Financial Reporting: Analysis of Financial Performance and Standards

VerifiedAdded on 2021/01/01

|17

|4560

|53

Report

AI Summary

This report provides a comprehensive overview of financial reporting, beginning with an introduction to the process and its importance in organizations. It delves into the requirements, purpose, and key principles of regulatory and conceptual frameworks, followed by an examination of the main stakeholders and their benefits from financial data. The report explores the value of financial data in meeting organizational growth and purpose, detailing various financial statements like profit and loss, changes in equity, financial position, and cash flow. It further analyzes how these statements communicate and interpret financial performance, highlighting the differences between IFRS and IAS, along with the benefits of IFRS and its varying degrees of compliance globally. The report includes financial statements, such as the statement of profit and loss, changes in equity, and statements of financial position, which are crucial for understanding a company's financial health. The analysis of financial statements includes calculations and interpretations of key financial metrics. The report concludes by summarizing the key findings and emphasizes the importance of accurate financial reporting for effective decision-making and organizational success.

Financial Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

1: Financial reporting...................................................................................................................1

2: Requirement, purpose and key principles of regulatory and concept framework...................2

3: Main stakeholders of an organisation and their advantage from financial data......................3

4: Value of financial data for meeting organisational growth and purpose.................................4

5: Financial statements of an organisation...................................................................................5

(a): Statement of profit and loss...................................................................................................5

(b): Changes in equity..................................................................................................................5

(c): Statements of financial position............................................................................................5

(d): Statements of cash-flow statements......................................................................................7

6: The way in which financial statements are used to communicate and interpret financial

performance.................................................................................................................................7

7: Difference between IFRS and IAS..........................................................................................8

8: Benefits of IFRS......................................................................................................................8

9: Varying degree of compliance of with IFRS by organisations across the world....................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

APPENDIX....................................................................................................................................12

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

1: Financial reporting...................................................................................................................1

2: Requirement, purpose and key principles of regulatory and concept framework...................2

3: Main stakeholders of an organisation and their advantage from financial data......................3

4: Value of financial data for meeting organisational growth and purpose.................................4

5: Financial statements of an organisation...................................................................................5

(a): Statement of profit and loss...................................................................................................5

(b): Changes in equity..................................................................................................................5

(c): Statements of financial position............................................................................................5

(d): Statements of cash-flow statements......................................................................................7

6: The way in which financial statements are used to communicate and interpret financial

performance.................................................................................................................................7

7: Difference between IFRS and IAS..........................................................................................8

8: Benefits of IFRS......................................................................................................................8

9: Varying degree of compliance of with IFRS by organisations across the world....................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

APPENDIX....................................................................................................................................12

INTRODUCTION

Financial reporting is a process of recording all the financial activities and position of an

organisation. It is prepared on the basis of relevant information in a well-structured manner and

in a form easy to understand (Mir, 2013). The primary motive of financial reporting is to provide

information regarding the financial position, present position and changes in the financial

position of business organisation like “MARKS AND SPENCER” that is valuable to large

range of users in making effective economic decision. This project report aimed on providing

crucial information regarding the purpose of using financial reporting. Apart from this, analysis

of the financial statement that are prepared by the company during the period. Along with this,

evaluation of financial reporting standard and theoretical model are also covered under this

report. Examination of international difference in financial accounting are identify effectively in

the project.

1: Financial reporting

In every business organisation, it is crucial to make use of reliable reporting systems that

can lead to generation of relevant profit in coming period of time. It is one of the effective

process of producing statements that can disclose “M&S” financial status to the owners and the

government. It is basically a combination of external financial statements such as income

statement, comprehensive statements, balance sheet and changes of stakeholder’s equity. It used

to provide investors, creditors and other business stakeholders an idea of integrity and worth of

the company. This will give crucial information that can be used to make reliable business

decision such as they should open new business with the available resources (Russo, Mitschow

and Schinski, 2015).

As per IASB “M&S” need to formulate financial records to show outcome status of the

company in front of their shareholders. There must be transparency of data can be helpful for the

business entities to deal with business effectively. It is crucial to follow every accounting related

principles, rules and regulation that could be helpful for recording data in different record so that

it should be helpful in depict real position of “M&S”. This company is preparing their financial

reports consistently to operate business at international level (Lu and Fang, 2013).

Purpose:

1

Financial reporting is a process of recording all the financial activities and position of an

organisation. It is prepared on the basis of relevant information in a well-structured manner and

in a form easy to understand (Mir, 2013). The primary motive of financial reporting is to provide

information regarding the financial position, present position and changes in the financial

position of business organisation like “MARKS AND SPENCER” that is valuable to large

range of users in making effective economic decision. This project report aimed on providing

crucial information regarding the purpose of using financial reporting. Apart from this, analysis

of the financial statement that are prepared by the company during the period. Along with this,

evaluation of financial reporting standard and theoretical model are also covered under this

report. Examination of international difference in financial accounting are identify effectively in

the project.

1: Financial reporting

In every business organisation, it is crucial to make use of reliable reporting systems that

can lead to generation of relevant profit in coming period of time. It is one of the effective

process of producing statements that can disclose “M&S” financial status to the owners and the

government. It is basically a combination of external financial statements such as income

statement, comprehensive statements, balance sheet and changes of stakeholder’s equity. It used

to provide investors, creditors and other business stakeholders an idea of integrity and worth of

the company. This will give crucial information that can be used to make reliable business

decision such as they should open new business with the available resources (Russo, Mitschow

and Schinski, 2015).

