Comprehensive Analysis: Financial Resource Management and Performance

VerifiedAdded on 2020/04/07

|32

|5887

|102

Report

AI Summary

This comprehensive report examines the management of financial resources and performance, encompassing various aspects such as evaluating performance, planning and control, and contemporary management accounting methodologies. The report delves into key performance ratios, accounting treatments, and comparative performance analysis, specifically focusing on Microsoft. It explores cost management techniques, including job, process, and contract costing, along with fixed and variable cost distinctions. Cost-volume-profit analysis, relevant cost applications, and traditional budgeting are also discussed. The report further analyzes activity-based management, lean enterprise concepts, and value chain analysis, alongside methods of resource allocation and capital investment techniques. International financial markets and the tensions between financial and strategic objectives are also considered. The report provides a detailed understanding of financial resource management practices.

MANAGEMENT OF FINANCIAL

RESOURCES AND PERFORMANCE

RESOURCES AND PERFORMANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Part- 1 Evaluating performance and appraising limitations............................................................3

Part 2- Planning and control of an organization’s Resources..........................................................5

Part3- Contemporary Management Accounting Methodology.......................................................8

Part- 4 Methods of Resource Allocation for Achieving Corporate Strategy.................................11

Part 5-Tensions between Financial and Strategic Objectives........................................................14

Part 6 Capital Investment Techniques...........................................................................................17

Part 7- International Financial Market...........................................................................................19

Part 8-.............................................................................................................................................22

Appendix 1.....................................................................................................................................27

Appendix 2.....................................................................................................................................28

Appendix 3.....................................................................................................................................28

References......................................................................................................................................29

TABLE OF FIGURES

Figure 1: Process of ABC................................................................................................................9

Figure 2: Model of Activity Based Costing...................................................................................10

Figure 3: Microsoft value chain analysis.......................................................................................11

Figure 4: qualitative and quantitative issues of strategic performance..........................................20

Figure 5: Approaches to managing risk.........................................................................................21

Figure 6: Indirect benefits of International Finance......................................................................22

Figure 7: various sources of finance..............................................................................................23

Figure 8: Risk map for resolving issues........................................................................................25

Part- 1 Evaluating performance and appraising limitations............................................................3

Part 2- Planning and control of an organization’s Resources..........................................................5

Part3- Contemporary Management Accounting Methodology.......................................................8

Part- 4 Methods of Resource Allocation for Achieving Corporate Strategy.................................11

Part 5-Tensions between Financial and Strategic Objectives........................................................14

Part 6 Capital Investment Techniques...........................................................................................17

Part 7- International Financial Market...........................................................................................19

Part 8-.............................................................................................................................................22

Appendix 1.....................................................................................................................................27

Appendix 2.....................................................................................................................................28

Appendix 3.....................................................................................................................................28

References......................................................................................................................................29

TABLE OF FIGURES

Figure 1: Process of ABC................................................................................................................9

Figure 2: Model of Activity Based Costing...................................................................................10

Figure 3: Microsoft value chain analysis.......................................................................................11

Figure 4: qualitative and quantitative issues of strategic performance..........................................20

Figure 5: Approaches to managing risk.........................................................................................21

Figure 6: Indirect benefits of International Finance......................................................................22

Figure 7: various sources of finance..............................................................................................23

Figure 8: Risk map for resolving issues........................................................................................25

