Financial Performance Evaluation: Jeffery & Son's Accounting Report

VerifiedAdded on 2023/04/22

|20

|5393

|438

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles applied to Jeffery & Son's, a manufacturing company. It covers various aspects of cost accounting, including the classification of different types of costs, calculation of unit and total job costs using job costing methods, and the allocation and apportionment of overhead costs. The report also delves into budgeting processes, preparing production and material purchase budgets, and cash budgets. Furthermore, it includes variance analysis to reconcile budgeted and actual figures, identifies key performance indicators for potential improvements, and discusses the role of responsibility centers. The analysis uses both machine hours and labor hours to determine overhead absorption rates, highlighting the differences in cost allocation. This detailed examination offers insights into enhancing business value, reducing costs, and improving overall quality, with the aim of optimizing financial performance for Jeffery & Son's. Desklib provides access to similar solved assignments and resources for students.

Unit 9 Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Classifying the different types of cost...................................................................................3

1.2 Calculating the unit cost and total job cost for job 444 by using job costing method..........4

1.3 calculating the cost of Exquisite by using appropriate techniques.......................................5

b. reapportion of the cost of service and support department into the production department...6

1.4 Analyzing the overhead absorption rate by using direct labor hours....................................7

Task 2...............................................................................................................................................7

AC 2.1 Preparation of cost report for Jeffrey & Sons.................................................................7

AC 2.2 performance indicators that identify the areas of potential improvements.....................9

AC 2.3 Enhance business value, reduce cost and improve quality.............................................9

TASK 3..........................................................................................................................................10

3.1 Stating the purpose and nature of the budgeting process to the marketing manager of

Jeffery & Son's..........................................................................................................................10

3.2 Appropriate budgeting method for the organization and its need.......................................10

3.3 Preparation of the production and material purchase budget for Jeffery & Son's..............11

3.4 Preparation of the cash budget............................................................................................12

TASK 4..........................................................................................................................................13

AC 4.1 Variance analysis..........................................................................................................13

AC 4.2 operating statement that reconcile both the budgeted and actual figures.....................13

AC 4.3 Responsibility centers...................................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION ..........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Classifying the different types of cost...................................................................................3

1.2 Calculating the unit cost and total job cost for job 444 by using job costing method..........4

1.3 calculating the cost of Exquisite by using appropriate techniques.......................................5

b. reapportion of the cost of service and support department into the production department...6

1.4 Analyzing the overhead absorption rate by using direct labor hours....................................7

Task 2...............................................................................................................................................7

AC 2.1 Preparation of cost report for Jeffrey & Sons.................................................................7

AC 2.2 performance indicators that identify the areas of potential improvements.....................9

AC 2.3 Enhance business value, reduce cost and improve quality.............................................9

TASK 3..........................................................................................................................................10

3.1 Stating the purpose and nature of the budgeting process to the marketing manager of

Jeffery & Son's..........................................................................................................................10

3.2 Appropriate budgeting method for the organization and its need.......................................10

3.3 Preparation of the production and material purchase budget for Jeffery & Son's..............11

3.4 Preparation of the cash budget............................................................................................12

TASK 4..........................................................................................................................................13

AC 4.1 Variance analysis..........................................................................................................13

AC 4.2 operating statement that reconcile both the budgeted and actual figures.....................13

AC 4.3 Responsibility centers...................................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting consists the technique through which manager of the

organization is able to make of the accounting information more effectively. It helps organization

in making management reports which provides deeper insight to them about the financial and

statistical information (Brender and Drazen, 2005). Besides this, management accounting also

helps organization in making control upon the cost and there by maximize their profitability

aspect. The present report is based upon the Jeffery and Son's which the manufacturing company

is. It offers many popular and branded products to their customers named as Exquisite. This

project report depicts the different types of cost which organization has to incur in order to

produce the product. Besides this, it will also develop understanding about the purpose and

nature of the budgeting process to the budget holder of the company. In addition to this, it also

depicts the ways through which organization can monitor their financial performance.

3

Management accounting consists the technique through which manager of the

organization is able to make of the accounting information more effectively. It helps organization

in making management reports which provides deeper insight to them about the financial and

statistical information (Brender and Drazen, 2005). Besides this, management accounting also

helps organization in making control upon the cost and there by maximize their profitability

aspect. The present report is based upon the Jeffery and Son's which the manufacturing company

is. It offers many popular and branded products to their customers named as Exquisite. This

project report depicts the different types of cost which organization has to incur in order to

produce the product. Besides this, it will also develop understanding about the purpose and

nature of the budgeting process to the budget holder of the company. In addition to this, it also

depicts the ways through which organization can monitor their financial performance.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 1

1.1 Classifying the different types of cost

Cost may be defined as expenses which Jeffery & Son's has to incur in order to produce

the product and services (Khan and jain, 2006). Classification of the different types of cost is

enumerated below:

On the basis of nature Material cost: It consists of the cost of the raw material which Jeffrey & Son's purchase

in order to produce the finished product. Labor cost: Labor cost refers to amount which organization pay to workers by taking into

consideration to the working hours. It also includes the rate per hour while company

make computation of the labor cost such as wages paid to labors.

Overhead cost: It consists of the expenses which organization incurred in the selling and

distribution of the products or services (Attwell and Laughlin, 2001). In addition to this,

it also includes the expenses which company incurred to make administration of the

business functions.

On the basis of the degree of the tractability of the product Direct expenses: It is also known as prime which is directly attributable to the production

of the product. It includes cost of material, labor and other production related expenses.

Indirect expenses: Indirect cost refers to the expenses which are not directly accountable

to a particular cost object. It may be either fixed or variable which is highly dependent

upon the nature of the expenses incurred by Jeffery & Son's.

On the basis of the changes in activity or volume Fixed cost: It may be defined as those which remains fixed irrespective of the changes

which take place in the level of output or production. In this, cost per unit is decreases

when production increase and vice versa. Fixed cost includes the cost of rent, salary of

the workers, insurance etc. Variable cost: It is highly associated with the unit produced by an organization. Variable

cost consists of the cost which varies as changes take place in the level of output

produced. For instance, material cost and labor cost get increases with increasing the

business production.

4

1.1 Classifying the different types of cost

Cost may be defined as expenses which Jeffery & Son's has to incur in order to produce

the product and services (Khan and jain, 2006). Classification of the different types of cost is

enumerated below:

On the basis of nature Material cost: It consists of the cost of the raw material which Jeffrey & Son's purchase

in order to produce the finished product. Labor cost: Labor cost refers to amount which organization pay to workers by taking into

consideration to the working hours. It also includes the rate per hour while company

make computation of the labor cost such as wages paid to labors.

Overhead cost: It consists of the expenses which organization incurred in the selling and

distribution of the products or services (Attwell and Laughlin, 2001). In addition to this,

it also includes the expenses which company incurred to make administration of the

business functions.

