Financial Analysis and Budgeting for Tourism and Hospitality Control

VerifiedAdded on 2023/04/10

|10

|2274

|390

Report

AI Summary

This report provides a comprehensive financial analysis of a tourism and hospitality company, covering key aspects from both a manager's and shareholder's perspective. Task 1 delves into ratio analysis, including profitability, efficiency, and stability metrics, alongside DuPont decomposition to assess Return on Assets (ROA). The analysis explores the company's financial performance, highlighting improvements in ROA, operating profit margin, and total asset turnover. Task 2 focuses on operational budgeting, explaining its purpose and application in the tourism and hospitality industry. It also includes projected cash flow statements, detailing cash receipts and disbursements, and concludes with an analysis of the company's liquidity balance. The report utilizes financial data to evaluate the company's performance and suggest strategies for financial management.

Running head: TOURISM AND HOSPITALIT CONTROL

Tourism and hospitality control

Name of the student

Name of the university

Student ID

Author note

Tourism and hospitality control

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TOURISM AND HOSPITALIT CONTROL

Table of Contents

Introduction..........................................................................................................................................2

Task 1...................................................................................................................................................2

From the managers perspective........................................................................................................2

Shareholder’s perspective.................................................................................................................3

Task 2...................................................................................................................................................4

1. Purpose of operational budget...................................................................................................4

2. Projected cash flow...................................................................................................................5

3. Liquidity balance.......................................................................................................................7

Reference..............................................................................................................................................8

Table of Contents

Introduction..........................................................................................................................................2

Task 1...................................................................................................................................................2

From the managers perspective........................................................................................................2

Shareholder’s perspective.................................................................................................................3

Task 2...................................................................................................................................................4

1. Purpose of operational budget...................................................................................................4

2. Projected cash flow...................................................................................................................5

3. Liquidity balance.......................................................................................................................7

Reference..............................................................................................................................................8

2TOURISM AND HOSPITALIT CONTROL

Introduction

The proposed report will cover 2 parts that is task 1 and task 2. Under task 1 it will focus on

the financial performance s of the company based on the ratio computed under the previous task.

Various aspects that will be covered under this part are the profitability aspect, efficiency aspect,

short term as well as long term stability aspects. Under task 2 the report will cover the budget

related aspects like purpose of budget, projection of budget and the company’s liability and will

suggest the possible methods for managing short term liquidity surplus or deficit (Polak &

Boughton, 2016).

Task 1

Analysis of ratios

From the managers perspective

Ratio analysis is the crucial tool for evaluating the financial performance of the entity and it helps in

–

Evaluating financial statement – ratios analysis is the useful technique used for evaluating

the company’s financial performance over the period under concern. It helps in

understanding the financial position. Managers use it to project the future performance

based on which it takes various important decisions like borrowing and investing.

Comparison of performance – managers shall know the exact position of the company as

compared to its peers. Ratio analysis helps to compare the performance of the company

with its peers and comparing with the previous period’s performances (Mohammadi &

Mahmudi, 2015).

Du-Pont decomposition – DuPont analysis is the framework used for analysing the fundamental

performance of the company and is considered as the useful technique for decomposing the various

drivers of ROA (return on assets). Decomposition of ROA allows the investors to concentrate on

key metrics of the financial performance on individual basis for recognising the weaknesses and

strengths. Analysing the Du-Pont decomposition of the entity it can be identified that the ROA of

the entity has been improved from 6.71% in 2016 to 14.10% in 2017. If the improvement is

analysed it can be identified that the company’s net profit is in improving trend and is increased to $

1136768 from net loss of $ 433482 in 2015. In the same way it can be identified that the operating

profit margin of the company has been increased to 20.23% in 2017 as compared to 10.38% in

Introduction

The proposed report will cover 2 parts that is task 1 and task 2. Under task 1 it will focus on

the financial performance s of the company based on the ratio computed under the previous task.

Various aspects that will be covered under this part are the profitability aspect, efficiency aspect,

short term as well as long term stability aspects. Under task 2 the report will cover the budget

related aspects like purpose of budget, projection of budget and the company’s liability and will

suggest the possible methods for managing short term liquidity surplus or deficit (Polak &

Boughton, 2016).

