Management Accounting Report: Accounting Systems for Nero Ltd

VerifiedAdded on 2020/12/30

|14

|4148

|441

Report

AI Summary

This management accounting report analyzes the financial performance of Nero Ltd, focusing on various accounting systems and their utilization. The report covers different types of accounting systems, including cost accounting, inventory management, and price optimization, emphasizing their importance in improving efficiency, measuring performance, and enabling effective management control. It also discusses various accounting systems used in reporting, such as performance reports, accounts receivable aging reports, inventory management reports, and job cost reports. Furthermore, the report explores different costing methods, including marginal costing and absorption costing, and their application in preparing income statements. The report also examines the merits and demerits of using planning tools in budgetary control and discusses various financial issues and measures to resolve them. The report provides a comprehensive overview of the accounting practices and financial strategies relevant to Nero Ltd, highlighting the importance of accurate financial reporting and effective decision-making for organizational success. This report is a valuable resource for students seeking to understand management accounting principles and their practical application. The assignment is contributed by a student to be published on the website Desklib, a platform which provides all the necessary AI based study tools for students.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

SECTION 1......................................................................................................................................3

P1: Different types of accounting system and their essential utilisation....................................3

P2: Various accounting system used in reporting.......................................................................5

P3: Different costing methods and preparation of income statement.........................................7

SECTION 2....................................................................................................................................10

PART A.........................................................................................................................................10

P4: Merits and demerits of using planning tools in budgetary control.....................................10

PART B..........................................................................................................................................12

P5: Various financial issues and measure to resolve it.............................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................3

SECTION 1......................................................................................................................................3

P1: Different types of accounting system and their essential utilisation....................................3

P2: Various accounting system used in reporting.......................................................................5

P3: Different costing methods and preparation of income statement.........................................7

SECTION 2....................................................................................................................................10

PART A.........................................................................................................................................10

P4: Merits and demerits of using planning tools in budgetary control.....................................10

PART B..........................................................................................................................................12

P5: Various financial issues and measure to resolve it.............................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting is more useful to identify, measure, analysis and preparation of

financial accounts and reports which helps in making an effective decision and suitable plans for

the betterment of an organisation. For this, accounting managers are liable to record all financial

as well as non-financial transactions happened on daily basis operations which help in

identifying the profitable areas where the company get profitable outcomes. Financial reports

should required to be made by company on annual basis so as to present company's financial

position towards their stakeholders. The present assignment report is based on Nero Ltd. With

the context of which all other aspects are explained under this report. The project report covers

various accounting systems and reporting which facilitate management to make an effective

decision and plans to achieve growth and success. Different planning tools used to control

budgetary process has been also discussed under this report (Ahadiat, 2013).

SECTION 1

P1: Different types of accounting system and their essential utilisation

There are lots of transactions made on daily basis business operations which must required

to be recorded and maintain financial reports such as profit & loss accounts, balance sheet, cash

flow statement etc. Such reports are prepared with an objective of identifying the actual

financial position of company due to which the management are more capable to make further

actions to resolve errors or deviations if any found in financial accounts. This forces

management to adopt various accounting systems which includes cost accounting systems,

inventory management systems, price optimisation system etc. Before adopt such accounting

systems within an organisation it is essential for managers to first identify their important which

are discussed under the below:

Increase in efficiency: It will help in finding out the efficiency level of business

activities through resolving errors or deviations which may restrict employees to perform in best

possible way (Albu and Albu, 2012).

Measurement of performance: Different accounting systems helps in analysing the

performance of employees through comparing their actual with standard performance. This will

help in finding out the deviation if any, due to which the mangers are in position to resolve as

quickly as possible.

Management accounting is more useful to identify, measure, analysis and preparation of

financial accounts and reports which helps in making an effective decision and suitable plans for

the betterment of an organisation. For this, accounting managers are liable to record all financial

as well as non-financial transactions happened on daily basis operations which help in

identifying the profitable areas where the company get profitable outcomes. Financial reports

should required to be made by company on annual basis so as to present company's financial

position towards their stakeholders. The present assignment report is based on Nero Ltd. With

the context of which all other aspects are explained under this report. The project report covers

various accounting systems and reporting which facilitate management to make an effective

decision and plans to achieve growth and success. Different planning tools used to control

budgetary process has been also discussed under this report (Ahadiat, 2013).

SECTION 1

P1: Different types of accounting system and their essential utilisation

There are lots of transactions made on daily basis business operations which must required

to be recorded and maintain financial reports such as profit & loss accounts, balance sheet, cash

flow statement etc. Such reports are prepared with an objective of identifying the actual

financial position of company due to which the management are more capable to make further

actions to resolve errors or deviations if any found in financial accounts. This forces

management to adopt various accounting systems which includes cost accounting systems,

inventory management systems, price optimisation system etc. Before adopt such accounting

systems within an organisation it is essential for managers to first identify their important which

are discussed under the below:

Increase in efficiency: It will help in finding out the efficiency level of business

activities through resolving errors or deviations which may restrict employees to perform in best

possible way (Albu and Albu, 2012).