On the basis of the degree of the tractability of the product Direct expenses: It is also known as prime which is directly attributable to the production

of the product. It includes cost of material, labor and other production related expenses.

Indirect expenses: Indirect cost refers to the expenses which are not directly accountable

to a particular cost object. It may be either fixed or variable which is highly dependent

upon the nature of the expenses incurred by Jeffery & Son's.

On the basis of the changes in activity or volume Fixed cost: It may be defined as those which remains fixed irrespective of the changes

which take place in the level of output or production. In this, cost per unit is decreases

when production increase and vice versa. Fixed cost includes the cost of rent, salary of

the workers, insurance etc. Variable cost: It is highly associated with the unit produced by an organization. Variable

cost consists of the cost which varies as changes take place in the level of output

produced. For instance, material cost and labor cost get increases with increasing the

business production.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Semi-variable cost: It is the combination of the fixed and variable cost. In this, cost

remains fixed at the certain level of output produced and it became variable as

predetermined level of output exceeds (Briers and Chua, 2001). For instance: Electricity

expenses

Stepped fixed cost: Expenditures that do not get change within a fixed interval of activity.

After breaching this threshold point, expenditures also tends to rise. For instance, Jeffrey

& Son's business needs to buy new machinery to increase their production level.

Cost classification on the basis of functions

Manufacturing costs: Expenditures that have been incurred on business productions

except direct material and direct labor. Jeffrey & Son's manufacturing expenses involves

indirect material, indirect labor and all the factory overheads such as supervisor salary,

heat, lighting and factory rent. It can be attributed to finished goods of the business.

Non manufacturing cost: office administration expenditures and selling and marketing

expenses are known as non manufacturing expenses. For instance, executive salary,

office rent, postage, printing charges and advertisement expenses.

