Comprehensive Financial Report: OOCL Performance Analysis (AAF0446)

VerifiedAdded on 2023/06/12

|13

|3066

|188

Report

AI Summary

This report provides a comprehensive analysis of Oriental Overseas Container Line (OOCL)'s financial and non-financial performance over the past two years, comparing it to key competitors like Cosco Shipping Line (CSL). The analysis includes ratio analysis of profitability, liquidity, efficiency, and gearing, highlighting trends and areas for improvement. Non-financial performance is evaluated through quarterly achievements and initiatives. A comparison with CSL reveals OOCL's strengths and weaknesses, leading to investment recommendations. The report concludes with an overall assessment of OOCL's financial health and future prospects, offering valuable insights for investors and stakeholders. Desklib provides access to this and many more solved assignments for students.

Accounting and Finance

AAF0446

AAF0446

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................4

Evaluating the performance of OOCL over the last two years in financial and non-financial....4

Terms...........................................................................................................................................4

Comparison of performance with key competitors......................................................................8

Recommendations to investors..................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................4

Evaluating the performance of OOCL over the last two years in financial and non-financial....4

Terms...........................................................................................................................................4

Comparison of performance with key competitors......................................................................8

Recommendations to investors..................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Accounting & finance are the crucial part that helps the organization to gain the relevant

information about the financial practices so that taking sound decision can become possible. In

the current era, having effectual financial reporting is important in order to obtain reliable

understanding so that making appropriate decision-making can become possible. The current

report is based on Oriental k Overseas Container Line which is one of the firm operating in the

container shipping and logistic service sector. The specified firm has the presence in the

transportation, logistic and terminal company along with possessing the vessels of the different

classes. The crucial features of the organization involves having safety, quality and

environmental management system that is helping the firm to perform well in the sector.

The one of the significant objective of the particular organization is to offer best and

innovative h international container transport & logistics service provider. The current financial

metric such as revenue, profitability, etc are indicating its good leading position in sector. There

are the various kinds of the resources which are used by the organization for gaining the ability

to coordinate with prevailing competition in sector. This involves using certified equipment,

operating homogenizes & oil purifiers, etc. These are the ways which helps in operating

successfully in the sector in turn achieving objective of gaining leading position in sector can

become possible.

There are few issues which are faced by the organization that has hampered its growth &

development and affected its ability to accomplish the objective. This includes ineffective

management of the container, inability to manage all dept, procurement & daily monitoring etc

that is leading to affect its capacity to function in the industry. These have impact on the ability t

attain the objectives of the organization. The current study will pay attention on assessing

performance in both financial and non financial terms. It will give emphasis on comparing its

performance with its key competitors such as Cosco Shipping Line (CSL) for understanding the

challenges faced by the company. This will pay attention on recommending that buying shares of

OOCL is beneficial or not.

Accounting & finance are the crucial part that helps the organization to gain the relevant

information about the financial practices so that taking sound decision can become possible. In

the current era, having effectual financial reporting is important in order to obtain reliable

understanding so that making appropriate decision-making can become possible. The current

report is based on Oriental k Overseas Container Line which is one of the firm operating in the

container shipping and logistic service sector. The specified firm has the presence in the

transportation, logistic and terminal company along with possessing the vessels of the different

classes. The crucial features of the organization involves having safety, quality and

environmental management system that is helping the firm to perform well in the sector.

The one of the significant objective of the particular organization is to offer best and

innovative h international container transport & logistics service provider. The current financial

metric such as revenue, profitability, etc are indicating its good leading position in sector. There

are the various kinds of the resources which are used by the organization for gaining the ability

to coordinate with prevailing competition in sector. This involves using certified equipment,

operating homogenizes & oil purifiers, etc. These are the ways which helps in operating

successfully in the sector in turn achieving objective of gaining leading position in sector can

become possible.

There are few issues which are faced by the organization that has hampered its growth &

development and affected its ability to accomplish the objective. This includes ineffective

management of the container, inability to manage all dept, procurement & daily monitoring etc

that is leading to affect its capacity to function in the industry. These have impact on the ability t

attain the objectives of the organization. The current study will pay attention on assessing

performance in both financial and non financial terms. It will give emphasis on comparing its

performance with its key competitors such as Cosco Shipping Line (CSL) for understanding the

challenges faced by the company. This will pay attention on recommending that buying shares of

OOCL is beneficial or not.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MAIN BODY

Evaluating the performance of OOCL over the last two years in financial and non-financial

Terms

It is important to get the significant information about the organization in both the

financial & non monetary terms so that accomplishing effective information about its

performance can be derived (Subalakshmi and Manikandan, 2018). Financial performance can

be judged by conducting the ratio analysis so that relevant and reliable evaluation of the

company's performance can be done.