Part- 1 Evaluating performance and appraising limitations

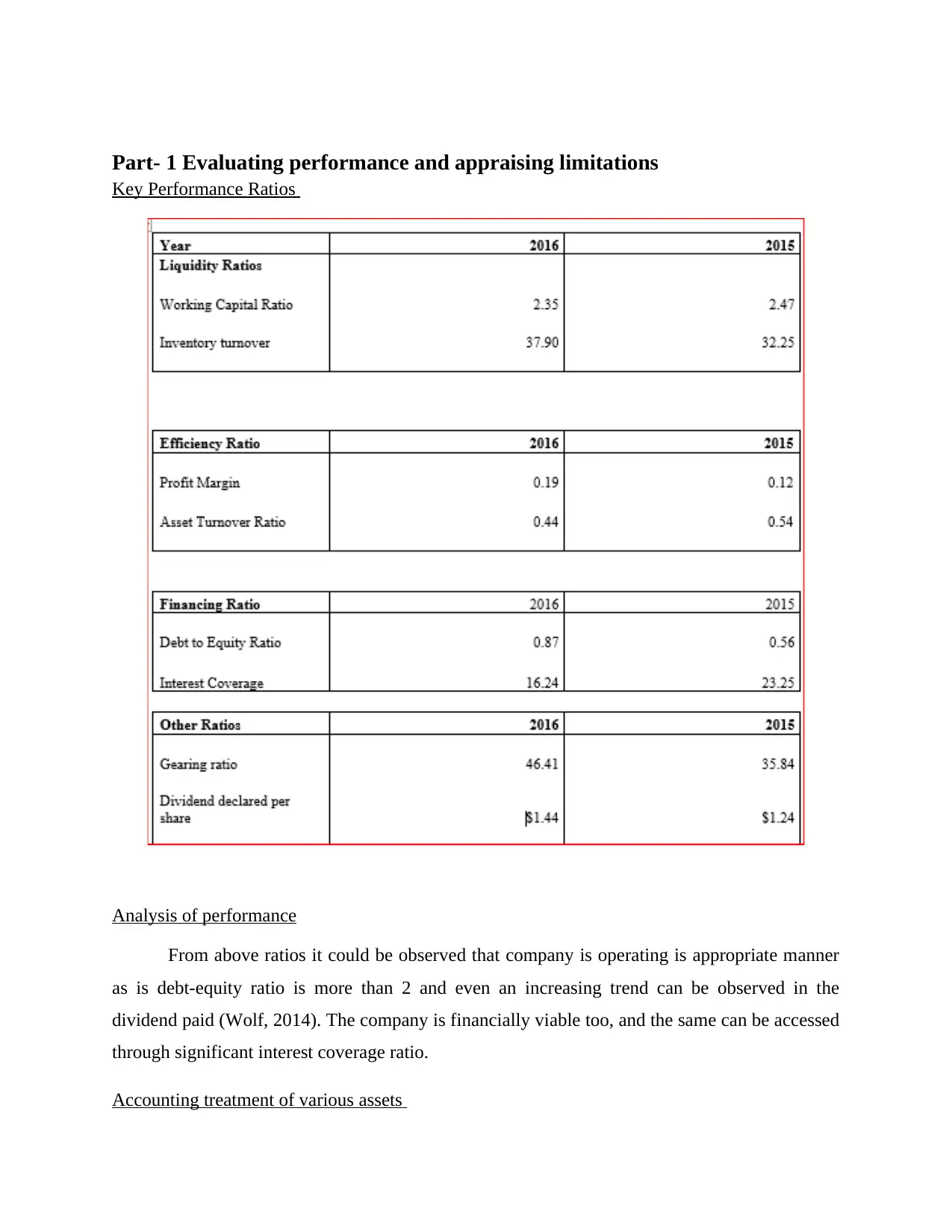

Key Performance Ratios

Analysis of performance

From above ratios it could be observed that company is operating is appropriate manner

as is debt-equity ratio is more than 2 and even an increasing trend can be observed in the

dividend paid (Wolf, 2014). The company is financially viable too, and the same can be accessed

through significant interest coverage ratio.

Accounting treatment of various assets

Key Performance Ratios

Analysis of performance

From above ratios it could be observed that company is operating is appropriate manner

as is debt-equity ratio is more than 2 and even an increasing trend can be observed in the

dividend paid (Wolf, 2014). The company is financially viable too, and the same can be accessed

through significant interest coverage ratio.

Accounting treatment of various assets

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

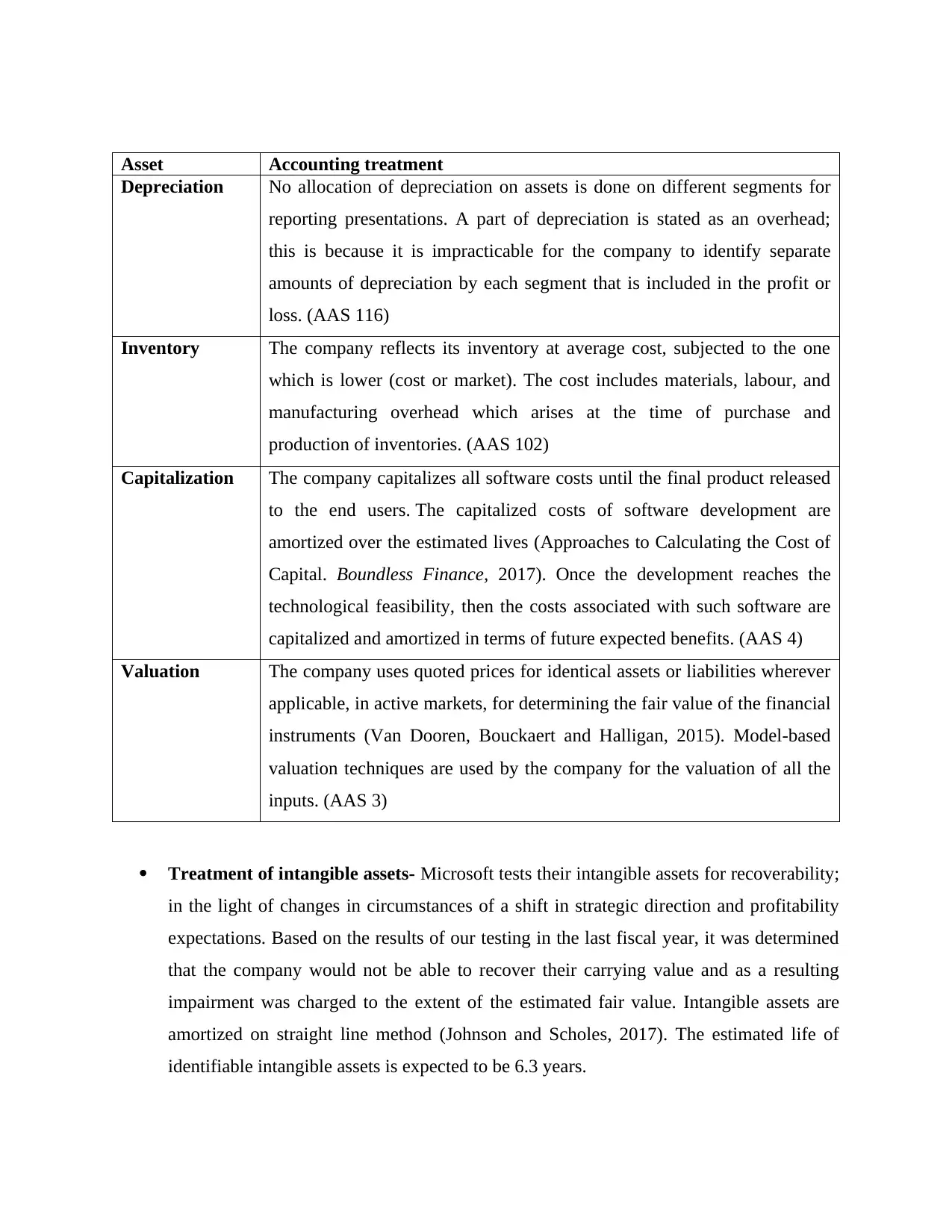

Asset Accounting treatment

Depreciation No allocation of depreciation on assets is done on different segments for

reporting presentations. A part of depreciation is stated as an overhead;

this is because it is impracticable for the company to identify separate

amounts of depreciation by each segment that is included in the profit or

loss. (AAS 116)

