Business Planning: Budgeted vs. Actual Financial Statement Analysis

VerifiedAdded on 2023/06/18

|14

|2157

|457

Practical Assignment

AI Summary

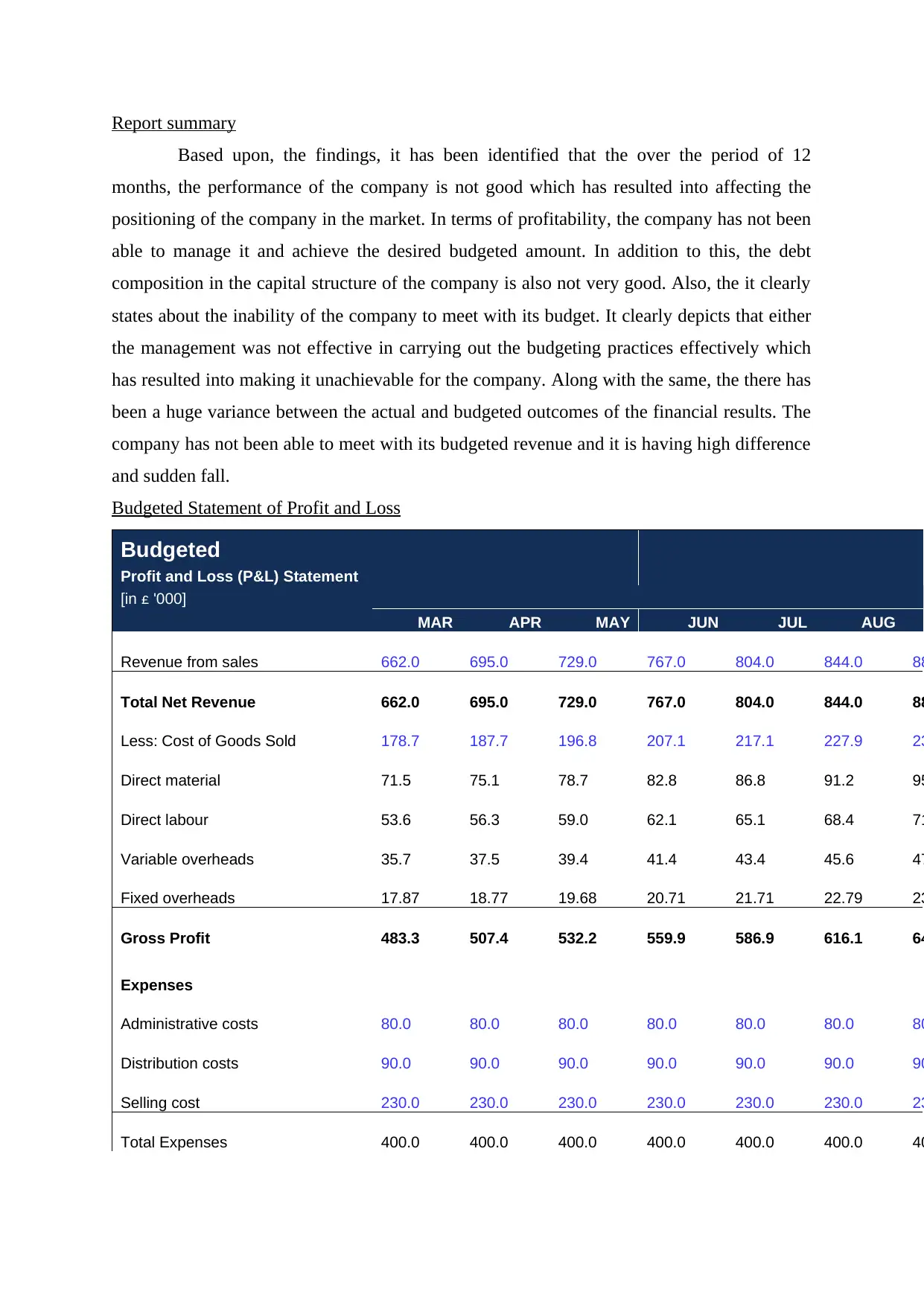

