Financial Ratio Analysis and Stakeholder Identification: Aston Martin

VerifiedAdded on 2020/12/09

|13

|2701

|313

Report

AI Summary

This report provides a comprehensive financial analysis of Aston Martin, focusing on key financial ratios to assess the company's performance. It calculates and explains profitability, efficiency, and liquidity ratios such as Return on Equity, Asset Turnover, Current Ratio, Debt to Equity Ratio, Earning per Share, Quick Ratio and Interest Coverage ratio for the years 2017 and 2018. The report analyzes the positive and negative implications of these ratios, highlighting trends and their impact on the business. Furthermore, the report identifies various stakeholders, including shareholders, investors, and financial institutions, who are interested in the published financial reports of Aston Martin and their respective interests. The report uses financial data from Aston Martin's balance sheet and income statement to support its analysis. The analysis reveals insights into Aston Martin's financial health, highlighting areas of strength and weakness, and the report is a valuable resource for understanding the company's financial performance and stakeholder relationships.

Business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY ..................................................................................................................................1

a) To calculate the key ratios covering profitability, efficiency and liquidity and also explain

the ratios ......................................................................................................................................1

b) Importance of the positive and negative outcomes of ratio ....................................................4

c) Group of stakeholders .............................................................................................................5

d) Identifying the stakeholders which are interested in published financial reports....................6

CONCLUSION................................................................................................................................6

REFERANCES ...............................................................................................................................7

Appendix .........................................................................................................................................8

Balance Sheet of Aston Martin ...................................................................................................8

Income Statement.......................................................................................................................10

INTRODUCTION...........................................................................................................................1

MAIN BODY ..................................................................................................................................1

a) To calculate the key ratios covering profitability, efficiency and liquidity and also explain

the ratios ......................................................................................................................................1

b) Importance of the positive and negative outcomes of ratio ....................................................4

c) Group of stakeholders .............................................................................................................5

d) Identifying the stakeholders which are interested in published financial reports....................6

CONCLUSION................................................................................................................................6

REFERANCES ...............................................................................................................................7

Appendix .........................................................................................................................................8

Balance Sheet of Aston Martin ...................................................................................................8

Income Statement.......................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

A business is defined as an corporation or enterprising entity which involves in

commercial, industrial or professional activities. It is organised efforts and activities of

individuals to produce & sell goods in order to gain profit. As the main motive of business is to

earn profit by satisfying the needs of consumers and it is helpful for the purpose of growth. To

better understand this concept Aston Martin has been chosen which is a British Independent

manufacturer of luxury sports cars. In this report, there are various topics has covered such as: to

select 6-8 key ratios covering profitability, efficiency and also explain them, to analyse positive

and negative nature of the ratios incorporating discussion on the movement in the ratios across

years. Apart from this, reports also discuss about to identifying the stakeholders who are

interested in published financial ratios (Weske, 2012).