Inventory The company reflects its inventory at average cost, subjected to the one

which is lower (cost or market). The cost includes materials, labour, and

manufacturing overhead which arises at the time of purchase and

production of inventories. (AAS 102)

Capitalization The company capitalizes all software costs until the final product released

to the end users. The capitalized costs of software development are

amortized over the estimated lives (Approaches to Calculating the Cost of

Capital. Boundless Finance, 2017). Once the development reaches the

technological feasibility, then the costs associated with such software are

capitalized and amortized in terms of future expected benefits. (AAS 4)

Valuation The company uses quoted prices for identical assets or liabilities wherever

applicable, in active markets, for determining the fair value of the financial

instruments (Van Dooren, Bouckaert and Halligan, 2015). Model-based

valuation techniques are used by the company for the valuation of all the

inputs. (AAS 3)

Treatment of intangible assets- Microsoft tests their intangible assets for recoverability;

in the light of changes in circumstances of a shift in strategic direction and profitability

expectations. Based on the results of our testing in the last fiscal year, it was determined

that the company would not be able to recover their carrying value and as a resulting

impairment was charged to the extent of the estimated fair value. Intangible assets are

amortized on straight line method (Johnson and Scholes, 2017). The estimated life of

identifiable intangible assets is expected to be 6.3 years.

Depreciation No allocation of depreciation on assets is done on different segments for

reporting presentations. A part of depreciation is stated as an overhead;

this is because it is impracticable for the company to identify separate

amounts of depreciation by each segment that is included in the profit or

loss. (AAS 116)

Inventory The company reflects its inventory at average cost, subjected to the one

which is lower (cost or market). The cost includes materials, labour, and

manufacturing overhead which arises at the time of purchase and

production of inventories. (AAS 102)

Capitalization The company capitalizes all software costs until the final product released

to the end users. The capitalized costs of software development are

amortized over the estimated lives (Approaches to Calculating the Cost of

Capital. Boundless Finance, 2017). Once the development reaches the

technological feasibility, then the costs associated with such software are

capitalized and amortized in terms of future expected benefits. (AAS 4)

Valuation The company uses quoted prices for identical assets or liabilities wherever

applicable, in active markets, for determining the fair value of the financial

instruments (Van Dooren, Bouckaert and Halligan, 2015). Model-based

valuation techniques are used by the company for the valuation of all the

inputs. (AAS 3)

Treatment of intangible assets- Microsoft tests their intangible assets for recoverability;

in the light of changes in circumstances of a shift in strategic direction and profitability

expectations. Based on the results of our testing in the last fiscal year, it was determined

that the company would not be able to recover their carrying value and as a resulting

impairment was charged to the extent of the estimated fair value. Intangible assets are

amortized on straight line method (Johnson and Scholes, 2017). The estimated life of

identifiable intangible assets is expected to be 6.3 years.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Differences in financial reporting- As per the analysis, there have been no differences

in the financial reporting of the company as compared to International Accounting

Standard.

1.3 Comparative Performance

After comparison of the financial performance of Microsoft to its competitors, it can be

said that the Total Revenue of the company decreased in 2015’s the 3 quarter -12.16 %. As

opposed to this, the revenue for other companies in the industry and the industry as a whole

increased by 29.94 %, in the same quarter (Shahzad, Rutherford and Sharfman, 2016). Although

Microsoft is a better performer from companies like Dow Jones Industrial, the company has been

continuously suffering from strong competition from Apple. Inc.

Microsoft mainly focuses on the analysis of processes undertaken within the organization

by fundamentally rethinking the way they improve customer service, reduce operational costs

thereby becoming world-class competitors (Saeidi and et al. 2015). Each process that either

result in finished good or as a base for the next process is evaluated separately. In the IT

industry’s which is multi-process, generic benchmarking is used to comparing information.

Part 2- Planning and control of an organization’s Resources

Treatment of indirect and direct cost- The direct costs are added to the cost of the product

whereas the indirect costs are reflected as an expense in the income statement or P&L account.

Different cost treatment of job, process and contracts

Job costing: as per this method, identification of costs is made for each work separately

because each job entails its own specifications and scope.

Contract costing: Contract costing is performed when the company invites tenders for

web development which involve heavy expenditure during an extended period of time

(Wang and Sarkis, 2013).

Process costing- when a company engages in activities which involve a lot of processes

like that of Microsoft, this kind of costing is used. Microsoft develops its software

through a planned series of steps.

in the financial reporting of the company as compared to International Accounting

Standard.

1.3 Comparative Performance

After comparison of the financial performance of Microsoft to its competitors, it can be

said that the Total Revenue of the company decreased in 2015’s the 3 quarter -12.16 %. As

opposed to this, the revenue for other companies in the industry and the industry as a whole

increased by 29.94 %, in the same quarter (Shahzad, Rutherford and Sharfman, 2016). Although

Microsoft is a better performer from companies like Dow Jones Industrial, the company has been

continuously suffering from strong competition from Apple. Inc.

Microsoft mainly focuses on the analysis of processes undertaken within the organization

by fundamentally rethinking the way they improve customer service, reduce operational costs

thereby becoming world-class competitors (Saeidi and et al. 2015). Each process that either

result in finished good or as a base for the next process is evaluated separately. In the IT

industry’s which is multi-process, generic benchmarking is used to comparing information.

