BSc Business Management: Financial Management and Performance Report

VerifiedAdded on 2023/06/05

|10

|2680

|414

Report

AI Summary

This report delves into the core concepts of financial management, emphasizing its critical role in organizational success. It defines financial management as the strategic process of handling an organization's finances, encompassing financing, investing, and dividend distribution. The report examines the importance of financial management, highlighting its role in fund arrangement, utilization, productivity enhancement, and cost reduction. It then discusses key financial statements, including the income statement, balance sheet, cash flow statement, and statement of changes in equity, and explains the use of financial ratios for assessing liquidity, activity, profitability, and solvency. The report presents a case study analysis, providing calculations for the Business Review Template, an income statement, and a balance sheet. It analyzes the company's profitability, liquidity, and efficiency using ratio analysis, interpreting the results and suggesting areas for improvement. Finally, the report suggests strategies like standard costing and disposal of unproductive assets to enhance financial performance, emphasizing the importance of profit generation for long-term sustainability.

BSc (Hons) Business Management with

Foundation

BMP3005

Applied Business Finance

The concept and importance of financial

management and the processes

businesses might use to improve their

financial performance

Submitted by:

Name:

ID:

Contents

Introduction p

0

Foundation

BMP3005

Applied Business Finance

The concept and importance of financial

management and the processes

businesses might use to improve their

financial performance

Submitted by:

Name:

ID:

Contents

Introduction p

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Section 1: Definition and discussion of the concept and

importance of financial management p

Section 2: Description and discussion of the main

financial statements and explain the use of ratios in

financial management

p

Section 3: Using the template provided p-p

i. Completing the Information on the ‘Business Review Template

(Ensure that you display your calculations for this detail)

p

ii. Using Excel producing an Income Statement for the Sample

Organisation (see Case Study). This should be included within

your appendices p

iii. Using Excel completing the Balance Sheet p

iv. Using the Case study information describing the profitability,

liquidity and efficiency of the company based on the results of

ratio analysis p

Section 4: Using examples from the case study describing

and discussing the processes this business might use to

improve their financial performance p

Conclusion p

References

Appendix p

1

importance of financial management p

Section 2: Description and discussion of the main

financial statements and explain the use of ratios in

financial management

p

Section 3: Using the template provided p-p

i. Completing the Information on the ‘Business Review Template

(Ensure that you display your calculations for this detail)

p

ii. Using Excel producing an Income Statement for the Sample

Organisation (see Case Study). This should be included within

your appendices p

iii. Using Excel completing the Balance Sheet p

iv. Using the Case study information describing the profitability,

liquidity and efficiency of the company based on the results of

ratio analysis p

Section 4: Using examples from the case study describing

and discussing the processes this business might use to

improve their financial performance p

Conclusion p

References

Appendix p

1

Introduction

Financial management is a set of practices where by a team of specialists the finance of an

organization is managed. There are number of actions are imparted but the three realms such

as financing, investing and dividend distribution are the activities which are managed. The

report would be covering sort financial statement associated with the undertaken case study

in attempt to fetch deeper understanding (Walmsley, et. al. 2018)

Section 1: Definition and discussion of the concept and

importance of financial management

Financial management can be articulated as the process of management where finance is kept

in center. Over the time, it is experienced that the modern business texture is having great

need to augment the efficiency of finance due to over-competitive market forms. In such

predicaments the sole way to notch up the notion is by enhancing control on finance which is

carried out in the financial management.

At the same time financial management can be defined as the process where all such actions

are taken which are intended to make the finance more performing or effective to the entiy.

With this respect number of actions are taken which are ultimately intended to boost up

overall performance of the entity.

In other words, this is a broad term which is used to reflect the all course of activities which

are imparted by an entity so can enhance the outcomes. Financial management can be

bifurcated in three parts which are accentuated by financial manager so these three segments

are based on three different activities which are characterized as core activities such as-

Financing activities

Investing activities

Dividend related activities

So it would be a fair position to say that financial management plays great role when it comes

to organizational performance. The importance of financial management is as-

Financial management brings better loop over arrangements of funds. It is supposed

to be a tough nut for organizations to arrange funds on time. In this field financial

management gives them upper hand and boost up their capacity.

At once when the funds are arranged then their proper utilization becomes anther

significant point. So to ensure its proper use financial management paves the way

forward.

It improves productivity factor. As it is seen that if there are disarrangements in term

of finance then the possibility of losing potential is quite higher. With the practice of

financial management this jeopardy can be dealt.

With a well-structured financial management, the growth of an organization can be

measured with best fits (Sutarno, et. al. 2019)

Earlier it was supposed that the role of finance management is all about arranging

funds but this idea is no longer there. This is giving wide coverage and making this

action more fruitful to the entity.

Reduction in cost is also possible. Over the period it is experienced that organizations

with better and suitable financial management policies are those having lower

financial cost.

Section 2: Description and discussion of the main

financial statements and explain the use of ratios in

financial management

2

Financial management is a set of practices where by a team of specialists the finance of an

organization is managed. There are number of actions are imparted but the three realms such

as financing, investing and dividend distribution are the activities which are managed. The

report would be covering sort financial statement associated with the undertaken case study

in attempt to fetch deeper understanding (Walmsley, et. al. 2018)

Section 1: Definition and discussion of the concept and

importance of financial management

Financial management can be articulated as the process of management where finance is kept

in center. Over the time, it is experienced that the modern business texture is having great

need to augment the efficiency of finance due to over-competitive market forms. In such

predicaments the sole way to notch up the notion is by enhancing control on finance which is

carried out in the financial management.

At the same time financial management can be defined as the process where all such actions

are taken which are intended to make the finance more performing or effective to the entiy.

