Financial Performance Management Report: Costing and Variance Analysis

VerifiedAdded on 2022/12/28

|12

|2145

|85

Report

AI Summary

This report provides a comprehensive analysis of financial performance management. It begins with an introduction to the importance of financial result management and the various methods used for measurement. The report then delves into a detailed analysis of costing methods, comparing the per-unit cost calculation using labor hours and the Activity-Based Costing (ABC) method, along with an evaluation of the results obtained from both approaches. The report further explores variance analysis, including material usage, mix, and yield variances, along with a discussion of the problems associated with the current system of calculating and reporting variances. The report also evaluates the effectiveness of zero-based budgeting (ZBB) and incremental budgeting (IB) for organizational preparation and control. The conclusion summarizes the key findings and emphasizes the importance of financial planning for effective financial result management.

Financial Performance Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

QUESTION 1.................................................................................................................................................3

QUESTION 2.................................................................................................................................................9

QUESTION 3...............................................................................................................................................11

CONCLUSION.............................................................................................................................................12

INTRODUCTION...........................................................................................................................................3

QUESTION 1.................................................................................................................................................3

QUESTION 2.................................................................................................................................................9

QUESTION 3...............................................................................................................................................11

CONCLUSION.............................................................................................................................................12

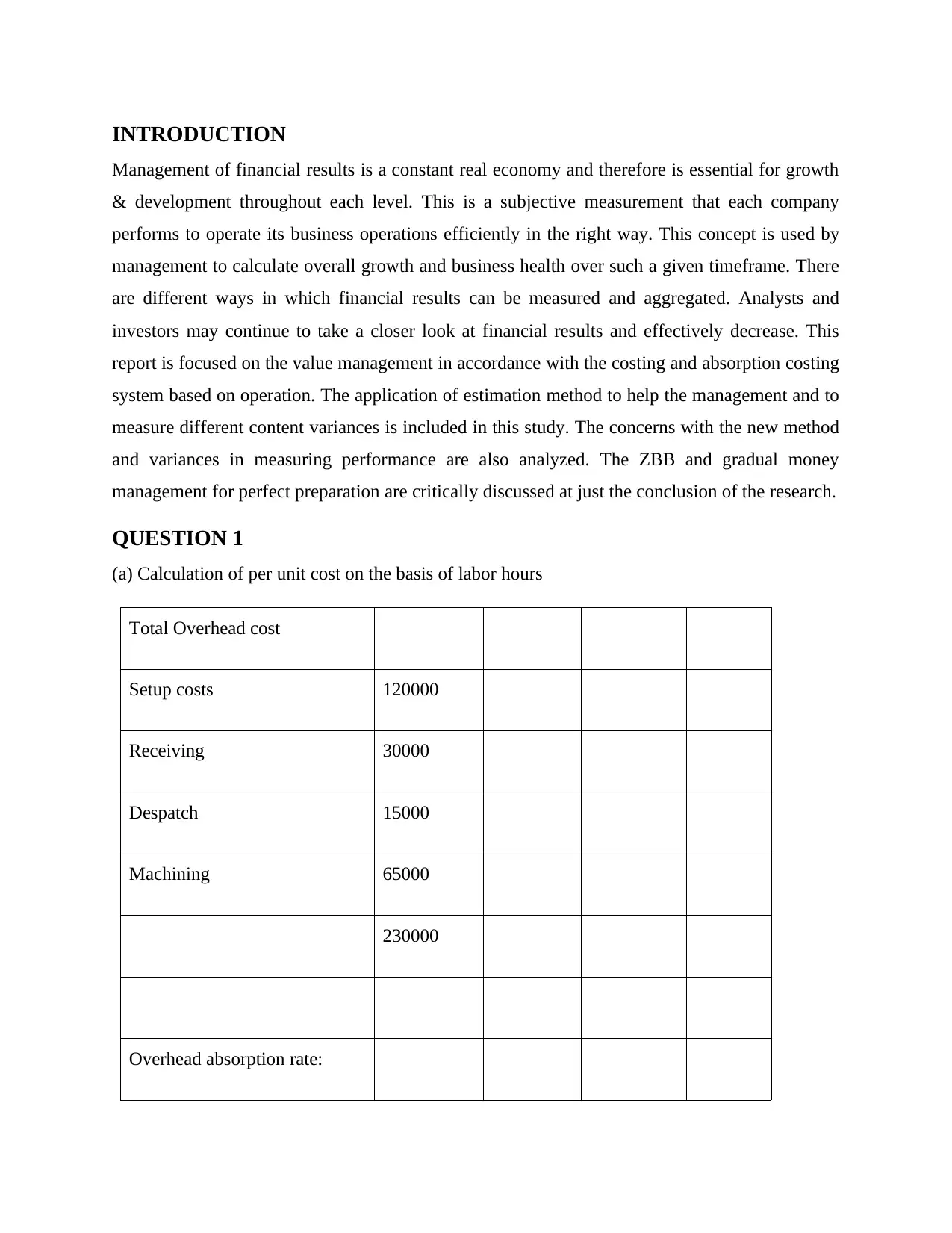

INTRODUCTION

Management of financial results is a constant real economy and therefore is essential for growth

& development throughout each level. This is a subjective measurement that each company

performs to operate its business operations efficiently in the right way. This concept is used by

management to calculate overall growth and business health over such a given timeframe. There

are different ways in which financial results can be measured and aggregated. Analysts and

investors may continue to take a closer look at financial results and effectively decrease. This

report is focused on the value management in accordance with the costing and absorption costing

system based on operation. The application of estimation method to help the management and to

measure different content variances is included in this study. The concerns with the new method

and variances in measuring performance are also analyzed. The ZBB and gradual money

management for perfect preparation are critically discussed at just the conclusion of the research.

