Financial Management Practices and Financial Performance: A Report

VerifiedAdded on 2021/09/20

|17

|3127

|38

Report

AI Summary

This report investigates the effect of financial management practices on the financial performance of non-financial firms listed on the National Securities Exchange (NSE). The study explores the influence of liquidity management, capital budgeting, and leverage on financial outcomes, considering the moderating role of inflation. The research employs a positivist paradigm, utilizing a fixed effects model and panel secondary data from financial statements spanning five years (2010-2014). Key variables include Return on Assets (ROA) as a measure of financial performance, and Liquidity Management, Capital Budgeting, and Leverage as independent variables representing financial management practices. The methodology encompasses data collection from the NSE and the bureau of statistics, followed by data analysis and diagnostic tests. The report aims to address research gaps by examining financial management practices comprehensively, including the moderating effect of inflation, providing a detailed analysis of their impact on firm performance, and offering valuable insights into the financial dynamics of non-financial sector firms.

Running head: FINANCIAL MANAGEMENT PRACTICES 1

Topic: Financial Management Practices

[Name of Student]

[Institutional Affiliation]

[Instructor’s Name]

[Date of Submission]

Topic: Financial Management Practices

[Name of Student]

[Institutional Affiliation]

[Instructor’s Name]

[Date of Submission]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL MANAGEMENT PRACTICES 2

Contents

Introduction......................................................................................................................................2

Financial Management practices in public sector........................................................................2

Research Questions and Hypotheses...............................................................................................3

Research Hypotheses...................................................................................................................4

Literature Review............................................................................................................................4

Methodology....................................................................................................................................6

Data Collection................................................................................................................................6

Timescale.........................................................................................................................................6

References........................................................................................................................................6

Contents

Introduction......................................................................................................................................2

Financial Management practices in public sector........................................................................2

Research Questions and Hypotheses...............................................................................................3

Research Hypotheses...................................................................................................................4

Literature Review............................................................................................................................4

Methodology....................................................................................................................................6

Data Collection................................................................................................................................6

Timescale.........................................................................................................................................6

References........................................................................................................................................6

FINANCIAL MANAGEMENT PRACTICES 3

Introduction

Financial management is one of management functional areas which is core to success of

business enterprises. Inefficient financial management, combined with the uncertainty of the

business environment often led Business Enterprises to serious problems (Deresse & Prabhakara,

2012). Paramasivan and Subramanian (2009) argued that financial management helps to improve

the profitability position of business organizations with the help of strong financial control

devices such as budgetary control and ratio analysis.

As the financial sector at The National Securities’ Exchange, which include banking,

investments and insurance firms, continues to record growth, some firms in the nonfinancial

sector have been characterized by a decline in performance and as a result market prices of their

shares at the National Securities Exchange has recorded a decline. Non-financial sector include,

Agricultural, Automobiles and accessories,

Commercial and services, Construction and allied, Energy and petroleum, Manufacturing and

allied, Telecommunication and technology, (NSE, 2014). Some companies listed under the non-

financial sector at the NSE have been delisted, suspended or even put under receivership due to

poor performance.

Business Enterprises have often recorded poor performance due to lack of knowledge of

efficient financial management (Deresse & Prabhakara, 2012). The uncertainty of the business

environment causes business enterprises to rely excessively on equity and maintain high

liquidity and these financial characteristics affect profitability (Deresse & Prabhakara, 2012). It

is therefore worth investigating the effect of financial management practices on financial

performance of non- financial firms.

Introduction

Financial management is one of management functional areas which is core to success of

business enterprises. Inefficient financial management, combined with the uncertainty of the

business environment often led Business Enterprises to serious problems (Deresse & Prabhakara,

2012). Paramasivan and Subramanian (2009) argued that financial management helps to improve

the profitability position of business organizations with the help of strong financial control

devices such as budgetary control and ratio analysis.

As the financial sector at The National Securities’ Exchange, which include banking,

investments and insurance firms, continues to record growth, some firms in the nonfinancial

sector have been characterized by a decline in performance and as a result market prices of their

shares at the National Securities Exchange has recorded a decline. Non-financial sector include,

Agricultural, Automobiles and accessories,

Commercial and services, Construction and allied, Energy and petroleum, Manufacturing and

allied, Telecommunication and technology, (NSE, 2014). Some companies listed under the non-

financial sector at the NSE have been delisted, suspended or even put under receivership due to

poor performance.

Business Enterprises have often recorded poor performance due to lack of knowledge of

efficient financial management (Deresse & Prabhakara, 2012). The uncertainty of the business

environment causes business enterprises to rely excessively on equity and maintain high

liquidity and these financial characteristics affect profitability (Deresse & Prabhakara, 2012). It

is therefore worth investigating the effect of financial management practices on financial

performance of non- financial firms.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL MANAGEMENT PRACTICES 4

Financial Management practices in public sector

The decision function of financial management can be broken down into three major areas: the

investment, financing, and asset management decisions. Financial management practices revolve

around these three key decisions. Efficient financial management requires the existence of some

objective or goal, because judgment as to whether or not a financial decision is efficient must be

made in light of some standard. Different authors and researchers approach the particular areas

of financial management in various ways given their area of focus. For instance, a study carried

out in Malaysia by Mohd et al., (2010) identified the components of financial management as

financial planning and control, financial accounting, financial analysis, management accounting,

capital budgeting and working capital management. Chung and Chuang (2010) studied five

particular areas of financial management practices: capital structure management, working

capital management, financial reporting and analysis, capital budgeting and accounting

information system. From the study variables, Financing, Investing and asset management

decisions play out.