With this respect number of actions are taken which are ultimately intended to boost up

overall performance of the entity.

In other words, this is a broad term which is used to reflect the all course of activities which

are imparted by an entity so can enhance the outcomes. Financial management can be

bifurcated in three parts which are accentuated by financial manager so these three segments

are based on three different activities which are characterized as core activities such as-

Financing activities

Investing activities

Dividend related activities

So it would be a fair position to say that financial management plays great role when it comes

to organizational performance. The importance of financial management is as-

Financial management brings better loop over arrangements of funds. It is supposed

to be a tough nut for organizations to arrange funds on time. In this field financial

management gives them upper hand and boost up their capacity.

At once when the funds are arranged then their proper utilization becomes anther

significant point. So to ensure its proper use financial management paves the way

forward.

It improves productivity factor. As it is seen that if there are disarrangements in term

of finance then the possibility of losing potential is quite higher. With the practice of

financial management this jeopardy can be dealt.

With a well-structured financial management, the growth of an organization can be

measured with best fits (Sutarno, et. al. 2019)

Earlier it was supposed that the role of finance management is all about arranging

funds but this idea is no longer there. This is giving wide coverage and making this

action more fruitful to the entity.

Reduction in cost is also possible. Over the period it is experienced that organizations

with better and suitable financial management policies are those having lower

financial cost.

Section 2: Description and discussion of the main

financial statements and explain the use of ratios in

financial management

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial statements can be defied as the statements which are made to articulate or to

present sort of financial information of an organization. For fulfilment of this aim some

reports are prepared. There are number of such statements which are prepared by

organizations but some salient statements are as-

Statement showing financial performance- This is also known Profit and Loss statement.

This statement is used to show the profit and loss status of an entity. This account reflects

both revenues and expenditures in a particular time frame. And on the basis of them the final

status of profit and loss is shown (Hatefi, 2019)

Statement of financial position- This is also known as balance sheet. This is made on

certain date to show the financial position of an organization. With the help of this statement

both assets and liabilities can be traced. At the same time, some better categories such as

short term, and long term assets, liabilities can also be perceived.

Cash flow statement- It is not enough for an organization to be aware of its profits, losses,

assets and liabilities but there is need to understand position of cash. With the progress of

time it is experienced that the cash is one of the most fluctuating aspect. This statement gives

deeper insights of cash flows.

Change in equity- This is the statement which shows the fluctuations in equity aspect. If in a

certain time frame some changes are imparted in equity, then it becomes inevitable to

perceive those changes. This statement fulfils this aim.

Financial accounting is a dynamic practice. With the passing days some new dimensions are

also taking place. Now there is need to be smart enough and brining hyper control on the use

of finance it is quite handy with the use of financial ratios. These rations are helpful in many

ways and paving the way forward. Their uses are as-

Liquidity ratios- It mainly covers current ratio, quick ratio, super quick ratio etc. these ratios

are helpful in understanding liquidity status of an organization. With the help of liquidity

ratios position of current assets, current liabilities can be understood.

Activity ratios- These ratios give deeper insights of organizational activities. There are some

rations such as debtor turnover ratio, creditor and stock turnover ratio etc. by observing these

better control can be set up on organizational activities.

Profitability ratios- Along with observation of liquidity and activity it is also necessary for

an entity to perceive the aspects of profitability. It gives good understanding of GPR, NPR

etc. which can be used as paradigm for performance augmentation.

Solvency ratios- with the help of these financial ratios. An entity may get deeper insights of

organizational ability of paying its long term debt. This is supposed to be very much

significant since in the present market scenario such notions are quite comprehensive.

These ratios bring ability of making comparison. By using them a good comparison is

possible among different aspects which can be ultimately be used in strategic decision

making. These ratios are used by entities to fulfil their aims and objectives. It gives them

ability to make comparison along with some paradigms. They can compare the organizational

performance with the parameters so betterment can be imparted (Prihartono and Asandimitra,

2018)

Section 3: Description and discussion of the main

financial statements and explain the use of ratios in

financial management

3

present sort of financial information of an organization. For fulfilment of this aim some

reports are prepared. There are number of such statements which are prepared by

organizations but some salient statements are as-

Statement showing financial performance- This is also known Profit and Loss statement.

This statement is used to show the profit and loss status of an entity. This account reflects

both revenues and expenditures in a particular time frame. And on the basis of them the final

status of profit and loss is shown (Hatefi, 2019)

Statement of financial position- This is also known as balance sheet. This is made on

certain date to show the financial position of an organization. With the help of this statement

both assets and liabilities can be traced. At the same time, some better categories such as

short term, and long term assets, liabilities can also be perceived.

Cash flow statement- It is not enough for an organization to be aware of its profits, losses,

assets and liabilities but there is need to understand position of cash. With the progress of

time it is experienced that the cash is one of the most fluctuating aspect. This statement gives

deeper insights of cash flows.

Change in equity- This is the statement which shows the fluctuations in equity aspect. If in a

certain time frame some changes are imparted in equity, then it becomes inevitable to

perceive those changes. This statement fulfils this aim.

Financial accounting is a dynamic practice. With the passing days some new dimensions are

also taking place. Now there is need to be smart enough and brining hyper control on the use

of finance it is quite handy with the use of financial ratios. These rations are helpful in many

ways and paving the way forward. Their uses are as-

Liquidity ratios- It mainly covers current ratio, quick ratio, super quick ratio etc. these ratios

are helpful in understanding liquidity status of an organization. With the help of liquidity

ratios position of current assets, current liabilities can be understood.

