Report: Financial Ratio Analysis of DAMAC and Al-Mazaya Holdings

VerifiedAdded on 2020/04/29

|42

|8122

|192

Report

AI Summary

This report presents a detailed financial analysis of DAMAC Properties and Al-Mazaya Holdings, two prominent real estate companies in the Middle East. The analysis focuses on key financial ratios, including operating profit margin, return on capital employed, capital gearing ratio, interest coverage ratio, asset turnover ratio, and P/E ratio, to assess their financial performance. The report examines the companies' missions, visions, and goals, providing context for the financial data. It compares the performance of both companies over two years, highlighting trends and significant changes in their financial health. The analysis also considers industry benchmarks and external factors influencing the companies' profitability and efficiency. The report concludes with an evaluation of each company's strengths and weaknesses, offering insights into their financial positions and future prospects. Appendices include detailed financial data and company overviews.

Running head: ACCOUNT

Account

Name of the student

Name of the university

Author note

Account

Name of the student

Name of the university

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNT

Table of Contents

Part 1..........................................................................................................................................3

Introduction............................................................................................................................3

Ratio analysis and financial performance..............................................................................5

Ratio analysis.........................................................................................................................6

Operating profit margin ratio.................................................................................................7

Return on capital employed...................................................................................................8

Capital gearing ratio...............................................................................................................9

Interest coverage ratio..........................................................................................................10

Asset turnover ratio..............................................................................................................10

P/E ratio................................................................................................................................11

Conclusion............................................................................................................................12

Part 2........................................................................................................................................13

Introduction..........................................................................................................................13

Sources of funds...................................................................................................................14

Final verdict.........................................................................................................................17

Part 3........................................................................................................................................20

Answer to Question 1...........................................................................................................20

Answer to Question 2...........................................................................................................21

Answer to Question 3...........................................................................................................21

Table of Contents

Part 1..........................................................................................................................................3

Introduction............................................................................................................................3

Ratio analysis and financial performance..............................................................................5

Ratio analysis.........................................................................................................................6

Operating profit margin ratio.................................................................................................7

Return on capital employed...................................................................................................8

Capital gearing ratio...............................................................................................................9

Interest coverage ratio..........................................................................................................10

Asset turnover ratio..............................................................................................................10

P/E ratio................................................................................................................................11

Conclusion............................................................................................................................12

Part 2........................................................................................................................................13

Introduction..........................................................................................................................13

Sources of funds...................................................................................................................14

Final verdict.........................................................................................................................17

Part 3........................................................................................................................................20

Answer to Question 1...........................................................................................................20

Answer to Question 2...........................................................................................................21

Answer to Question 3...........................................................................................................21

2ACCOUNT

Answer to Question 4...........................................................................................................23

Answer to Question 5...........................................................................................................24

Answer to Question 6...........................................................................................................25

Answer to Question 7...........................................................................................................25

Answer to Question 8...........................................................................................................26

Answer to Question 9...........................................................................................................26

Answer to Question 10.........................................................................................................27

References................................................................................................................................29

Appendix..................................................................................................................................34

DAMAC Properties..............................................................................................................34

Al-Mazaya Holdings............................................................................................................37

Answer to Question 4...........................................................................................................23

Answer to Question 5...........................................................................................................24

Answer to Question 6...........................................................................................................25

Answer to Question 7...........................................................................................................25

Answer to Question 8...........................................................................................................26

Answer to Question 9...........................................................................................................26

Answer to Question 10.........................................................................................................27

References................................................................................................................................29

Appendix..................................................................................................................................34

DAMAC Properties..............................................................................................................34

Al-Mazaya Holdings............................................................................................................37

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNT

Part 1

Introduction

DAMAC Properties

The DAMAC properties is at forefront of the luxury real estate market of Middle East

since 2002 that delivers leisure, commercial and luxury residential properties all over Saudi

Arabia, UAE, Jordan Qatar, United Kingdom and Lebanon. Making their mark at highest end

of the stylish living, the company cemented the leading place in the industry and it delivers to

almost 20,000 homes with the development portfolio for more than 44,000 units at different

progress stages. It prides itself on the uncompromising commitment for serving excellence

service to the clients irrespective of whether they are assisting the young couple searching for

new homes or providing the advises to the investors with regard to properties. That is why the

company is identified among the leaders with respect to the luxury developers in Middle

East.

The vision of the company is to become the leader in the luxury developer all over the

Middle East and realises that the customers dreams through building the highest quality

commercial, leisure and residential developments. At heart of DAMAC properties the culture

Part 1

Introduction

DAMAC Properties

The DAMAC properties is at forefront of the luxury real estate market of Middle East

since 2002 that delivers leisure, commercial and luxury residential properties all over Saudi

Arabia, UAE, Jordan Qatar, United Kingdom and Lebanon. Making their mark at highest end

of the stylish living, the company cemented the leading place in the industry and it delivers to

almost 20,000 homes with the development portfolio for more than 44,000 units at different

progress stages. It prides itself on the uncompromising commitment for serving excellence

service to the clients irrespective of whether they are assisting the young couple searching for

new homes or providing the advises to the investors with regard to properties. That is why the

company is identified among the leaders with respect to the luxury developers in Middle

East.

The vision of the company is to become the leader in the luxury developer all over the

Middle East and realises that the customers dreams through building the highest quality

commercial, leisure and residential developments. At heart of DAMAC properties the culture

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNT

focuses on the preferences of the customers to deliver the vision to them. For ensuring the

vision development the customers are delivered with highest standards possible, the company

delivers the proper working environment for their talented employees, chooses right partners

and develops the project in the prime locations and utilises the building material that is most

sophisticated.

The mission statement of the company is – “DAMAC Properties, as the leading

developer for luxury real estate, strives to deliver the unique living concepts and dream

homes to the customers from all over the world”.

