Financial Analysis of Easyflight Plc: Performance and Appraisal

VerifiedAdded on 2021/02/19

|14

|4464

|52

Report

AI Summary

This report provides a comprehensive financial analysis of Easyflight Plc, examining its performance in 2017 and 2018. Part 1 focuses on business performance analysis, including statements of profit or loss, financial position, and cash flows, along with market segment analysis for England, France, and Scotland. Ratio analysis is used to evaluate profitability (gross and net profit margins) and liquidity (current and quick ratios). Part 2 delves into investment appraisal, covering management forecasts, investment appraisal techniques, sources of finance, and non-financial factors influencing investment decisions. The analysis highlights key financial metrics, identifies areas for improvement, and offers insights into the company's financial health and strategic direction. The report emphasizes the importance of efficient operations, cost management, and strategic planning for sustained profitability and growth. The report also discusses the operating cash cycle and cash flow margin ratio. Overall, the report provides a detailed assessment of Easyflight Plc's financial performance and its ability to make sound investment decisions.

FINANCIAL DECISION

MAKING

MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

PART 1: BUSINESS PERFORMANCE ANALYSIS....................................................................1

1.1 Statement of profit or Loss ...................................................................................................1

1.2 Statement of Financial Position.............................................................................................2

1.3 Statement of Cash Flows.......................................................................................................4

1.4 Market Segment Analysis......................................................................................................6

PART 2: INVESTMENT APPRAISAL..........................................................................................6

2.1 (A) Management forecast......................................................................................................6

2.1 (B) Investment appraisal techniques......................................................................................6

2.2 Sources of Finance.................................................................................................................8

2.3 Non-financial factors...........................................................................................................10

REFERENCES .............................................................................................................................12

PART 1: BUSINESS PERFORMANCE ANALYSIS....................................................................1

1.1 Statement of profit or Loss ...................................................................................................1

1.2 Statement of Financial Position.............................................................................................2

1.3 Statement of Cash Flows.......................................................................................................4

1.4 Market Segment Analysis......................................................................................................6

PART 2: INVESTMENT APPRAISAL..........................................................................................6

2.1 (A) Management forecast......................................................................................................6

2.1 (B) Investment appraisal techniques......................................................................................6

2.2 Sources of Finance.................................................................................................................8

2.3 Non-financial factors...........................................................................................................10

REFERENCES .............................................................................................................................12