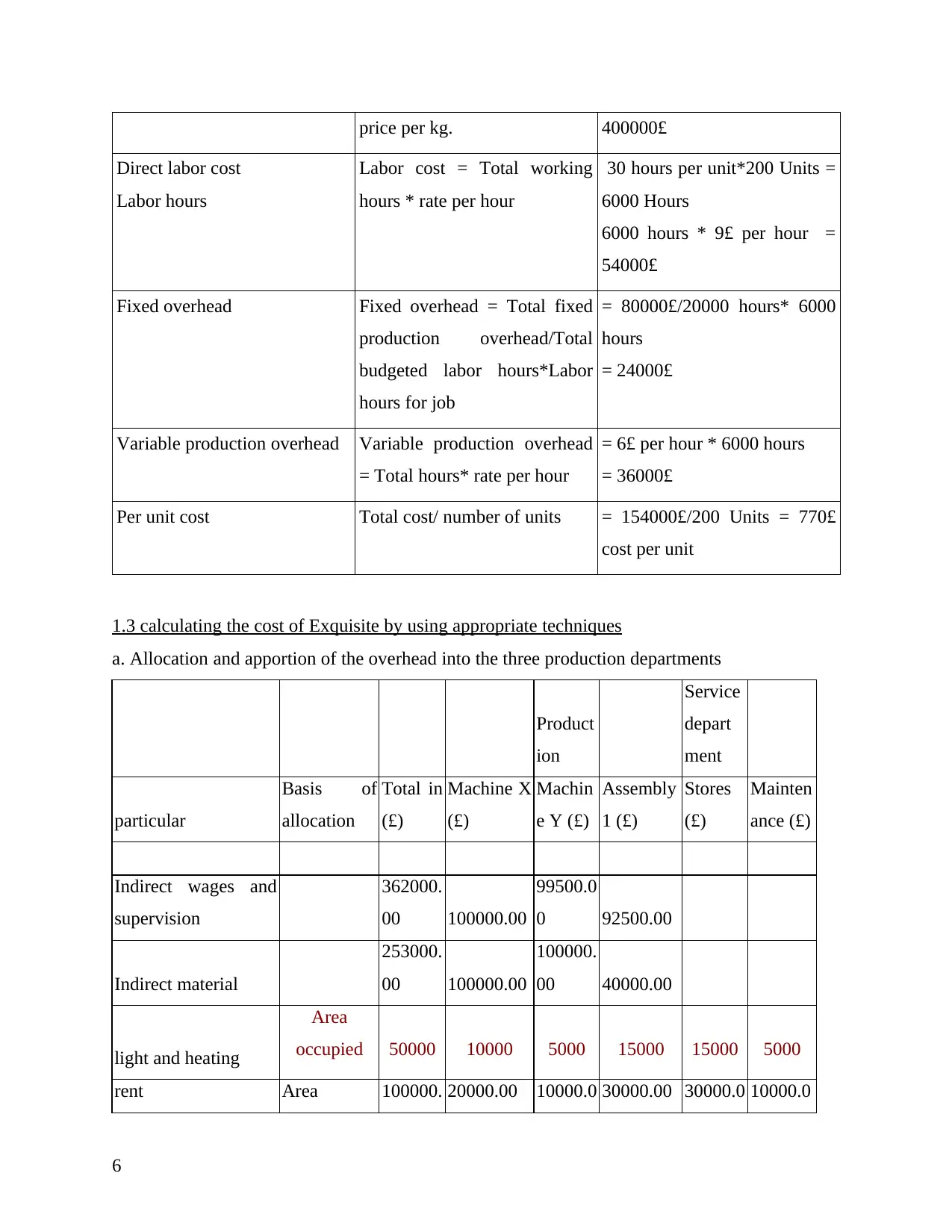

1.2 Calculating the unit cost and total job cost for job 444 by using job costing method

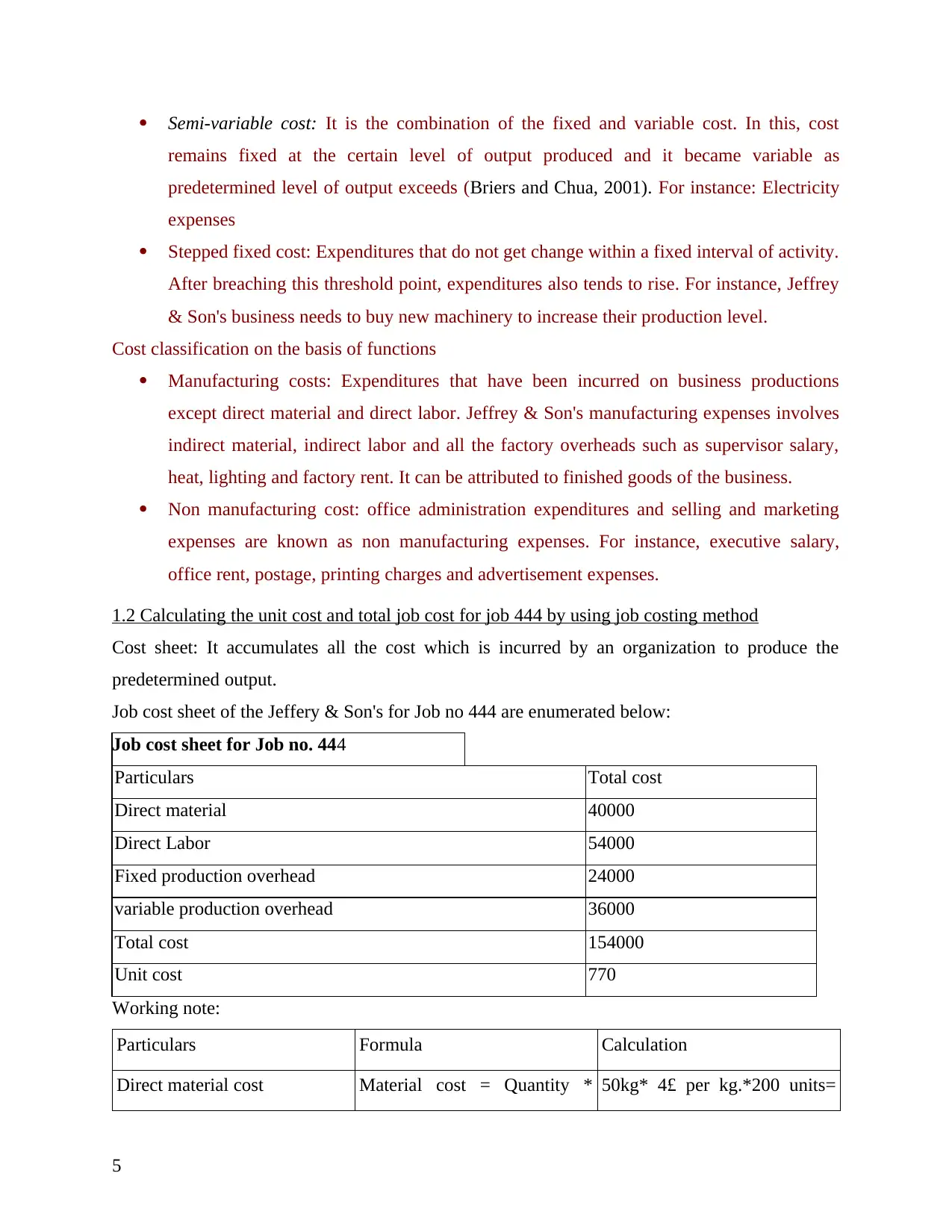

Cost sheet: It accumulates all the cost which is incurred by an organization to produce the

predetermined output.

Job cost sheet of the Jeffery & Son's for Job no 444 are enumerated below:

Job cost sheet for Job no. 444

Particulars Total cost

Direct material 40000

Direct Labor 54000

Fixed production overhead 24000

variable production overhead 36000

Total cost 154000

Unit cost 770

Working note:

Particulars Formula Calculation

Direct material cost Material cost = Quantity * 50kg* 4£ per kg.*200 units=

5

remains fixed at the certain level of output produced and it became variable as

predetermined level of output exceeds (Briers and Chua, 2001). For instance: Electricity

expenses

Stepped fixed cost: Expenditures that do not get change within a fixed interval of activity.

After breaching this threshold point, expenditures also tends to rise. For instance, Jeffrey

& Son's business needs to buy new machinery to increase their production level.

Cost classification on the basis of functions

Manufacturing costs: Expenditures that have been incurred on business productions

except direct material and direct labor. Jeffrey & Son's manufacturing expenses involves

indirect material, indirect labor and all the factory overheads such as supervisor salary,

heat, lighting and factory rent. It can be attributed to finished goods of the business.

Non manufacturing cost: office administration expenditures and selling and marketing

expenses are known as non manufacturing expenses. For instance, executive salary,

office rent, postage, printing charges and advertisement expenses.

1.2 Calculating the unit cost and total job cost for job 444 by using job costing method

Cost sheet: It accumulates all the cost which is incurred by an organization to produce the

predetermined output.

Job cost sheet of the Jeffery & Son's for Job no 444 are enumerated below:

Job cost sheet for Job no. 444

Particulars Total cost

Direct material 40000

Direct Labor 54000

Fixed production overhead 24000

variable production overhead 36000

Total cost 154000

Unit cost 770

Working note:

Particulars Formula Calculation

Direct material cost Material cost = Quantity * 50kg* 4£ per kg.*200 units=

5

price per kg. 400000£

Direct labor cost

Labor hours

Labor cost = Total working

hours * rate per hour

30 hours per unit*200 Units =

6000 Hours

6000 hours * 9£ per hour =

54000£

Fixed overhead Fixed overhead = Total fixed

production overhead/Total

budgeted labor hours*Labor

hours for job

= 80000£/20000 hours* 6000

hours

= 24000£

Variable production overhead Variable production overhead

= Total hours* rate per hour

= 6£ per hour * 6000 hours

= 36000£

Per unit cost Total cost/ number of units = 154000£/200 Units = 770£

cost per unit

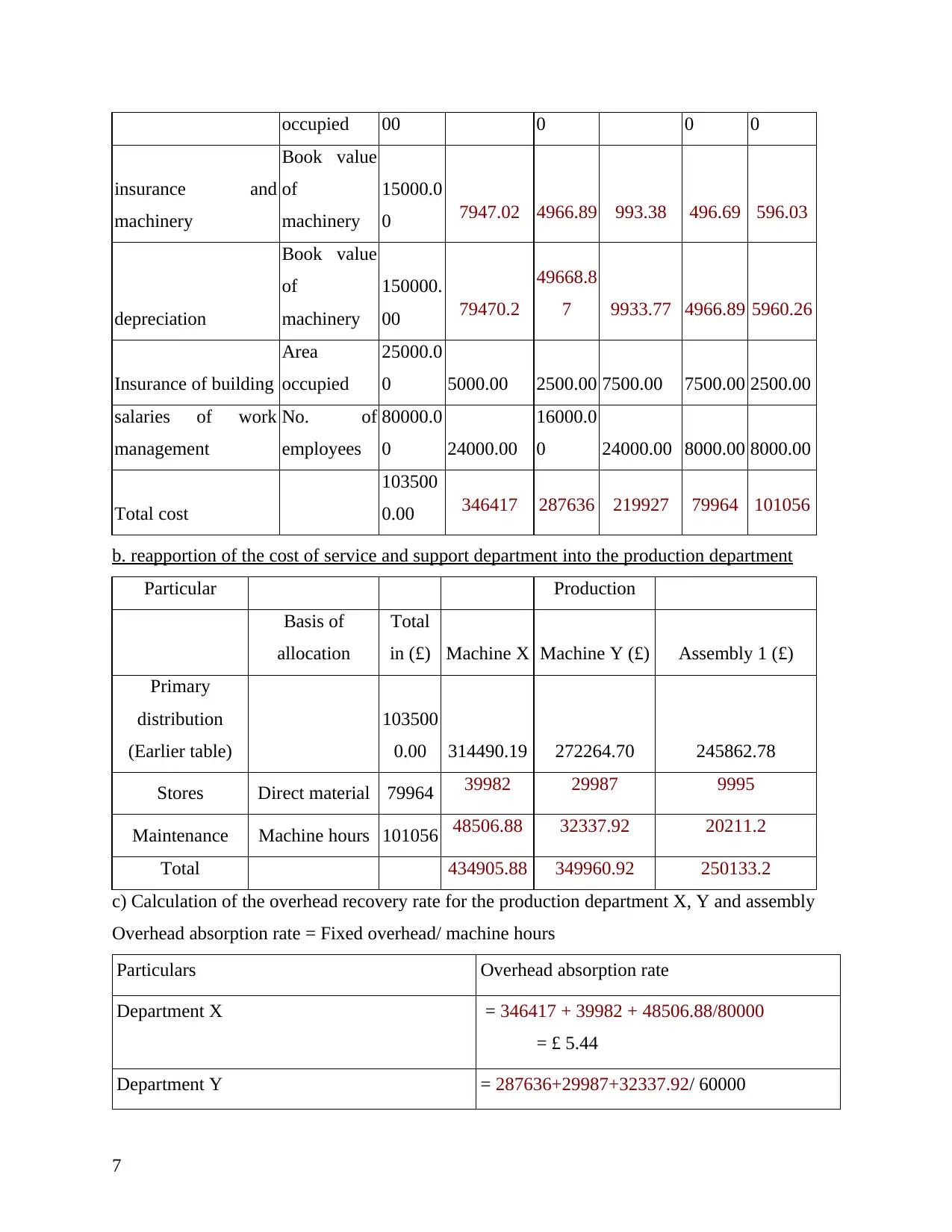

1.3 calculating the cost of Exquisite by using appropriate techniques

a. Allocation and apportion of the overhead into the three production departments

Product

ion

Service

depart

ment

particular

Basis of

allocation

Total in

(£)

Machine X

(£)

Machin

e Y (£)

Assembly

1 (£)

Stores

(£)

Mainten

ance (£)

Indirect wages and

supervision

362000.

00 100000.00

99500.0

0 92500.00

Indirect material

253000.

00 100000.00

100000.

00 40000.00

light and heating

Area

occupied 50000 10000 5000 15000 15000 5000

rent Area 100000. 20000.00 10000.0 30000.00 30000.0 10000.0

6

Direct labor cost

Labor hours

Labor cost = Total working

hours * rate per hour

30 hours per unit*200 Units =

6000 Hours

6000 hours * 9£ per hour =

54000£

Fixed overhead Fixed overhead = Total fixed

production overhead/Total

budgeted labor hours*Labor

hours for job

= 80000£/20000 hours* 6000

hours

= 24000£

Variable production overhead Variable production overhead

= Total hours* rate per hour

= 6£ per hour * 6000 hours

= 36000£

Per unit cost Total cost/ number of units = 154000£/200 Units = 770£

cost per unit

1.3 calculating the cost of Exquisite by using appropriate techniques

a. Allocation and apportion of the overhead into the three production departments

Product

ion

Service

depart

ment

particular

Basis of

allocation

Total in

(£)

Machine X

(£)

Machin

e Y (£)

Assembly

1 (£)

Stores

(£)

Mainten

ance (£)

Indirect wages and

supervision

362000.

00 100000.00

99500.0

0 92500.00

Indirect material

253000.

00 100000.00

100000.

00 40000.00

light and heating

Area

occupied 50000 10000 5000 15000 15000 5000

rent Area 100000. 20000.00 10000.0 30000.00 30000.0 10000.0

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

occupied 00 0 0 0

insurance and

machinery

Book value

of

machinery

15000.0

0 7947.02 4966.89 993.38 496.69 596.03

depreciation

Book value

of

machinery

150000.

00 79470.2

49668.8

7 9933.77 4966.89 5960.26

Insurance of building

Area

occupied

25000.0

0 5000.00 2500.00 7500.00 7500.00 2500.00

salaries of work

management

No. of

employees

80000.0

0 24000.00

16000.0

0 24000.00 8000.00 8000.00

Total cost

103500

0.00 346417 287636 219927 79964 101056

b. reapportion of the cost of service and support department into the production department

Particular Production

Basis of

allocation

Total

in (£) Machine X Machine Y (£) Assembly 1 (£)

Primary

distribution

(Earlier table)

103500

0.00 314490.19 272264.70 245862.78

Stores Direct material 79964 39982 29987 9995

Maintenance Machine hours 101056 48506.88 32337.92 20211.2

Total 434905.88 349960.92 250133.2

c) Calculation of the overhead recovery rate for the production department X, Y and assembly

Overhead absorption rate = Fixed overhead/ machine hours

Particulars Overhead absorption rate

Department X = 346417 + 39982 + 48506.88/80000

= £ 5.44

Department Y = 287636+29987+32337.92/ 60000

7

insurance and

machinery

Book value

of

machinery

15000.0

0 7947.02 4966.89 993.38 496.69 596.03

depreciation

Book value

of

machinery

150000.

00 79470.2

49668.8

7 9933.77 4966.89 5960.26

Insurance of building

Area

occupied

25000.0

0 5000.00 2500.00 7500.00 7500.00 2500.00

salaries of work

management

No. of

employees

80000.0

0 24000.00

16000.0

0 24000.00 8000.00 8000.00

Total cost

103500

0.00 346417 287636 219927 79964 101056

b. reapportion of the cost of service and support department into the production department

Particular Production

Basis of

allocation

Total

in (£) Machine X Machine Y (£) Assembly 1 (£)

Primary

distribution

(Earlier table)

103500

0.00 314490.19 272264.70 245862.78

Stores Direct material 79964 39982 29987 9995

Maintenance Machine hours 101056 48506.88 32337.92 20211.2

Total 434905.88 349960.92 250133.2

c) Calculation of the overhead recovery rate for the production department X, Y and assembly

