Managerial Finance: Comparative Analysis of M&S PLC and Next PLC

VerifiedAdded on 2020/12/09

|14

|4030

|491

Report

AI Summary

This report presents a comparative financial analysis of Marks and Spencer PLC and Next PLC for the years 2018 and 2017. It begins with an executive summary and a table of contents, followed by a detailed calculation and analysis of ten financial ratios for both companies, including current ratio, quick ratio, and profitability metrics. The report compares the financial positions of the two organizations, highlighting the strengths and weaknesses of each. It then evaluates a capital investment project for Brooks Private Limited, utilizing investment appraisal techniques to determine the most profitable project. The analysis includes discussions on the limitations of relying on financial ratios and investment appraisal techniques. Finally, the report provides recommendations for improving the financial performance of Next PLC, concluding with a summary of findings and a reference list.

MANAGERIAL FINANCE

STUDENT’S NAME:

STUDENT’S ID:

STUDENT’S NAME:

STUDENT’S ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive summary

The present report has focused on evaluating and calculating the financial report of both Marks

and Spencer PLC and Next PLC for the years 2018 and 2017. Based on the financial ratios this

report has compared the current financial position of both organisations in the market. Finally,

this report has analysed the project of Brooks Private Limited. Using relevant investment

appraisal technique the report has determined the most profitable project for the company. The

financial position of Marks and Spencer PLC is better than Next PLC. The liquidity ratios of

both companies have shown that Marks and Spencer PLC has high current and quick ratio rate

compared to Next PLC. This has increased financial crisis for Next PLC in the current financial

year. Additionally, Next PLC can face difficulties to meet their short-term and long-term market

liabilities compared to Marks and Spencer PLC. Based on the investment appraisal techniques of

both projects it can be understood that Alpha project is more appropriate compared to Beta

project. The Beta project can reduce the payback period for the company. Nonetheless, the rate

of returns can decrease and the cash expenses can expand in future.

2

The present report has focused on evaluating and calculating the financial report of both Marks

and Spencer PLC and Next PLC for the years 2018 and 2017. Based on the financial ratios this

report has compared the current financial position of both organisations in the market. Finally,

this report has analysed the project of Brooks Private Limited. Using relevant investment

appraisal technique the report has determined the most profitable project for the company. The

financial position of Marks and Spencer PLC is better than Next PLC. The liquidity ratios of

both companies have shown that Marks and Spencer PLC has high current and quick ratio rate

compared to Next PLC. This has increased financial crisis for Next PLC in the current financial

year. Additionally, Next PLC can face difficulties to meet their short-term and long-term market

liabilities compared to Marks and Spencer PLC. Based on the investment appraisal techniques of

both projects it can be understood that Alpha project is more appropriate compared to Beta

project. The Beta project can reduce the payback period for the company. Nonetheless, the rate

of returns can decrease and the cash expenses can expand in future.

2

Table of Contents

Introduction......................................................................................................................................4

Task 1:.............................................................................................................................................4

Calculation of 10 financial ratios of both companies..................................................................4

Analysis the performance, financial position and investment potential of both companies........6

Recommendations for the financial performance of poorly performing business improvement 8

Discussion of limitations of relying on financial ratios to interpret companies’ performance....9

Task 2: Capital Investment Appraisal............................................................................................10

Advising senior management on whether they should opt for the Alpha project or Beta project

based on investment appraisal techniques.................................................................................10

Discussion the limitations of using investment appraisal techniques to help in long-term

decision making.........................................................................................................................11

Conclusion.....................................................................................................................................12

Reference list.................................................................................................................................13

3

Introduction......................................................................................................................................4

Task 1:.............................................................................................................................................4

Calculation of 10 financial ratios of both companies..................................................................4

Analysis the performance, financial position and investment potential of both companies........6

Recommendations for the financial performance of poorly performing business improvement 8

Discussion of limitations of relying on financial ratios to interpret companies’ performance....9

Task 2: Capital Investment Appraisal............................................................................................10

Advising senior management on whether they should opt for the Alpha project or Beta project

based on investment appraisal techniques.................................................................................10

Discussion the limitations of using investment appraisal techniques to help in long-term

decision making.........................................................................................................................11

Conclusion.....................................................................................................................................12

Reference list.................................................................................................................................13

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Ratio analysis can help business organisations to identify their current financial health. The

present report has focused on evaluating and calculating the financial report of both Marks and

Spencer PLC and Next PLC for the years 2018 and 2017. Marks and Spencer PLC is a large

retailing organisation of United Kingdom. The organisation has more than 1,025 stores in the

country (Marksandspencer, 2018). Next PLC is a retail organisation that has been launched in

February 1982. In the current year Next has more than 500 stores in the United Kingdom (Next,

2018). Based on the financial ratios this report has compared the current financial position of

both organisations in the market. Finally, this report has analysed the project of Brooks Private

Limited. Using relevant investment appraisal technique the report has determined the most

profitable project for the company.