MAIN BODY

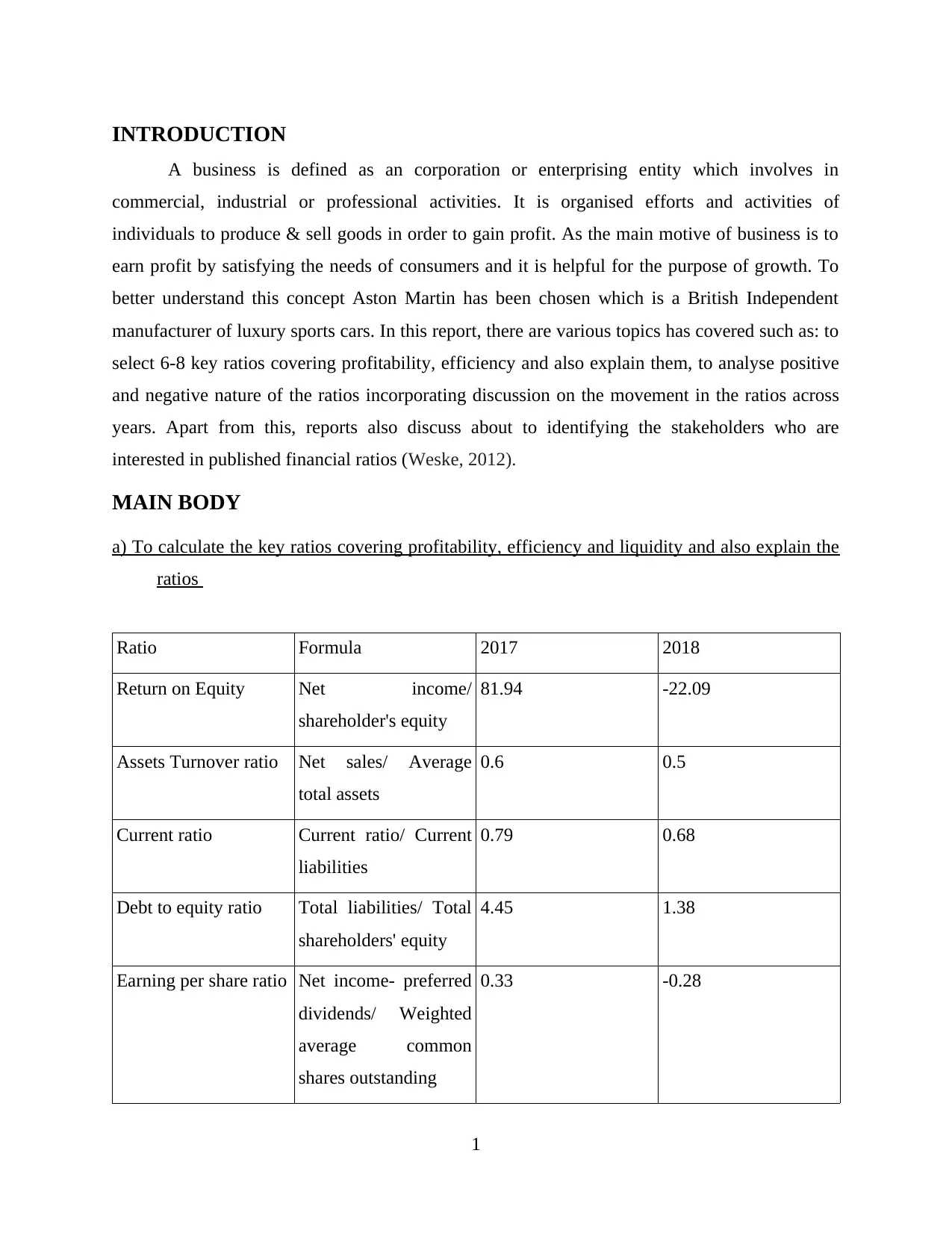

a) To calculate the key ratios covering profitability, efficiency and liquidity and also explain the

ratios

Ratio Formula 2017 2018

Return on Equity Net income/

shareholder's equity

81.94 -22.09

Assets Turnover ratio Net sales/ Average

total assets

0.6 0.5

Current ratio Current ratio/ Current

liabilities

0.79 0.68

Debt to equity ratio Total liabilities/ Total

shareholders' equity

4.45 1.38

Earning per share ratio Net income- preferred

dividends/ Weighted

average common

shares outstanding

0.33 -0.28

1

A business is defined as an corporation or enterprising entity which involves in

commercial, industrial or professional activities. It is organised efforts and activities of

individuals to produce & sell goods in order to gain profit. As the main motive of business is to

earn profit by satisfying the needs of consumers and it is helpful for the purpose of growth. To

better understand this concept Aston Martin has been chosen which is a British Independent

manufacturer of luxury sports cars. In this report, there are various topics has covered such as: to

select 6-8 key ratios covering profitability, efficiency and also explain them, to analyse positive

and negative nature of the ratios incorporating discussion on the movement in the ratios across

years. Apart from this, reports also discuss about to identifying the stakeholders who are

interested in published financial ratios (Weske, 2012).

MAIN BODY

a) To calculate the key ratios covering profitability, efficiency and liquidity and also explain the