Activity ratios- These ratios give deeper insights of organizational activities. There are some

rations such as debtor turnover ratio, creditor and stock turnover ratio etc. by observing these

better control can be set up on organizational activities.

Profitability ratios- Along with observation of liquidity and activity it is also necessary for

an entity to perceive the aspects of profitability. It gives good understanding of GPR, NPR

etc. which can be used as paradigm for performance augmentation.

Solvency ratios- with the help of these financial ratios. An entity may get deeper insights of

organizational ability of paying its long term debt. This is supposed to be very much

significant since in the present market scenario such notions are quite comprehensive.

These ratios bring ability of making comparison. By using them a good comparison is

possible among different aspects which can be ultimately be used in strategic decision

making. These ratios are used by entities to fulfil their aims and objectives. It gives them

ability to make comparison along with some paradigms. They can compare the organizational

performance with the parameters so betterment can be imparted (Prihartono and Asandimitra,

2018)

Section 3: Description and discussion of the main

financial statements and explain the use of ratios in

financial management

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

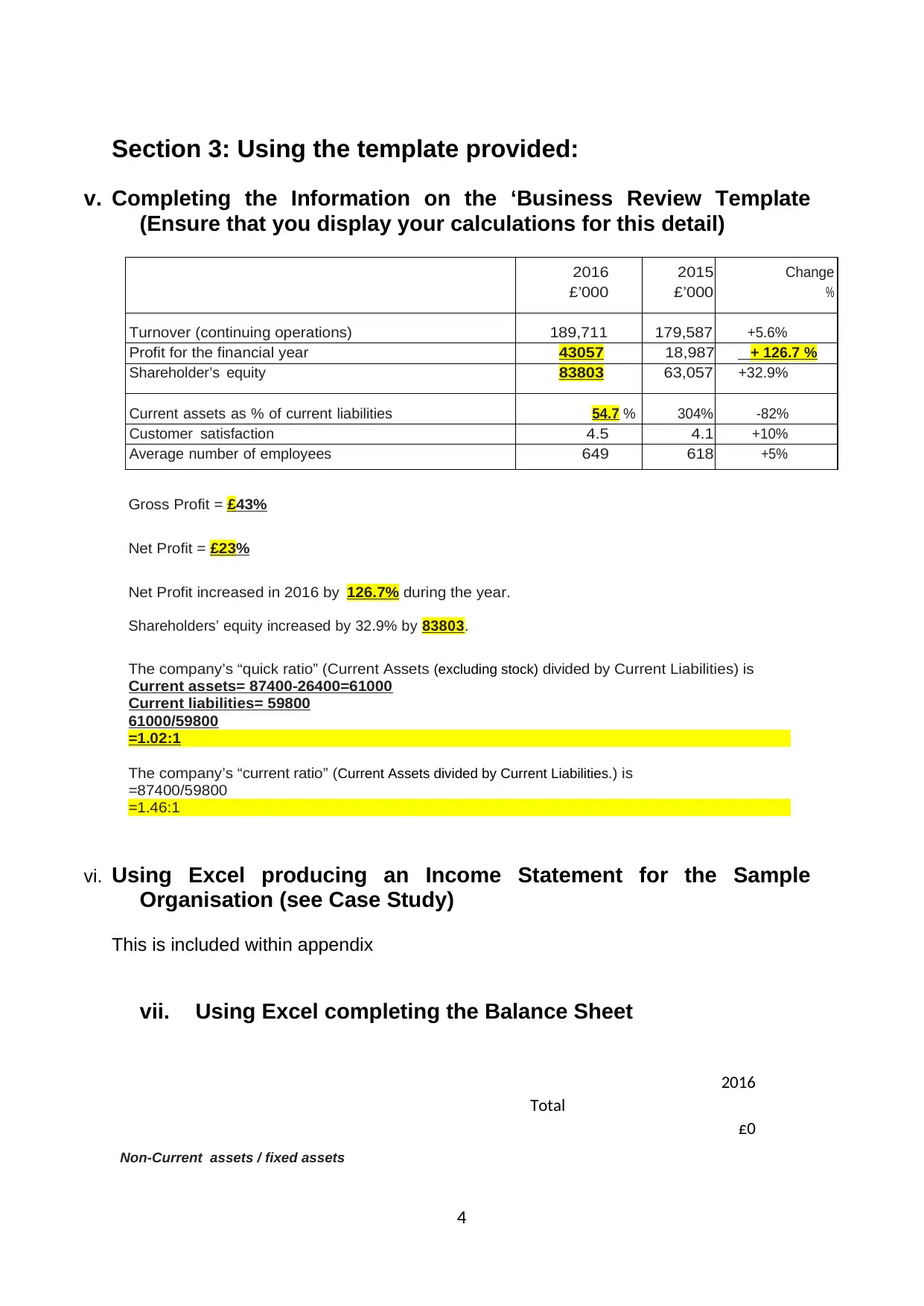

Section 3: Using the template provided:

v. Completing the Information on the ‘Business Review Template

(Ensure that you display your calculations for this detail)

2016

£’000

2015

£’000

Change

%

Turnover (continuing operations) 189,711 179,587 +5.6%

Profit for the financial year 43057 18,987 + 126.7 %

Shareholder’s equity 83803 63,057 +32.9%

Current assets as % of current liabilities 54.7 % 304% -82%

Customer satisfaction 4.5 4.1 +10%

Average number of employees 649 618 +5%

Gross Profit = £43%

Net Profit = £23%

Net Profit increased in 2016 by 126.7% during the year.

Shareholders’ equity increased by 32.9% by 83803.