Measurement of performance: Different accounting systems helps in analysing the

performance of employees through comparing their actual with standard performance. This will

help in finding out the deviation if any, due to which the mangers are in position to resolve as

quickly as possible.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

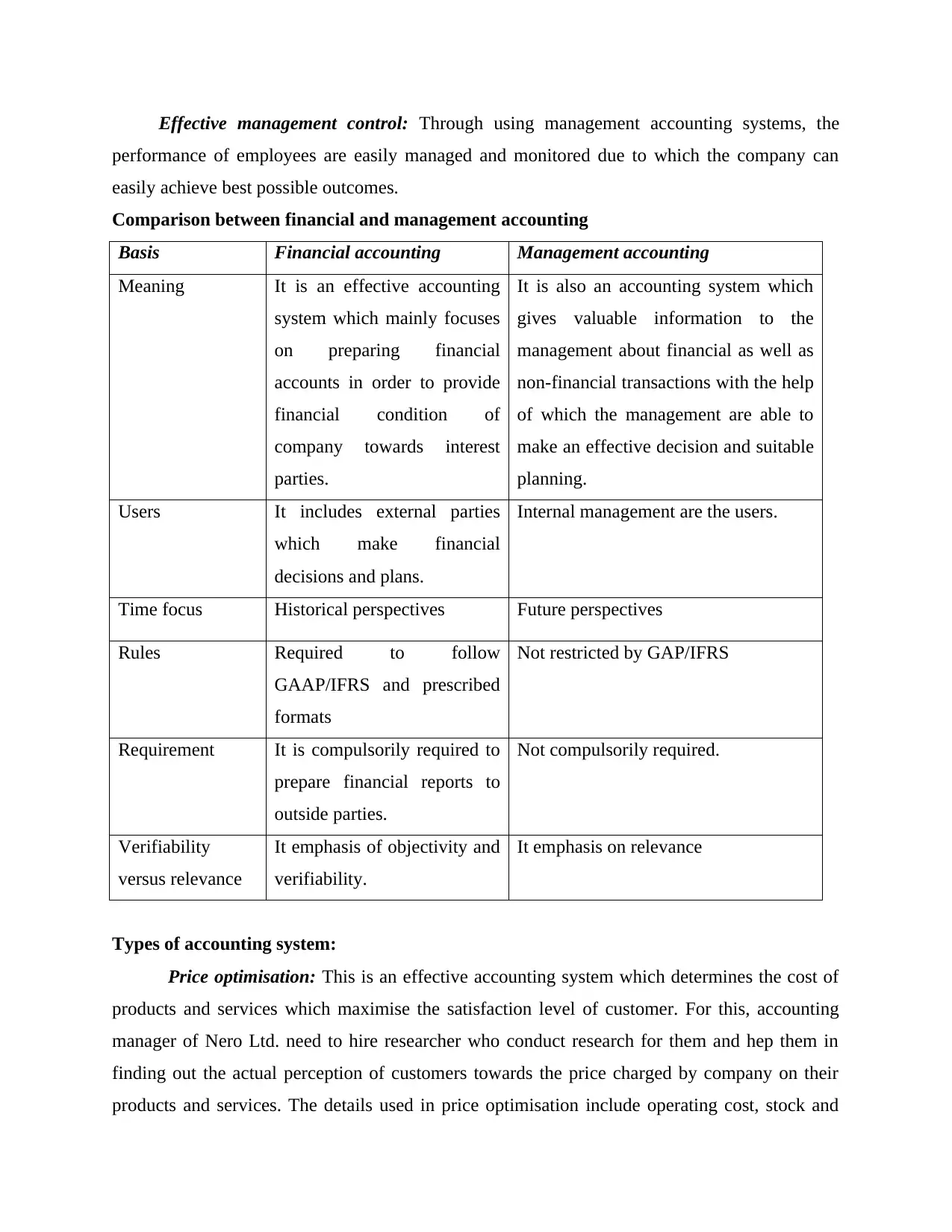

Effective management control: Through using management accounting systems, the

performance of employees are easily managed and monitored due to which the company can

easily achieve best possible outcomes.

Comparison between financial and management accounting

Basis Financial accounting Management accounting

Meaning It is an effective accounting

system which mainly focuses

on preparing financial

accounts in order to provide

financial condition of

company towards interest

parties.

It is also an accounting system which

gives valuable information to the

management about financial as well as

non-financial transactions with the help

of which the management are able to

make an effective decision and suitable

planning.

Users It includes external parties

which make financial

decisions and plans.

Internal management are the users.

Time focus Historical perspectives Future perspectives

Rules Required to follow

GAAP/IFRS and prescribed

formats

Not restricted by GAP/IFRS

Requirement It is compulsorily required to

prepare financial reports to

outside parties.

Not compulsorily required.

Verifiability

versus relevance

It emphasis of objectivity and

verifiability.

It emphasis on relevance

Types of accounting system:

Price optimisation: This is an effective accounting system which determines the cost of

products and services which maximise the satisfaction level of customer. For this, accounting

manager of Nero Ltd. need to hire researcher who conduct research for them and hep them in

finding out the actual perception of customers towards the price charged by company on their

products and services. The details used in price optimisation include operating cost, stock and

performance of employees are easily managed and monitored due to which the company can

easily achieve best possible outcomes.

Comparison between financial and management accounting

Basis Financial accounting Management accounting

Meaning It is an effective accounting

system which mainly focuses

on preparing financial

accounts in order to provide

financial condition of

company towards interest

parties.

It is also an accounting system which

gives valuable information to the

management about financial as well as

non-financial transactions with the help

of which the management are able to

make an effective decision and suitable

planning.

Users It includes external parties

which make financial

decisions and plans.

Internal management are the users.

Time focus Historical perspectives Future perspectives

Rules Required to follow

GAAP/IFRS and prescribed

formats

Not restricted by GAP/IFRS

Requirement It is compulsorily required to

prepare financial reports to

outside parties.

Not compulsorily required.

Verifiability

versus relevance

It emphasis of objectivity and

verifiability.

It emphasis on relevance

Types of accounting system:

Price optimisation: This is an effective accounting system which determines the cost of

products and services which maximise the satisfaction level of customer. For this, accounting

manager of Nero Ltd. need to hire researcher who conduct research for them and hep them in

finding out the actual perception of customers towards the price charged by company on their

products and services. The details used in price optimisation include operating cost, stock and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

historical value. Thus, after identifying the current satisfaction level of customers the manager

of Nero are able to set an optimum prices which increases buying behaviour of customers as well

as increases profit of company as well (Alleyne and Weekes-Marshall, 2011).