ratios

Ratio Formula 2017 2018

Return on Equity Net income/

shareholder's equity

81.94 -22.09

Assets Turnover ratio Net sales/ Average

total assets

0.6 0.5

Current ratio Current ratio/ Current

liabilities

0.79 0.68

Debt to equity ratio Total liabilities/ Total

shareholders' equity

4.45 1.38

Earning per share ratio Net income- preferred

dividends/ Weighted

average common

shares outstanding

0.33 -0.28

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

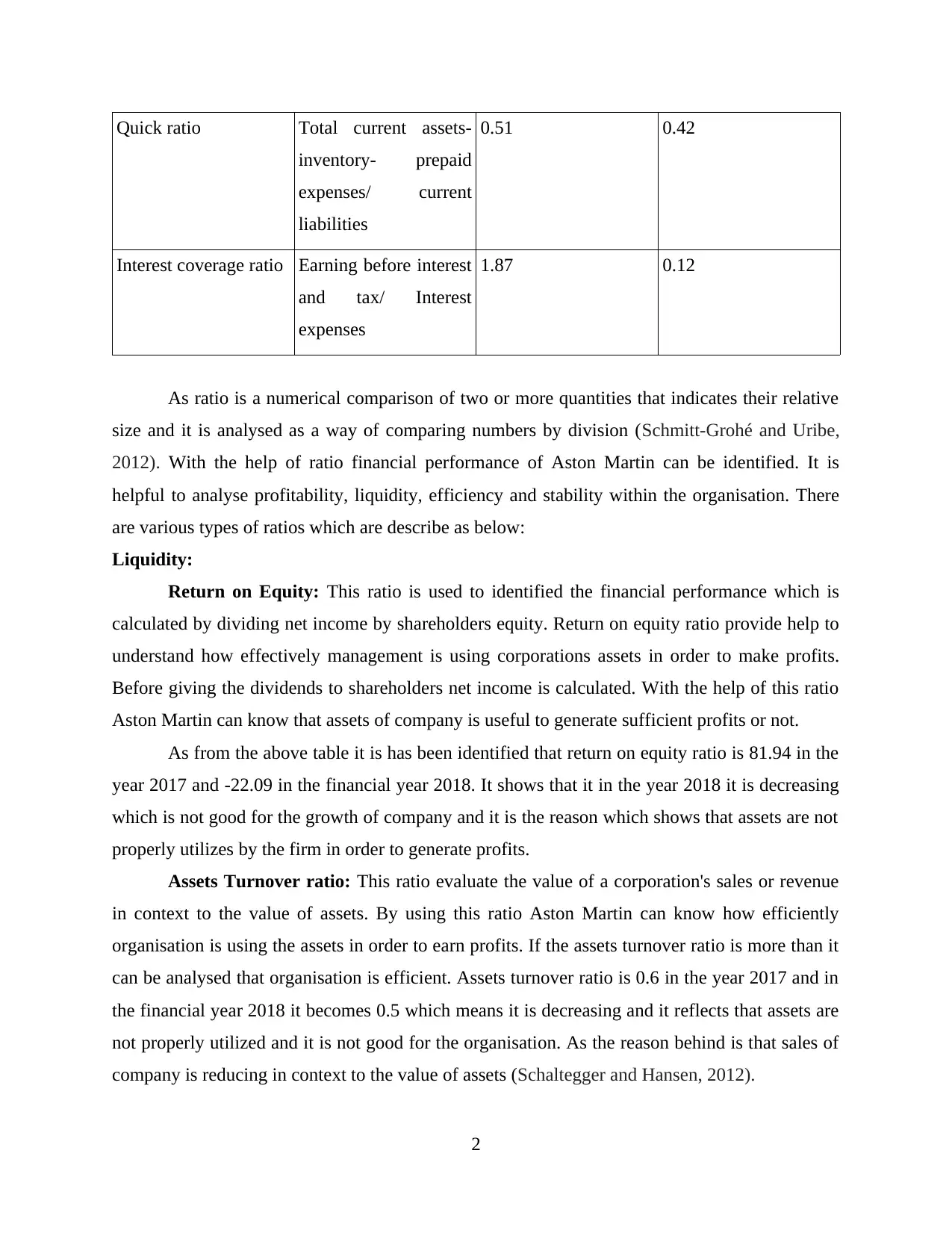

Quick ratio Total current assets-

inventory- prepaid

expenses/ current

liabilities

0.51 0.42

Interest coverage ratio Earning before interest

and tax/ Interest

expenses

1.87 0.12

As ratio is a numerical comparison of two or more quantities that indicates their relative

size and it is analysed as a way of comparing numbers by division (Schmitt‐Grohé and Uribe,

2012). With the help of ratio financial performance of Aston Martin can be identified. It is

helpful to analyse profitability, liquidity, efficiency and stability within the organisation. There

are various types of ratios which are describe as below:

Liquidity:

Return on Equity: This ratio is used to identified the financial performance which is

calculated by dividing net income by shareholders equity. Return on equity ratio provide help to

understand how effectively management is using corporations assets in order to make profits.

Before giving the dividends to shareholders net income is calculated. With the help of this ratio

Aston Martin can know that assets of company is useful to generate sufficient profits or not.

As from the above table it is has been identified that return on equity ratio is 81.94 in the

year 2017 and -22.09 in the financial year 2018. It shows that it in the year 2018 it is decreasing

which is not good for the growth of company and it is the reason which shows that assets are not

properly utilizes by the firm in order to generate profits.

Assets Turnover ratio: This ratio evaluate the value of a corporation's sales or revenue

in context to the value of assets. By using this ratio Aston Martin can know how efficiently

organisation is using the assets in order to earn profits. If the assets turnover ratio is more than it

can be analysed that organisation is efficient. Assets turnover ratio is 0.6 in the year 2017 and in

the financial year 2018 it becomes 0.5 which means it is decreasing and it reflects that assets are

not properly utilized and it is not good for the organisation. As the reason behind is that sales of

company is reducing in context to the value of assets (Schaltegger and Hansen, 2012).

2

inventory- prepaid

expenses/ current

liabilities

0.51 0.42

Interest coverage ratio Earning before interest

and tax/ Interest

expenses

1.87 0.12

As ratio is a numerical comparison of two or more quantities that indicates their relative

size and it is analysed as a way of comparing numbers by division (Schmitt‐Grohé and Uribe,

2012). With the help of ratio financial performance of Aston Martin can be identified. It is

helpful to analyse profitability, liquidity, efficiency and stability within the organisation. There

are various types of ratios which are describe as below:

Liquidity:

Return on Equity: This ratio is used to identified the financial performance which is

calculated by dividing net income by shareholders equity. Return on equity ratio provide help to

understand how effectively management is using corporations assets in order to make profits.

Before giving the dividends to shareholders net income is calculated. With the help of this ratio

Aston Martin can know that assets of company is useful to generate sufficient profits or not.

As from the above table it is has been identified that return on equity ratio is 81.94 in the

year 2017 and -22.09 in the financial year 2018. It shows that it in the year 2018 it is decreasing

which is not good for the growth of company and it is the reason which shows that assets are not

properly utilizes by the firm in order to generate profits.

Assets Turnover ratio: This ratio evaluate the value of a corporation's sales or revenue

in context to the value of assets. By using this ratio Aston Martin can know how efficiently

organisation is using the assets in order to earn profits. If the assets turnover ratio is more than it

can be analysed that organisation is efficient. Assets turnover ratio is 0.6 in the year 2017 and in

the financial year 2018 it becomes 0.5 which means it is decreasing and it reflects that assets are

not properly utilized and it is not good for the organisation. As the reason behind is that sales of

company is reducing in context to the value of assets (Schaltegger and Hansen, 2012).

2

Current ratio: This ratio is helpful to analyse the ability of an organisation to meet the

short term obligations related to a specific period of time. By using it Aston Martin can know

how much assets held by company in order to make short term payment. The ideal current ratio

is 2:1. As it has been analysed that in the year 2017 current ratio is 0.79 where as in the year

2018 it was 0.68 which shows that this ratio is reducing and it is not beneficial for the company.

It shows that current assets are not properly managed in order to fulfil the obligations. The

reason behind is that company does not have sufficient current assets as compare to the current

liability.