Task 1

Analysis of ratios

From the managers perspective

Ratio analysis is the crucial tool for evaluating the financial performance of the entity and it helps in

–

Evaluating financial statement – ratios analysis is the useful technique used for evaluating

the company’s financial performance over the period under concern. It helps in

understanding the financial position. Managers use it to project the future performance

based on which it takes various important decisions like borrowing and investing.

Comparison of performance – managers shall know the exact position of the company as

compared to its peers. Ratio analysis helps to compare the performance of the company

with its peers and comparing with the previous period’s performances (Mohammadi &

Mahmudi, 2015).

Du-Pont decomposition – DuPont analysis is the framework used for analysing the fundamental

performance of the company and is considered as the useful technique for decomposing the various

drivers of ROA (return on assets). Decomposition of ROA allows the investors to concentrate on

key metrics of the financial performance on individual basis for recognising the weaknesses and

strengths. Analysing the Du-Pont decomposition of the entity it can be identified that the ROA of

the entity has been improved from 6.71% in 2016 to 14.10% in 2017. If the improvement is

analysed it can be identified that the company’s net profit is in improving trend and is increased to $

1136768 from net loss of $ 433482 in 2015. In the same way it can be identified that the operating

profit margin of the company has been increased to 20.23% in 2017 as compared to 10.38% in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TOURISM AND HOSPITALIT CONTROL

2016. Major reason behind that is the entity was able to generate higher amount from the room

revenue. Room revenue generated in 2017 amounted to $ 82,33,379 whereas the same was $

52,92,068 in the year 2015. Further, if the total asset turnover is evaluated it can be observed that

the same has been increased from 0.65 to 0.70 over the years from 2016 to 2017. Reason behind

increase in the TATO ratio is the increase in the profit margin of the company over the years from

2016 to 2017. Hence, it can be observed that owing to increase in revenue as well as increase in the

net profit of the company ROA, operating profit margin and TATO of the entity are is improving

trend. From the analysis the management can take investment related decisions s the performance of

the company over the years are in improving trend (Becker et al., 2016).

Shareholder’s perspective

Shareholders are required to make informed decision based on the information provided in

the financial reports. However, looking into the financial information only thy may not be able to

take all the decisions. However, the ratios provide them with the readily available data for taking

different decisions regarding their investments. For instance, the profitability ratios help them to

evaluate whether the company is able to generate sufficient income for providing return to the

shareholders.

Return on equity (ROE) – ROE is the profitability ratios used for measuring the entity’s ability to

generate income from the investment made by the shareholders. It is further used for measuring the

efficiency of the management in context of using the equity finance for funding the operations and

growth of the entity. It is identified that the ROE of the company has been improved from 6.81% in

2016 to 11.33% in 2017. Hence, the company is earning 11 cents on each dollar of shareholders

equity whereas in 2016 it was earning 7 cents approximately on each dollar of equity. If the

improvement is analysed it can be identified that the company’s net profit is in improving trend and

is increased to $ 1136768 from net loss of $ 433482 in 2015 (Pérez-Rave, Muñoz-Giraldo &

Correa-Morales, 2017)

Return on assets (ROA) – ROA is the profitability metrics that is used to measure net earnings

generated by the entity. To be more specific ROA measures the efficiency of the entity in context of

managing the assets for producing profits during the concerned period. It can be identified that the

ROA of the entity has been improved from 6.71% in 2016 to 14.10% in 2017. Reason behind

increase in the ROA is the increase in the profit margin of the company over the years from 2016 to

2017.

2016. Major reason behind that is the entity was able to generate higher amount from the room

revenue. Room revenue generated in 2017 amounted to $ 82,33,379 whereas the same was $

52,92,068 in the year 2015. Further, if the total asset turnover is evaluated it can be observed that

the same has been increased from 0.65 to 0.70 over the years from 2016 to 2017. Reason behind

increase in the TATO ratio is the increase in the profit margin of the company over the years from

2016 to 2017. Hence, it can be observed that owing to increase in revenue as well as increase in the

net profit of the company ROA, operating profit margin and TATO of the entity are is improving

trend. From the analysis the management can take investment related decisions s the performance of

the company over the years are in improving trend (Becker et al., 2016).