Cost accounting system: Such accounting system is useful to adopt in order to determine

the total cost or expenses incurred in production process so as to manufacture quality products

due to which the company set their margin on each products. For this, the manager of Nero Ltd.

should aim to focus on reducing cost through educating their employees to work on modern

technology which help them in producing quality products at minimum cost due to which

profitability of company may increases.

Inventory management system: It is an accounting system which determines and monitor

the non-capital assets and inventory products. It is an affective to use such system which help

company in knowing what amount of stock available with company at present times. This will

provide an opportunity to manager of Nero Ltd. to place order to inventory from suppliers in

order to achieve optimum level of inventory at warehouses so that the production process are not

interrupted in any case and meet demands of customers within shorter period of time.

Job costing system: Such system of accounting is more helpful for manager of Nero Ltd.

to allocate cost to produce specific product or bunch of products in optimum quality. This will

motive client to think how to reduce cost of operations and find the areas where the cost should

required to invent more. This will help manager in fixation of budget for reach job activity on the

basis of their time of manufacturing and profitable outcomes received in future (Bodie, 2013).

P2: Various accounting system used in reporting

In order to make an effective decisions and suitable planning, the accounting manager

need to have important information about the financial position of company ans the resources the

company have at present so that future business activities can be executed in more effective way.

Therefore, it must required for every business organisation such as Nero Ltd. to prepare different

reports on continuous basis so as to get information whenever required. The crucial information

the manager can get is from profit & loss accounts, balance sheet, cash flow statements etc. Such

reports help in identifying the potentiality of company that whether firm are able to deal with

short as well as long term debts in future or not. All the future decision take by manager should

required to consider the information available through such reports so that influencing aspects

which affects the performance of company will be easily identified (Gond and et. al., 2012).

of Nero are able to set an optimum prices which increases buying behaviour of customers as well

as increases profit of company as well (Alleyne and Weekes-Marshall, 2011).

Cost accounting system: Such accounting system is useful to adopt in order to determine

the total cost or expenses incurred in production process so as to manufacture quality products

due to which the company set their margin on each products. For this, the manager of Nero Ltd.

should aim to focus on reducing cost through educating their employees to work on modern

technology which help them in producing quality products at minimum cost due to which

profitability of company may increases.

Inventory management system: It is an accounting system which determines and monitor

the non-capital assets and inventory products. It is an affective to use such system which help

company in knowing what amount of stock available with company at present times. This will

provide an opportunity to manager of Nero Ltd. to place order to inventory from suppliers in

order to achieve optimum level of inventory at warehouses so that the production process are not

interrupted in any case and meet demands of customers within shorter period of time.

Job costing system: Such system of accounting is more helpful for manager of Nero Ltd.

to allocate cost to produce specific product or bunch of products in optimum quality. This will

motive client to think how to reduce cost of operations and find the areas where the cost should

required to invent more. This will help manager in fixation of budget for reach job activity on the

basis of their time of manufacturing and profitable outcomes received in future (Bodie, 2013).

P2: Various accounting system used in reporting

In order to make an effective decisions and suitable planning, the accounting manager

need to have important information about the financial position of company ans the resources the

company have at present so that future business activities can be executed in more effective way.

Therefore, it must required for every business organisation such as Nero Ltd. to prepare different

reports on continuous basis so as to get information whenever required. The crucial information

the manager can get is from profit & loss accounts, balance sheet, cash flow statements etc. Such

reports help in identifying the potentiality of company that whether firm are able to deal with

short as well as long term debts in future or not. All the future decision take by manager should

required to consider the information available through such reports so that influencing aspects

which affects the performance of company will be easily identified (Gond and et. al., 2012).

If making some modifications according to the fluctuations in market conditions,

preparation of such reports are more useful. On the other hand, such reports cannot be made

without having support from the different departments. Therefore, adequate support from them is

must which enable company to known the requirements of each department in execution of

particular business activities. Thus, for this the manages must required to use various reporting

system that help them in reporting their financial transactions. This will help in identifying the

true and fair financial position of company. Such reporting system includes:

Performance report: Such reports maintained by company with an objective of analysing

the performance of employees as well as an organisation which help them in finding out the

issues and deviations which may comes in the process of executing business activities in more

effective manner. Such reports includes the information related with utilisation of resources,

future opportunities to achieve growth for outside parties. This will help in determining the

current situation of organisation and accordingly put maximum efforts in maximising their

performance through removing all barriers and deviations (Christ and Burritt, 2013).

Account receivable ageing report: It contains the details of unpaid debtors of company

which directs the management to implement some actions and plans to recover the same along

with the interest. It help company in making an effective policies regarding the eliminating of

such situation in near future. Thus, essential to make such reports which provides the accounting

details that are related with credit payment options.

Inventory management report: It is much difficult for inventory management to control

stock at maximum level which can be resolved through using an appropriate stock tool that will

help in analysing the inventory level of an organisation. Such tools includes EOQ, ABC costing

and inventory management ratios etc. Thus, such reports provided the adequate information

about the current level of inventory which directs the managers to make decision whether to

place order to suppliers or not (Kotas, 2014).

Job cost report: Such reports is helpful for manager to track total expenses incurred in

production process so that invested cost of producing each product can be easily identified. This

will help manager in setting up prices of products after making properly analysis of expenditures

and its profitable outcomes. It is more helpful in allocating cost to project activity in order to deal

with financial efficiency and productivity during the time (Cinquini and Tenucci, 2010).

preparation of such reports are more useful. On the other hand, such reports cannot be made

without having support from the different departments. Therefore, adequate support from them is

must which enable company to known the requirements of each department in execution of

particular business activities. Thus, for this the manages must required to use various reporting

system that help them in reporting their financial transactions. This will help in identifying the

true and fair financial position of company. Such reporting system includes:

Performance report: Such reports maintained by company with an objective of analysing

the performance of employees as well as an organisation which help them in finding out the

issues and deviations which may comes in the process of executing business activities in more

effective manner. Such reports includes the information related with utilisation of resources,

future opportunities to achieve growth for outside parties. This will help in determining the

current situation of organisation and accordingly put maximum efforts in maximising their

performance through removing all barriers and deviations (Christ and Burritt, 2013).