As per IASB “M&S” need to formulate financial records to show outcome status of the

company in front of their shareholders. There must be transparency of data can be helpful for the

business entities to deal with business effectively. It is crucial to follow every accounting related

principles, rules and regulation that could be helpful for recording data in different record so that

it should be helpful in depict real position of “M&S”. This company is preparing their financial

reports consistently to operate business at international level (Lu and Fang, 2013).

Purpose:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The main objective of the financial reporting is to deliver information regarding the

financial position, performance and changes in financial position of an organisation that is

valuable for an organisation in longer period of time. To help managers of M&S to make

accurate strategic planning so that external stakeholders can increase total sales, profits and

market share in order to gain competitive advantage over other company.

2: Requirement, purpose and key principles of regulatory and concept framework

Conceptual framework is basically an effective type of analytical component with the

motive of variable quantity and certain related textual aspects. It is applied through organisation

when overall performance and status of business is being needed (Lu and Fang, 2013). It is

basically used by most of the companies to make variation and arrange innovative ideas more

effectively. Regulatory framework is the combination of legal obligations and regulations that

are set the by higher authority of UK regarding various companies that are operating in business

environment. According to the law and rules that are implemented in the company is been

required to conducts financial reports for their business because it used to examine actual

position and financial stability of M&S. This is related with the following regulation that are

based on IASB because, it can be helpful the stakeholders to analyse organisational performance

effectively. These rules and regulations are imposed in the specific format of IFRS as mentioned

below:

IFRS: It Stands for International financial reporting standards that are introduced through

IASB. According to this particular body which is responsible for formulating principles and

specific set of regulatory norms. There are certain key principles which are explained below:

IFRS 1: It is associated with the initial implementation of IFRS, under which companies

adopt IFRS for the first time. It would have related directly with M&S to develop with financial

statements effectively.

IFRS 3: This is associated with the combination under which merger and acquisition are

taken into account. It would assist organisation to combine all their assets and liabilities so that

liabilities can be paid to reduce financial losses (Lemieux, 2012).

Purpose of regulatory and conceptual framework:

There is specific objective of regulatory design that is responsible for guiding organisation

towards right direction as it will help in attaining overall aims and objectives of M&S during

future times. The primary purpose of framework is to examine overall performance of a business

2

financial position, performance and changes in financial position of an organisation that is

valuable for an organisation in longer period of time. To help managers of M&S to make

accurate strategic planning so that external stakeholders can increase total sales, profits and

market share in order to gain competitive advantage over other company.

2: Requirement, purpose and key principles of regulatory and concept framework

Conceptual framework is basically an effective type of analytical component with the

motive of variable quantity and certain related textual aspects. It is applied through organisation

when overall performance and status of business is being needed (Lu and Fang, 2013). It is

basically used by most of the companies to make variation and arrange innovative ideas more

effectively. Regulatory framework is the combination of legal obligations and regulations that

are set the by higher authority of UK regarding various companies that are operating in business

environment. According to the law and rules that are implemented in the company is been

required to conducts financial reports for their business because it used to examine actual

position and financial stability of M&S. This is related with the following regulation that are

based on IASB because, it can be helpful the stakeholders to analyse organisational performance

effectively. These rules and regulations are imposed in the specific format of IFRS as mentioned

below:

IFRS: It Stands for International financial reporting standards that are introduced through

IASB. According to this particular body which is responsible for formulating principles and

specific set of regulatory norms. There are certain key principles which are explained below:

IFRS 1: It is associated with the initial implementation of IFRS, under which companies

adopt IFRS for the first time. It would have related directly with M&S to develop with financial

statements effectively.

IFRS 3: This is associated with the combination under which merger and acquisition are

taken into account. It would assist organisation to combine all their assets and liabilities so that

liabilities can be paid to reduce financial losses (Lemieux, 2012).

Purpose of regulatory and conceptual framework:

There is specific objective of regulatory design that is responsible for guiding organisation

towards right direction as it will help in attaining overall aims and objectives of M&S during

future times. The primary purpose of framework is to examine overall performance of a business

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

firms so that stakeholders can take effective decisions regarding the company. There are certain

objectives related with the regulatory and conceptual framework which is related with the

international regulation so that business can be plan their activities more effectively (Singh,

2015).

Quality feature of financial information: There are specific characteristics of financial

data that can assist them to make more reliable decision in coming period of time ( Kimbro and

Xu, 2016). There are certain points:

Relevance: It is most crucial for an organisation to record actual data so that it can assist

them to analyse their actual performance or financial position of the company.

Faithful representation: This is valuable aspects to gain overall trust of stakeholder such

as investors and shareholder because of this they can assure that organisation is in good situation

and can get long term benefits such as higher return on capital investments.

3: Main stakeholders of an organisation and their advantage from financial data

The primary users of financial record are basically said to be more common grouped as

investors and potential investors that are interested in their potential gains and overall security of

their investments. In case of future profits, it can be predicated from the targeted companies past

performance as mentioned in the income statements. Stakeholder are considered as primary

aspects of M&S that are associated with internal and external parties of M&S (Khanzhyn, 2012).

The company is having wide number of stakeholders with the assistance of operating business

more effectively. There are various benefits financial information to stakeholders such as:

Internal stakeholders: These are directly associated with the operation departments of

an organisation. It consists of certain parties that are mentioned below:

Shareholders: They are considered as valuable part of the company as individual that are

providing capital to M&S. Company is entirely relies on their investments through which

future plans can be made accordingly. They can get benefited by the financial

information of dividend reports from which they can ascertain their profitability.