Al - Mazaya

Al – Mzaya is is well known among the highly thought and most important in the real

estate development entity in Middle East market with various impressive projects. The

company believes that with the requirements of rigorous and strong investment in the sector

and with respect to maintain and create the trust of wide range of investors in Kuwati market

and in the overseas market. The company is engaged in various other fields related to real

estate like ownership, selling and purchasing the lands and developing the land for outside of

Kuwait and inside of the company. The company handles the management, properties of the

parties, investment and operation, renting the hotels, leasing, health clubs, recreational parks,

exhibitions, restaurants, commercial and residential complexes, health resorts and tourists.

focuses on the preferences of the customers to deliver the vision to them. For ensuring the

vision development the customers are delivered with highest standards possible, the company

delivers the proper working environment for their talented employees, chooses right partners

and develops the project in the prime locations and utilises the building material that is most

sophisticated.

The mission statement of the company is – “DAMAC Properties, as the leading

developer for luxury real estate, strives to deliver the unique living concepts and dream

homes to the customers from all over the world”.

Al - Mazaya

Al – Mzaya is is well known among the highly thought and most important in the real

estate development entity in Middle East market with various impressive projects. The

company believes that with the requirements of rigorous and strong investment in the sector

and with respect to maintain and create the trust of wide range of investors in Kuwati market

and in the overseas market. The company is engaged in various other fields related to real

estate like ownership, selling and purchasing the lands and developing the land for outside of

Kuwait and inside of the company. The company handles the management, properties of the

parties, investment and operation, renting the hotels, leasing, health clubs, recreational parks,

exhibitions, restaurants, commercial and residential complexes, health resorts and tourists.

5ACCOUNT

The vision of the company is to be among the market leaders in the sector of the

development of real estate and to work with the targeted prospective and the strong brand

name that will deliver the distinguished products to the customers.

The mission of the company is to –

Develop the land mark projects

Sustain the value added quality for the projects

Develop the human capital with high calibre

Diversify projects for encompassing the wide spectrum for real estate sectors.

Further, as per the message of the cEO, the company’s goals are –

Sidestepping the market risks

Boarding on the new developments in each fiscal years

Deliver and execute periodical sales for the real estate developments

10% growth in the net profits

Managing the debt of the company in sound way and securing the high credit ranking

from the agencies those are internationally recognized.

Ratio analysis and financial performance

Ratio analysis is the quantitative analysis for the contained information in the

financial statement of the company. The analysis of the ratios are based on the line items in

the financial statements of the company like income statement, balance sheet and cash flow

sttaemnet (Amornkitvikai and Harvie 2017). The analysis of ratios is utilised for evaluating

the different aspects of the company’s financial and operating performances with regard to its

liquidity, efficiency, solvency and profitability. The ratio trends over the time is analysed and

compared with the competitors and the industry average to evaluate whether they are

The vision of the company is to be among the market leaders in the sector of the

development of real estate and to work with the targeted prospective and the strong brand

name that will deliver the distinguished products to the customers.

The mission of the company is to –

Develop the land mark projects

Sustain the value added quality for the projects

Develop the human capital with high calibre

Diversify projects for encompassing the wide spectrum for real estate sectors.

Further, as per the message of the cEO, the company’s goals are –

Sidestepping the market risks

Boarding on the new developments in each fiscal years

Deliver and execute periodical sales for the real estate developments

10% growth in the net profits

Managing the debt of the company in sound way and securing the high credit ranking

from the agencies those are internationally recognized.

Ratio analysis and financial performance

Ratio analysis is the quantitative analysis for the contained information in the

financial statement of the company. The analysis of the ratios are based on the line items in

the financial statements of the company like income statement, balance sheet and cash flow

sttaemnet (Amornkitvikai and Harvie 2017). The analysis of ratios is utilised for evaluating

the different aspects of the company’s financial and operating performances with regard to its

liquidity, efficiency, solvency and profitability. The ratio trends over the time is analysed and

compared with the competitors and the industry average to evaluate whether they are

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNT

improving or getting worsen. Though various ratios are there, the invstors are mainly

concerned with the key ratios mainly like profitability ratio, capital gearing ratio, P/E ratio.

Further, most of the companies have the specific range as the benchmark and while the

company’s ratio does not fall within the range then it will be regarded as overvalued and

undervalued based on the ratios (Ashton and Gregoriou 2017).

The ratios are generally compared across various companies from the same sector as

the acceptable ratio in the one industry can be considered as too high for another. For

instance, the companies in the utility sectors may have high ratio for debt-equity, however the

similar ratio for the technology company may be considered as exceptionally high (Babalola

and Abiola 2013). Normally the successful entities have the strong ratios in all aspects and

the hints of the weaknesses in one sector may highlight the significant selling-off the

inventories. Few ratios are closely analyzed as their relevance to the specific sector, for

instance, the inventory turnover for retail sector and the outstanding sales for days for the

technology sectors.