Account receivable ageing report: It contains the details of unpaid debtors of company

which directs the management to implement some actions and plans to recover the same along

with the interest. It help company in making an effective policies regarding the eliminating of

such situation in near future. Thus, essential to make such reports which provides the accounting

details that are related with credit payment options.

Inventory management report: It is much difficult for inventory management to control

stock at maximum level which can be resolved through using an appropriate stock tool that will

help in analysing the inventory level of an organisation. Such tools includes EOQ, ABC costing

and inventory management ratios etc. Thus, such reports provided the adequate information

about the current level of inventory which directs the managers to make decision whether to

place order to suppliers or not (Kotas, 2014).

Job cost report: Such reports is helpful for manager to track total expenses incurred in

production process so that invested cost of producing each product can be easily identified. This

will help manager in setting up prices of products after making properly analysis of expenditures

and its profitable outcomes. It is more helpful in allocating cost to project activity in order to deal

with financial efficiency and productivity during the time (Cinquini and Tenucci, 2010).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

P3: Different costing methods and preparation of income statement

Cost: It refers to value of amount which is invested in the process of executing different

business activities so as to achieve profitable outcomes in ear future. Such activities includes

marketing activities, production activities etc. For example, cost incurred in executing production

activities includes labour cost, raw material cost and overhead expanses.

Therefore, it is essential for the management of Nero Ltd. to use different costing methods in

order to setting up the prices for their products and services which maximises the satisfaction

level of customers as well as increase profitability of company. There are come costing methods

which help in overcoming the extra cost of company. Such costing methods includes:

Marginal costing: It refers to the cost invested in producing an additional unit of output

so as to meet customer’s needs and requirements. It is also more effective to use in stock

valuation due to considering variable cost the inventory value is undervalued. Therefore, such

costing methods doesn't include fixed cost and consider only variable cost (Endenich, Brandau,

and Hoffjan, 2011).

Absorption costing: Such costing methods includes all expenses incurred in

manufacturing process which means fixed as well as variable cost are required to consider at the

time of valuation of products and services. It incudes every thing which is directly impact the

products. Such cost includes Labour cost, material cost, overhead expenses.

Comparison between Marginal and Absorption costing

Marginal costing Absorption costing

It only determines the variable cost and

ignore fined cost at the time of valuation of

products and services.

It adds both fixed and variable cost at the

time of valuation.

Using such method, the profitability appears

more due to gathering profits from each

individual sales.

Under this method, the profitability appear at

minimum.

Such method is useful for making an short

decisions in an organisation.

Such method is useful for making long-term

decisions.

Cost: It refers to value of amount which is invested in the process of executing different

business activities so as to achieve profitable outcomes in ear future. Such activities includes

marketing activities, production activities etc. For example, cost incurred in executing production

activities includes labour cost, raw material cost and overhead expanses.

Therefore, it is essential for the management of Nero Ltd. to use different costing methods in

order to setting up the prices for their products and services which maximises the satisfaction

level of customers as well as increase profitability of company. There are come costing methods

which help in overcoming the extra cost of company. Such costing methods includes:

Marginal costing: It refers to the cost invested in producing an additional unit of output

so as to meet customer’s needs and requirements. It is also more effective to use in stock

valuation due to considering variable cost the inventory value is undervalued. Therefore, such

costing methods doesn't include fixed cost and consider only variable cost (Endenich, Brandau,

and Hoffjan, 2011).

Absorption costing: Such costing methods includes all expenses incurred in

manufacturing process which means fixed as well as variable cost are required to consider at the

time of valuation of products and services. It incudes every thing which is directly impact the

products. Such cost includes Labour cost, material cost, overhead expenses.

Comparison between Marginal and Absorption costing

Marginal costing Absorption costing

It only determines the variable cost and

ignore fined cost at the time of valuation of

products and services.

It adds both fixed and variable cost at the

time of valuation.

Using such method, the profitability appears

more due to gathering profits from each

individual sales.

Under this method, the profitability appear at

minimum.

Such method is useful for making an short

decisions in an organisation.