Part 2- Planning and control of an organization’s Resources

Treatment of indirect and direct cost- The direct costs are added to the cost of the product

whereas the indirect costs are reflected as an expense in the income statement or P&L account.

Different cost treatment of job, process and contracts

Job costing: as per this method, identification of costs is made for each work separately

because each job entails its own specifications and scope.

Contract costing: Contract costing is performed when the company invites tenders for

web development which involve heavy expenditure during an extended period of time

(Wang and Sarkis, 2013).

Process costing- when a company engages in activities which involve a lot of processes

like that of Microsoft, this kind of costing is used. Microsoft develops its software

through a planned series of steps.

Absorption costing- This costing type has its origin from managerial accounting which

expenses all costs associated with developing a particular product; this type of costing is

the time required by external reporting GAAP (generally accepted accounting principles).

Absorption costing is done for costs which are directly relatable to the development of

the product (Tantalo and Priem, 2016).

Distinction between fixed and variable cost

A company's cost which is linked to the amount of goods or services it produces is called

variable cost. The variable cost of the company increases and decreases with the volume of

production undertaken. On the other hand, the costs which do not vary with the level of output

are known as a fixed cost. This part of cost remains constant at each level of production.

Cost volume profit analysis Short-term decision analysis

The analysis is applied to ascertain the

manner in which change in cost and volume

affects operating as well as net income of

company (Harrison and Wicks, 2013). For

accomplishing the analysis, various

components such as sale price per unit are

assumed constant.

This technique is used by the company as a

new way for evaluating costs which assist in

managerial decision making. Instead of

evaluating components of cost this analysis,

re-arranges the costs into variable costs, fixed

costs, and mixed costs (Rivera, Muñoz and

Moneva, 2017). In this technique, the company

allocates salary to fixed costs and bonus to

variable costs.

Relevant cost and its application to decision-making

The objective cost of a business decision is determined by relevant costs. An objective

measure cost of a decision is a number of cash outflows that result from its implementation.

Thus, it assists in decision making through revealing the amount of cash outflow resulting from a

cost. Some of the relevant costs are future cash flows, avoidable cost, opportunity cost and

incremental cost.

Role and Limitations of Traditional Budgets

expenses all costs associated with developing a particular product; this type of costing is

the time required by external reporting GAAP (generally accepted accounting principles).

Absorption costing is done for costs which are directly relatable to the development of

the product (Tantalo and Priem, 2016).

Distinction between fixed and variable cost

A company's cost which is linked to the amount of goods or services it produces is called

variable cost. The variable cost of the company increases and decreases with the volume of

production undertaken. On the other hand, the costs which do not vary with the level of output

are known as a fixed cost. This part of cost remains constant at each level of production.

Cost volume profit analysis Short-term decision analysis

The analysis is applied to ascertain the

manner in which change in cost and volume

affects operating as well as net income of

company (Harrison and Wicks, 2013). For

accomplishing the analysis, various

components such as sale price per unit are

assumed constant.

This technique is used by the company as a

new way for evaluating costs which assist in

managerial decision making. Instead of

evaluating components of cost this analysis,

re-arranges the costs into variable costs, fixed

costs, and mixed costs (Rivera, Muñoz and

Moneva, 2017). In this technique, the company

allocates salary to fixed costs and bonus to

variable costs.

Relevant cost and its application to decision-making

The objective cost of a business decision is determined by relevant costs. An objective

measure cost of a decision is a number of cash outflows that result from its implementation.

Thus, it assists in decision making through revealing the amount of cash outflow resulting from a

cost. Some of the relevant costs are future cash flows, avoidable cost, opportunity cost and

incremental cost.

Role and Limitations of Traditional Budgets

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

A detailed statement of financial results that are predictable for a given period of time in

the future is known as the process of Budgeting. Traditional functional budgets can be effective

only when the organization is divided into many units which together contribute to

organizational goal (Mir and Pinnington, 2014). If the entity runs on the basis of annual goals, it

may need a functional budget for a short period just to keep the company on the right track.

Problems and motivational impact of functional annual budgets - The problem

associated with functional budgets is that it created unnecessary pressure in the mind of

the staff and promoted unhealthy competition (Guerreiro, 2015). However, if

communicated in a positive way can provide a guide to managers and their employees in

achieving the organizational objectives.

Alternatives to functional budgets

Budget Description

Activity-based budgets This type of budgeting is the one in which the

activities of the organization which incur

costs are recorded, and their relationships

with each other are defined and analyzed.

Continuous Budgets It is the process of continually adding months

to a multi-period budget with each passing

month by revising the assumptions of the

budget for every incremental period of the

budget (Endrikat, Guenther and Hoppe,

2014).

Beyond Budgeting Roundtable This technique emphasizes a holistic focus on

the objectives to be achieved and their

relation with the processes undertaken to

accomplish them. Microsoft encourages full-

scale recreation of processes instead of sub-

processes being optimized.

the future is known as the process of Budgeting. Traditional functional budgets can be effective

only when the organization is divided into many units which together contribute to

organizational goal (Mir and Pinnington, 2014). If the entity runs on the basis of annual goals, it

may need a functional budget for a short period just to keep the company on the right track.

Problems and motivational impact of functional annual budgets - The problem

associated with functional budgets is that it created unnecessary pressure in the mind of

the staff and promoted unhealthy competition (Guerreiro, 2015). However, if

communicated in a positive way can provide a guide to managers and their employees in

achieving the organizational objectives.

Alternatives to functional budgets

Budget Description

Activity-based budgets This type of budgeting is the one in which the

activities of the organization which incur

costs are recorded, and their relationships

with each other are defined and analyzed.