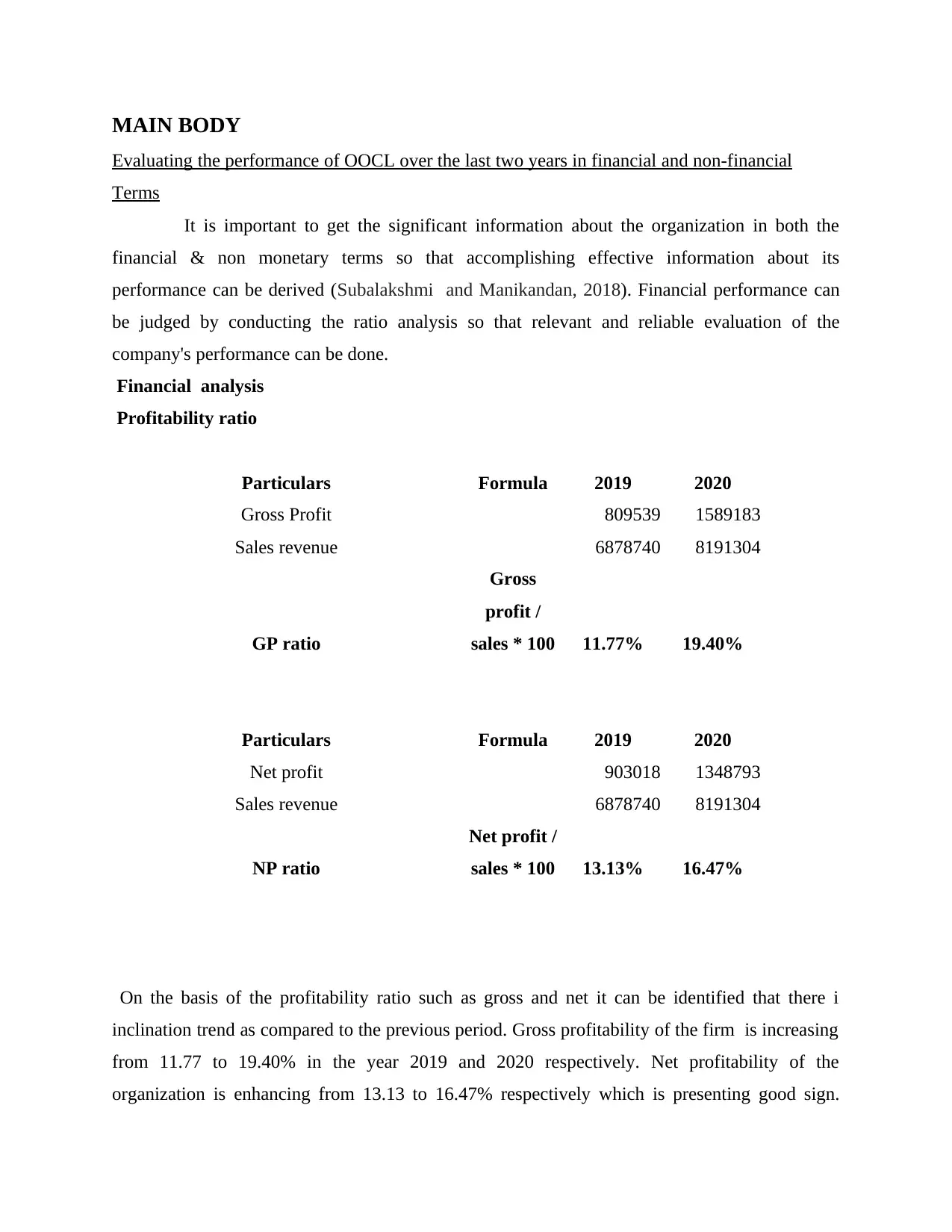

Financial analysis

Profitability ratio

Particulars Formula 2019 2020

Gross Profit 809539 1589183

Sales revenue 6878740 8191304

GP ratio

Gross

profit /

sales * 100 11.77% 19.40%

Particulars Formula 2019 2020

Net profit 903018 1348793

Sales revenue 6878740 8191304

NP ratio

Net profit /

sales * 100 13.13% 16.47%

On the basis of the profitability ratio such as gross and net it can be identified that there i

inclination trend as compared to the previous period. Gross profitability of the firm is increasing

from 11.77 to 19.40% in the year 2019 and 2020 respectively. Net profitability of the

organization is enhancing from 13.13 to 16.47% respectively which is presenting good sign.

Evaluating the performance of OOCL over the last two years in financial and non-financial

Terms

It is important to get the significant information about the organization in both the

financial & non monetary terms so that accomplishing effective information about its

performance can be derived (Subalakshmi and Manikandan, 2018). Financial performance can

be judged by conducting the ratio analysis so that relevant and reliable evaluation of the

company's performance can be done.

Financial analysis

Profitability ratio

Particulars Formula 2019 2020

Gross Profit 809539 1589183

Sales revenue 6878740 8191304

GP ratio

Gross

profit /

sales * 100 11.77% 19.40%

Particulars Formula 2019 2020

Net profit 903018 1348793

Sales revenue 6878740 8191304

NP ratio

Net profit /

sales * 100 13.13% 16.47%

On the basis of the profitability ratio such as gross and net it can be identified that there i

inclination trend as compared to the previous period. Gross profitability of the firm is increasing

from 11.77 to 19.40% in the year 2019 and 2020 respectively. Net profitability of the

organization is enhancing from 13.13 to 16.47% respectively which is presenting good sign.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

