Financial Performance Analysis Report: Super Entertainers Overview

VerifiedAdded on 2022/11/18

|12

|1124

|183

Report

AI Summary

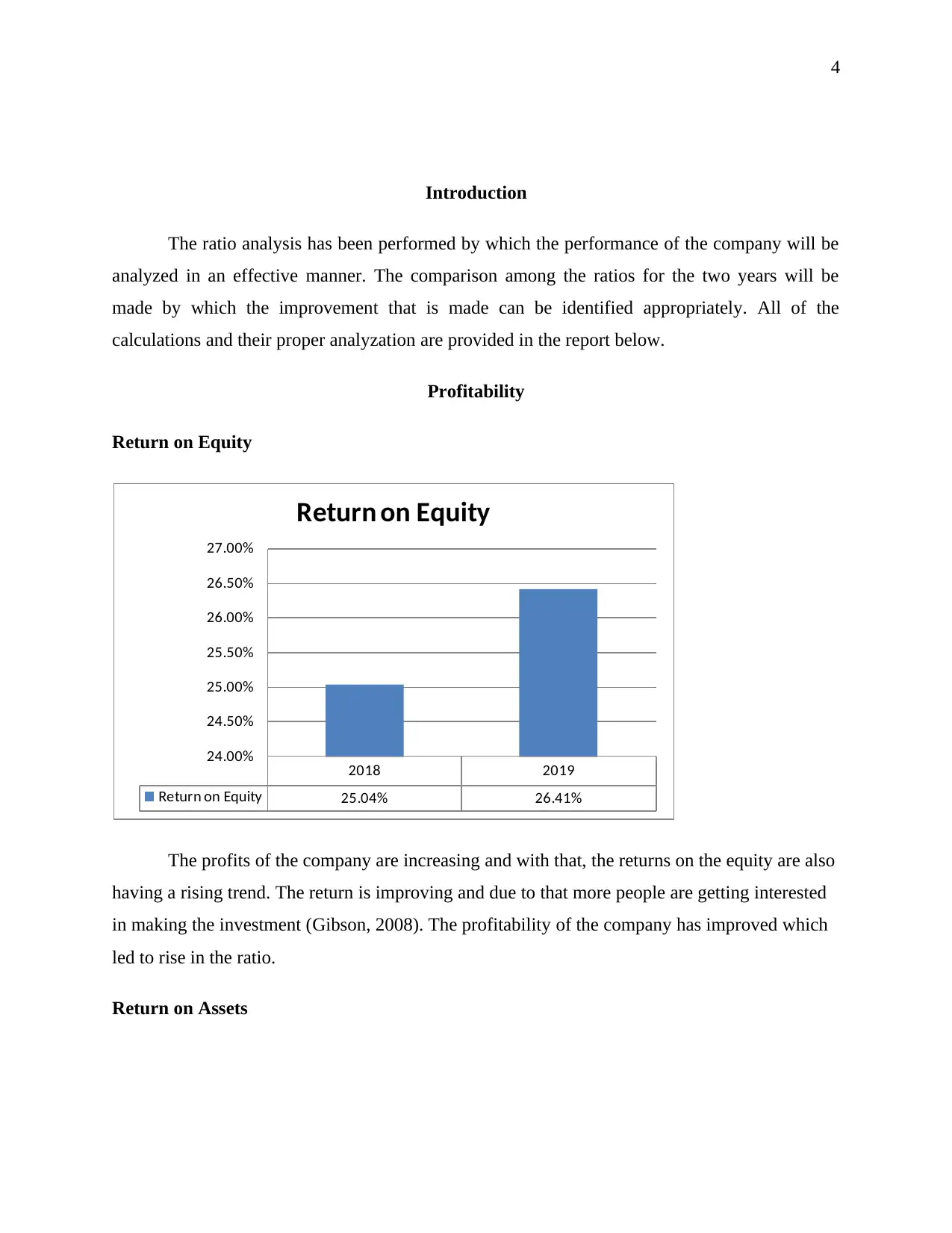