Overhead absorption rate = Fixed overhead/ machine hours

Particulars Overhead absorption rate

Department X = 346417 + 39982 + 48506.88/80000

= £ 5.44

Department Y = 287636+29987+32337.92/ 60000

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

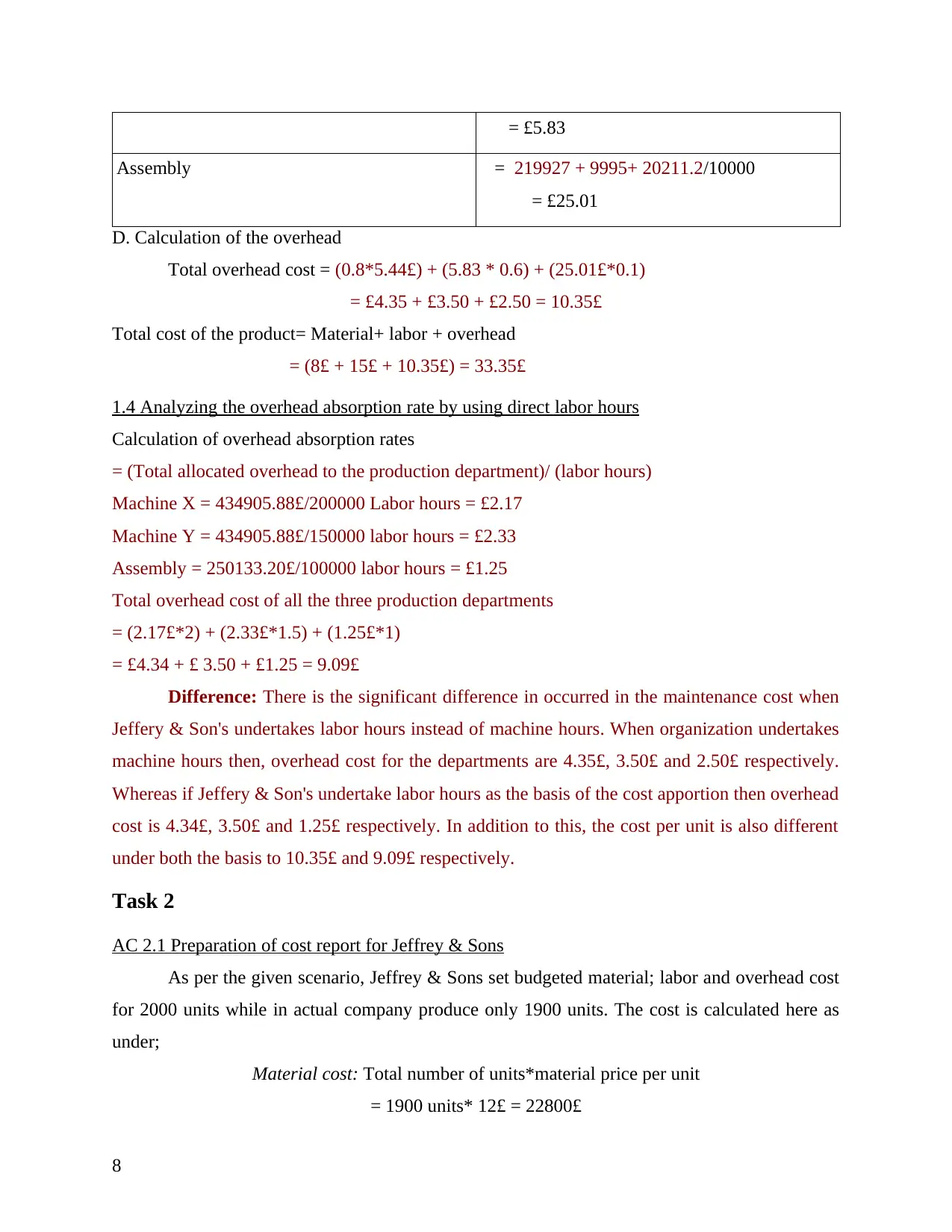

= £5.83

Assembly = 219927 + 9995+ 20211.2/10000

= £25.01

D. Calculation of the overhead

Total overhead cost = (0.8*5.44£) + (5.83 * 0.6) + (25.01£*0.1)

= £4.35 + £3.50 + £2.50 = 10.35£

Total cost of the product= Material+ labor + overhead

= (8£ + 15£ + 10.35£) = 33.35£

1.4 Analyzing the overhead absorption rate by using direct labor hours

Calculation of overhead absorption rates

= (Total allocated overhead to the production department)/ (labor hours)

Machine X = 434905.88£/200000 Labor hours = £2.17

Machine Y = 434905.88£/150000 labor hours = £2.33

Assembly = 250133.20£/100000 labor hours = £1.25

Total overhead cost of all the three production departments

= (2.17£*2) + (2.33£*1.5) + (1.25£*1)

= £4.34 + £ 3.50 + £1.25 = 9.09£

Difference: There is the significant difference in occurred in the maintenance cost when

Jeffery & Son's undertakes labor hours instead of machine hours. When organization undertakes

machine hours then, overhead cost for the departments are 4.35£, 3.50£ and 2.50£ respectively.

Whereas if Jeffery & Son's undertake labor hours as the basis of the cost apportion then overhead

cost is 4.34£, 3.50£ and 1.25£ respectively. In addition to this, the cost per unit is also different

under both the basis to 10.35£ and 9.09£ respectively.

Task 2

AC 2.1 Preparation of cost report for Jeffrey & Sons

As per the given scenario, Jeffrey & Sons set budgeted material; labor and overhead cost

for 2000 units while in actual company produce only 1900 units. The cost is calculated here as

under;

Material cost: Total number of units*material price per unit

= 1900 units* 12£ = 22800£

8

Assembly = 219927 + 9995+ 20211.2/10000

= £25.01

D. Calculation of the overhead

Total overhead cost = (0.8*5.44£) + (5.83 * 0.6) + (25.01£*0.1)

= £4.35 + £3.50 + £2.50 = 10.35£

Total cost of the product= Material+ labor + overhead

= (8£ + 15£ + 10.35£) = 33.35£

1.4 Analyzing the overhead absorption rate by using direct labor hours

Calculation of overhead absorption rates

= (Total allocated overhead to the production department)/ (labor hours)

Machine X = 434905.88£/200000 Labor hours = £2.17

Machine Y = 434905.88£/150000 labor hours = £2.33

Assembly = 250133.20£/100000 labor hours = £1.25

Total overhead cost of all the three production departments

= (2.17£*2) + (2.33£*1.5) + (1.25£*1)

= £4.34 + £ 3.50 + £1.25 = 9.09£

Difference: There is the significant difference in occurred in the maintenance cost when

Jeffery & Son's undertakes labor hours instead of machine hours. When organization undertakes

machine hours then, overhead cost for the departments are 4.35£, 3.50£ and 2.50£ respectively.

Whereas if Jeffery & Son's undertake labor hours as the basis of the cost apportion then overhead

cost is 4.34£, 3.50£ and 1.25£ respectively. In addition to this, the cost per unit is also different

under both the basis to 10.35£ and 9.09£ respectively.