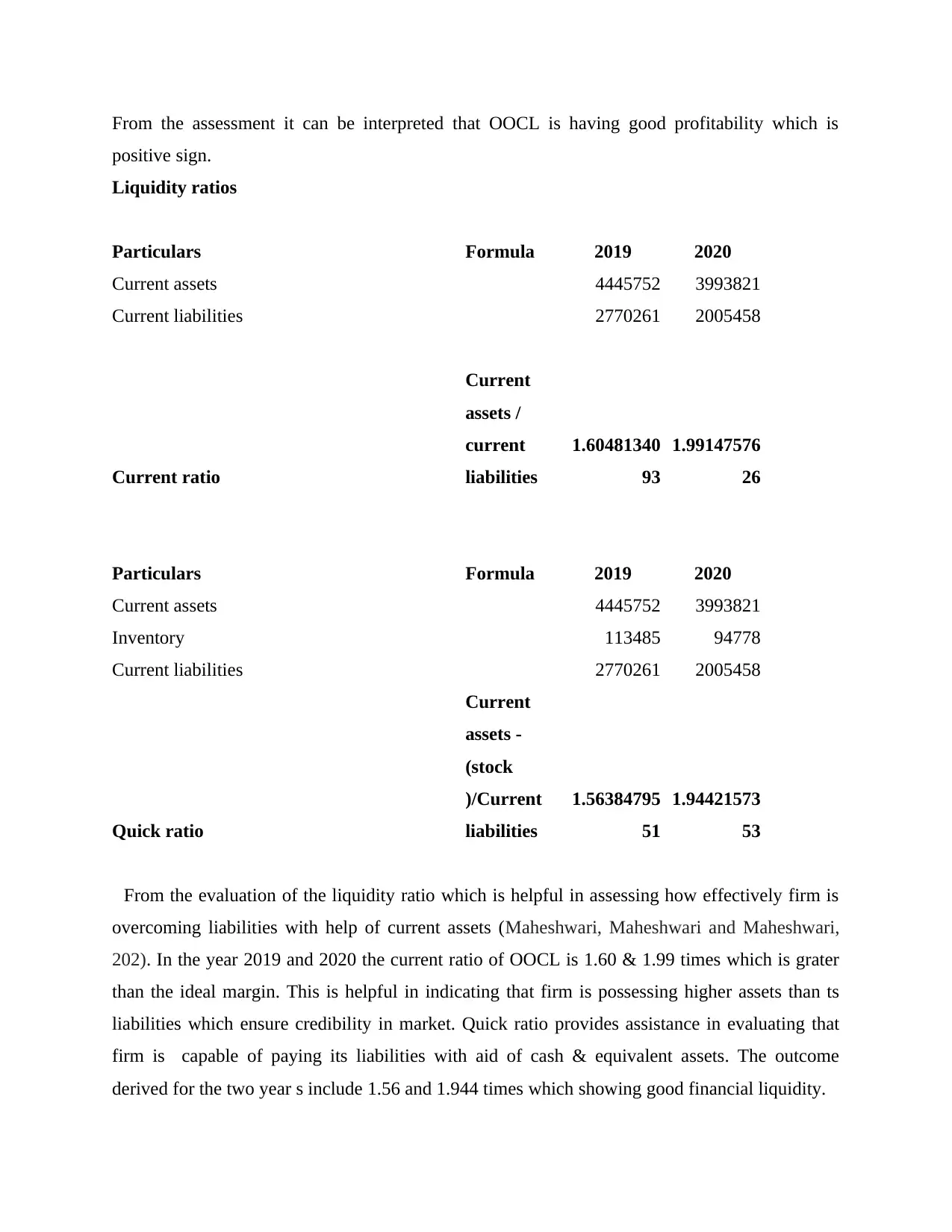

From the assessment it can be interpreted that OOCL is having good profitability which is

positive sign.

Liquidity ratios

Particulars Formula 2019 2020

Current assets 4445752 3993821

Current liabilities 2770261 2005458

Current ratio

Current

assets /

current

liabilities

1.60481340

93

1.99147576

26

Particulars Formula 2019 2020

Current assets 4445752 3993821

Inventory 113485 94778

Current liabilities 2770261 2005458

Quick ratio

Current

assets -

(stock

)/Current

liabilities

1.56384795

51

1.94421573

53

From the evaluation of the liquidity ratio which is helpful in assessing how effectively firm is

overcoming liabilities with help of current assets (Maheshwari, Maheshwari and Maheshwari,

202). In the year 2019 and 2020 the current ratio of OOCL is 1.60 & 1.99 times which is grater

than the ideal margin. This is helpful in indicating that firm is possessing higher assets than ts

liabilities which ensure credibility in market. Quick ratio provides assistance in evaluating that

firm is capable of paying its liabilities with aid of cash & equivalent assets. The outcome

derived for the two year s include 1.56 and 1.944 times which showing good financial liquidity.

positive sign.

Liquidity ratios

Particulars Formula 2019 2020

Current assets 4445752 3993821

Current liabilities 2770261 2005458

Current ratio

Current

assets /

current

liabilities

1.60481340

93

1.99147576

26

Particulars Formula 2019 2020

Current assets 4445752 3993821

Inventory 113485 94778

Current liabilities 2770261 2005458

Quick ratio

Current

assets -

(stock

)/Current

liabilities

1.56384795

51

1.94421573

53

From the evaluation of the liquidity ratio which is helpful in assessing how effectively firm is

overcoming liabilities with help of current assets (Maheshwari, Maheshwari and Maheshwari,

202). In the year 2019 and 2020 the current ratio of OOCL is 1.60 & 1.99 times which is grater

than the ideal margin. This is helpful in indicating that firm is possessing higher assets than ts

liabilities which ensure credibility in market. Quick ratio provides assistance in evaluating that

firm is capable of paying its liabilities with aid of cash & equivalent assets. The outcome

derived for the two year s include 1.56 and 1.944 times which showing good financial liquidity.

