Accounting Project: Managing Financial Performance and Ledger

VerifiedAdded on 2021/01/02

|9

|1812

|140

Project

AI Summary

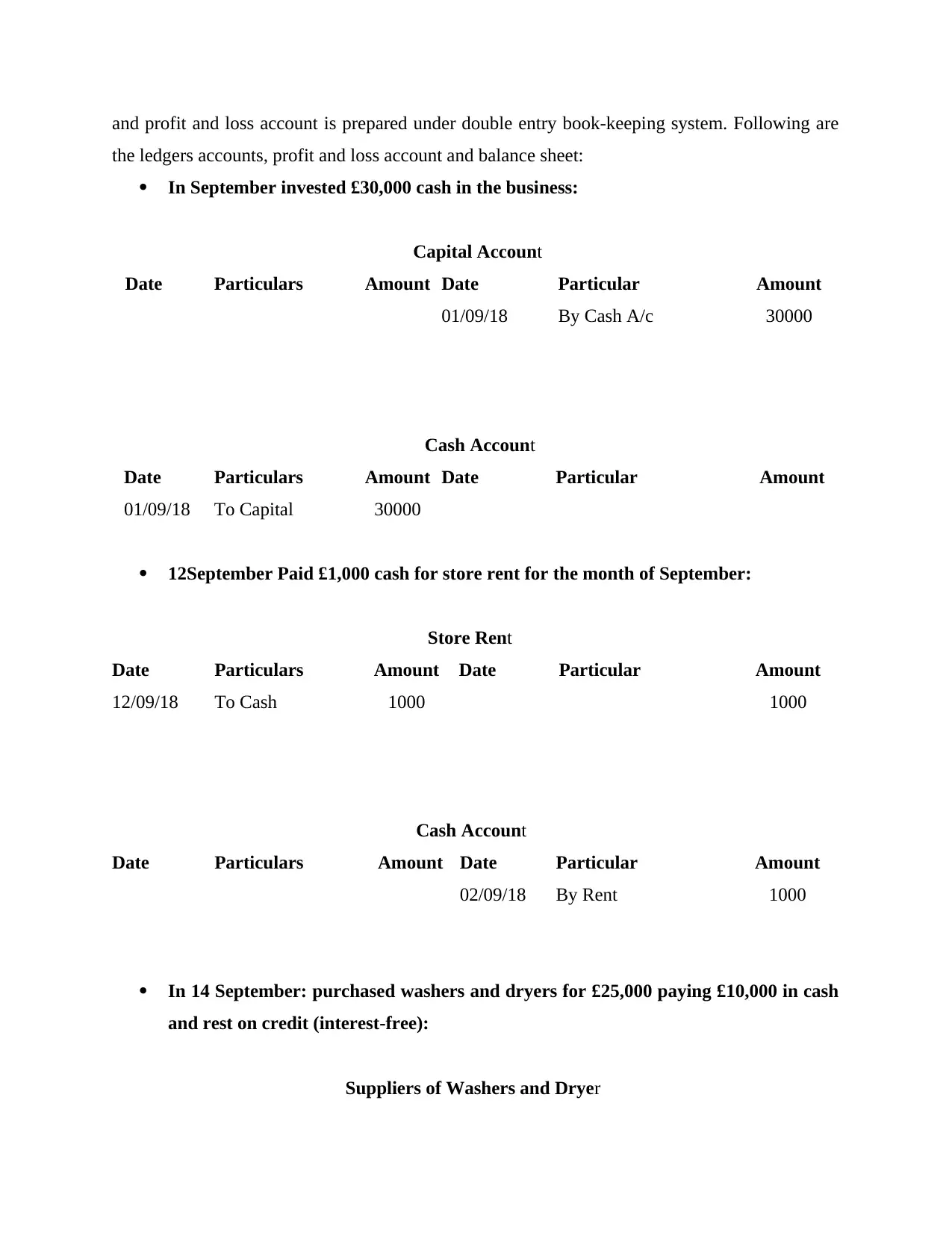

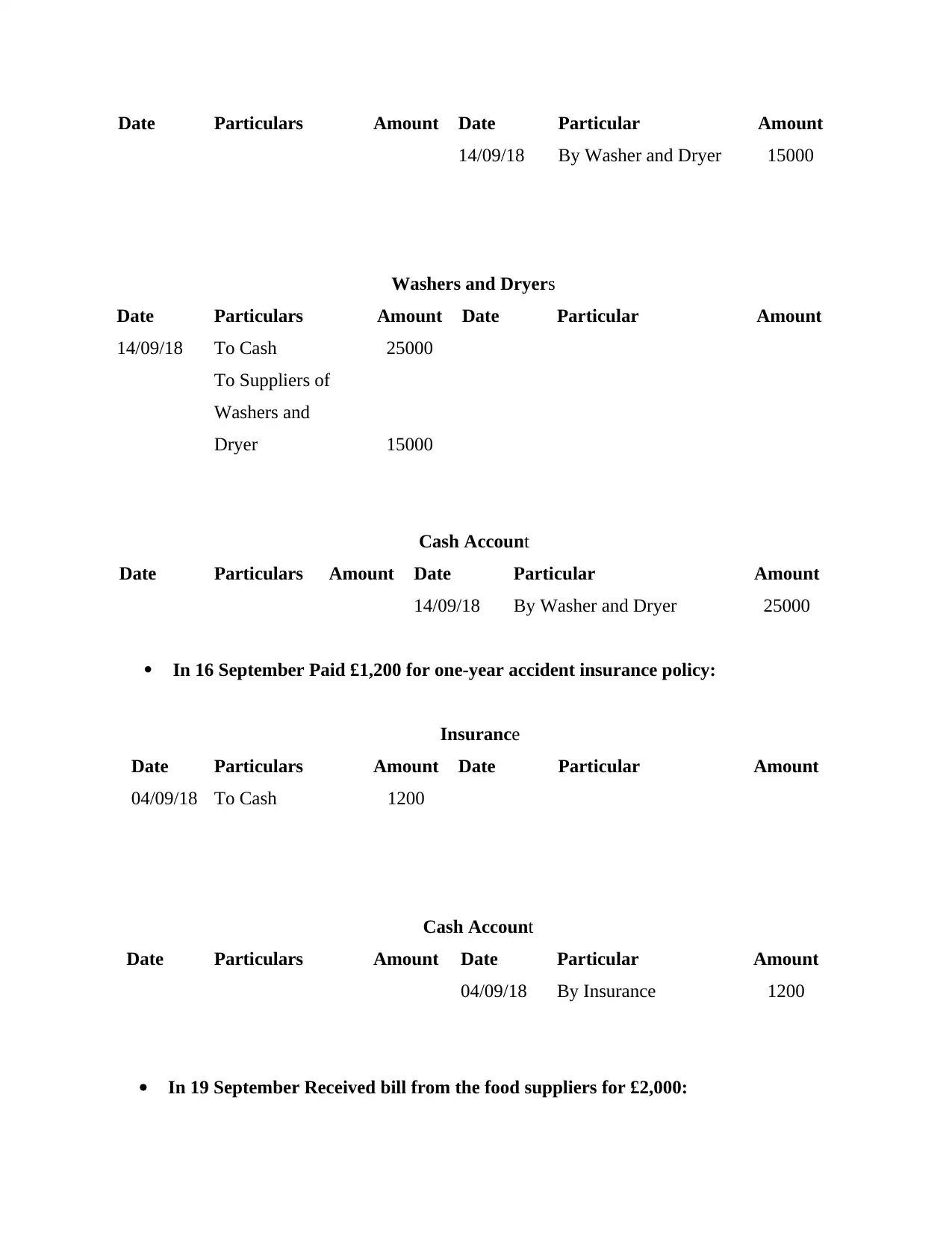