Managers: In M&S, managers can get benefited by using financial information as it

would help them to make valuable decision through analysing the organisational

performance. In case, operations are not in effective manner they can implement

appropriate plan to overcome those issues (Jayasinghe, 2014).

3

objectives related with the regulatory and conceptual framework which is related with the

international regulation so that business can be plan their activities more effectively (Singh,

2015).

Quality feature of financial information: There are specific characteristics of financial

data that can assist them to make more reliable decision in coming period of time ( Kimbro and

Xu, 2016). There are certain points:

Relevance: It is most crucial for an organisation to record actual data so that it can assist

them to analyse their actual performance or financial position of the company.

Faithful representation: This is valuable aspects to gain overall trust of stakeholder such

as investors and shareholder because of this they can assure that organisation is in good situation

and can get long term benefits such as higher return on capital investments.

3: Main stakeholders of an organisation and their advantage from financial data

The primary users of financial record are basically said to be more common grouped as

investors and potential investors that are interested in their potential gains and overall security of

their investments. In case of future profits, it can be predicated from the targeted companies past

performance as mentioned in the income statements. Stakeholder are considered as primary

aspects of M&S that are associated with internal and external parties of M&S (Khanzhyn, 2012).

The company is having wide number of stakeholders with the assistance of operating business

more effectively. There are various benefits financial information to stakeholders such as:

Internal stakeholders: These are directly associated with the operation departments of

an organisation. It consists of certain parties that are mentioned below:

Shareholders: They are considered as valuable part of the company as individual that are

providing capital to M&S. Company is entirely relies on their investments through which

future plans can be made accordingly. They can get benefited by the financial

information of dividend reports from which they can ascertain their profitability.

Managers: In M&S, managers can get benefited by using financial information as it

would help them to make valuable decision through analysing the organisational

performance. In case, operations are not in effective manner they can implement

appropriate plan to overcome those issues (Jayasinghe, 2014).

3

External stakeholders: They are not directly associated with M&S of an organisation but

they are having right option to collect financial data because they are essential part of the

company. some of valuable parts are:

Investors: They are primary part of the group of an individual that invest their money in

M&S projects for the motive of earning maximum profits. They can get benefited from

balance sheet of the organisation as they can ascertain probable return that can be gained

by them.

Creditors: The individual that can provide goods on credits to M&S are considered as

creditors. Financial data can assist them in analysing the organisation performance to pay

back their amount in the given period of time.

4: Value of financial data for meeting organisational growth and purpose

Financial reporting would assist in overall management of organisational performance

that will assist them attaining overall aims and objectives M&S is operating all around the nation

and for which appropriate financial statements so that all the stakeholders of the company which

can get satisfied and show more interest in the company. Objectives of M&S is to attract most of

the investors, satisfy clients and increase profit from the total amount of sales. Most of the

investors used to attract toward maximum return on their overall investments. Customers

satisfaction can be attaining with the help of positive market position which can be determine

through the help of increase revenue for the company for the longer period of time. In case of

M&S is having good image in the market that can help client to satisfied because they can get

assured about the using products of a company.

The organisation is performing good in the market than it will assist them more

competitive in the market and will try to acquire maximum profit for the company. Effective and

accurate financial statements can assist an organisation to examine the overall growth and

opportunity and will make efforts to grab them to attain more competitive benefits in near future

time. For this purpose, finance account of M&S can be right option to analyse the organisation

efficiency and profitability position of the company (Hung, and Chuang, 2012).

Financial statements of M&S can another valuable business that can be examine to

determine financial position in the market in order to assist specific growth in near future time.

The another aspect of this statements is to attain competitive advantage over by measuring the

4

they are having right option to collect financial data because they are essential part of the

company. some of valuable parts are:

Investors: They are primary part of the group of an individual that invest their money in

M&S projects for the motive of earning maximum profits. They can get benefited from

balance sheet of the organisation as they can ascertain probable return that can be gained

by them.

Creditors: The individual that can provide goods on credits to M&S are considered as

creditors. Financial data can assist them in analysing the organisation performance to pay

back their amount in the given period of time.

4: Value of financial data for meeting organisational growth and purpose

Financial reporting would assist in overall management of organisational performance

that will assist them attaining overall aims and objectives M&S is operating all around the nation

and for which appropriate financial statements so that all the stakeholders of the company which

can get satisfied and show more interest in the company. Objectives of M&S is to attract most of

the investors, satisfy clients and increase profit from the total amount of sales. Most of the

investors used to attract toward maximum return on their overall investments. Customers

satisfaction can be attaining with the help of positive market position which can be determine

through the help of increase revenue for the company for the longer period of time. In case of

M&S is having good image in the market that can help client to satisfied because they can get

assured about the using products of a company.

The organisation is performing good in the market than it will assist them more

competitive in the market and will try to acquire maximum profit for the company. Effective and

accurate financial statements can assist an organisation to examine the overall growth and

opportunity and will make efforts to grab them to attain more competitive benefits in near future

time. For this purpose, finance account of M&S can be right option to analyse the organisation

efficiency and profitability position of the company (Hung, and Chuang, 2012).

Financial statements of M&S can another valuable business that can be examine to

determine financial position in the market in order to assist specific growth in near future time.

The another aspect of this statements is to attain competitive advantage over by measuring the

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

strength of the company. By the help of this, company can easily be able to attain maximum

amount of profit in coming period of time.