Shareholder’s perspective

Shareholders are required to make informed decision based on the information provided in

the financial reports. However, looking into the financial information only thy may not be able to

take all the decisions. However, the ratios provide them with the readily available data for taking

different decisions regarding their investments. For instance, the profitability ratios help them to

evaluate whether the company is able to generate sufficient income for providing return to the

shareholders.

Return on equity (ROE) – ROE is the profitability ratios used for measuring the entity’s ability to

generate income from the investment made by the shareholders. It is further used for measuring the

efficiency of the management in context of using the equity finance for funding the operations and

growth of the entity. It is identified that the ROE of the company has been improved from 6.81% in

2016 to 11.33% in 2017. Hence, the company is earning 11 cents on each dollar of shareholders

equity whereas in 2016 it was earning 7 cents approximately on each dollar of equity. If the

improvement is analysed it can be identified that the company’s net profit is in improving trend and

is increased to $ 1136768 from net loss of $ 433482 in 2015 (Pérez-Rave, Muñoz-Giraldo &

Correa-Morales, 2017)

Return on assets (ROA) – ROA is the profitability metrics that is used to measure net earnings

generated by the entity. To be more specific ROA measures the efficiency of the entity in context of

managing the assets for producing profits during the concerned period. It can be identified that the

ROA of the entity has been improved from 6.71% in 2016 to 14.10% in 2017. Reason behind

increase in the ROA is the increase in the profit margin of the company over the years from 2016 to

2017.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TOURISM AND HOSPITALIT CONTROL

Equity multiplier – it is used for measuring the company’s financial leverage that is the proportion

of capital funded through borrowing and proportion funded through equity. The company’s equity

multiplier ratio of 1.16 and 1.17 in 2016 and 2017 is signifying that the company has significantly

low amount of debt as compared to equity. Hence, the company follows conservative policy is

taking debt.

Profitability ratio – profitability ratio is used for measuring the profit earning capability of the

company. Considering all the profitability ratios of the entity it can be identified that all ratios are in

improving trend and the major reason is the increase in revenue that led to increase in all the

profitability metrics.

Turnover ratio – it measures the ability of the company to in converting its balance sheet items into

income statement items. Account receivable settlement period had been reduced from 40.51 days to

39.95 days whereas the average number of inventory days increased from 9.99 days to 10.39 days

(Sponem & Lambert, 2016).

Short term financial stability – looking into the short term stability of the company it can be

identified that both current ratio as well as the acid test ratio of the entity has been improved over

the years from 2016 to 2017. It is signifying that the company is financially stable.

Long-term financial stability – looking into the long term stability of the company it can be

identified that the company has significantly low amount of debt as compared to equity. Further, the

operating profits are sufficient to cover the interest payment as high as 39.70 times. It is signifying

that the company is financially stable (Foster, 2017).

Task 2

1. Purpose of operational budget

Operational budget is the plan or the expenses those are required for maintaining the

business function for any entity. Generally the operational budget includes projected labour and

material cost required for running the business and for manufacturing the products or for providing

services. Operational budget is used for –

Managing current expenses – it can be used by the management for focussing on the current

expenses through comparing the same through the actual result. It further helps is

identifying the areas with more expenses and the profitable areas.

Equity multiplier – it is used for measuring the company’s financial leverage that is the proportion

of capital funded through borrowing and proportion funded through equity. The company’s equity

multiplier ratio of 1.16 and 1.17 in 2016 and 2017 is signifying that the company has significantly

low amount of debt as compared to equity. Hence, the company follows conservative policy is

taking debt.

Profitability ratio – profitability ratio is used for measuring the profit earning capability of the

company. Considering all the profitability ratios of the entity it can be identified that all ratios are in

improving trend and the major reason is the increase in revenue that led to increase in all the

profitability metrics.

Turnover ratio – it measures the ability of the company to in converting its balance sheet items into

income statement items. Account receivable settlement period had been reduced from 40.51 days to

39.95 days whereas the average number of inventory days increased from 9.99 days to 10.39 days

(Sponem & Lambert, 2016).

Short term financial stability – looking into the short term stability of the company it can be

identified that both current ratio as well as the acid test ratio of the entity has been improved over

the years from 2016 to 2017. It is signifying that the company is financially stable.

Long-term financial stability – looking into the long term stability of the company it can be

identified that the company has significantly low amount of debt as compared to equity. Further, the

operating profits are sufficient to cover the interest payment as high as 39.70 times. It is signifying

that the company is financially stable (Foster, 2017).