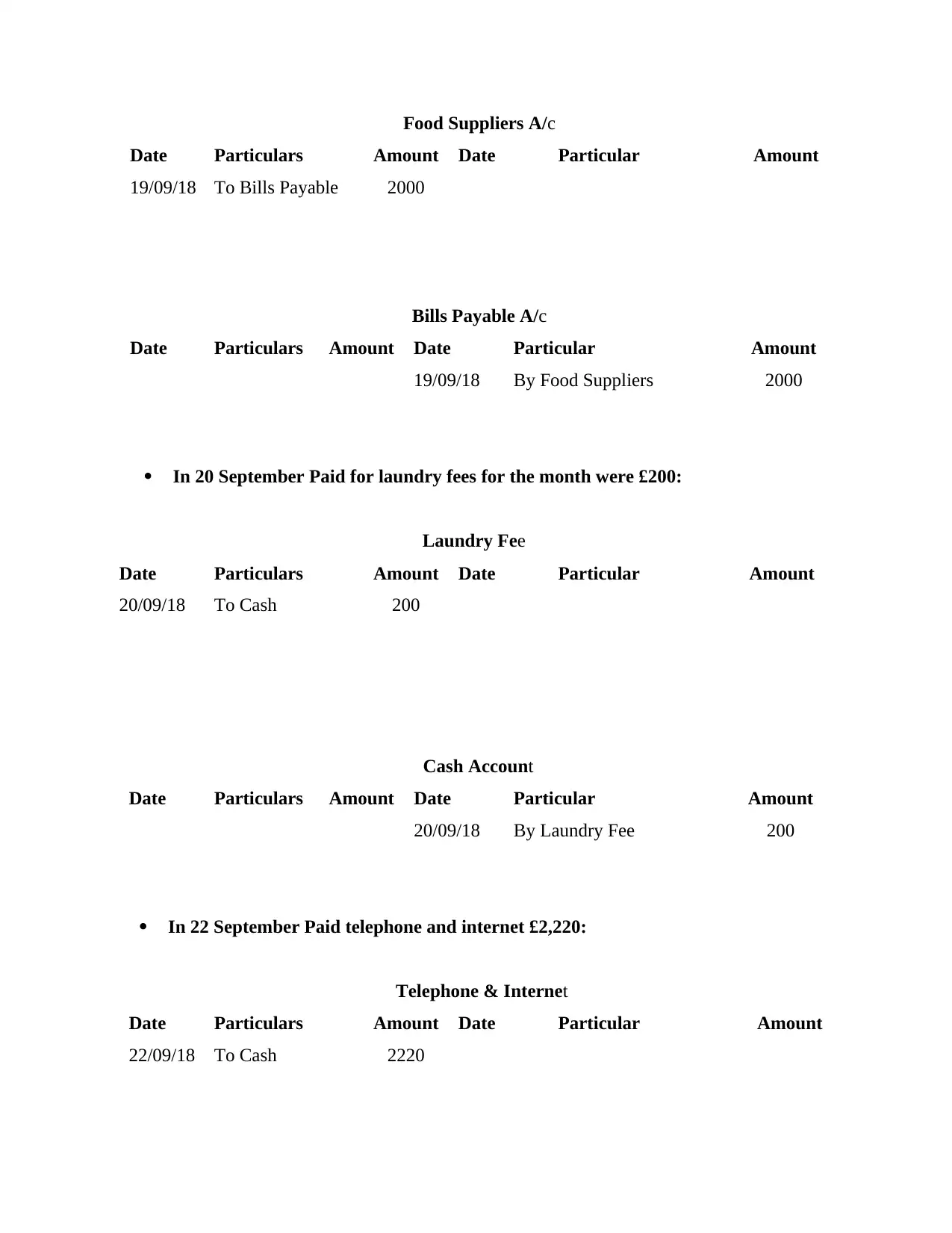

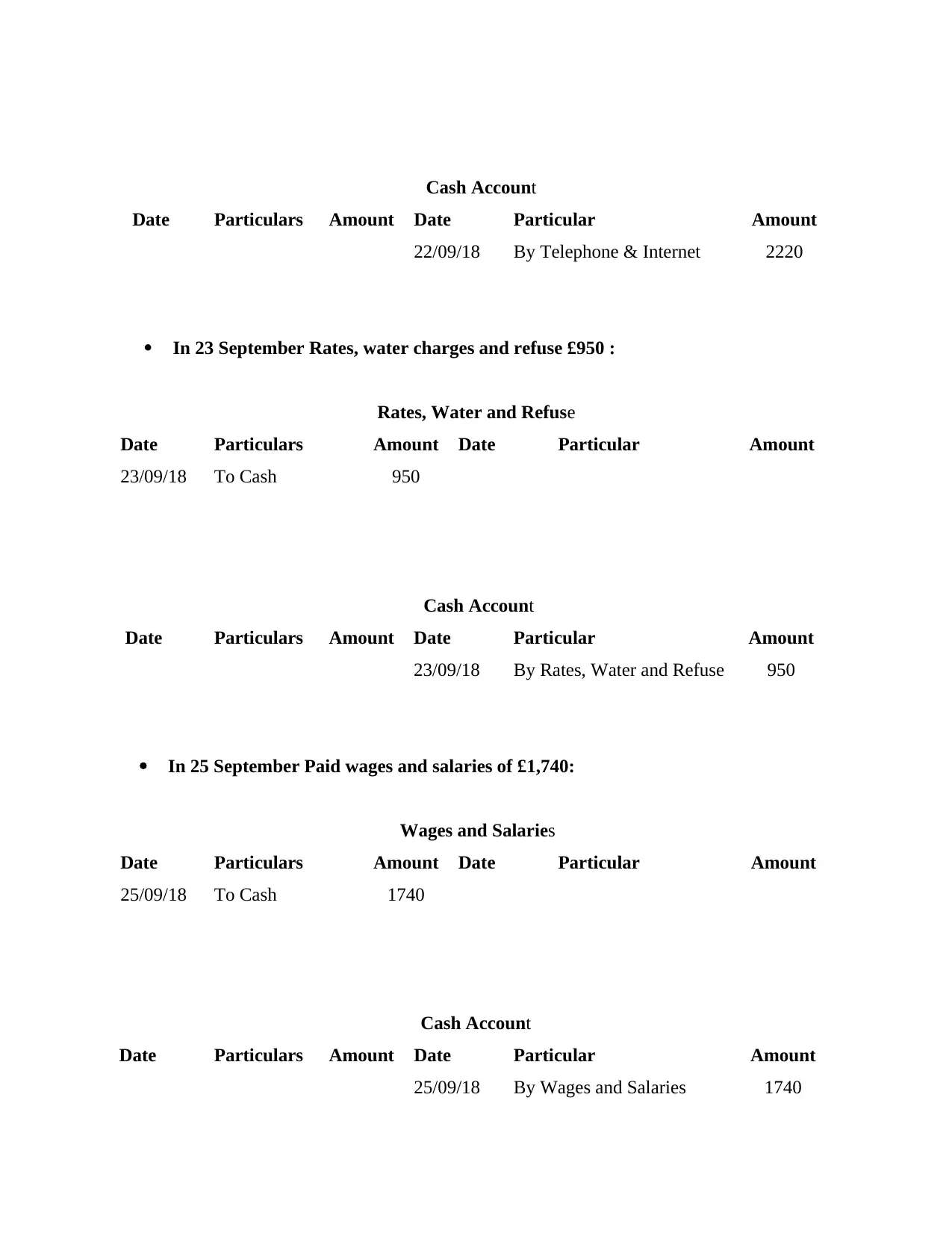

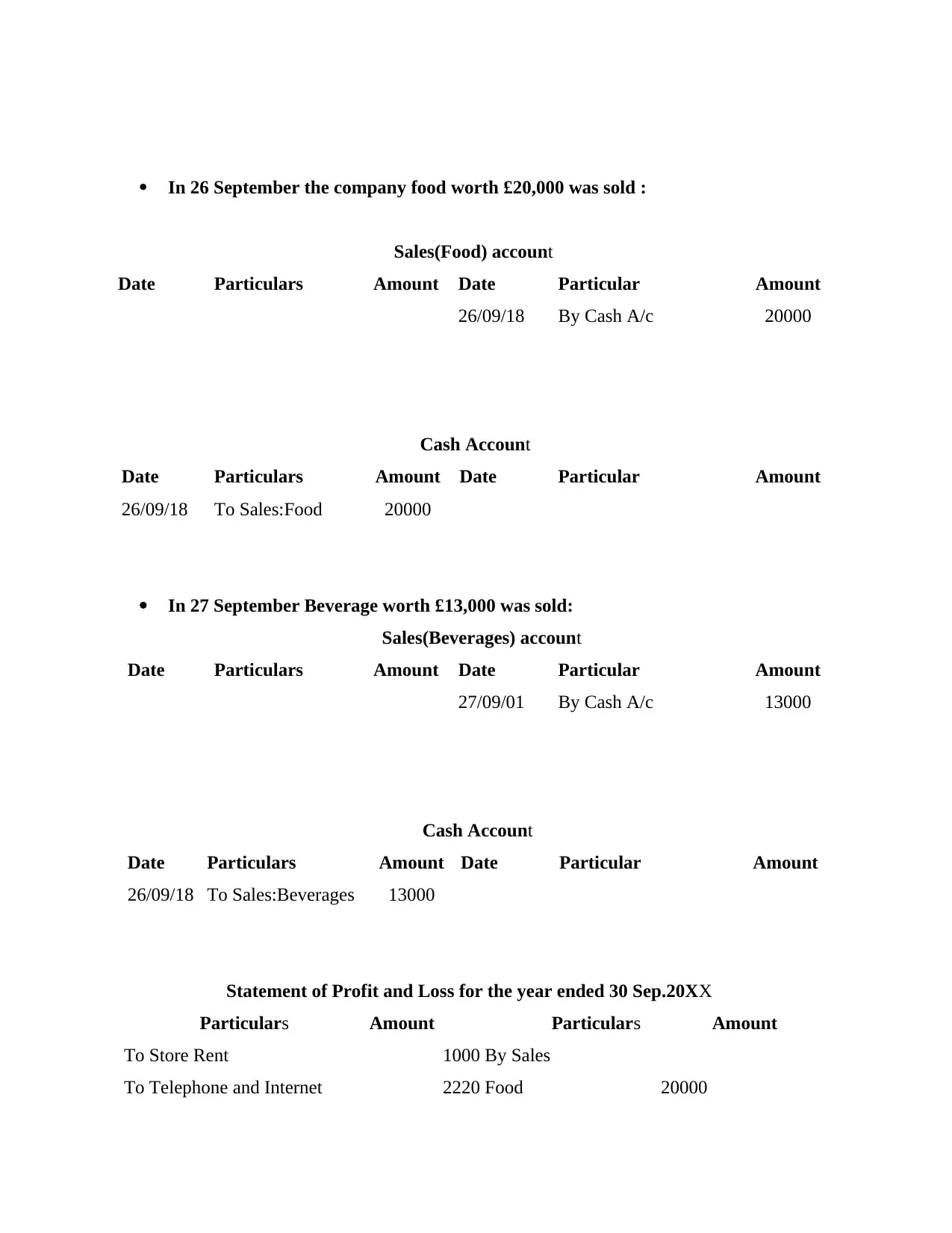

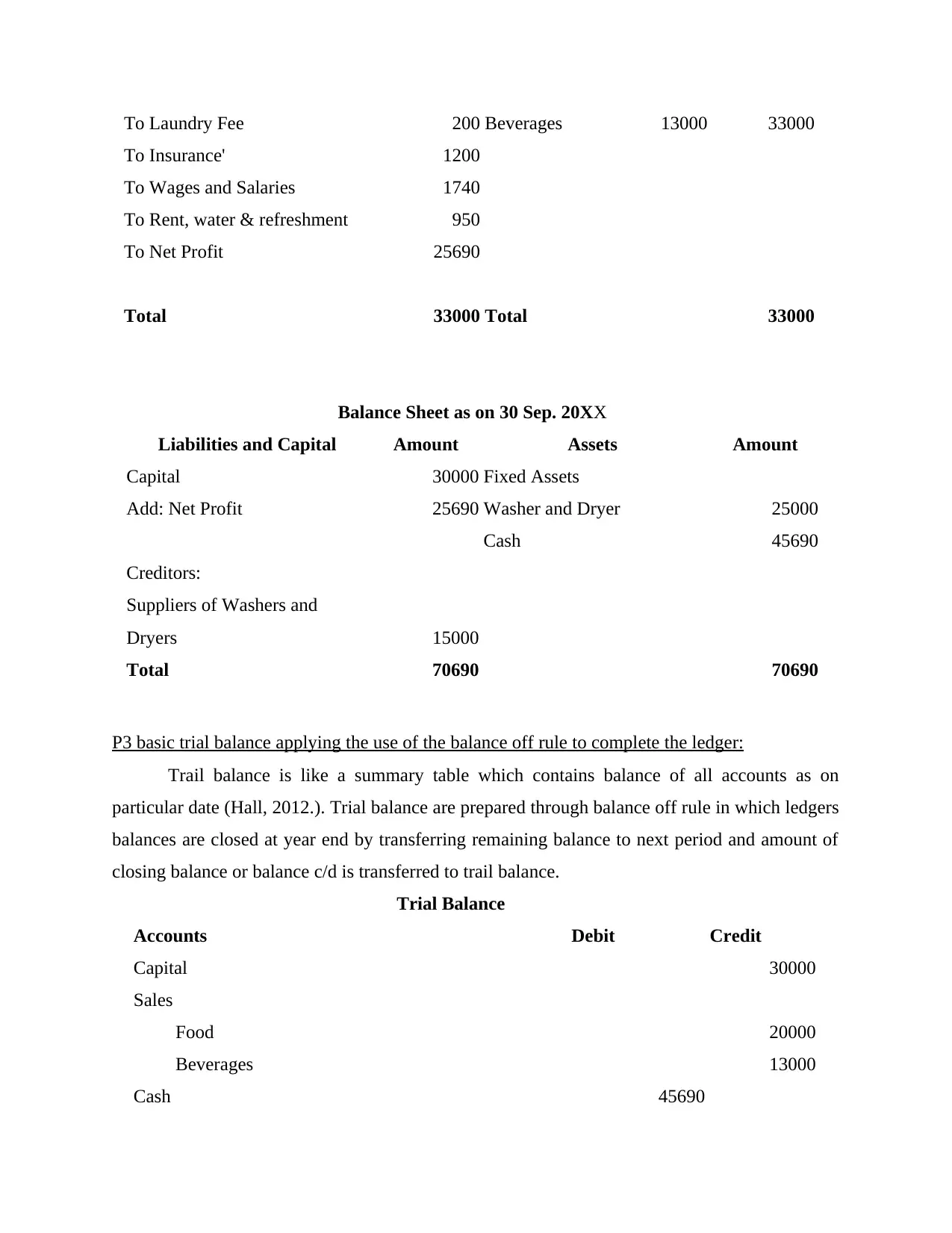

This accounting project delves into the principles of managing and monitoring financial performance, emphasizing the preparation of key financial statements, analysis of overheads, inventory records, and competitive analysis. The project extensively covers the double-entry bookkeeping system, detailing the recording of sales and purchase transactions in a general ledger, providing illustrative examples of journal entries for various financial activities, including investments, rent payments, purchases, insurance, and sales. The project also demonstrates the preparation of a statement of profit and loss and a balance sheet, culminating in the creation of a basic trial balance using the balance off rule. The assignment includes a comprehensive understanding of accounting principles and practical application through detailed ledger entries, financial statements, and the trial balance, offering a complete overview of financial accounting processes.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.