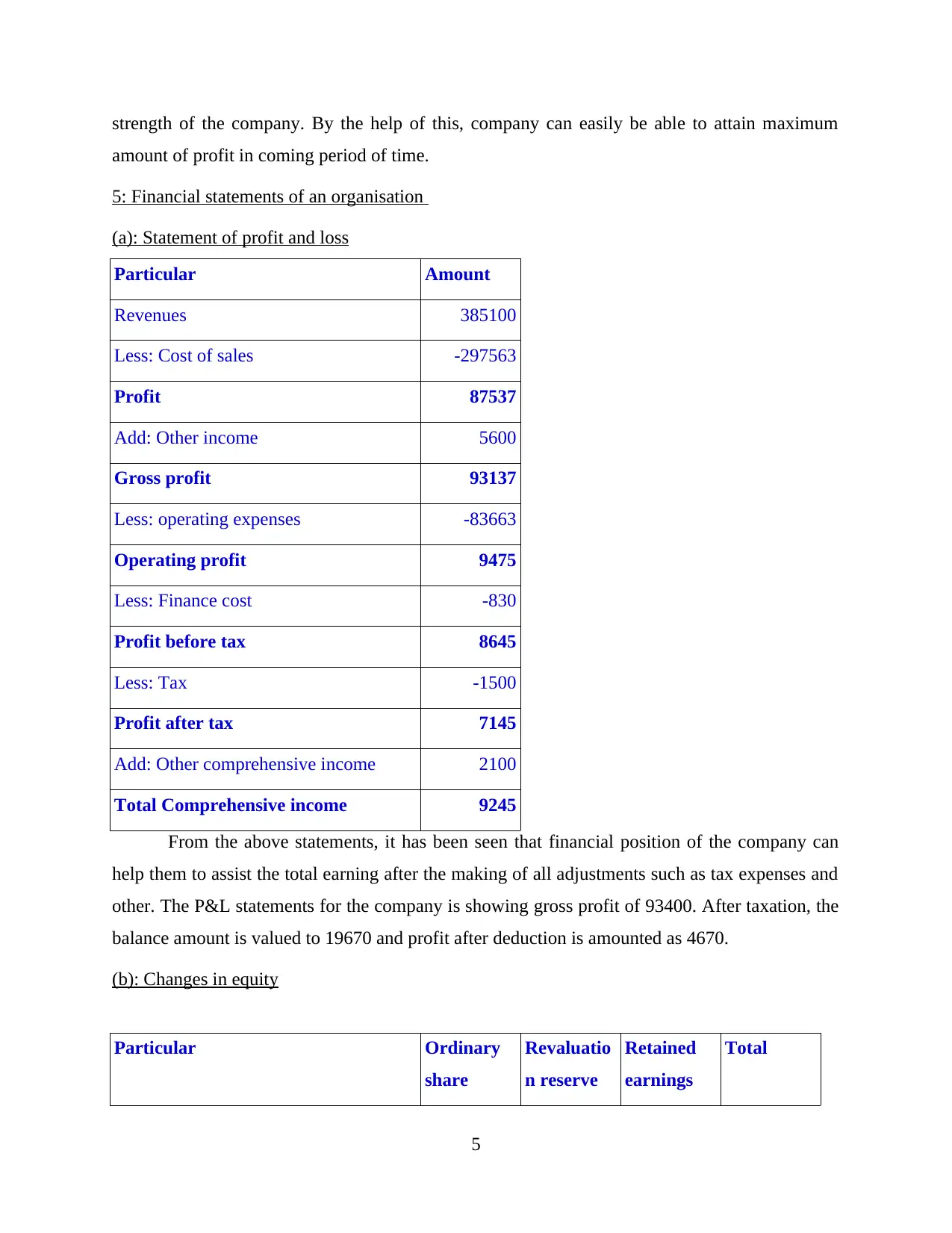

5: Financial statements of an organisation

(a): Statement of profit and loss

Particular Amount

Revenues 385100

Less: Cost of sales -297563

Profit 87537

Add: Other income 5600

Gross profit 93137

Less: operating expenses -83663

Operating profit 9475

Less: Finance cost -830

Profit before tax 8645

Less: Tax -1500

Profit after tax 7145

Add: Other comprehensive income 2100

Total Comprehensive income 9245

From the above statements, it has been seen that financial position of the company can

help them to assist the total earning after the making of all adjustments such as tax expenses and

other. The P&L statements for the company is showing gross profit of 93400. After taxation, the

balance amount is valued to 19670 and profit after deduction is amounted as 4670.

(b): Changes in equity

Particular Ordinary

share

Revaluatio

n reserve

Retained

earnings

Total

5

amount of profit in coming period of time.

5: Financial statements of an organisation

(a): Statement of profit and loss

Particular Amount

Revenues 385100

Less: Cost of sales -297563

Profit 87537

Add: Other income 5600

Gross profit 93137

Less: operating expenses -83663

Operating profit 9475

Less: Finance cost -830

Profit before tax 8645

Less: Tax -1500

Profit after tax 7145

Add: Other comprehensive income 2100

Total Comprehensive income 9245

From the above statements, it has been seen that financial position of the company can

help them to assist the total earning after the making of all adjustments such as tax expenses and

other. The P&L statements for the company is showing gross profit of 93400. After taxation, the

balance amount is valued to 19670 and profit after deduction is amounted as 4670.