PART 1: BUSINESS PERFORMANCE ANALYSIS

1.1 Statement of profit or Loss

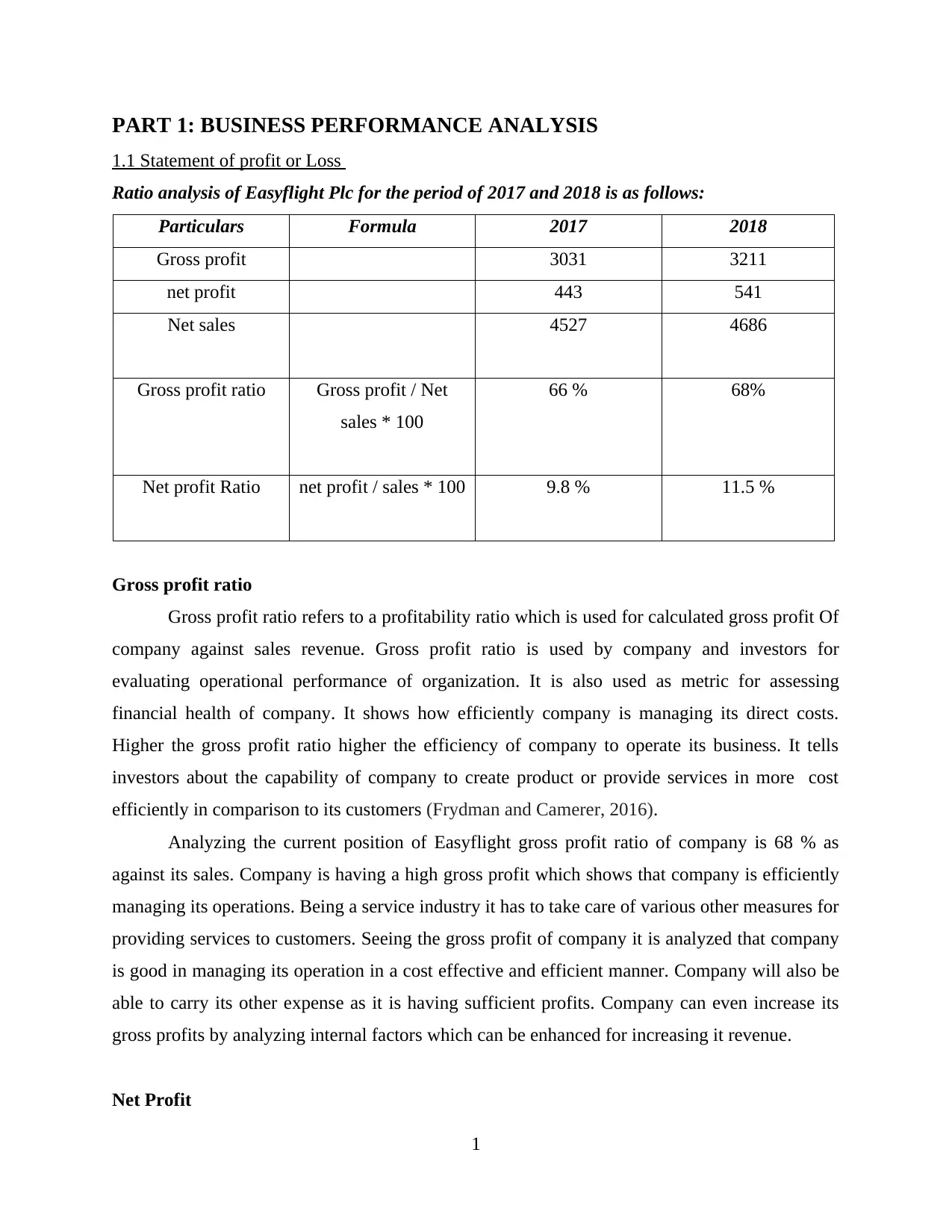

Ratio analysis of Easyflight Plc for the period of 2017 and 2018 is as follows:

Particulars Formula 2017 2018

Gross profit 3031 3211

net profit 443 541

Net sales 4527 4686

Gross profit ratio Gross profit / Net

sales * 100

66 % 68%

Net profit Ratio net profit / sales * 100 9.8 % 11.5 %

Gross profit ratio

Gross profit ratio refers to a profitability ratio which is used for calculated gross profit Of

company against sales revenue. Gross profit ratio is used by company and investors for

evaluating operational performance of organization. It is also used as metric for assessing

financial health of company. It shows how efficiently company is managing its direct costs.

Higher the gross profit ratio higher the efficiency of company to operate its business. It tells

investors about the capability of company to create product or provide services in more cost

efficiently in comparison to its customers (Frydman and Camerer, 2016).

Analyzing the current position of Easyflight gross profit ratio of company is 68 % as

against its sales. Company is having a high gross profit which shows that company is efficiently

managing its operations. Being a service industry it has to take care of various other measures for

providing services to customers. Seeing the gross profit of company it is analyzed that company

is good in managing its operation in a cost effective and efficient manner. Company will also be

able to carry its other expense as it is having sufficient profits. Company can even increase its

gross profits by analyzing internal factors which can be enhanced for increasing it revenue.

Net Profit

1

1.1 Statement of profit or Loss

Ratio analysis of Easyflight Plc for the period of 2017 and 2018 is as follows:

Particulars Formula 2017 2018

Gross profit 3031 3211

net profit 443 541

Net sales 4527 4686

Gross profit ratio Gross profit / Net

sales * 100

66 % 68%

Net profit Ratio net profit / sales * 100 9.8 % 11.5 %

Gross profit ratio

Gross profit ratio refers to a profitability ratio which is used for calculated gross profit Of

company against sales revenue. Gross profit ratio is used by company and investors for

evaluating operational performance of organization. It is also used as metric for assessing

financial health of company. It shows how efficiently company is managing its direct costs.

Higher the gross profit ratio higher the efficiency of company to operate its business. It tells

investors about the capability of company to create product or provide services in more cost

efficiently in comparison to its customers (Frydman and Camerer, 2016).

Analyzing the current position of Easyflight gross profit ratio of company is 68 % as

against its sales. Company is having a high gross profit which shows that company is efficiently

managing its operations. Being a service industry it has to take care of various other measures for

providing services to customers. Seeing the gross profit of company it is analyzed that company

is good in managing its operation in a cost effective and efficient manner. Company will also be

able to carry its other expense as it is having sufficient profits. Company can even increase its

gross profits by analyzing internal factors which can be enhanced for increasing it revenue.

Net Profit

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Net profit ratio is also a profitability ratio that is used for calculating net profits in

percentage terms. It shows with how much amount company is left after incurring all cost and

expenses that are related to production, administration & financing. It is used to analyze strength

of company to manage its operation after production costs that is from gross profits that are

available to company. By analyzing the above ratios it can be said that company has increased its

profits from last year (Harrison, 2016).

Company is presently having Net profit ratio of 11.5 % in year 2018 which is quite good.

Company has gained a rise in its net profit from previous year which shows that company is

putting its efforts for improvements and to increase its profit. Company is required to take steps

and new strategies for better management of its operating cost for increasing its profits.

Company should analyze possible costs that could be reduced so that company's profit can rise.

Company is facing costs mainly at ground handling therefore company should deeply assess the

areas which are unproductive or which are acquiring costs with no returns. Apart from that

company is not having considerable financing cost. It is essential for company to focus on its

operating activities to provide increase returns to investors. Increase in profit will enable

company to have resources that are necessary for expansion plans. Expansion is not possible id

company is not available with adequate profits, therefore it is important to focus on managing its

operations. Company has to manage its operation in such a manner so that is available with

sufficient profits. Profits are very important as they are the main source through which company

will be planning for future activities and plans.