Task 2

1. Purpose of operational budget

Operational budget is the plan or the expenses those are required for maintaining the

business function for any entity. Generally the operational budget includes projected labour and

material cost required for running the business and for manufacturing the products or for providing

services. Operational budget is used for –

Managing current expenses – it can be used by the management for focussing on the current

expenses through comparing the same through the actual result. It further helps is

identifying the areas with more expenses and the profitable areas.

5TOURISM AND HOSPITALIT CONTROL

Projecting the future expenses – it helps in projecting future expenses based on the trend of

current expenses. Based on the past projection like over estimation or under estimation it

helps in making proper adjustments while projecting the expenses for future period (Dudin

et al., 2015).

Use of budget in tourism and hospitality industry

Budgets are used in tourism and hospitality industry to measure the performance and setting

up the financial target. It is not only used for planning for the future but also for setting up the target

and improving the performance of individual department or sector. In tourism and hospitality

industry budget can be used for various key factors like projecting the revenues, expenses and costs

based on the past performances. It can also be used for identifying the less productive or

unproductive area of business and taking decisions regarding whether to close down the sector or

apply any other technique to improve the same. Moreover, it helps is finalising the information with

the department manager before incorporating the same into the report (Vargas-Hernández, Cárdenaz

& Vargas, 2019)