Deresse and Prabhakara (2012), used independent variables such as accounting, reporting, and

analysis, working capital management, fixed asset management and financial planning to

represent financial management practices in the study on the effect of financial management

practices and characteristics on profitability. Other variables which they considered were

Liquidity, Leverage and asset turnover.

Kieu (2006) used financial management practices variables such as accounting information

system, financial reporting and analysis, working capital management, fixed asset management,

financial planning and good performance in financial characteristics such as liquidity and

business activity. Therefore, the study emphasized on three key variables to represent financial

Financial Management practices in public sector

The decision function of financial management can be broken down into three major areas: the

investment, financing, and asset management decisions. Financial management practices revolve

around these three key decisions. Efficient financial management requires the existence of some

objective or goal, because judgment as to whether or not a financial decision is efficient must be

made in light of some standard. Different authors and researchers approach the particular areas

of financial management in various ways given their area of focus. For instance, a study carried

out in Malaysia by Mohd et al., (2010) identified the components of financial management as

financial planning and control, financial accounting, financial analysis, management accounting,

capital budgeting and working capital management. Chung and Chuang (2010) studied five

particular areas of financial management practices: capital structure management, working

capital management, financial reporting and analysis, capital budgeting and accounting

information system. From the study variables, Financing, Investing and asset management

decisions play out.

Deresse and Prabhakara (2012), used independent variables such as accounting, reporting, and

analysis, working capital management, fixed asset management and financial planning to

represent financial management practices in the study on the effect of financial management

practices and characteristics on profitability. Other variables which they considered were

Liquidity, Leverage and asset turnover.

Kieu (2006) used financial management practices variables such as accounting information

system, financial reporting and analysis, working capital management, fixed asset management,

financial planning and good performance in financial characteristics such as liquidity and

business activity. Therefore, the study emphasized on three key variables to represent financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL MANAGEMENT PRACTICES 5

management practices. The key variables are, Liquidity management, Capital budgeting and

Leverage.

Research Questions and Hypotheses

The main objective of the study was to establish the effect of financial management practices on

financial performance of non-financial firms listed at the National securities exchange.

i. To determine the effect of liquidity management on financial performance of non-

financial firms

ii. To establish the effect of capital budgeting on financial performance of nonfinancial

firms.

iii. To determine the effect of leverage on financial performance of non-financial firms

iv. To evaluate the moderating effect of inflation on the relationship between financial

management practices and financial performance of non-financial firms.

Research Hypotheses

In view of the research objectives the study sought to test the following null hypotheses.

H01: Liquidity management has no significant effect on the financial performance of non-

financial firms listed at the NSE.

H02: Capital budgeting has no significant effect on the financial performance of nonfinancial

firms listed at the NSE.

H03: Leverage has no significant effect on the financial performance of on-financial firms listed

at the NSE.

H04: Inflation has no significant effect on the relationship between financial management

practices and financial performance of non-financial firms listed at the NSE.

management practices. The key variables are, Liquidity management, Capital budgeting and

Leverage.

Research Questions and Hypotheses

The main objective of the study was to establish the effect of financial management practices on

financial performance of non-financial firms listed at the National securities exchange.

i. To determine the effect of liquidity management on financial performance of non-

financial firms

ii. To establish the effect of capital budgeting on financial performance of nonfinancial

firms.

iii. To determine the effect of leverage on financial performance of non-financial firms

iv. To evaluate the moderating effect of inflation on the relationship between financial

management practices and financial performance of non-financial firms.

Research Hypotheses

In view of the research objectives the study sought to test the following null hypotheses.

H01: Liquidity management has no significant effect on the financial performance of non-

financial firms listed at the NSE.

H02: Capital budgeting has no significant effect on the financial performance of nonfinancial

firms listed at the NSE.

H03: Leverage has no significant effect on the financial performance of on-financial firms listed

at the NSE.

H04: Inflation has no significant effect on the relationship between financial management

practices and financial performance of non-financial firms listed at the NSE.

FINANCIAL MANAGEMENT PRACTICES 6

Literature Review

Concerned with financial management practices, previous researchers have concentrated on

examining, investigating and describing the behaviour of Securities Exchange market in

practising financial management. Their findings are mainly related to exploring and describing

the behaviour of Securities Exchange market towards financial management practices. Although

they provided much descriptive statistical data and empirical evidence on Securities Exchange

market financial management practices, it appears that there still are some gaps in the literature,

which need to be addressed. Most research work on performance have looked at individual

components of financial management and not financial management as a whole.

Though comprehensive studies looking at financial management as a whole have been carried

out in developed countries, few studies have been carried out in developing countries.