The company’s “quick ratio” (Current Assets (excluding stock) divided by Current Liabilities) is

Current assets= 87400-26400=61000

Current liabilities= 59800

61000/59800

=1.02:1

The company’s “current ratio” (Current Assets divided by Current Liabilities. ) is

=87400/59800

=1.46:1

vi. Using Excel producing an Income Statement for the Sample

Organisation (see Case Study)

This is included within appendix

vii. Using Excel completing the Balance Sheet

2016

Total

£0

Non-Current assets / fixed assets

4

v. Completing the Information on the ‘Business Review Template

(Ensure that you display your calculations for this detail)

2016

£’000

2015

£’000

Change

%

Turnover (continuing operations) 189,711 179,587 +5.6%

Profit for the financial year 43057 18,987 + 126.7 %

Shareholder’s equity 83803 63,057 +32.9%

Current assets as % of current liabilities 54.7 % 304% -82%

Customer satisfaction 4.5 4.1 +10%

Average number of employees 649 618 +5%

Gross Profit = £43%

Net Profit = £23%

Net Profit increased in 2016 by 126.7% during the year.

Shareholders’ equity increased by 32.9% by 83803.

The company’s “quick ratio” (Current Assets (excluding stock) divided by Current Liabilities) is

Current assets= 87400-26400=61000

Current liabilities= 59800

61000/59800

=1.02:1

The company’s “current ratio” (Current Assets divided by Current Liabilities. ) is

=87400/59800

=1.46:1

vi. Using Excel producing an Income Statement for the Sample

Organisation (see Case Study)

This is included within appendix

vii. Using Excel completing the Balance Sheet

2016

Total

£0

Non-Current assets / fixed assets

4

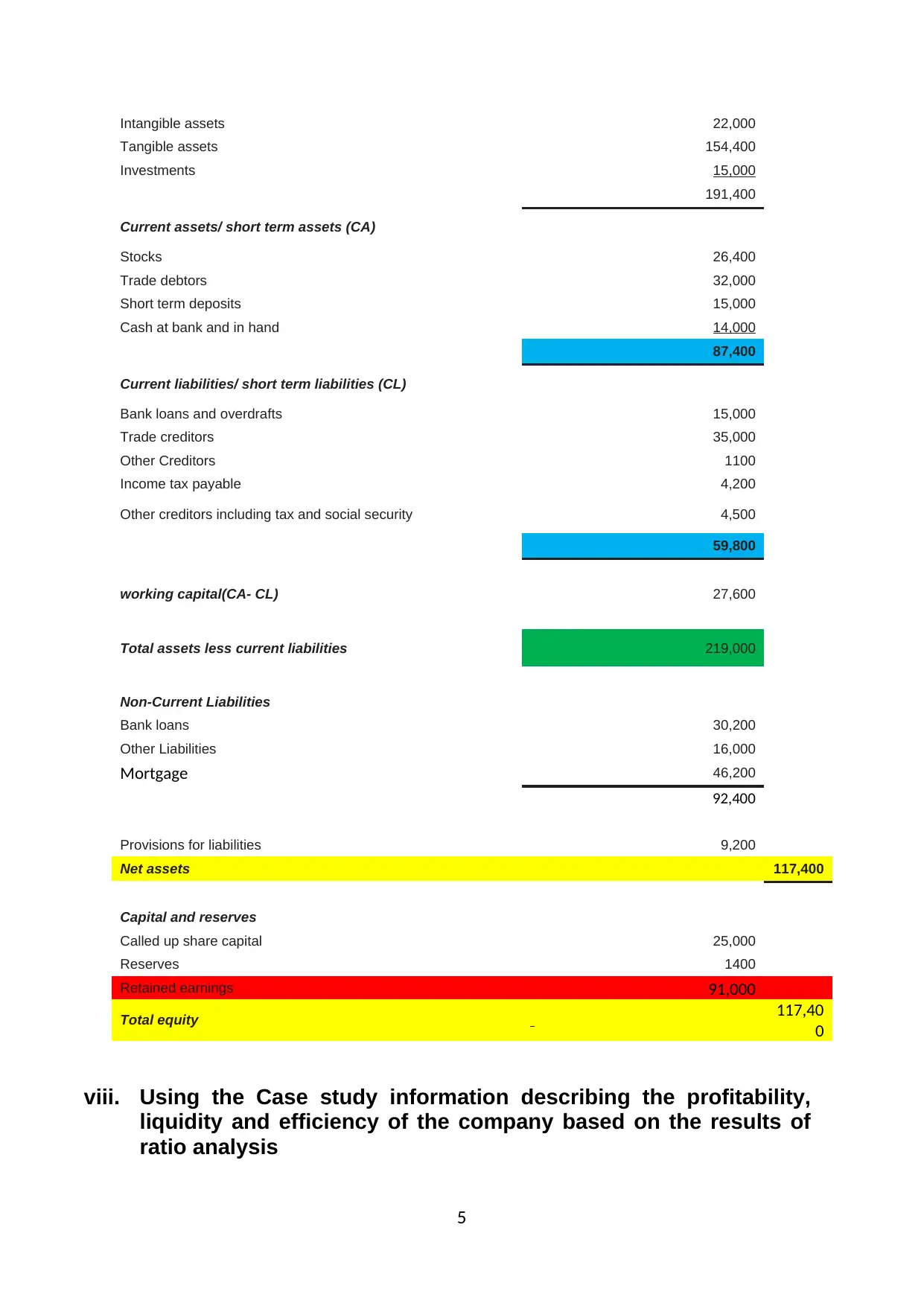

Intangible assets 22,000

Tangible assets 154,400

Investments 15,000

191,400

Current assets/ short term assets (CA)