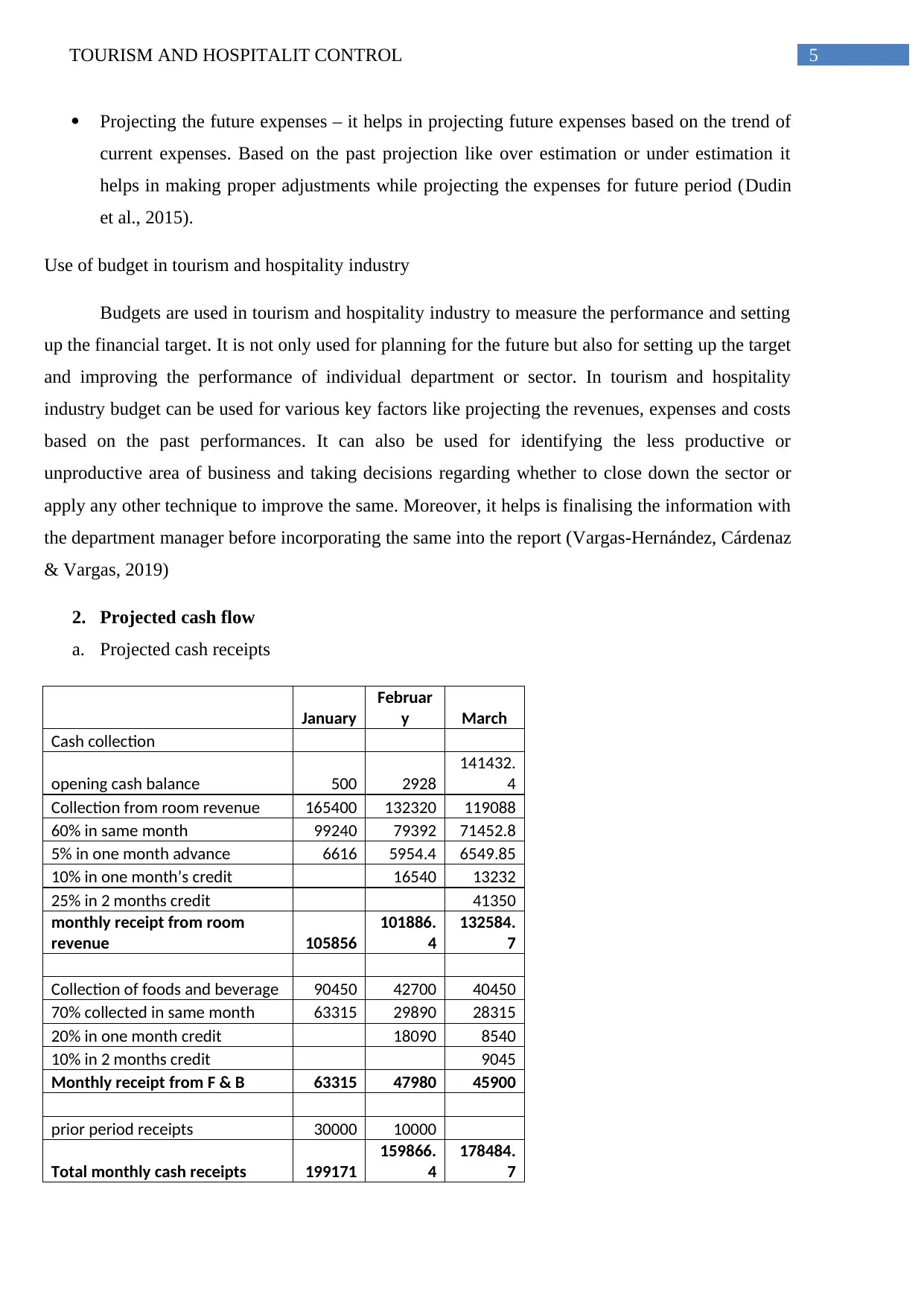

2. Projected cash flow

a. Projected cash receipts

January

Februar

y March

Cash collection

opening cash balance 500 2928

141432.

4

Collection from room revenue 165400 132320 119088

60% in same month 99240 79392 71452.8

5% in one month advance 6616 5954.4 6549.85

10% in one month’s credit 16540 13232

25% in 2 months credit 41350

monthly receipt from room

revenue 105856

101886.

4

132584.

7

Collection of foods and beverage 90450 42700 40450

70% collected in same month 63315 29890 28315

20% in one month credit 18090 8540

10% in 2 months credit 9045

Monthly receipt from F & B 63315 47980 45900

prior period receipts 30000 10000

Total monthly cash receipts 199171

159866.

4

178484.

7

Projecting the future expenses – it helps in projecting future expenses based on the trend of

current expenses. Based on the past projection like over estimation or under estimation it

helps in making proper adjustments while projecting the expenses for future period (Dudin

et al., 2015).

Use of budget in tourism and hospitality industry

Budgets are used in tourism and hospitality industry to measure the performance and setting

up the financial target. It is not only used for planning for the future but also for setting up the target

and improving the performance of individual department or sector. In tourism and hospitality

industry budget can be used for various key factors like projecting the revenues, expenses and costs

based on the past performances. It can also be used for identifying the less productive or

unproductive area of business and taking decisions regarding whether to close down the sector or

apply any other technique to improve the same. Moreover, it helps is finalising the information with

the department manager before incorporating the same into the report (Vargas-Hernández, Cárdenaz

& Vargas, 2019)

2. Projected cash flow

a. Projected cash receipts

January

Februar

y March

Cash collection

opening cash balance 500 2928

141432.

4

Collection from room revenue 165400 132320 119088

60% in same month 99240 79392 71452.8

5% in one month advance 6616 5954.4 6549.85

10% in one month’s credit 16540 13232

25% in 2 months credit 41350

monthly receipt from room

revenue 105856

101886.

4

132584.

7

Collection of foods and beverage 90450 42700 40450

70% collected in same month 63315 29890 28315

20% in one month credit 18090 8540

10% in 2 months credit 9045

Monthly receipt from F & B 63315 47980 45900

prior period receipts 30000 10000

Total monthly cash receipts 199171

159866.

4

178484.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TOURISM AND HOSPITALIT CONTROL