QUESTION 1

(a) Calculation of per unit cost on the basis of labor hours

Total Overhead cost

Setup costs 120000

Receiving 30000

Despatch 15000

Machining 65000

230000

Overhead absorption rate:

Management of financial results is a constant real economy and therefore is essential for growth

& development throughout each level. This is a subjective measurement that each company

performs to operate its business operations efficiently in the right way. This concept is used by

management to calculate overall growth and business health over such a given timeframe. There

are different ways in which financial results can be measured and aggregated. Analysts and

investors may continue to take a closer look at financial results and effectively decrease. This

report is focused on the value management in accordance with the costing and absorption costing

system based on operation. The application of estimation method to help the management and to

measure different content variances is included in this study. The concerns with the new method

and variances in measuring performance are also analyzed. The ZBB and gradual money

management for perfect preparation are critically discussed at just the conclusion of the research.

QUESTION 1

(a) Calculation of per unit cost on the basis of labor hours

Total Overhead cost

Setup costs 120000

Receiving 30000

Despatch 15000

Machining 65000

230000

Overhead absorption rate:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

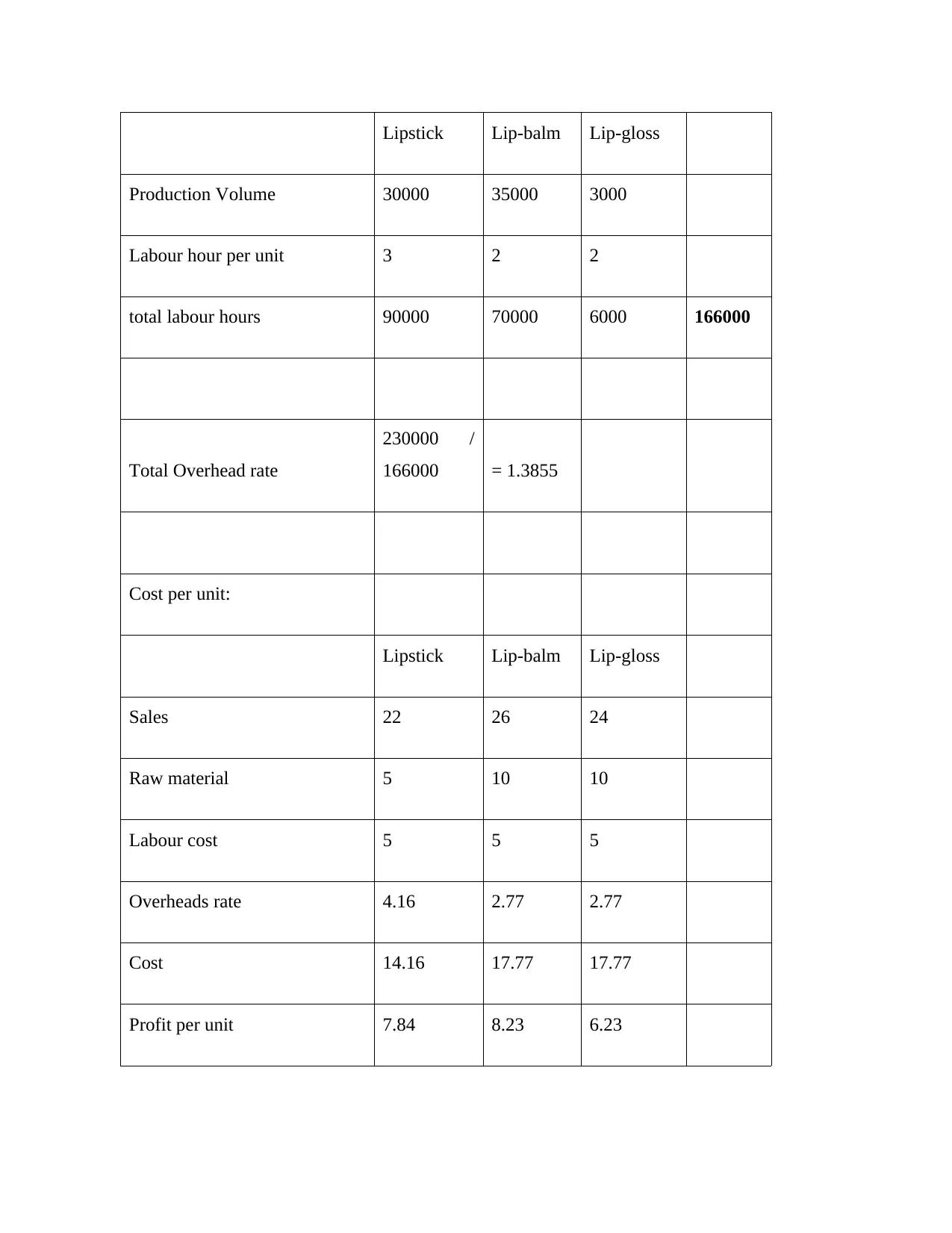

Lipstick Lip-balm Lip-gloss

Production Volume 30000 35000 3000

Labour hour per unit 3 2 2

total labour hours 90000 70000 6000 166000

Total Overhead rate

230000 /

166000 = 1.3855

Cost per unit:

Lipstick Lip-balm Lip-gloss

Sales 22 26 24

Raw material 5 10 10

Labour cost 5 5 5

Overheads rate 4.16 2.77 2.77

Cost 14.16 17.77 17.77

Profit per unit 7.84 8.23 6.23

Production Volume 30000 35000 3000

Labour hour per unit 3 2 2

total labour hours 90000 70000 6000 166000

Total Overhead rate

230000 /

166000 = 1.3855

Cost per unit:

Lipstick Lip-balm Lip-gloss

Sales 22 26 24

Raw material 5 10 10

Labour cost 5 5 5

Overheads rate 4.16 2.77 2.77

Cost 14.16 17.77 17.77

Profit per unit 7.84 8.23 6.23

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Units 30000 35000 3000

Profit 235301.20 288012.05 18686.75

(b) Calculation per unit cost on basis of ABC method.

