Financial Report: Capital Budgeting, Ratio Analysis, and CVP

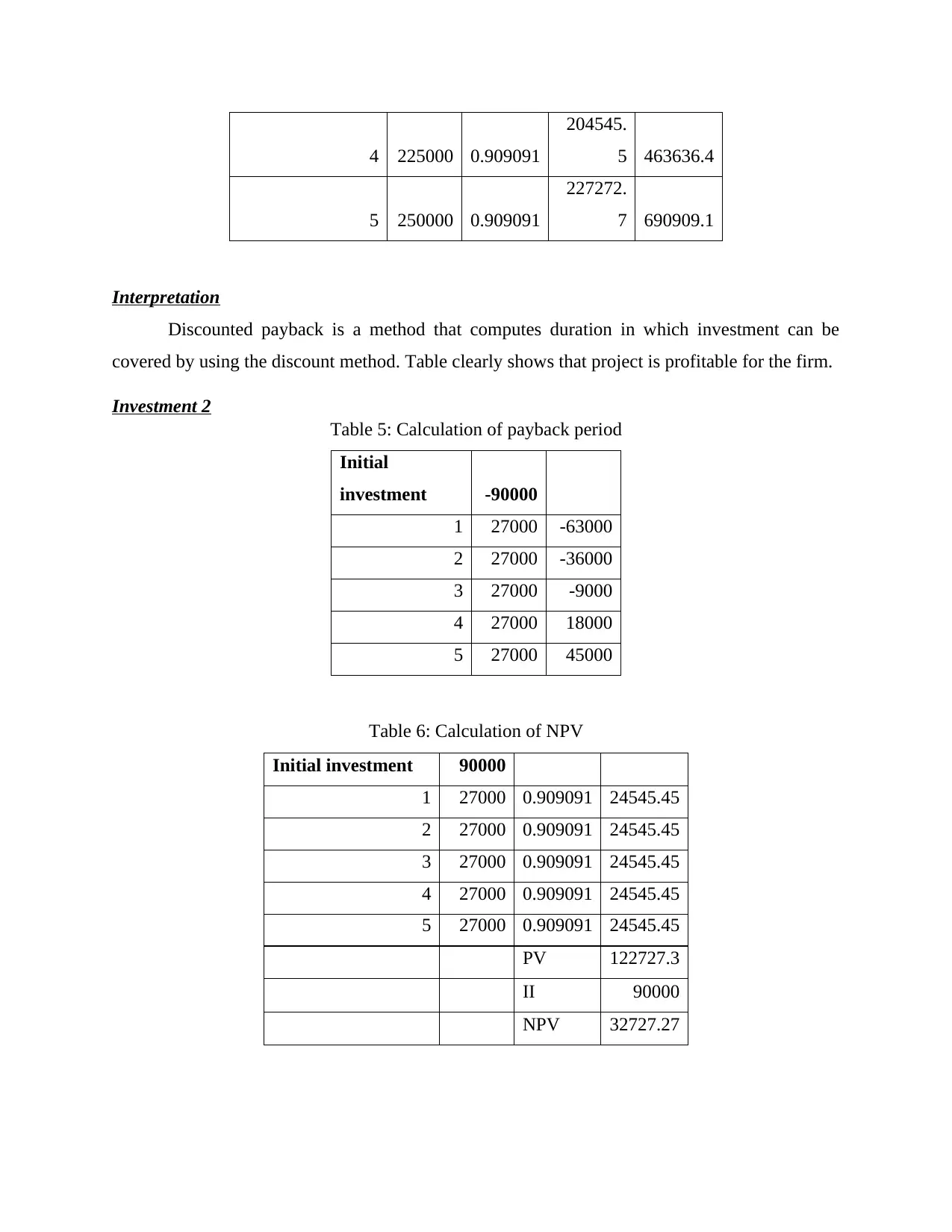

VerifiedAdded on 2020/02/03

|14

|2792

|36

Report

AI Summary

This finance report provides a comprehensive analysis of capital budgeting techniques, including payback period, NPV, IRR, and discounted payback. It evaluates three investment projects, assessing their profitability and risks. The report also examines financial ratio analysis of Morrison PLC, interpreting ratios like gross profit, net profit, current ratio, asset turnover, and debt-equity ratio, and discusses the information needs of stakeholders. Additionally, it explores break-even analysis, computing contribution, sales volume, and profit margins for two products, while also evaluating the advantages and disadvantages of their cost profiles. The report concludes with a discussion on the importance of the present value concept and the benefits of contribution and cost-volume-profit analysis.

FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................4

Question 1........................................................................................................................................4

(a) Project evaluation...................................................................................................................4

(b) Project risks and their impact on calculation..........................................................................9

(c) Importance of present value concept......................................................................................9

Question 2......................................................................................................................................10

(a) Ratio analysis.......................................................................................................................10

(b) Information needs of stakeholders.......................................................................................11

(c) Evaluation of use of ratio analysis........................................................................................11

Question 3......................................................................................................................................12

(a) Compute contribution, sales volume and sales value needed for break even......................12

(b) Calculation of profit and margin of safety...........................................................................13

(c) Advantage and disadvantage of cost profile of two products...............................................13

(d) Benefits of contribution analysis and cost volume profit analysis.......................................14

Conclusion.....................................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................4

Question 1........................................................................................................................................4

(a) Project evaluation...................................................................................................................4

(b) Project risks and their impact on calculation..........................................................................9

(c) Importance of present value concept......................................................................................9

Question 2......................................................................................................................................10

(a) Ratio analysis.......................................................................................................................10

(b) Information needs of stakeholders.......................................................................................11

(c) Evaluation of use of ratio analysis........................................................................................11

Question 3......................................................................................................................................12

(a) Compute contribution, sales volume and sales value needed for break even......................12

(b) Calculation of profit and margin of safety...........................................................................13

(c) Advantage and disadvantage of cost profile of two products...............................................13

(d) Benefits of contribution analysis and cost volume profit analysis.......................................14

Conclusion.....................................................................................................................................14

REFERENCES..............................................................................................................................15

LIST OF TABLES

Table 1: Calculation of payback period method............................................................................4

Table 2: Calculation of NPV..........................................................................................................4

Table 3: Calculation of IRR...........................................................................................................5

Table 4: Discounted payback.........................................................................................................5

Table 5: Calculation of payback period.........................................................................................6

Table 6: Calculation of NPV..........................................................................................................6