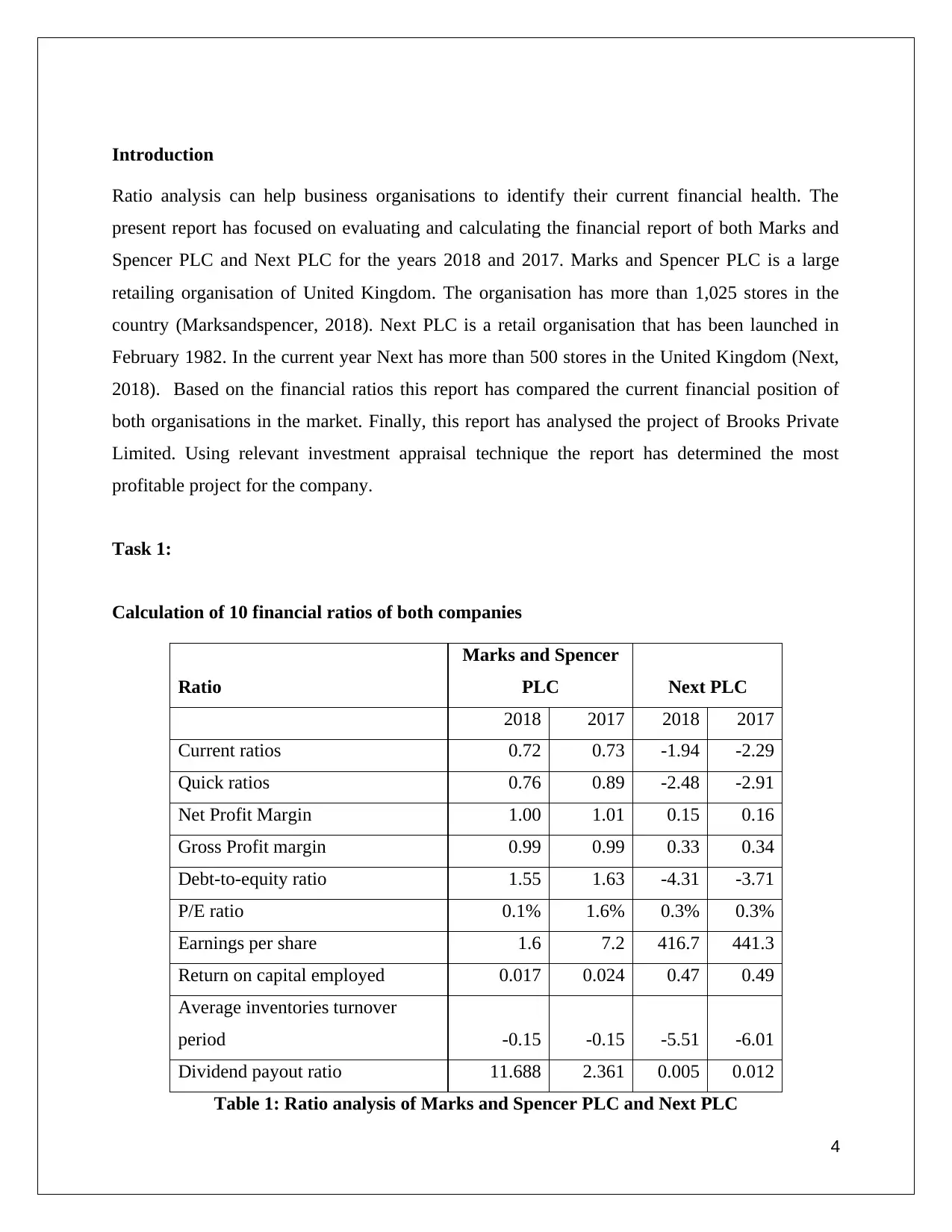

Task 1:

Calculation of 10 financial ratios of both companies

Ratio

Marks and Spencer

PLC Next PLC

2018 2017 2018 2017

Current ratios 0.72 0.73 -1.94 -2.29

Quick ratios 0.76 0.89 -2.48 -2.91

Net Profit Margin 1.00 1.01 0.15 0.16

Gross Profit margin 0.99 0.99 0.33 0.34

Debt-to-equity ratio 1.55 1.63 -4.31 -3.71

P/E ratio 0.1% 1.6% 0.3% 0.3%

Earnings per share 1.6 7.2 416.7 441.3

Return on capital employed 0.017 0.024 0.47 0.49

Average inventories turnover

period -0.15 -0.15 -5.51 -6.01

Dividend payout ratio 11.688 2.361 0.005 0.012

Table 1: Ratio analysis of Marks and Spencer PLC and Next PLC

4

Ratio analysis can help business organisations to identify their current financial health. The

present report has focused on evaluating and calculating the financial report of both Marks and

Spencer PLC and Next PLC for the years 2018 and 2017. Marks and Spencer PLC is a large

retailing organisation of United Kingdom. The organisation has more than 1,025 stores in the

country (Marksandspencer, 2018). Next PLC is a retail organisation that has been launched in

February 1982. In the current year Next has more than 500 stores in the United Kingdom (Next,

2018). Based on the financial ratios this report has compared the current financial position of

both organisations in the market. Finally, this report has analysed the project of Brooks Private

Limited. Using relevant investment appraisal technique the report has determined the most

profitable project for the company.

Task 1:

Calculation of 10 financial ratios of both companies

Ratio

Marks and Spencer

PLC Next PLC

2018 2017 2018 2017

Current ratios 0.72 0.73 -1.94 -2.29

Quick ratios 0.76 0.89 -2.48 -2.91

Net Profit Margin 1.00 1.01 0.15 0.16

Gross Profit margin 0.99 0.99 0.33 0.34

Debt-to-equity ratio 1.55 1.63 -4.31 -3.71

P/E ratio 0.1% 1.6% 0.3% 0.3%

Earnings per share 1.6 7.2 416.7 441.3

Return on capital employed 0.017 0.024 0.47 0.49

Average inventories turnover

period -0.15 -0.15 -5.51 -6.01

Dividend payout ratio 11.688 2.361 0.005 0.012

Table 1: Ratio analysis of Marks and Spencer PLC and Next PLC

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

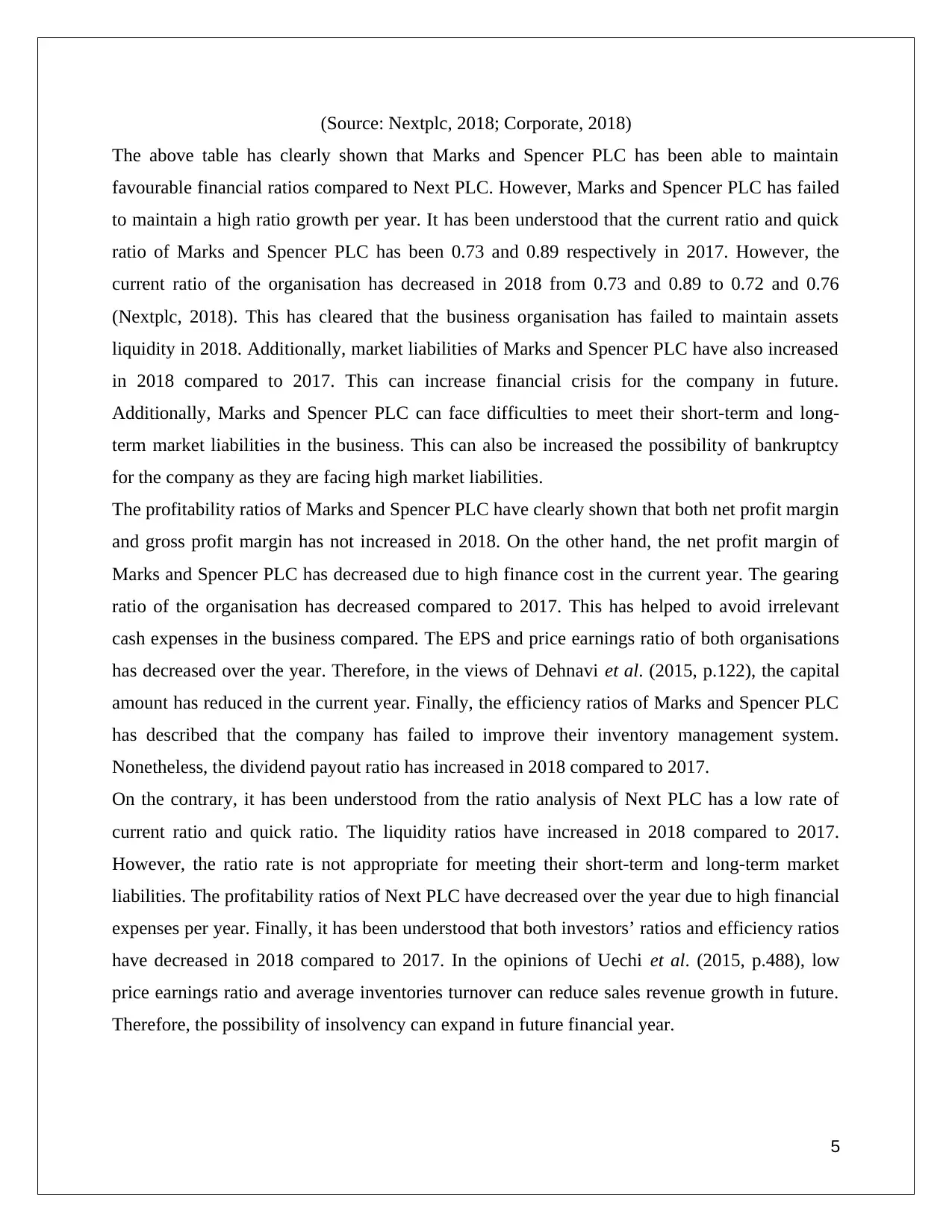

(Source: Nextplc, 2018; Corporate, 2018)

The above table has clearly shown that Marks and Spencer PLC has been able to maintain

favourable financial ratios compared to Next PLC. However, Marks and Spencer PLC has failed

to maintain a high ratio growth per year. It has been understood that the current ratio and quick

ratio of Marks and Spencer PLC has been 0.73 and 0.89 respectively in 2017. However, the

current ratio of the organisation has decreased in 2018 from 0.73 and 0.89 to 0.72 and 0.76

(Nextplc, 2018). This has cleared that the business organisation has failed to maintain assets

liquidity in 2018. Additionally, market liabilities of Marks and Spencer PLC have also increased

in 2018 compared to 2017. This can increase financial crisis for the company in future.

Additionally, Marks and Spencer PLC can face difficulties to meet their short-term and long-

term market liabilities in the business. This can also be increased the possibility of bankruptcy

for the company as they are facing high market liabilities.

The profitability ratios of Marks and Spencer PLC have clearly shown that both net profit margin

and gross profit margin has not increased in 2018. On the other hand, the net profit margin of

Marks and Spencer PLC has decreased due to high finance cost in the current year. The gearing

ratio of the organisation has decreased compared to 2017. This has helped to avoid irrelevant

cash expenses in the business compared. The EPS and price earnings ratio of both organisations

has decreased over the year. Therefore, in the views of Dehnavi et al. (2015, p.122), the capital

amount has reduced in the current year. Finally, the efficiency ratios of Marks and Spencer PLC

has described that the company has failed to improve their inventory management system.

Nonetheless, the dividend payout ratio has increased in 2018 compared to 2017.

On the contrary, it has been understood from the ratio analysis of Next PLC has a low rate of

current ratio and quick ratio. The liquidity ratios have increased in 2018 compared to 2017.

However, the ratio rate is not appropriate for meeting their short-term and long-term market

liabilities. The profitability ratios of Next PLC have decreased over the year due to high financial

expenses per year. Finally, it has been understood that both investors’ ratios and efficiency ratios

have decreased in 2018 compared to 2017. In the opinions of Uechi et al. (2015, p.488), low

price earnings ratio and average inventories turnover can reduce sales revenue growth in future.

Therefore, the possibility of insolvency can expand in future financial year.

5

The above table has clearly shown that Marks and Spencer PLC has been able to maintain

favourable financial ratios compared to Next PLC. However, Marks and Spencer PLC has failed

to maintain a high ratio growth per year. It has been understood that the current ratio and quick

ratio of Marks and Spencer PLC has been 0.73 and 0.89 respectively in 2017. However, the

current ratio of the organisation has decreased in 2018 from 0.73 and 0.89 to 0.72 and 0.76

(Nextplc, 2018). This has cleared that the business organisation has failed to maintain assets

liquidity in 2018. Additionally, market liabilities of Marks and Spencer PLC have also increased

in 2018 compared to 2017. This can increase financial crisis for the company in future.

Additionally, Marks and Spencer PLC can face difficulties to meet their short-term and long-

term market liabilities in the business. This can also be increased the possibility of bankruptcy

for the company as they are facing high market liabilities.

The profitability ratios of Marks and Spencer PLC have clearly shown that both net profit margin

and gross profit margin has not increased in 2018. On the other hand, the net profit margin of

Marks and Spencer PLC has decreased due to high finance cost in the current year. The gearing

ratio of the organisation has decreased compared to 2017. This has helped to avoid irrelevant

cash expenses in the business compared. The EPS and price earnings ratio of both organisations

has decreased over the year. Therefore, in the views of Dehnavi et al. (2015, p.122), the capital

amount has reduced in the current year. Finally, the efficiency ratios of Marks and Spencer PLC

has described that the company has failed to improve their inventory management system.

Nonetheless, the dividend payout ratio has increased in 2018 compared to 2017.

On the contrary, it has been understood from the ratio analysis of Next PLC has a low rate of

current ratio and quick ratio. The liquidity ratios have increased in 2018 compared to 2017.

However, the ratio rate is not appropriate for meeting their short-term and long-term market

liabilities. The profitability ratios of Next PLC have decreased over the year due to high financial

expenses per year. Finally, it has been understood that both investors’ ratios and efficiency ratios

have decreased in 2018 compared to 2017. In the opinions of Uechi et al. (2015, p.488), low

price earnings ratio and average inventories turnover can reduce sales revenue growth in future.

Therefore, the possibility of insolvency can expand in future financial year.