Continuous Budgets It is the process of continually adding months

to a multi-period budget with each passing

month by revising the assumptions of the

budget for every incremental period of the

budget (Endrikat, Guenther and Hoppe,

2014).

Beyond Budgeting Roundtable This technique emphasizes a holistic focus on

the objectives to be achieved and their

relation with the processes undertaken to

accomplish them. Microsoft encourages full-

scale recreation of processes instead of sub-

processes being optimized.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Part3- Contemporary Management Accounting Methodology

Role of Activity-Based Management

‘Relevance lost’ -The traditional system of accounting overhead is done through

allocating it to the product in the proportion of direct labour or machine hours which may

not reflect the actual consumption of resources. There is a relevant loss of useful

resources as the traditional management accounting fail to provide accurate product cost

(Grant, 2016). The traditional system of accounting has failed to keep pace with new

technologies by focusing on short-term profits instead of short-term financial measure of

non-performance. Traditional accounting focuses on volume-related drivers, like labour

hours, while the modern costing method uses transaction-based drivers, like a number of

orders received.

Appraisal of activity-based costing (ABC)-

This technique is considered as the modern alternative to the traditional system of accounting

that is absorption costing; this allows the managers to understand the product and net

profitability in a much better way. This also provides the management with improved

information for making value-based and leading to more effective managerial decisions. ABC

technique focuses on cost drivers- the activities increase costs. Thus this technique gives accurate

results in terms of cost and profitability.

Figure 1: Process of ABC

Activity-based costing fills the information needed for re-engineering and benchmarking by

providing cost of each activity separately. This costing method also provides operating

information about the true cost of services, products, processes, distribution channels, activities,

Role of Activity-Based Management

‘Relevance lost’ -The traditional system of accounting overhead is done through

allocating it to the product in the proportion of direct labour or machine hours which may

not reflect the actual consumption of resources. There is a relevant loss of useful

resources as the traditional management accounting fail to provide accurate product cost

(Grant, 2016). The traditional system of accounting has failed to keep pace with new

technologies by focusing on short-term profits instead of short-term financial measure of

non-performance. Traditional accounting focuses on volume-related drivers, like labour

hours, while the modern costing method uses transaction-based drivers, like a number of

orders received.

Appraisal of activity-based costing (ABC)-

This technique is considered as the modern alternative to the traditional system of accounting

that is absorption costing; this allows the managers to understand the product and net

profitability in a much better way. This also provides the management with improved

information for making value-based and leading to more effective managerial decisions. ABC

technique focuses on cost drivers- the activities increase costs. Thus this technique gives accurate

results in terms of cost and profitability.

Figure 1: Process of ABC

Activity-based costing fills the information needed for re-engineering and benchmarking by

providing cost of each activity separately. This costing method also provides operating

information about the true cost of services, products, processes, distribution channels, activities,