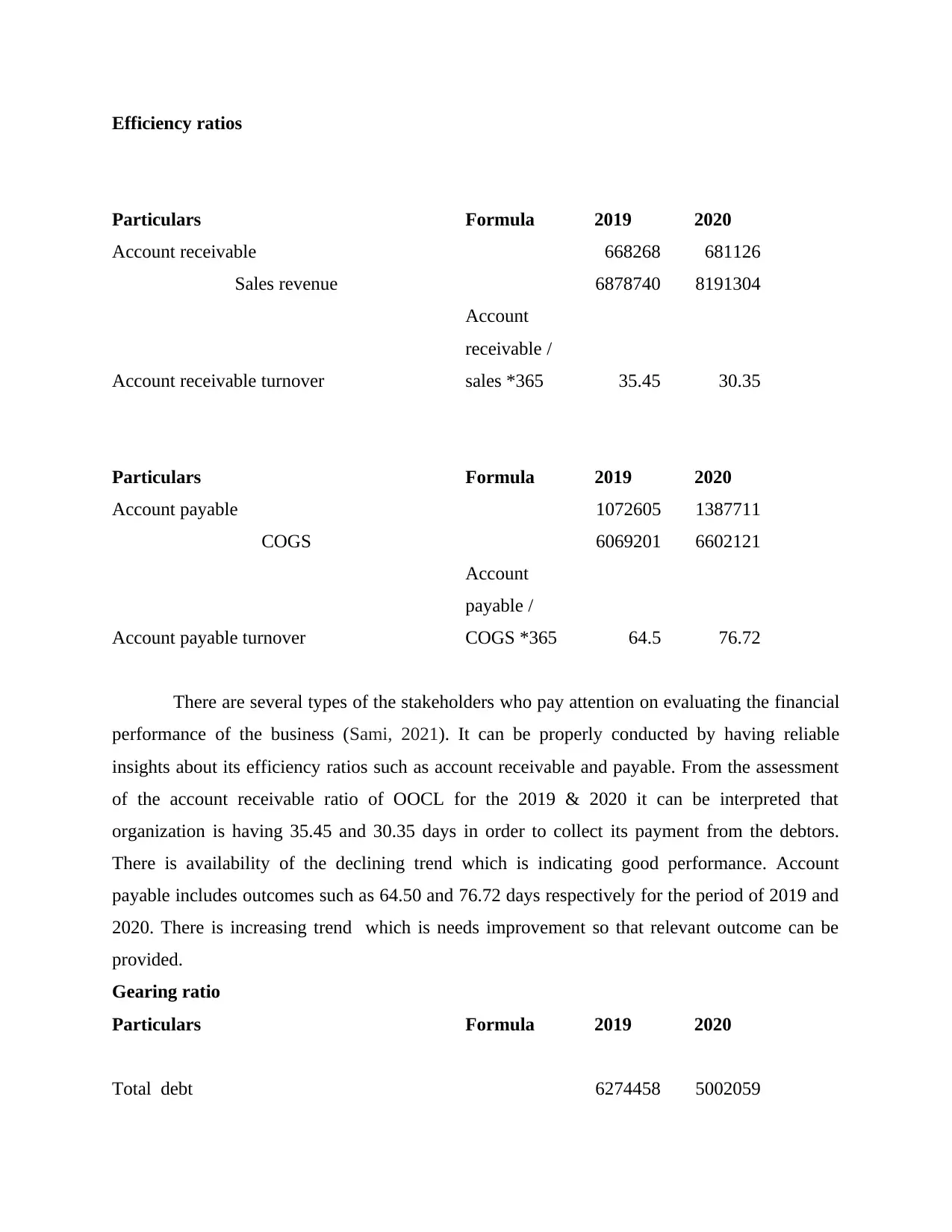

Efficiency ratios

Particulars Formula 2019 2020

Account receivable 668268 681126

Sales revenue 6878740 8191304

Account receivable turnover

Account

receivable /

sales *365 35.45 30.35

Particulars Formula 2019 2020

Account payable 1072605 1387711

COGS 6069201 6602121

Account payable turnover

Account

payable /

COGS *365 64.5 76.72

There are several types of the stakeholders who pay attention on evaluating the financial

performance of the business (Sami, 2021). It can be properly conducted by having reliable

insights about its efficiency ratios such as account receivable and payable. From the assessment

of the account receivable ratio of OOCL for the 2019 & 2020 it can be interpreted that

organization is having 35.45 and 30.35 days in order to collect its payment from the debtors.

There is availability of the declining trend which is indicating good performance. Account

payable includes outcomes such as 64.50 and 76.72 days respectively for the period of 2019 and

2020. There is increasing trend which is needs improvement so that relevant outcome can be

provided.

Gearing ratio

Particulars Formula 2019 2020

Total debt 6274458 5002059

Particulars Formula 2019 2020

Account receivable 668268 681126

Sales revenue 6878740 8191304

Account receivable turnover

Account

receivable /

sales *365 35.45 30.35

Particulars Formula 2019 2020

Account payable 1072605 1387711

COGS 6069201 6602121

Account payable turnover

Account

payable /

COGS *365 64.5 76.72

There are several types of the stakeholders who pay attention on evaluating the financial

performance of the business (Sami, 2021). It can be properly conducted by having reliable

insights about its efficiency ratios such as account receivable and payable. From the assessment

of the account receivable ratio of OOCL for the 2019 & 2020 it can be interpreted that

organization is having 35.45 and 30.35 days in order to collect its payment from the debtors.

There is availability of the declining trend which is indicating good performance. Account

payable includes outcomes such as 64.50 and 76.72 days respectively for the period of 2019 and

2020. There is increasing trend which is needs improvement so that relevant outcome can be

provided.