Debt to equity ratio: It is a financial liquidity ratio which compares corporation's total

debt to total equity. By using this ratio Aston Martin can measure the financial leverage of

organisation. It shows that ability of shareholder equity to cover all outstanding debts in the

event of a business downturn. In the financial year 2017 debt to equity ratio was 4.45 which

becomes 1.38 in the financial year 2018 which shows that it is decreasing and it is good for the

company because debts is reducing which is the main reason behind it (Kiyotaki and Moore,

2012).

Quick ratio: This ratio identifies that in how much time a company can pay short term

obligation by having assets which are readily convertible into cash and it involves marketable

securities, accounts receivable & cash. By using this ratio Aston Martin can know in how much

time its quick assets can be converted into cash. It has been analysed that quick ratio was 0.51 in

the year 2017 which becomes 0.42 in the year 2018 which is not good because it can minimize

the liquidity.

Efficiency and stability:

Earning per share ratio: EPS is the net earnings of the organisation earned on one

share. With the help of this ratio Aston Martin can measure the amount of net income earned per

share of stock outstanding. It has been analysed that in the year 2017 earning per share was 0.33

which becomes -0.28 in the financial year 2018. It shows that the earning per share of

organisation is reducing that is not good in context to the growth of business.

Interest coverage ratio: This ratio analyse the ability of firm to meet its interest

payments. With the help of it Aston Marin can know how easily it can pay interest expenses on

outstanding debt. As from the above table, it has been analysed that in the year 2017 the interest

coverage ratio was 1.87 where as in the financial year 2018 it is 0.12 which shows that it is

3

short term obligations related to a specific period of time. By using it Aston Martin can know

how much assets held by company in order to make short term payment. The ideal current ratio

is 2:1. As it has been analysed that in the year 2017 current ratio is 0.79 where as in the year

2018 it was 0.68 which shows that this ratio is reducing and it is not beneficial for the company.

It shows that current assets are not properly managed in order to fulfil the obligations. The

reason behind is that company does not have sufficient current assets as compare to the current

liability.

Debt to equity ratio: It is a financial liquidity ratio which compares corporation's total

debt to total equity. By using this ratio Aston Martin can measure the financial leverage of

organisation. It shows that ability of shareholder equity to cover all outstanding debts in the

event of a business downturn. In the financial year 2017 debt to equity ratio was 4.45 which

becomes 1.38 in the financial year 2018 which shows that it is decreasing and it is good for the

company because debts is reducing which is the main reason behind it (Kiyotaki and Moore,

2012).

Quick ratio: This ratio identifies that in how much time a company can pay short term

obligation by having assets which are readily convertible into cash and it involves marketable

securities, accounts receivable & cash. By using this ratio Aston Martin can know in how much

time its quick assets can be converted into cash. It has been analysed that quick ratio was 0.51 in

the year 2017 which becomes 0.42 in the year 2018 which is not good because it can minimize

the liquidity.

Efficiency and stability:

Earning per share ratio: EPS is the net earnings of the organisation earned on one

share. With the help of this ratio Aston Martin can measure the amount of net income earned per

share of stock outstanding. It has been analysed that in the year 2017 earning per share was 0.33

which becomes -0.28 in the financial year 2018. It shows that the earning per share of

organisation is reducing that is not good in context to the growth of business.

Interest coverage ratio: This ratio analyse the ability of firm to meet its interest

payments. With the help of it Aston Marin can know how easily it can pay interest expenses on

outstanding debt. As from the above table, it has been analysed that in the year 2017 the interest

coverage ratio was 1.87 where as in the financial year 2018 it is 0.12 which shows that it is

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

decreasing and it is not good for the firm because it can not make payment of interest to the

creditors (Kastalli and Van Looy, 2013).

b) Importance of the positive and negative outcomes of ratio

With the help of ratio analysis an organisation can know the financial performance of its

business over a period of time. It is beneficial to know stability, liquidity and efficiency of the

firm. The positive outcomes shows that Aston Martin is earning is earning good profits and

business is performing well where as negative outcomes shows that organisation is not

performing well and it is not earning sufficient profits. The importance of positive and negative

outcomes of ratio is describes as below:

Return on Equity: This ratio was positive in the year 2017 and that was 81.94 but it

becomes negative (-22.09) in the year 2018. It shows that Aston Martin is not utilizing the assets

for generating profit so it is important for the firm to increase this ratio so that assets can be used

properly in order to earn more revenue (Gilchrist and Zakrajšek, 2012).

Assets Turnover ratio: This ratio was positive in the year 2017 and it was 0.6 but in the

financial year 2018 it reduce and become 0.5 which is a negative sign for the Aston Martin

because it shows that assets are not properly utilized by the organisation that's why it is not

earning profits form the assets. So it is important for the company to properly used the assets as a

result it can get maximum returns.

Current ratio: In the year 2017 this ratio was positive and it was 0.79 where as in the

year 2018 it minimize & becomes 0.68 which is negative in context to the growth of Aston

Martin. It reflects that current liabilities of firm is increasing as compare to the current assets. So

it is important for the organisation to make it positive so that current assets can be increase and

liabilities can be decrease.

Debt to equity ratio: This ratio was 4.45 in the financial year 2017 which is get reduced

and become1.38 in the year 2018 which is a positive sign for Aston Martin because it is

important for an organisation to reduce the liability so that profits can be maximize.

Earning per share ratio: In the year 2017 this ratio was positive (0.33) where as in the

year 2017 it becomes negative (-0.28) which is not good for Aston Martin. So it is important for

organisation to make better strategies so that earning per share can be increase which is

beneficial for the growth of firm (DaSilva and Trkman, 2014).