Such method is useful for making long-term

decisions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

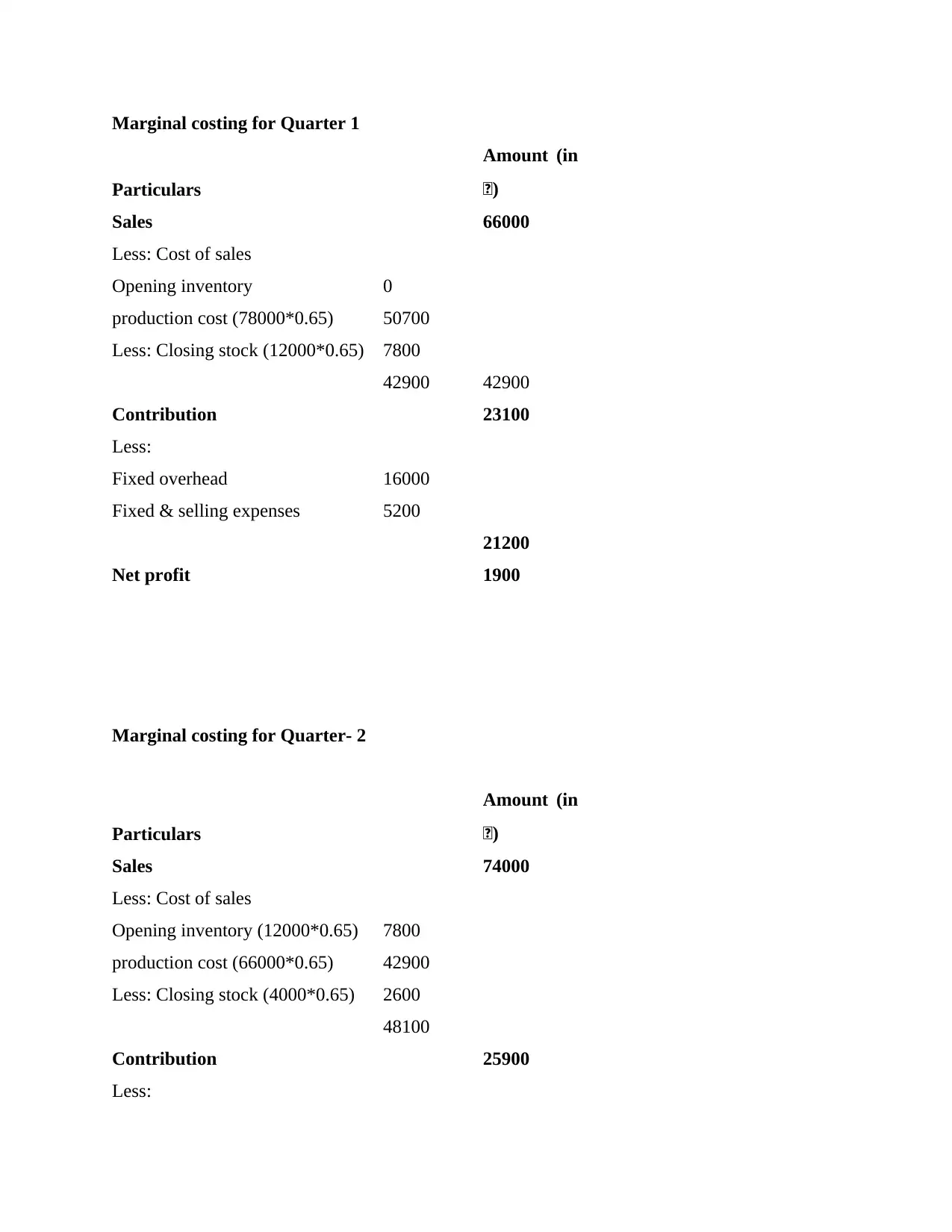

Marginal costing for Quarter 1

Particulars

Amount (in

£)

Sales 66000

Less: Cost of sales

Opening inventory 0

production cost (78000*0.65) 50700

Less: Closing stock (12000*0.65) 7800

42900 42900

Contribution 23100

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

Net profit 1900

Marginal costing for Quarter- 2

Particulars

Amount (in

£)

Sales 74000

Less: Cost of sales

Opening inventory (12000*0.65) 7800

production cost (66000*0.65) 42900

Less: Closing stock (4000*0.65) 2600

48100

Contribution 25900

Less:

Particulars

Amount (in

£)

Sales 66000

Less: Cost of sales

Opening inventory 0

production cost (78000*0.65) 50700

Less: Closing stock (12000*0.65) 7800

42900 42900

Contribution 23100

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

Net profit 1900

Marginal costing for Quarter- 2

Particulars

Amount (in

£)