Task 2

AC 2.1 Preparation of cost report for Jeffrey & Sons

As per the given scenario, Jeffrey & Sons set budgeted material; labor and overhead cost

for 2000 units while in actual company produce only 1900 units. The cost is calculated here as

under;

Material cost: Total number of units*material price per unit

= 1900 units* 12£ = 22800£

8

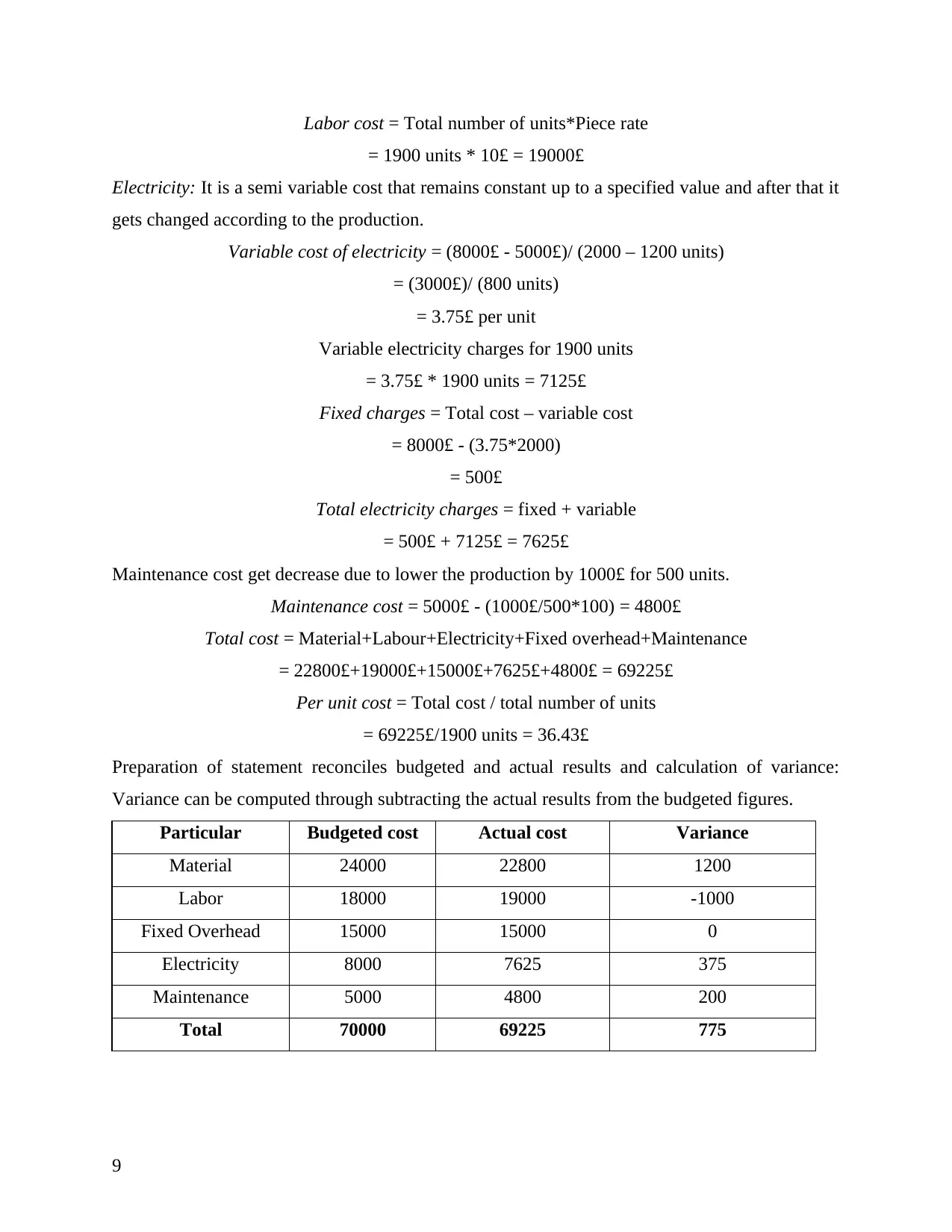

Labor cost = Total number of units*Piece rate

= 1900 units * 10£ = 19000£

Electricity: It is a semi variable cost that remains constant up to a specified value and after that it

gets changed according to the production.

Variable cost of electricity = (8000£ - 5000£)/ (2000 – 1200 units)

= (3000£)/ (800 units)

= 3.75£ per unit

Variable electricity charges for 1900 units

= 3.75£ * 1900 units = 7125£

Fixed charges = Total cost – variable cost

= 8000£ - (3.75*2000)

= 500£

Total electricity charges = fixed + variable

= 500£ + 7125£ = 7625£

Maintenance cost get decrease due to lower the production by 1000£ for 500 units.

Maintenance cost = 5000£ - (1000£/500*100) = 4800£

Total cost = Material+Labour+Electricity+Fixed overhead+Maintenance

= 22800£+19000£+15000£+7625£+4800£ = 69225£

Per unit cost = Total cost / total number of units

= 69225£/1900 units = 36.43£

Preparation of statement reconciles budgeted and actual results and calculation of variance:

Variance can be computed through subtracting the actual results from the budgeted figures.

Particular Budgeted cost Actual cost Variance

Material 24000 22800 1200

Labor 18000 19000 -1000

Fixed Overhead 15000 15000 0

Electricity 8000 7625 375

Maintenance 5000 4800 200

Total 70000 69225 775

9

= 1900 units * 10£ = 19000£

Electricity: It is a semi variable cost that remains constant up to a specified value and after that it

gets changed according to the production.

Variable cost of electricity = (8000£ - 5000£)/ (2000 – 1200 units)

= (3000£)/ (800 units)

= 3.75£ per unit

Variable electricity charges for 1900 units

= 3.75£ * 1900 units = 7125£

Fixed charges = Total cost – variable cost

= 8000£ - (3.75*2000)

= 500£

Total electricity charges = fixed + variable

= 500£ + 7125£ = 7625£

Maintenance cost get decrease due to lower the production by 1000£ for 500 units.

Maintenance cost = 5000£ - (1000£/500*100) = 4800£

Total cost = Material+Labour+Electricity+Fixed overhead+Maintenance

= 22800£+19000£+15000£+7625£+4800£ = 69225£

Per unit cost = Total cost / total number of units

= 69225£/1900 units = 36.43£

Preparation of statement reconciles budgeted and actual results and calculation of variance:

Variance can be computed through subtracting the actual results from the budgeted figures.

Particular Budgeted cost Actual cost Variance

Material 24000 22800 1200

Labor 18000 19000 -1000

Fixed Overhead 15000 15000 0

Electricity 8000 7625 375

Maintenance 5000 4800 200

Total 70000 69225 775

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Interpretation: Material price variance does not get changed from 12£ while the total

material cost get declined to 22800£. The reason behind such declines is that the actual

production of the company gets declined to 1900 units. However, the budgeted Labor piece rate

was 9£ per unit get increased to 10£ per unit. Therefore the total labor cost get inclined create

negative impact to the company. Further, electricity and maintenance charges get decrease

because of production decreases.