4

creditors (Kastalli and Van Looy, 2013).

b) Importance of the positive and negative outcomes of ratio

With the help of ratio analysis an organisation can know the financial performance of its

business over a period of time. It is beneficial to know stability, liquidity and efficiency of the

firm. The positive outcomes shows that Aston Martin is earning is earning good profits and

business is performing well where as negative outcomes shows that organisation is not

performing well and it is not earning sufficient profits. The importance of positive and negative

outcomes of ratio is describes as below:

Return on Equity: This ratio was positive in the year 2017 and that was 81.94 but it

becomes negative (-22.09) in the year 2018. It shows that Aston Martin is not utilizing the assets

for generating profit so it is important for the firm to increase this ratio so that assets can be used

properly in order to earn more revenue (Gilchrist and Zakrajšek, 2012).

Assets Turnover ratio: This ratio was positive in the year 2017 and it was 0.6 but in the

financial year 2018 it reduce and become 0.5 which is a negative sign for the Aston Martin

because it shows that assets are not properly utilized by the organisation that's why it is not

earning profits form the assets. So it is important for the company to properly used the assets as a

result it can get maximum returns.

Current ratio: In the year 2017 this ratio was positive and it was 0.79 where as in the

year 2018 it minimize & becomes 0.68 which is negative in context to the growth of Aston

Martin. It reflects that current liabilities of firm is increasing as compare to the current assets. So

it is important for the organisation to make it positive so that current assets can be increase and

liabilities can be decrease.

Debt to equity ratio: This ratio was 4.45 in the financial year 2017 which is get reduced

and become1.38 in the year 2018 which is a positive sign for Aston Martin because it is

important for an organisation to reduce the liability so that profits can be maximize.

Earning per share ratio: In the year 2017 this ratio was positive (0.33) where as in the

year 2017 it becomes negative (-0.28) which is not good for Aston Martin. So it is important for

organisation to make better strategies so that earning per share can be increase which is

beneficial for the growth of firm (DaSilva and Trkman, 2014).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Quick ratio: This ratio was 0.51 in the year 2017 that it get minimise in the year 2018

and becomes 0.42 which does not good for Aston Martin. For that purpose it is important for

company to make better plans so that quick assets can be converted in cash in very short period.

Interest coverage ratio: As from the above table it has been analysed that in the year

2017 this ratio was 1.87 but in the financial year 2018 it was reduced and becomes 0.12 that is

not good. In this regard, it is important for Aston Martin to formulate better strategies so that it

can pay the interest to the creditors (Boons and Wagner, 2013).

So as a conclusion it can be said that if ratio is positive it means organisation is

performing well and if these are negative than it reflects that company does not performing well

and further improvements are needed for the growth of business.

c) Group of stakeholders

Stakeholders are the persons which are directly or indirectly related to the business of

firm and have some interest in the business of company. Group of stakeholders in context to