Stocks 26,400

Trade debtors 32,000

Short term deposits 15,000

Cash at bank and in hand 14,000

87,400

Current liabilities/ short term liabilities (CL)

Bank loans and overdrafts 15,000

Trade creditors 35,000

Other Creditors 1100

Income tax payable 4,200

Other creditors including tax and social security 4,500

59,800

working capital(CA- CL) 27,600

Total assets less current liabilities 219,000

Non-Current Liabilities

Bank loans 30,200

Other Liabilities 16,000

Mortgage 46,200

92,400

Provisions for liabilities 9,200

Net assets 117,400

Capital and reserves

Called up share capital 25,000

Reserves 1400

Retained earnings 91,000

Total equity 117,40

0

viii. Using the Case study information describing the profitability,

liquidity and efficiency of the company based on the results of

ratio analysis

5

Tangible assets 154,400

Investments 15,000

191,400

Current assets/ short term assets (CA)

Stocks 26,400

Trade debtors 32,000

Short term deposits 15,000

Cash at bank and in hand 14,000

87,400

Current liabilities/ short term liabilities (CL)

Bank loans and overdrafts 15,000

Trade creditors 35,000

Other Creditors 1100

Income tax payable 4,200

Other creditors including tax and social security 4,500

59,800

working capital(CA- CL) 27,600

Total assets less current liabilities 219,000

Non-Current Liabilities

Bank loans 30,200

Other Liabilities 16,000

Mortgage 46,200

92,400

Provisions for liabilities 9,200

Net assets 117,400

Capital and reserves

Called up share capital 25,000

Reserves 1400

Retained earnings 91,000

Total equity 117,40

0

viii. Using the Case study information describing the profitability,

liquidity and efficiency of the company based on the results of

ratio analysis

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

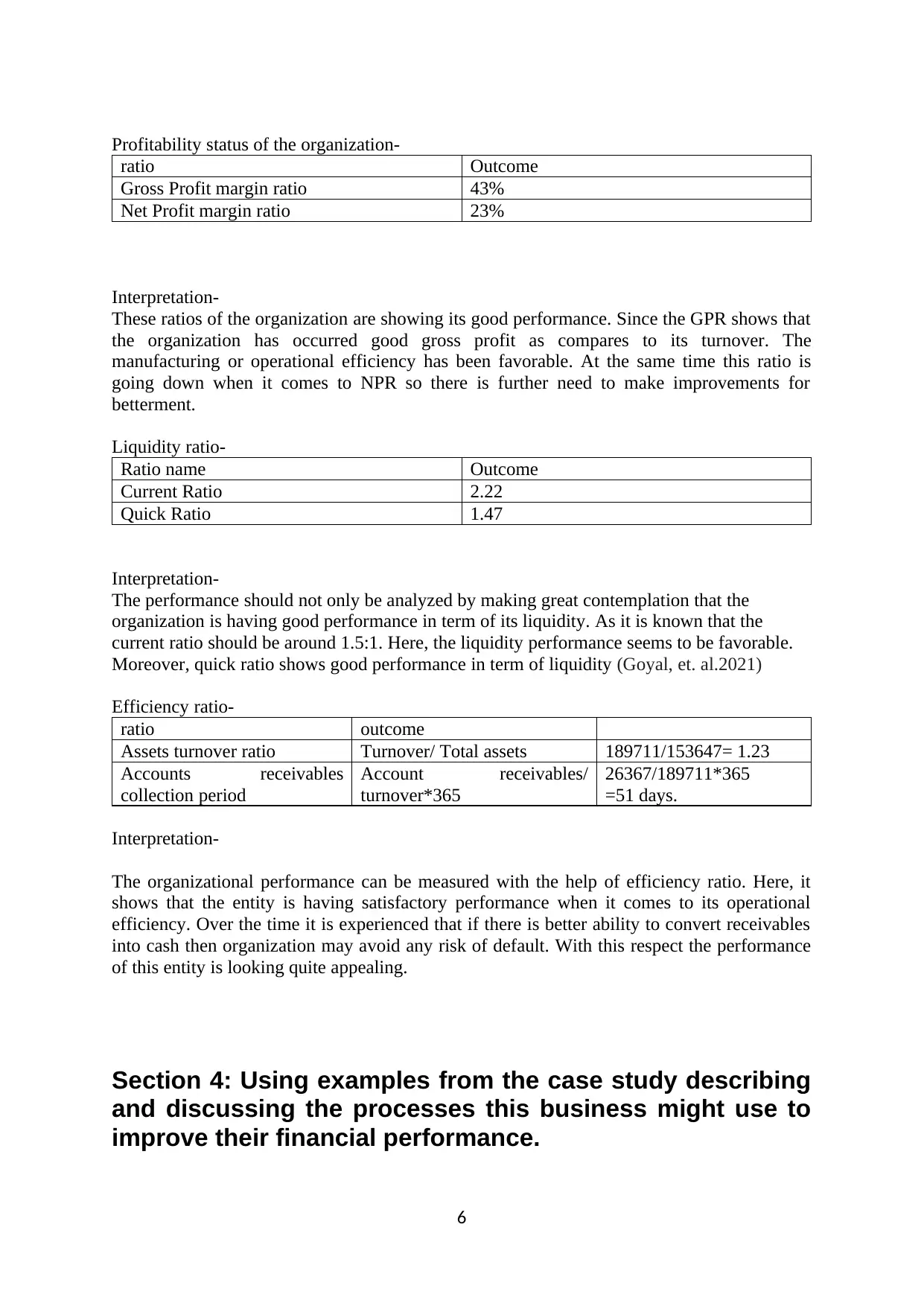

Profitability status of the organization-

ratio Outcome

Gross Profit margin ratio 43%

Net Profit margin ratio 23%

Interpretation-

These ratios of the organization are showing its good performance. Since the GPR shows that

the organization has occurred good gross profit as compares to its turnover. The

manufacturing or operational efficiency has been favorable. At the same time this ratio is

going down when it comes to NPR so there is further need to make improvements for

betterment.