(b): Changes in equity

Particular Ordinary

share

Revaluatio

n reserve

Retained

earnings

Total

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

capital

As per trial balance 86700 40700 32100 159500

Total Comprehensive income 2100 7145 9245

Preference dividend -2330 -2330

Ordinary dividend -4340 -4340

86700 42800 32575 162075

(c): Statements of financial position

Assets Amount

Non current assets:

Land and property 115000

Plant and equipment 37275

Investment property 25400

Total non current assets 177675

Current assets:

Inventory 17300

Trade inventories 62000

Total current assets 85300

Total assets 262975

Equities and liabilities

Ordinary Share @25 each 86700

Revaluation reserve 42800

Retained earning 32575

6

As per trial balance 86700 40700 32100 159500

Total Comprehensive income 2100 7145 9245

Preference dividend -2330 -2330

Ordinary dividend -4340 -4340

86700 42800 32575 162075

(c): Statements of financial position

Assets Amount

Non current assets:

Land and property 115000

Plant and equipment 37275

Investment property 25400

Total non current assets 177675

Current assets:

Inventory 17300

Trade inventories 62000

Total current assets 85300

Total assets 262975

Equities and liabilities

Ordinary Share @25 each 86700

Revaluation reserve 42800

Retained earning 32575

6

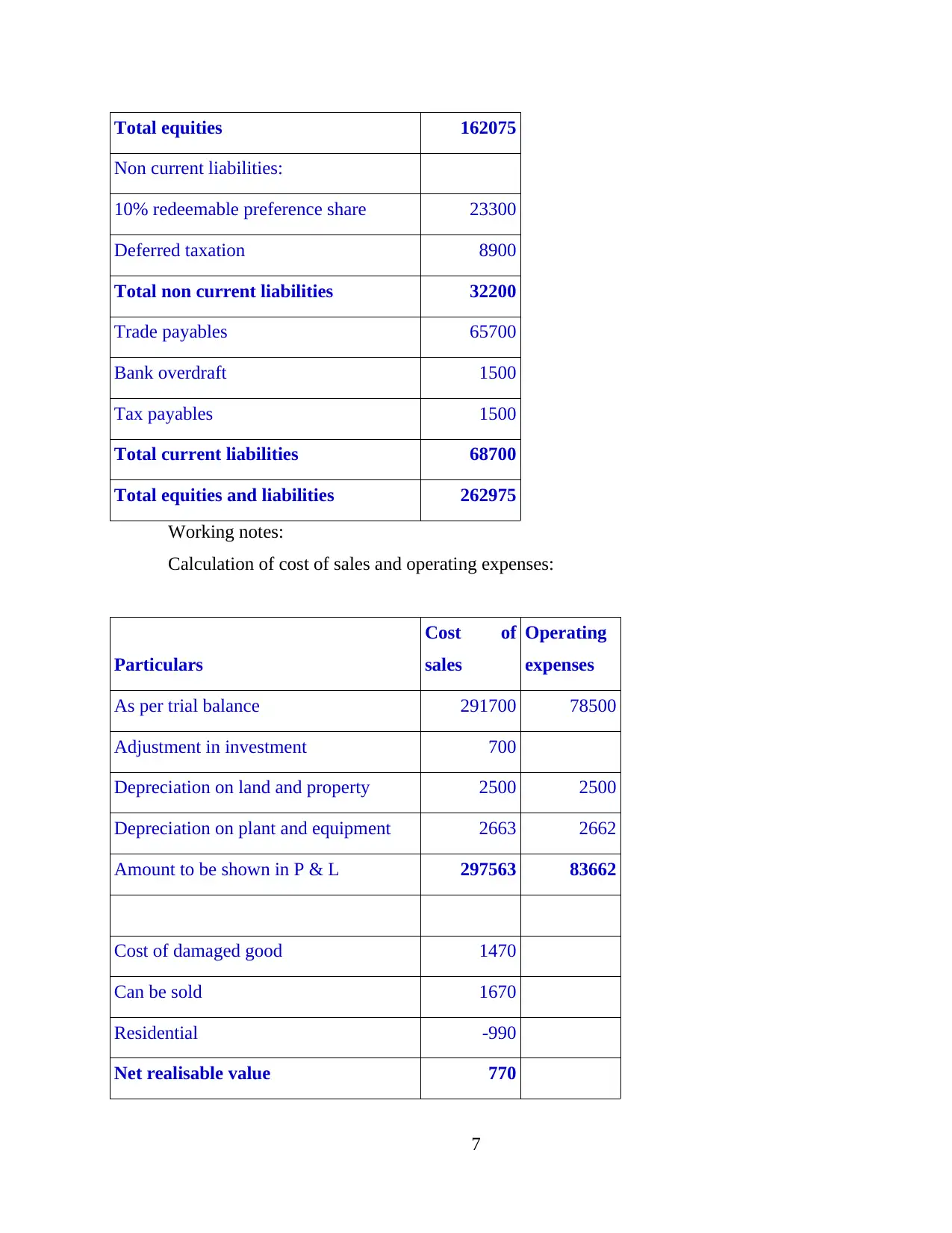

Total equities 162075

Non current liabilities:

10% redeemable preference share 23300

Deferred taxation 8900

Total non current liabilities 32200

Trade payables 65700

Bank overdraft 1500

Tax payables 1500

Total current liabilities 68700

Total equities and liabilities 262975

Working notes:

Calculation of cost of sales and operating expenses:

Particulars

Cost of

sales

Operating

expenses

As per trial balance 291700 78500

Adjustment in investment 700

Depreciation on land and property 2500 2500

Depreciation on plant and equipment 2663 2662

Amount to be shown in P & L 297563 83662

Cost of damaged good 1470

Can be sold 1670

Residential -990

Net realisable value 770

7

Non current liabilities:

10% redeemable preference share 23300

Deferred taxation 8900

Total non current liabilities 32200

Trade payables 65700

Bank overdraft 1500

Tax payables 1500

Total current liabilities 68700

Total equities and liabilities 262975

Working notes:

Calculation of cost of sales and operating expenses:

Particulars

Cost of

sales

Operating

expenses

As per trial balance 291700 78500

Adjustment in investment 700

Depreciation on land and property 2500 2500

Depreciation on plant and equipment 2663 2662

Amount to be shown in P & L 297563 83662

Cost of damaged good 1470

Can be sold 1670

Residential -990

Net realisable value 770

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

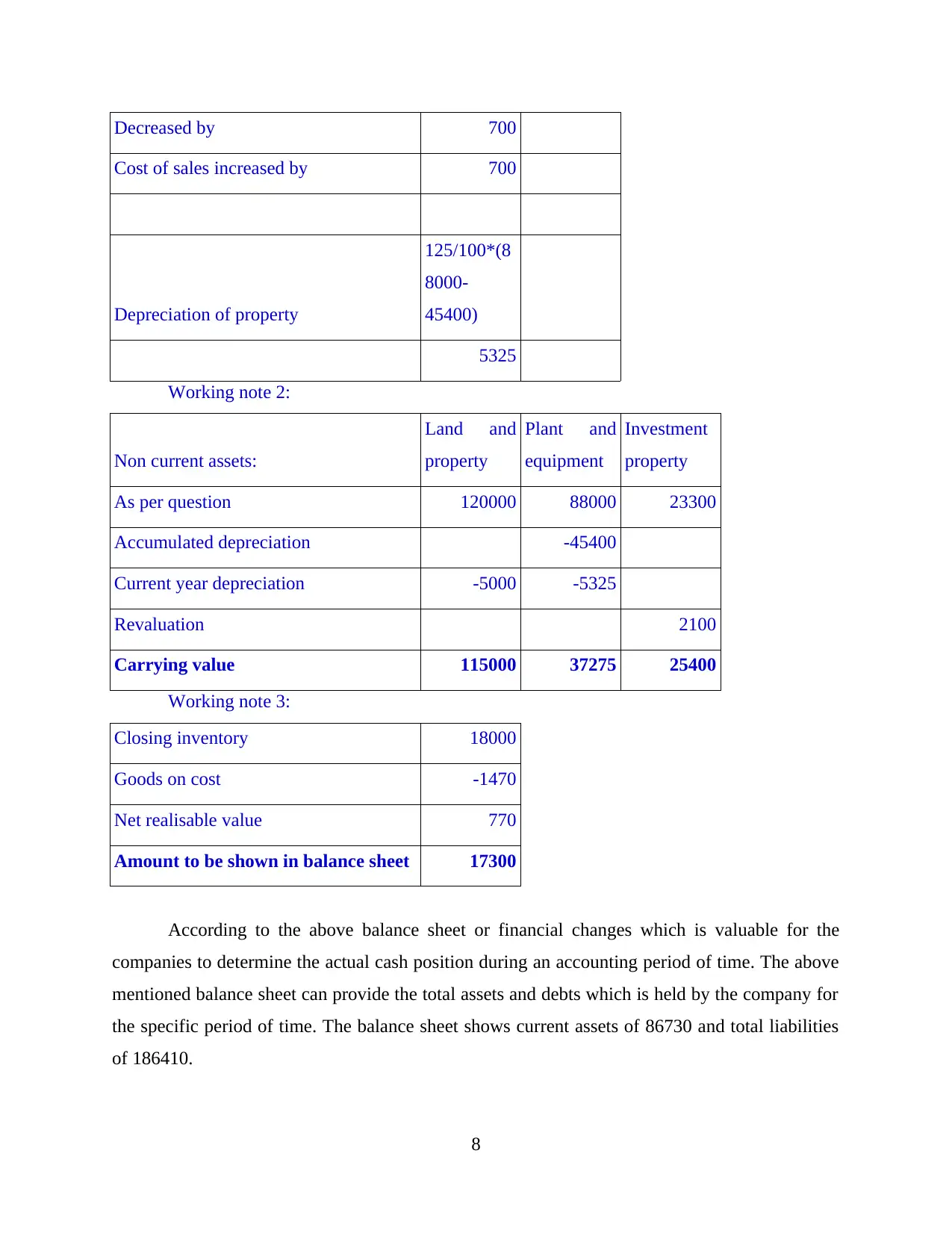

Decreased by 700

Cost of sales increased by 700

Depreciation of property

125/100*(8

8000-

45400)

5325

Working note 2:

Non current assets:

Land and

property

Plant and

equipment

Investment

property

As per question 120000 88000 23300

Accumulated depreciation -45400

Current year depreciation -5000 -5325

Revaluation 2100

Carrying value 115000 37275 25400

Working note 3:

Closing inventory 18000

Goods on cost -1470

Net realisable value 770

Amount to be shown in balance sheet 17300

According to the above balance sheet or financial changes which is valuable for the

companies to determine the actual cash position during an accounting period of time. The above

mentioned balance sheet can provide the total assets and debts which is held by the company for

the specific period of time. The balance sheet shows current assets of 86730 and total liabilities

of 186410.