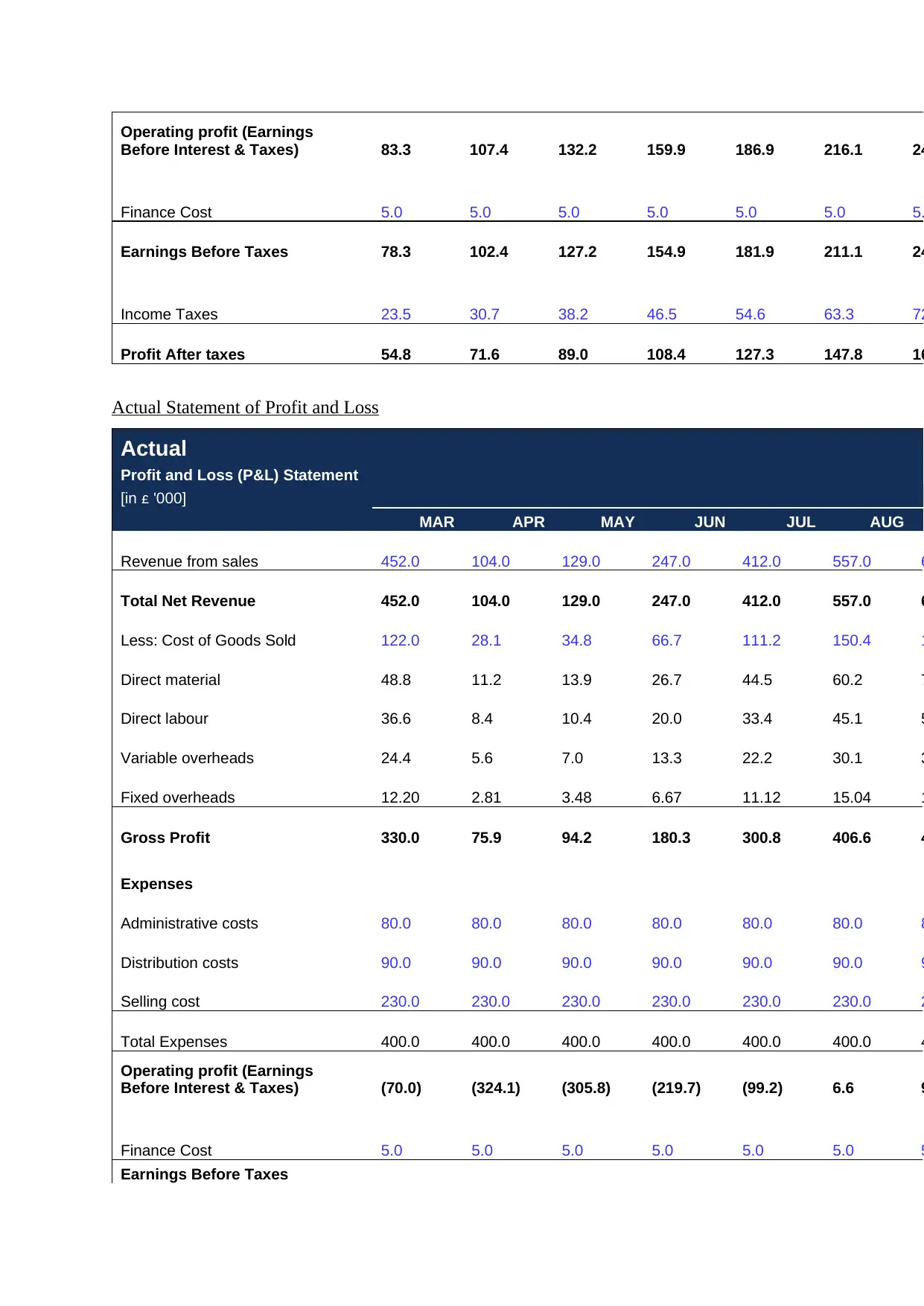

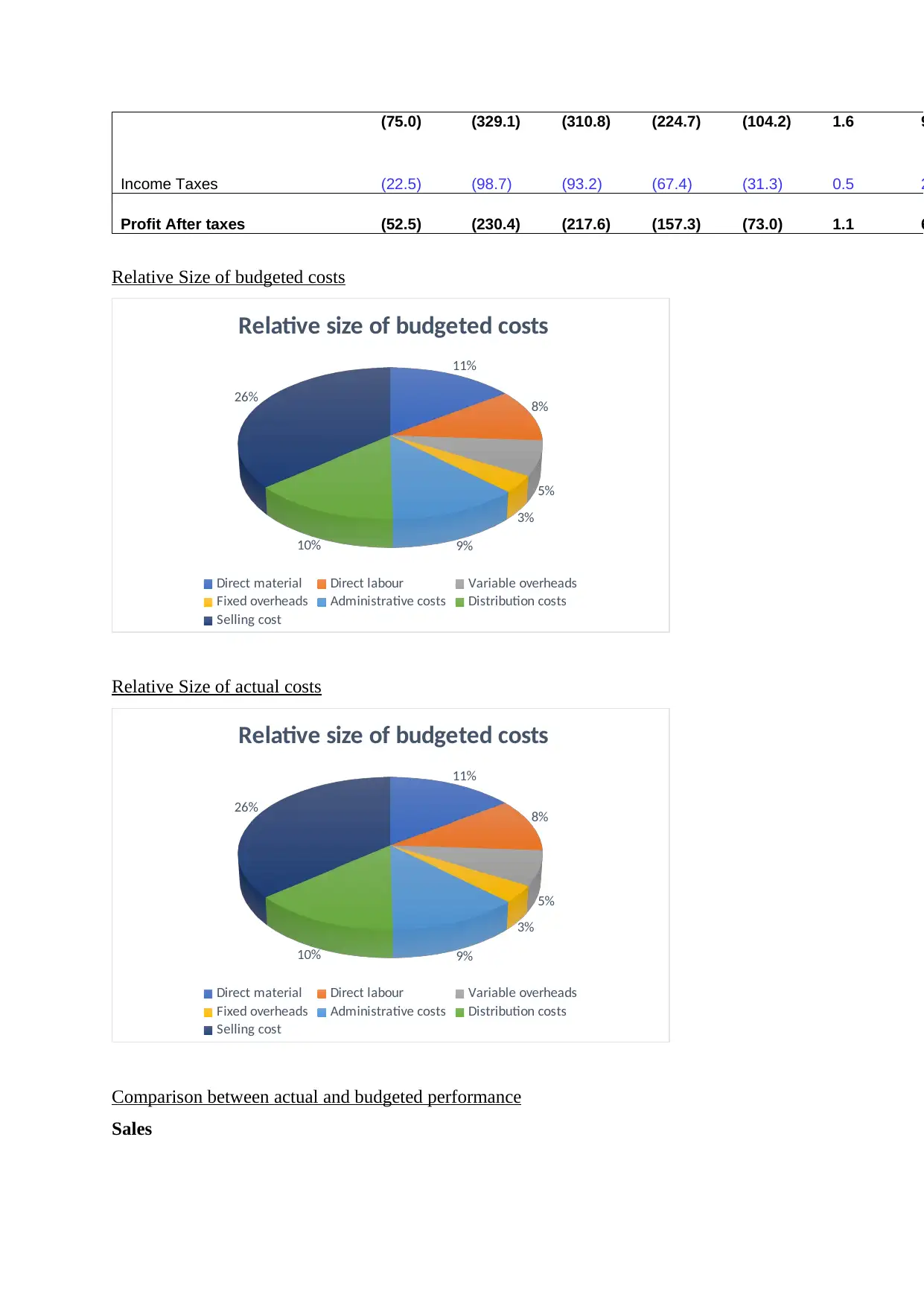

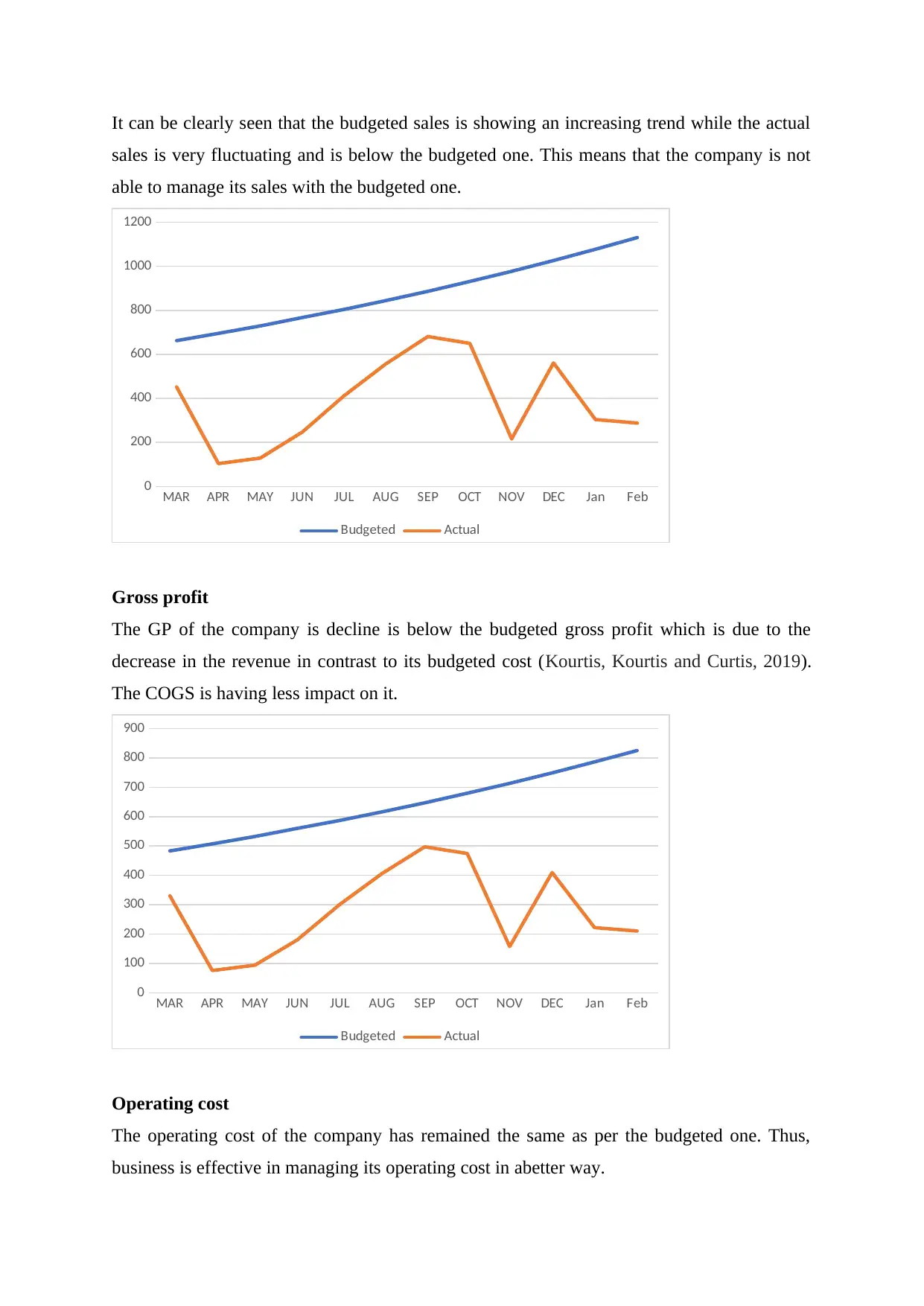

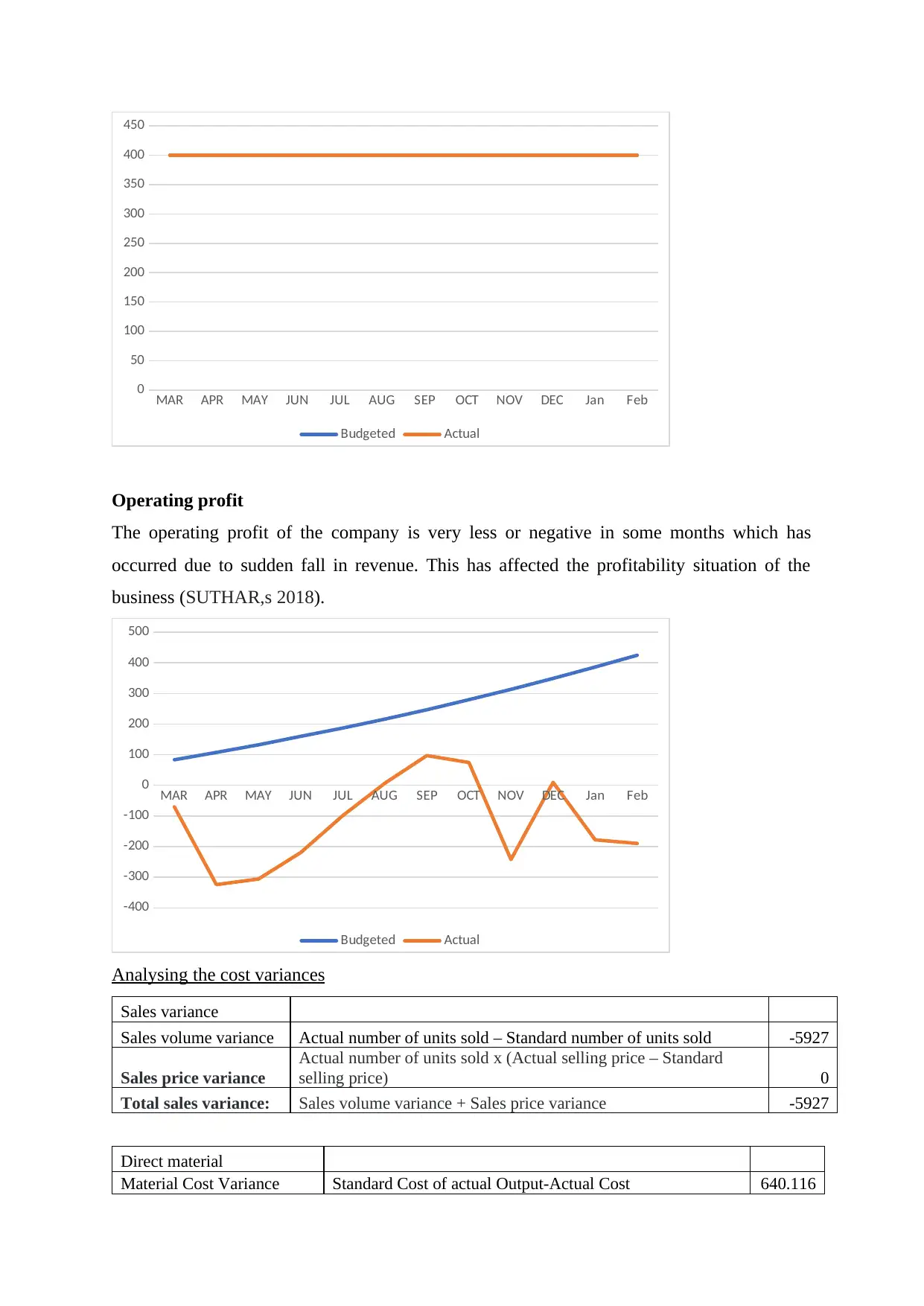