Table 7: Calculation of IRR...........................................................................................................6

Table 8: Discounted payback period..............................................................................................7

Table 9: Calculation of payback period.........................................................................................7

Table 10: Calculation of NPV........................................................................................................8

Table 11: Calculation of IRR.........................................................................................................8

Table 12: Calculation of discounted payback period.....................................................................8

Table 13: Ratio analysis of Morrison.............................................................................................9

Table 14: Computation of breakeven analysis.............................................................................11

Table 15: Computation of profit and margin of safety.................................................................12

Table 1: Calculation of payback period method............................................................................4

Table 2: Calculation of NPV..........................................................................................................4

Table 3: Calculation of IRR...........................................................................................................5

Table 4: Discounted payback.........................................................................................................5

Table 5: Calculation of payback period.........................................................................................6

Table 6: Calculation of NPV..........................................................................................................6

Table 7: Calculation of IRR...........................................................................................................6

Table 8: Discounted payback period..............................................................................................7

Table 9: Calculation of payback period.........................................................................................7

Table 10: Calculation of NPV........................................................................................................8

Table 11: Calculation of IRR.........................................................................................................8

Table 12: Calculation of discounted payback period.....................................................................8

Table 13: Ratio analysis of Morrison.............................................................................................9

Table 14: Computation of breakeven analysis.............................................................................11

Table 15: Computation of profit and margin of safety.................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

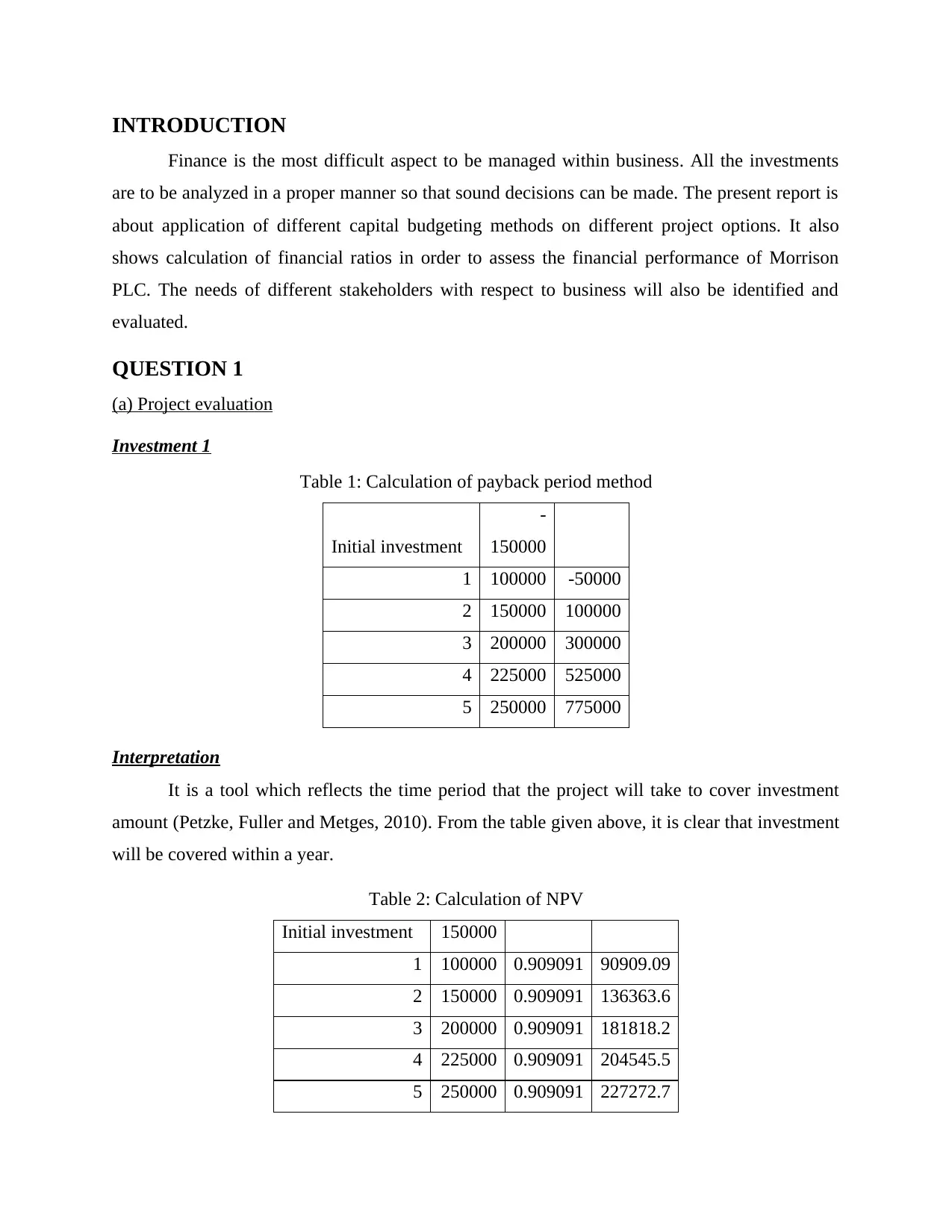

INTRODUCTION

Finance is the most difficult aspect to be managed within business. All the investments

are to be analyzed in a proper manner so that sound decisions can be made. The present report is

about application of different capital budgeting methods on different project options. It also

shows calculation of financial ratios in order to assess the financial performance of Morrison

PLC. The needs of different stakeholders with respect to business will also be identified and

evaluated.

QUESTION 1

(a) Project evaluation

Investment 1

Table 1: Calculation of payback period method

Initial investment

-

150000

1 100000 -50000

2 150000 100000

3 200000 300000

4 225000 525000

5 250000 775000

Interpretation

It is a tool which reflects the time period that the project will take to cover investment

amount (Petzke, Fuller and Metges, 2010). From the table given above, it is clear that investment

will be covered within a year.

Table 2: Calculation of NPV

Initial investment 150000

1 100000 0.909091 90909.09

2 150000 0.909091 136363.6

3 200000 0.909091 181818.2

4 225000 0.909091 204545.5

5 250000 0.909091 227272.7

Finance is the most difficult aspect to be managed within business. All the investments

are to be analyzed in a proper manner so that sound decisions can be made. The present report is

about application of different capital budgeting methods on different project options. It also

shows calculation of financial ratios in order to assess the financial performance of Morrison

PLC. The needs of different stakeholders with respect to business will also be identified and

evaluated.