Liquidity ratio-

Ratio name Outcome

Current Ratio 2.22

Quick Ratio 1.47

Interpretation-

The performance should not only be analyzed by making great contemplation that the

organization is having good performance in term of its liquidity. As it is known that the

current ratio should be around 1.5:1. Here, the liquidity performance seems to be favorable.

Moreover, quick ratio shows good performance in term of liquidity (Goyal, et. al.2021)

Efficiency ratio-

ratio outcome

Assets turnover ratio Turnover/ Total assets 189711/153647= 1.23

Accounts receivables

collection period

Account receivables/

turnover*365

26367/189711*365

=51 days.

Interpretation-

The organizational performance can be measured with the help of efficiency ratio. Here, it

shows that the entity is having satisfactory performance when it comes to its operational

efficiency. Over the time it is experienced that if there is better ability to convert receivables

into cash then organization may avoid any risk of default. With this respect the performance

of this entity is looking quite appealing.

Section 4: Using examples from the case study describing

and discussing the processes this business might use to

improve their financial performance.

6

ratio Outcome

Gross Profit margin ratio 43%

Net Profit margin ratio 23%

Interpretation-

These ratios of the organization are showing its good performance. Since the GPR shows that

the organization has occurred good gross profit as compares to its turnover. The

manufacturing or operational efficiency has been favorable. At the same time this ratio is

going down when it comes to NPR so there is further need to make improvements for

betterment.

Liquidity ratio-

Ratio name Outcome

Current Ratio 2.22

Quick Ratio 1.47

Interpretation-

The performance should not only be analyzed by making great contemplation that the

organization is having good performance in term of its liquidity. As it is known that the

current ratio should be around 1.5:1. Here, the liquidity performance seems to be favorable.

Moreover, quick ratio shows good performance in term of liquidity (Goyal, et. al.2021)

Efficiency ratio-

ratio outcome

Assets turnover ratio Turnover/ Total assets 189711/153647= 1.23

Accounts receivables

collection period

Account receivables/

turnover*365

26367/189711*365

=51 days.

Interpretation-

The organizational performance can be measured with the help of efficiency ratio. Here, it

shows that the entity is having satisfactory performance when it comes to its operational

efficiency. Over the time it is experienced that if there is better ability to convert receivables

into cash then organization may avoid any risk of default. With this respect the performance

of this entity is looking quite appealing.

Section 4: Using examples from the case study describing

and discussing the processes this business might use to

improve their financial performance.

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The organizational performance is satisfactory yet there is need to bring some better practices in

order to be highly productive and eradiating all the potential troubles which may bring severe

catastrophe to it in the future-

Standard costing- this is the method which might be used in order to reduce or control the cost

factor. As in the case it was found there were issues pertaining to overhead control. This is a tough

nut to crack. So this technique is quite helpful since with the help of standard costing separate

attention can be paid to all material, labor and overhead costs.

Disposal of worthless resources- As it is seen that there are some factors which are making

organization underperformed. So the only way to deal with this problem is to dispose some

unproductive or less productive assets so can enhance the performance (Kuo, 2019)

Transactional strategies- For instance- the organization is supposed to make some drastic

decisions so can boost up its profits. Since profits are nothing but bloodline of any organization. If

an entity is not generating good profits, then it cannot be sustained in the present cut throat

market. Some discount offers, bonus, coupon can be introduced it would be making the walk

simpler and the entity will be able to hike its profitability.

Strong Inventory Management System- There may be a good inventory management

system which can be used since if an entity is not able to control its inventory to the fullest

extent then would not be able to reduce the waste and would also be occurring some

additional costs. As in this case the entity is generating GP of 43% but when it comes to NP

then they are having around 23% so it shows there is rigors need to work on operational

realm. This technique will be helping in that manner (Shim, 2022)

Conclusion

From the report above it can be twigged that the role of financial management is quite higher

in an organization. The report has presented greater insights of the usefulness or importance it

bears. Range of rations and their usefulness had been described. At the same time, the case

study was undertaken to reflect better understanding pertaining financial management.

7

order to be highly productive and eradiating all the potential troubles which may bring severe

catastrophe to it in the future-

Standard costing- this is the method which might be used in order to reduce or control the cost

factor. As in the case it was found there were issues pertaining to overhead control. This is a tough

nut to crack. So this technique is quite helpful since with the help of standard costing separate

attention can be paid to all material, labor and overhead costs.

Disposal of worthless resources- As it is seen that there are some factors which are making

organization underperformed. So the only way to deal with this problem is to dispose some

unproductive or less productive assets so can enhance the performance (Kuo, 2019)

Transactional strategies- For instance- the organization is supposed to make some drastic

decisions so can boost up its profits. Since profits are nothing but bloodline of any organization. If

an entity is not generating good profits, then it cannot be sustained in the present cut throat

market. Some discount offers, bonus, coupon can be introduced it would be making the walk

simpler and the entity will be able to hike its profitability.

Strong Inventory Management System- There may be a good inventory management

system which can be used since if an entity is not able to control its inventory to the fullest

extent then would not be able to reduce the waste and would also be occurring some

additional costs. As in this case the entity is generating GP of 43% but when it comes to NP

then they are having around 23% so it shows there is rigors need to work on operational

realm. This technique will be helping in that manner (Shim, 2022)

Conclusion

From the report above it can be twigged that the role of financial management is quite higher

in an organization. The report has presented greater insights of the usefulness or importance it

bears. Range of rations and their usefulness had been described. At the same time, the case

study was undertaken to reflect better understanding pertaining financial management.

