Detailed Budgeting and Variance Analysis Report for Hospitality

VerifiedAdded on 2022/11/14

|7

|1898

|128

Report

AI Summary

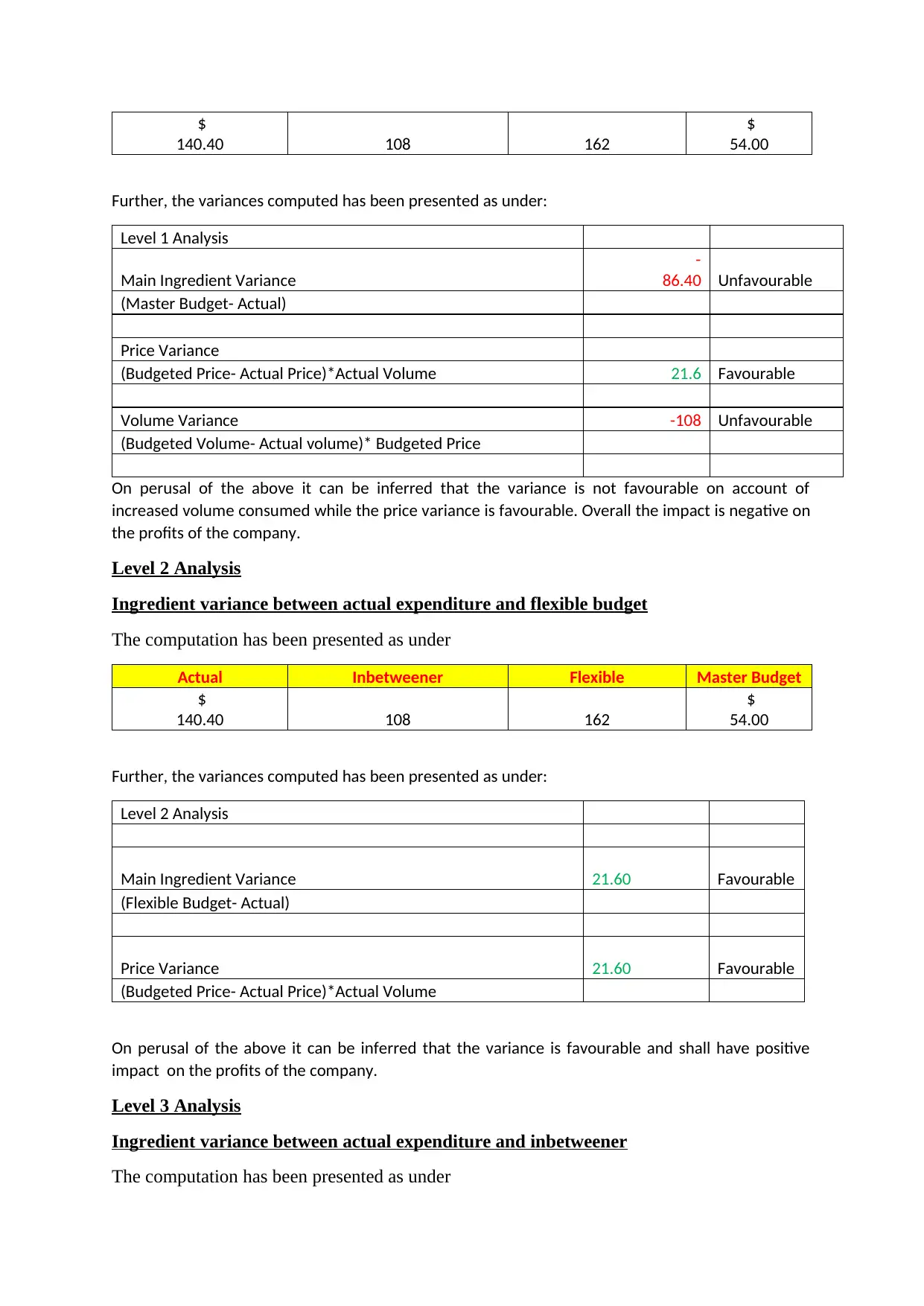

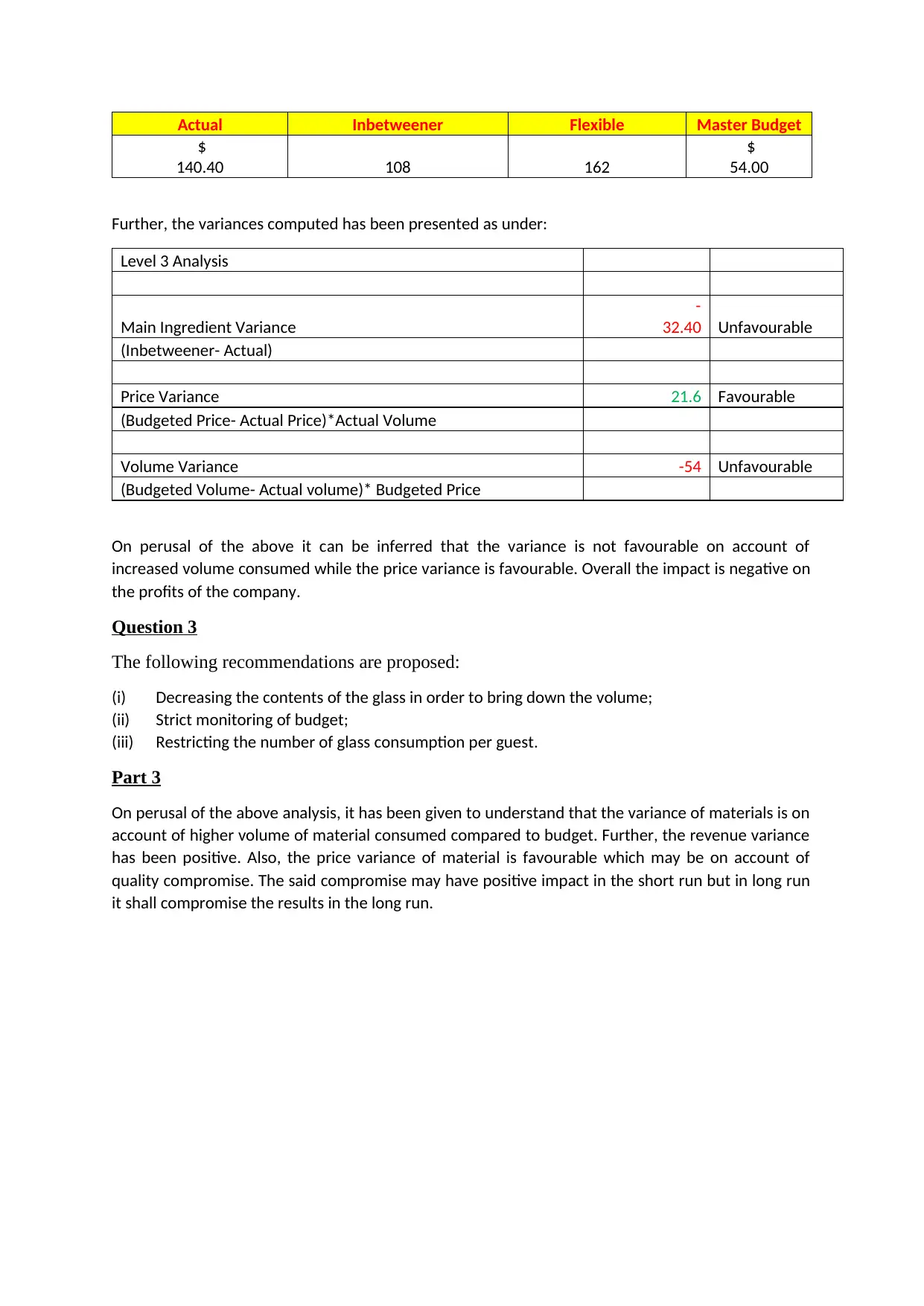

This report provides a comprehensive analysis of budgeting practices within the hospitality industry. Part 1 discusses the reasons for using budgets, highlighting their role in setting financial targets, coordinating departmental objectives, and guiding future planning. It also examines potential behavioral problems associated with budget implementation, such as the impact of environmental changes and time-consuming processes. Part 2 focuses on the shortfalls of using budgets for staff performance evaluation, including the limitations of assumptions and the potential for unrealistic targets. The report further presents revenue and ingredient variance analyses for specific events, exploring the differences between actual and budgeted figures, and identifying price and volume variances. The analysis includes recommendations for improvement, such as strict budget monitoring and controlling consumption. The report concludes by emphasizing the impact of material variance and the importance of balancing short-term gains with long-term quality considerations.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.