1.2 Statement of Financial Position

Particulars Formula 2017 2018

Current assets (CA) 1382 403

Current liabilities

(CL)

576 538

Stock 121 154

Prepaid expenses 0 0

Quick assets (QA) CA – (Inventory +

prepaid expenses)

1261 249

Current ratio CA / CL 2.4 0.74

2

percentage terms. It shows with how much amount company is left after incurring all cost and

expenses that are related to production, administration & financing. It is used to analyze strength

of company to manage its operation after production costs that is from gross profits that are

available to company. By analyzing the above ratios it can be said that company has increased its

profits from last year (Harrison, 2016).

Company is presently having Net profit ratio of 11.5 % in year 2018 which is quite good.

Company has gained a rise in its net profit from previous year which shows that company is

putting its efforts for improvements and to increase its profit. Company is required to take steps

and new strategies for better management of its operating cost for increasing its profits.

Company should analyze possible costs that could be reduced so that company's profit can rise.

Company is facing costs mainly at ground handling therefore company should deeply assess the

areas which are unproductive or which are acquiring costs with no returns. Apart from that

company is not having considerable financing cost. It is essential for company to focus on its

operating activities to provide increase returns to investors. Increase in profit will enable

company to have resources that are necessary for expansion plans. Expansion is not possible id

company is not available with adequate profits, therefore it is important to focus on managing its

operations. Company has to manage its operation in such a manner so that is available with

sufficient profits. Profits are very important as they are the main source through which company

will be planning for future activities and plans.

1.2 Statement of Financial Position

Particulars Formula 2017 2018

Current assets (CA) 1382 403

Current liabilities

(CL)

576 538

Stock 121 154

Prepaid expenses 0 0

Quick assets (QA) CA – (Inventory +

prepaid expenses)

1261 249

Current ratio CA / CL 2.4 0.74

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Quick ratio QA / CL 2.18 0.46

Current Ratio

Current ratio is a liquidity ratio which is used for measuring ability of company to pay its

short term obligations or that are due within a year. It is used by investors for assessing how

company can maximize current assets on balance sheet (Frydman and Camerer, 2016). Company

had high current ratio in previous year of 2.4 which shows high strength of company. current

ratio of company has declined to very low level. It shows how much assets are available that can

be liquidated for meeting its current liabilities. Current ratio of Easy flight is 0.74 times which

shows that company is not having enough assets that can be utilized by it for other factors of

company . . High current ratio shows strong position of company to repay its debts and short

term obligations. Company should take necessary steps for evaluating areas that can improve the

effectiveness of company.

Liquid assets are necessary but more than required gives a negative image to investors

about company. They may frame an image of ineffectiveness, inefficiency or lack in managing

its operations. Company is having high trade receivables that shows company is facing problems

of collecting its outstandings company's current assets are high because of trade receivables,

and there is risk factor involved in that case as not all debtors are good and company might have

to face drawback because of bad debts. Company should evaluate the tenure of receivables and

make suitable bad debts provision for managing its further operations. Higher Current ratio of

company shows is considered acceptable as it shows that company is able to meet its liability,

whereas lower current ratio shows that company is at risk of default. At the same time very high

current ratio indicates that the assets of company are not being efficiently used. Company has to

make appropriate utilization of resources.

Quick Ratio

Quick ratio is also known as acid test ratio, that shows company's ability in meeting its

short term operational needs by using liquid assets of company (Stewart and et.al., 2018). This

3

Current Ratio

Current ratio is a liquidity ratio which is used for measuring ability of company to pay its

short term obligations or that are due within a year. It is used by investors for assessing how

company can maximize current assets on balance sheet (Frydman and Camerer, 2016). Company

had high current ratio in previous year of 2.4 which shows high strength of company. current

ratio of company has declined to very low level. It shows how much assets are available that can

be liquidated for meeting its current liabilities. Current ratio of Easy flight is 0.74 times which

shows that company is not having enough assets that can be utilized by it for other factors of

company . . High current ratio shows strong position of company to repay its debts and short

term obligations. Company should take necessary steps for evaluating areas that can improve the

effectiveness of company.

Liquid assets are necessary but more than required gives a negative image to investors

about company. They may frame an image of ineffectiveness, inefficiency or lack in managing

its operations. Company is having high trade receivables that shows company is facing problems

of collecting its outstandings company's current assets are high because of trade receivables,

and there is risk factor involved in that case as not all debtors are good and company might have

to face drawback because of bad debts. Company should evaluate the tenure of receivables and

make suitable bad debts provision for managing its further operations. Higher Current ratio of

company shows is considered acceptable as it shows that company is able to meet its liability,

whereas lower current ratio shows that company is at risk of default. At the same time very high

current ratio indicates that the assets of company are not being efficiently used. Company has to

make appropriate utilization of resources.