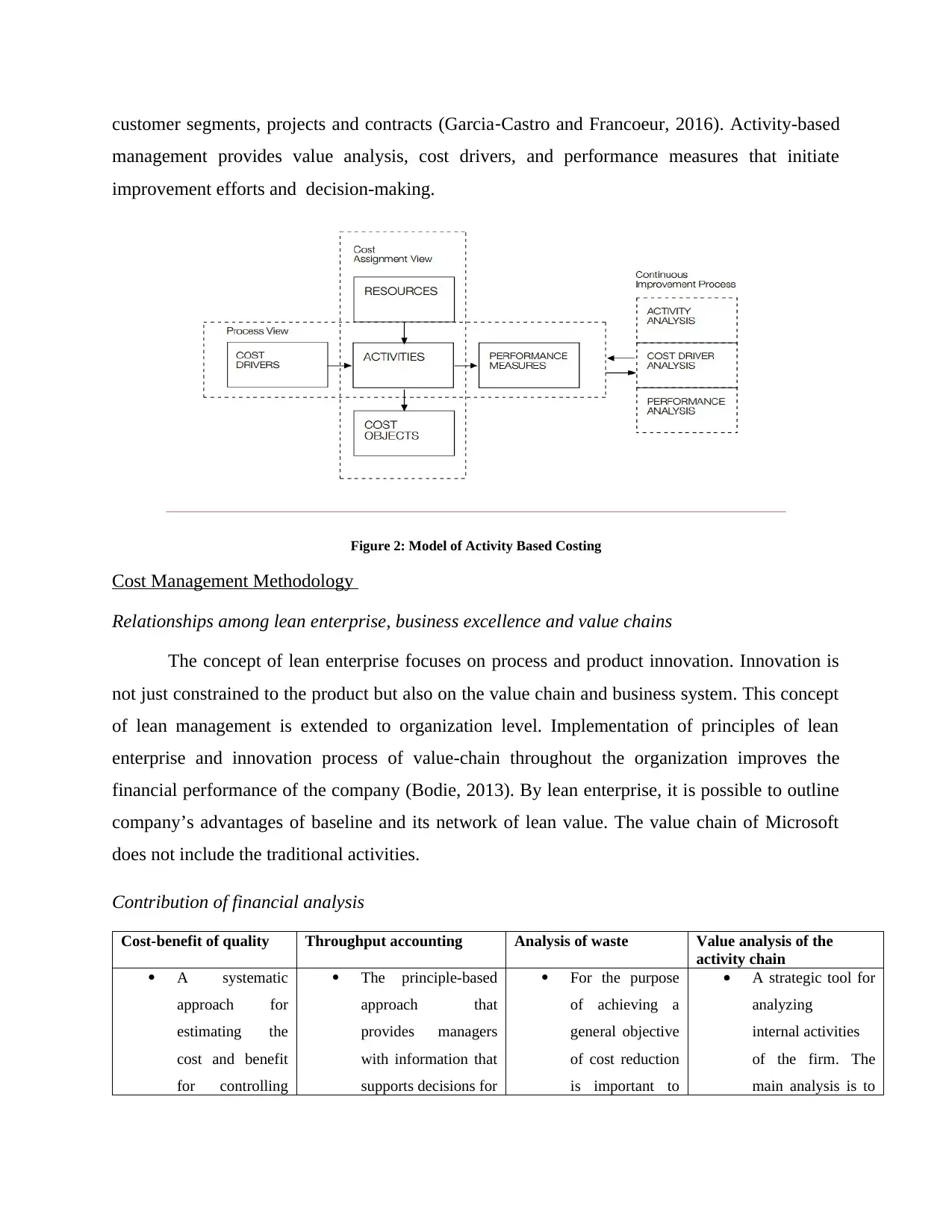

customer segments, projects and contracts (Garcia‐Castro and Francoeur, 2016). Activity-based

management provides value analysis, cost drivers, and performance measures that initiate

improvement efforts and decision-making.

Figure 2: Model of Activity Based Costing

Cost Management Methodology

Relationships among lean enterprise, business excellence and value chains

The concept of lean enterprise focuses on process and product innovation. Innovation is

not just constrained to the product but also on the value chain and business system. This concept

of lean management is extended to organization level. Implementation of principles of lean

enterprise and innovation process of value-chain throughout the organization improves the

financial performance of the company (Bodie, 2013). By lean enterprise, it is possible to outline

company’s advantages of baseline and its network of lean value. The value chain of Microsoft

does not include the traditional activities.

Contribution of financial analysis

Cost-benefit of quality Throughput accounting Analysis of waste Value analysis of the

activity chain

A systematic

approach for

estimating the

cost and benefit

for controlling

The principle-based

approach that

provides managers

with information that

supports decisions for

For the purpose

of achieving a

general objective

of cost reduction

is important to

A strategic tool for

analyzing

internal activities

of the firm. The

main analysis is to

management provides value analysis, cost drivers, and performance measures that initiate

improvement efforts and decision-making.

Figure 2: Model of Activity Based Costing

Cost Management Methodology

Relationships among lean enterprise, business excellence and value chains

The concept of lean enterprise focuses on process and product innovation. Innovation is

not just constrained to the product but also on the value chain and business system. This concept

of lean management is extended to organization level. Implementation of principles of lean

enterprise and innovation process of value-chain throughout the organization improves the

financial performance of the company (Bodie, 2013). By lean enterprise, it is possible to outline

company’s advantages of baseline and its network of lean value. The value chain of Microsoft

does not include the traditional activities.

Contribution of financial analysis

Cost-benefit of quality Throughput accounting Analysis of waste Value analysis of the

activity chain

A systematic

approach for

estimating the

cost and benefit

for controlling

The principle-based

approach that

provides managers

with information that

supports decisions for

For the purpose

of achieving a

general objective

of cost reduction

is important to

A strategic tool for

analyzing

internal activities

of the firm. The

main analysis is to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

quality. The

options that

provide benefits

are preserved.

improvement of

enterprise

profitability.

analyze the

activities which

do not contribute

to the product.

This is done by

process

management

through

implementation

of the lean

business process

model.

recognize

the activities which

are most valuable

to the entity and

the ones that need

improvement to

provide a

competitive

advantage.