5

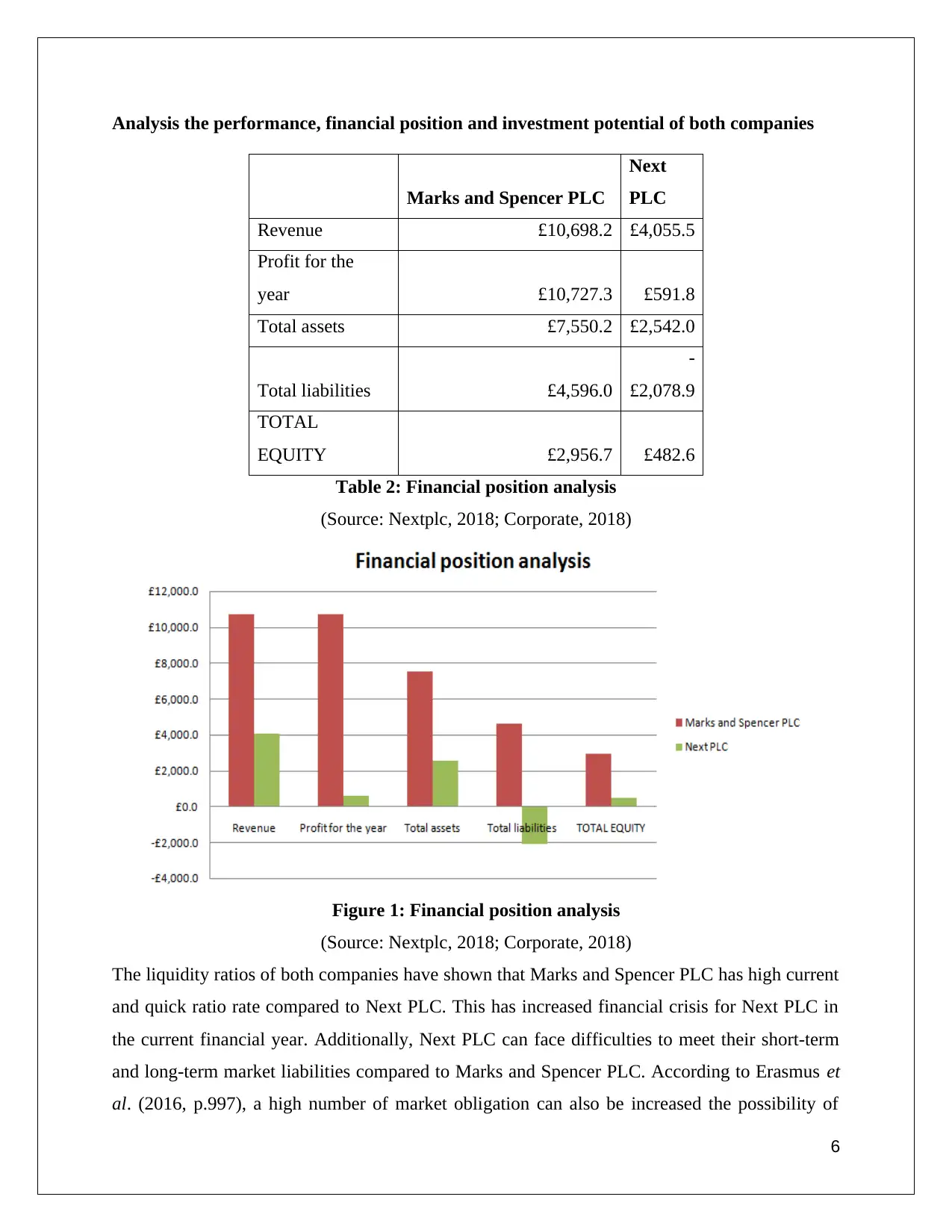

Analysis the performance, financial position and investment potential of both companies

Marks and Spencer PLC

Next

PLC

Revenue £10,698.2 £4,055.5

Profit for the

year £10,727.3 £591.8

Total assets £7,550.2 £2,542.0

Total liabilities £4,596.0

-

£2,078.9

TOTAL

EQUITY £2,956.7 £482.6

Table 2: Financial position analysis

(Source: Nextplc, 2018; Corporate, 2018)

Figure 1: Financial position analysis

(Source: Nextplc, 2018; Corporate, 2018)

The liquidity ratios of both companies have shown that Marks and Spencer PLC has high current

and quick ratio rate compared to Next PLC. This has increased financial crisis for Next PLC in

the current financial year. Additionally, Next PLC can face difficulties to meet their short-term

and long-term market liabilities compared to Marks and Spencer PLC. According to Erasmus et

al. (2016, p.997), a high number of market obligation can also be increased the possibility of

6

Marks and Spencer PLC

Next

PLC

Revenue £10,698.2 £4,055.5

Profit for the

year £10,727.3 £591.8

Total assets £7,550.2 £2,542.0

Total liabilities £4,596.0

-

£2,078.9

TOTAL

EQUITY £2,956.7 £482.6

Table 2: Financial position analysis

(Source: Nextplc, 2018; Corporate, 2018)

Figure 1: Financial position analysis

(Source: Nextplc, 2018; Corporate, 2018)

The liquidity ratios of both companies have shown that Marks and Spencer PLC has high current

and quick ratio rate compared to Next PLC. This has increased financial crisis for Next PLC in

the current financial year. Additionally, Next PLC can face difficulties to meet their short-term

and long-term market liabilities compared to Marks and Spencer PLC. According to Erasmus et

al. (2016, p.997), a high number of market obligation can also be increased the possibility of

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

bankruptcy for Next PLC and Marks and Spencer PLC can gain competitive over Next PLC.

Marks and Spencer PLC can also attract the customers of Next PLC based on better product

quality and service quality.

The financial positions of both companies have decreased in 2018 compared to 2017. However,

it has been understood from the financial statement of both organisations that Marks and Spencer

PLC has collected high net profit compared to Next PLC. This has helped Marks and Spencer

PLC to increase their cash assets and improve their product and service quality compared to Next

PLC. On the other hand, Next PLC has faced high amount of expenses in their financial income

statement. Therefore, the cash assets of the organisation have decreased over the years and Next

PLC has failed to improve their product quality. This can increase financial difficulties for the

business in future (Trivedi et al. 2016, p.80). Similarly, the numbers of both customers and

shareholders can decrease in future.