Quick Ratio

Quick ratio is also known as acid test ratio, that shows company's ability in meeting its

short term operational needs by using liquid assets of company (Stewart and et.al., 2018). This

3

ratio is similar to current ratio. Quick ratio is mainly used by lenders for analyzing position of

company to repay its debts. Company is having quick ratio of 0.46 times which is considerable

after deducting inventory it shows more reliable position of company but when compared to

previous years it has declined to very low level as in previous year it was 2.18. The decline may

be because of company has utilized its assets for other activities. By seeing the position of

company by quick ratio it is having enough assets to repay its debt for which it can get loans and

funds when in need. Where a typical analyst will also see that company is having trade

receivables, which can change decision of investors. They also need to assess the capacity of

company to collect its debts. When talking about overall financial position that company is

having sound position I market. Company is having high retained earnings that could be utilized

for various expansion plans as well enhancement of its servicing facilities. It can also be figured

that company do not give more dividends to its shareholders and retains major portion of its

earnings. Retained earnings can also be used for payments of dividend in case where company is

not having adequate profits for distribution. Retained earnings shows that company is not taking

steps towards improvements or innovation. Retain earnings has grown at a considerable rate

therefore it is necessary to assess the sources and transfers. In company's non current assets

property has also increased that shows company has purchased assets for company. Purchase of

assets may be because company is planning to make addition in its flight services or for other

providing other related services.

This ratio is given more preference over current ratio as it gives more reliable results

about company's financial strength. The difference in this ratio is that it does not considers

inventory in current assets and only compares quick assets to current liabilities. Values for quick

ratio vary with company and industry. Theoretically it is considered that high ratio shows that

position of company is better, but analyst and investors compare quick ratio with industry

average. Inventory is not considered as it sometimes becomes difficult for companies their

liquidity (Tamir and et.al., 2015).

1.3 Statement of Cash Flows

Operating Cash Cycle

Operating cycle is defined as length time between purchase time of inventory and time

taken by company to collect cash from accounts receivable. It states the time required by

4

company to repay its debts. Company is having quick ratio of 0.46 times which is considerable

after deducting inventory it shows more reliable position of company but when compared to

previous years it has declined to very low level as in previous year it was 2.18. The decline may

be because of company has utilized its assets for other activities. By seeing the position of

company by quick ratio it is having enough assets to repay its debt for which it can get loans and

funds when in need. Where a typical analyst will also see that company is having trade

receivables, which can change decision of investors. They also need to assess the capacity of

company to collect its debts. When talking about overall financial position that company is

having sound position I market. Company is having high retained earnings that could be utilized

for various expansion plans as well enhancement of its servicing facilities. It can also be figured

that company do not give more dividends to its shareholders and retains major portion of its

earnings. Retained earnings can also be used for payments of dividend in case where company is

not having adequate profits for distribution. Retained earnings shows that company is not taking

steps towards improvements or innovation. Retain earnings has grown at a considerable rate

therefore it is necessary to assess the sources and transfers. In company's non current assets

property has also increased that shows company has purchased assets for company. Purchase of

assets may be because company is planning to make addition in its flight services or for other

providing other related services.

This ratio is given more preference over current ratio as it gives more reliable results

about company's financial strength. The difference in this ratio is that it does not considers

inventory in current assets and only compares quick assets to current liabilities. Values for quick

ratio vary with company and industry. Theoretically it is considered that high ratio shows that

position of company is better, but analyst and investors compare quick ratio with industry

average. Inventory is not considered as it sometimes becomes difficult for companies their

liquidity (Tamir and et.al., 2015).

1.3 Statement of Cash Flows

Operating Cash Cycle

Operating cycle is defined as length time between purchase time of inventory and time

taken by company to collect cash from accounts receivable. It states the time required by