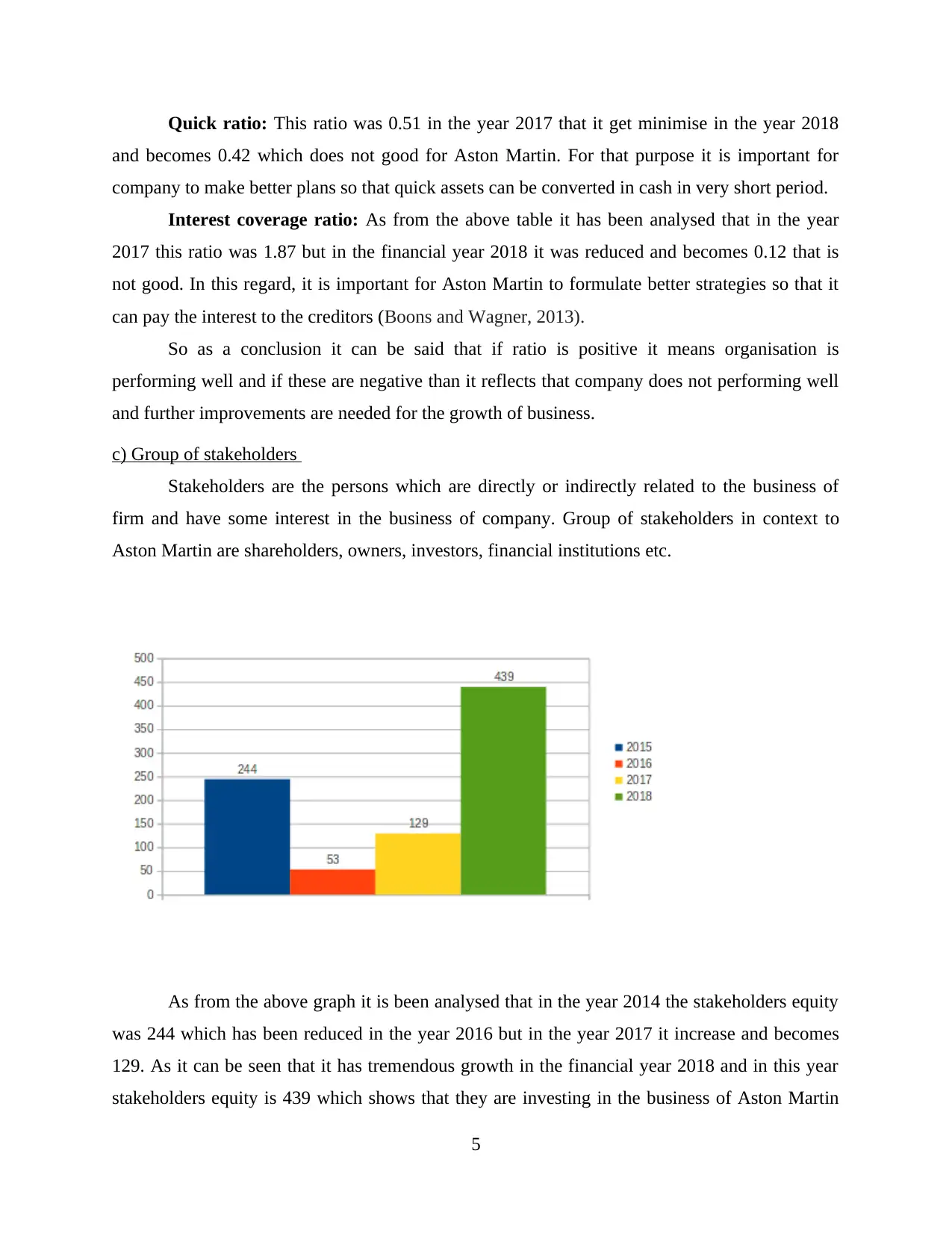

Aston Martin are shareholders, owners, investors, financial institutions etc.

As from the above graph it is been analysed that in the year 2014 the stakeholders equity

was 244 which has been reduced in the year 2016 but in the year 2017 it increase and becomes

129. As it can be seen that it has tremendous growth in the financial year 2018 and in this year

stakeholders equity is 439 which shows that they are investing in the business of Aston Martin

5

and becomes 0.42 which does not good for Aston Martin. For that purpose it is important for

company to make better plans so that quick assets can be converted in cash in very short period.

Interest coverage ratio: As from the above table it has been analysed that in the year

2017 this ratio was 1.87 but in the financial year 2018 it was reduced and becomes 0.12 that is

not good. In this regard, it is important for Aston Martin to formulate better strategies so that it

can pay the interest to the creditors (Boons and Wagner, 2013).

So as a conclusion it can be said that if ratio is positive it means organisation is

performing well and if these are negative than it reflects that company does not performing well

and further improvements are needed for the growth of business.

c) Group of stakeholders

Stakeholders are the persons which are directly or indirectly related to the business of

firm and have some interest in the business of company. Group of stakeholders in context to

Aston Martin are shareholders, owners, investors, financial institutions etc.

As from the above graph it is been analysed that in the year 2014 the stakeholders equity

was 244 which has been reduced in the year 2016 but in the year 2017 it increase and becomes

129. As it can be seen that it has tremendous growth in the financial year 2018 and in this year

stakeholders equity is 439 which shows that they are investing in the business of Aston Martin

5

which is good for the growth of company. Stakeholders Group are investing in the organisation

which is helpful to expand the business and earn more profits (Bilbiie and Melitz, 2012).

d) Identifying the stakeholders which are interested in published financial reports

An organisation have different types of stakeholders which are interested in the published

financial reports and in this context Aston Martin has different stakeholders which are as

mention below:

Shareholders or investors: These are those persons who invest in the business of firm in

order to get higher returns. Before making investment they analyse the recent financial report

which is published by Aston Martin. They are interest in published financial reports because on

the basis of it they can take investment decision whether they have to invest in the shares or not.

As because financial reports provide the financial position of company and for investors it is

helpful to take investment decision.

Financial institutions: These are the big corporations which provide loan to the Aston

Martin. They are interested in financial reports so that they can decide how much loan should be

given and if financial position of firm is not good as per the information of financial reports than

financial institutions will not provide loan (Bell and Harley, 2018).

Government: It is also interested in published financial report of Aston Martin so that

government can determine the tax liability of the company.

CONCLUSION

As from the above report, it has been analysed that with the help of ratio analysis

company can determine stability, efficiency, profitability and liquidity of business. It is

important to know the positive and negative nature of ratios so that movement of ratios can be

analysed over the years. There are various stakeholders which are interested in financial reports

so that they can take better decisions in context to the investment.

6

which is helpful to expand the business and earn more profits (Bilbiie and Melitz, 2012).

d) Identifying the stakeholders which are interested in published financial reports

An organisation have different types of stakeholders which are interested in the published

financial reports and in this context Aston Martin has different stakeholders which are as

mention below:

Shareholders or investors: These are those persons who invest in the business of firm in

order to get higher returns. Before making investment they analyse the recent financial report

which is published by Aston Martin. They are interest in published financial reports because on

the basis of it they can take investment decision whether they have to invest in the shares or not.

As because financial reports provide the financial position of company and for investors it is

helpful to take investment decision.

Financial institutions: These are the big corporations which provide loan to the Aston

Martin. They are interested in financial reports so that they can decide how much loan should be

given and if financial position of firm is not good as per the information of financial reports than

financial institutions will not provide loan (Bell and Harley, 2018).

Government: It is also interested in published financial report of Aston Martin so that

government can determine the tax liability of the company.

CONCLUSION

As from the above report, it has been analysed that with the help of ratio analysis

company can determine stability, efficiency, profitability and liquidity of business. It is

important to know the positive and negative nature of ratios so that movement of ratios can be

analysed over the years. There are various stakeholders which are interested in financial reports

so that they can take better decisions in context to the investment.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERANCES

Books and Journals

Bell, E., Bryman, A. and Harley, B., 2018. Business research methods. Oxford university press.

