Initial Equiment Cost (2,000,000.00)$

Salvage Value 200,000.00$

Working Capital

Initial Requirement (600,000.00)$

Recovery 600,000.00$

Net Cash Flows (2,600,000.00)$ 1,605,000.00$ 1,605,000.00$ 1,605,000.00$ 2,405,000.00$

PVF @ 10% 1.000 0.909 0.826 0.751 0.683

(2,600,000.00)$ 1,459,090.91$ 1,326,446.28$ 1,205,860.26$ 1,642,647.36$

Net Present Value 3,034,044.81$

Cash Flows during the life of the project in normal Case

Years

Particulars

(Reilly and Brown, 2011)

12

0 1 2 3 4

Cash Inflows

Selling Units 270000 270000 270000 270000

Selling price 20.00$ 20.00$ 20.00$ 20.00$

Net Cash Inflows 5,400,000.00$ 5,400,000.00$ 5,400,000.00$ 5,400,000.00$

Cash Outflows

Variable Cost 3,240,000.00$ 3,240,000.00$ 3,240,000.00$ 3,240,000.00$

Fixed Cost 300,000.00$ 300,000.00$ 300,000.00$ 300,000.00$

Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Total Cash outflows 3,990,000.00$ 3,990,000.00$ 3,990,000.00$ 3,990,000.00$

Cash flows before tax 1,410,000.00$ 1,410,000.00$ 1,410,000.00$ 1,410,000.00$

Less: Tax @ 30% 423,000.00$ 423,000.00$ 423,000.00$ 423,000.00$

Cash Flows after tax 987,000.00$ 987,000.00$ 987,000.00$ 987,000.00$

Add: Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Cash Flows before

depreciation after 1,437,000.00$ 1,437,000.00$ 1,437,000.00$ 1,437,000.00$

Initial Equiment Cost (2,000,000.00)$

Salvage Value 200,000.00$

Working Capital

Initial Requirement (600,000.00)$

Recovery 600,000.00$

Net Cash Flows (2,600,000.00)$ 1,437,000.00$ 1,437,000.00$ 1,437,000.00$ 2,237,000.00$

PVF @ 10% 1.000 0.909 0.826 0.751 0.683

(2,600,000.00)$ 1,306,363.64$ 1,187,603.31$ 1,079,639.37$ 1,527,901.10$

Net Present Value 2,501,507.41$

Particulars Years

Statement of Cash flows when Unit sales decrease by 10%

(Schlichting, 2013)

0 1 2 3 4

Cash Inflows

Selling Units 270000 270000 270000 270000

Selling price 20.00$ 20.00$ 20.00$ 20.00$

Net Cash Inflows 5,400,000.00$ 5,400,000.00$ 5,400,000.00$ 5,400,000.00$

Cash Outflows

Variable Cost 3,240,000.00$ 3,240,000.00$ 3,240,000.00$ 3,240,000.00$

Fixed Cost 300,000.00$ 300,000.00$ 300,000.00$ 300,000.00$

Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Total Cash outflows 3,990,000.00$ 3,990,000.00$ 3,990,000.00$ 3,990,000.00$

Cash flows before tax 1,410,000.00$ 1,410,000.00$ 1,410,000.00$ 1,410,000.00$

Less: Tax @ 30% 423,000.00$ 423,000.00$ 423,000.00$ 423,000.00$

Cash Flows after tax 987,000.00$ 987,000.00$ 987,000.00$ 987,000.00$

Add: Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Cash Flows before

depreciation after 1,437,000.00$ 1,437,000.00$ 1,437,000.00$ 1,437,000.00$

Initial Equiment Cost (2,000,000.00)$

Salvage Value 200,000.00$

Working Capital

Initial Requirement (600,000.00)$

Recovery 600,000.00$

Net Cash Flows (2,600,000.00)$ 1,437,000.00$ 1,437,000.00$ 1,437,000.00$ 2,237,000.00$

PVF @ 10% 1.000 0.909 0.826 0.751 0.683

(2,600,000.00)$ 1,306,363.64$ 1,187,603.31$ 1,079,639.37$ 1,527,901.10$

Net Present Value 2,501,507.41$

Particulars Years

Statement of Cash flows when Unit sales decrease by 10%

(Schlichting, 2013)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.