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

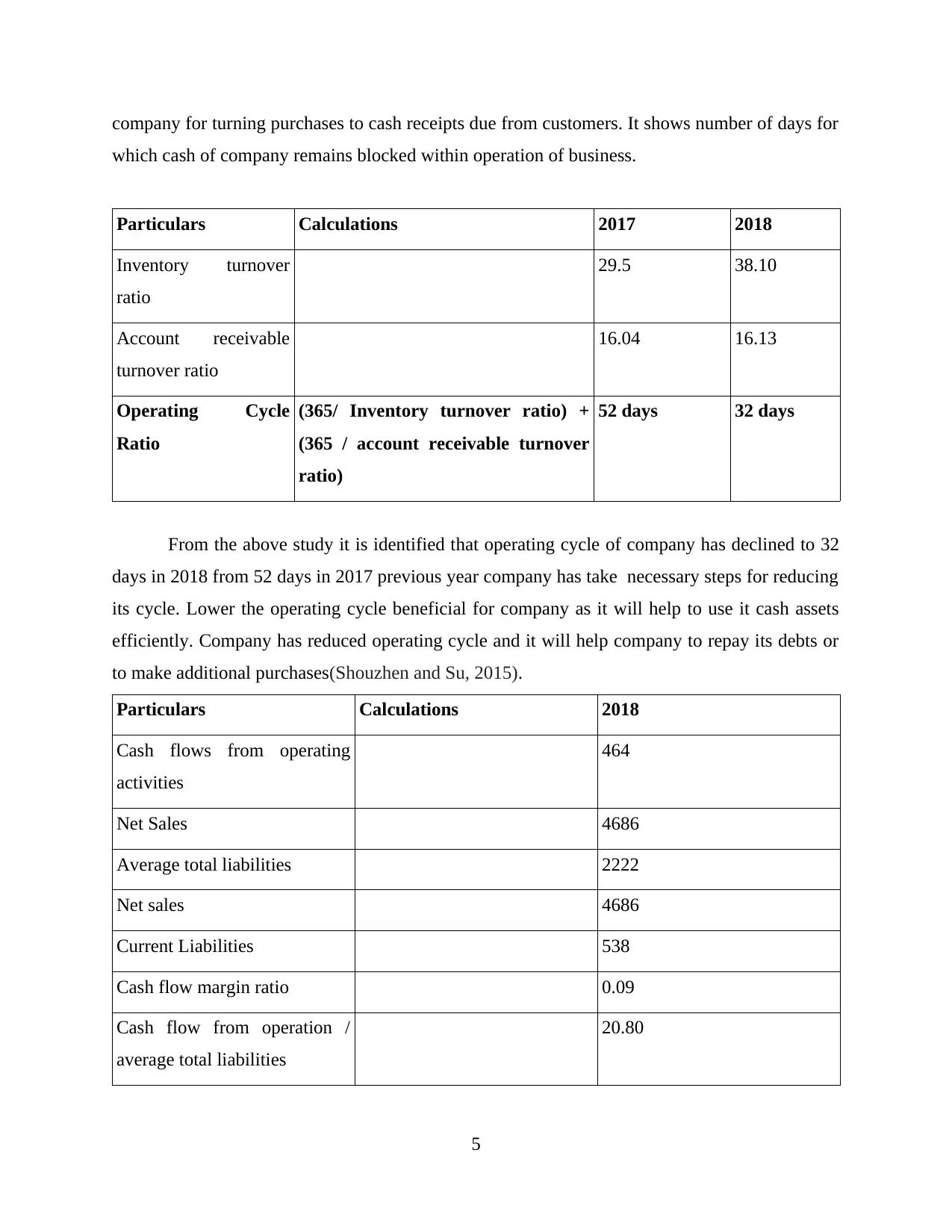

company for turning purchases to cash receipts due from customers. It shows number of days for

which cash of company remains blocked within operation of business.

Particulars Calculations 2017 2018

Inventory turnover

ratio

29.5 38.10

Account receivable

turnover ratio

16.04 16.13

Operating Cycle

Ratio

(365/ Inventory turnover ratio) +

(365 / account receivable turnover

ratio)

52 days 32 days

From the above study it is identified that operating cycle of company has declined to 32

days in 2018 from 52 days in 2017 previous year company has take necessary steps for reducing

its cycle. Lower the operating cycle beneficial for company as it will help to use it cash assets

efficiently. Company has reduced operating cycle and it will help company to repay its debts or

to make additional purchases(Shouzhen and Su, 2015).

Particulars Calculations 2018

Cash flows from operating

activities

464

Net Sales 4686

Average total liabilities 2222

Net sales 4686

Current Liabilities 538

Cash flow margin ratio 0.09

Cash flow from operation /

average total liabilities

20.80

5

which cash of company remains blocked within operation of business.

Particulars Calculations 2017 2018

Inventory turnover

ratio

29.5 38.10

Account receivable

turnover ratio

16.04 16.13

Operating Cycle

Ratio

(365/ Inventory turnover ratio) +

(365 / account receivable turnover

ratio)

52 days 32 days

From the above study it is identified that operating cycle of company has declined to 32

days in 2018 from 52 days in 2017 previous year company has take necessary steps for reducing

its cycle. Lower the operating cycle beneficial for company as it will help to use it cash assets

efficiently. Company has reduced operating cycle and it will help company to repay its debts or

to make additional purchases(Shouzhen and Su, 2015).

Particulars Calculations 2018

Cash flows from operating

activities

464

Net Sales 4686

Average total liabilities 2222

Net sales 4686

Current Liabilities 538

Cash flow margin ratio 0.09

Cash flow from operation /

average total liabilities

20.80

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From analysing cash flows it is identified that company is seen that company has high

cash inflows during the period. Cash flow margin ratio of company is adequate that, low ratio

shows that company makes less cash sales. Operating activities has gone down as company has

paid dividend in current year.

Company has paid dividend in year 2018, and has also made purchases in current year of

property. But it is identified that company has paid dividend because of which net cash flows has

reduced of company. Company should not have paid dividend this year because its purchases of

property.

1.4 Market Segment Analysis

From reports it is analysed that in England company is having gross profit ratio of 63 %

but its net profit is only 10.95 % which shows that company has lacking in managing its

operations with increase in profits. For improving its revenue company should use skimming

pricing policy. For enhancing its operation it should use modern budgeting technique.

In France net profits are 33.04 % which shows that it is efficiently managing its

operations. It is not having high revenues but seeing its position it is efficiently managing its

operations. Penetration pricing policy can be used for increasing its sales. ABC analysis should

be used by company for its operating effectiveness.

Looking at reports of Scotland performance of company is good. It is also having net

profit of 14.72 % which is increase from previous year. Company can still increase its profits by

focusing on operating activities of company. Here also company should use penetration policy. It

should use budgetary technique for properly managing its operation to reduce its expenses.