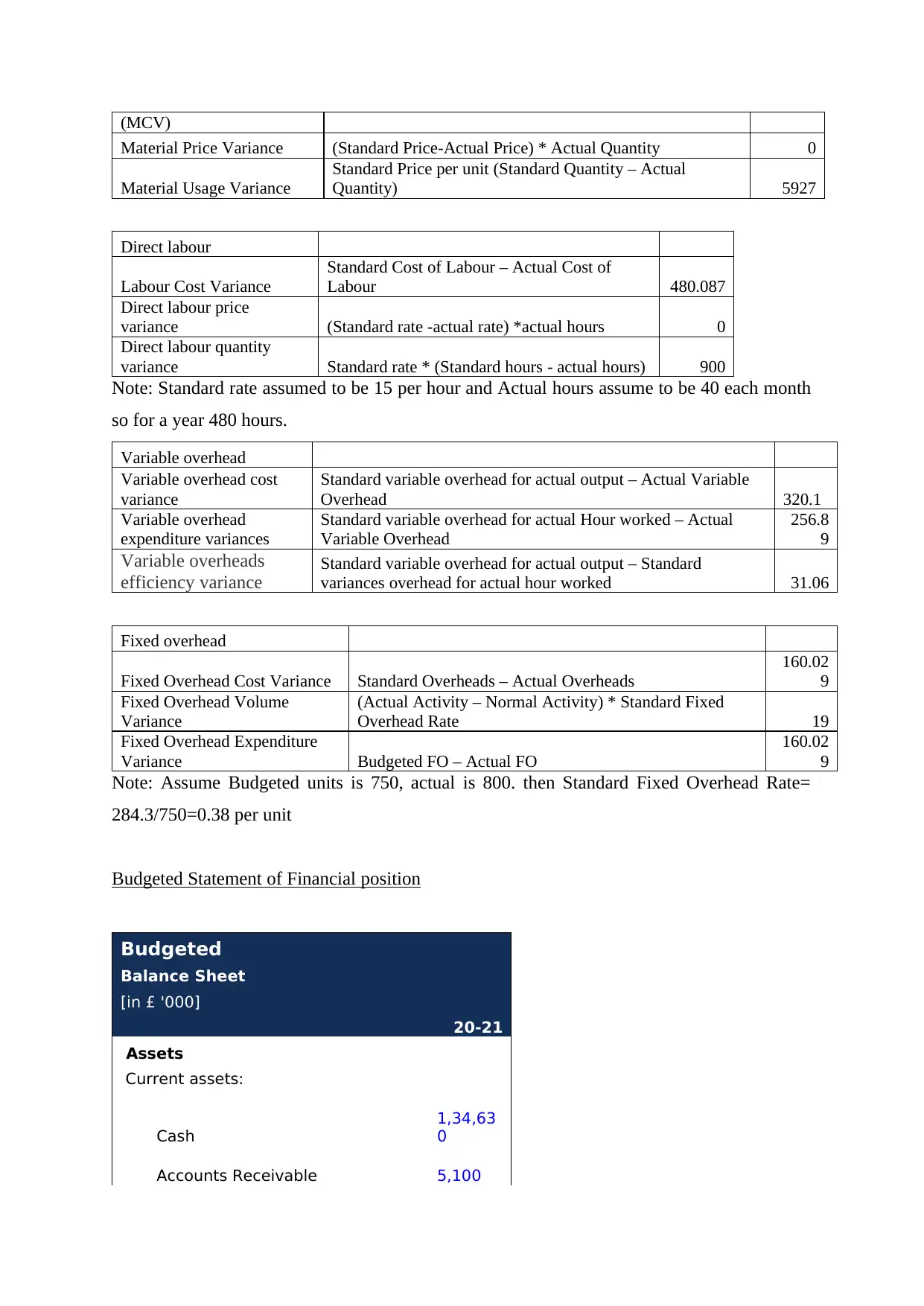

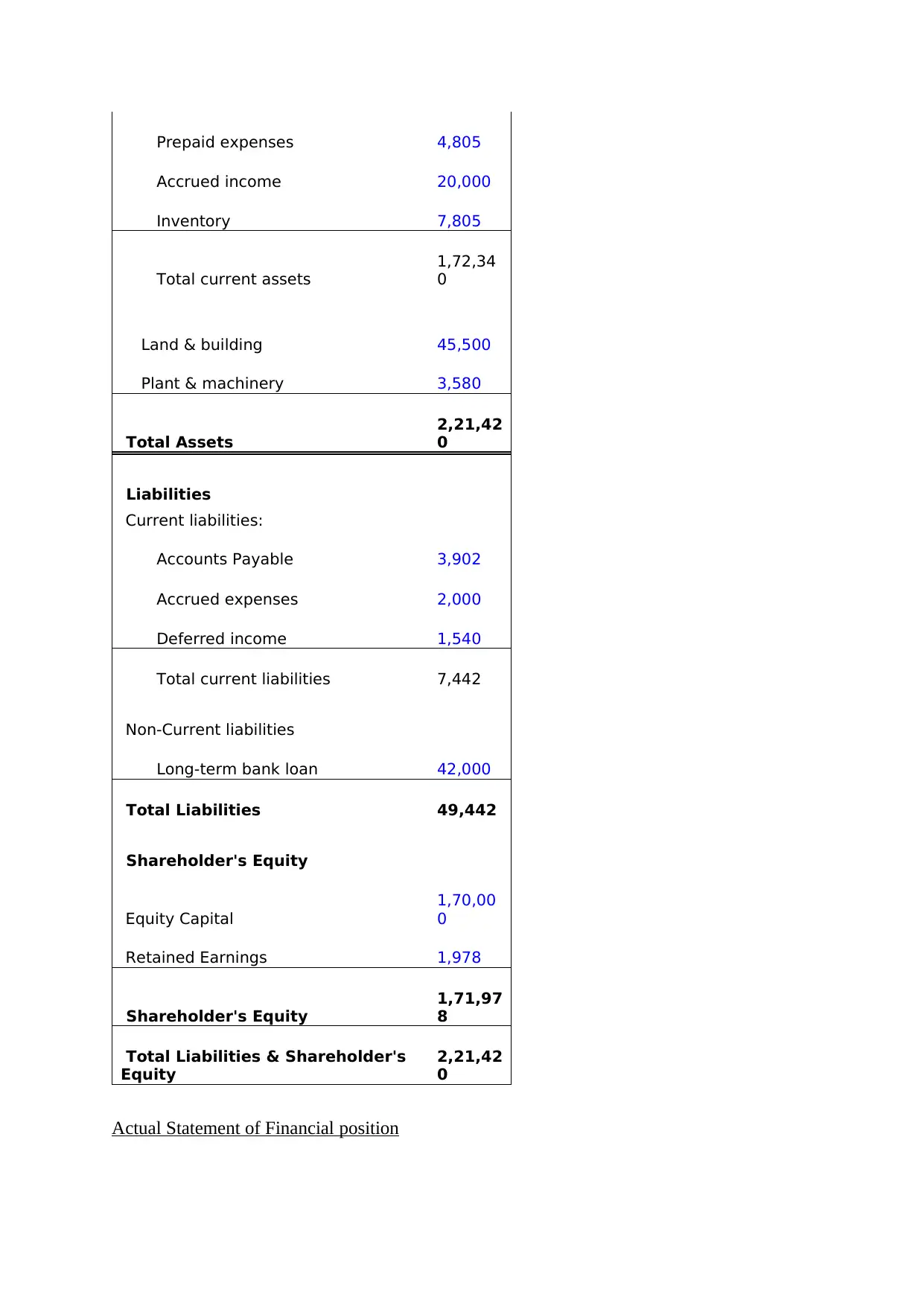

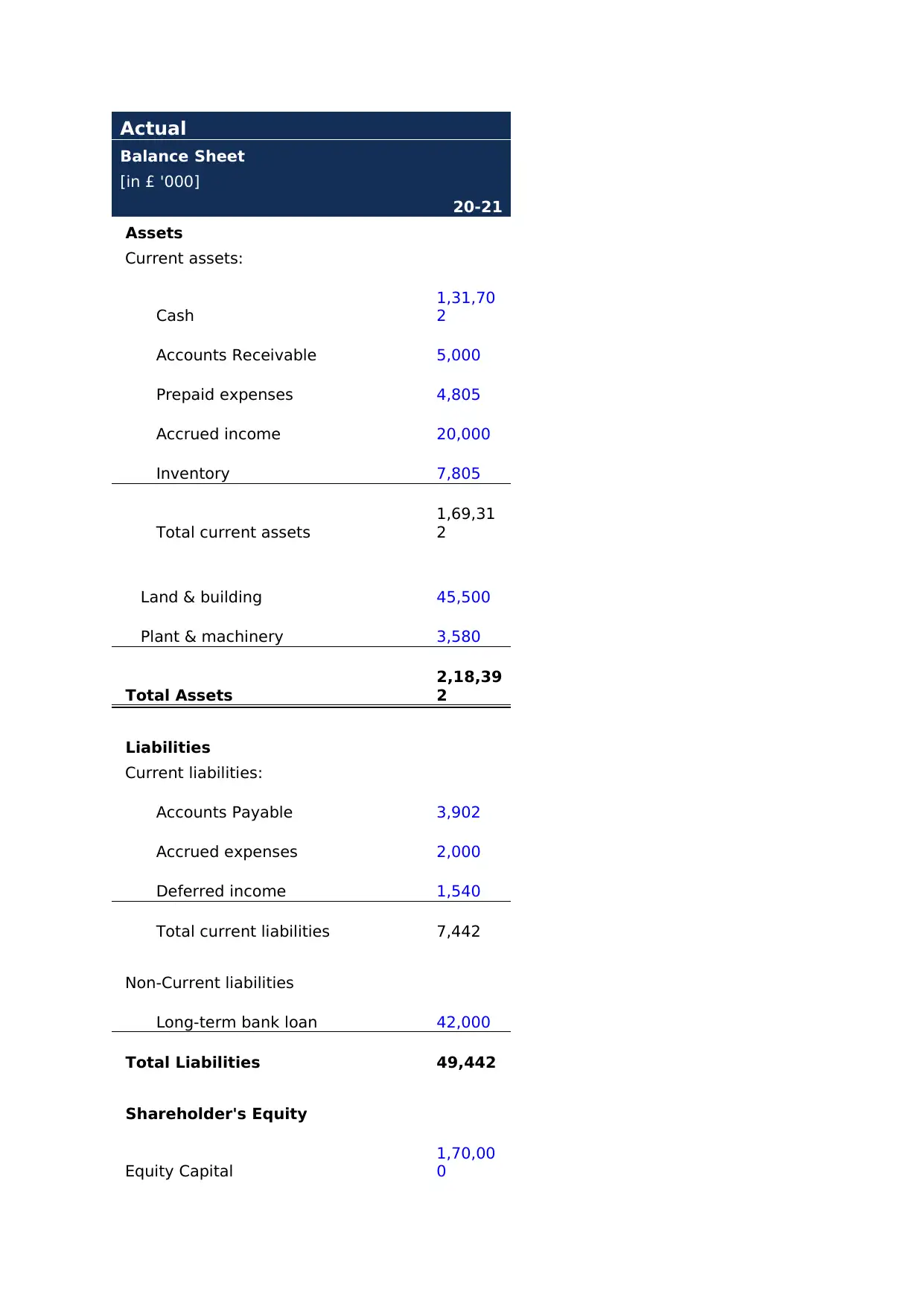

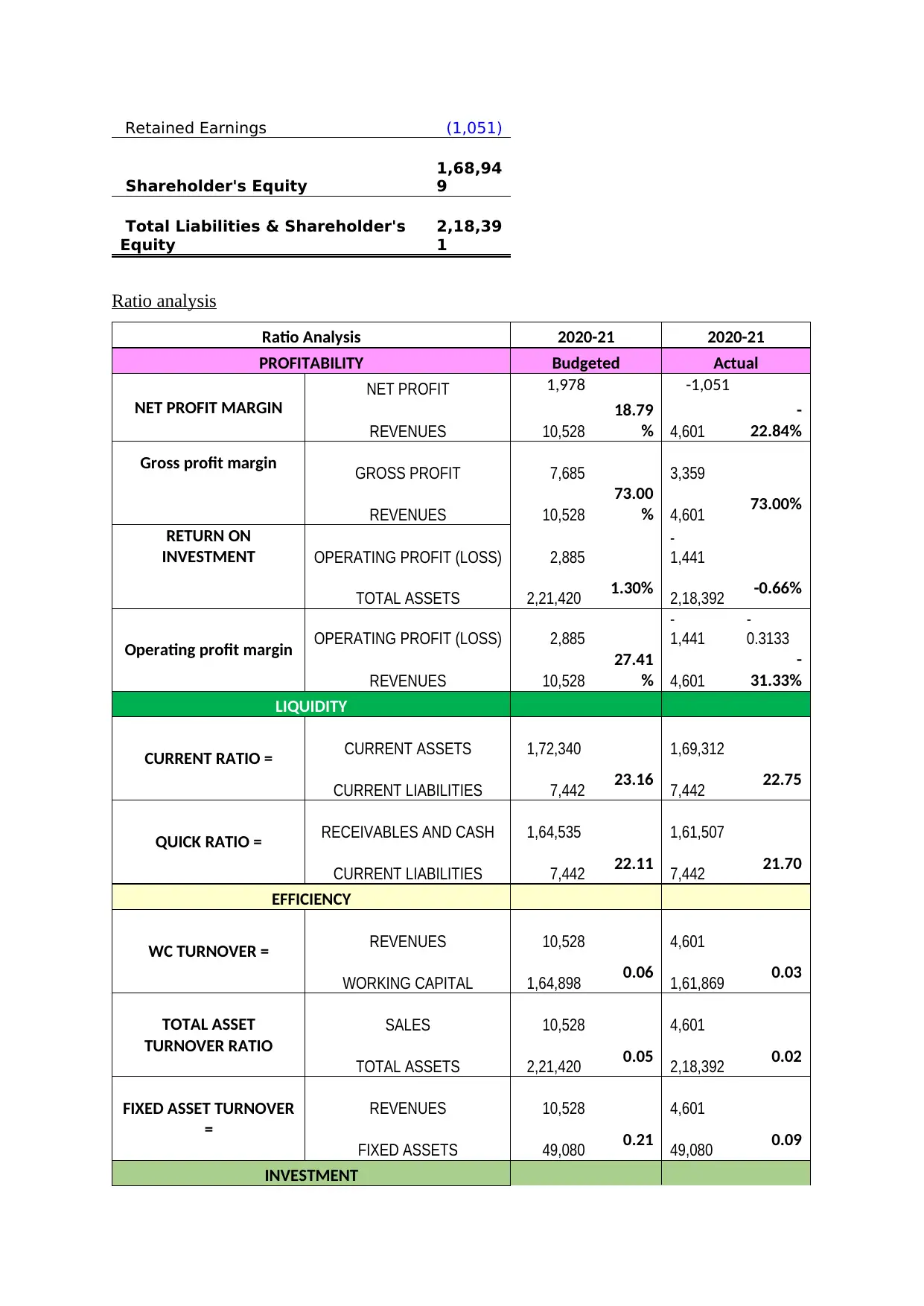