Table 1: Summary of Research Gaps

RESEARC

H

AUT

HOR

VARIAB

LES

METHOD

O

LOGY/

MODEL

FINDIN

GS

RESEA

RCH

GAPS

HOW

GAPS ARE

ADDRESS

ED

Financial

Manageme

nt Practices

and

performanc

e

Butt,

Hunj

r a

and

Reh

m

an

(201

0)

Investment

appraisal

techniques

Financial

Assessment

Capital

structure

decision

Dividend

Policy

Working

Capital

Policy

Organizatio

nal

60

companies

listed at

Ellbi stock

exchange

covering

2008-

2009.

The

results

show a

positive and

significant

Relationshi

p between

financial

managemen

t practices

and

organizatio

nal

performanc

e in

Pakistani

corporate

Study

conducte

d outside

Africa.

Moderati

ng effect

of

Inflation

not

considere

d.

Considere

d

moderatin

g effect of

inflation

on

variables.

Literature Review

Concerned with financial management practices, previous researchers have concentrated on

examining, investigating and describing the behaviour of Securities Exchange market in

practising financial management. Their findings are mainly related to exploring and describing

the behaviour of Securities Exchange market towards financial management practices. Although

they provided much descriptive statistical data and empirical evidence on Securities Exchange

market financial management practices, it appears that there still are some gaps in the literature,

which need to be addressed. Most research work on performance have looked at individual

components of financial management and not financial management as a whole.

Though comprehensive studies looking at financial management as a whole have been carried

out in developed countries, few studies have been carried out in developing countries.

Table 1: Summary of Research Gaps

RESEARC

H

AUT

HOR

VARIAB

LES

METHOD

O

LOGY/

MODEL

FINDIN

GS

RESEA

RCH

GAPS

HOW

GAPS ARE

ADDRESS

ED

Financial

Manageme

nt Practices

and

performanc

e

Butt,

Hunj

r a

and

Reh

m

an

(201

0)

Investment

appraisal

techniques

Financial

Assessment

Capital

structure

decision

Dividend

Policy

Working

Capital

Policy

Organizatio

nal

60

companies

listed at

Ellbi stock

exchange

covering

2008-

2009.

The

results

show a

positive and

significant

Relationshi

p between

financial

managemen

t practices

and

organizatio

nal

performanc

e in

Pakistani

corporate

Study

conducte

d outside

Africa.

Moderati

ng effect

of

Inflation

not

considere

d.

Considere

d

moderatin

g effect of

inflation

on

variables.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL MANAGEMENT PRACTICES 7

Performanc

e

sector.