PART 2: INVESTMENT APPRAISAL

2.1 (A) Management forecast

As per the given exhibit 3, initial investment in France in 2017 was £3000 million.

Management forecast shows that there will be increase in the revenue in coming 10 years. It is

beneficial for Easyflight company to expand its business in France as variable cost is increasing

over a period of time as well as contribution has also increases from 75 to £863 million. Forecast

says that company has earned revenue after deducting debts from £100 million to £1121 million.

2.1 (B) Investment appraisal techniques

Investment appraisal is used to determine attractiveness of investment. There are

collection of techniques through which company assess project viability (Carvalho, Meier and

6

cash inflows during the period. Cash flow margin ratio of company is adequate that, low ratio

shows that company makes less cash sales. Operating activities has gone down as company has

paid dividend in current year.

Company has paid dividend in year 2018, and has also made purchases in current year of

property. But it is identified that company has paid dividend because of which net cash flows has

reduced of company. Company should not have paid dividend this year because its purchases of

property.

1.4 Market Segment Analysis

From reports it is analysed that in England company is having gross profit ratio of 63 %

but its net profit is only 10.95 % which shows that company has lacking in managing its

operations with increase in profits. For improving its revenue company should use skimming

pricing policy. For enhancing its operation it should use modern budgeting technique.

In France net profits are 33.04 % which shows that it is efficiently managing its

operations. It is not having high revenues but seeing its position it is efficiently managing its

operations. Penetration pricing policy can be used for increasing its sales. ABC analysis should

be used by company for its operating effectiveness.

Looking at reports of Scotland performance of company is good. It is also having net

profit of 14.72 % which is increase from previous year. Company can still increase its profits by

focusing on operating activities of company. Here also company should use penetration policy. It

should use budgetary technique for properly managing its operation to reduce its expenses.

PART 2: INVESTMENT APPRAISAL

2.1 (A) Management forecast

As per the given exhibit 3, initial investment in France in 2017 was £3000 million.

Management forecast shows that there will be increase in the revenue in coming 10 years. It is

beneficial for Easyflight company to expand its business in France as variable cost is increasing

over a period of time as well as contribution has also increases from 75 to £863 million. Forecast

says that company has earned revenue after deducting debts from £100 million to £1121 million.

2.1 (B) Investment appraisal techniques

Investment appraisal is used to determine attractiveness of investment. There are

collection of techniques through which company assess project viability (Carvalho, Meier and

6

Wang, 2016). Easyflight company use these techniques in measuring the cash flows and then

give priority to projects accordingly. There are various techniques which are as follows:

Payback period:

It is one of the most effective techniques used by companies to measure risk associated

with investment. It identifies the total time required to recover funds invested time taken to reach

breakeven point. This investment technique is suitable for small investment projects. It is

important to evaluate and determine the time taken for cash flows of project to pay the initial

investment of the project. It is used by the management of company in effective decision

making (Frydman and Camerer, 2016). Thus, it is beneficial for Easyflight if its payback period

is shortest, firm reaches breakeven point quickly. It is mostly used when liquidity is essential

element to select a project.

Benefits

It assists company in ranking the projects.

It is beneficial for the company which are related to instability, change in technology and

uncertainty because it does not allow cash flow projection beyond a period.

Limitations

Payback ignores time value of money so it cannot determine the selection of right project.

It ignores profitability of project as if there is short payback period that doesn't means

that it cannot generate profits (Francis and et.al., 2015).

From the exhibit 3 it can be interpreted that Easyflight payback period is approximately 7

years and 11 months and the total time taken to complete the project is 8 years. If firm invest in

France than breakeven point will arise in 7 years 11 months.

Accounting rate of return:

It is the return expected on the initial investments in percentage. Higher the ARR higher

is the return and vice versa. It is used to compare the returns of ARR and management of

company in order to reject or accept the project. It is beneficial for Easyflight in decision making

and earn higher return (Stewart and et.al., 2018).

Benefits

No other reports are used in determining ARR as accounting information is taken as base.

ARR measure the profitability of investment.

Share options are available to employees as a part of incentive.

7

give priority to projects accordingly. There are various techniques which are as follows:

Payback period:

It is one of the most effective techniques used by companies to measure risk associated

with investment. It identifies the total time required to recover funds invested time taken to reach

breakeven point. This investment technique is suitable for small investment projects. It is

important to evaluate and determine the time taken for cash flows of project to pay the initial

investment of the project. It is used by the management of company in effective decision

making (Frydman and Camerer, 2016). Thus, it is beneficial for Easyflight if its payback period

is shortest, firm reaches breakeven point quickly. It is mostly used when liquidity is essential

element to select a project.

Benefits

It assists company in ranking the projects.

It is beneficial for the company which are related to instability, change in technology and

uncertainty because it does not allow cash flow projection beyond a period.

Limitations

Payback ignores time value of money so it cannot determine the selection of right project.

It ignores profitability of project as if there is short payback period that doesn't means

that it cannot generate profits (Francis and et.al., 2015).