The balance sheet statements of both organisations have stated that the Marks and Spencer PLC

has high amount of market assets compared to Next PLC. Nevertheless, compared to 2017 the

assets amount of Marks and Spencer PLC has decreased in the current year. The financial

performance of Marks and Spencer PLC is slow per year still the assets amount is high compared

to Next PLC. On the contrary, Next PLC had a low asset amount of 2,404.8 million pounds in

2017 compared to Marks and Spencer PLC. From that amount, it has increased to $2,542 million

pounds (Nextplc, 2018). However, compared to Marks and Spencer PLC it is low and therefore

Marks and Spencer PLC has a strong market position in the country. Based on stabilised market

position of Marks and Spencer PLC it is able to attract high number of investors in the business.

Therefore, the equity share capital of this organisation can increase in the future years. However,

Next PLC can face difficulties in attracting high number of customers toward the business. This

can reduce the share price of Next PLC in future. Moreover, the organisation share equity

amount can decrease based on low share price.

It has been understood from the price earnings ratio and earnings per share Next PLC has high

share price in 2017. However, the growth rates of these both ratios have reduced in 2018 due to

low organisational performance of Next. Both investor ratios of Marks and Spencer PLC have

also decreased in 2018 compared to 2018. However, the earings of Marks and Spencer PLC are

better than Next PLC. Therefore, it can be understood that investors can receive profit from

Marks and Spencer PLC compared to Next PLC. Additionally, the dividend amount of Marks

7

Marks and Spencer PLC can also attract the customers of Next PLC based on better product

quality and service quality.

The financial positions of both companies have decreased in 2018 compared to 2017. However,

it has been understood from the financial statement of both organisations that Marks and Spencer

PLC has collected high net profit compared to Next PLC. This has helped Marks and Spencer

PLC to increase their cash assets and improve their product and service quality compared to Next

PLC. On the other hand, Next PLC has faced high amount of expenses in their financial income

statement. Therefore, the cash assets of the organisation have decreased over the years and Next

PLC has failed to improve their product quality. This can increase financial difficulties for the

business in future (Trivedi et al. 2016, p.80). Similarly, the numbers of both customers and

shareholders can decrease in future.

The balance sheet statements of both organisations have stated that the Marks and Spencer PLC

has high amount of market assets compared to Next PLC. Nevertheless, compared to 2017 the

assets amount of Marks and Spencer PLC has decreased in the current year. The financial

performance of Marks and Spencer PLC is slow per year still the assets amount is high compared

to Next PLC. On the contrary, Next PLC had a low asset amount of 2,404.8 million pounds in

2017 compared to Marks and Spencer PLC. From that amount, it has increased to $2,542 million

pounds (Nextplc, 2018). However, compared to Marks and Spencer PLC it is low and therefore

Marks and Spencer PLC has a strong market position in the country. Based on stabilised market

position of Marks and Spencer PLC it is able to attract high number of investors in the business.

Therefore, the equity share capital of this organisation can increase in the future years. However,

Next PLC can face difficulties in attracting high number of customers toward the business. This

can reduce the share price of Next PLC in future. Moreover, the organisation share equity

amount can decrease based on low share price.

It has been understood from the price earnings ratio and earnings per share Next PLC has high

share price in 2017. However, the growth rates of these both ratios have reduced in 2018 due to

low organisational performance of Next. Both investor ratios of Marks and Spencer PLC have

also decreased in 2018 compared to 2018. However, the earings of Marks and Spencer PLC are

better than Next PLC. Therefore, it can be understood that investors can receive profit from

Marks and Spencer PLC compared to Next PLC. Additionally, the dividend amount of Marks

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and Spencer PLC has increased in 2018 compared to Next. This has helped Marks and Spencer

PLC to collect high number of international stakeholder in 2018 and Marks and Spencer PLC has

expanded the market share compared to Next PLC.

The returns on capital employed of both organisations have decreased in 2018. This can increase

financial crisis for the organisation can increase in future as the cash growth has decreased.

Additionally, both business organisations have failed to improve their inventory management

system in the current compared to 2017. This can increase financial crisis of the company in

future and the organisations can decrease their financial performance per year (Qiu et al. 2016,

p.102). Based on the Return on capital employed and Average inventories turnover period both

Marks and Spencer PLC and Next PLC can face high market risks in future. This can reduce

their product and service quality and both companies can face market risks in future.

Recommendations for the financial performance of poorly performing business

improvement

Based on the financial statement of both companies it is clear that Next has poor performance

compared to Marks and Spencer PLC. Therefore, Next PLC can maintain the following steps in

the business.

Proper evaluation of financial statement

The CEO of Next PLC has to evaluate their financial statement per year to understand the

authenticity of annual report. This can increase help the company to reduce their unnecessary

expenses in the business. Additionally, CEO can introduce a new business policy to decrease the

wastage of raw materials in future. Low wastage of raw materials can help the organisation

increase their efficiency ratios in future year.

Introduce new and innovative business tools

Next PLC has increased their financial expenses in the current year. This has reduced their cash

assets in 2018 compared to 2017. Therefore, the business organisation can introduce new and

innovative strategy to gain external opportunities such as tax benefits. As influenced by the

opinions of Baum and Crosby (2014, p.17), in case the organisation managed to gain tax benefits

then the tax expenses of Next can decrease over the years. Moreover, the business organisation

can be able to maintain high profitability growth rate per year due to low financial expenses.

8

PLC to collect high number of international stakeholder in 2018 and Marks and Spencer PLC has

expanded the market share compared to Next PLC.

The returns on capital employed of both organisations have decreased in 2018. This can increase

financial crisis for the organisation can increase in future as the cash growth has decreased.

Additionally, both business organisations have failed to improve their inventory management

system in the current compared to 2017. This can increase financial crisis of the company in

future and the organisations can decrease their financial performance per year (Qiu et al. 2016,

p.102). Based on the Return on capital employed and Average inventories turnover period both

Marks and Spencer PLC and Next PLC can face high market risks in future. This can reduce

their product and service quality and both companies can face market risks in future.

Recommendations for the financial performance of poorly performing business

improvement

Based on the financial statement of both companies it is clear that Next has poor performance

compared to Marks and Spencer PLC. Therefore, Next PLC can maintain the following steps in

the business.

Proper evaluation of financial statement

The CEO of Next PLC has to evaluate their financial statement per year to understand the

authenticity of annual report. This can increase help the company to reduce their unnecessary

expenses in the business. Additionally, CEO can introduce a new business policy to decrease the

wastage of raw materials in future. Low wastage of raw materials can help the organisation

increase their efficiency ratios in future year.

