Financial Performance Analysis Exam - Finance Module, Semester 1

VerifiedAdded on 2022/12/28

|11

|2239

|50

Quiz and Exam

AI Summary

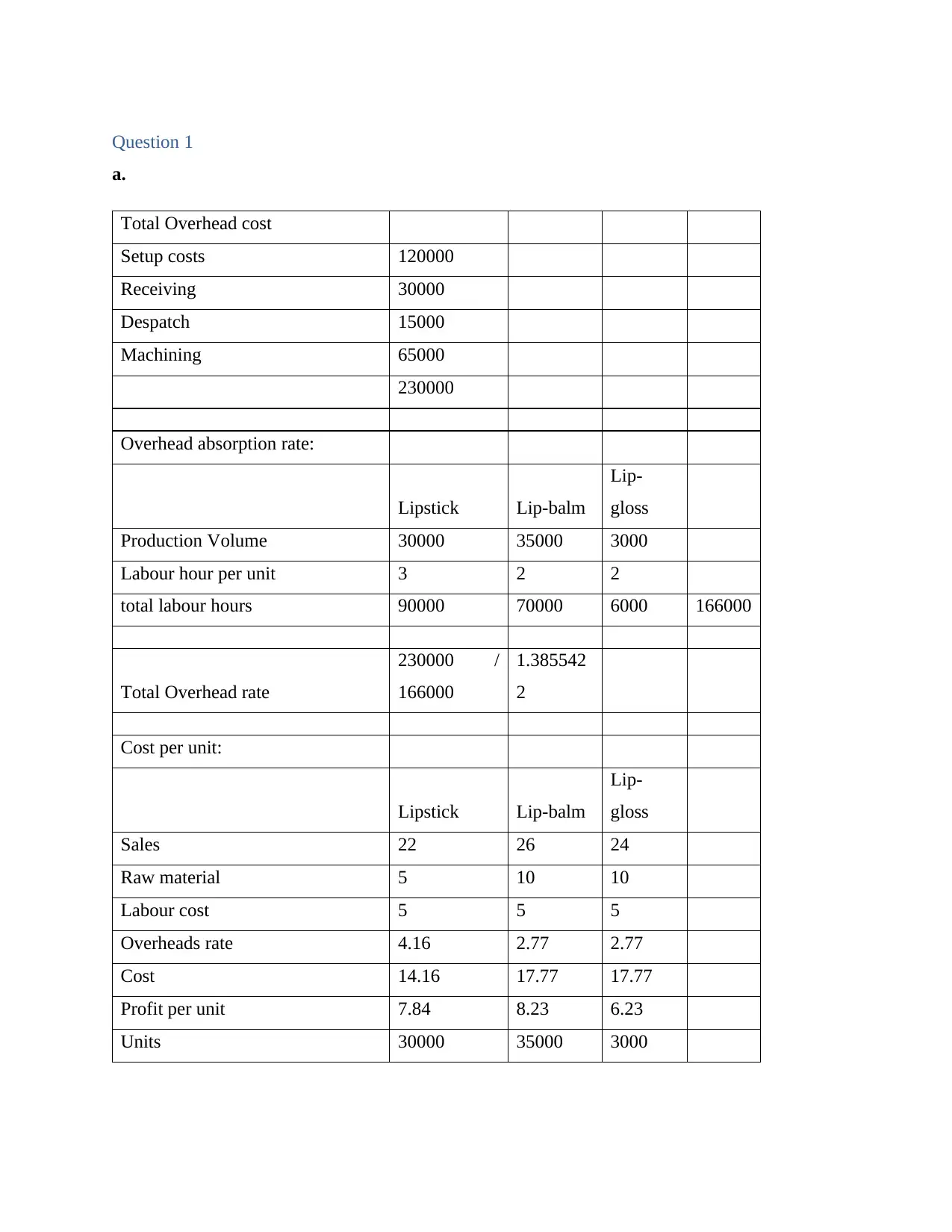

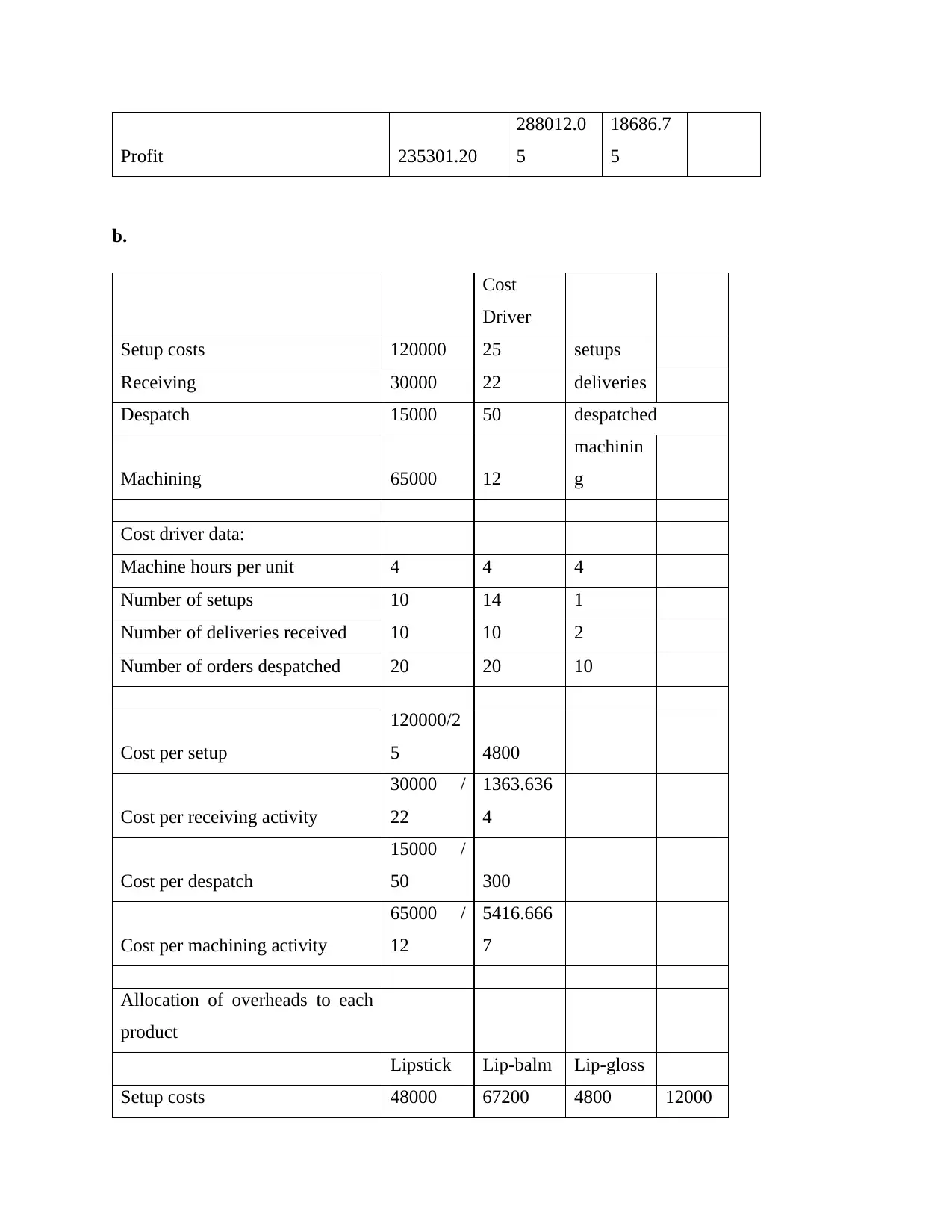

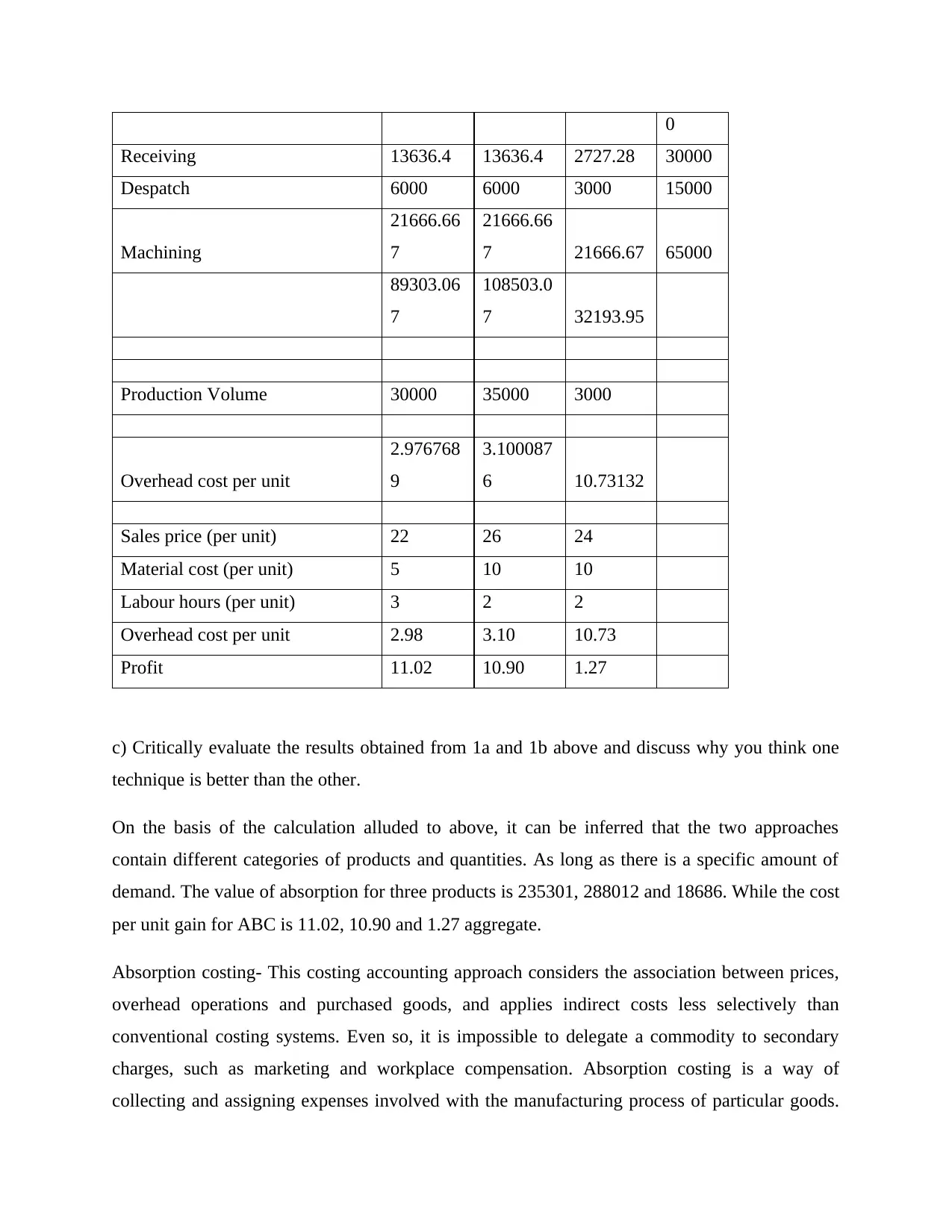

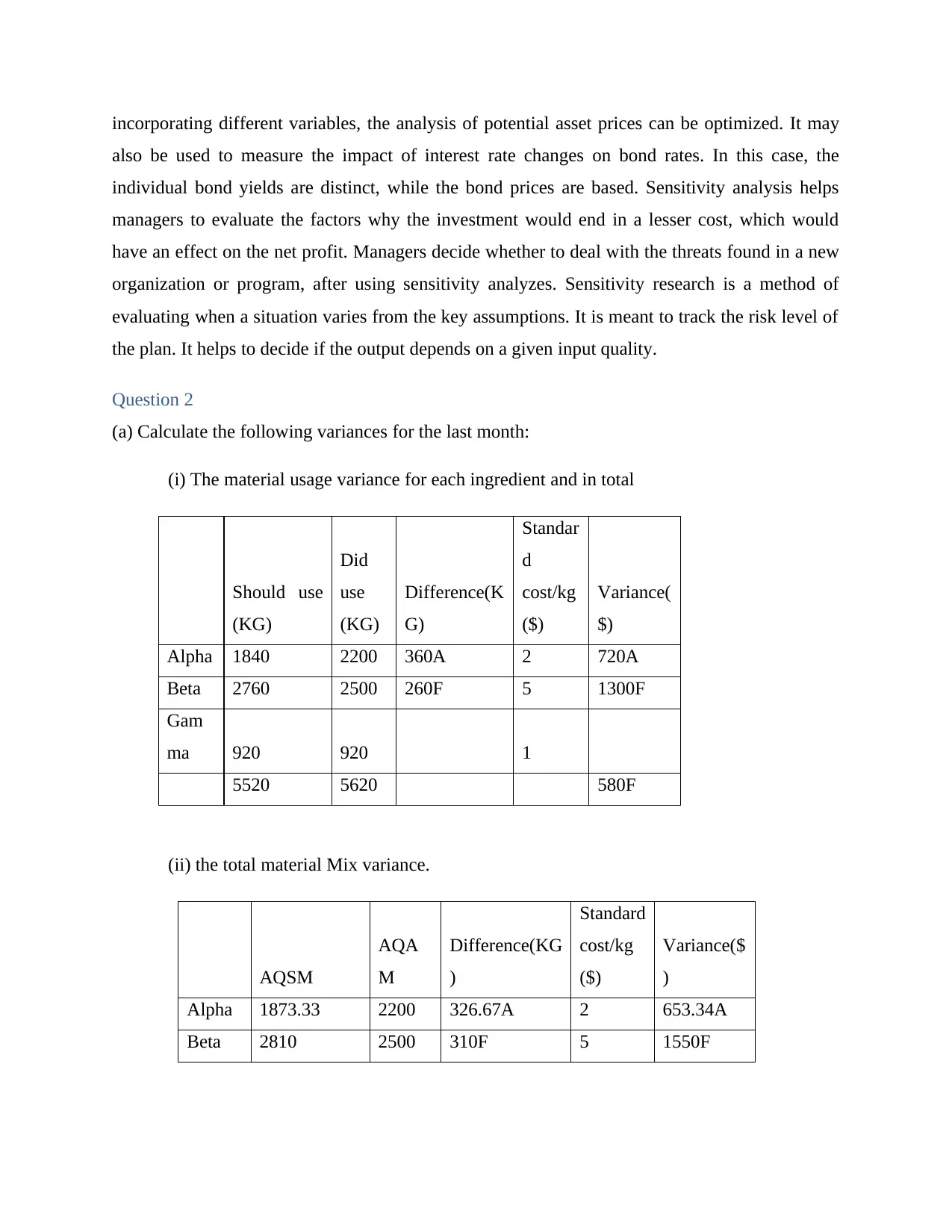