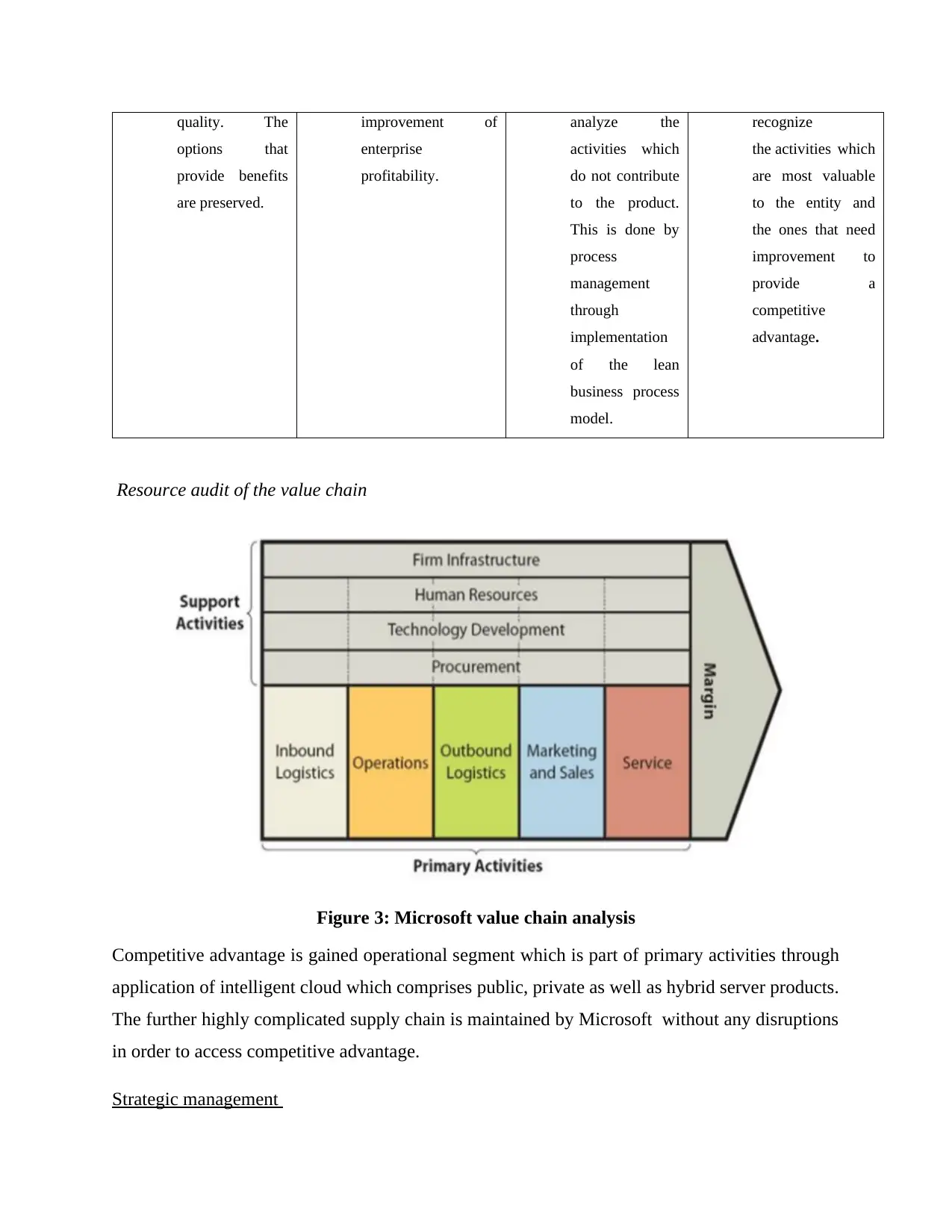

Resource audit of the value chain

Figure 3: Microsoft value chain analysis

Competitive advantage is gained operational segment which is part of primary activities through

application of intelligent cloud which comprises public, private as well as hybrid server products.

The further highly complicated supply chain is maintained by Microsoft without any disruptions

in order to access competitive advantage.

Strategic management

options that

provide benefits

are preserved.

improvement of

enterprise

profitability.

analyze the

activities which

do not contribute

to the product.

This is done by

process

management

through

implementation

of the lean

business process

model.

recognize

the activities which

are most valuable

to the entity and

the ones that need

improvement to

provide a

competitive

advantage.

Resource audit of the value chain

Figure 3: Microsoft value chain analysis

Competitive advantage is gained operational segment which is part of primary activities through

application of intelligent cloud which comprises public, private as well as hybrid server products.

The further highly complicated supply chain is maintained by Microsoft without any disruptions

in order to access competitive advantage.

Strategic management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

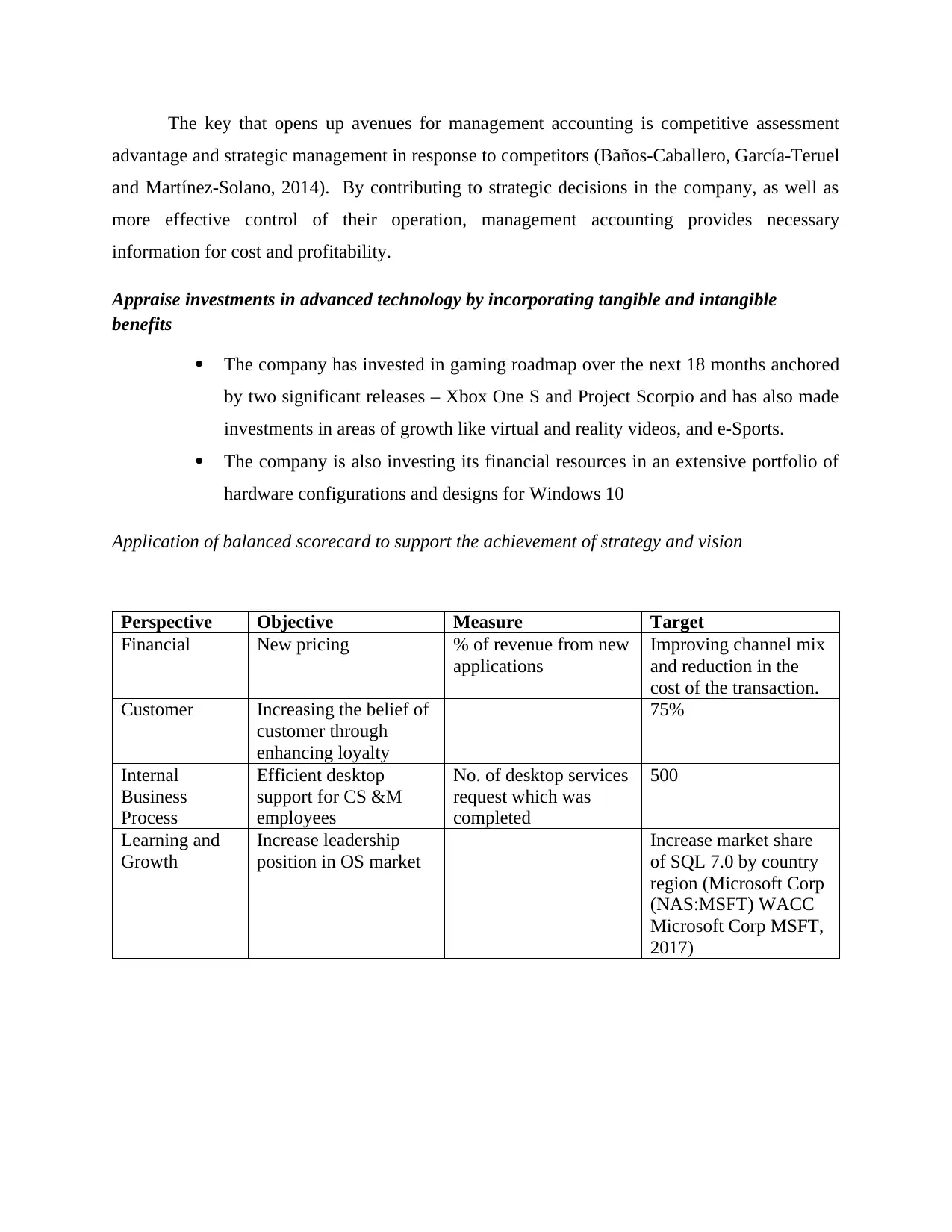

The key that opens up avenues for management accounting is competitive assessment

advantage and strategic management in response to competitors (Baños-Caballero, García-Teruel

and Martínez-Solano, 2014). By contributing to strategic decisions in the company, as well as

more effective control of their operation, management accounting provides necessary

information for cost and profitability.