Sales 74000

Less: Cost of sales

Opening inventory (12000*0.65) 7800

production cost (66000*0.65) 42900

Less: Closing stock (4000*0.65) 2600

48100

Contribution 25900

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

Net profit 4700

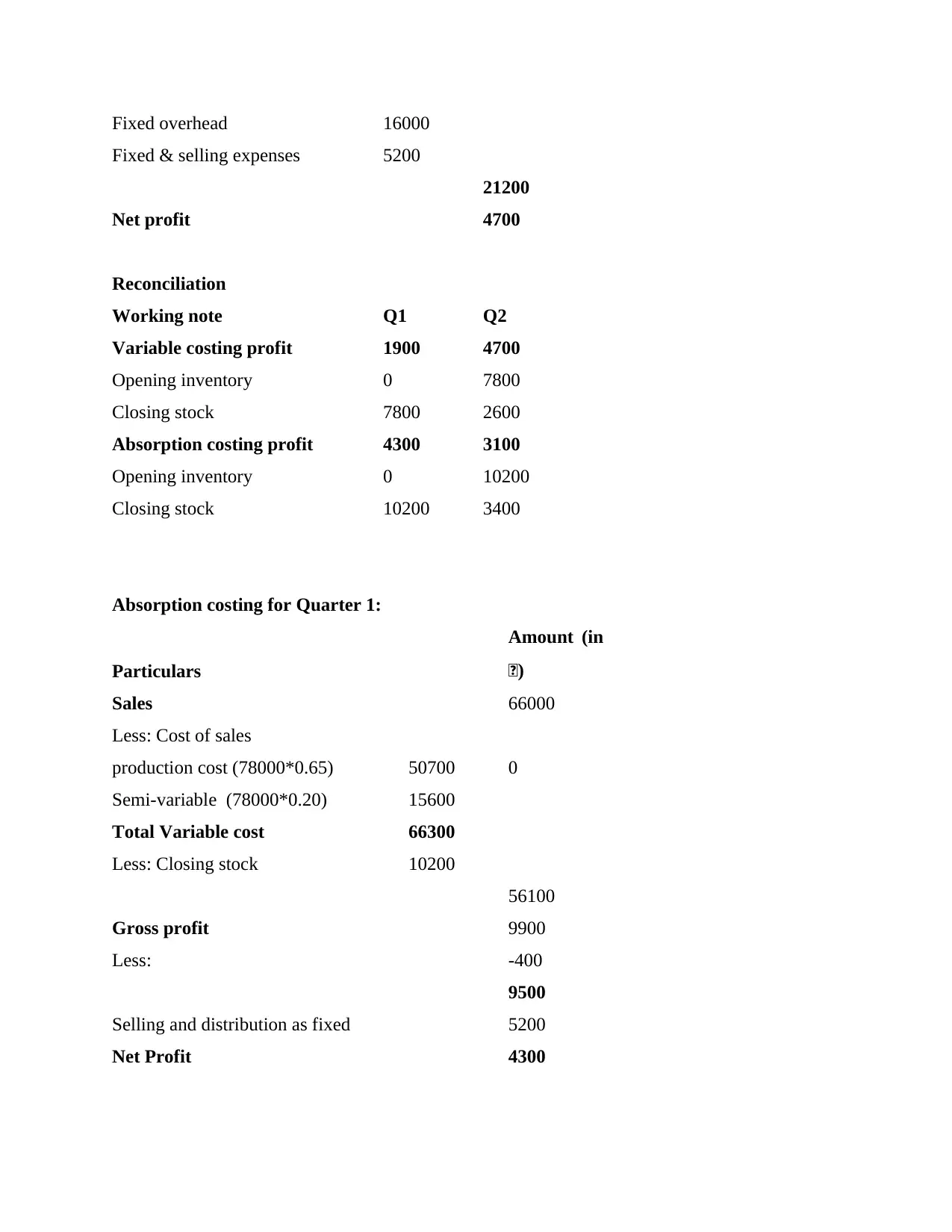

Reconciliation

Working note Q1 Q2

Variable costing profit 1900 4700

Opening inventory 0 7800

Closing stock 7800 2600

Absorption costing profit 4300 3100

Opening inventory 0 10200

Closing stock 10200 3400

Absorption costing for Quarter 1:

Particulars

Amount (in

£)

Sales 66000

Less: Cost of sales

production cost (78000*0.65) 50700 0

Semi-variable (78000*0.20) 15600

Total Variable cost 66300

Less: Closing stock 10200

56100

Gross profit 9900

Less: -400

9500

Selling and distribution as fixed 5200

Net Profit 4300

Fixed & selling expenses 5200

21200

Net profit 4700

Reconciliation

Working note Q1 Q2

Variable costing profit 1900 4700

Opening inventory 0 7800

Closing stock 7800 2600

Absorption costing profit 4300 3100

Opening inventory 0 10200

Closing stock 10200 3400

Absorption costing for Quarter 1:

Particulars

Amount (in

£)