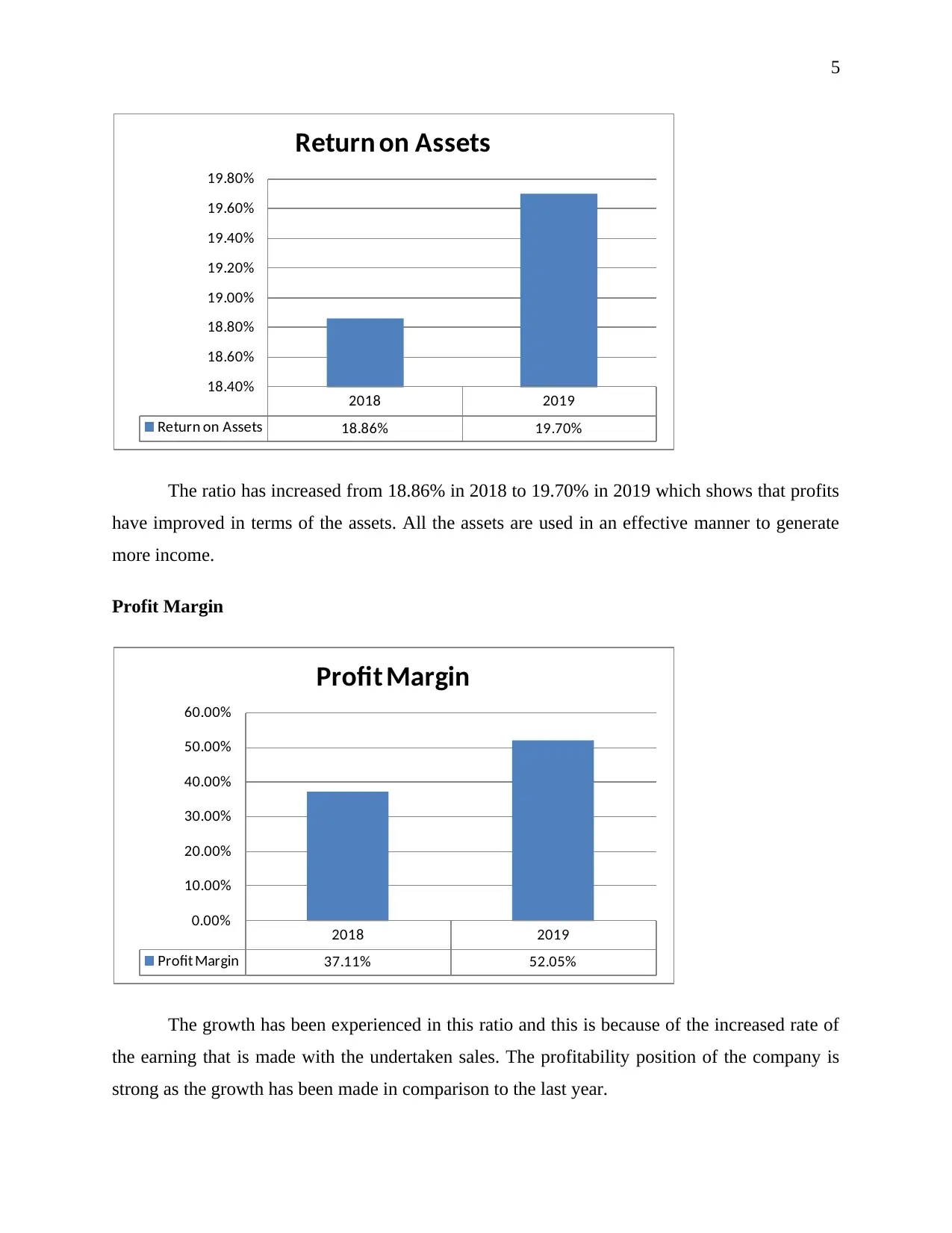

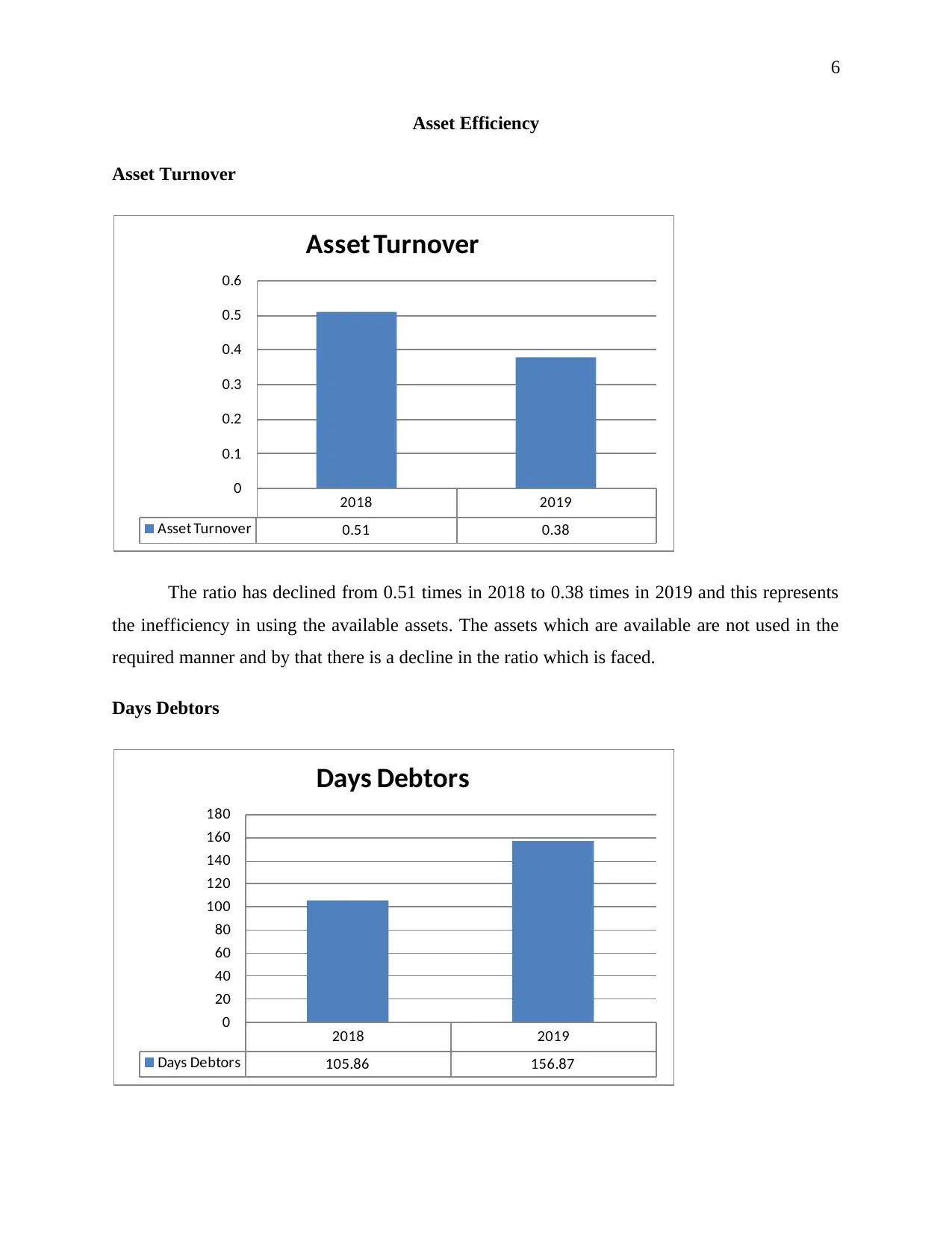

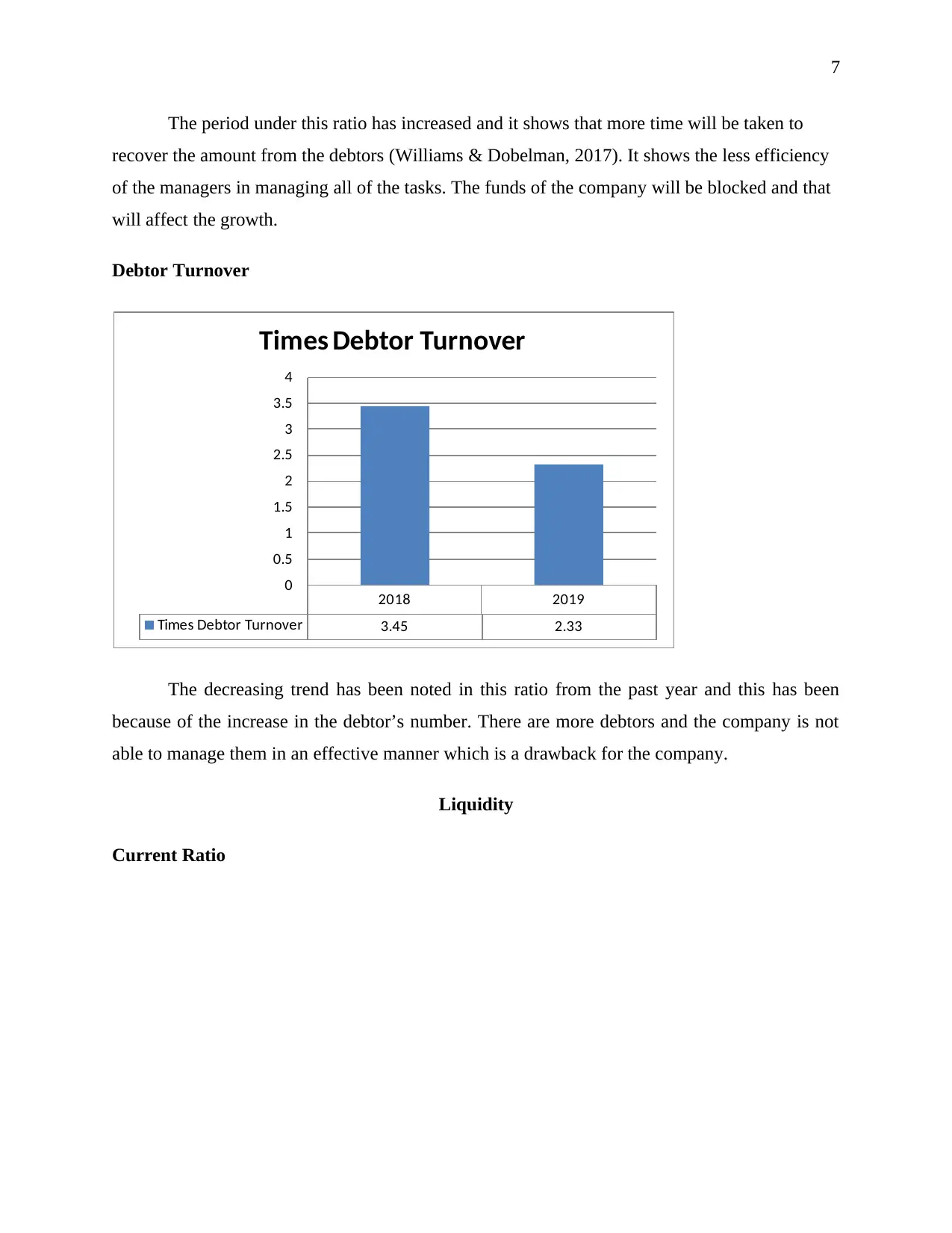

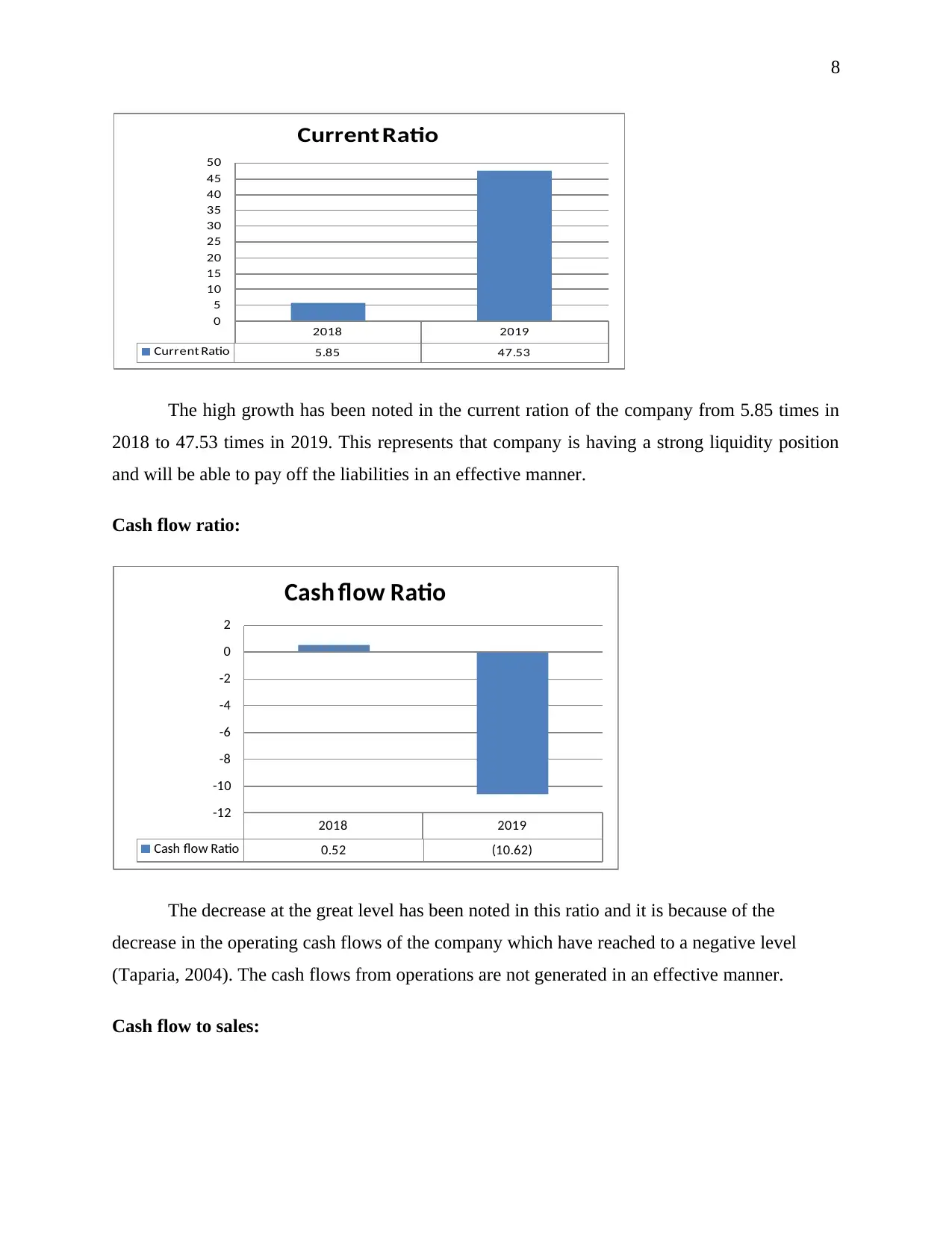

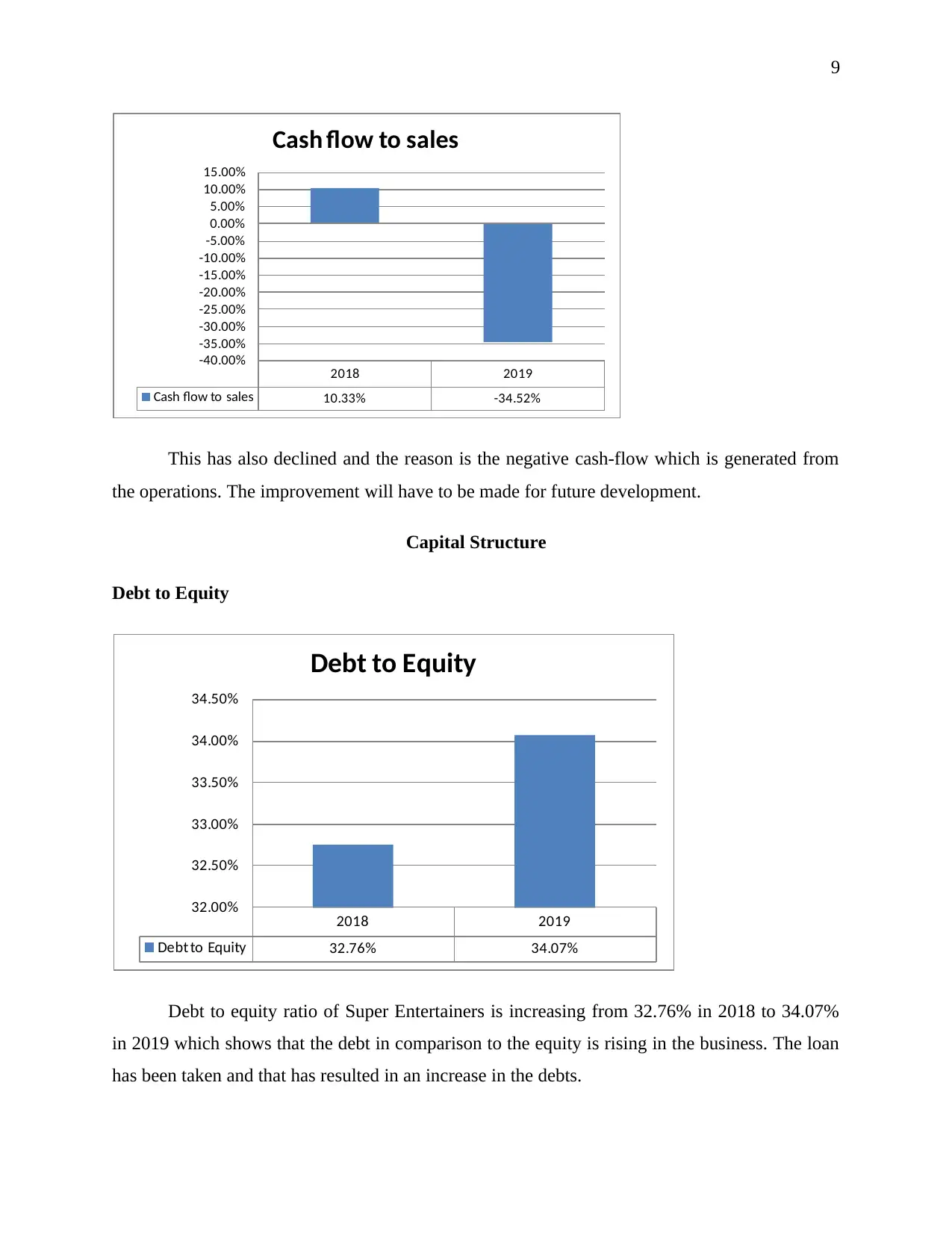