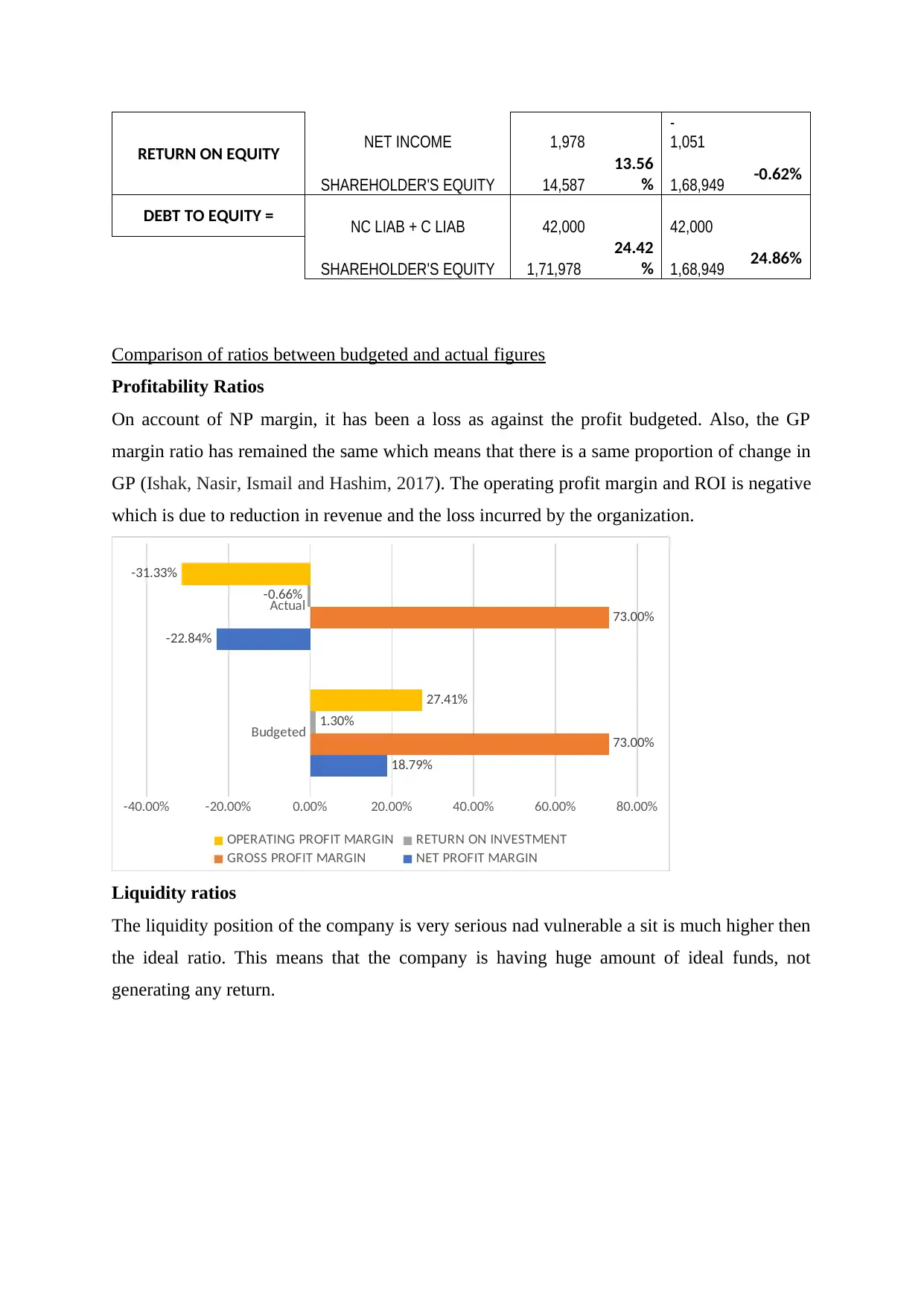

This practical assignment provides a comprehensive financial analysis of a business, comparing budgeted and actual performance over a 12-month period. It includes budgeted and actual statements of profit and loss, highlighting variances in sales, gross profit, and operating profit. The analysis delves into cost variances for direct materials, direct labor, and overhead, alongside a review of budgeted and actual statements of financial position. Key financial ratios are calculated and compared, revealing insights into profitability, liquidity, activity, and risk. The report identifies the company's inability to meet budgeted targets, manage debt effectively, and maintain consistent sales, ultimately affecting its market position. Desklib offers this and similar solved assignments to aid students in their studies.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.