Sales 66000

Less: Cost of sales

production cost (78000*0.65) 50700 0

Semi-variable (78000*0.20) 15600

Total Variable cost 66300

Less: Closing stock 10200

56100

Gross profit 9900

Less: -400

9500

Selling and distribution as fixed 5200

Net Profit 4300

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

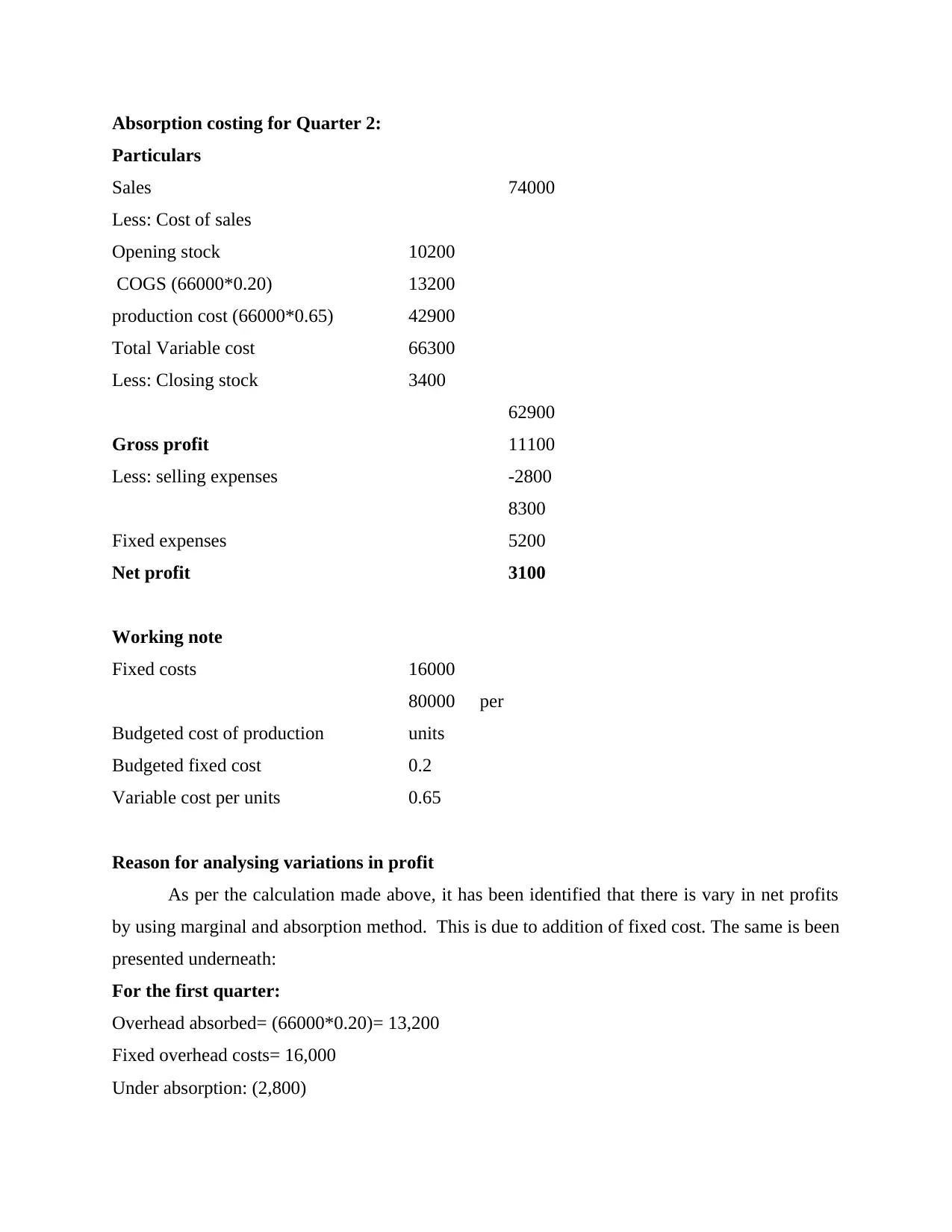

Absorption costing for Quarter 2:

Particulars

Sales 74000

Less: Cost of sales

Opening stock 10200

COGS (66000*0.20) 13200

production cost (66000*0.65) 42900

Total Variable cost 66300

Less: Closing stock 3400

62900

Gross profit 11100

Less: selling expenses -2800

8300

Fixed expenses 5200

Net profit 3100

Working note

Fixed costs 16000

Budgeted cost of production

80000 per

units

Budgeted fixed cost 0.2

Variable cost per units 0.65

Reason for analysing variations in profit

As per the calculation made above, it has been identified that there is vary in net profits

by using marginal and absorption method. This is due to addition of fixed cost. The same is been

presented underneath:

For the first quarter:

Overhead absorbed= (66000*0.20)= 13,200

Fixed overhead costs= 16,000

Under absorption: (2,800)

Particulars

Sales 74000

Less: Cost of sales

Opening stock 10200

COGS (66000*0.20) 13200

production cost (66000*0.65) 42900

Total Variable cost 66300

Less: Closing stock 3400

62900

Gross profit 11100

Less: selling expenses -2800

8300

Fixed expenses 5200

Net profit 3100

Working note

Fixed costs 16000

Budgeted cost of production

80000 per

units

Budgeted fixed cost 0.2

Variable cost per units 0.65

Reason for analysing variations in profit

As per the calculation made above, it has been identified that there is vary in net profits

by using marginal and absorption method. This is due to addition of fixed cost. The same is been

presented underneath:

For the first quarter:

Overhead absorbed= (66000*0.20)= 13,200

Fixed overhead costs= 16,000

Under absorption: (2,800)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

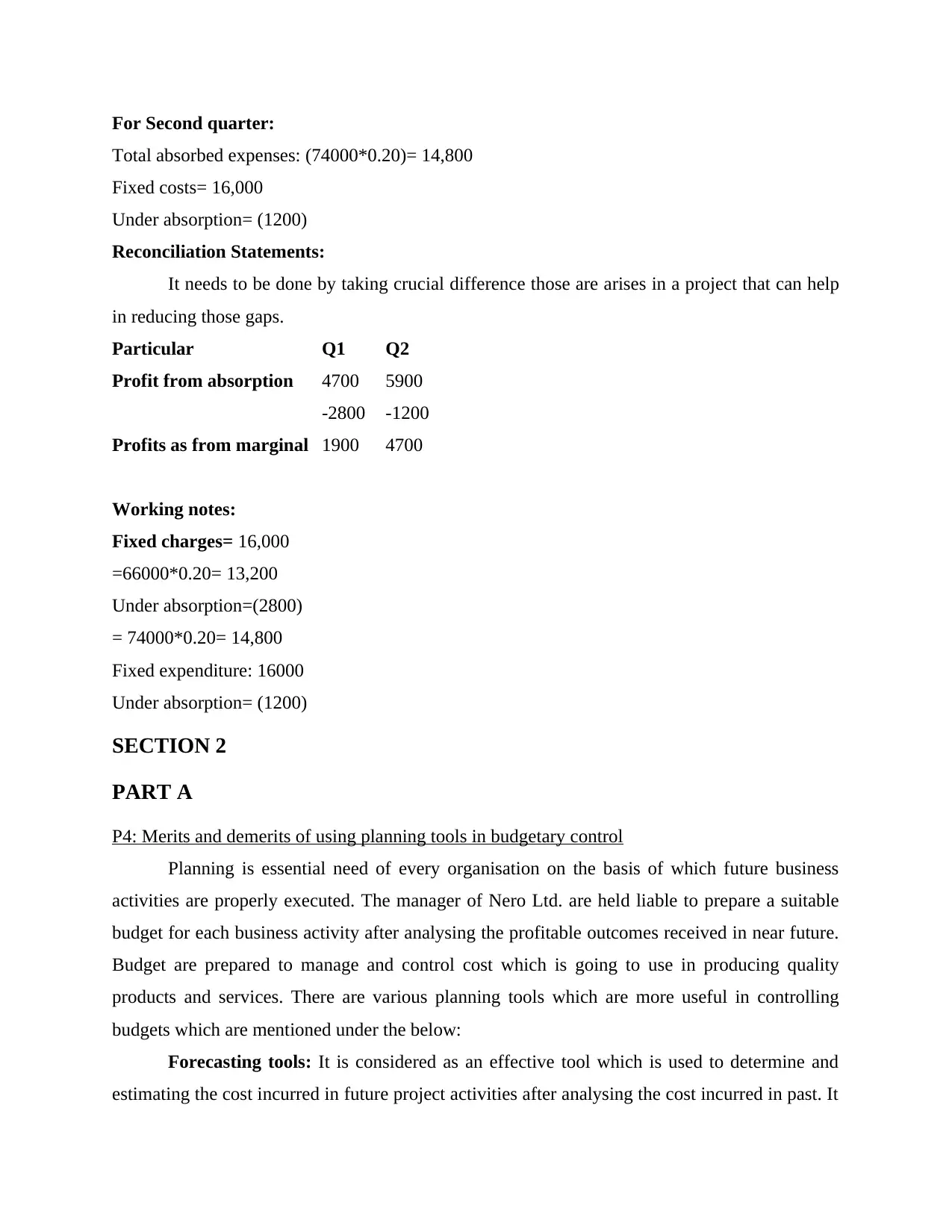

For Second quarter:

Total absorbed expenses: (74000*0.20)= 14,800

Fixed costs= 16,000

Under absorption= (1200)

Reconciliation Statements:

It needs to be done by taking crucial difference those are arises in a project that can help

in reducing those gaps.