Bilbiie, F. O., Ghironi, F. and Melitz, M. J., 2012. Endogenous entry, product variety, and

business cycles. Journal of Political Economy.120(2). pp.304-345.

Boons, F., Montalvo, C., Quist, J. and Wagner, M., 2013. Sustainable innovation, business

models and economic performance: an overview. Journal of Cleaner Production.45.

pp.1-8.

DaSilva, C. M. and Trkman, P., 2014. Business model: What it is and what it is not. Long range

planning.47(6). pp.379-389.

Gilchrist, S. and Zakrajšek, E., 2012. Credit spreads and business cycle fluctuations. American

Economic Review.102(4). pp.1692-1720.

Kastalli, I. V. and Van Looy, B., 2013. Servitization: Disentangling the impact of service

business model innovation on manufacturing firm performance. Journal of Operations

Management.31(4). pp.169-180.

Kiyotaki, N. and Moore, J., 2012. Liquidity, business cycles, and monetary policy.

Schaltegger, S., Lüdeke-Freund, F. and Hansen, E. G., 2012. Business cases for sustainability:

the role of business model innovation for corporate sustainability. International Journal

of Innovation and Sustainable Development.6(2). pp.95-119.

Schmitt‐Grohé, S. and Uribe, M., 2012. What's news in business cycles. Econometrica.80(6).

pp.2733-2764.

Weske, M., 2012. Business process management architectures. In Business Process Management

(pp. 333-371). Springer, Berlin, Heidelberg.

7

Books and Journals

Bell, E., Bryman, A. and Harley, B., 2018. Business research methods. Oxford university press.

Bilbiie, F. O., Ghironi, F. and Melitz, M. J., 2012. Endogenous entry, product variety, and

business cycles. Journal of Political Economy.120(2). pp.304-345.

Boons, F., Montalvo, C., Quist, J. and Wagner, M., 2013. Sustainable innovation, business

models and economic performance: an overview. Journal of Cleaner Production.45.

pp.1-8.

DaSilva, C. M. and Trkman, P., 2014. Business model: What it is and what it is not. Long range

planning.47(6). pp.379-389.

Gilchrist, S. and Zakrajšek, E., 2012. Credit spreads and business cycle fluctuations. American

Economic Review.102(4). pp.1692-1720.

Kastalli, I. V. and Van Looy, B., 2013. Servitization: Disentangling the impact of service

business model innovation on manufacturing firm performance. Journal of Operations

Management.31(4). pp.169-180.

Kiyotaki, N. and Moore, J., 2012. Liquidity, business cycles, and monetary policy.

Schaltegger, S., Lüdeke-Freund, F. and Hansen, E. G., 2012. Business cases for sustainability:

the role of business model innovation for corporate sustainability. International Journal

of Innovation and Sustainable Development.6(2). pp.95-119.

Schmitt‐Grohé, S. and Uribe, M., 2012. What's news in business cycles. Econometrica.80(6).

pp.2733-2764.

Weske, M., 2012. Business process management architectures. In Business Process Management

(pp. 333-371). Springer, Berlin, Heidelberg.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