Appraise investments in advanced technology by incorporating tangible and intangible

benefits

The company has invested in gaming roadmap over the next 18 months anchored

by two significant releases – Xbox One S and Project Scorpio and has also made

investments in areas of growth like virtual and reality videos, and e-Sports.

The company is also investing its financial resources in an extensive portfolio of

hardware configurations and designs for Windows 10

Application of balanced scorecard to support the achievement of strategy and vision

Perspective Objective Measure Target

Financial New pricing % of revenue from new

applications

Improving channel mix

and reduction in the

cost of the transaction.

Customer Increasing the belief of

customer through

enhancing loyalty

75%

Internal

Business

Process

Efficient desktop

support for CS &M

employees

No. of desktop services

request which was

completed

500

Learning and

Growth

Increase leadership

position in OS market

Increase market share

of SQL 7.0 by country

region (Microsoft Corp

(NAS:MSFT) WACC

Microsoft Corp MSFT,

2017)

advantage and strategic management in response to competitors (Baños-Caballero, García-Teruel

and Martínez-Solano, 2014). By contributing to strategic decisions in the company, as well as

more effective control of their operation, management accounting provides necessary

information for cost and profitability.

Appraise investments in advanced technology by incorporating tangible and intangible

benefits

The company has invested in gaming roadmap over the next 18 months anchored

by two significant releases – Xbox One S and Project Scorpio and has also made

investments in areas of growth like virtual and reality videos, and e-Sports.

The company is also investing its financial resources in an extensive portfolio of

hardware configurations and designs for Windows 10

Application of balanced scorecard to support the achievement of strategy and vision

Perspective Objective Measure Target

Financial New pricing % of revenue from new

applications

Improving channel mix

and reduction in the

cost of the transaction.

Customer Increasing the belief of

customer through

enhancing loyalty

75%

Internal

Business

Process

Efficient desktop

support for CS &M

employees

No. of desktop services

request which was

completed

500

Learning and

Growth

Increase leadership

position in OS market

Increase market share

of SQL 7.0 by country

region (Microsoft Corp

(NAS:MSFT) WACC

Microsoft Corp MSFT,

2017)

Part- 4 Methods of Resource Allocation for Achieving Corporate Strategy

Strategic planning: this is the first stage in resource allocation. This stage is concerned with

planning vision and goals for the future. The vision and strategic goals are accomplished through

achievement of objectives (Guerreiro, 2015).

Budgeting- in this stage, a budget is set for each activity to which the resources are to be

allocated. Resources are allocated on the basis of strategic planning and identifying that which

areas need maximum and minimum resources.

Logistical management- at this stage the resources are moved physically to areas requiring

them.

Criteria to evaluate the allocation of resources-

One of the most important tools used by Microsoft to assist and monitor the resource

allocation program is the APR technique. Annual Performance Report is a reporting tool

which is used to track progress and accomplishments of resource allocation programs and

inform the management about the competitive advantage (Grant, 2016). The APR can is

an effective management tool that provides with high data quality to evaluate the entire

process if resource allocation.

Identification and management of gaps between strategic need and availability-Gap

analysis provide the guide on how to develop strategies and initiatives for closing gaps

and mitigate associated risks by classifying activities on profitability and priority basis.

Re-engineering and business re-engineering

Microsoft continually seeks to radically restructure their organizations by concentrating

on the basic designs of their business processes. A business process can be reoffered to as set

tasks which are logically related to each other and capable of being performed to achieve a

defined outcome in the business.

Principles of re-engineering and its impact on management style

Radical redesign associated with BPR has a positive correlation with the processes and

performance of the organizational. In this way, the management enhances the potency and

Strategic planning: this is the first stage in resource allocation. This stage is concerned with

planning vision and goals for the future. The vision and strategic goals are accomplished through

achievement of objectives (Guerreiro, 2015).

Budgeting- in this stage, a budget is set for each activity to which the resources are to be

allocated. Resources are allocated on the basis of strategic planning and identifying that which

areas need maximum and minimum resources.

Logistical management- at this stage the resources are moved physically to areas requiring

them.

Criteria to evaluate the allocation of resources-

One of the most important tools used by Microsoft to assist and monitor the resource

allocation program is the APR technique. Annual Performance Report is a reporting tool

which is used to track progress and accomplishments of resource allocation programs and

inform the management about the competitive advantage (Grant, 2016). The APR can is

an effective management tool that provides with high data quality to evaluate the entire

process if resource allocation.

Identification and management of gaps between strategic need and availability-Gap

analysis provide the guide on how to develop strategies and initiatives for closing gaps

and mitigate associated risks by classifying activities on profitability and priority basis.

Re-engineering and business re-engineering

Microsoft continually seeks to radically restructure their organizations by concentrating

on the basic designs of their business processes. A business process can be reoffered to as set

tasks which are logically related to each other and capable of being performed to achieve a

defined outcome in the business.

Principles of re-engineering and its impact on management style

Radical redesign associated with BPR has a positive correlation with the processes and

performance of the organizational. In this way, the management enhances the potency and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 32

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.