QUESTION 1

(a) Project evaluation

Investment 1

Table 1: Calculation of payback period method

Initial investment

-

150000

1 100000 -50000

2 150000 100000

3 200000 300000

4 225000 525000

5 250000 775000

Interpretation

It is a tool which reflects the time period that the project will take to cover investment

amount (Petzke, Fuller and Metges, 2010). From the table given above, it is clear that investment

will be covered within a year.

Table 2: Calculation of NPV

Initial investment 150000

1 100000 0.909091 90909.09

2 150000 0.909091 136363.6

3 200000 0.909091 181818.2

4 225000 0.909091 204545.5

5 250000 0.909091 227272.7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

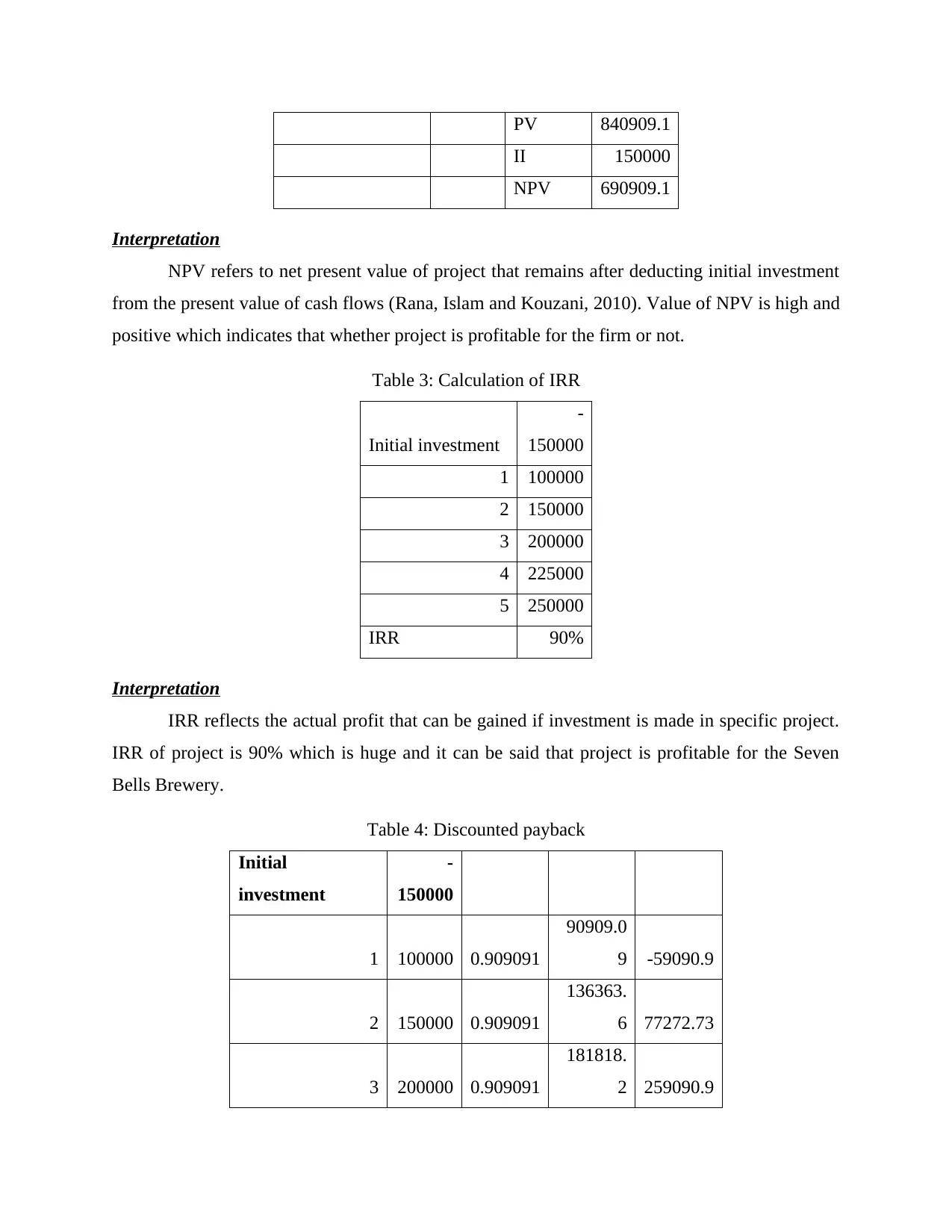

PV 840909.1

II 150000

NPV 690909.1

Interpretation

NPV refers to net present value of project that remains after deducting initial investment

from the present value of cash flows (Rana, Islam and Kouzani, 2010). Value of NPV is high and

positive which indicates that whether project is profitable for the firm or not.

Table 3: Calculation of IRR

Initial investment

-

150000

1 100000

2 150000

3 200000

4 225000

5 250000

IRR 90%

Interpretation

IRR reflects the actual profit that can be gained if investment is made in specific project.

IRR of project is 90% which is huge and it can be said that project is profitable for the Seven

Bells Brewery.

Table 4: Discounted payback

Initial

investment

-

150000

1 100000 0.909091

90909.0

9 -59090.9

2 150000 0.909091

136363.

6 77272.73

3 200000 0.909091

181818.

2 259090.9

II 150000

NPV 690909.1

Interpretation

NPV refers to net present value of project that remains after deducting initial investment

from the present value of cash flows (Rana, Islam and Kouzani, 2010). Value of NPV is high and

positive which indicates that whether project is profitable for the firm or not.

Table 3: Calculation of IRR

Initial investment

-

150000

1 100000

2 150000

3 200000

4 225000

5 250000

IRR 90%

Interpretation

IRR reflects the actual profit that can be gained if investment is made in specific project.

IRR of project is 90% which is huge and it can be said that project is profitable for the Seven

Bells Brewery.

Table 4: Discounted payback

Initial

investment

-

150000

1 100000 0.909091

90909.0

9 -59090.9

2 150000 0.909091

136363.

6 77272.73

3 200000 0.909091

181818.

2 259090.9

4 225000 0.909091

204545.

5 463636.4

5 250000 0.909091

227272.

7 690909.1

Interpretation

Discounted payback is a method that computes duration in which investment can be

covered by using the discount method. Table clearly shows that project is profitable for the firm.