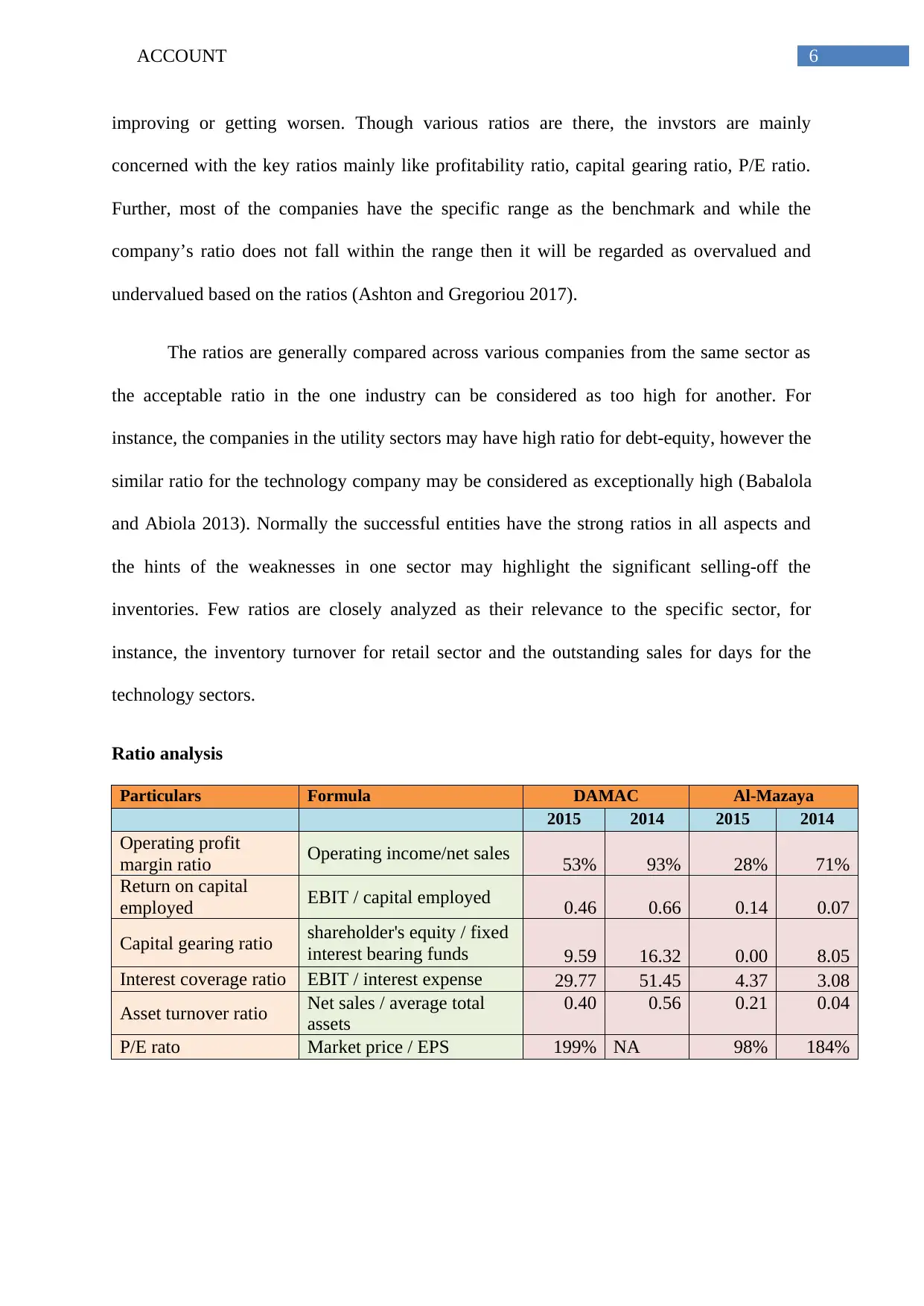

Ratio analysis

Particulars Formula DAMAC Al-Mazaya

2015 2014 2015 2014

Operating profit

margin ratio Operating income/net sales 53% 93% 28% 71%

Return on capital

employed EBIT / capital employed 0.46 0.66 0.14 0.07

Capital gearing ratio shareholder's equity / fixed

interest bearing funds 9.59 16.32 0.00 8.05

Interest coverage ratio EBIT / interest expense 29.77 51.45 4.37 3.08

Asset turnover ratio Net sales / average total

assets

0.40 0.56 0.21 0.04

P/E rato Market price / EPS 199% NA 98% 184%

improving or getting worsen. Though various ratios are there, the invstors are mainly

concerned with the key ratios mainly like profitability ratio, capital gearing ratio, P/E ratio.

Further, most of the companies have the specific range as the benchmark and while the

company’s ratio does not fall within the range then it will be regarded as overvalued and

undervalued based on the ratios (Ashton and Gregoriou 2017).

The ratios are generally compared across various companies from the same sector as

the acceptable ratio in the one industry can be considered as too high for another. For

instance, the companies in the utility sectors may have high ratio for debt-equity, however the

similar ratio for the technology company may be considered as exceptionally high (Babalola

and Abiola 2013). Normally the successful entities have the strong ratios in all aspects and

the hints of the weaknesses in one sector may highlight the significant selling-off the

inventories. Few ratios are closely analyzed as their relevance to the specific sector, for

instance, the inventory turnover for retail sector and the outstanding sales for days for the

technology sectors.

Ratio analysis

Particulars Formula DAMAC Al-Mazaya

2015 2014 2015 2014

Operating profit

margin ratio Operating income/net sales 53% 93% 28% 71%

Return on capital

employed EBIT / capital employed 0.46 0.66 0.14 0.07

Capital gearing ratio shareholder's equity / fixed

interest bearing funds 9.59 16.32 0.00 8.05

Interest coverage ratio EBIT / interest expense 29.77 51.45 4.37 3.08

Asset turnover ratio Net sales / average total

assets

0.40 0.56 0.21 0.04

P/E rato Market price / EPS 199% NA 98% 184%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNT

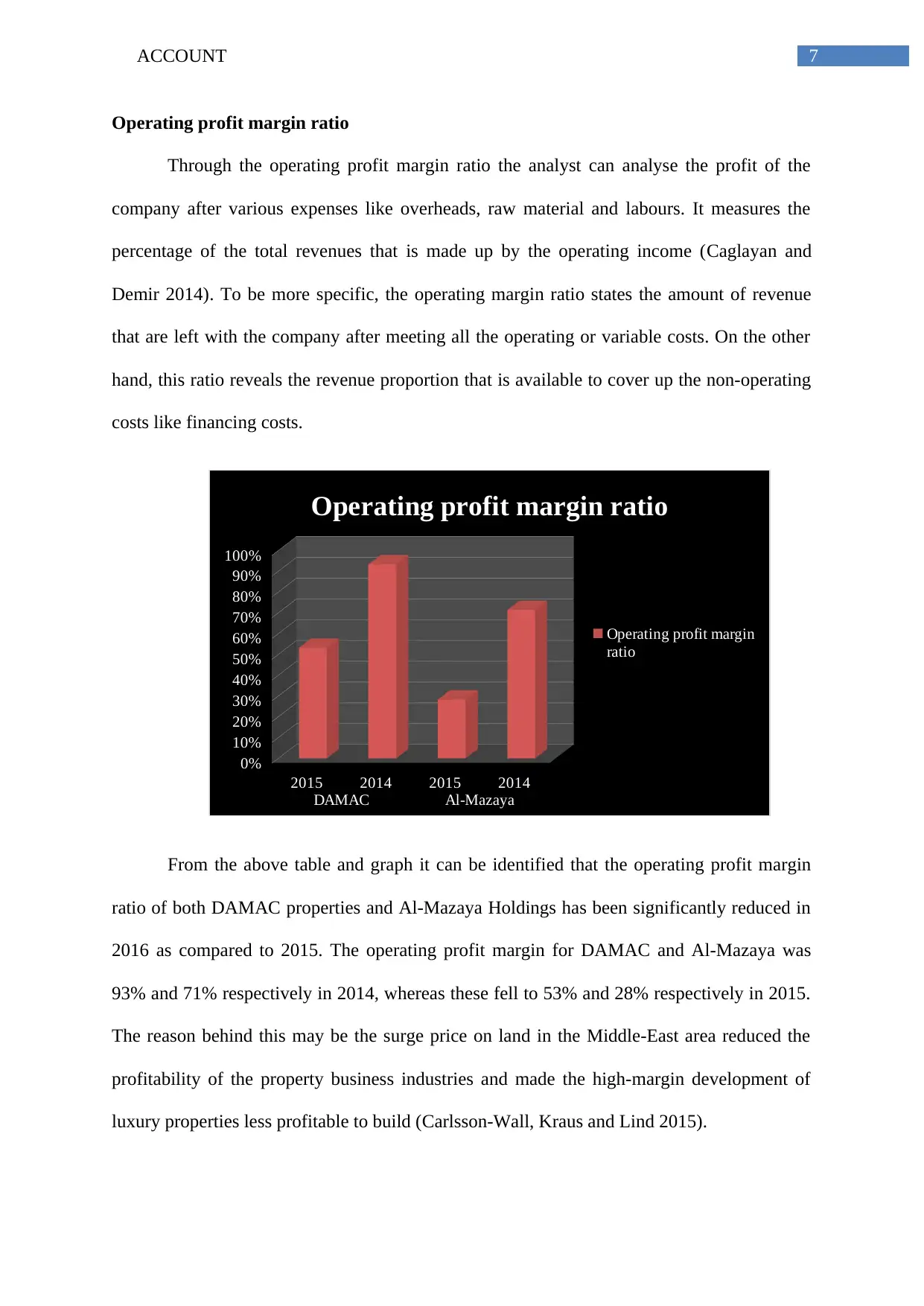

Operating profit margin ratio

Through the operating profit margin ratio the analyst can analyse the profit of the

company after various expenses like overheads, raw material and labours. It measures the

percentage of the total revenues that is made up by the operating income (Caglayan and

Demir 2014). To be more specific, the operating margin ratio states the amount of revenue

that are left with the company after meeting all the operating or variable costs. On the other

hand, this ratio reveals the revenue proportion that is available to cover up the non-operating

costs like financing costs.

2015 2014 2015 2014

DAMAC Al-Mazaya

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Operating profit margin ratio

Operating profit margin

ratio

From the above table and graph it can be identified that the operating profit margin

ratio of both DAMAC properties and Al-Mazaya Holdings has been significantly reduced in

2016 as compared to 2015. The operating profit margin for DAMAC and Al-Mazaya was

93% and 71% respectively in 2014, whereas these fell to 53% and 28% respectively in 2015.

The reason behind this may be the surge price on land in the Middle-East area reduced the

profitability of the property business industries and made the high-margin development of

luxury properties less profitable to build (Carlsson-Wall, Kraus and Lind 2015).

Operating profit margin ratio

Through the operating profit margin ratio the analyst can analyse the profit of the

company after various expenses like overheads, raw material and labours. It measures the

percentage of the total revenues that is made up by the operating income (Caglayan and

Demir 2014). To be more specific, the operating margin ratio states the amount of revenue

that are left with the company after meeting all the operating or variable costs. On the other

hand, this ratio reveals the revenue proportion that is available to cover up the non-operating

costs like financing costs.

2015 2014 2015 2014

DAMAC Al-Mazaya

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Operating profit margin ratio

Operating profit margin

ratio

From the above table and graph it can be identified that the operating profit margin

ratio of both DAMAC properties and Al-Mazaya Holdings has been significantly reduced in

2016 as compared to 2015. The operating profit margin for DAMAC and Al-Mazaya was

93% and 71% respectively in 2014, whereas these fell to 53% and 28% respectively in 2015.

The reason behind this may be the surge price on land in the Middle-East area reduced the

profitability of the property business industries and made the high-margin development of

luxury properties less profitable to build (Carlsson-Wall, Kraus and Lind 2015).