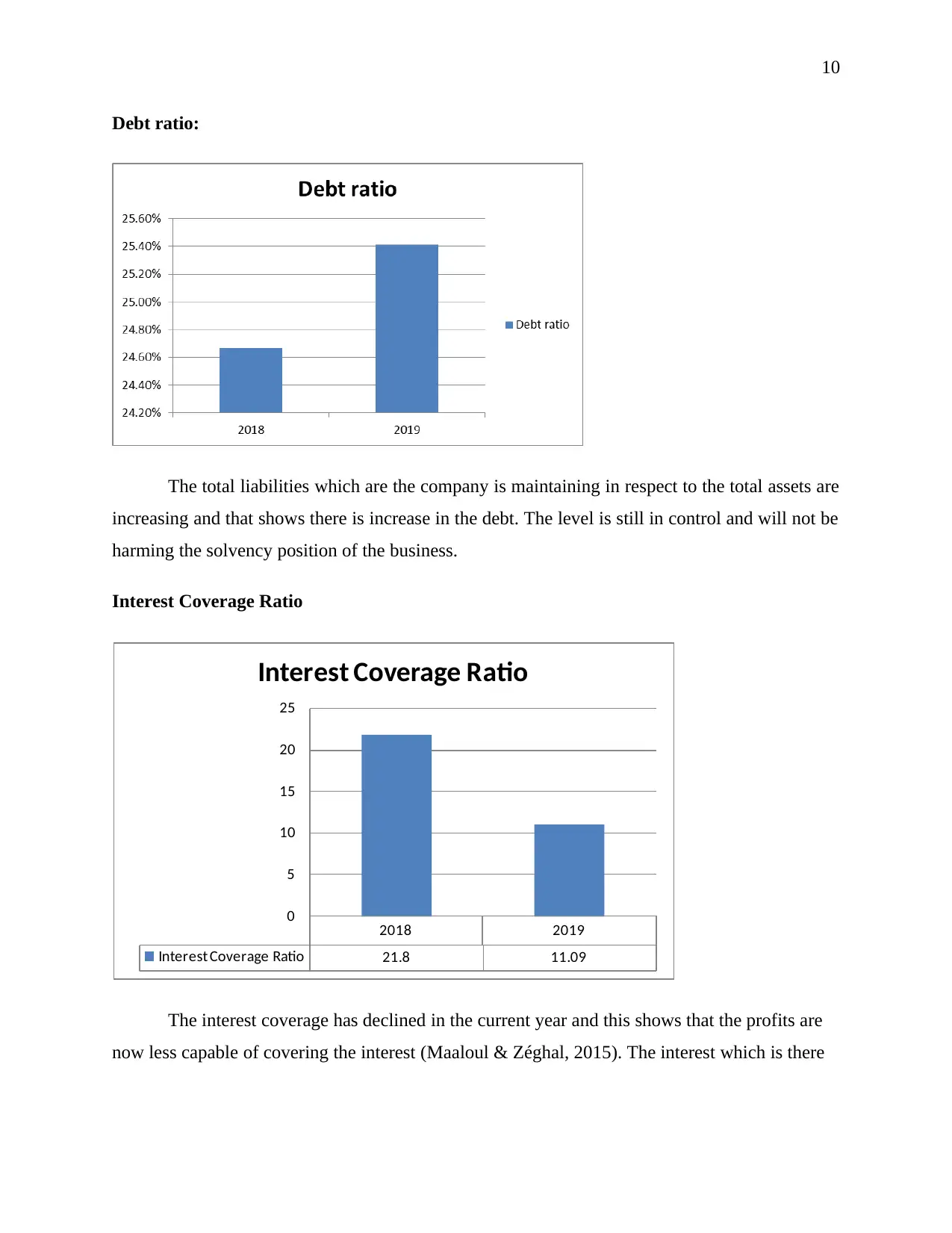

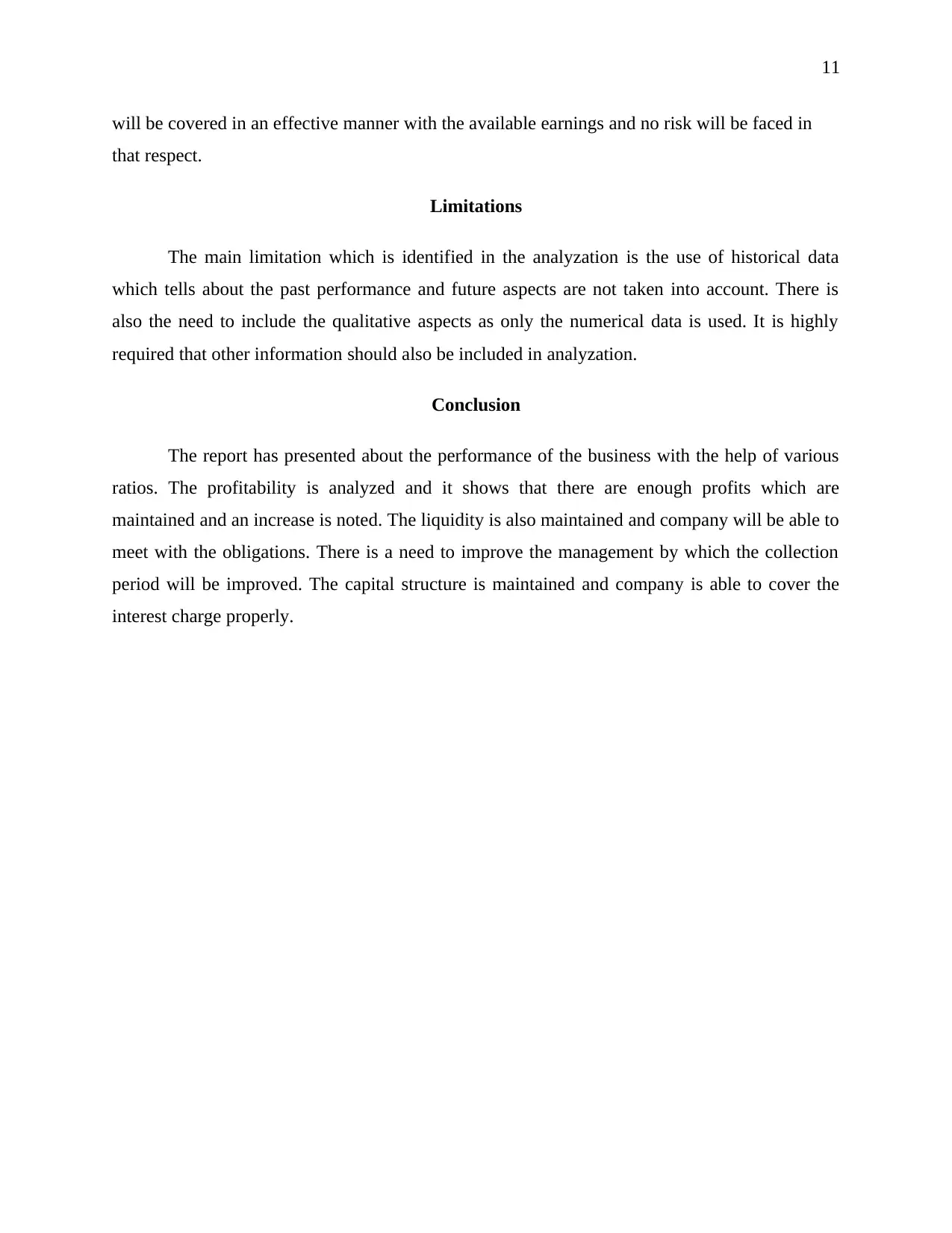

This report presents a comprehensive financial performance analysis of Super Entertainers, evaluating its performance using ratio analysis for the years 2018 and 2019. The analysis covers key areas, including profitability, asset efficiency, liquidity, and capital structure. The report identifies a growing profitability trend, with improvements in return on equity and assets, indicating effective use of resources. Although the company maintains a strong liquidity position, with a high current ratio, operating cash flows are negative. The capital structure is healthy, with higher equity funds compared to debt, resulting in a high solvency ratio. However, the analysis highlights inefficiencies in managing debtors, requiring improvement. The report concludes with limitations, such as the use of historical data and the need for qualitative aspects, and provides references to support the findings. This report provides valuable insights into the financial health and operational efficiency of Super Entertainers.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.