Introduce new and innovative business tools

Next PLC has increased their financial expenses in the current year. This has reduced their cash

assets in 2018 compared to 2017. Therefore, the business organisation can introduce new and

innovative strategy to gain external opportunities such as tax benefits. As influenced by the

opinions of Baum and Crosby (2014, p.17), in case the organisation managed to gain tax benefits

then the tax expenses of Next can decrease over the years. Moreover, the business organisation

can be able to maintain high profitability growth rate per year due to low financial expenses.

8

High cash assets can help the company to sustain their position in the competitive market and the

organisation can meet their long-term market obligations.

Hire highly experienced financial employees

The human resource manager of Next PLC has to hire highly skilled and experienced financial

employees in the business. Therefore, the employees can perform a proper investigation on the

management and collect accurate financial data in the business. This can help the business

organisation to reduce fraud and mistake on the financial statement and additionally the

organisation can gain competitive advantage over the rival organisations. Finally, the business

organisation can be able to maintain a relevant financial forecast in future.

Reduce number of borrowings

The CEO of Next PLC has to evaluate the past financial expenses in the business. Based on the

financial expenses the CEO can take a relevant business decision to reduce number of debts in

the market. As influenced by the opinions of Jacksoncan et al. (2015, p.43) low number of debts

help the business organisation to avoid high-interest rate in the market and maintain high

profitability growth from year to year. This can also help the business organisation to reduce

their market liabilities and sustain their position in the competitive market in future. In case Next

PLC manages to reduce their number of borrowing in the current financial year then they can

meet their market obligations.

Discussion of limitations of relying on financial ratios to interpret companies’ performance

In relation to the profitability, liquidity, investors and efficiency ratios both Next PLC and Marks

and Spencer PLC has faced some limitations in 2018. The limitations of both organisations have

been described below.

i) The liquidity ratios rates for both organisations have decreased in 2017 compared to 2018. It

has been clear that both organisations are unable to improve their assets liquidity per year. In

case the liquidity ratio of Next PLC and Marks and Spencer PLC decrease in future then

possibility of bankruptcy for both companies can increase in future.

ii) The profitability ratios of both companies have shown that both net profit margin and gross

profit margin have decreased in 2018. Due to high operating cost and finance cost, the operating

margins have decreased in the current year compared to 2017. This can reduce organisational

performances and both companies can expand market risks (Alkaraan, 2017, p.67).

9

organisation can meet their long-term market obligations.

Hire highly experienced financial employees

The human resource manager of Next PLC has to hire highly skilled and experienced financial

employees in the business. Therefore, the employees can perform a proper investigation on the

management and collect accurate financial data in the business. This can help the business

organisation to reduce fraud and mistake on the financial statement and additionally the

organisation can gain competitive advantage over the rival organisations. Finally, the business

organisation can be able to maintain a relevant financial forecast in future.

Reduce number of borrowings

The CEO of Next PLC has to evaluate the past financial expenses in the business. Based on the

financial expenses the CEO can take a relevant business decision to reduce number of debts in

the market. As influenced by the opinions of Jacksoncan et al. (2015, p.43) low number of debts

help the business organisation to avoid high-interest rate in the market and maintain high

profitability growth from year to year. This can also help the business organisation to reduce

their market liabilities and sustain their position in the competitive market in future. In case Next

PLC manages to reduce their number of borrowing in the current financial year then they can

meet their market obligations.

Discussion of limitations of relying on financial ratios to interpret companies’ performance

In relation to the profitability, liquidity, investors and efficiency ratios both Next PLC and Marks

and Spencer PLC has faced some limitations in 2018. The limitations of both organisations have

been described below.

i) The liquidity ratios rates for both organisations have decreased in 2017 compared to 2018. It

has been clear that both organisations are unable to improve their assets liquidity per year. In

case the liquidity ratio of Next PLC and Marks and Spencer PLC decrease in future then

possibility of bankruptcy for both companies can increase in future.

ii) The profitability ratios of both companies have shown that both net profit margin and gross

profit margin have decreased in 2018. Due to high operating cost and finance cost, the operating

margins have decreased in the current year compared to 2017. This can reduce organisational

performances and both companies can expand market risks (Alkaraan, 2017, p.67).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