Investment 2

Table 5: Calculation of payback period

Initial

investment -90000

1 27000 -63000

2 27000 -36000

3 27000 -9000

4 27000 18000

5 27000 45000

Table 6: Calculation of NPV

Initial investment 90000

1 27000 0.909091 24545.45

2 27000 0.909091 24545.45

3 27000 0.909091 24545.45

4 27000 0.909091 24545.45

5 27000 0.909091 24545.45

PV 122727.3

II 90000

NPV 32727.27

204545.

5 463636.4

5 250000 0.909091

227272.

7 690909.1

Interpretation

Discounted payback is a method that computes duration in which investment can be

covered by using the discount method. Table clearly shows that project is profitable for the firm.

Investment 2

Table 5: Calculation of payback period

Initial

investment -90000

1 27000 -63000

2 27000 -36000

3 27000 -9000

4 27000 18000

5 27000 45000

Table 6: Calculation of NPV

Initial investment 90000

1 27000 0.909091 24545.45

2 27000 0.909091 24545.45

3 27000 0.909091 24545.45

4 27000 0.909091 24545.45

5 27000 0.909091 24545.45

PV 122727.3

II 90000

NPV 32727.27

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

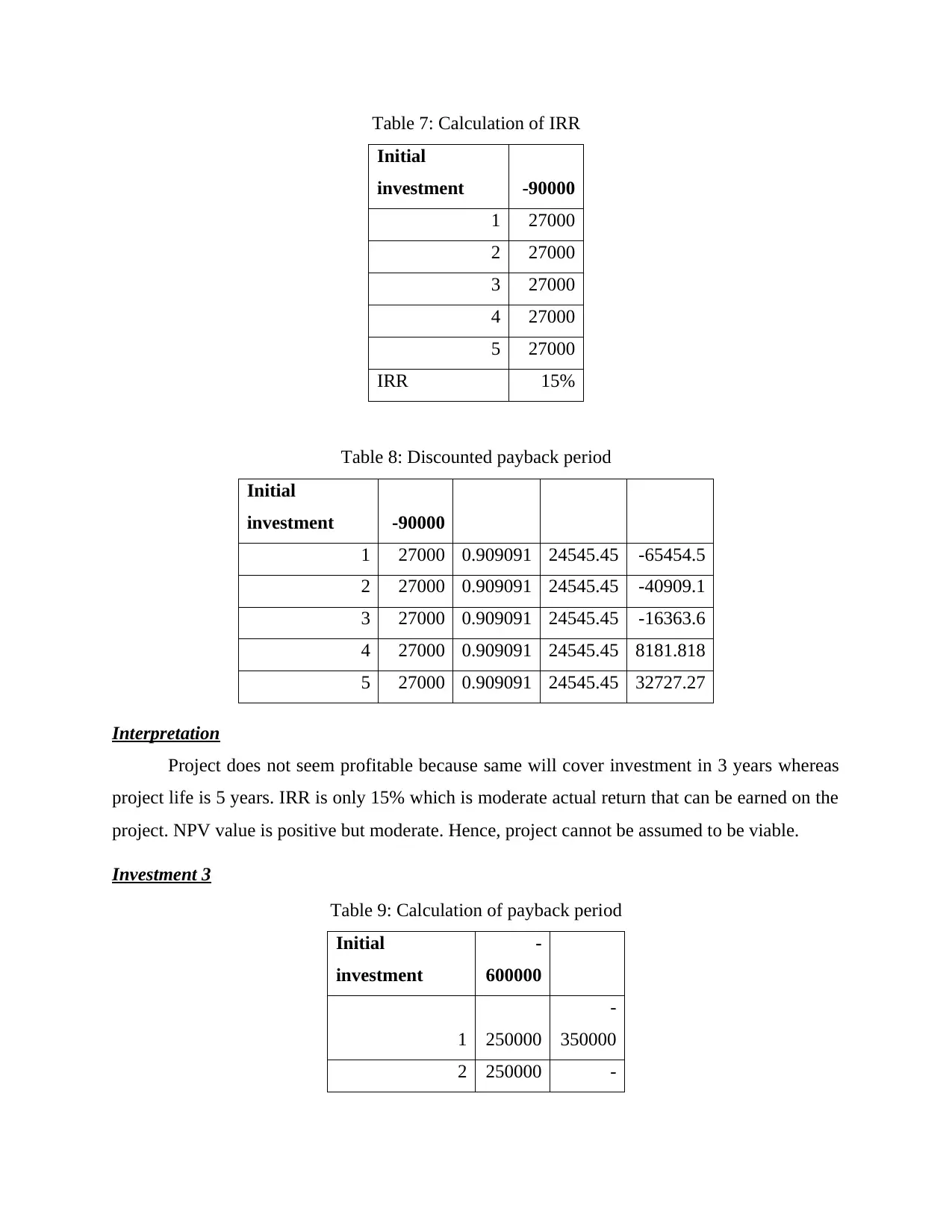

Table 7: Calculation of IRR

Initial

investment -90000

1 27000

2 27000

3 27000

4 27000

5 27000

IRR 15%

Table 8: Discounted payback period

Initial

investment -90000

1 27000 0.909091 24545.45 -65454.5

2 27000 0.909091 24545.45 -40909.1

3 27000 0.909091 24545.45 -16363.6

4 27000 0.909091 24545.45 8181.818

5 27000 0.909091 24545.45 32727.27

Interpretation

Project does not seem profitable because same will cover investment in 3 years whereas

project life is 5 years. IRR is only 15% which is moderate actual return that can be earned on the

project. NPV value is positive but moderate. Hence, project cannot be assumed to be viable.

Investment 3

Table 9: Calculation of payback period

Initial

investment

-

600000

1 250000

-

350000

2 250000 -

Initial

investment -90000

1 27000

2 27000

3 27000

4 27000

5 27000

IRR 15%

Table 8: Discounted payback period

Initial

investment -90000

1 27000 0.909091 24545.45 -65454.5

2 27000 0.909091 24545.45 -40909.1

3 27000 0.909091 24545.45 -16363.6

4 27000 0.909091 24545.45 8181.818

5 27000 0.909091 24545.45 32727.27

Interpretation

Project does not seem profitable because same will cover investment in 3 years whereas

project life is 5 years. IRR is only 15% which is moderate actual return that can be earned on the

project. NPV value is positive but moderate. Hence, project cannot be assumed to be viable.