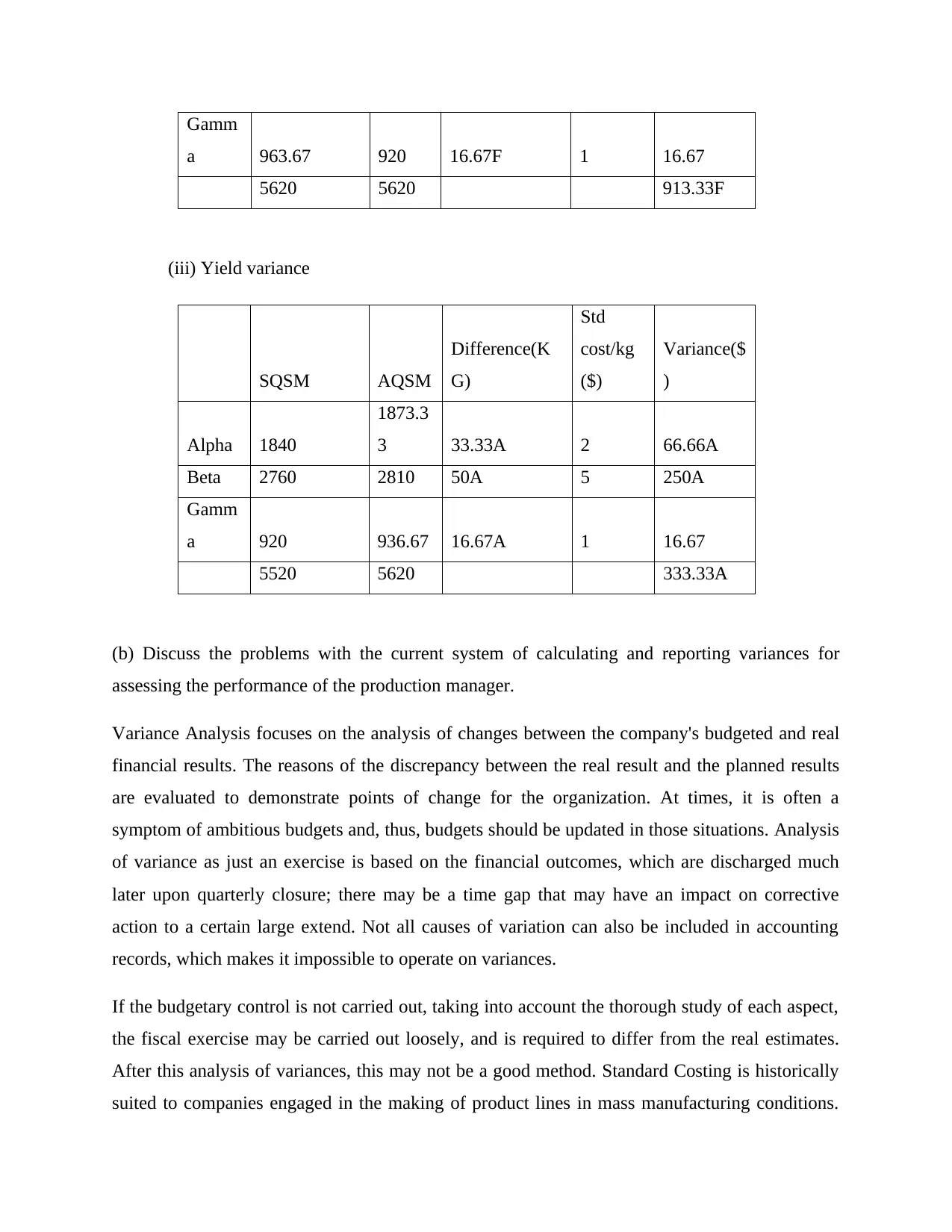

This document presents a comprehensive solution to a financial performance exam, addressing key concepts in cost accounting and financial analysis. The solution begins with an overhead cost allocation problem using both traditional absorption costing and activity-based costing (ABC), comparing the results and discussing the advantages of each method. It then delves into sensitivity analysis, explaining how it helps managers cope with uncertainties in decision-making. The second question focuses on variance analysis, calculating material usage, mix, and yield variances, and critically evaluating the limitations of variance analysis in assessing production manager performance. Finally, the solution explores budgeting techniques, comparing and contrasting zero-based budgeting (ZBB) and incremental budgeting (IB), highlighting their roles in planning and coordination within an organization. The document provides detailed calculations, explanations, and critical evaluations of the concepts, offering a thorough understanding of financial performance measurement and management.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.