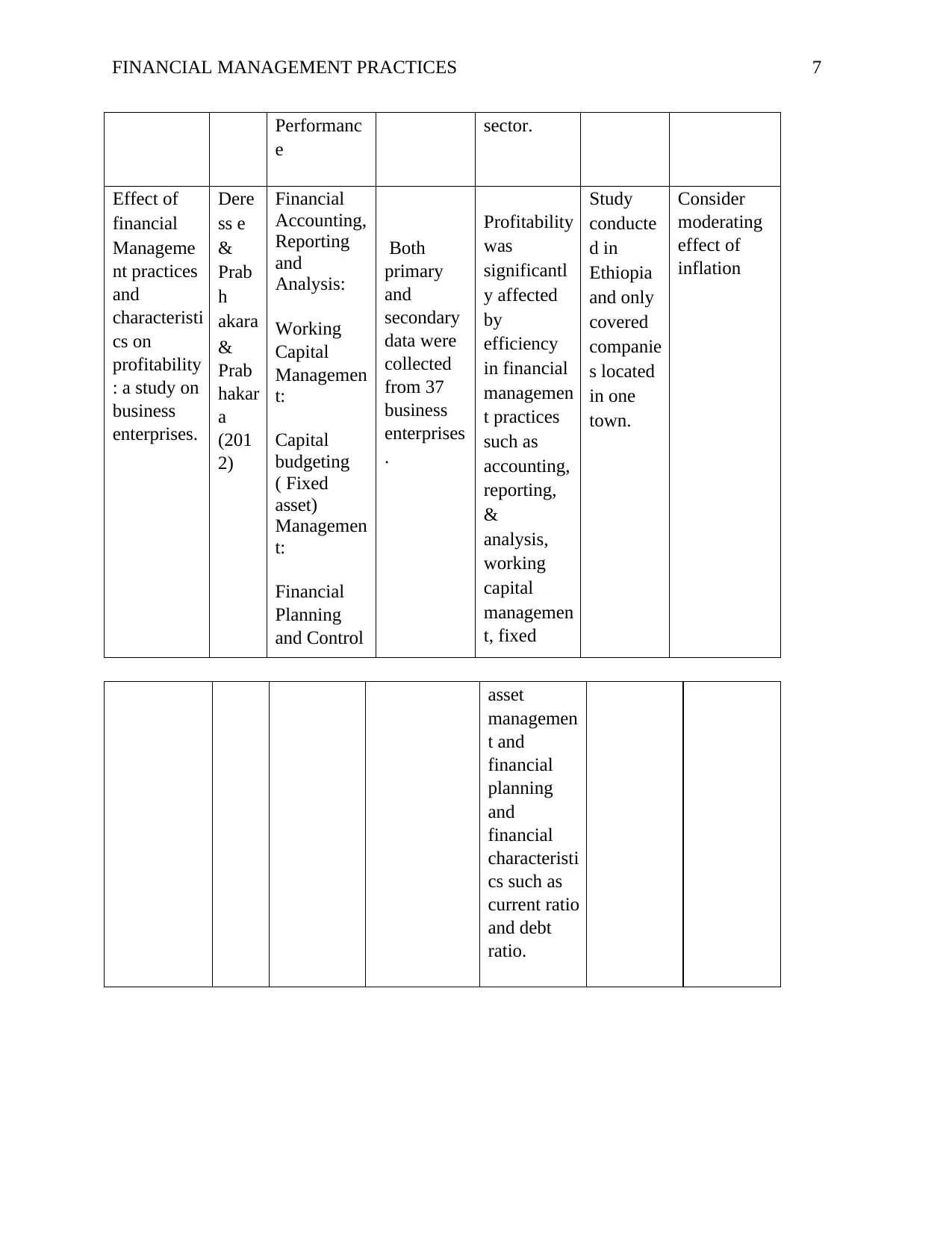

Effect of

financial

Manageme

nt practices

and

characteristi

cs on

profitability

: a study on

business

enterprises.

Dere

ss e

&

Prab

h

akara

&

Prab

hakar

a

(201

2)

Financial

Accounting,

Reporting

and

Analysis:

Working

Capital

Managemen

t:

Capital

budgeting

( Fixed

asset)

Managemen

t:

Financial

Planning

and Control

Both

primary

and

secondary

data were

collected

from 37

business

enterprises

.

Profitability

was

significantl

y affected

by

efficiency

in financial

managemen

t practices

such as

accounting,

reporting,

&

analysis,

working

capital

managemen

t, fixed

Study

conducte

d in

Ethiopia

and only

covered

companie

s located

in one

town.

Consider

moderating

effect of

inflation

asset

managemen

t and

financial

planning

and

financial

characteristi

cs such as

current ratio

and debt

ratio.

Performanc

e

sector.

Effect of

financial

Manageme

nt practices

and

characteristi

cs on

profitability

: a study on

business

enterprises.

Dere

ss e

&

Prab

h

akara

&

Prab

hakar

a

(201

2)

Financial

Accounting,

Reporting

and

Analysis:

Working

Capital

Managemen

t:

Capital

budgeting

( Fixed

asset)

Managemen

t:

Financial

Planning

and Control

Both

primary

and

secondary

data were

collected

from 37

business

enterprises

.

Profitability

was

significantl

y affected

by

efficiency

in financial

managemen

t practices

such as

accounting,

reporting,

&

analysis,

working

capital

managemen

t, fixed

Study

conducte

d in

Ethiopia

and only

covered

companie

s located

in one

town.

Consider

moderating

effect of

inflation

asset

managemen

t and

financial

planning

and

financial

characteristi

cs such as

current ratio

and debt

ratio.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL MANAGEMENT PRACTICES 8