Investment 3

Table 9: Calculation of payback period

Initial

investment

-

600000

1 250000

-

350000

2 250000 -

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

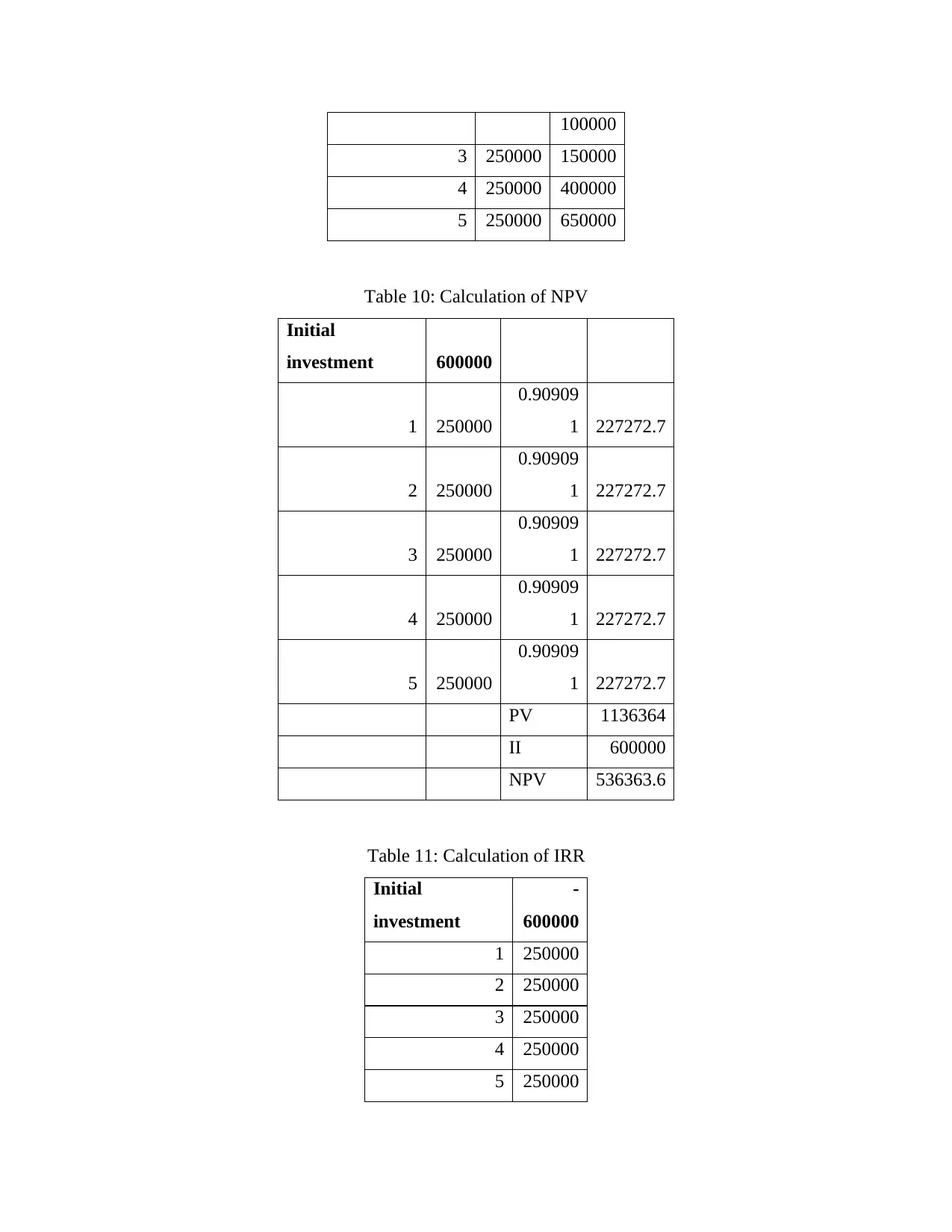

100000

3 250000 150000

4 250000 400000

5 250000 650000

Table 10: Calculation of NPV

Initial

investment 600000

1 250000

0.90909

1 227272.7

2 250000

0.90909

1 227272.7

3 250000

0.90909

1 227272.7

4 250000

0.90909

1 227272.7

5 250000

0.90909

1 227272.7

PV 1136364

II 600000

NPV 536363.6

Table 11: Calculation of IRR

Initial

investment

-

600000

1 250000

2 250000

3 250000

4 250000

5 250000

3 250000 150000

4 250000 400000

5 250000 650000

Table 10: Calculation of NPV

Initial

investment 600000

1 250000

0.90909

1 227272.7

2 250000

0.90909

1 227272.7

3 250000

0.90909

1 227272.7

4 250000

0.90909

1 227272.7

5 250000

0.90909

1 227272.7

PV 1136364

II 600000

NPV 536363.6

Table 11: Calculation of IRR

Initial

investment

-

600000

1 250000

2 250000

3 250000

4 250000

5 250000

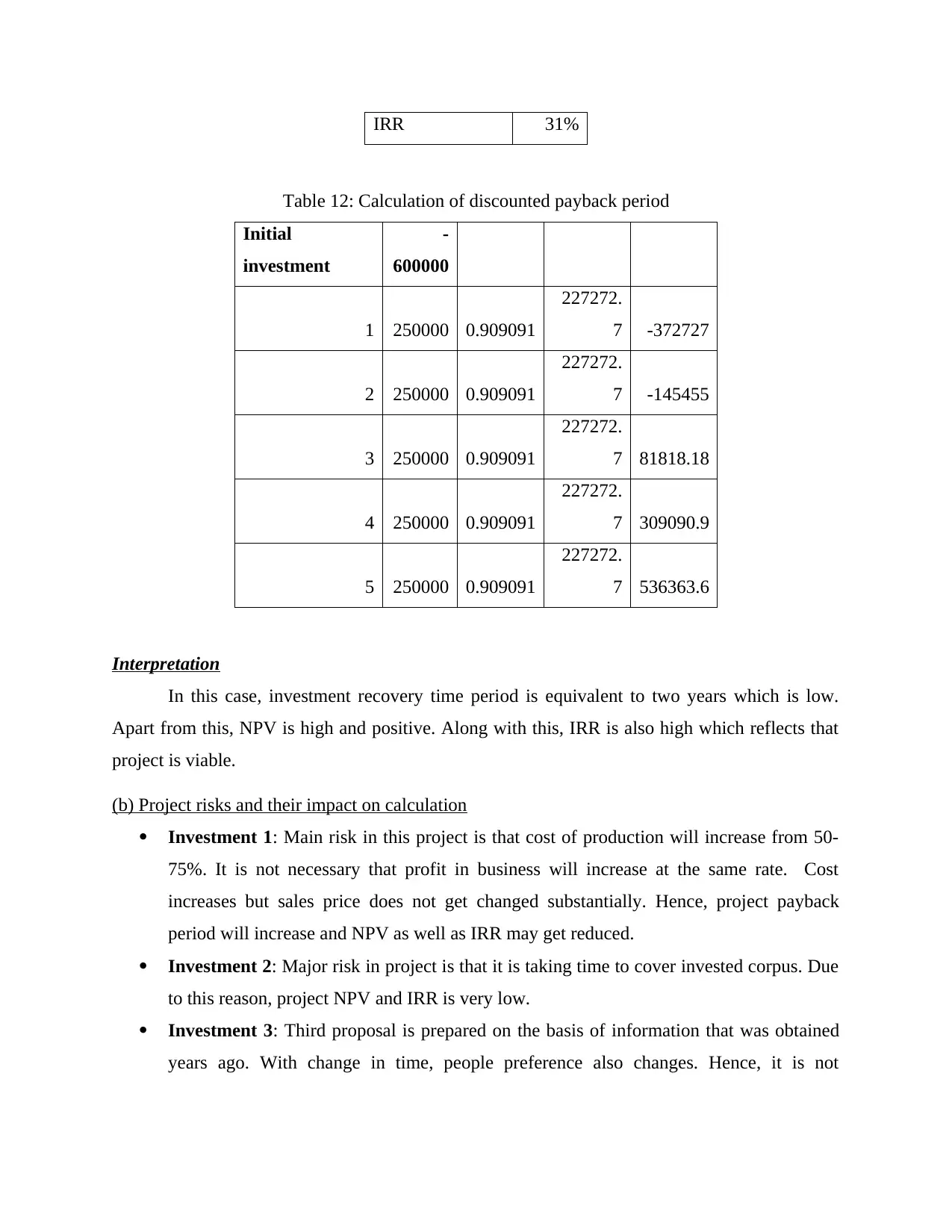

IRR 31%

Table 12: Calculation of discounted payback period

Initial

investment

-

600000

1 250000 0.909091

227272.

7 -372727

2 250000 0.909091

227272.

7 -145455

3 250000 0.909091

227272.

7 81818.18

4 250000 0.909091

227272.

7 309090.9

5 250000 0.909091

227272.

7 536363.6

Interpretation

In this case, investment recovery time period is equivalent to two years which is low.

Apart from this, NPV is high and positive. Along with this, IRR is also high which reflects that

project is viable.

(b) Project risks and their impact on calculation

Investment 1: Main risk in this project is that cost of production will increase from 50-

75%. It is not necessary that profit in business will increase at the same rate. Cost

increases but sales price does not get changed substantially. Hence, project payback

period will increase and NPV as well as IRR may get reduced.

Investment 2: Major risk in project is that it is taking time to cover invested corpus. Due

