Accounting Capstone Report: Financial Performance Analysis

VerifiedAdded on 2022/10/19

|11

|2291

|377

Report

AI Summary

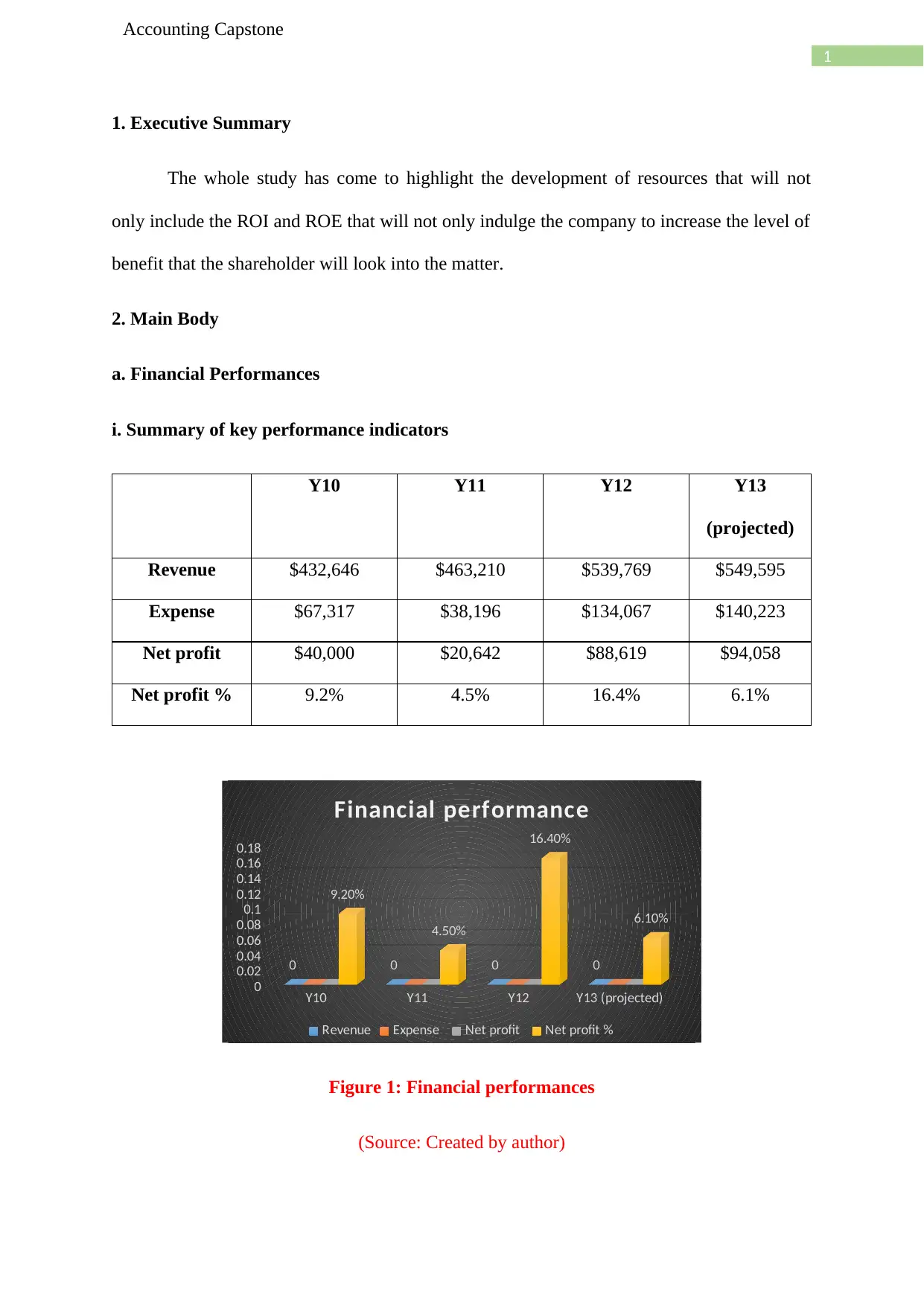

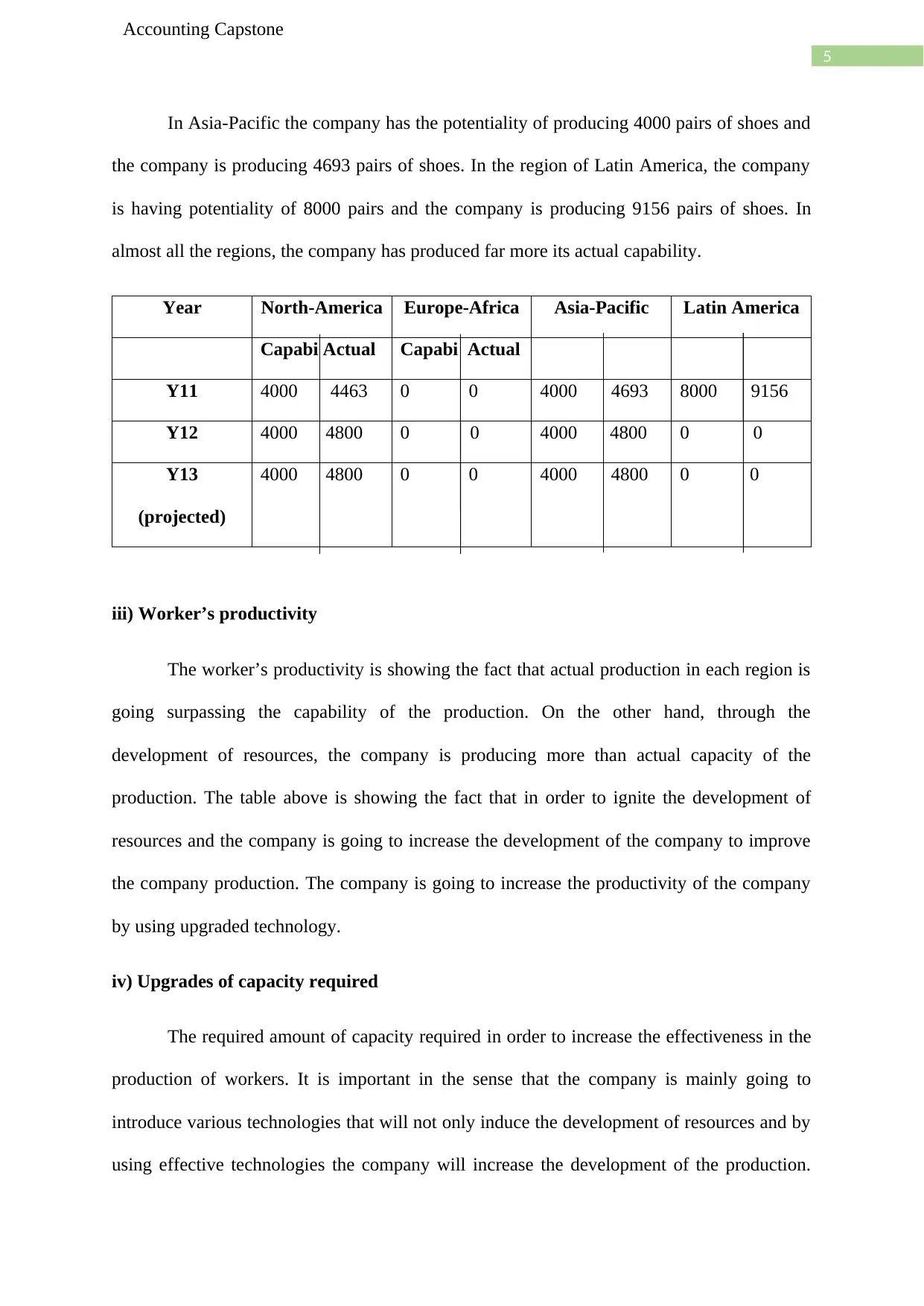

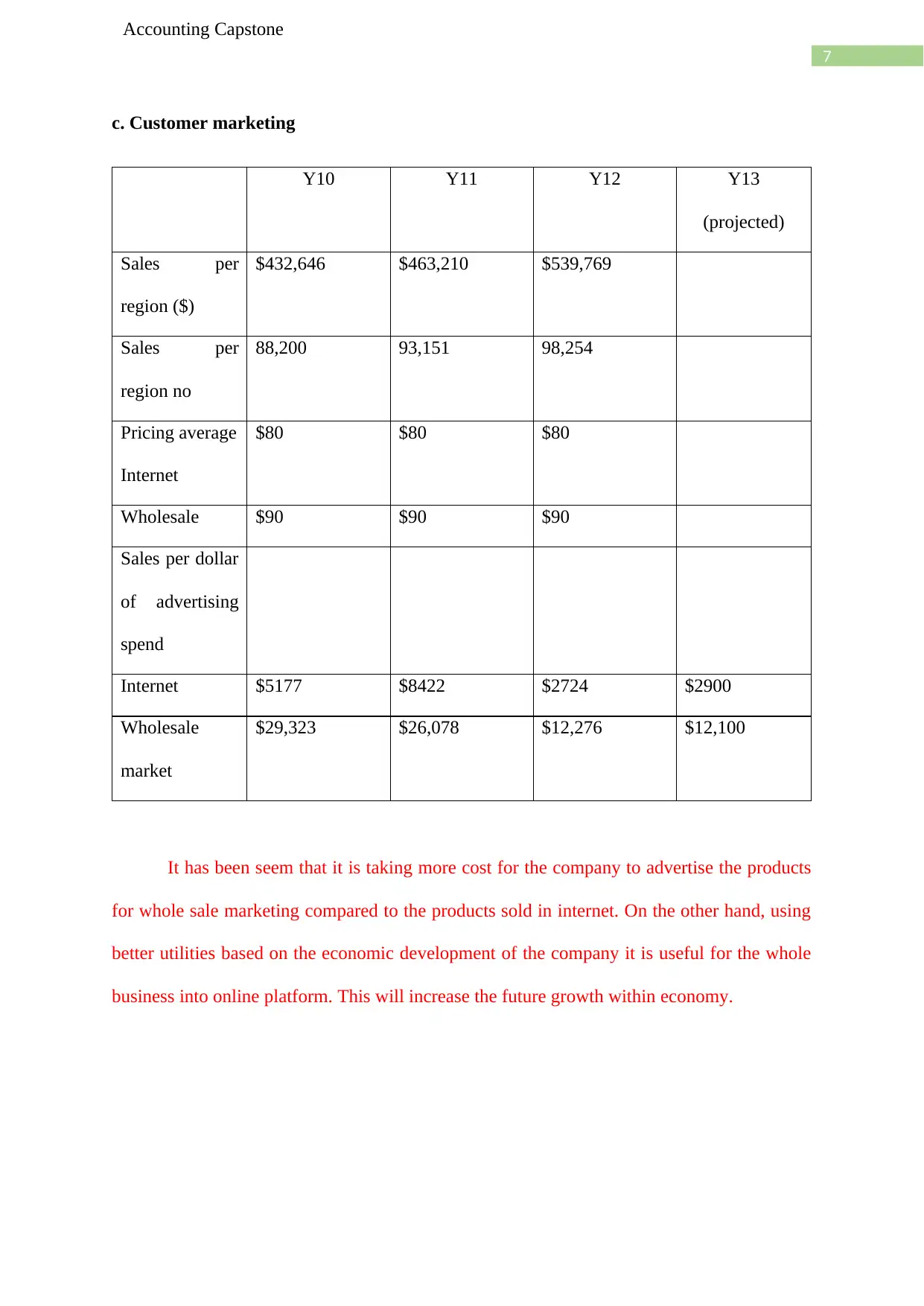

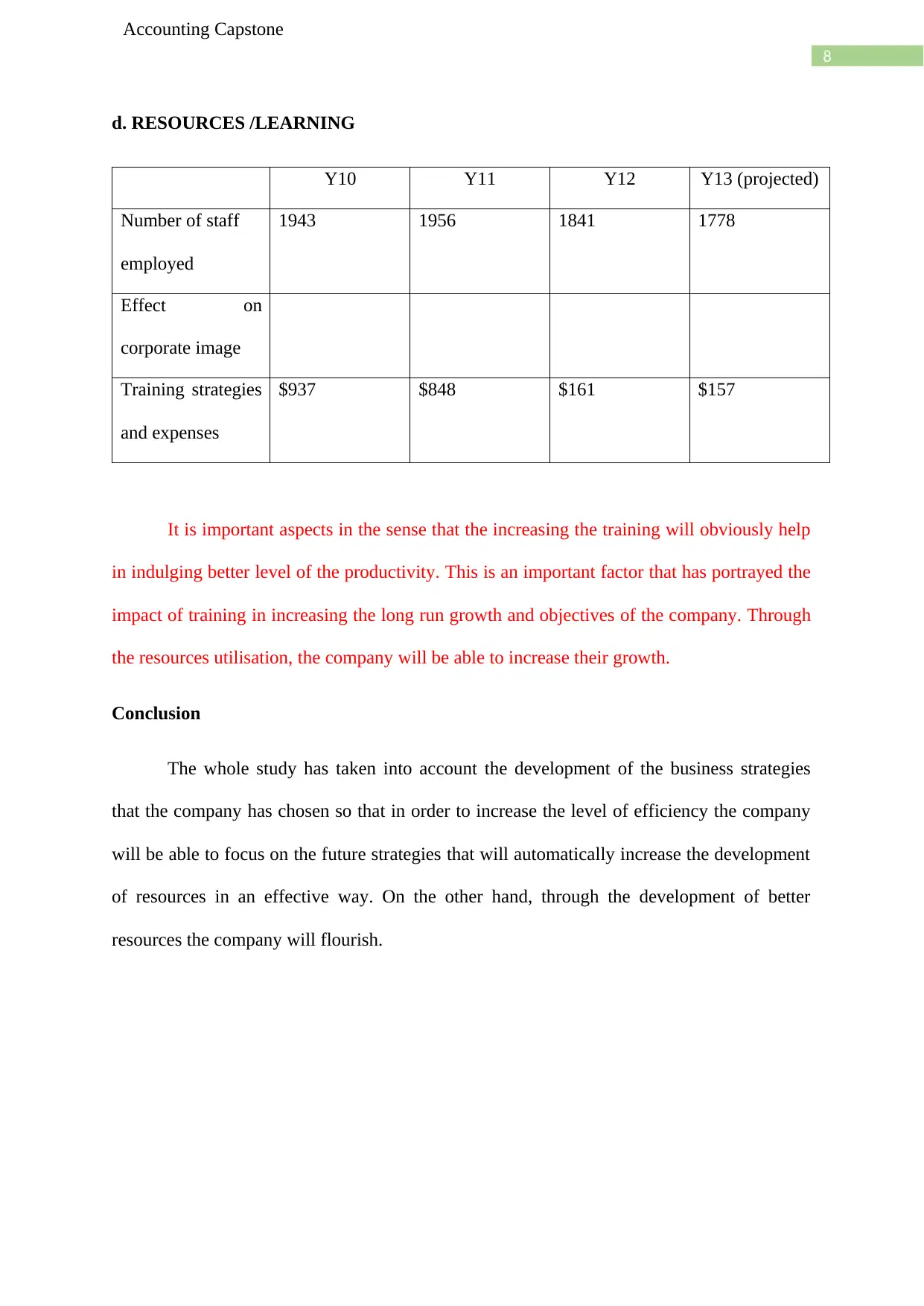

This report provides a comprehensive analysis of the I Bata Company's financial performance over several years, including projected data. It begins with an executive summary outlining the company's overall strategy and key outcomes. The main body of the report delves into financial performance, presenting key performance indicators such as revenue, expenses, and net profit, along with calculations of ROI and ROE. The report also examines revenue streams from internet and wholesale markets, balance sheet data, liquidity ratios, and cash position. The operations section assesses stock and production levels, worker productivity, and plant capacity utilization across different regions. The customer marketing section analyzes sales per region and advertising effectiveness. Finally, the report evaluates resource management, including staffing, training, and their impact on corporate image. The conclusion summarizes business strategies and provides a reference list of sources used.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.