Cost

Driver

Setup costs 120000 25 setups

Receiving 30000 22 deliveries

Despatch 15000 50 despatched

Machining 65000 12 machining

Cost driver data:

Machine hours per unit 4 4 4

Number of setups 10 14 1

Number of deliveries received 10 10 2

Number of orders despatched 20

20 10 20 20 10

Profit 235301.20 288012.05 18686.75

(b) Calculation per unit cost on basis of ABC method.

Cost

Driver

Setup costs 120000 25 setups

Receiving 30000 22 deliveries

Despatch 15000 50 despatched

Machining 65000 12 machining

Cost driver data:

Machine hours per unit 4 4 4

Number of setups 10 14 1

Number of deliveries received 10 10 2

Number of orders despatched 20

20 10 20 20 10

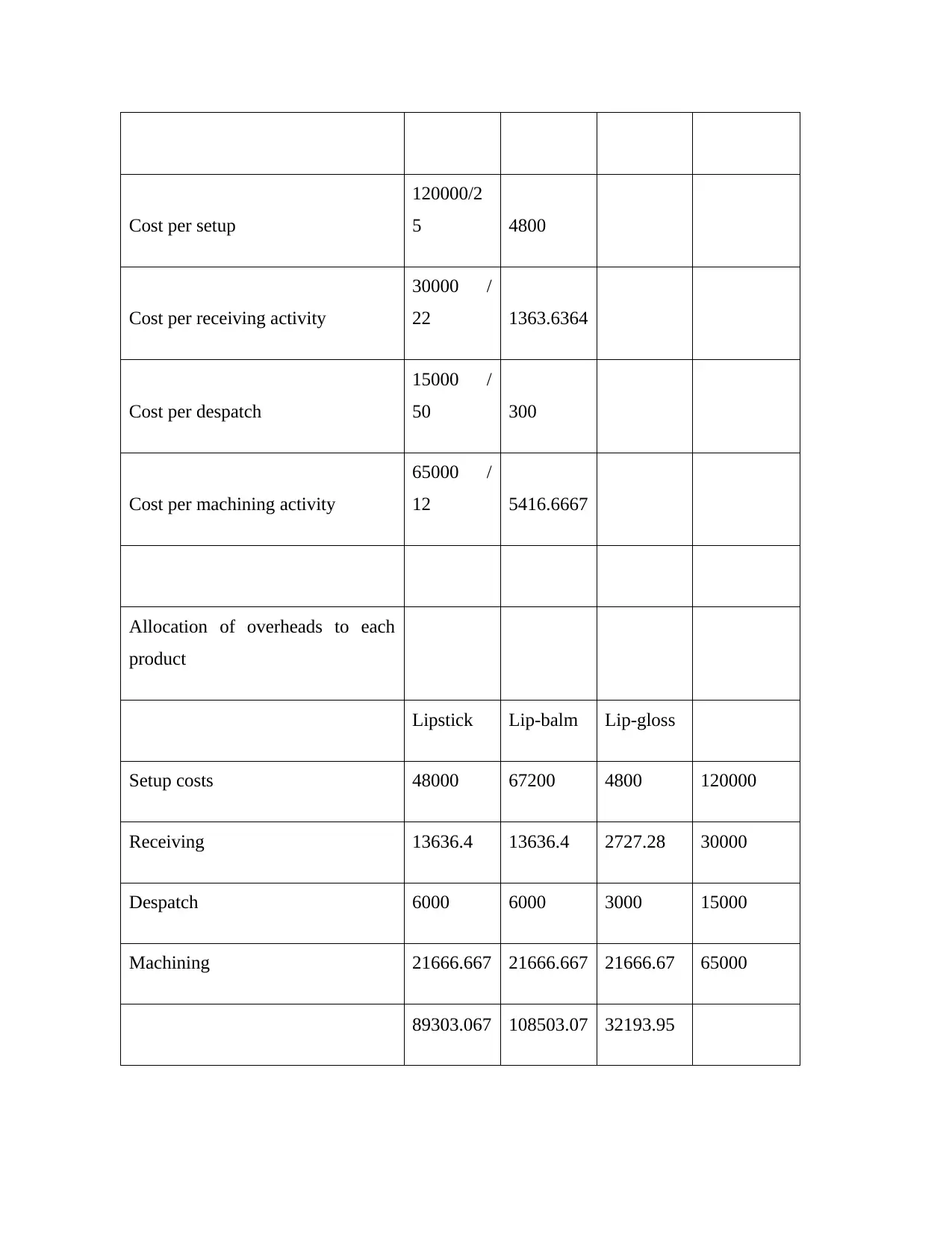

Cost per setup

120000/2

5 4800

Cost per receiving activity

30000 /

22 1363.6364

Cost per despatch

15000 /

50 300

Cost per machining activity

65000 /

12 5416.6667

Allocation of overheads to each

product

Lipstick Lip-balm Lip-gloss

Setup costs 48000 67200 4800 120000

Receiving 13636.4 13636.4 2727.28 30000

Despatch 6000 6000 3000 15000

Machining 21666.667 21666.667 21666.67 65000

89303.067 108503.07 32193.95

120000/2

5 4800

Cost per receiving activity

30000 /

22 1363.6364

Cost per despatch

15000 /

50 300

Cost per machining activity

65000 /

12 5416.6667

Allocation of overheads to each