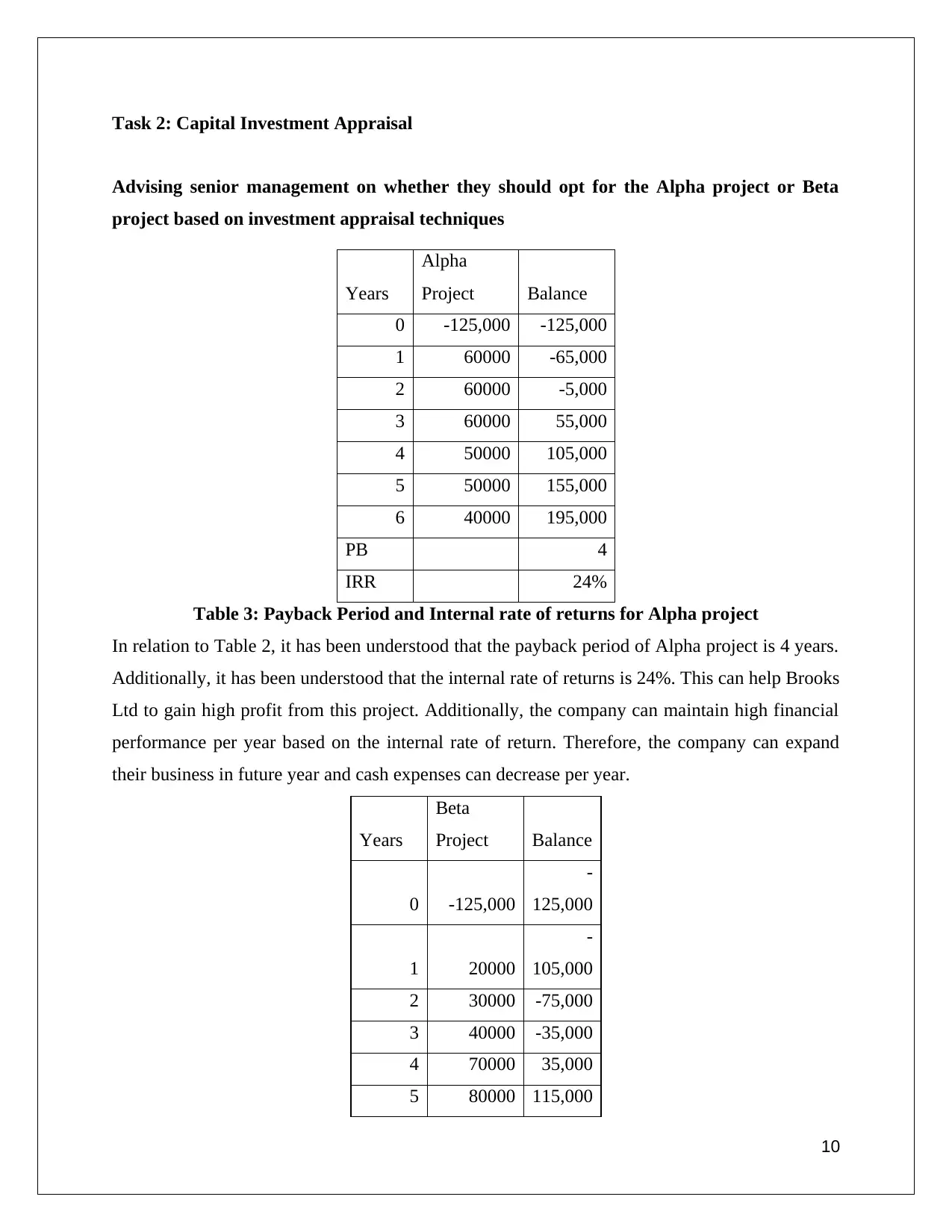

Task 2: Capital Investment Appraisal

Advising senior management on whether they should opt for the Alpha project or Beta

project based on investment appraisal techniques

Years

Alpha

Project Balance

0 -125,000 -125,000

1 60000 -65,000

2 60000 -5,000

3 60000 55,000

4 50000 105,000

5 50000 155,000

6 40000 195,000

PB 4

IRR 24%

Table 3: Payback Period and Internal rate of returns for Alpha project

In relation to Table 2, it has been understood that the payback period of Alpha project is 4 years.

Additionally, it has been understood that the internal rate of returns is 24%. This can help Brooks

Ltd to gain high profit from this project. Additionally, the company can maintain high financial

performance per year based on the internal rate of return. Therefore, the company can expand

their business in future year and cash expenses can decrease per year.

Years

Beta

Project Balance

0 -125,000

-

125,000

1 20000

-

105,000

2 30000 -75,000

3 40000 -35,000

4 70000 35,000

5 80000 115,000

10

Advising senior management on whether they should opt for the Alpha project or Beta

project based on investment appraisal techniques

Years

Alpha

Project Balance

0 -125,000 -125,000

1 60000 -65,000

2 60000 -5,000

3 60000 55,000

4 50000 105,000

5 50000 155,000

6 40000 195,000

PB 4

IRR 24%

Table 3: Payback Period and Internal rate of returns for Alpha project

In relation to Table 2, it has been understood that the payback period of Alpha project is 4 years.

Additionally, it has been understood that the internal rate of returns is 24%. This can help Brooks

Ltd to gain high profit from this project. Additionally, the company can maintain high financial

performance per year based on the internal rate of return. Therefore, the company can expand

their business in future year and cash expenses can decrease per year.

Years

Beta

Project Balance

0 -125,000

-

125,000

1 20000

-

105,000

2 30000 -75,000

3 40000 -35,000

4 70000 35,000

5 80000 115,000

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

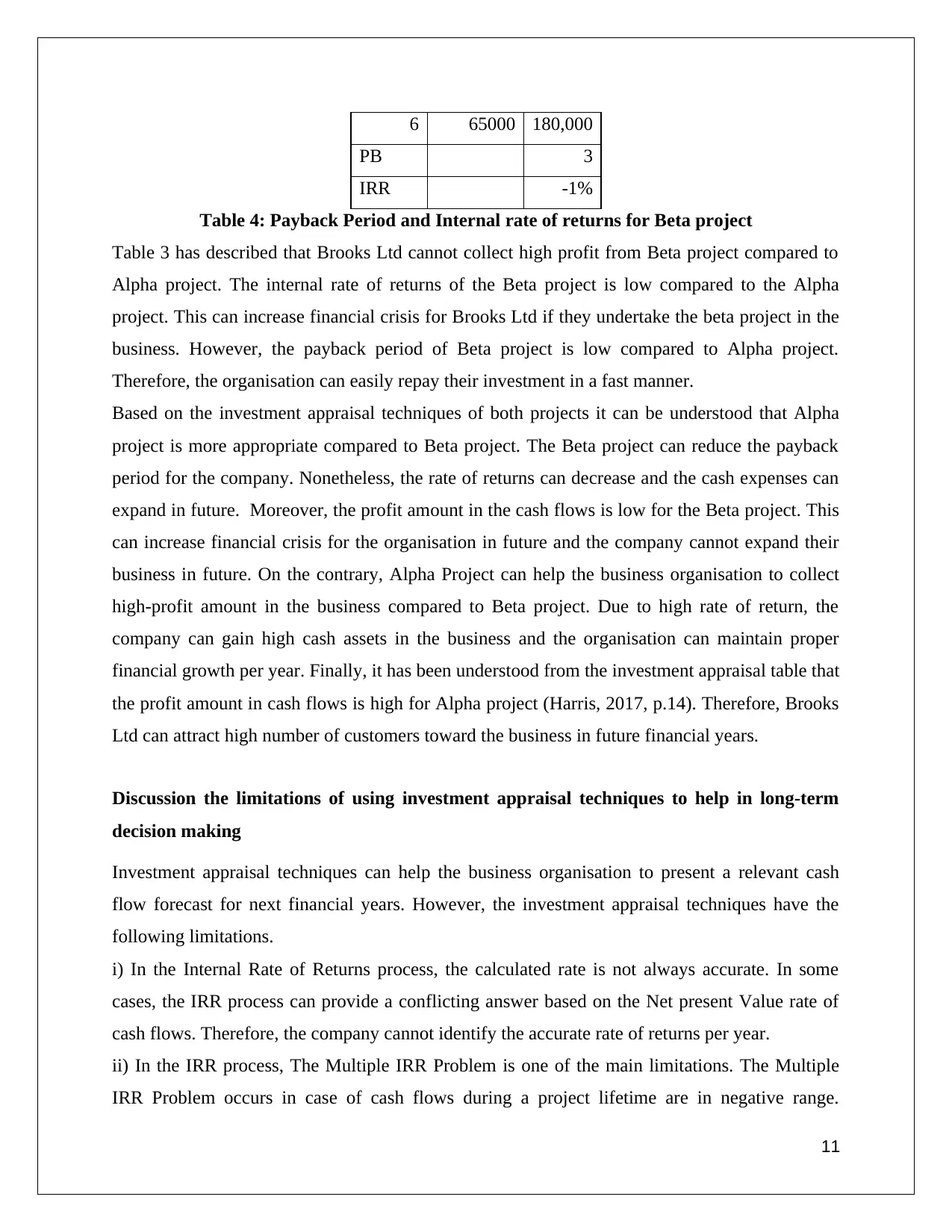

6 65000 180,000

PB 3

IRR -1%

Table 4: Payback Period and Internal rate of returns for Beta project

Table 3 has described that Brooks Ltd cannot collect high profit from Beta project compared to

