Financial Performance Management: Costing and Budgeting Report

VerifiedAdded on 2022/12/28

|10

|1917

|39

Report

AI Summary

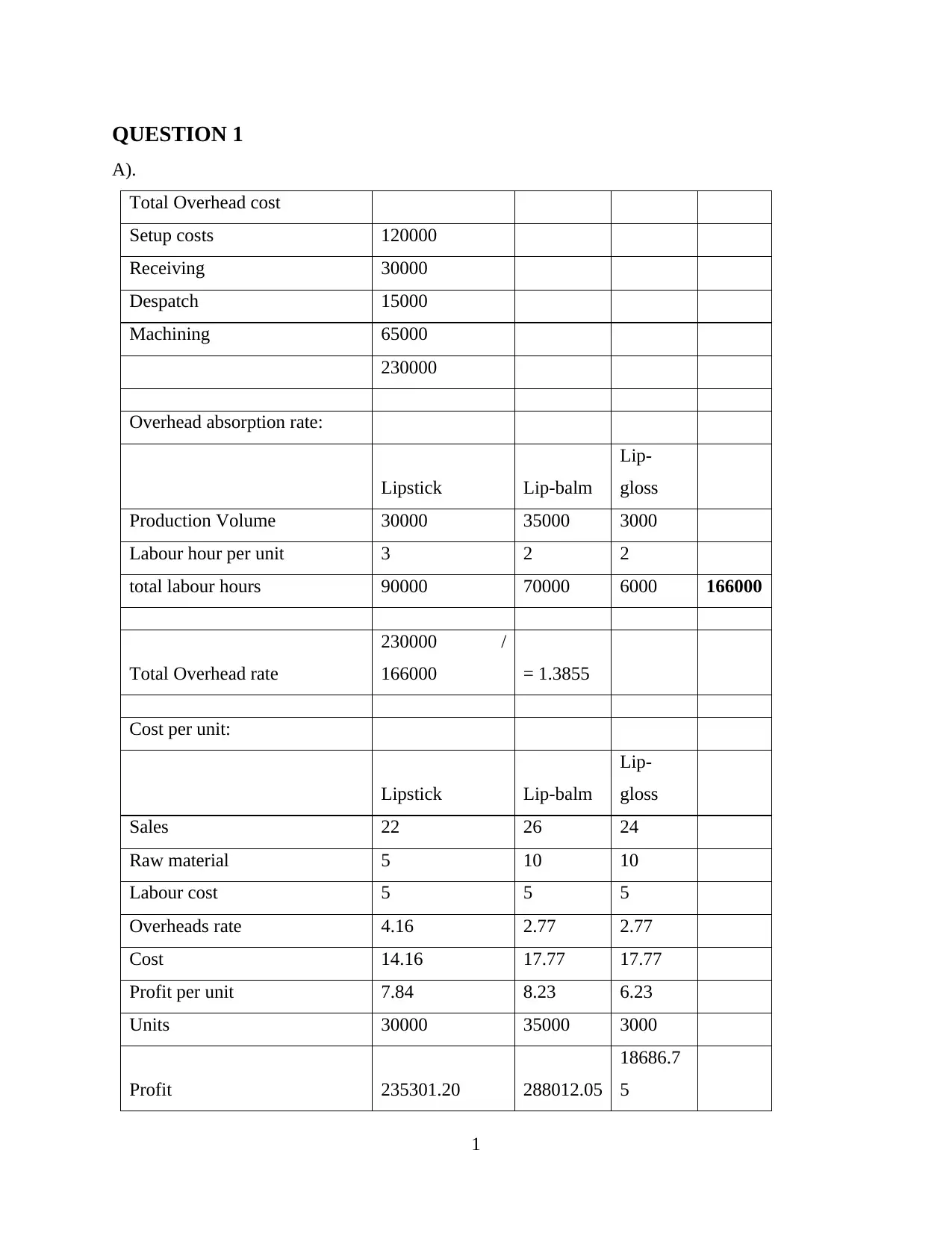

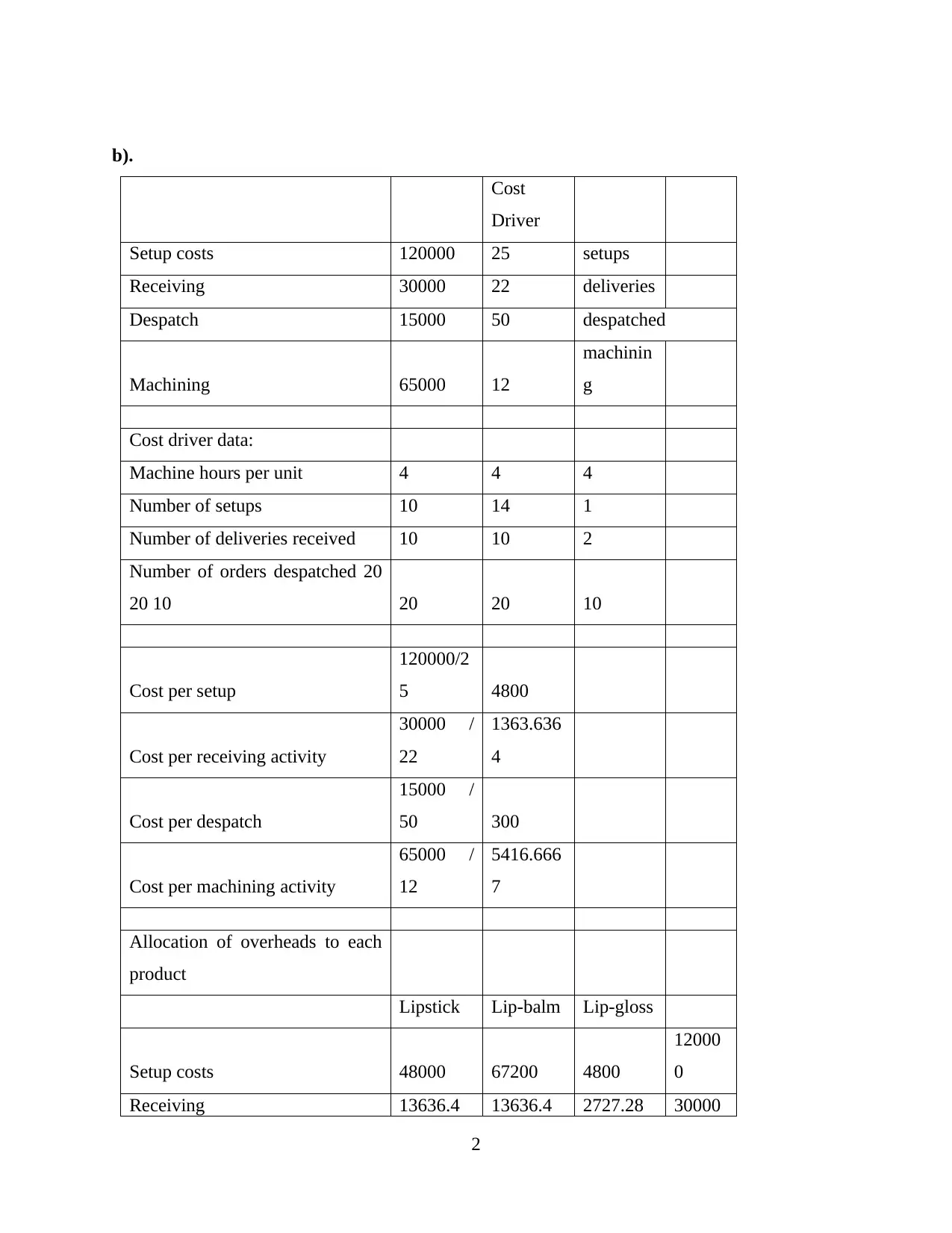

This report delves into the intricacies of financial performance management, offering a comprehensive analysis of costing methods, including absorption costing and activity-based costing (ABC). It examines overhead allocation, cost driver analysis, and the impact of different costing approaches on product profitability. The report also explores variance analysis, calculating material usage, mix, and yield variances, and discusses the implications of these variances on production management. Furthermore, it contrasts zero-based budgeting with incremental budgeting, outlining the advantages and disadvantages of each approach. The analysis includes sensitivity analysis, assessing how changes in input information impact model results. The report uses numerical examples and calculations to illustrate the concepts, providing a practical understanding of financial performance management principles.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.