7

References

Walmsley, T. G., et. al. 2018. Energy Ratio analysis and accounting for renewable and non-

renewable electricity generation: A review. Renewable and Sustainable Energy

Reviews, 98, pp.328-345.

Sutarno, S., et. al. 2019, December. Implementation of Multi-Objective Optimazation on the

Base of Ratio Analysis (MOORA) in Improving Support for Decision on Sales

Location Determination. In Journal of Physics: Conference Series (Vol. 1424, No.

1, p. 012019). IOP Publishing.

Hatefi, M. A., 2019. Indifference threshold-based attribute ratio analysis: A method for

assigning the weights to the attributes in multiple attribute decision

making. Applied Soft Computing, 74, pp.643-651.

Prihartono, M. R. D. and Asandimitra, N., 2018. Analysis factors influencing financial

management behaviour. International Journal of Academic Research in Business

and Social Sciences, 8(8), pp.308-326.

Goyal, K., et. al.2021. Antecedents and consequences of Personal Financial Management

Behavior: a systematic literature review and future research agenda. International

Journal of Bank Marketing.

Kuo, W., 2019. International financial management.

Shim, J. K., 2022. Financial management. Professor of Finance and Accounting Queens

College City University of New York.

Appendix:

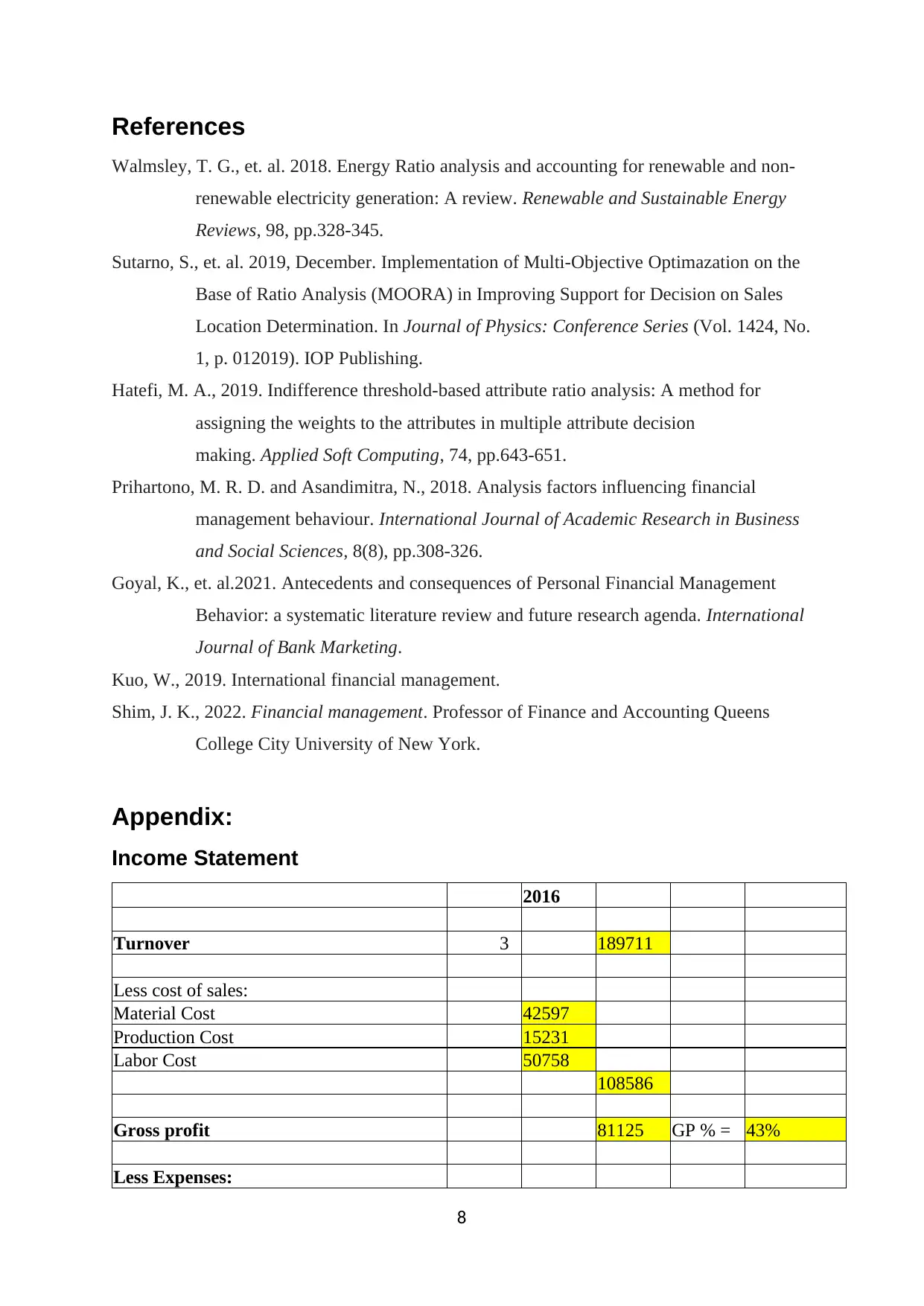

Income Statement

2016

Turnover 3 189711

Less cost of sales:

Material Cost 42597

Production Cost 15231

Labor Cost 50758

108586

Gross profit 81125 GP % = 43%

Less Expenses:

8

Walmsley, T. G., et. al. 2018. Energy Ratio analysis and accounting for renewable and non-

renewable electricity generation: A review. Renewable and Sustainable Energy

Reviews, 98, pp.328-345.