8

Cost of sales increased by 700

Depreciation of property

125/100*(8

8000-

45400)

5325

Working note 2:

Non current assets:

Land and

property

Plant and

equipment

Investment

property

As per question 120000 88000 23300

Accumulated depreciation -45400

Current year depreciation -5000 -5325

Revaluation 2100

Carrying value 115000 37275 25400

Working note 3:

Closing inventory 18000

Goods on cost -1470

Net realisable value 770

Amount to be shown in balance sheet 17300

According to the above balance sheet or financial changes which is valuable for the

companies to determine the actual cash position during an accounting period of time. The above

mentioned balance sheet can provide the total assets and debts which is held by the company for

the specific period of time. The balance sheet shows current assets of 86730 and total liabilities

of 186410.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(d): Statements of cash-flow statements

In the financial reporting, a cash flow statements shows total changes in overall balance

sheet accounts and profit affects cash and cash equivalents. It would break the analysis down to

operating, investing and financing. The company can use this information for the purpose of

analysing total inflows and outflow. The primary objective of preparing cash flow statements for

a specific period is to show information regarding availability of cash and total amount going out

from the business. Cash flow statement is mentioned in the appendix. The information is related

with the reduction in the capital and expenditure which was partially offset through weaker

business performance with adjusted operating gain down with 94.3 million. Working capital was

internationally flat on the overall year with reduction in clothing and home inventory offset

trough minimising creditors.

6: The way in which financial statements are used to communicate and interpret financial

performance

As analysed form the appendix Revenues of Marks and Spencer for year 2017 were

10622000 and these are increased in year 2018 and reached up to 10698200. Cost of sales for

both the years are 6629300 and 6745600 for year 2017 and 2018 respectively. Gross profit was

reduced up to 3952600 in year 2018 form 3992700 which was for year 2017. Operating period

for both the years are 707300 and 677400 respectively. Net income for the organization were

117100 and 25700 for both the years 2017 and 2018. Cash and cash equivalents of Marks and

Spencer were decreased up to 207700 in year 2018 as compare to 468600 which was for year

2017. Total current assets in year 2017 were 1723300 that are decreased up to 1317900 in year

2018. Long term investment of the organization for year 2017 were 51500 that are decreased in

year 2018. Total assets of the organization were 7550200 in year 2018 and for 2017 there were

8292500. Total liabilities in year 2018 are 4596000 that are decreased as compare to year 2017.

Total shareholder’s equity for year 2017 were 3156300 that are decreased up to 2357500 in year

2018.

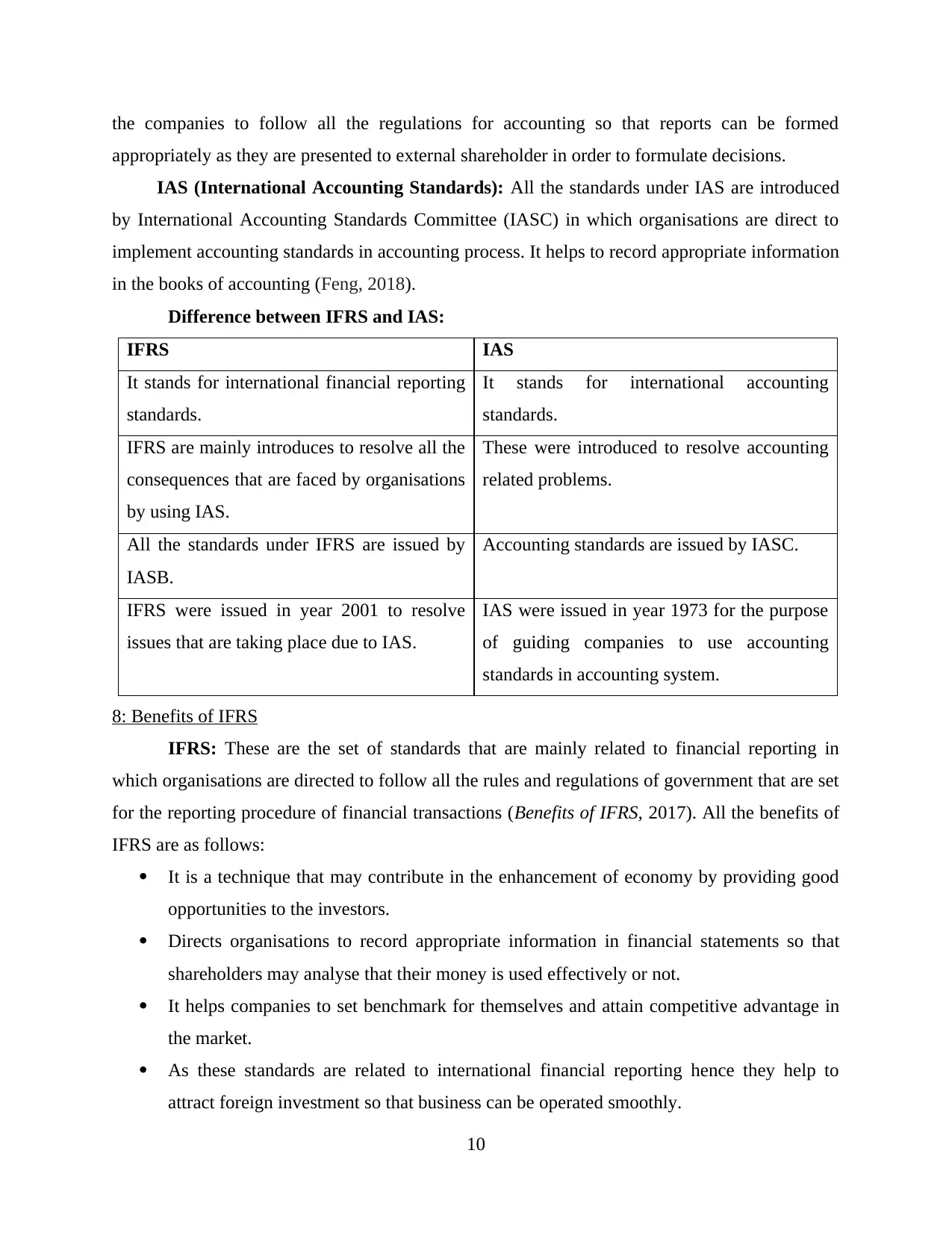

7: Difference between IFRS and IAS

IFRS (International Financial Reporting Standards): These were induced by IASB

which is international accounting standard board that are introduced for the organisations to

provide guidance while recording transactions in financial statements. It is very important for all