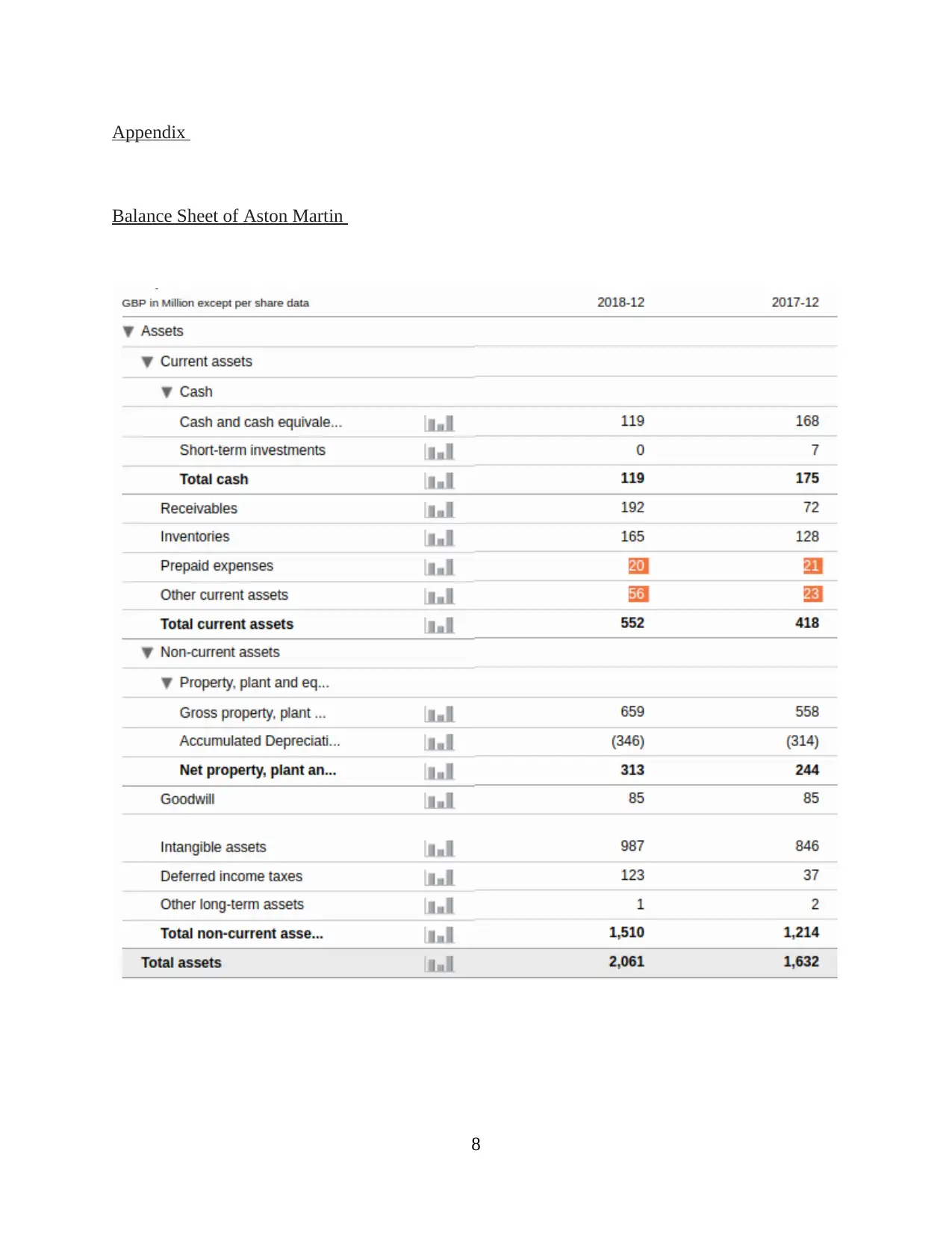

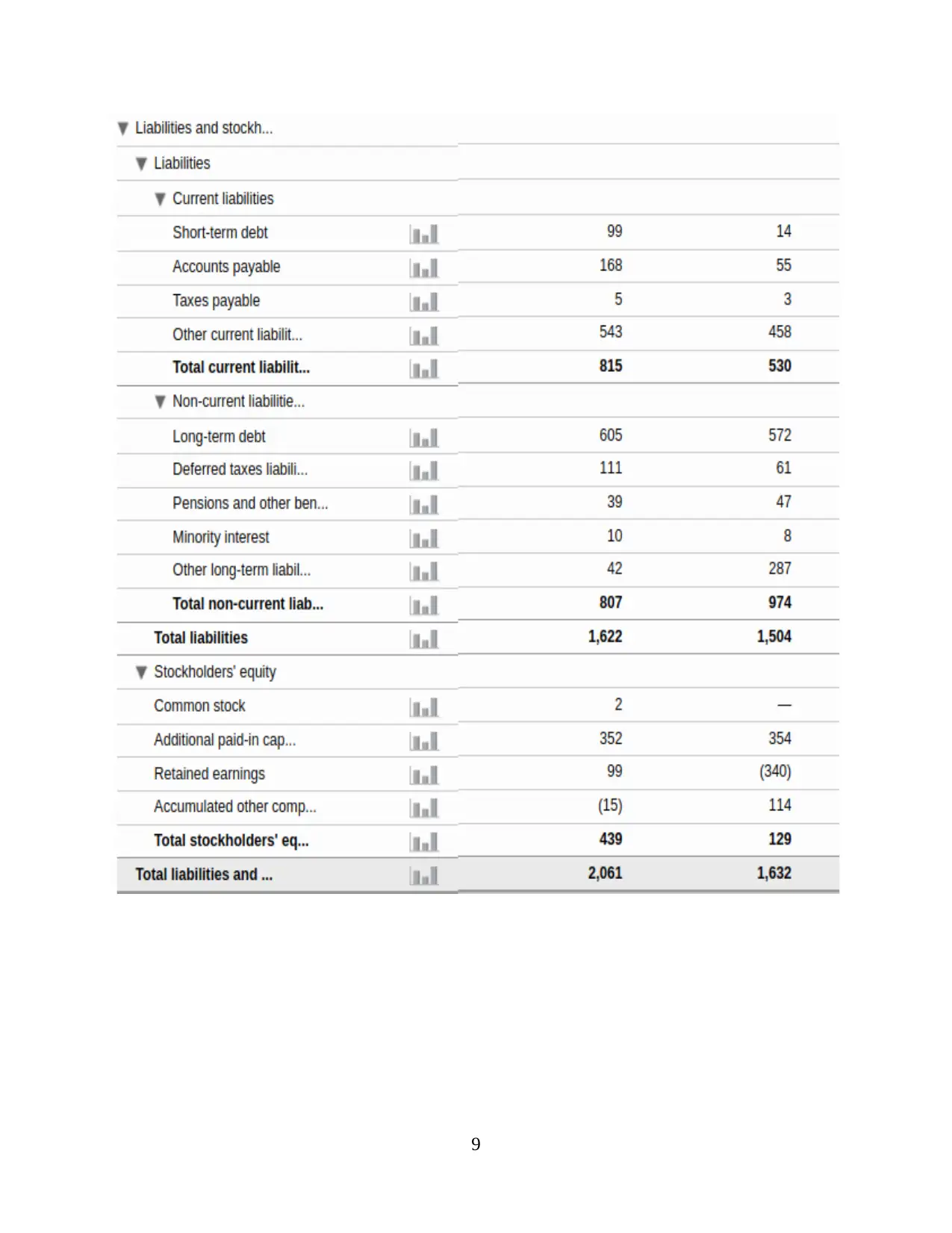

Appendix

Balance Sheet of Aston Martin

8

Balance Sheet of Aston Martin

8

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.