Alpha project. The internal rate of returns of the Beta project is low compared to the Alpha

project. This can increase financial crisis for Brooks Ltd if they undertake the beta project in the

business. However, the payback period of Beta project is low compared to Alpha project.

Therefore, the organisation can easily repay their investment in a fast manner.

Based on the investment appraisal techniques of both projects it can be understood that Alpha

project is more appropriate compared to Beta project. The Beta project can reduce the payback

period for the company. Nonetheless, the rate of returns can decrease and the cash expenses can

expand in future. Moreover, the profit amount in the cash flows is low for the Beta project. This

can increase financial crisis for the organisation in future and the company cannot expand their

business in future. On the contrary, Alpha Project can help the business organisation to collect

high-profit amount in the business compared to Beta project. Due to high rate of return, the

company can gain high cash assets in the business and the organisation can maintain proper

financial growth per year. Finally, it has been understood from the investment appraisal table that

the profit amount in cash flows is high for Alpha project (Harris, 2017, p.14). Therefore, Brooks

Ltd can attract high number of customers toward the business in future financial years.

Discussion the limitations of using investment appraisal techniques to help in long-term

decision making

Investment appraisal techniques can help the business organisation to present a relevant cash

flow forecast for next financial years. However, the investment appraisal techniques have the

following limitations.

i) In the Internal Rate of Returns process, the calculated rate is not always accurate. In some

cases, the IRR process can provide a conflicting answer based on the Net present Value rate of

cash flows. Therefore, the company cannot identify the accurate rate of returns per year.

ii) In the IRR process, The Multiple IRR Problem is one of the main limitations. The Multiple

IRR Problem occurs in case of cash flows during a project lifetime are in negative range.

11

PB 3

IRR -1%

Table 4: Payback Period and Internal rate of returns for Beta project

Table 3 has described that Brooks Ltd cannot collect high profit from Beta project compared to

Alpha project. The internal rate of returns of the Beta project is low compared to the Alpha

project. This can increase financial crisis for Brooks Ltd if they undertake the beta project in the

business. However, the payback period of Beta project is low compared to Alpha project.

Therefore, the organisation can easily repay their investment in a fast manner.

Based on the investment appraisal techniques of both projects it can be understood that Alpha

project is more appropriate compared to Beta project. The Beta project can reduce the payback

period for the company. Nonetheless, the rate of returns can decrease and the cash expenses can

expand in future. Moreover, the profit amount in the cash flows is low for the Beta project. This

can increase financial crisis for the organisation in future and the company cannot expand their

business in future. On the contrary, Alpha Project can help the business organisation to collect

high-profit amount in the business compared to Beta project. Due to high rate of return, the

company can gain high cash assets in the business and the organisation can maintain proper

financial growth per year. Finally, it has been understood from the investment appraisal table that

the profit amount in cash flows is high for Alpha project (Harris, 2017, p.14). Therefore, Brooks

Ltd can attract high number of customers toward the business in future financial years.

Discussion the limitations of using investment appraisal techniques to help in long-term

decision making

Investment appraisal techniques can help the business organisation to present a relevant cash

flow forecast for next financial years. However, the investment appraisal techniques have the

following limitations.

i) In the Internal Rate of Returns process, the calculated rate is not always accurate. In some

cases, the IRR process can provide a conflicting answer based on the Net present Value rate of

cash flows. Therefore, the company cannot identify the accurate rate of returns per year.

ii) In the IRR process, The Multiple IRR Problem is one of the main limitations. The Multiple

IRR Problem occurs in case of cash flows during a project lifetime are in negative range.

11

Therefore, this investment appraisal technique cannot calculate the relevant rate of returns in the

business. This can increase financial crisis for the company in future and the organisation

forecast can be corrupted.

iii) The payback period process takes no consideration of time value of money. Additionally, it

ignores the fact that some project has a greater payback period based on long payback period.

Therefore, it cannot be able to project proper investment repay amount in the business. This can

increase market risks for companies in future.

Conclusion

It can be concluded that from the above discussion that the financial position of Marks and

Spencer PLC is better than Next PLC. The liquidity ratios of both companies have shown that

Marks and Spencer PLC has high current and quick ratio rate compared to Next PLC. This has

increased financial crisis for Next PLC in the current financial year. Additionally, Next PLC can

face difficulties to meet their short-term and long-term market liabilities compared to Marks and

Spencer PLC. Based on the investment appraisal techniques of both projects it can be understood

that Alpha project is more appropriate compared to Beta project. The Beta project can reduce the

payback period for the company. Nonetheless, the rate of returns can decrease and the cash

expenses can expand in future.

12

business. This can increase financial crisis for the company in future and the organisation

forecast can be corrupted.

iii) The payback period process takes no consideration of time value of money. Additionally, it

ignores the fact that some project has a greater payback period based on long payback period.

Therefore, it cannot be able to project proper investment repay amount in the business. This can

increase market risks for companies in future.

Conclusion

It can be concluded that from the above discussion that the financial position of Marks and

Spencer PLC is better than Next PLC. The liquidity ratios of both companies have shown that

Marks and Spencer PLC has high current and quick ratio rate compared to Next PLC. This has

increased financial crisis for Next PLC in the current financial year. Additionally, Next PLC can

face difficulties to meet their short-term and long-term market liabilities compared to Marks and

Spencer PLC. Based on the investment appraisal techniques of both projects it can be understood

that Alpha project is more appropriate compared to Beta project. The Beta project can reduce the

payback period for the company. Nonetheless, the rate of returns can decrease and the cash

expenses can expand in future.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.