product

Lipstick Lip-balm Lip-gloss

Setup costs 48000 67200 4800 120000

Receiving 13636.4 13636.4 2727.28 30000

Despatch 6000 6000 3000 15000

Machining 21666.667 21666.667 21666.67 65000

89303.067 108503.07 32193.95

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Production Volume 30000 35000 3000

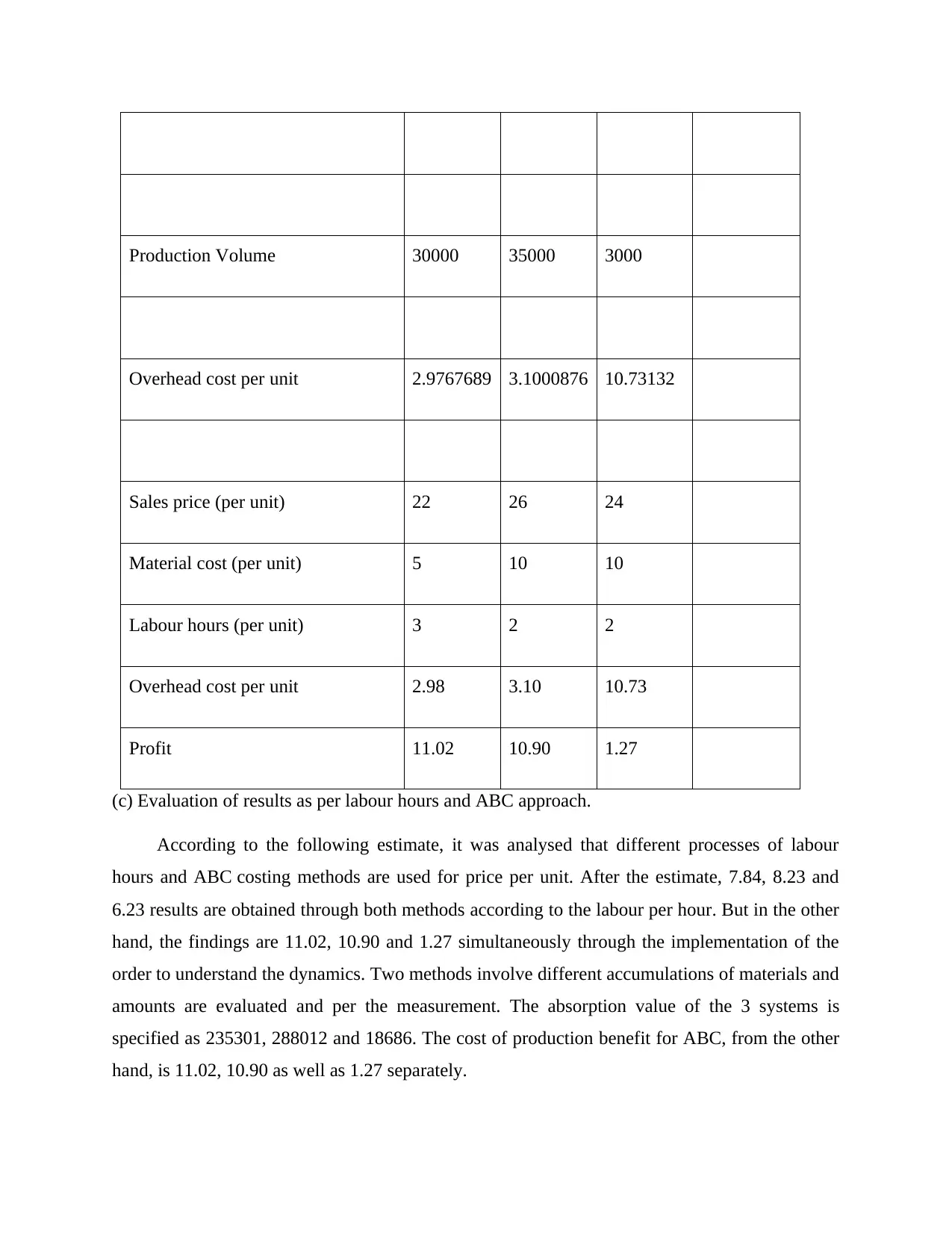

Overhead cost per unit 2.9767689 3.1000876 10.73132

Sales price (per unit) 22 26 24

Material cost (per unit) 5 10 10

Labour hours (per unit) 3 2 2

Overhead cost per unit 2.98 3.10 10.73

Profit 11.02 10.90 1.27

(c) Evaluation of results as per labour hours and ABC approach.

According to the following estimate, it was analysed that different processes of labour

hours and ABC costing methods are used for price per unit. After the estimate, 7.84, 8.23 and

6.23 results are obtained through both methods according to the labour per hour. But in the other

hand, the findings are 11.02, 10.90 and 1.27 simultaneously through the implementation of the

order to understand the dynamics. Two methods involve different accumulations of materials and

amounts are evaluated and per the measurement. The absorption value of the 3 systems is

specified as 235301, 288012 and 18686. The cost of production benefit for ABC, from the other

hand, is 11.02, 10.90 as well as 1.27 separately.