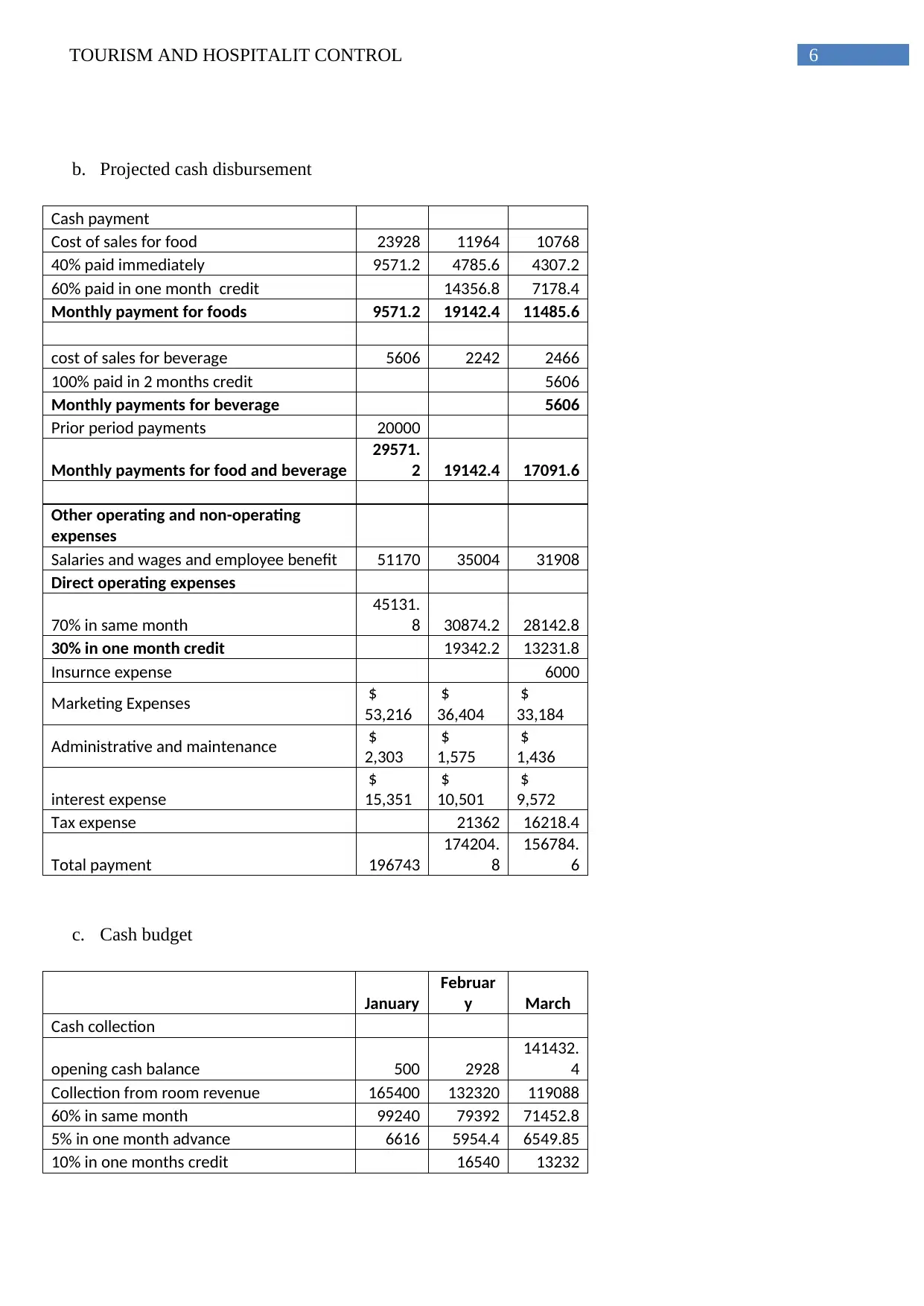

b. Projected cash disbursement

Cash payment

Cost of sales for food 23928 11964 10768

40% paid immediately 9571.2 4785.6 4307.2

60% paid in one month credit 14356.8 7178.4

Monthly payment for foods 9571.2 19142.4 11485.6

cost of sales for beverage 5606 2242 2466

100% paid in 2 months credit 5606

Monthly payments for beverage 5606

Prior period payments 20000

Monthly payments for food and beverage

29571.

2 19142.4 17091.6

Other operating and non-operating

expenses

Salaries and wages and employee benefit 51170 35004 31908

Direct operating expenses

70% in same month

45131.

8 30874.2 28142.8

30% in one month credit 19342.2 13231.8

Insurnce expense 6000

Marketing Expenses $

53,216

$

36,404

$

33,184

Administrative and maintenance $

2,303

$

1,575

$

1,436

interest expense

$

15,351

$

10,501

$

9,572

Tax expense 21362 16218.4

Total payment 196743

174204.

8

156784.

6

c. Cash budget

January

Februar

y March

Cash collection

opening cash balance 500 2928

141432.