8ACCOUNT

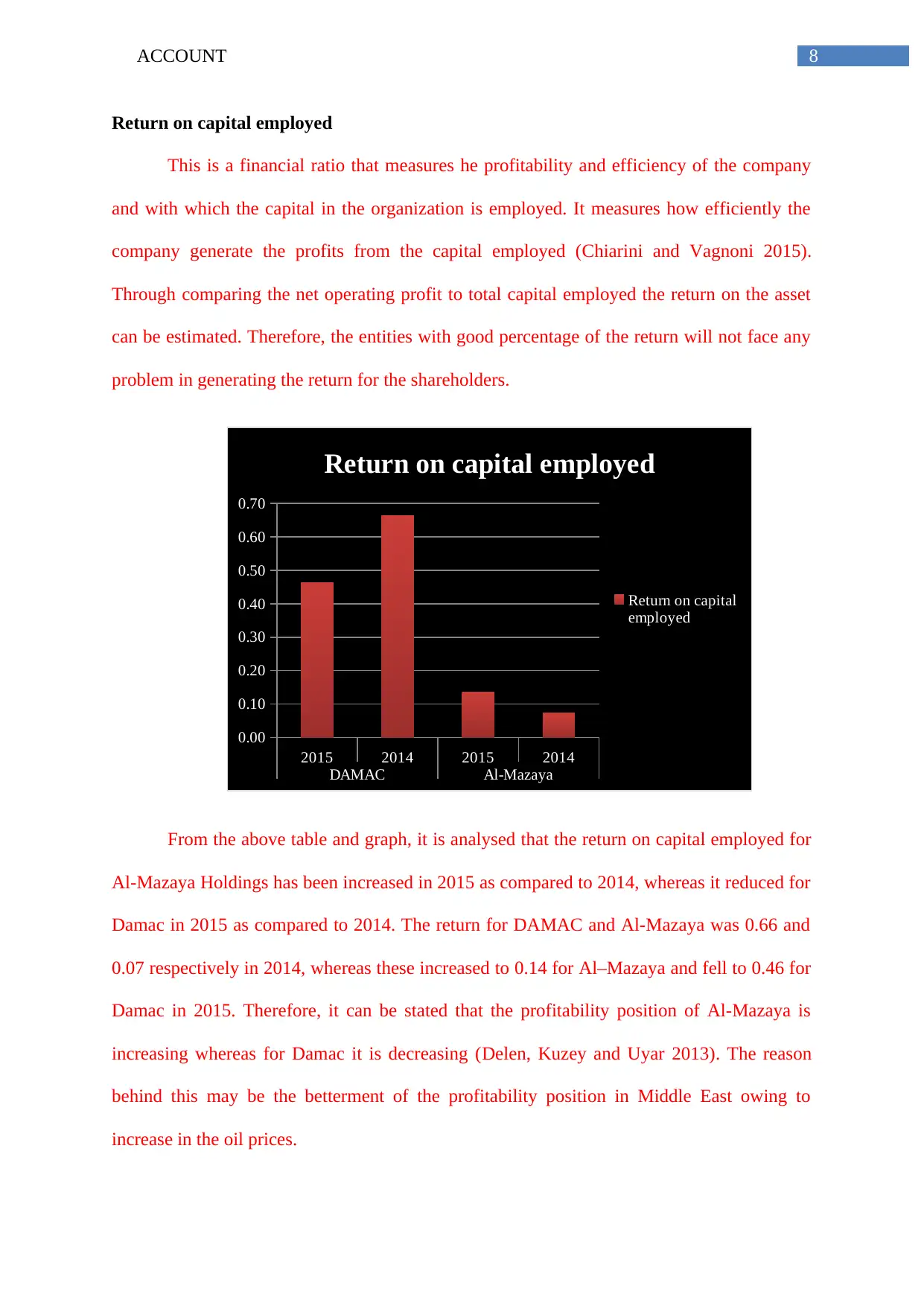

Return on capital employed

This is a financial ratio that measures he profitability and efficiency of the company

and with which the capital in the organization is employed. It measures how efficiently the

company generate the profits from the capital employed (Chiarini and Vagnoni 2015).

Through comparing the net operating profit to total capital employed the return on the asset

can be estimated. Therefore, the entities with good percentage of the return will not face any

problem in generating the return for the shareholders.

2015 2014 2015 2014

DAMAC Al-Mazaya

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

Return on capital employed

Return on capital

employed

From the above table and graph, it is analysed that the return on capital employed for

Al-Mazaya Holdings has been increased in 2015 as compared to 2014, whereas it reduced for

Damac in 2015 as compared to 2014. The return for DAMAC and Al-Mazaya was 0.66 and

0.07 respectively in 2014, whereas these increased to 0.14 for Al–Mazaya and fell to 0.46 for

Damac in 2015. Therefore, it can be stated that the profitability position of Al-Mazaya is

increasing whereas for Damac it is decreasing (Delen, Kuzey and Uyar 2013). The reason

behind this may be the betterment of the profitability position in Middle East owing to

increase in the oil prices.

Return on capital employed

This is a financial ratio that measures he profitability and efficiency of the company

and with which the capital in the organization is employed. It measures how efficiently the

company generate the profits from the capital employed (Chiarini and Vagnoni 2015).

Through comparing the net operating profit to total capital employed the return on the asset

can be estimated. Therefore, the entities with good percentage of the return will not face any

problem in generating the return for the shareholders.