9

In the financial reporting, a cash flow statements shows total changes in overall balance

sheet accounts and profit affects cash and cash equivalents. It would break the analysis down to

operating, investing and financing. The company can use this information for the purpose of

analysing total inflows and outflow. The primary objective of preparing cash flow statements for

a specific period is to show information regarding availability of cash and total amount going out

from the business. Cash flow statement is mentioned in the appendix. The information is related

with the reduction in the capital and expenditure which was partially offset through weaker

business performance with adjusted operating gain down with 94.3 million. Working capital was

internationally flat on the overall year with reduction in clothing and home inventory offset

trough minimising creditors.

6: The way in which financial statements are used to communicate and interpret financial

performance

As analysed form the appendix Revenues of Marks and Spencer for year 2017 were

10622000 and these are increased in year 2018 and reached up to 10698200. Cost of sales for

both the years are 6629300 and 6745600 for year 2017 and 2018 respectively. Gross profit was

reduced up to 3952600 in year 2018 form 3992700 which was for year 2017. Operating period

for both the years are 707300 and 677400 respectively. Net income for the organization were

117100 and 25700 for both the years 2017 and 2018. Cash and cash equivalents of Marks and

Spencer were decreased up to 207700 in year 2018 as compare to 468600 which was for year

2017. Total current assets in year 2017 were 1723300 that are decreased up to 1317900 in year

2018. Long term investment of the organization for year 2017 were 51500 that are decreased in

year 2018. Total assets of the organization were 7550200 in year 2018 and for 2017 there were

8292500. Total liabilities in year 2018 are 4596000 that are decreased as compare to year 2017.

Total shareholder’s equity for year 2017 were 3156300 that are decreased up to 2357500 in year

2018.

7: Difference between IFRS and IAS

IFRS (International Financial Reporting Standards): These were induced by IASB

which is international accounting standard board that are introduced for the organisations to

provide guidance while recording transactions in financial statements. It is very important for all

9

the companies to follow all the regulations for accounting so that reports can be formed

appropriately as they are presented to external shareholder in order to formulate decisions.

IAS (International Accounting Standards): All the standards under IAS are introduced

by International Accounting Standards Committee (IASC) in which organisations are direct to

implement accounting standards in accounting process. It helps to record appropriate information

in the books of accounting (Feng, 2018).

Difference between IFRS and IAS:

IFRS IAS

It stands for international financial reporting

standards.

It stands for international accounting

standards.

IFRS are mainly introduces to resolve all the

consequences that are faced by organisations

by using IAS.

These were introduced to resolve accounting

related problems.

All the standards under IFRS are issued by

IASB.

Accounting standards are issued by IASC.

IFRS were issued in year 2001 to resolve

issues that are taking place due to IAS.

IAS were issued in year 1973 for the purpose

of guiding companies to use accounting

standards in accounting system.

8: Benefits of IFRS

IFRS: These are the set of standards that are mainly related to financial reporting in

which organisations are directed to follow all the rules and regulations of government that are set

for the reporting procedure of financial transactions (Benefits of IFRS, 2017). All the benefits of

IFRS are as follows:

It is a technique that may contribute in the enhancement of economy by providing good

opportunities to the investors.

Directs organisations to record appropriate information in financial statements so that

shareholders may analyse that their money is used effectively or not.

It helps companies to set benchmark for themselves and attain competitive advantage in

the market.

As these standards are related to international financial reporting hence they help to

attract foreign investment so that business can be operated smoothly.

10

appropriately as they are presented to external shareholder in order to formulate decisions.

IAS (International Accounting Standards): All the standards under IAS are introduced

by International Accounting Standards Committee (IASC) in which organisations are direct to

implement accounting standards in accounting process. It helps to record appropriate information

in the books of accounting (Feng, 2018).

Difference between IFRS and IAS:

IFRS IAS

It stands for international financial reporting

standards.

It stands for international accounting

standards.

IFRS are mainly introduces to resolve all the

consequences that are faced by organisations

by using IAS.

These were introduced to resolve accounting

related problems.

All the standards under IFRS are issued by

IASB.

Accounting standards are issued by IASC.

IFRS were issued in year 2001 to resolve

issues that are taking place due to IAS.

IAS were issued in year 1973 for the purpose

of guiding companies to use accounting

standards in accounting system.

8: Benefits of IFRS

IFRS: These are the set of standards that are mainly related to financial reporting in

which organisations are directed to follow all the rules and regulations of government that are set

for the reporting procedure of financial transactions (Benefits of IFRS, 2017). All the benefits of

IFRS are as follows:

It is a technique that may contribute in the enhancement of economy by providing good

opportunities to the investors.

Directs organisations to record appropriate information in financial statements so that

shareholders may analyse that their money is used effectively or not.

It helps companies to set benchmark for themselves and attain competitive advantage in

the market.

As these standards are related to international financial reporting hence they help to

attract foreign investment so that business can be operated smoothly.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.