Auditing and Assurance: Financial Analysis of Temple & Webster Group

VerifiedAdded on 2023/06/10

|5

|933

|128

Report

AI Summary

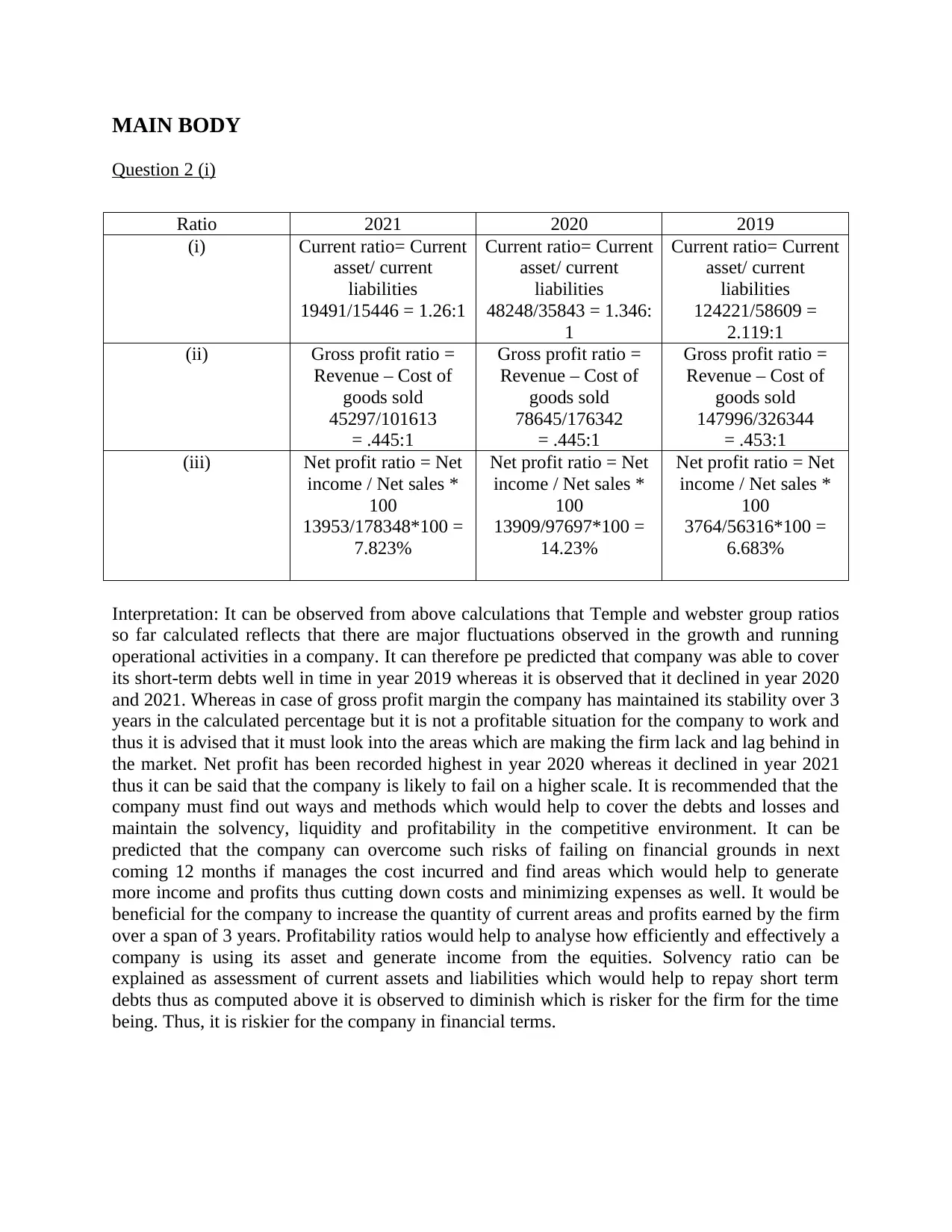

This report presents a financial analysis of Temple & Webster Group, focusing on auditing and assurance principles. The analysis includes a detailed examination of key financial ratios, such as current, gross profit, and net profit ratios, over a three-year period (2019-2021). The report interprets these ratios to assess the company's financial performance, identifying trends in solvency, liquidity, and profitability. Furthermore, it highlights two key accounts – revenue and fixed assets – and discusses their potential risks of material misstatement. The report recommends strategies to improve financial stability and performance, emphasizing the importance of managing costs, generating income, and maintaining the asset lifecycle.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.