to this reason, project NPV and IRR is very low.

Investment 3: Third proposal is prepared on the basis of information that was obtained

years ago. With change in time, people preference also changes. Hence, it is not

Table 12: Calculation of discounted payback period

Initial

investment

-

600000

1 250000 0.909091

227272.

7 -372727

2 250000 0.909091

227272.

7 -145455

3 250000 0.909091

227272.

7 81818.18

4 250000 0.909091

227272.

7 309090.9

5 250000 0.909091

227272.

7 536363.6

Interpretation

In this case, investment recovery time period is equivalent to two years which is low.

Apart from this, NPV is high and positive. Along with this, IRR is also high which reflects that

project is viable.

(b) Project risks and their impact on calculation

Investment 1: Main risk in this project is that cost of production will increase from 50-

75%. It is not necessary that profit in business will increase at the same rate. Cost

increases but sales price does not get changed substantially. Hence, project payback

period will increase and NPV as well as IRR may get reduced.

Investment 2: Major risk in project is that it is taking time to cover invested corpus. Due

to this reason, project NPV and IRR is very low.

Investment 3: Third proposal is prepared on the basis of information that was obtained

years ago. With change in time, people preference also changes. Hence, it is not

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

necessary that estimated cash flow will really happen in the business. If estimations are

made wrong, the project evaluation methods will produce negative results.

(c) Importance of present value concept

Present value concept helps individuals in doing valuation of the project by making use

of estimated cash flow for current time period (Morris and Pinto, 2010). Value of money is high

in current time period then in the upcoming years. Hence, it becomes very important to do

valuation of project for current time period.