4

Collection from room revenue 165400 132320 119088

60% in same month 99240 79392 71452.8

5% in one month advance 6616 5954.4 6549.85

10% in one months credit 16540 13232

b. Projected cash disbursement

Cash payment

Cost of sales for food 23928 11964 10768

40% paid immediately 9571.2 4785.6 4307.2

60% paid in one month credit 14356.8 7178.4

Monthly payment for foods 9571.2 19142.4 11485.6

cost of sales for beverage 5606 2242 2466

100% paid in 2 months credit 5606

Monthly payments for beverage 5606

Prior period payments 20000

Monthly payments for food and beverage

29571.

2 19142.4 17091.6

Other operating and non-operating

expenses

Salaries and wages and employee benefit 51170 35004 31908

Direct operating expenses

70% in same month

45131.

8 30874.2 28142.8

30% in one month credit 19342.2 13231.8

Insurnce expense 6000

Marketing Expenses $

53,216

$

36,404

$

33,184

Administrative and maintenance $

2,303

$

1,575

$

1,436

interest expense

$

15,351

$

10,501

$

9,572

Tax expense 21362 16218.4

Total payment 196743

174204.

8

156784.

6

c. Cash budget

January

Februar

y March

Cash collection

opening cash balance 500 2928

141432.

4

Collection from room revenue 165400 132320 119088

60% in same month 99240 79392 71452.8

5% in one month advance 6616 5954.4 6549.85

10% in one months credit 16540 13232

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TOURISM AND HOSPITALIT CONTROL

25% in 2 months credit 41350

monthly receipt from room revenue 105856

101886.

4

132584.

7

Collection of foods and beverage 90450 42700 40450

70% collected in same month 63315 29890 28315

20% in one month credit 18090 8540

10% in 2 months credit 9045

Monthly receipt from F & B 63315 47980 45900

prior period receipts 30000 10000

Total monthly cash receipts 199171

159866.

4

178484.

7

Cash payment

Cost of sales for food 23928 11964 10768

40% paid immediatel 9571.2 4785.6 4307.2

60% paid in one month credit 14356.8 7178.4

Monthly paymnet for foods 9571.2 19142.4 11485.6

cost of sales for beverage 5606 2242 2466

100% paid in 2 months credit 5606

Monthly payments for beverage 5606

Prior period payments 20000

Monthly payments for food and beverage

29571.

2 19142.4 17091.6

Other operating and non-operating

expenses

Salaries and wages and employee benefit 51170 35004 31908

Direct operating expenses

70% in same month

45131.

8 30874.2 28142.8

30% in one month credit 19342.2 13231.8

Insurance expense 6000

Marketing Expenses $

53,216

$

36,404

$

33,184

Administrative and maintenance $

2,303

$

1,575

$

1,436

interest expense

$

15,351

$

10,501

$

9,572

Tax expense 21362 16218.4

Total payment 196743

174204.

8

156784.

6

Closing cash balance 2928

141432.

4

163132.

5

25% in 2 months credit 41350

monthly receipt from room revenue 105856

101886.

4

132584.

7

Collection of foods and beverage 90450 42700 40450

70% collected in same month 63315 29890 28315

20% in one month credit 18090 8540

10% in 2 months credit 9045

Monthly receipt from F & B 63315 47980 45900

prior period receipts 30000 10000

Total monthly cash receipts 199171

159866.

4

178484.

7

Cash payment

Cost of sales for food 23928 11964 10768

40% paid immediatel 9571.2 4785.6 4307.2

60% paid in one month credit 14356.8 7178.4

Monthly paymnet for foods 9571.2 19142.4 11485.6

cost of sales for beverage 5606 2242 2466

100% paid in 2 months credit 5606

Monthly payments for beverage 5606

Prior period payments 20000

Monthly payments for food and beverage

29571.

2 19142.4 17091.6

Other operating and non-operating

expenses

Salaries and wages and employee benefit 51170 35004 31908

Direct operating expenses

70% in same month

45131.

8 30874.2 28142.8

30% in one month credit 19342.2 13231.8

Insurance expense 6000

Marketing Expenses $

53,216

$

36,404

$

33,184

Administrative and maintenance $

2,303

$

1,575

$

1,436

interest expense

$

15,351

$

10,501

$

9,572

Tax expense 21362 16218.4

Total payment 196743

174204.

8

156784.

6

Closing cash balance 2928

141432.