From the exhibit 3 it can be interpreted that Easyflight payback period is approximately 7

years and 11 months and the total time taken to complete the project is 8 years. If firm invest in

France than breakeven point will arise in 7 years 11 months.

Accounting rate of return:

It is the return expected on the initial investments in percentage. Higher the ARR higher

is the return and vice versa. It is used to compare the returns of ARR and management of

company in order to reject or accept the project. It is beneficial for Easyflight in decision making

and earn higher return (Stewart and et.al., 2018).

Benefits

No other reports are used in determining ARR as accounting information is taken as base.

ARR measure the profitability of investment.

Share options are available to employees as a part of incentive.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Limitations

ARR methods dismiss time factor.

There is no benchmarking system to decide whether project need to be rejected or not.

Company uses net income instead of cash flows and net income may be manipulated

which may not provide accurate return (Chambers, Echenique and Saito, 2016).

It can be interpreted that ARR or rate of return on investment of Easyflight is 11.4%.

ARR is neither high nor lower so Easyflight can make investments in France and earn return of

11.4%.

Net present value:

NPV is variation between present value of cash inflows and outflows. It is used by

company in planning and analyzing profitability associated with investment. If NPV is higher

than it is said that company will get higher return.

It gives importance to time factor which makes it accurate.

High priority is given to risk and profitability.

It assists in deciding profitability with the help of cash flows instead of profits.

Limitations

It is not useful in comparing two projects.

It requires prediction of cash flows which may be sometimes incorrect (Mitchell,

Hammond and Utkus, 2017).

There is difficulty in determining accurate cost of capital.

From the exhibit 3 it can be interpreted that Easyflight NPV is 830. It is beneficial for

company to invest in France as the future value of investment after 10 years is 3000. It is

concluded that company will increase its revenue by investing in France.

2.2 Sources of Finance

As Easyflight want to invest in airport retail business in 2019 for which company need

funds. There are various sources of funds such as retained earnings, term loans, bank loan,

working capital loan and venture capitalist etc. Easyflight may use its retained earnings and take

bank loan for funds (Tamir and et.al., 2015).

Bank loan:

It is one of the most easiest and common form for taking fund. Bank provides medium

and long term loans with various interest rates according to the bank. Bank loan is beneficial for

8

ARR methods dismiss time factor.

There is no benchmarking system to decide whether project need to be rejected or not.

Company uses net income instead of cash flows and net income may be manipulated

which may not provide accurate return (Chambers, Echenique and Saito, 2016).

It can be interpreted that ARR or rate of return on investment of Easyflight is 11.4%.

ARR is neither high nor lower so Easyflight can make investments in France and earn return of

11.4%.

Net present value:

NPV is variation between present value of cash inflows and outflows. It is used by

company in planning and analyzing profitability associated with investment. If NPV is higher

than it is said that company will get higher return.

It gives importance to time factor which makes it accurate.

High priority is given to risk and profitability.

It assists in deciding profitability with the help of cash flows instead of profits.

Limitations

It is not useful in comparing two projects.

It requires prediction of cash flows which may be sometimes incorrect (Mitchell,

Hammond and Utkus, 2017).

There is difficulty in determining accurate cost of capital.

From the exhibit 3 it can be interpreted that Easyflight NPV is 830. It is beneficial for

company to invest in France as the future value of investment after 10 years is 3000. It is

concluded that company will increase its revenue by investing in France.

2.2 Sources of Finance

As Easyflight want to invest in airport retail business in 2019 for which company need

funds. There are various sources of funds such as retained earnings, term loans, bank loan,

working capital loan and venture capitalist etc. Easyflight may use its retained earnings and take

bank loan for funds (Tamir and et.al., 2015).

Bank loan:

It is one of the most easiest and common form for taking fund. Bank provides medium

and long term loans with various interest rates according to the bank. Bank loan is beneficial for

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

investing in plant & machinery, land and buildings etc. Banks charge lower rate of interest. Bank

grant loans to companies by checking and evaluating their financial statements whether the

company is capable of repaying back the amount of loan with interest. Loan is given for specific

period of time and is expected to be repaid with interest.

Benefits

Flexibility: Bank loan is flexible for organizations, there is no need to make regular

installments rather when bank demands full amount is paid (Smith and et.al., 2018).

Cost effective: Bank loans are cheap in position of interest rate as compared to credit

cards and overdrafts. Having lower interest rate, company prefer bank loan over credit

cards.

Ownership: Bank does not have any ownership on the company after giving loan. Whole

ownership is with the company. Bank does not have any right to monitor who company is

using the funds.

Limitations

Strict requirements: For granting bank loans there are some requirements that need to be

fulfilled by the company. Bank needs some security in return like collateral, assets etc

(Guastello, 2016). Company need to be capable of repaying the money back with interest.

It is find by evaluating financial statements of the company.

Repayment burden: There is a need to make periodic payment to banks which may create

burden upon companies. If companies make late payment than bank report to credit

bureaus which make a negative impact on credit scores.