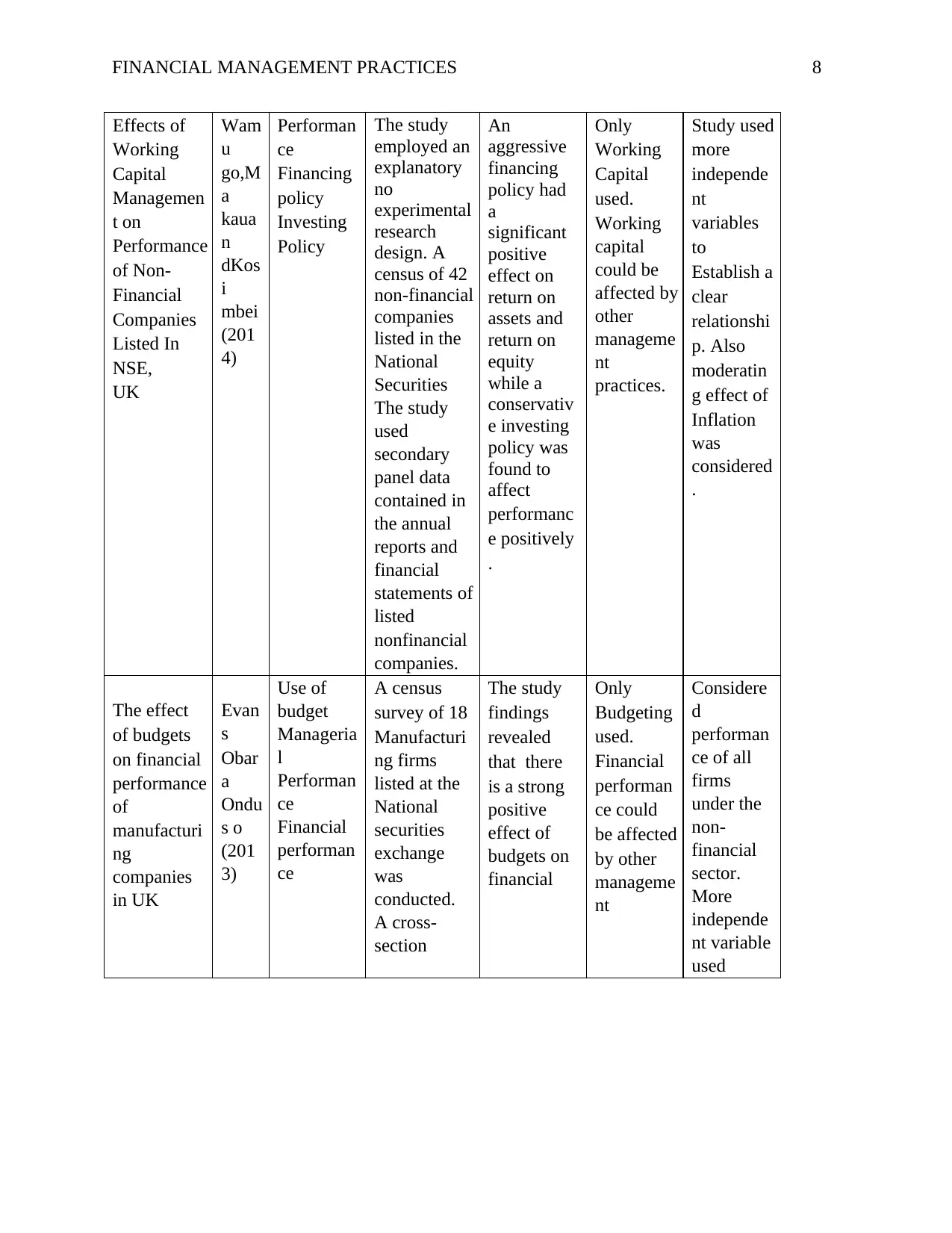

Effects of

Working

Capital

Managemen

t on

Performance

of Non-

Financial

Companies

Listed In

NSE,

UK

Wam

u

go,M

a

kaua

n

dKos

i

mbei

(201

4)

Performan

ce

Financing

policy

Investing

Policy

The study

employed an

explanatory

no

experimental

research

design. A

census of 42

non-financial

companies

listed in the

National

Securities

The study

used

secondary

panel data

contained in

the annual

reports and

financial

statements of

listed

nonfinancial

companies.

An

aggressive

financing

policy had

a

significant

positive

effect on

return on

assets and

return on

equity

while a

conservativ

e investing

policy was

found to

affect

performanc

e positively

.

Only

Working

Capital

used.

Working

capital

could be

affected by

other

manageme

nt

practices.

Study used

more

independe

nt

variables

to

Establish a

clear

relationshi

p. Also

moderatin

g effect of

Inflation

was

considered

.

The effect

of budgets

on financial

performance

of

manufacturi

ng

companies

in UK

Evan

s

Obar

a

Ondu

s o

(201

3)

Use of

budget

Manageria

l

Performan

ce

Financial

performan

ce

A census

survey of 18

Manufacturi

ng firms

listed at the

National

securities

exchange

was

conducted.

A cross-

section

The study

findings

revealed

that there

is a strong

positive

effect of

budgets on

financial

Only

Budgeting

used.

Financial

performan

ce could

be affected

by other

manageme

nt

Considere

d

performan

ce of all

firms

under the

non-

financial

sector.

More

independe

nt variable

used

Effects of

Working

Capital

Managemen

t on

Performance

of Non-

Financial

Companies

Listed In

NSE,

UK

Wam

u

go,M

a

kaua

n

dKos

i

mbei

(201

4)

Performan

ce

Financing

policy

Investing

Policy

The study

employed an

explanatory

no

experimental

research

design. A

census of 42

non-financial

companies

listed in the

National

Securities

The study

used

secondary

panel data

contained in

the annual

reports and

financial

statements of

listed

nonfinancial

companies.

An

aggressive

financing

policy had

a

significant

positive

effect on

return on

assets and

return on

equity

while a

conservativ

e investing

policy was

found to

affect

performanc

e positively

.

Only

Working

Capital

used.

Working

capital

could be

affected by

other

manageme

nt

practices.

Study used

more

independe

nt

variables

to

Establish a

clear

relationshi

p. Also

moderatin

g effect of

Inflation

was

considered

.

The effect

of budgets

on financial

performance

of

manufacturi

ng

companies

in UK

Evan

s

Obar

a

Ondu

s o

(201

3)

Use of

budget

Manageria

l

Performan

ce

Financial

performan

ce

A census

survey of 18

Manufacturi

ng firms

listed at the

National

securities

exchange

was

conducted.

A cross-

section

The study

findings

revealed

that there

is a strong

positive

effect of

budgets on

financial

Only

Budgeting

used.

Financial

performan

ce could

be affected

by other

manageme

nt

Considere

d

performan

ce of all

firms

under the

non-

financial

sector.