2015 2014 2015 2014

DAMAC Al-Mazaya

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

Return on capital employed

Return on capital

employed

From the above table and graph, it is analysed that the return on capital employed for

Al-Mazaya Holdings has been increased in 2015 as compared to 2014, whereas it reduced for

Damac in 2015 as compared to 2014. The return for DAMAC and Al-Mazaya was 0.66 and

0.07 respectively in 2014, whereas these increased to 0.14 for Al–Mazaya and fell to 0.46 for

Damac in 2015. Therefore, it can be stated that the profitability position of Al-Mazaya is

increasing whereas for Damac it is decreasing (Delen, Kuzey and Uyar 2013). The reason

behind this may be the betterment of the profitability position in Middle East owing to

increase in the oil prices.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNT

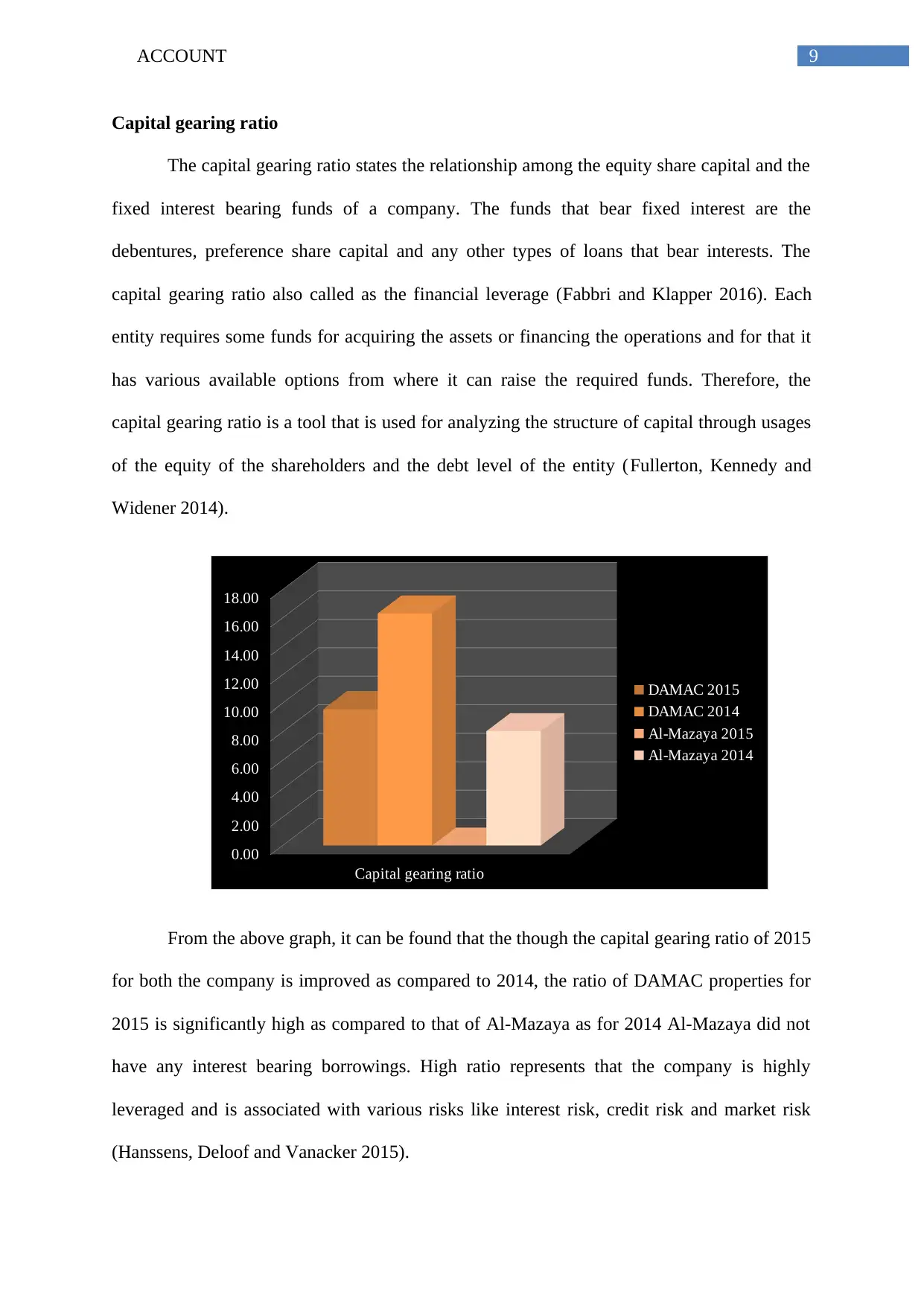

Capital gearing ratio

The capital gearing ratio states the relationship among the equity share capital and the

fixed interest bearing funds of a company. The funds that bear fixed interest are the

debentures, preference share capital and any other types of loans that bear interests. The

capital gearing ratio also called as the financial leverage (Fabbri and Klapper 2016). Each

entity requires some funds for acquiring the assets or financing the operations and for that it

has various available options from where it can raise the required funds. Therefore, the

capital gearing ratio is a tool that is used for analyzing the structure of capital through usages

of the equity of the shareholders and the debt level of the entity (Fullerton, Kennedy and

Widener 2014).

Capital gearing ratio

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

DAMAC 2015

DAMAC 2014

Al-Mazaya 2015

Al-Mazaya 2014

From the above graph, it can be found that the though the capital gearing ratio of 2015

for both the company is improved as compared to 2014, the ratio of DAMAC properties for

2015 is significantly high as compared to that of Al-Mazaya as for 2014 Al-Mazaya did not

have any interest bearing borrowings. High ratio represents that the company is highly

leveraged and is associated with various risks like interest risk, credit risk and market risk

(Hanssens, Deloof and Vanacker 2015).

Capital gearing ratio

The capital gearing ratio states the relationship among the equity share capital and the

fixed interest bearing funds of a company. The funds that bear fixed interest are the

debentures, preference share capital and any other types of loans that bear interests. The

capital gearing ratio also called as the financial leverage (Fabbri and Klapper 2016). Each

entity requires some funds for acquiring the assets or financing the operations and for that it

has various available options from where it can raise the required funds. Therefore, the

capital gearing ratio is a tool that is used for analyzing the structure of capital through usages

of the equity of the shareholders and the debt level of the entity (Fullerton, Kennedy and

Widener 2014).