QUESTION 2

(a)Ratio analysis

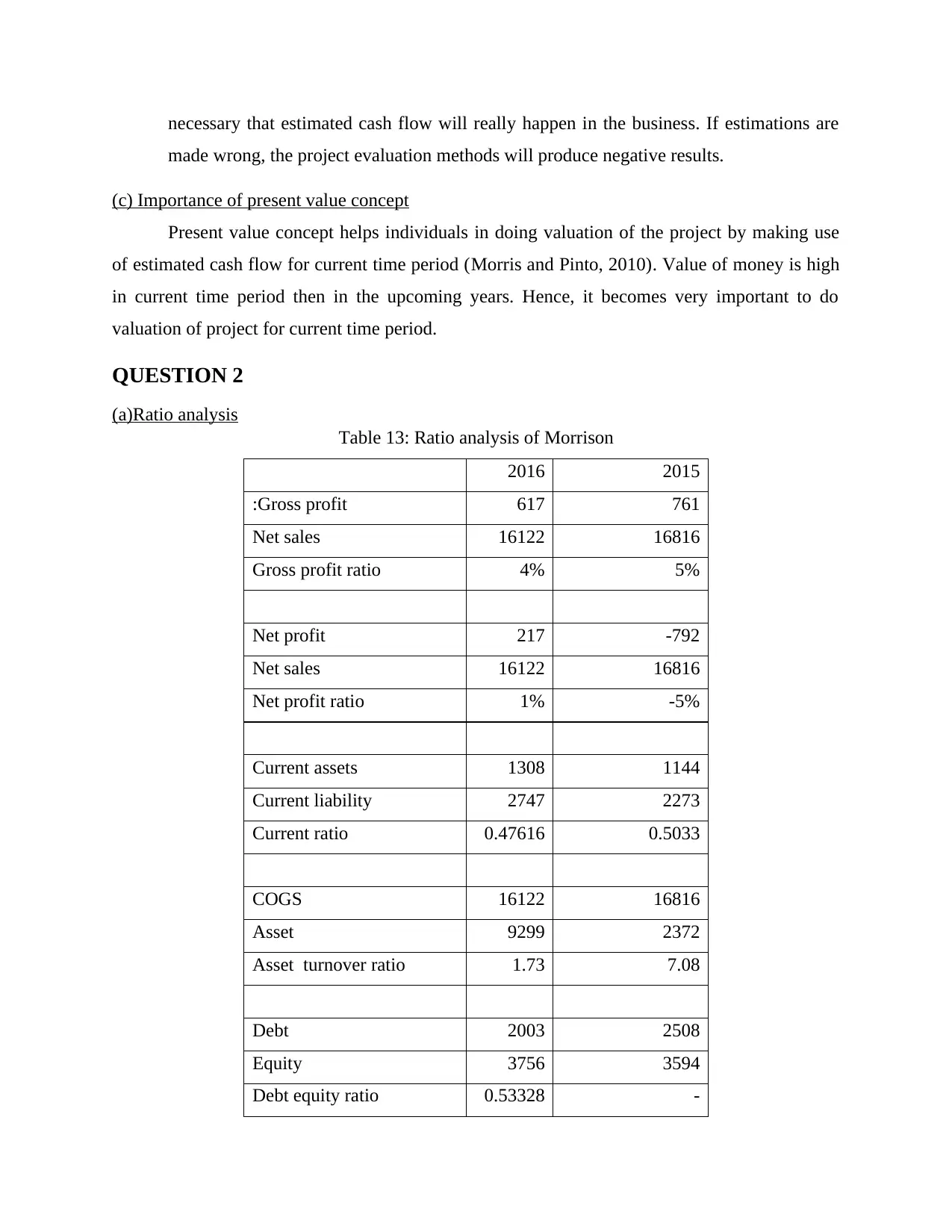

Table 13: Ratio analysis of Morrison

2016 2015

:Gross profit 617 761

Net sales 16122 16816

Gross profit ratio 4% 5%

Net profit 217 -792

Net sales 16122 16816

Net profit ratio 1% -5%

Current assets 1308 1144

Current liability 2747 2273

Current ratio 0.47616 0.5033

COGS 16122 16816

Asset 9299 2372

Asset turnover ratio 1.73 7.08

Debt 2003 2508

Equity 3756 3594

Debt equity ratio 0.53328 -

made wrong, the project evaluation methods will produce negative results.

(c) Importance of present value concept

Present value concept helps individuals in doing valuation of the project by making use

of estimated cash flow for current time period (Morris and Pinto, 2010). Value of money is high

in current time period then in the upcoming years. Hence, it becomes very important to do

valuation of project for current time period.

QUESTION 2

(a)Ratio analysis

Table 13: Ratio analysis of Morrison

2016 2015

:Gross profit 617 761

Net sales 16122 16816

Gross profit ratio 4% 5%

Net profit 217 -792

Net sales 16122 16816

Net profit ratio 1% -5%

Current assets 1308 1144

Current liability 2747 2273

Current ratio 0.47616 0.5033

COGS 16122 16816

Asset 9299 2372

Asset turnover ratio 1.73 7.08

Debt 2003 2508

Equity 3756 3594

Debt equity ratio 0.53328 -

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

0.69783

Interpretation

Gross profit of the firm declines because sales of Morrison get reduced in FY 2016

relative to FY 2015. Lack of control on expenses is another reason for such a poor performance

that is observed in the business (Sinha and Labi, 2011). Despite of the fact that decline is

observed in sales net profit, ratio of firm got improved and this happened because firm

effectively implemented its indirect cost control strategy at the workplace. Liquidity condition of

business is very poor and value of ratio is below 1:1 which reflects that firm is not able to pay its

current liabilities on time by using current assets (Current ratio, 2016). Availability of current

assets for every single pound of liability is reduced from 0.50£ to 0.47£. Firm failed to make

effective use of its assets as reflected by decline in asset turnover ratio. Value of ratio declined

from 7.08 to 1.73. Debt equity ratio reduced from 0.69 to 0.53 which is good for business

because it reflects that proportion of debt is relative to equity which is reduced in capital

structure.

(b) Information needs of stakeholders

Shareholders: They needed financial statements of the firm in order to evaluate

company’s profitability, fundamentals and liquidity position. On the basis of results

depicted by financial statements, shareholders decide that whether they must keep

investment in the firm or should exit from the same.

Managers: They require income statement, balance sheet and cash flow statement in

order to identify weak points of the firm (Lenfle, 2012). Managers form a business

strategy and by using the same, they convert weak points into strong one.

Lenders: Lenders needed balance sheet and income statement as by using the same, they

do ratio analysis and measure firm’s payment making capability. On the basis of results

of ratio, they make lending related business decisions.

(c) Evaluation of the use of ratio analysis

Ratio analysis is the one of the most important tools that is used to evaluate business

performance. By using ratio analysis method, business performance is evaluated from different

sides. However, this method is not error free and have some limitations. For example, in case of

Interpretation

Gross profit of the firm declines because sales of Morrison get reduced in FY 2016

relative to FY 2015. Lack of control on expenses is another reason for such a poor performance

that is observed in the business (Sinha and Labi, 2011). Despite of the fact that decline is

observed in sales net profit, ratio of firm got improved and this happened because firm

effectively implemented its indirect cost control strategy at the workplace. Liquidity condition of

business is very poor and value of ratio is below 1:1 which reflects that firm is not able to pay its

current liabilities on time by using current assets (Current ratio, 2016). Availability of current

assets for every single pound of liability is reduced from 0.50£ to 0.47£. Firm failed to make

effective use of its assets as reflected by decline in asset turnover ratio. Value of ratio declined

from 7.08 to 1.73. Debt equity ratio reduced from 0.69 to 0.53 which is good for business

because it reflects that proportion of debt is relative to equity which is reduced in capital

structure.

(b) Information needs of stakeholders

Shareholders: They needed financial statements of the firm in order to evaluate

company’s profitability, fundamentals and liquidity position. On the basis of results

depicted by financial statements, shareholders decide that whether they must keep

investment in the firm or should exit from the same.

Managers: They require income statement, balance sheet and cash flow statement in

order to identify weak points of the firm (Lenfle, 2012). Managers form a business

strategy and by using the same, they convert weak points into strong one.