More

independe

nt variable

used

FINANCIAL MANAGEMENT PRACTICES 9

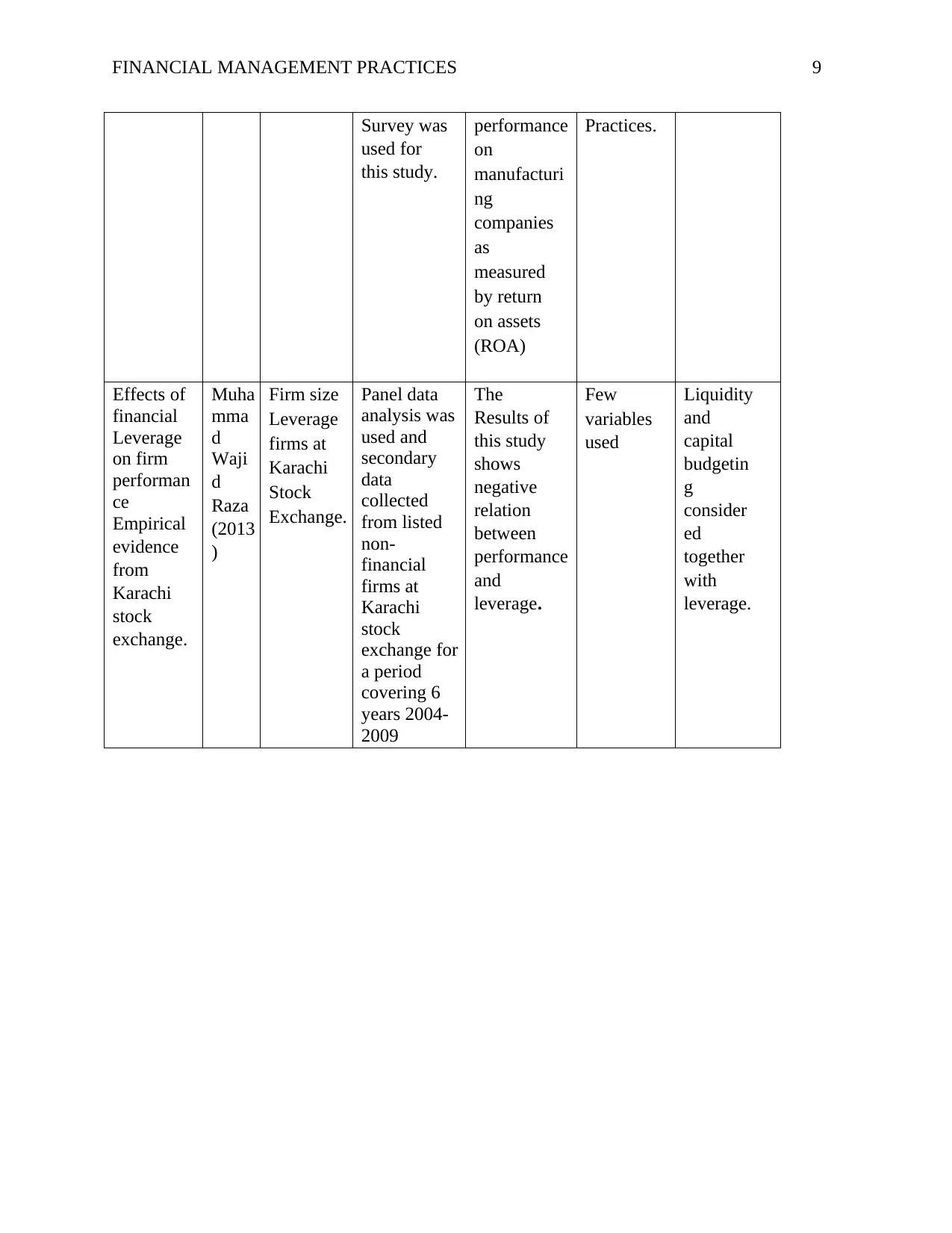

Survey was

used for

this study.

performance

on

manufacturi

ng

companies

as

measured

by return

on assets

(ROA)

Practices.

Effects of

financial

Leverage

on firm

performan

ce

Empirical

evidence

from

Karachi

stock

exchange.

Muha

mma

d

Waji

d

Raza

(2013

)

Firm size

Leverage

firms at

Karachi

Stock

Exchange.

Panel data

analysis was

used and

secondary

data

collected

from listed

non-

financial

firms at

Karachi

stock

exchange for

a period

covering 6

years 2004-

2009

The

Results of

this study

shows

negative

relation

between

performance

and

leverage.

Few

variables

used

Liquidity

and

capital

budgetin

g

consider

ed

together

with

leverage.

Survey was

used for

this study.

performance

on

manufacturi

ng

companies

as

measured

by return

on assets

(ROA)

Practices.

Effects of

financial

Leverage

on firm

performan

ce

Empirical

evidence

from

Karachi

stock

exchange.

Muha

mma

d

Waji

d

Raza

(2013

)

Firm size

Leverage

firms at

Karachi

Stock

Exchange.

Panel data

analysis was

used and

secondary

data

collected

from listed

non-

financial

firms at

Karachi

stock

exchange for

a period

covering 6

years 2004-

2009

The

Results of

this study

shows

negative

relation

between

performance

and

leverage.