Sutarno, S., et. al. 2019, December. Implementation of Multi-Objective Optimazation on the

Base of Ratio Analysis (MOORA) in Improving Support for Decision on Sales

Location Determination. In Journal of Physics: Conference Series (Vol. 1424, No.

1, p. 012019). IOP Publishing.

Hatefi, M. A., 2019. Indifference threshold-based attribute ratio analysis: A method for

assigning the weights to the attributes in multiple attribute decision

making. Applied Soft Computing, 74, pp.643-651.

Prihartono, M. R. D. and Asandimitra, N., 2018. Analysis factors influencing financial

management behaviour. International Journal of Academic Research in Business

and Social Sciences, 8(8), pp.308-326.

Goyal, K., et. al.2021. Antecedents and consequences of Personal Financial Management

Behavior: a systematic literature review and future research agenda. International

Journal of Bank Marketing.

Kuo, W., 2019. International financial management.

Shim, J. K., 2022. Financial management. Professor of Finance and Accounting Queens

College City University of New York.

Appendix:

Income Statement

2016

Turnover 3 189711

Less cost of sales:

Material Cost 42597

Production Cost 15231

Labor Cost 50758

108586

Gross profit 81125 GP % = 43%

Less Expenses:

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

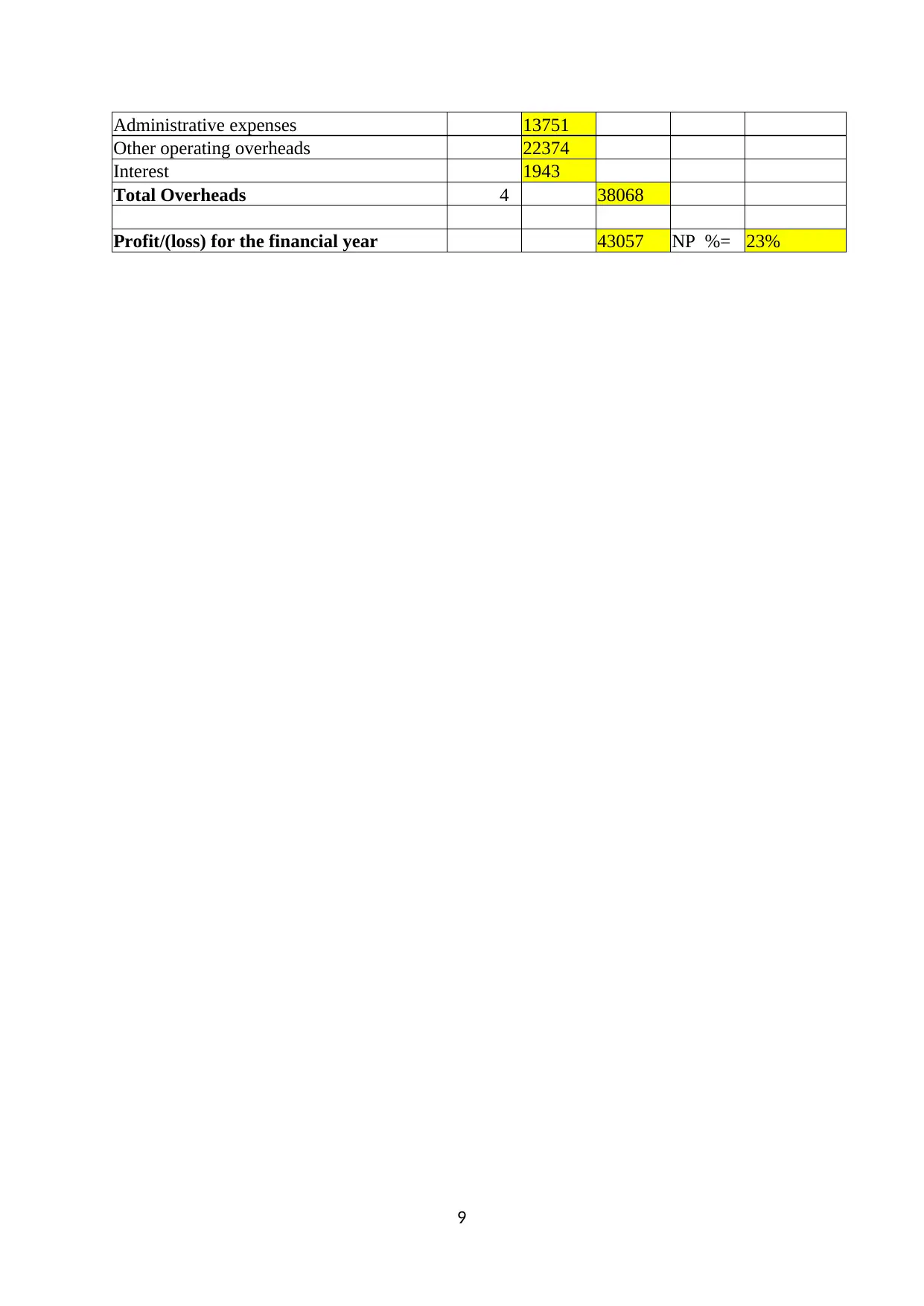

Administrative expenses 13751

Other operating overheads 22374

Interest 1943

Total Overheads 4 38068

Profit/(loss) for the financial year 43057 NP %= 23%

9

Other operating overheads 22374

Interest 1943

Total Overheads 4 38068

Profit/(loss) for the financial year 43057 NP %= 23%

9

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.