Financial Performance Management Report: FNN 6800 Assessment Analysis

VerifiedAdded on 2022/12/28

|9

|1519

|45

Report

AI Summary

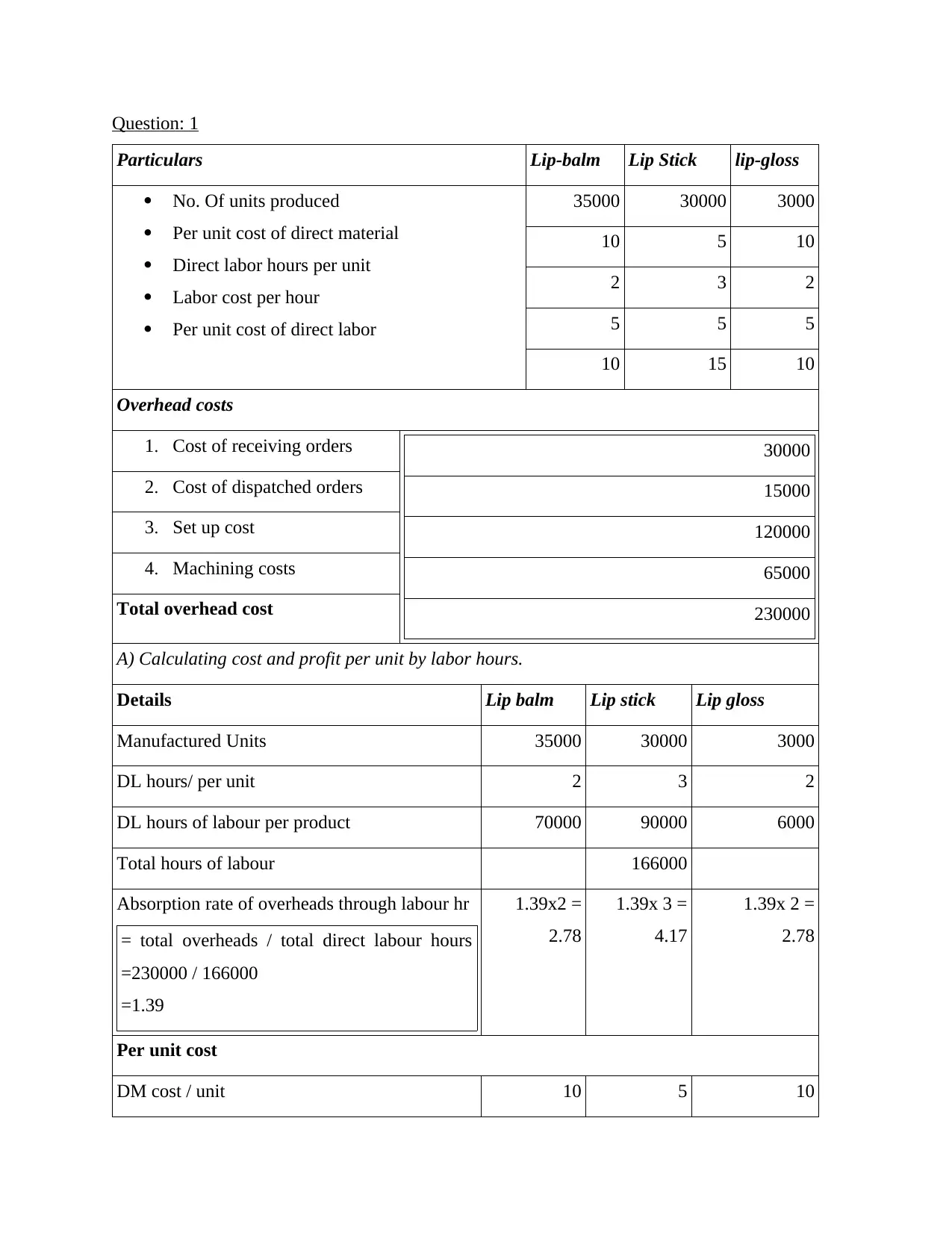

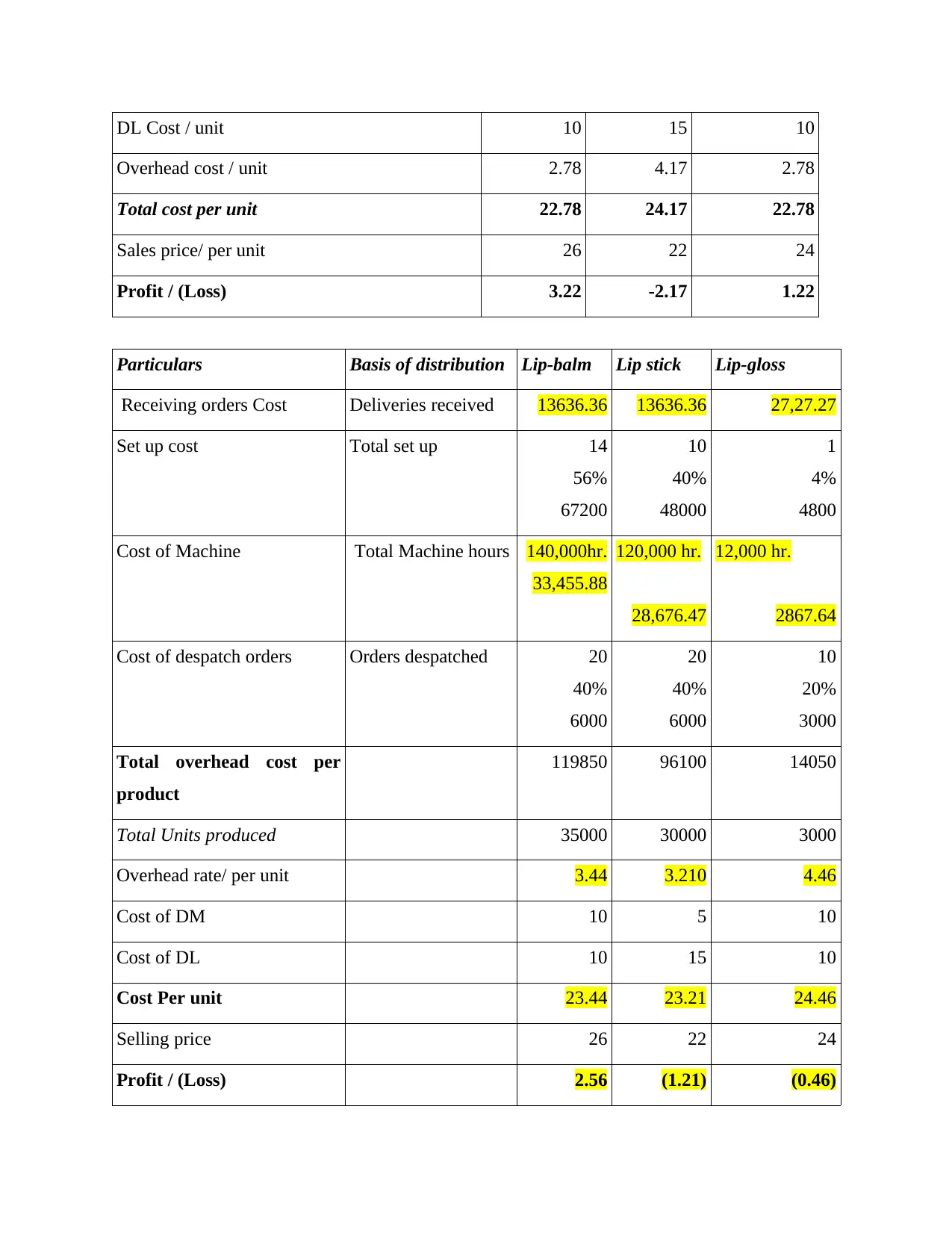

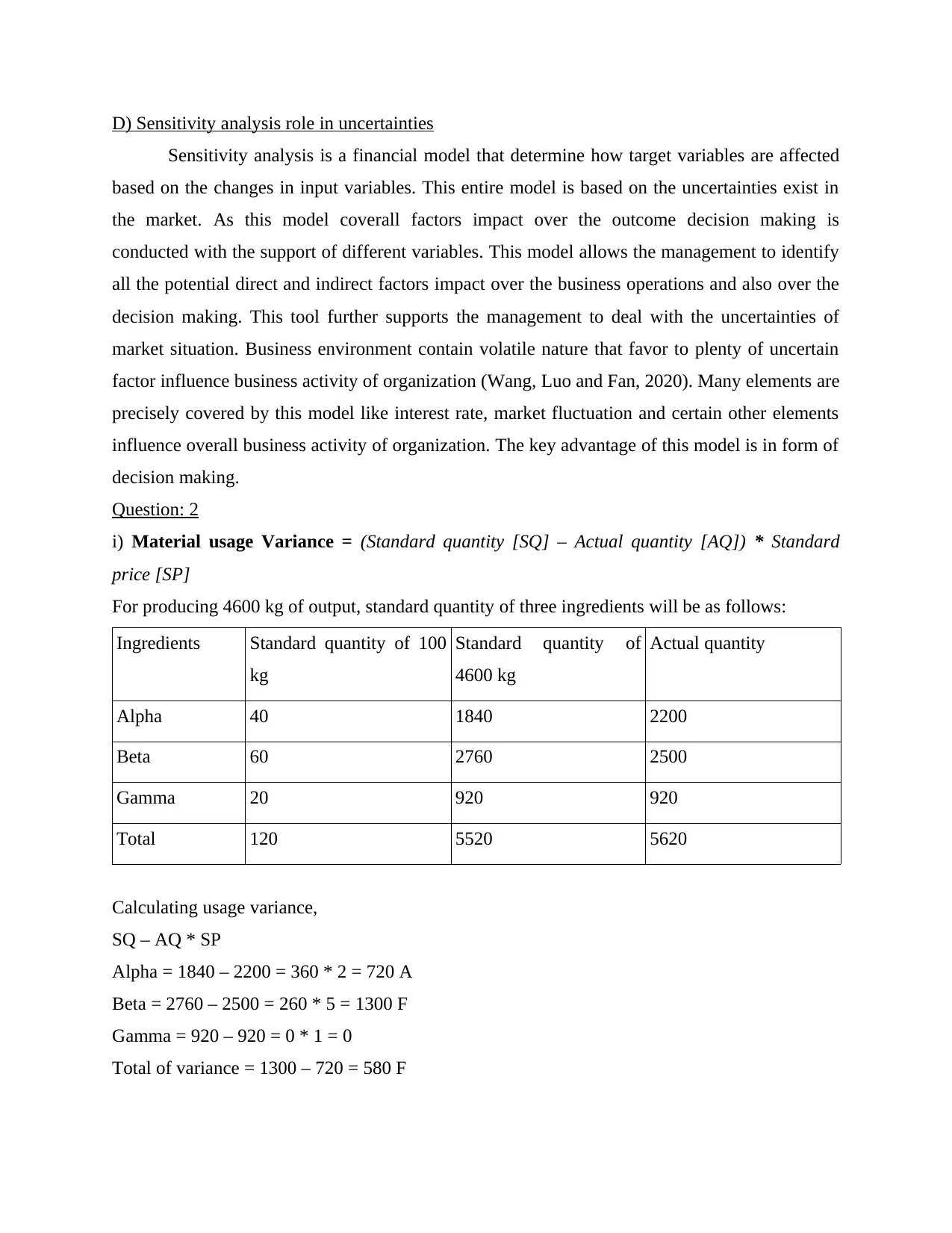