Few

variables

used

Liquidity

and

capital

budgetin

g

consider

ed

together

with

leverage.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL MANAGEMENT PRACTICES 10

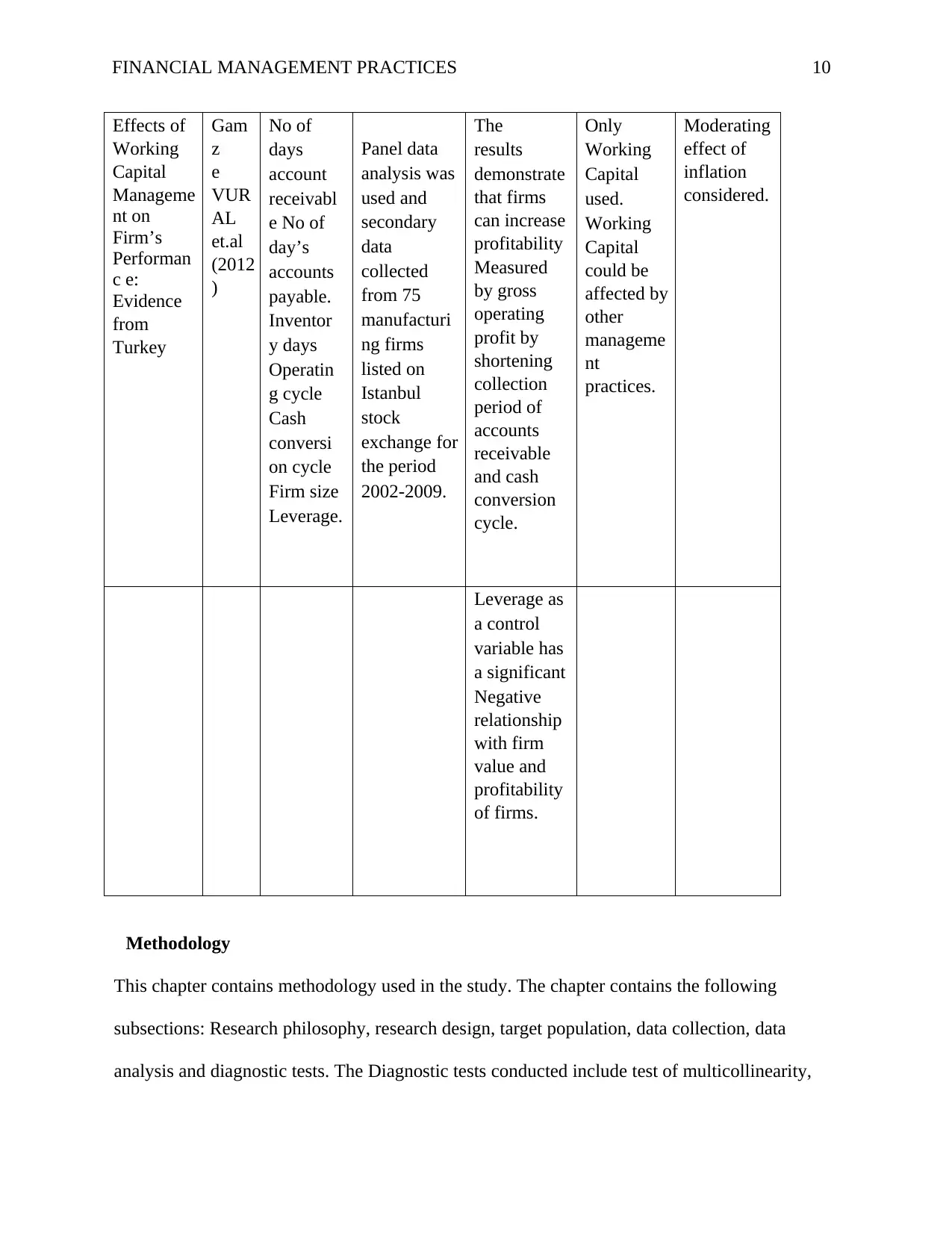

Effects of

Working

Capital

Manageme

nt on

Firm’s

Performan

c e:

Evidence

from

Turkey

Gam

z

e

VUR

AL

et.al

(2012

)

No of

days

account

receivabl

e No of

day’s

accounts

payable.

Inventor

y days

Operatin

g cycle

Cash

conversi

on cycle

Firm size

Leverage.

Panel data

analysis was

used and

secondary

data

collected

from 75

manufacturi

ng firms

listed on

Istanbul

stock

exchange for

the period

2002-2009.

The

results

demonstrate

that firms

can increase

profitability

Measured

by gross

operating

profit by

shortening

collection

period of

accounts

receivable

and cash

conversion

cycle.

Only

Working

Capital

used.

Working

Capital

could be

affected by

other

manageme

nt

practices.

Moderating

effect of

inflation

considered.

Leverage as

a control

variable has

a significant

Negative

relationship

with firm

value and

profitability

of firms.

Methodology

This chapter contains methodology used in the study. The chapter contains the following

subsections: Research philosophy, research design, target population, data collection, data

analysis and diagnostic tests. The Diagnostic tests conducted include test of multicollinearity,

Effects of

Working

Capital

Manageme

nt on

Firm’s

Performan

c e:

Evidence

from

Turkey

Gam

z

e

VUR

AL

et.al

(2012

)

No of

days

account

receivabl

e No of

day’s

accounts

payable.

Inventor

y days

Operatin

g cycle

Cash

conversi

on cycle

Firm size

Leverage.

Panel data

analysis was

used and

secondary

data

collected

from 75

manufacturi

ng firms

listed on

Istanbul

stock

exchange for

the period

2002-2009.

The

results

demonstrate

that firms

can increase

profitability

Measured

by gross

operating

profit by

shortening

collection

period of

accounts

receivable

and cash

conversion

cycle.