Gearing ratio

Particulars Formula 2019 2020

Total debt 6274458 5002059

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

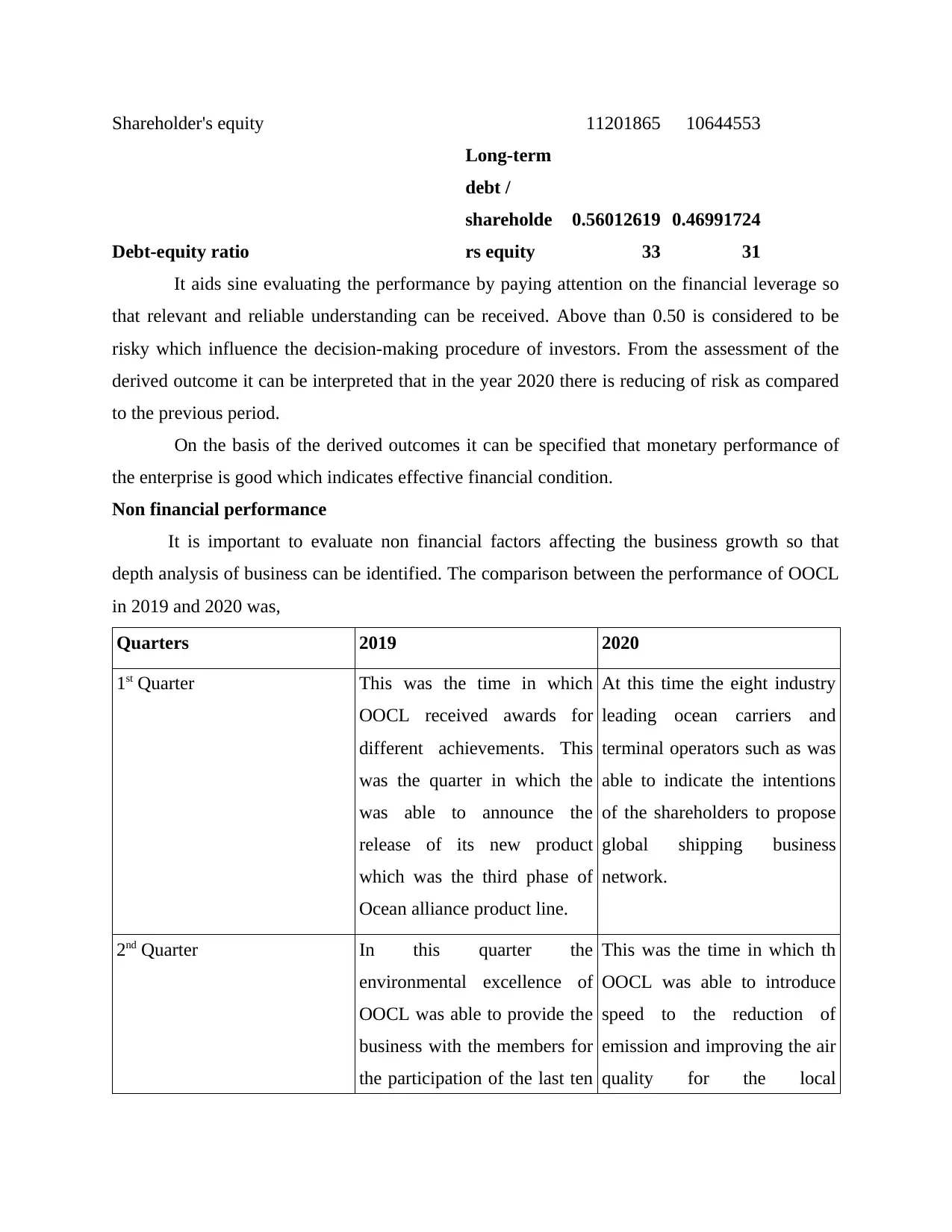

Shareholder's equity 11201865 10644553

Debt-equity ratio

Long-term

debt /

shareholde

rs equity

0.56012619

33

0.46991724

31

It aids sine evaluating the performance by paying attention on the financial leverage so

that relevant and reliable understanding can be received. Above than 0.50 is considered to be

risky which influence the decision-making procedure of investors. From the assessment of the

derived outcome it can be interpreted that in the year 2020 there is reducing of risk as compared

to the previous period.

On the basis of the derived outcomes it can be specified that monetary performance of

the enterprise is good which indicates effective financial condition.

Non financial performance

It is important to evaluate non financial factors affecting the business growth so that

depth analysis of business can be identified. The comparison between the performance of OOCL

in 2019 and 2020 was,

Quarters 2019 2020

1st Quarter This was the time in which

OOCL received awards for

different achievements. This

was the quarter in which the

was able to announce the

release of its new product

which was the third phase of

Ocean alliance product line.

At this time the eight industry

leading ocean carriers and

terminal operators such as was

able to indicate the intentions

of the shareholders to propose

global shipping business

network.

2nd Quarter In this quarter the

environmental excellence of

OOCL was able to provide the

business with the members for

the participation of the last ten

This was the time in which th

OOCL was able to introduce

speed to the reduction of

emission and improving the air

quality for the local

Debt-equity ratio

Long-term

debt /

shareholde

rs equity

0.56012619

33

0.46991724

31

It aids sine evaluating the performance by paying attention on the financial leverage so

that relevant and reliable understanding can be received. Above than 0.50 is considered to be

risky which influence the decision-making procedure of investors. From the assessment of the

derived outcome it can be interpreted that in the year 2020 there is reducing of risk as compared

to the previous period.

On the basis of the derived outcomes it can be specified that monetary performance of

the enterprise is good which indicates effective financial condition.

Non financial performance

It is important to evaluate non financial factors affecting the business growth so that

depth analysis of business can be identified. The comparison between the performance of OOCL

in 2019 and 2020 was,

Quarters 2019 2020

1st Quarter This was the time in which

OOCL received awards for

different achievements. This

was the quarter in which the

was able to announce the

release of its new product

which was the third phase of

Ocean alliance product line.