Retained earnings:

It is the amount left called net income after paying all the expenses, dividends. Retained

earnings are personal savings of company. Company may re-invest this money in expanding its

business. The money which is not paid to the shareholders is called retained earnings. It is also

used by the company in emergency situation. It reduces the cost of issuing equity, ownership

remains with the company. It is useful for companies in operating daily activities of business and

further capital investment. The purpose of retained earning is to repay the old debts, meeting

needs of working capital etc (Shouzhen and Su, 2015).

Benefits

9

grant loans to companies by checking and evaluating their financial statements whether the

company is capable of repaying back the amount of loan with interest. Loan is given for specific

period of time and is expected to be repaid with interest.

Benefits

Flexibility: Bank loan is flexible for organizations, there is no need to make regular

installments rather when bank demands full amount is paid (Smith and et.al., 2018).

Cost effective: Bank loans are cheap in position of interest rate as compared to credit

cards and overdrafts. Having lower interest rate, company prefer bank loan over credit

cards.

Ownership: Bank does not have any ownership on the company after giving loan. Whole

ownership is with the company. Bank does not have any right to monitor who company is

using the funds.

Limitations

Strict requirements: For granting bank loans there are some requirements that need to be

fulfilled by the company. Bank needs some security in return like collateral, assets etc

(Guastello, 2016). Company need to be capable of repaying the money back with interest.

It is find by evaluating financial statements of the company.

Repayment burden: There is a need to make periodic payment to banks which may create

burden upon companies. If companies make late payment than bank report to credit

bureaus which make a negative impact on credit scores.

Retained earnings:

It is the amount left called net income after paying all the expenses, dividends. Retained

earnings are personal savings of company. Company may re-invest this money in expanding its

business. The money which is not paid to the shareholders is called retained earnings. It is also

used by the company in emergency situation. It reduces the cost of issuing equity, ownership

remains with the company. It is useful for companies in operating daily activities of business and

further capital investment. The purpose of retained earning is to repay the old debts, meeting

needs of working capital etc (Shouzhen and Su, 2015).

Benefits

9

Expansion and diversification: Companies uses retained earnings in expanding and

developing their business globally. There is no need for company to take loans from

banks as firm has enough savings for further capital investment.

No obligations: If companies issue equity shares than firm has to pay dividends to their

shareholders and if companies take help of debt finance interest need to be paid.

Whereas if company uses retained earnings there is no obligation of paying interests and

dividends.

Limitations

Over capitalization: If company started to invest retained earnings regularly than their

will be insufficient funds. It will create challenge for company in dealing with difficult

situation (Harrison, 2016).

Shareholders criticism: Shareholders are affected by the policy of dividend, if company

invest more retained earnings than it will create disputes among shareholders and

company. Shareholders have ownership stake in the company. They may take decision in

keeping the retained earnings high or low.

From the above discussion of sources of finance it can be recommended that Easyflight

need to invest some of its retained earnings and remaining amount can be taken as bank loan.

Company want to invest £2000 million and there is £1822 million earnings available. It is

beneficial for company to invest some of its retained earnings so that there is no burden of

repayment of loan. Saving some of the retained earnings will lower down shareholders criticism.

2.3 Non-financial factors

There are various non-financial factors which need to be kept in mind by Easyflight

company in planning investment and decision making. These factors are as follows:

Future legislation: Company need to critically analyze the market in which they want to

invest. Company need to compare the legislation's and laws of countries through which

firm take decisions. For instance in UK there are different employee legislation acts,

company need to analyze itself whether it has capability to match the requirements of

current and future legislation (Francis and et.al., 2015). Easyflight want to expand its

business in airport retail thus, firm need to do research about retail business of country in

which they want to expand.

10

developing their business globally. There is no need for company to take loans from

banks as firm has enough savings for further capital investment.

No obligations: If companies issue equity shares than firm has to pay dividends to their

shareholders and if companies take help of debt finance interest need to be paid.

Whereas if company uses retained earnings there is no obligation of paying interests and

dividends.

Limitations

Over capitalization: If company started to invest retained earnings regularly than their

will be insufficient funds. It will create challenge for company in dealing with difficult

situation (Harrison, 2016).

Shareholders criticism: Shareholders are affected by the policy of dividend, if company

invest more retained earnings than it will create disputes among shareholders and

company. Shareholders have ownership stake in the company. They may take decision in

keeping the retained earnings high or low.

From the above discussion of sources of finance it can be recommended that Easyflight

need to invest some of its retained earnings and remaining amount can be taken as bank loan.

Company want to invest £2000 million and there is £1822 million earnings available. It is

beneficial for company to invest some of its retained earnings so that there is no burden of

repayment of loan. Saving some of the retained earnings will lower down shareholders criticism.

2.3 Non-financial factors

There are various non-financial factors which need to be kept in mind by Easyflight

company in planning investment and decision making. These factors are as follows:

Future legislation: Company need to critically analyze the market in which they want to

invest. Company need to compare the legislation's and laws of countries through which

firm take decisions. For instance in UK there are different employee legislation acts,

company need to analyze itself whether it has capability to match the requirements of

current and future legislation (Francis and et.al., 2015). Easyflight want to expand its

business in airport retail thus, firm need to do research about retail business of country in

which they want to expand.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.