4

163132.

5

8TOURISM AND HOSPITALIT CONTROL

3. Liquidity balance

a. Surplus or deficit

During the 1st quarter of the year the company will have surplus cash flows amounting to

29,28,000, 141432400 and 163132500 for January, February and March consecutively.

b. Possible changes

For improving the cash balance the company shall reduce the credit period allowed to the

airline companies and shall make early payments to the beverage suppliers. It will help to further

improve the company’s liquidity position

3. Liquidity balance

a. Surplus or deficit

During the 1st quarter of the year the company will have surplus cash flows amounting to

29,28,000, 141432400 and 163132500 for January, February and March consecutively.

b. Possible changes

For improving the cash balance the company shall reduce the credit period allowed to the

airline companies and shall make early payments to the beverage suppliers. It will help to further

improve the company’s liquidity position

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TOURISM AND HOSPITALIT CONTROL

Reference

Becker, S. D., Mahlendorf, M. D., Schäffer, U., & Thaten, M. (2016). Budgeting in times of

economic crisis. Contemporary Accounting Research, 33(4), 1489-1517.

Dudin, M., Kucuri, G., Fedorova, I., Dzusova, S., & Namitulina, A. (2015). The innovative business

model canvas in the system of effective budgeting. Asian Social Science, 11(7), 290-296.

Foster, T. A. (2017). Budget planning, budget control, business age, and financial performance in

small businesses.

Mohammadi, A. M., & Mahmudi, A. (2015). The Feasibility of Operational Budgeting

Implementation in Social Security Organization of East Azerbaijan Province. European Online

Journal of Natural and Social Sciences: Proceedings, 4(1 (s)), pp-878.

Pérez-Rave, J., Muñoz-Giraldo, L., & Correa-Morales, J. C. (2017). Use of control charts with

regression analysis for autocorrelated data in the context of logistic financial budgeting. Computers

& Industrial Engineering, 112, 71-83.

Polak, J. J., & Boughton, J. M. (2016). Streamlining the financial structure of the International

Monetary Fund. In Economic Theory and Financial Policy (pp. 175-199). Routledge.

Sponem, S., & Lambert, C. (2016). Exploring differences in budget characteristics, roles and

satisfaction: A configurational approach. Management Accounting Research, 30, 47-61.

Vargas-Hernández, J. G., Cárdenaz, R. C., & Vargas, O. B. (2019). The Budget In The Financial

Management Of The Smes Assisted By The Administrative Process As A Competitive

Tool. Revista Intercontinental De Gestão Desportiva-Rigd, 8(3), 15-35.

Reference

Becker, S. D., Mahlendorf, M. D., Schäffer, U., & Thaten, M. (2016). Budgeting in times of

economic crisis. Contemporary Accounting Research, 33(4), 1489-1517.

Dudin, M., Kucuri, G., Fedorova, I., Dzusova, S., & Namitulina, A. (2015). The innovative business

model canvas in the system of effective budgeting. Asian Social Science, 11(7), 290-296.

Foster, T. A. (2017). Budget planning, budget control, business age, and financial performance in

small businesses.

Mohammadi, A. M., & Mahmudi, A. (2015). The Feasibility of Operational Budgeting

Implementation in Social Security Organization of East Azerbaijan Province. European Online

Journal of Natural and Social Sciences: Proceedings, 4(1 (s)), pp-878.

Pérez-Rave, J., Muñoz-Giraldo, L., & Correa-Morales, J. C. (2017). Use of control charts with

regression analysis for autocorrelated data in the context of logistic financial budgeting. Computers

& Industrial Engineering, 112, 71-83.

Polak, J. J., & Boughton, J. M. (2016). Streamlining the financial structure of the International

Monetary Fund. In Economic Theory and Financial Policy (pp. 175-199). Routledge.

Sponem, S., & Lambert, C. (2016). Exploring differences in budget characteristics, roles and

satisfaction: A configurational approach. Management Accounting Research, 30, 47-61.

Vargas-Hernández, J. G., Cárdenaz, R. C., & Vargas, O. B. (2019). The Budget In The Financial

Management Of The Smes Assisted By The Administrative Process As A Competitive

Tool. Revista Intercontinental De Gestão Desportiva-Rigd, 8(3), 15-35.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.