Overhead cost per unit 2.9767689 3.1000876 10.73132

Sales price (per unit) 22 26 24

Material cost (per unit) 5 10 10

Labour hours (per unit) 3 2 2

Overhead cost per unit 2.98 3.10 10.73

Profit 11.02 10.90 1.27

(c) Evaluation of results as per labour hours and ABC approach.

According to the following estimate, it was analysed that different processes of labour

hours and ABC costing methods are used for price per unit. After the estimate, 7.84, 8.23 and

6.23 results are obtained through both methods according to the labour per hour. But in the other

hand, the findings are 11.02, 10.90 and 1.27 simultaneously through the implementation of the

order to understand the dynamics. Two methods involve different accumulations of materials and

amounts are evaluated and per the measurement. The absorption value of the 3 systems is

specified as 235301, 288012 and 18686. The cost of production benefit for ABC, from the other

hand, is 11.02, 10.90 as well as 1.27 separately.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Unless the absorption price is applied, various inventory expenses like fixed operating

costs, energy bills including factory storage losses are included in the measure. There are

multiple expenses, like direct supplies, labor and capital spending, including the site manager's

salary and company tax. These goods contribute to the study of real profitability and less of the

sales value. In this process, fixed output overhead is allocated as item expense and assists in

judgment on product range. In addition, the cost of absorption offers a poor assessment of the

real cost of producing each commodity.

Activity-based technology is used to reliably assign production expenses by ascribing tasks

to them. All the expense calculation is based on unique intellectual honesty operations. The

concept will be based on the elimination of overhead expenses in negative ways. ABC works

well in traditional circumstances where it is not straightforward to learn a great deal of objects

and devices. For example, the environment where production cycles become cut down does not

have a condensed value. There are several data requests that are centred mostly on ABC method.

But at the other hand, in terms of precise collection of data, the information will be accessible

except when designing a system and that will assist in the judgment process. If, after coming to a

decision, an organization may use the standard ABC framework to find that relevant information

is not needed. At the end of the process, the framework is focused on the protocol and collects

economic impact research based mostly on choice and endorses the method cost and provides

optimized performance with advantage details. In addition, the overall review presents the use of

activity-based approaches for critical assessment.

(d) Sensitivity analysis help managers to cope with uncertainties

Analysis of sensitivity is a template of results for changing input information and predicting

possible cash flows that rely largely on future events, sales, habits, transactions. The stream will

affect the value of the forecast in complex equations. Based on study, some input data can be

removed and further data analysis as well as analysis can be performed. It is linked to the results

where, if not necessary, all data and model uncertainties should be eliminated before investing

quantity and space to gather additional data for the production and calculate device output for the

process of analysis. This study describes about the various independent variables that effect on

costs, energy bills including factory storage losses are included in the measure. There are

multiple expenses, like direct supplies, labor and capital spending, including the site manager's

salary and company tax. These goods contribute to the study of real profitability and less of the

sales value. In this process, fixed output overhead is allocated as item expense and assists in

judgment on product range. In addition, the cost of absorption offers a poor assessment of the

real cost of producing each commodity.

Activity-based technology is used to reliably assign production expenses by ascribing tasks

to them. All the expense calculation is based on unique intellectual honesty operations. The

concept will be based on the elimination of overhead expenses in negative ways. ABC works

well in traditional circumstances where it is not straightforward to learn a great deal of objects

and devices. For example, the environment where production cycles become cut down does not

have a condensed value. There are several data requests that are centred mostly on ABC method.

But at the other hand, in terms of precise collection of data, the information will be accessible

except when designing a system and that will assist in the judgment process. If, after coming to a

decision, an organization may use the standard ABC framework to find that relevant information

is not needed. At the end of the process, the framework is focused on the protocol and collects

economic impact research based mostly on choice and endorses the method cost and provides

optimized performance with advantage details. In addition, the overall review presents the use of

activity-based approaches for critical assessment.

(d) Sensitivity analysis help managers to cope with uncertainties

Analysis of sensitivity is a template of results for changing input information and predicting

possible cash flows that rely largely on future events, sales, habits, transactions. The stream will

affect the value of the forecast in complex equations. Based on study, some input data can be

removed and further data analysis as well as analysis can be performed. It is linked to the results

where, if not necessary, all data and model uncertainties should be eliminated before investing

quantity and space to gather additional data for the production and calculate device output for the

process of analysis. This study describes about the various independent variables that effect on

singular event practices. For the study need a prepare a technique to use for candidate models are

affected on the inner expression adjustment known as input concern.

The basic model is split into a statistical model and a means of analyzing outcomes based on the

number of parameters. This study of the empirical approach is focused on different variables that

affect the findings by generating a sequence of variables. The observer examines the significant

effect of the adjustment and performance signal on the target. The sensitivity of the improvement

of human organizations' securities can be measured and consists of market income, portfolio

estimates, the number of rivals competing in the business and the effect on stock prices of

different variables. There is analysis on the prices of properties that can be refined by choosing

various hypotheses and adding several parameters. The appraisal allows managers to evaluate the

multiple components that will affect the results, such as the decrease in investment costs. As a

consequence, after doing sensitivity analysis, it would impact on future income and assessment

to put up with the uncertainties carried out in a new market entity. It is a means of evaluating

situations that the center anticipates differently. It is meant to observe the extent of risk of the

operation that helps the outcomes to be evaluated depending on the accuracy of inputs.