Capital gearing ratio

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

DAMAC 2015

DAMAC 2014

Al-Mazaya 2015

Al-Mazaya 2014

From the above graph, it can be found that the though the capital gearing ratio of 2015

for both the company is improved as compared to 2014, the ratio of DAMAC properties for

2015 is significantly high as compared to that of Al-Mazaya as for 2014 Al-Mazaya did not

have any interest bearing borrowings. High ratio represents that the company is highly

leveraged and is associated with various risks like interest risk, credit risk and market risk

(Hanssens, Deloof and Vanacker 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNT

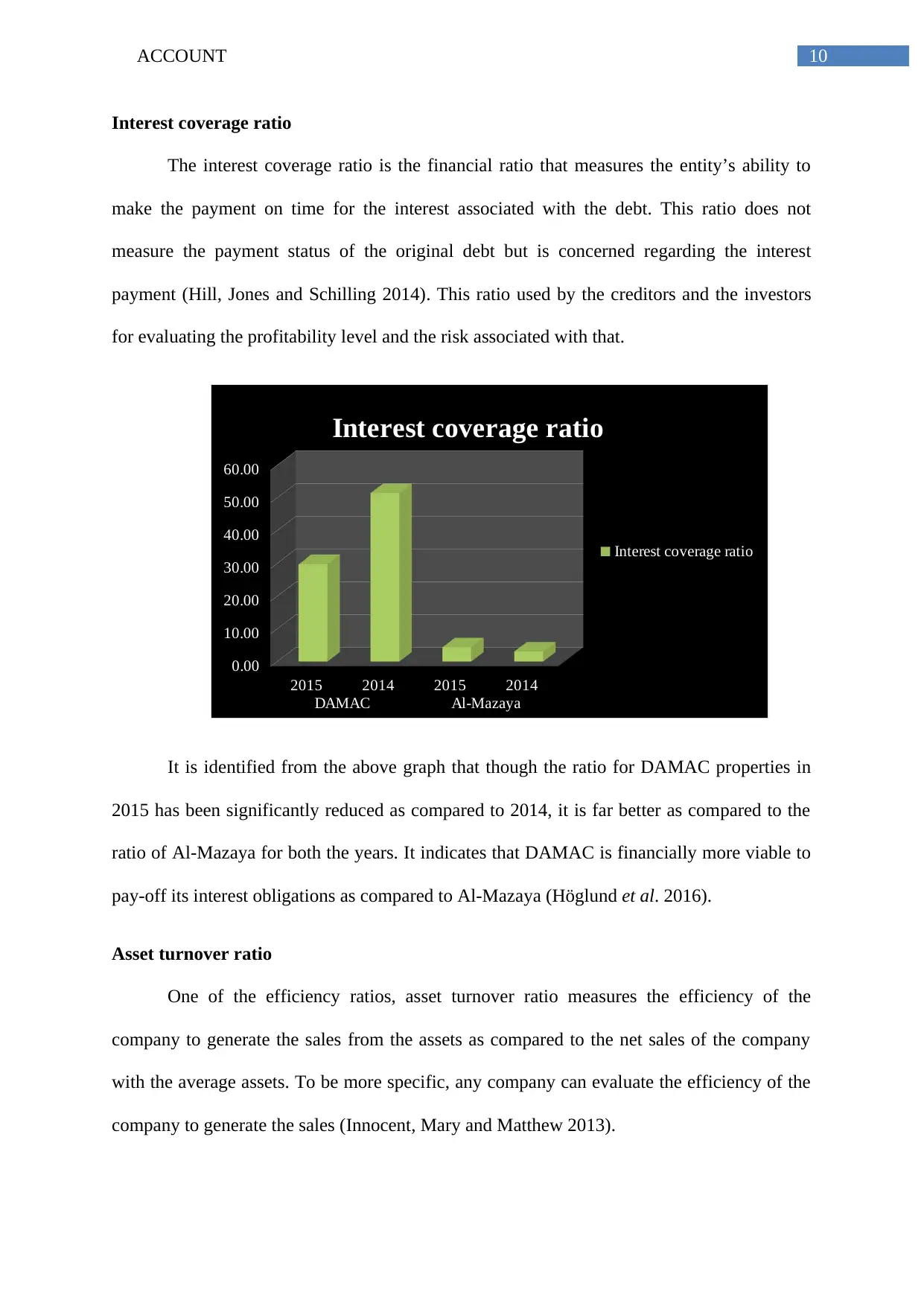

Interest coverage ratio

The interest coverage ratio is the financial ratio that measures the entity’s ability to

make the payment on time for the interest associated with the debt. This ratio does not

measure the payment status of the original debt but is concerned regarding the interest

payment (Hill, Jones and Schilling 2014). This ratio used by the creditors and the investors

for evaluating the profitability level and the risk associated with that.

2015 2014 2015 2014

DAMAC Al-Mazaya

0.00

10.00

20.00

30.00

40.00

50.00

60.00

Interest coverage ratio

Interest coverage ratio

It is identified from the above graph that though the ratio for DAMAC properties in

2015 has been significantly reduced as compared to 2014, it is far better as compared to the

ratio of Al-Mazaya for both the years. It indicates that DAMAC is financially more viable to

pay-off its interest obligations as compared to Al-Mazaya (Höglund et al. 2016).