At this time the eight industry

leading ocean carriers and

terminal operators such as was

able to indicate the intentions

of the shareholders to propose

global shipping business

network.

2nd Quarter In this quarter the

environmental excellence of

OOCL was able to provide the

business with the members for

the participation of the last ten

This was the time in which th

OOCL was able to introduce

speed to the reduction of

emission and improving the air

quality for the local

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

years for the fourth year. This

was also the time in which this

business won OOCL received

the Top Ranked Carrier 2019

award.

communities. It also started

offering competitive transit

between Chile and Southern

china.

3rd Quarter This was also able to announce

the appointment for the new

executive officer for the

business was able to leverage

new technologies for such as

artificial intelligence which

helped the business in the

management of the

organization operations.

In this stage it was able to

launch new products with the

name of china starits servcies 1

and china stratits services 2

which has been able to

enhance the market coverage

between the china Singapore

and Malaysia for providing

them competitive and reliable

shipment.

4th Quarter This was the time when the

OOCL was honoured to

receive the excellence award at

2019 Lloyd's list Europe

awards. This is considered to

be the communication of the

unsustainably exercise for

minimization of marine

environment.

In the last quarter this business

was able to increase its

operations very efficiently for

which it hired many new

employees that were the reason

for the organization of the

industry.

was also the time in which this

business won OOCL received

the Top Ranked Carrier 2019

award.

communities. It also started

offering competitive transit

between Chile and Southern

china.

3rd Quarter This was also able to announce

the appointment for the new

executive officer for the

business was able to leverage

new technologies for such as

artificial intelligence which

helped the business in the

management of the

organization operations.

In this stage it was able to

launch new products with the

name of china starits servcies 1

and china stratits services 2

which has been able to

enhance the market coverage

between the china Singapore

and Malaysia for providing

them competitive and reliable

shipment.

4th Quarter This was the time when the

OOCL was honoured to

receive the excellence award at

2019 Lloyd's list Europe

awards. This is considered to

be the communication of the

unsustainably exercise for

minimization of marine

environment.

In the last quarter this business

was able to increase its

operations very efficiently for

which it hired many new

employees that were the reason

for the organization of the

industry.

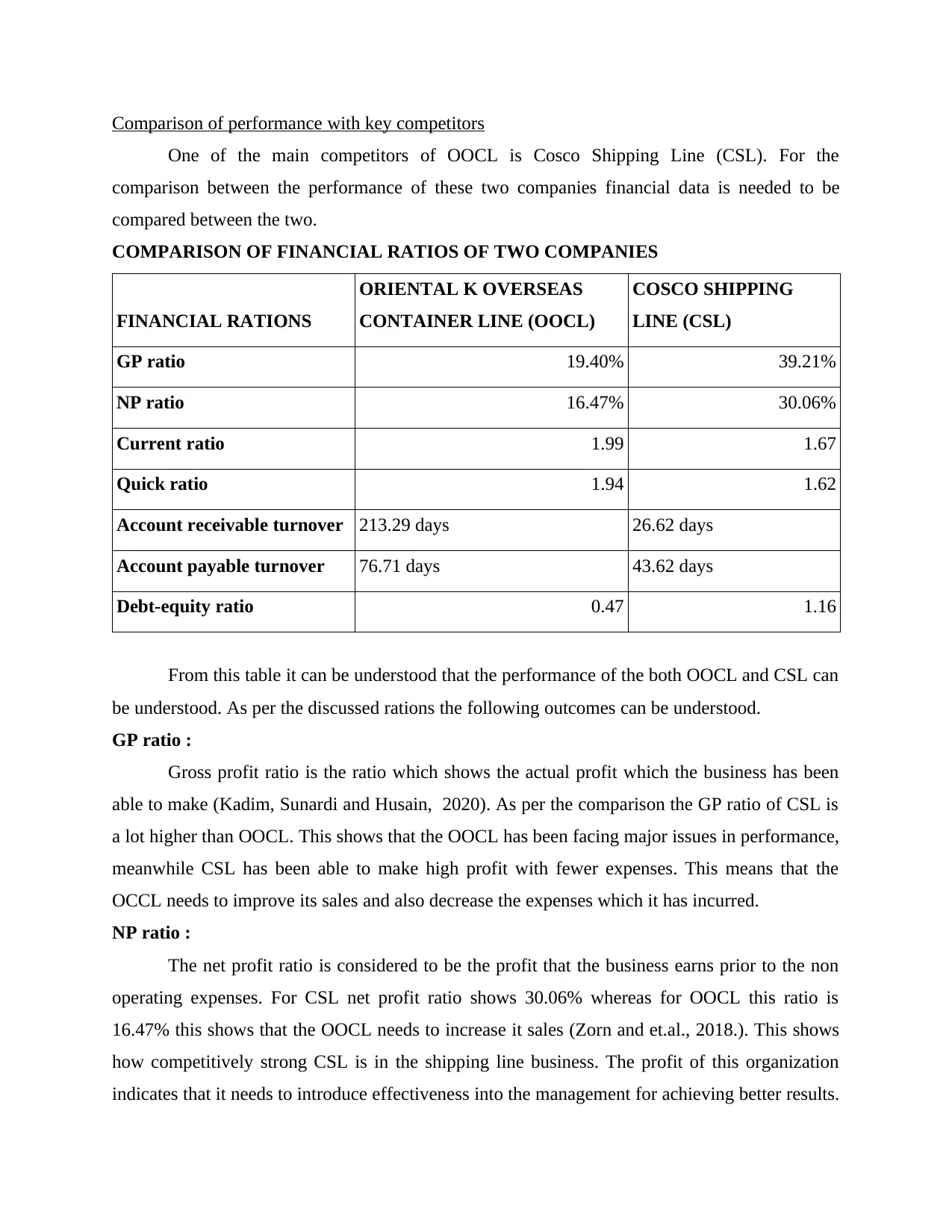

Comparison of performance with key competitors

One of the main competitors of OOCL is Cosco Shipping Line (CSL). For the

comparison between the performance of these two companies financial data is needed to be

compared between the two.