QUESTION 2

(a) Calculation of variances

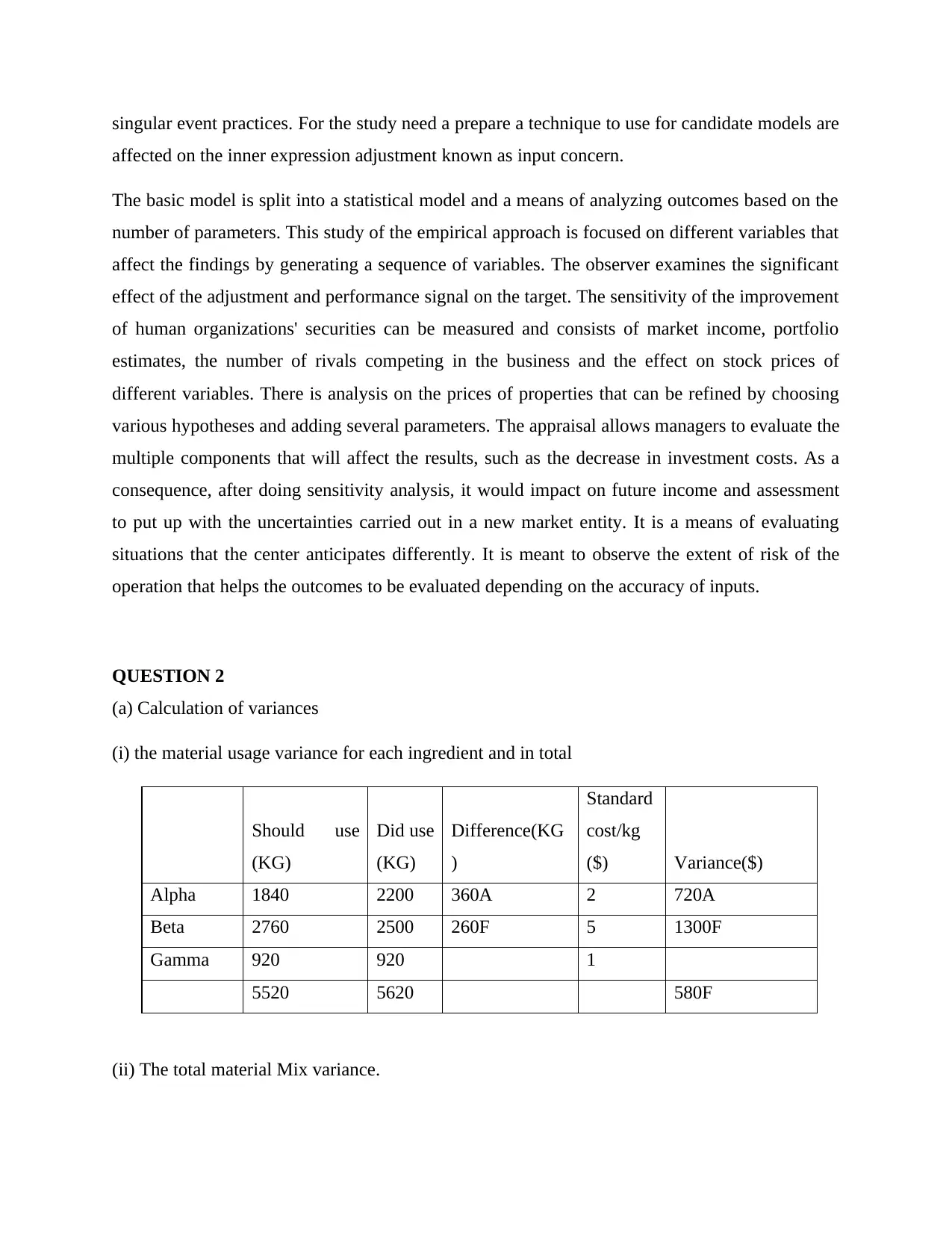

(i) the material usage variance for each ingredient and in total

Should use

(KG)

Did use

(KG)

Difference(KG

)

Standard

cost/kg

($) Variance($)

Alpha 1840 2200 360A 2 720A

Beta 2760 2500 260F 5 1300F

Gamma 920 920 1

5520 5620 580F

(ii) The total material Mix variance.

affected on the inner expression adjustment known as input concern.

The basic model is split into a statistical model and a means of analyzing outcomes based on the

number of parameters. This study of the empirical approach is focused on different variables that

affect the findings by generating a sequence of variables. The observer examines the significant

effect of the adjustment and performance signal on the target. The sensitivity of the improvement

of human organizations' securities can be measured and consists of market income, portfolio

estimates, the number of rivals competing in the business and the effect on stock prices of

different variables. There is analysis on the prices of properties that can be refined by choosing

various hypotheses and adding several parameters. The appraisal allows managers to evaluate the

multiple components that will affect the results, such as the decrease in investment costs. As a

consequence, after doing sensitivity analysis, it would impact on future income and assessment

to put up with the uncertainties carried out in a new market entity. It is a means of evaluating

situations that the center anticipates differently. It is meant to observe the extent of risk of the

operation that helps the outcomes to be evaluated depending on the accuracy of inputs.