Only

Working

Capital

used.

Working

Capital

could be

affected by

other

manageme

nt

practices.

Moderating

effect of

inflation

considered.

Leverage as

a control

variable has

a significant

Negative

relationship

with firm

value and

profitability

of firms.

Methodology

This chapter contains methodology used in the study. The chapter contains the following

subsections: Research philosophy, research design, target population, data collection, data

analysis and diagnostic tests. The Diagnostic tests conducted include test of multicollinearity,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL MANAGEMENT PRACTICES 11

equality of means, stationary and houseman test. According to Hudson and Ozanne (1988),

“positivism ontology asserts that there is a single, external and objective reality to any research

question regardless of the researcher’s belief. Thus, the positivist researchers take a controlled

and structural approach in conducting research by initially identifying a research topic,

constructing appropriate research questions and hypotheses and by adopting a suitable

methodology. As positivists’, researchers seek objectivity and use consistently rational and

logical approaches to research.

Further, statistical and mathematical techniques are central in the research methods adopted by

positivist researchers and they adhere to specifically structured research techniques to uncover

single and objective realities. The goal of positivist research is to make generalizations because

human actions can be explained as a result of real causes that precedes their behavior.

An interpretive researcher enters the field with some sort of prior insight about the research topic

but assumes that it is insufficient in developing a fixed research design due to complex, multiple

and unpredictable nature of what is perceived as reality. During data collection stage, the

researcher and his informants are interdependent and mutually interactive with each other. The

goal of interpretive research is to understand and interpret human behavior rather than to

generalize and predict causes and effects (Hopkins, 2000).Given the research problem of this

study positivist paradigm was adopted.

The model used was fixed effects model to test research hypothesis. Independent variables used

were variables to define financial management practices which include Liquidity management,

Capital budgeting and Leverage. Financial performance was measured by ROA ratio. As an

indicator of liquidity (LIQ) the conventional definition was used: The ratio of current assets to

equality of means, stationary and houseman test. According to Hudson and Ozanne (1988),

“positivism ontology asserts that there is a single, external and objective reality to any research

question regardless of the researcher’s belief. Thus, the positivist researchers take a controlled

and structural approach in conducting research by initially identifying a research topic,

constructing appropriate research questions and hypotheses and by adopting a suitable

methodology. As positivists’, researchers seek objectivity and use consistently rational and

logical approaches to research.

Further, statistical and mathematical techniques are central in the research methods adopted by

positivist researchers and they adhere to specifically structured research techniques to uncover

single and objective realities. The goal of positivist research is to make generalizations because

human actions can be explained as a result of real causes that precedes their behavior.

An interpretive researcher enters the field with some sort of prior insight about the research topic

but assumes that it is insufficient in developing a fixed research design due to complex, multiple

and unpredictable nature of what is perceived as reality. During data collection stage, the

researcher and his informants are interdependent and mutually interactive with each other. The

goal of interpretive research is to understand and interpret human behavior rather than to

generalize and predict causes and effects (Hopkins, 2000).Given the research problem of this

study positivist paradigm was adopted.

The model used was fixed effects model to test research hypothesis. Independent variables used

were variables to define financial management practices which include Liquidity management,

Capital budgeting and Leverage. Financial performance was measured by ROA ratio. As an

indicator of liquidity (LIQ) the conventional definition was used: The ratio of current assets to

FINANCIAL MANAGEMENT PRACTICES 12

current liabilities (Jong, Kabir, & Nguyen, 2008).Capital budgeting was measured by ROCE

ratio and Leverage was measured by use of debt ratio.

The model of the effect of financial management practices on financial performance was

formulated as follows: ROA= f (LM, FCB, and LR) Where:

ROA= Return on assets

LM= Liquidity Management

FCB = Capital budgeting

LR = Leverage ratio

Equation1………..

(Reduced Equation)

Equation 2……….

(Full Equation)

Where: the coefficients, ε is the error variable,

ELM, EFCB& LR are independent variables related to financial management practices.

i is Number of non- financial firms (38 firms were studied) t

is time. ie Year 2010,2011,2012,2013 and 2014

I is Inflation

Data Collection

The study used panel secondary data to test hypotheses. The secondary data was contained in the

financial statements of listed non-financial firms. A work plan was drawn to extract data relating

current liabilities (Jong, Kabir, & Nguyen, 2008).Capital budgeting was measured by ROCE

ratio and Leverage was measured by use of debt ratio.

The model of the effect of financial management practices on financial performance was

formulated as follows: ROA= f (LM, FCB, and LR) Where:

ROA= Return on assets

LM= Liquidity Management

FCB = Capital budgeting

LR = Leverage ratio

Equation1………..

(Reduced Equation)

Equation 2……….

(Full Equation)

Where: the coefficients, ε is the error variable,

ELM, EFCB& LR are independent variables related to financial management practices.

i is Number of non- financial firms (38 firms were studied) t

is time. ie Year 2010,2011,2012,2013 and 2014

I is Inflation

Data Collection

The study used panel secondary data to test hypotheses. The secondary data was contained in the

financial statements of listed non-financial firms. A work plan was drawn to extract data relating

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.