Particular Q1 Q2

Profit from absorption 4700 5900

-2800 -1200

Profits as from marginal 1900 4700

Working notes:

Fixed charges= 16,000

=66000*0.20= 13,200

Under absorption=(2800)

= 74000*0.20= 14,800

Fixed expenditure: 16000

Under absorption= (1200)

SECTION 2

PART A

P4: Merits and demerits of using planning tools in budgetary control

Planning is essential need of every organisation on the basis of which future business

activities are properly executed. The manager of Nero Ltd. are held liable to prepare a suitable

budget for each business activity after analysing the profitable outcomes received in near future.

Budget are prepared to manage and control cost which is going to use in producing quality

products and services. There are various planning tools which are more useful in controlling

budgets which are mentioned under the below:

Forecasting tools: It is considered as an effective tool which is used to determine and

estimating the cost incurred in future project activities after analysing the cost incurred in past. It

Total absorbed expenses: (74000*0.20)= 14,800

Fixed costs= 16,000

Under absorption= (1200)

Reconciliation Statements:

It needs to be done by taking crucial difference those are arises in a project that can help

in reducing those gaps.

Particular Q1 Q2

Profit from absorption 4700 5900

-2800 -1200

Profits as from marginal 1900 4700

Working notes:

Fixed charges= 16,000

=66000*0.20= 13,200

Under absorption=(2800)

= 74000*0.20= 14,800

Fixed expenditure: 16000

Under absorption= (1200)

SECTION 2

PART A

P4: Merits and demerits of using planning tools in budgetary control

Planning is essential need of every organisation on the basis of which future business

activities are properly executed. The manager of Nero Ltd. are held liable to prepare a suitable

budget for each business activity after analysing the profitable outcomes received in near future.

Budget are prepared to manage and control cost which is going to use in producing quality

products and services. There are various planning tools which are more useful in controlling

budgets which are mentioned under the below:

Forecasting tools: It is considered as an effective tool which is used to determine and

estimating the cost incurred in future project activities after analysing the cost incurred in past. It

is more reliable and accurate as al the data and information are available and gather from internal

and external departments (Morales and Lambert, 2013). Merits: It helps in determining the estimation of cost which are going to incurred in

future project activities that makes company ready with the sufficient resources.

Demerits: Estimations are not accurate due to which the chances of getting profitable

outcomes in ear future will be low.

Contingency tools: Such tools is useful to deal with contingent situation that may occur in

execution of future business activities. This will help management in identifying the risk which

may influence the profitability of company. To deal with them in more effective manner, suitable

contingency tools are required to prepare for the purpose of analysing risk. Merit: It may not influences even at the time of contingencies which empowered

employees to make an effective decisions in order to cope up with future challenges.

Demerit: It consumes more time and money which affects the profitability of company.

Scenario planning: It is also an effective tool which is used to adopt in order to deal with

flexible situation at may arise in the process of long term business activities. This, such tools are

adopted by every organisation in order to achieve better possible outcomes from future business

activities (Otley and Emmanuel,2013). Merit: It brings beneficial result to company through analysing the uncertainties and

complexities which may affects profitability.

Demerit: It is much difficult for management to analyse future contingencies and

flexibilities due to which lots of issues and challenges may arises in the process of future

business activities.

PART B

P5: Various financial issues and measure to resolve it

Every organisation whether small, medium or large wants to maintain their strong

financial position in market which make them more capable to compete with their rivals. But due

to financial issues and problems the sustainability of company even many come in danger thus

must required to resolve such issues as quickly as possible through adopting various financial

tools and technique. Such tools and techniques includes:

and external departments (Morales and Lambert, 2013). Merits: It helps in determining the estimation of cost which are going to incurred in

future project activities that makes company ready with the sufficient resources.

Demerits: Estimations are not accurate due to which the chances of getting profitable

outcomes in ear future will be low.

Contingency tools: Such tools is useful to deal with contingent situation that may occur in

execution of future business activities. This will help management in identifying the risk which

may influence the profitability of company. To deal with them in more effective manner, suitable

contingency tools are required to prepare for the purpose of analysing risk. Merit: It may not influences even at the time of contingencies which empowered

employees to make an effective decisions in order to cope up with future challenges.

Demerit: It consumes more time and money which affects the profitability of company.

Scenario planning: It is also an effective tool which is used to adopt in order to deal with

flexible situation at may arise in the process of long term business activities. This, such tools are

adopted by every organisation in order to achieve better possible outcomes from future business

activities (Otley and Emmanuel,2013). Merit: It brings beneficial result to company through analysing the uncertainties and

complexities which may affects profitability.

Demerit: It is much difficult for management to analyse future contingencies and

flexibilities due to which lots of issues and challenges may arises in the process of future

business activities.

PART B

P5: Various financial issues and measure to resolve it

Every organisation whether small, medium or large wants to maintain their strong

financial position in market which make them more capable to compete with their rivals. But due

to financial issues and problems the sustainability of company even many come in danger thus

must required to resolve such issues as quickly as possible through adopting various financial

tools and technique. Such tools and techniques includes:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.