QUESTION 2

(a) Calculation of variances

(i) the material usage variance for each ingredient and in total

Should use

(KG)

Did use

(KG)

Difference(KG

)

Standard

cost/kg

($) Variance($)

Alpha 1840 2200 360A 2 720A

Beta 2760 2500 260F 5 1300F

Gamma 920 920 1

5520 5620 580F

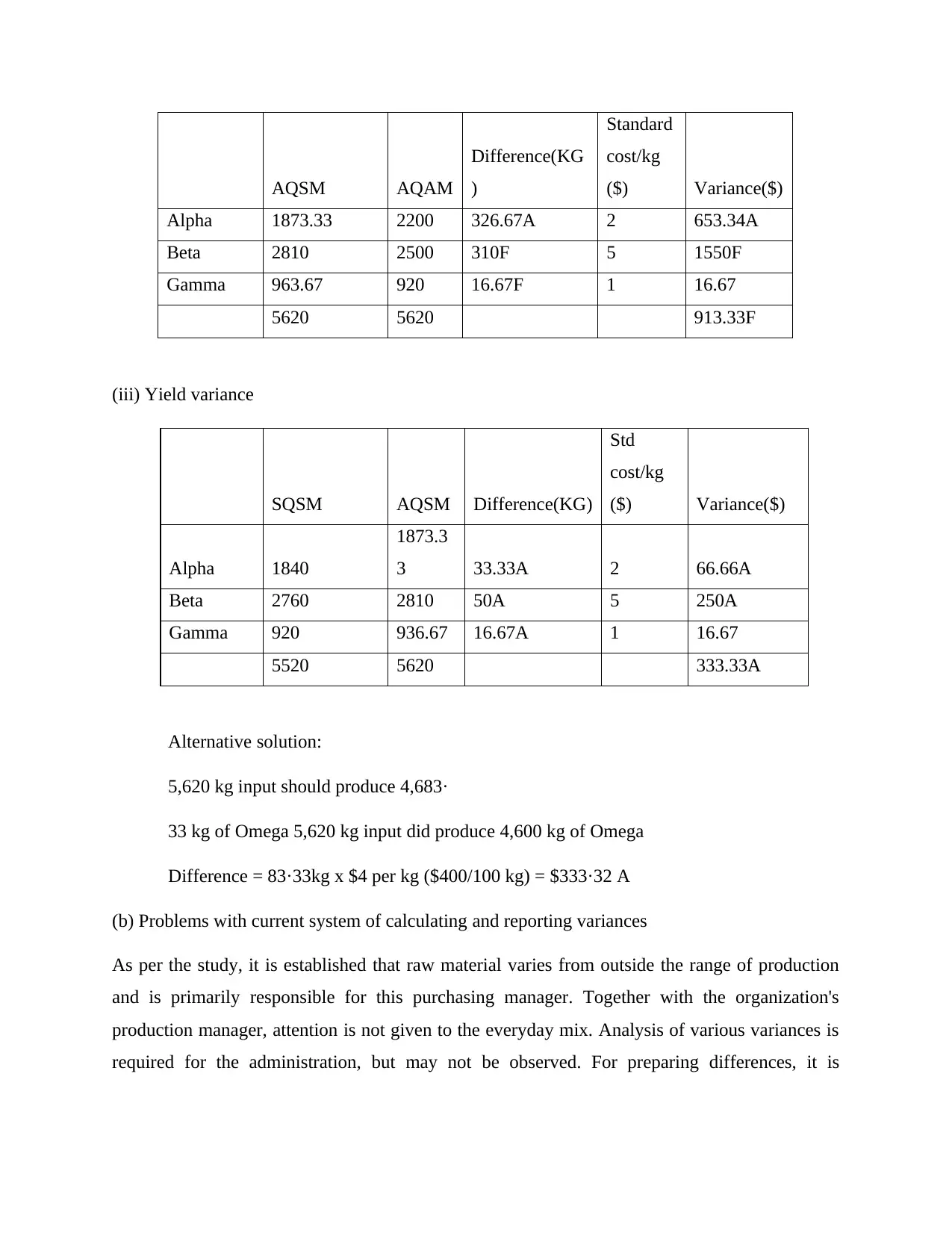

(ii) The total material Mix variance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AQSM AQAM

Difference(KG

)

Standard

cost/kg

($) Variance($)

Alpha 1873.33 2200 326.67A 2 653.34A

Beta 2810 2500 310F 5 1550F

Gamma 963.67 920 16.67F 1 16.67

5620 5620 913.33F

(iii) Yield variance

SQSM AQSM Difference(KG)

Std

cost/kg

($) Variance($)

Alpha 1840

1873.3

3 33.33A 2 66.66A

Beta 2760 2810 50A 5 250A

Gamma 920 936.67 16.67A 1 16.67

5520 5620 333.33A

Alternative solution:

5,620 kg input should produce 4,683·

33 kg of Omega 5,620 kg input did produce 4,600 kg of Omega

Difference = 83·33kg x $4 per kg ($400/100 kg) = $333·32 A

(b) Problems with current system of calculating and reporting variances

As per the study, it is established that raw material varies from outside the range of production

and is primarily responsible for this purchasing manager. Together with the organization's

production manager, attention is not given to the everyday mix. Analysis of various variances is

required for the administration, but may not be observed. For preparing differences, it is

Difference(KG

)

Standard

cost/kg

($) Variance($)

Alpha 1873.33 2200 326.67A 2 653.34A

Beta 2810 2500 310F 5 1550F

Gamma 963.67 920 16.67F 1 16.67

5620 5620 913.33F

(iii) Yield variance

SQSM AQSM Difference(KG)

Std

cost/kg

($) Variance($)

Alpha 1840

1873.3

3 33.33A 2 66.66A

Beta 2760 2810 50A 5 250A

Gamma 920 936.67 16.67A 1 16.67

5520 5620 333.33A

Alternative solution:

5,620 kg input should produce 4,683·

33 kg of Omega 5,620 kg input did produce 4,600 kg of Omega

Difference = 83·33kg x $4 per kg ($400/100 kg) = $333·32 A

(b) Problems with current system of calculating and reporting variances

As per the study, it is established that raw material varies from outside the range of production

and is primarily responsible for this purchasing manager. Together with the organization's

production manager, attention is not given to the everyday mix. Analysis of various variances is

required for the administration, but may not be observed. For preparing differences, it is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

important since they will not evaluate them. Price levels and productivity of three products is

being adjustable and the use of rates as per the requirements for combining yield.