Lenders: Lenders needed balance sheet and income statement as by using the same, they

do ratio analysis and measure firm’s payment making capability. On the basis of results

of ratio, they make lending related business decisions.

(c) Evaluation of the use of ratio analysis

Ratio analysis is the one of the most important tools that is used to evaluate business

performance. By using ratio analysis method, business performance is evaluated from different

sides. However, this method is not error free and have some limitations. For example, in case of

current ratio, parameter is determined which is 2:1 which means that for every one pound of

current liability, there must be two pounds of current assets (Keller, Parameswaran and Jacob,

2011). If business conditions are not good then it is not possible to maintain standard value

which is 2:1. Managers always make use of 2:1 in order to evaluate liquidity in business without

considering the current market conditions. Hence, to some extent, they evaluate the performance

of business in a wrong way. This is one of the major shortcoming of ratio analysis.

QUESTION 3

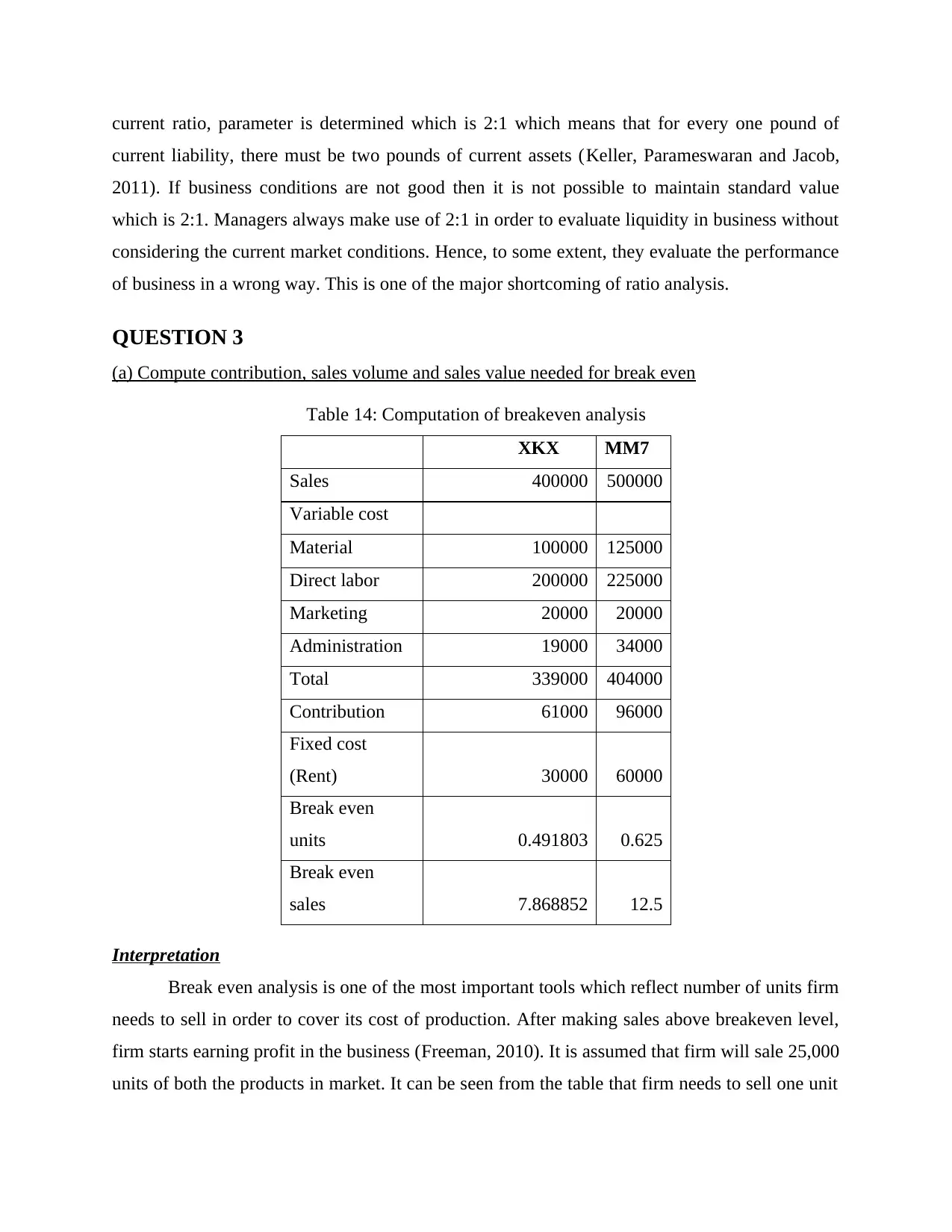

(a) Compute contribution, sales volume and sales value needed for break even

Table 14: Computation of breakeven analysis

XKX MM7

Sales 400000 500000

Variable cost

Material 100000 125000

Direct labor 200000 225000

Marketing 20000 20000

Administration 19000 34000

Total 339000 404000

Contribution 61000 96000

Fixed cost

(Rent) 30000 60000

Break even

units 0.491803 0.625

Break even

sales 7.868852 12.5

Interpretation

Break even analysis is one of the most important tools which reflect number of units firm

needs to sell in order to cover its cost of production. After making sales above breakeven level,

firm starts earning profit in the business (Freeman, 2010). It is assumed that firm will sale 25,000

units of both the products in market. It can be seen from the table that firm needs to sell one unit

current liability, there must be two pounds of current assets (Keller, Parameswaran and Jacob,

2011). If business conditions are not good then it is not possible to maintain standard value

which is 2:1. Managers always make use of 2:1 in order to evaluate liquidity in business without

considering the current market conditions. Hence, to some extent, they evaluate the performance

of business in a wrong way. This is one of the major shortcoming of ratio analysis.

QUESTION 3

(a) Compute contribution, sales volume and sales value needed for break even

Table 14: Computation of breakeven analysis

XKX MM7

Sales 400000 500000

Variable cost

Material 100000 125000

Direct labor 200000 225000

Marketing 20000 20000

Administration 19000 34000

Total 339000 404000

Contribution 61000 96000

Fixed cost

(Rent) 30000 60000

Break even

units 0.491803 0.625

Break even

sales 7.868852 12.5

Interpretation

Break even analysis is one of the most important tools which reflect number of units firm

needs to sell in order to cover its cost of production. After making sales above breakeven level,

firm starts earning profit in the business (Freeman, 2010). It is assumed that firm will sale 25,000

units of both the products in market. It can be seen from the table that firm needs to sell one unit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.