AC 2.2 performance indicators that identify the areas of potential improvements

Jeffrey & Son's business has to assess the business performance on the regular basis. It

helps to make improvement and moving business in right direction. Key performance indicators

help the business in this way. Performance indicators are the set of quantitative measurement that

and business analyses to compare with the set targets. Business revenues are one of the great

important indicators that include the total business sales. If the business revenues get declined

over the period than Jeffrey & son's need to identify the reason for such decreases (Ward, 2012).

Moreover, the expenditure or cost also can be measured if business revenue is stable and cost is

decreasing than it will create an adverse impact to the organization. Therefore, all the

organization requires increasing the business sales and reducing its expenditures. On contrary,

profitability measures the business operational results. In case of declining the profits, Jeffrey &

Son's have to take necessary steps to improve it. Further, the customer satisfaction level, number

of customers, utilization of resources also helps to measure Jeffrey & Son's performance.

Increase the customers and their satisfaction level company will be able to attain customer

loyalty and retain it for longer time period. In addition, if Jeffrey & Son's utilizes the available

resources such as human resources and financial resources in an effective way, it can achieve

growth and make development. Moreover, business expansion, its market growth and corporate

image also helps to identify the areas for potential improvement.

AC 2.3 Enhance business value, reduce cost and improve quality

Each and every business has the objective to increase profitability and the financial

performance. Therefore business requires enhancing its value, declining its cost and increasing

the quality.

Business value: Business value can be improved through increasing the business profits

to a great extent. Moreover, skilled and able workforce can be employed in Jeffrey & Son's that

helps to improve the business turnover lead to increase profits (Whitecotton, Libby and Phillips,

10

material cost get declined to 22800£. The reason behind such declines is that the actual

production of the company gets declined to 1900 units. However, the budgeted Labor piece rate

was 9£ per unit get increased to 10£ per unit. Therefore the total labor cost get inclined create

negative impact to the company. Further, electricity and maintenance charges get decrease

because of production decreases.

AC 2.2 performance indicators that identify the areas of potential improvements

Jeffrey & Son's business has to assess the business performance on the regular basis. It

helps to make improvement and moving business in right direction. Key performance indicators

help the business in this way. Performance indicators are the set of quantitative measurement that

and business analyses to compare with the set targets. Business revenues are one of the great

important indicators that include the total business sales. If the business revenues get declined

over the period than Jeffrey & son's need to identify the reason for such decreases (Ward, 2012).

Moreover, the expenditure or cost also can be measured if business revenue is stable and cost is

decreasing than it will create an adverse impact to the organization. Therefore, all the

organization requires increasing the business sales and reducing its expenditures. On contrary,

profitability measures the business operational results. In case of declining the profits, Jeffrey &

Son's have to take necessary steps to improve it. Further, the customer satisfaction level, number

of customers, utilization of resources also helps to measure Jeffrey & Son's performance.

Increase the customers and their satisfaction level company will be able to attain customer

loyalty and retain it for longer time period. In addition, if Jeffrey & Son's utilizes the available

resources such as human resources and financial resources in an effective way, it can achieve

growth and make development. Moreover, business expansion, its market growth and corporate

image also helps to identify the areas for potential improvement.

AC 2.3 Enhance business value, reduce cost and improve quality

Each and every business has the objective to increase profitability and the financial

performance. Therefore business requires enhancing its value, declining its cost and increasing

the quality.

Business value: Business value can be improved through increasing the business profits

to a great extent. Moreover, skilled and able workforce can be employed in Jeffrey & Son's that

helps to improve the business turnover lead to increase profits (Whitecotton, Libby and Phillips,

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2013). Further, Jeffrey & son's can differentiate its produced products and services from the

competitors. In addition to it, the expansion programs and new capital investment project also

contributes to improving the business value.

Reduce cost: It directly contributes to increasing the business profitability. All the

organizations have to establish an effective cost control system in the company. Purchase cost

can be declined through searching new source that provides material cheaper rate. Further,

company should employ the skilled workforce at reasonable work rate (Kokubu and et. al.,

2009). In addition to it, company can set targets and match it with the actual figures and take

corrective actions if the actual cost is high than budgeted. Further, business has to full utilize its

production capacity and reduce the wastage for that purpose.

Improve quality: Quality can be improved through using efficient technology and

efficient workforce. In case of any default corrective actions should be taken immediately.

Moreover, quality measurement tools and an effective training and development program can be

organized for this purpose.

TASK 3

3.1 Stating the purpose and nature of the budgeting process to the marketing manager of Jeffery

& Son's

Budget is the estimation of the receipts and payments of Jeffrey & Son's for the

predetermined time period. It facilitates effective allocation and use of the financial resources to

the large extent.

Purpose of the budgeting process: Purpose of the marketing manager of Jeffery & Son's behind

the preparation of the budget is as follows:

One of the main objectives of marketing manager is to make proper allocation of the

financial resource in accordance with the functions organization need to perform. Further, another objective of budgeting process is to exert control over the expenditure by

comparing the actual performance with the budgeted figure (Burns, Hopper and Yazdifar,

2004). Through this, manager is able to assess the deviations which occurred in the

performance of an organization and thereby able to undertake the corrective measures.

Nature of the budgeting process: In the budgeting process marketing manager who is the budget

holder of Jeffrey & Son’s requires to assess the financial environment on the basis of previous

11

competitors. In addition to it, the expansion programs and new capital investment project also

contributes to improving the business value.

Reduce cost: It directly contributes to increasing the business profitability. All the

organizations have to establish an effective cost control system in the company. Purchase cost

can be declined through searching new source that provides material cheaper rate. Further,

company should employ the skilled workforce at reasonable work rate (Kokubu and et. al.,

2009). In addition to it, company can set targets and match it with the actual figures and take

corrective actions if the actual cost is high than budgeted. Further, business has to full utilize its

production capacity and reduce the wastage for that purpose.

Improve quality: Quality can be improved through using efficient technology and

efficient workforce. In case of any default corrective actions should be taken immediately.

Moreover, quality measurement tools and an effective training and development program can be

organized for this purpose.

TASK 3

3.1 Stating the purpose and nature of the budgeting process to the marketing manager of Jeffery

& Son's

Budget is the estimation of the receipts and payments of Jeffrey & Son's for the

predetermined time period. It facilitates effective allocation and use of the financial resources to

the large extent.

Purpose of the budgeting process: Purpose of the marketing manager of Jeffery & Son's behind

the preparation of the budget is as follows:

One of the main objectives of marketing manager is to make proper allocation of the

financial resource in accordance with the functions organization need to perform. Further, another objective of budgeting process is to exert control over the expenditure by

comparing the actual performance with the budgeted figure (Burns, Hopper and Yazdifar,

2004). Through this, manager is able to assess the deviations which occurred in the

performance of an organization and thereby able to undertake the corrective measures.