Improvements in the consistency and costs of simple mixture and product related products have

not improved in 5 years. It has become the justification for conducting control operations based

on the numerous variances and setting obsolete expectations. Since the kappa organization

actually has no feedback and opinions attributable to fewer true pictures and becomes the

production manager's justification for performance. While Kappa co does not affect numerous

variations that are capable of observing costs and being complacent.

QUESTION 3

Evaluation of neither ZBB nor the IB delivers the impeccable toll for preparation organization

and control

Zero-based budgetary control is an expenditure plan that begins at zero and that is not

linked to the previous budget. This budget is intended to measure the annual budgets to be

generated in the year. This encourages the organization to look at the current number, not the

previous number. It needs workers to make decisions and strengthen the organization's teamwork

and communication. By determining the unnecessary expenditures in the sector that could be

eliminated, it allows the organization save more money as well as produce profitability. Capital

expenditure, from the other hand, seems to be the budget planned from the existing budget as a

basis and incorporates the sum of the increase in the current budget cycle. Companies may

terminate rivals in this budget or build the benefit of true equality between units but the same

sum to change from the previous year.

The zero-based budgetary control does not take into account the expenditure of the current

year, it begins with the initial and also the funds allocated to each division are calculated in

relation to the costs of that year, while the invested capital is planned for the present year since

the preceding year's budget basis. ZBB is planned by allocating the maximum funds to certain

business processes that benefit the organization. This budget takes time since this strategy begins

around zero and requires awhile throughout current operations to plan the budget. It takes less

time to plan for budget estimates, since the new budget is measured from the previous budget.

This expenditure plan requires tools and knowledge to plan the budgetary, and it is simple to

process in gradual terms because it wouldn't involve budget planning training. This budget

being adjustable and the use of rates as per the requirements for combining yield.

Improvements in the consistency and costs of simple mixture and product related products have

not improved in 5 years. It has become the justification for conducting control operations based

on the numerous variances and setting obsolete expectations. Since the kappa organization

actually has no feedback and opinions attributable to fewer true pictures and becomes the

production manager's justification for performance. While Kappa co does not affect numerous

variations that are capable of observing costs and being complacent.

QUESTION 3

Evaluation of neither ZBB nor the IB delivers the impeccable toll for preparation organization

and control

Zero-based budgetary control is an expenditure plan that begins at zero and that is not

linked to the previous budget. This budget is intended to measure the annual budgets to be

generated in the year. This encourages the organization to look at the current number, not the

previous number. It needs workers to make decisions and strengthen the organization's teamwork

and communication. By determining the unnecessary expenditures in the sector that could be

eliminated, it allows the organization save more money as well as produce profitability. Capital

expenditure, from the other hand, seems to be the budget planned from the existing budget as a

basis and incorporates the sum of the increase in the current budget cycle. Companies may

terminate rivals in this budget or build the benefit of true equality between units but the same

sum to change from the previous year.

The zero-based budgetary control does not take into account the expenditure of the current

year, it begins with the initial and also the funds allocated to each division are calculated in

relation to the costs of that year, while the invested capital is planned for the present year since

the preceding year's budget basis. ZBB is planned by allocating the maximum funds to certain

business processes that benefit the organization. This budget takes time since this strategy begins

around zero and requires awhile throughout current operations to plan the budget. It takes less

time to plan for budget estimates, since the new budget is measured from the previous budget.

This expenditure plan requires tools and knowledge to plan the budgetary, and it is simple to

process in gradual terms because it wouldn't involve budget planning training. This budget

also takes the expenses incurred to develop the expenditure since it is due to begin and therefore

does not entail any costs to draft the expenditure incrementally. Zero-based financial planning

decreases the risk and confusion potential in the operations as it calculates the base expenditure

but does not pay much attention to this aspect in an operation in incremental terms because it

adds or subtracts from the previous budget.

CONCLUSION

As per the above report, it has been assumed that success in financial planning is a way of

controlling and evaluating an entity's financial results. The key justification for the management

to compare and approximate current expenditure values and make changes accordingly. Analysis

of the content variances and labor variances in this study on the basis of various methods after

which different outcomes are effectively obtained.

does not entail any costs to draft the expenditure incrementally. Zero-based financial planning

decreases the risk and confusion potential in the operations as it calculates the base expenditure

but does not pay much attention to this aspect in an operation in incremental terms because it

adds or subtracts from the previous budget.

CONCLUSION

As per the above report, it has been assumed that success in financial planning is a way of

controlling and evaluating an entity's financial results. The key justification for the management

to compare and approximate current expenditure values and make changes accordingly. Analysis

of the content variances and labor variances in this study on the basis of various methods after

which different outcomes are effectively obtained.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.