COMPARISON OF FINANCIAL RATIOS OF TWO COMPANIES

FINANCIAL RATIONS

ORIENTAL K OVERSEAS

CONTAINER LINE (OOCL)

COSCO SHIPPING

LINE (CSL)

GP ratio 19.40% 39.21%

NP ratio 16.47% 30.06%

Current ratio 1.99 1.67

Quick ratio 1.94 1.62

Account receivable turnover 213.29 days 26.62 days

Account payable turnover 76.71 days 43.62 days

Debt-equity ratio 0.47 1.16

From this table it can be understood that the performance of the both OOCL and CSL can

be understood. As per the discussed rations the following outcomes can be understood.

GP ratio :

Gross profit ratio is the ratio which shows the actual profit which the business has been

able to make (Kadim, Sunardi and Husain, 2020). As per the comparison the GP ratio of CSL is

a lot higher than OOCL. This shows that the OOCL has been facing major issues in performance,

meanwhile CSL has been able to make high profit with fewer expenses. This means that the

OCCL needs to improve its sales and also decrease the expenses which it has incurred.

NP ratio :

The net profit ratio is considered to be the profit that the business earns prior to the non

operating expenses. For CSL net profit ratio shows 30.06% whereas for OOCL this ratio is

16.47% this shows that the OOCL needs to increase it sales (Zorn and et.al., 2018.). This shows

how competitively strong CSL is in the shipping line business. The profit of this organization

indicates that it needs to introduce effectiveness into the management for achieving better results.

One of the main competitors of OOCL is Cosco Shipping Line (CSL). For the

comparison between the performance of these two companies financial data is needed to be

compared between the two.

COMPARISON OF FINANCIAL RATIOS OF TWO COMPANIES

FINANCIAL RATIONS

ORIENTAL K OVERSEAS

CONTAINER LINE (OOCL)

COSCO SHIPPING

LINE (CSL)

GP ratio 19.40% 39.21%

NP ratio 16.47% 30.06%

Current ratio 1.99 1.67

Quick ratio 1.94 1.62

Account receivable turnover 213.29 days 26.62 days

Account payable turnover 76.71 days 43.62 days

Debt-equity ratio 0.47 1.16

From this table it can be understood that the performance of the both OOCL and CSL can

be understood. As per the discussed rations the following outcomes can be understood.

GP ratio :

Gross profit ratio is the ratio which shows the actual profit which the business has been

able to make (Kadim, Sunardi and Husain, 2020). As per the comparison the GP ratio of CSL is

a lot higher than OOCL. This shows that the OOCL has been facing major issues in performance,

meanwhile CSL has been able to make high profit with fewer expenses. This means that the

OCCL needs to improve its sales and also decrease the expenses which it has incurred.

NP ratio :

The net profit ratio is considered to be the profit that the business earns prior to the non

operating expenses. For CSL net profit ratio shows 30.06% whereas for OOCL this ratio is

16.47% this shows that the OOCL needs to increase it sales (Zorn and et.al., 2018.). This shows

how competitively strong CSL is in the shipping line business. The profit of this organization

indicates that it needs to introduce effectiveness into the management for achieving better results.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Current ratio :

Current ratio is the ratio which measures the company's ability to pay short-term

obligations for those within one year. This is considered to be the factor which influences the

growth in the organization as it helps the business to have the capacity to run its business. The

idea current ratio for an organization is 2:1. In this comparison table the CSL has 1.67 current

ratio but OOCL has 1.99 which is very close to idea current ratio (COSCO SHIPPING Holdings

Co Ltd, 2021). This is the indication of OOCL having efficiency in the management of the assets

and liabilities and being very effective in the management of the ability to pay of the short-term

obligation in comparison to competitors CSL.

Quick Ratio :

Quick ratio is the measurement of the company's capacity to pay its current liabilities

without needing to sell its inventory for obtaining the additional financing. This ratio is

considered to be the ratio which is the quickest for the measuring the efficiency of the

organization. Quick ratio is considered to be good and healthy between 1.2 to 2. In this

comparison OOCL has 1.94 as the quick ratio which is very ideal but in comparison to CSL has

an upper hand.

Account receivable turnover :

Account receivable turnover is number of days which the business takes per year for the

collection of the average accounts receivable (Lukason and Andresson, 2019). The accountants

and analysts are known to use the accounts receivable turnover for the measurement of the

efficiency of the business for the collection of the credit provided by the customers. As per this

analysation OOCL is facing major issues as it has 213.29 days of accounts receivable turnover.

This is the indication of the average time which the business takes to recover its receivables.

CSL has been very efficient in the collection of the receivable which is 26.62 days.

Account Payable turnover :

This is the average time which is taken by the organization to pay of its obligations

(Niggle, 2019). These obligations indicate that the OOCL is more efficient in comparison to

CSL. This is due to the fact that payable turnover needs to be higher for an organization. This

shows that the business can have control on the money for a longer period. It can help the

company to reinvest that money for generating more income.