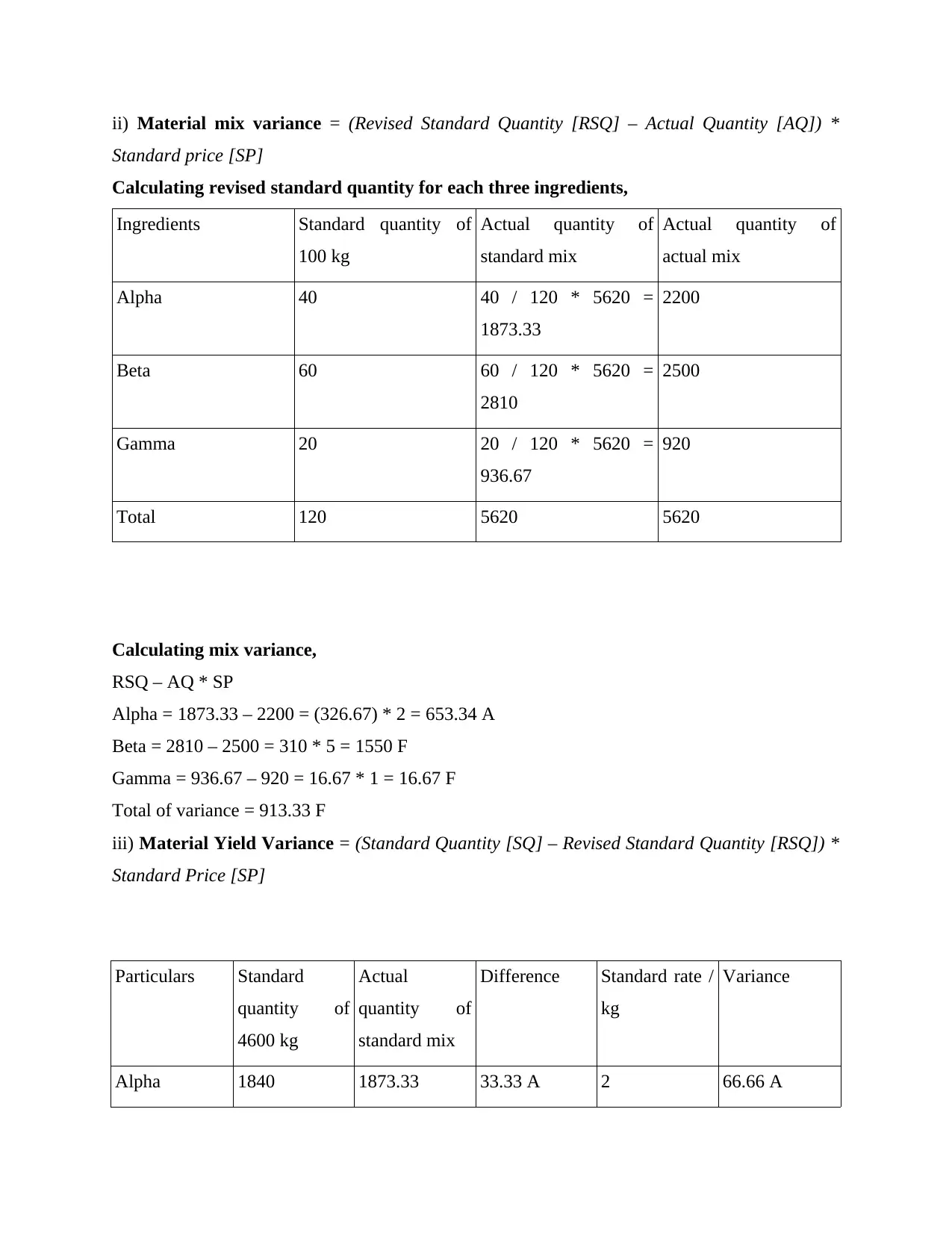

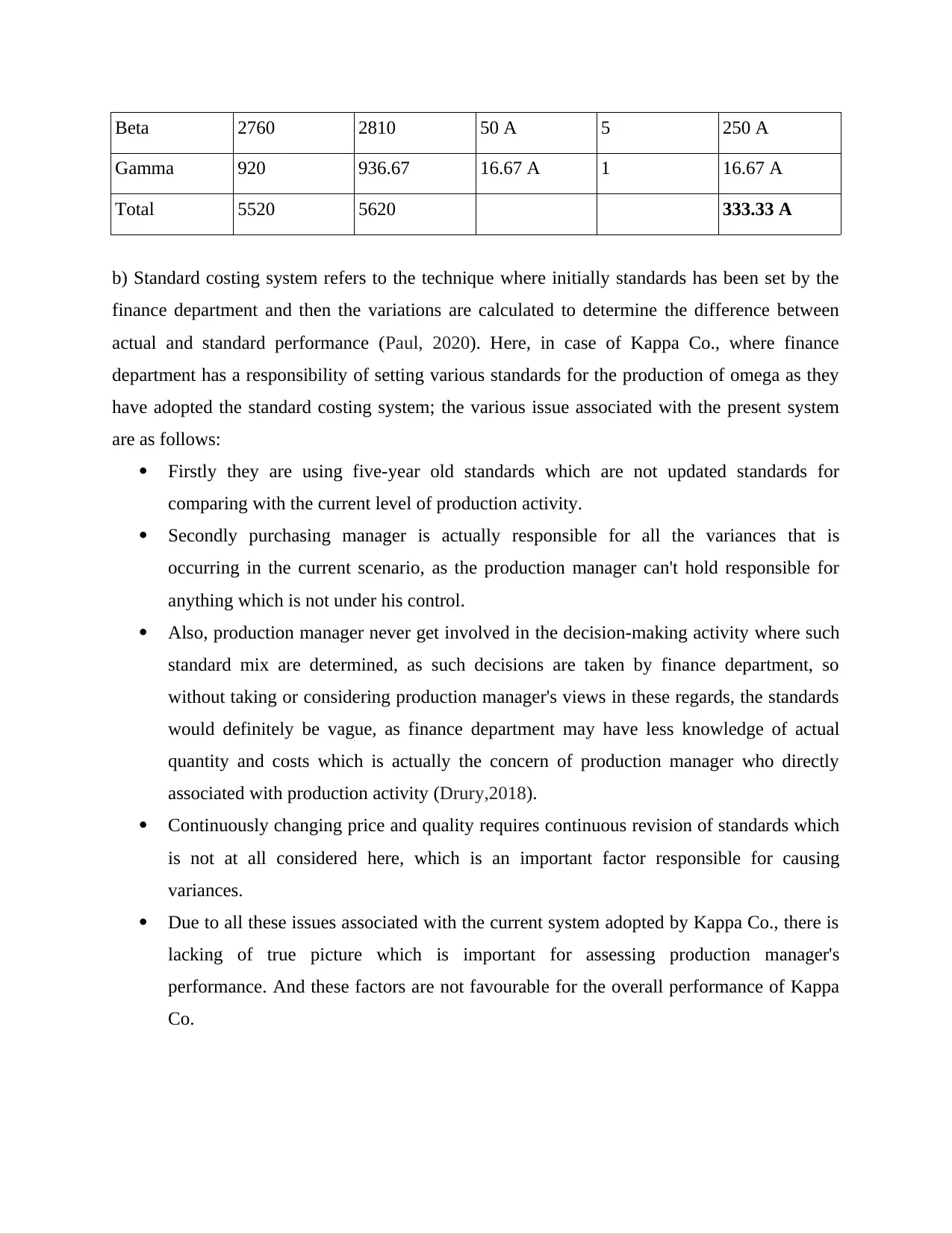

This report analyzes the financial performance management of Ruislip plc, covering various aspects of cost accounting and budgeting. Question 1 focuses on calculating costs and profits per unit for lipstick, lip-balm, and lip-gloss, using both labor hours and activity-based costing to determine overhead absorption rates and profitability. The analysis includes sensitivity analysis to assess the impact of uncertainties. Question 2 delves into variance analysis, including material usage, mix, and yield variances, and discusses the application of a standard costing system, highlighting potential issues with outdated standards and the roles of different departments. Question 3 examines planning, coordination, and control through budgeting, comparing and contrasting zero-based budgeting and incremental budgeting approaches and their suitability for business planning.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.