Nature of the budgeting process: In the budgeting process marketing manager who is the budget

holder of Jeffrey & Son’s requires to assess the financial environment on the basis of previous

11

budget. Thereafter manager make estimation of the expenses which Jeffery & Son's will incur

over the period of time. In addition to this, marketing manager also make assessment of the

revenue which organization will generate during the predetermined time period. At last manager

subtracts inflow from the outflow and there by identify the condition of deficit and surplus.

3.2 Appropriate budgeting method for the organization and its need

Jeffrey & Son's prepared their budget by taking into consideration the incremental

budgeting in order to prepare budget. There are several drawbacks of incremental budgeting

which negatively impacts the financial performance of an organization. Thus, Jeffrey & Son's

requires to adopt the zero base budgeting which helps them in preparing the more effective

budget for the accounting year. In zero base budgeting managers take zero bases for the income

and expenditures. In this, organization prepares the budget by estimating the actual expenses

which they have to incur during the predetermined time period. In addition to this, manager also

makes assessment of the each possible alternative for the income and expenses (Cole, 2007).

Thus, it is based upon the realistic aspects rather than assumption. Therefore, zero base budgets

helps organization in getting the desired output.

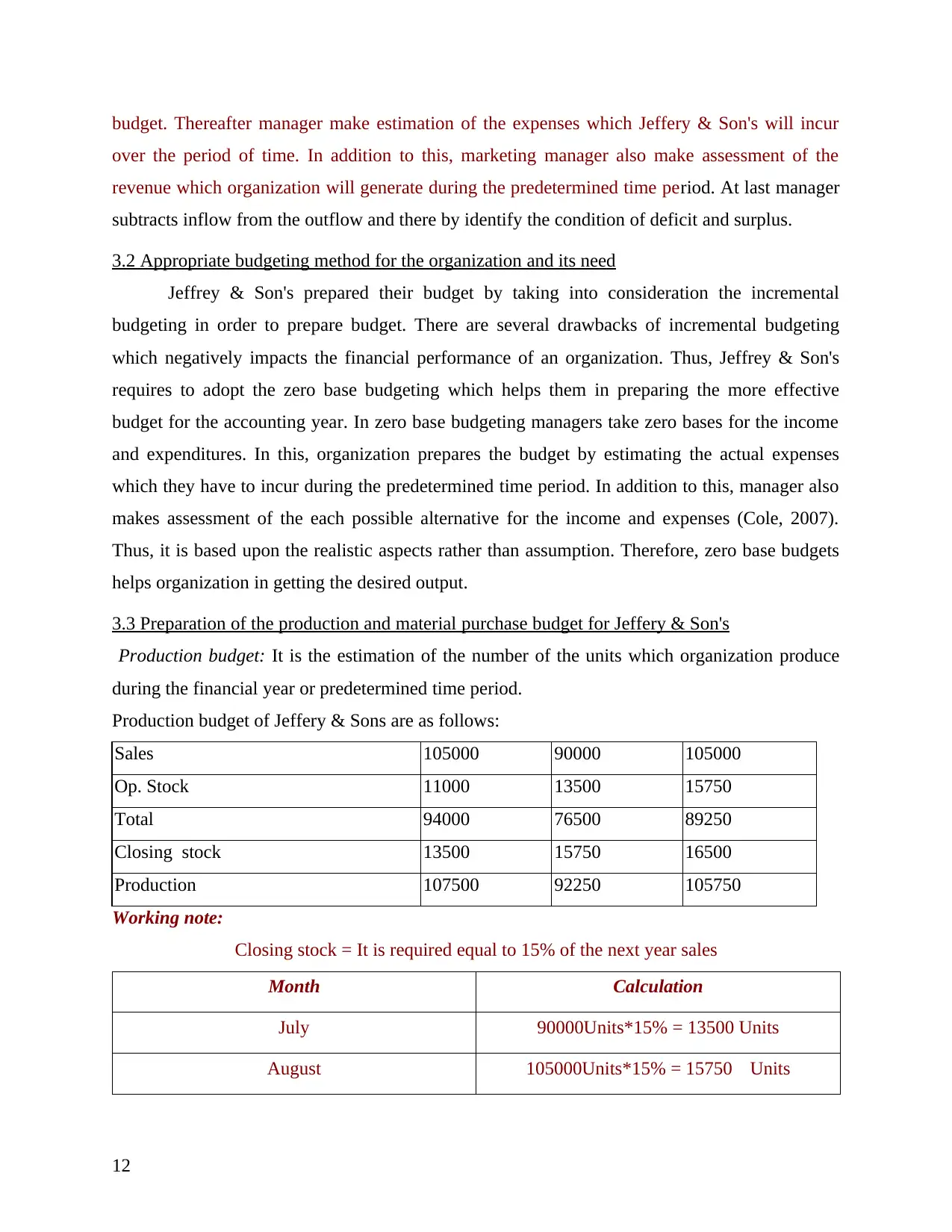

3.3 Preparation of the production and material purchase budget for Jeffery & Son's

Production budget: It is the estimation of the number of the units which organization produce

during the financial year or predetermined time period.

Production budget of Jeffery & Sons are as follows:

Sales 105000 90000 105000

Op. Stock 11000 13500 15750

Total 94000 76500 89250

Closing stock 13500 15750 16500

Production 107500 92250 105750

Working note:

Closing stock = It is required equal to 15% of the next year sales

Month Calculation

July 90000Units*15% = 13500 Units

August 105000Units*15% = 15750 Units

12

over the period of time. In addition to this, marketing manager also make assessment of the

revenue which organization will generate during the predetermined time period. At last manager

subtracts inflow from the outflow and there by identify the condition of deficit and surplus.

3.2 Appropriate budgeting method for the organization and its need

Jeffrey & Son's prepared their budget by taking into consideration the incremental

budgeting in order to prepare budget. There are several drawbacks of incremental budgeting

which negatively impacts the financial performance of an organization. Thus, Jeffrey & Son's

requires to adopt the zero base budgeting which helps them in preparing the more effective

budget for the accounting year. In zero base budgeting managers take zero bases for the income

and expenditures. In this, organization prepares the budget by estimating the actual expenses

which they have to incur during the predetermined time period. In addition to this, manager also

makes assessment of the each possible alternative for the income and expenses (Cole, 2007).

Thus, it is based upon the realistic aspects rather than assumption. Therefore, zero base budgets

helps organization in getting the desired output.

3.3 Preparation of the production and material purchase budget for Jeffery & Son's

Production budget: It is the estimation of the number of the units which organization produce

during the financial year or predetermined time period.

Production budget of Jeffery & Sons are as follows:

Sales 105000 90000 105000

Op. Stock 11000 13500 15750

Total 94000 76500 89250

Closing stock 13500 15750 16500

Production 107500 92250 105750

Working note:

Closing stock = It is required equal to 15% of the next year sales

Month Calculation

July 90000Units*15% = 13500 Units

August 105000Units*15% = 15750 Units

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.