Debt equity ratio :

Current ratio is the ratio which measures the company's ability to pay short-term

obligations for those within one year. This is considered to be the factor which influences the

growth in the organization as it helps the business to have the capacity to run its business. The

idea current ratio for an organization is 2:1. In this comparison table the CSL has 1.67 current

ratio but OOCL has 1.99 which is very close to idea current ratio (COSCO SHIPPING Holdings

Co Ltd, 2021). This is the indication of OOCL having efficiency in the management of the assets

and liabilities and being very effective in the management of the ability to pay of the short-term

obligation in comparison to competitors CSL.

Quick Ratio :

Quick ratio is the measurement of the company's capacity to pay its current liabilities

without needing to sell its inventory for obtaining the additional financing. This ratio is

considered to be the ratio which is the quickest for the measuring the efficiency of the

organization. Quick ratio is considered to be good and healthy between 1.2 to 2. In this

comparison OOCL has 1.94 as the quick ratio which is very ideal but in comparison to CSL has

an upper hand.

Account receivable turnover :

Account receivable turnover is number of days which the business takes per year for the

collection of the average accounts receivable (Lukason and Andresson, 2019). The accountants

and analysts are known to use the accounts receivable turnover for the measurement of the

efficiency of the business for the collection of the credit provided by the customers. As per this

analysation OOCL is facing major issues as it has 213.29 days of accounts receivable turnover.

This is the indication of the average time which the business takes to recover its receivables.

CSL has been very efficient in the collection of the receivable which is 26.62 days.

Account Payable turnover :

This is the average time which is taken by the organization to pay of its obligations

(Niggle, 2019). These obligations indicate that the OOCL is more efficient in comparison to

CSL. This is due to the fact that payable turnover needs to be higher for an organization. This

shows that the business can have control on the money for a longer period. It can help the

company to reinvest that money for generating more income.

Debt equity ratio :

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This compares the company's total liabilities to its shareholder equity (Le and Viviani,

2018). Thus, this is the ratio that is useful for measuring the risk of that the business faces.

Higher debt to equity shows that the business is at more risk which is the case with CSL.

However, OOCL is able to gain the competitive advantage by having less debt-equity ratio at

0.47.

The conditions face by this CSL is very similar OOCL however there are differences in

the customers which can be considered to be based on the performance of the organization.

Challenges face by this organization might be different due to the differences in the government

policies of the different countries for which they operate.

Recommendations to investors

From the evaluation of the financial ratio it was can be said that it will be a reasonable

argument for the investors to buy the shares of OOCL. The reason why the investors needs to

invest in the shares can be said to be the debt-equity ratio which for OOCL is 0.47 (Ding, Peng

and Wang, 2019). Higher the debt the equity ratio the business is at higher risk. Thus, in

comparison to the market this ratio for OOCL is very low. This is the indication of low risk at the

business of the organization it can be considered to be the factor which influences the investment

decisions taken by the organization.

Other than than it is also very important for the investor to consider the gross profit and

net profit ratio of this organization which in comparison to its competitors is quite low. This

shows that the business is actually falling short of its actual capacity which impacts the growth of

the organization. For instance, it can be said that the investors needs to focus on areas which can

bring both value and earlier. The investment of the shares of OOCL can be said as a risk free

investment due to the financial feasibility it indicates.

CONCLUSION

In this project I was able to conclude that the performance of OOCL in the past 3 years

have improved significantly. I was able to identify this through the comparison of the non

financial and financial data of 2019 and 2020. My knowledge about the financial ratio

calculation was very handling in this situation for analysing the results and interpreting the

performance of the organization. I research about the competitors of this organization and was

able to find that CSL was one of the biggest competitors of this company and was the major

2018). Thus, this is the ratio that is useful for measuring the risk of that the business faces.

Higher debt to equity shows that the business is at more risk which is the case with CSL.

However, OOCL is able to gain the competitive advantage by having less debt-equity ratio at

0.47.

The conditions face by this CSL is very similar OOCL however there are differences in

the customers which can be considered to be based on the performance of the organization.

Challenges face by this organization might be different due to the differences in the government

policies of the different countries for which they operate.

Recommendations to investors

From the evaluation of the financial ratio it was can be said that it will be a reasonable

argument for the investors to buy the shares of OOCL. The reason why the investors needs to

invest in the shares can be said to be the debt-equity ratio which for OOCL is 0.47 (Ding, Peng

and Wang, 2019). Higher the debt the equity ratio the business is at higher risk. Thus, in

comparison to the market this ratio for OOCL is very low. This is the indication of low risk at the

business of the organization it can be considered to be the factor which influences the investment

decisions taken by the organization.

Other than than it is also very important for the investor to consider the gross profit and

net profit ratio of this organization which in comparison to its competitors is quite low. This

shows that the business is actually falling short of its actual capacity which impacts the growth of

the organization. For instance, it can be said that the investors needs to focus on areas which can

bring both value and earlier. The investment of the shares of OOCL can be said as a risk free

investment due to the financial feasibility it indicates.

CONCLUSION

In this project I was able to conclude that the performance of OOCL in the past 3 years

have improved significantly. I was able to identify this through the comparison of the non

financial and financial data of 2019 and 2020. My knowledge about the financial ratio

calculation was very handling in this situation for analysing the results and interpreting the

performance of the organization. I research about the competitors of this organization and was

able to find that CSL was one of the biggest competitors of this company and was the major

competitive threat to this organization. I was able to gather the information regarding the

financial viability of CSL and this allowed me to compare both the companies and find out the

areas in which OOCL had competitive advantage. In this project I focused on studying the

performance of OOCL and identify whether investors should invest in there shares or not.

financial viability of CSL and this allowed me to compare both the companies and find out the

areas in which OOCL had competitive advantage. In this project I focused on studying the

performance of OOCL and identify whether investors should invest in there shares or not.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.