Financial Management and Control: Primetown Plc Performance Report

VerifiedAdded on 2020/01/07

|25

|5462

|190

Report

AI Summary

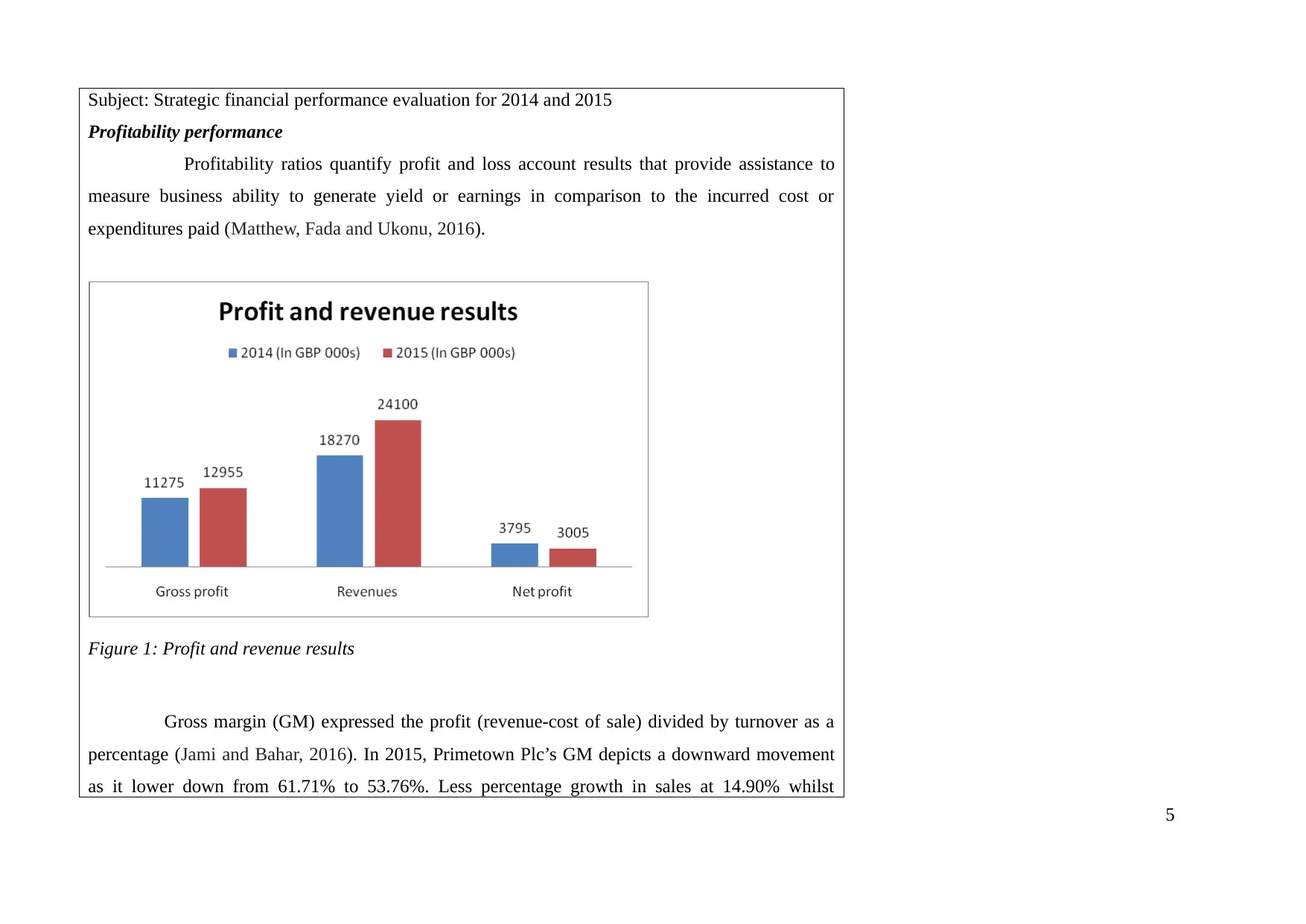

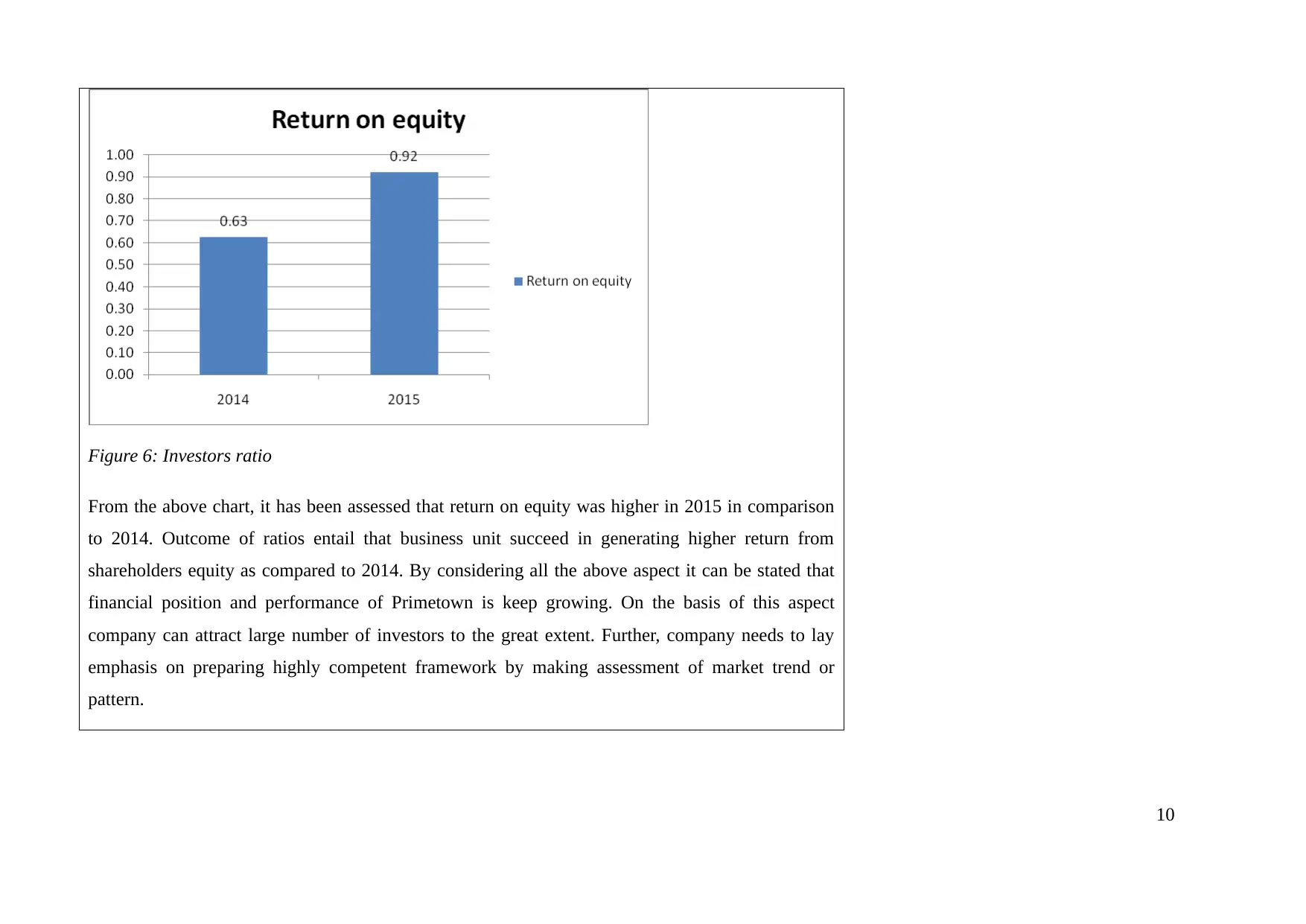

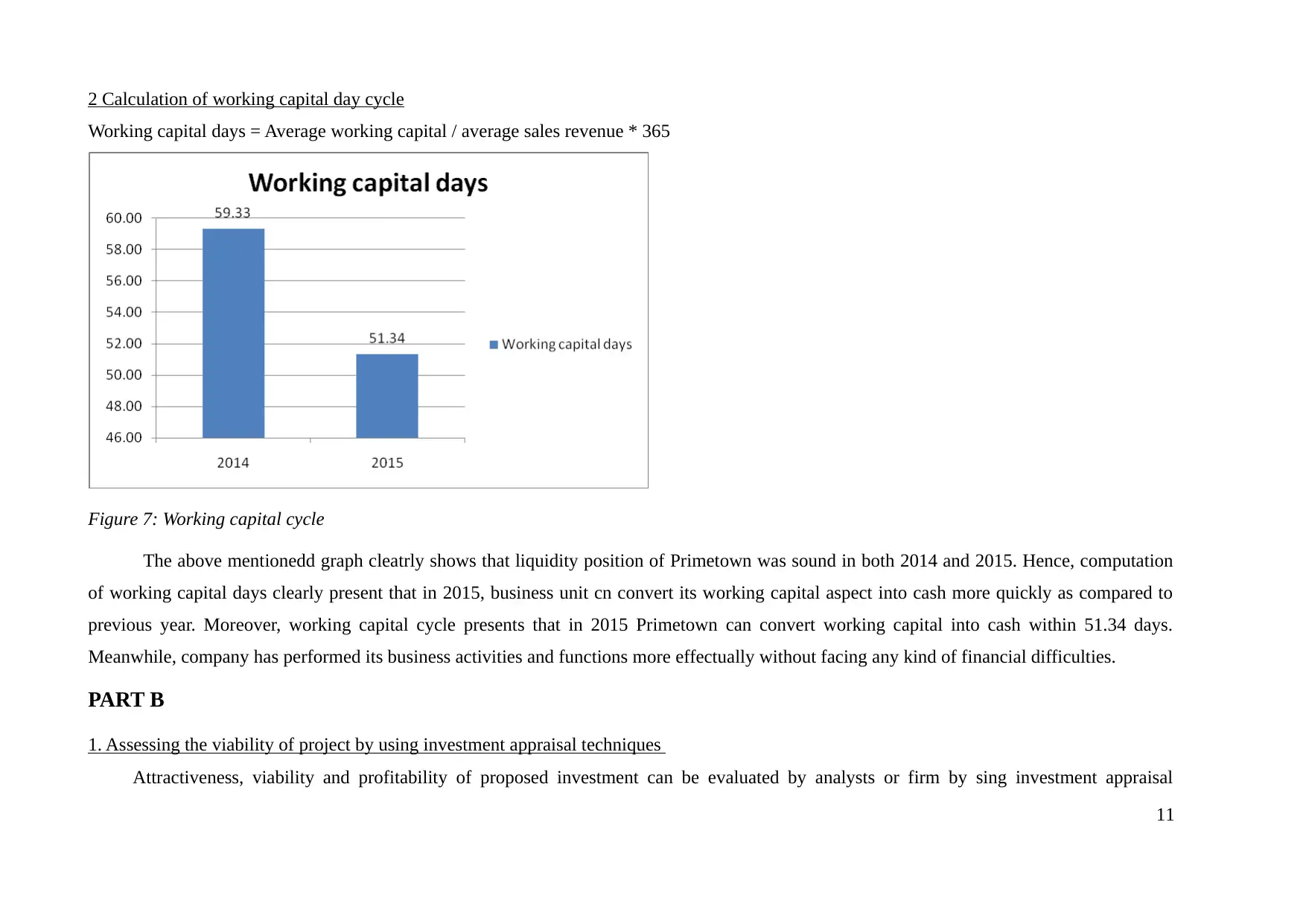

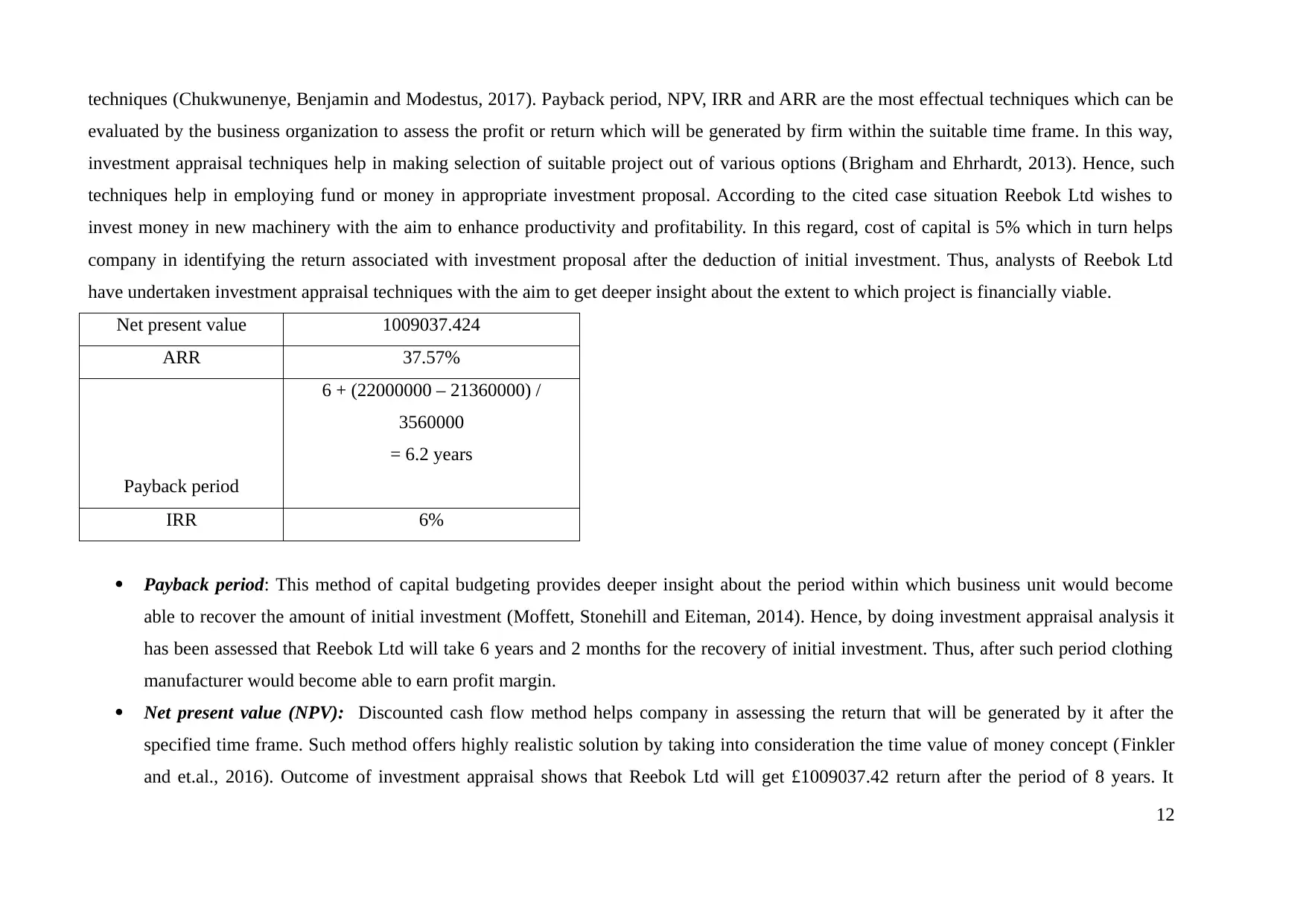

This report provides a comprehensive financial analysis of Primetown Plc, examining its performance from 2014 to 2015. It begins with an introduction to financial management and control, emphasizing the importance of capital for business operations. The report then presents a detailed analysis of Primetown Plc's financial statements using ratio analysis to assess profitability, liquidity, gearing, asset efficiency, and investor ratios. A key component is the calculation and interpretation of the working capital day cycle. Furthermore, the report delves into investment appraisal techniques, evaluating the viability of potential projects using methods such as Payback Period, Net Present Value (NPV), Average Rate of Return (ARR), and Internal Rate of Return (IRR). The merits and limitations of these appraisal techniques are critically assessed. The report also explores the role of budgeting in short-term decision-making and evaluates the practical implications of break-even analysis. The analysis uses figures and tables to support the findings, providing a clear picture of Primetown Plc's financial health and investment opportunities.

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.