Asset turnover ratio

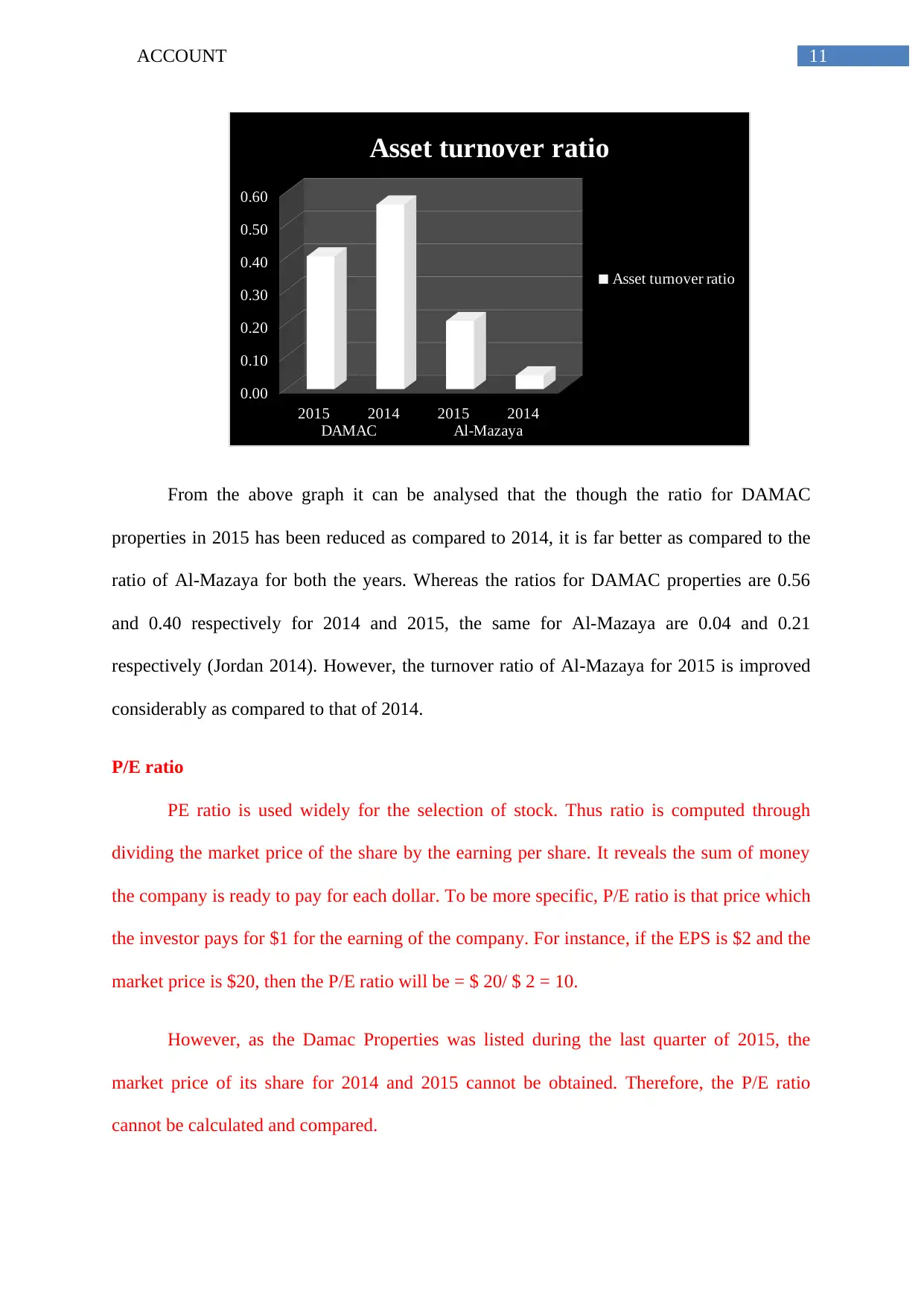

One of the efficiency ratios, asset turnover ratio measures the efficiency of the

company to generate the sales from the assets as compared to the net sales of the company

with the average assets. To be more specific, any company can evaluate the efficiency of the

company to generate the sales (Innocent, Mary and Matthew 2013).

Interest coverage ratio

The interest coverage ratio is the financial ratio that measures the entity’s ability to

make the payment on time for the interest associated with the debt. This ratio does not

measure the payment status of the original debt but is concerned regarding the interest

payment (Hill, Jones and Schilling 2014). This ratio used by the creditors and the investors

for evaluating the profitability level and the risk associated with that.

2015 2014 2015 2014

DAMAC Al-Mazaya

0.00

10.00

20.00

30.00

40.00

50.00

60.00

Interest coverage ratio

Interest coverage ratio

It is identified from the above graph that though the ratio for DAMAC properties in

2015 has been significantly reduced as compared to 2014, it is far better as compared to the

ratio of Al-Mazaya for both the years. It indicates that DAMAC is financially more viable to

pay-off its interest obligations as compared to Al-Mazaya (Höglund et al. 2016).

Asset turnover ratio

One of the efficiency ratios, asset turnover ratio measures the efficiency of the

company to generate the sales from the assets as compared to the net sales of the company

with the average assets. To be more specific, any company can evaluate the efficiency of the

company to generate the sales (Innocent, Mary and Matthew 2013).

11ACCOUNT

2015 2014 2015 2014

DAMAC Al-Mazaya

0.00

0.10

0.20

0.30

0.40

0.50

0.60

Asset turnover ratio

Asset turnover ratio

From the above graph it can be analysed that the though the ratio for DAMAC

properties in 2015 has been reduced as compared to 2014, it is far better as compared to the

ratio of Al-Mazaya for both the years. Whereas the ratios for DAMAC properties are 0.56

and 0.40 respectively for 2014 and 2015, the same for Al-Mazaya are 0.04 and 0.21

respectively (Jordan 2014). However, the turnover ratio of Al-Mazaya for 2015 is improved

considerably as compared to that of 2014.

P/E ratio

PE ratio is used widely for the selection of stock. Thus ratio is computed through

dividing the market price of the share by the earning per share. It reveals the sum of money

the company is ready to pay for each dollar. To be more specific, P/E ratio is that price which

the investor pays for $1 for the earning of the company. For instance, if the EPS is $2 and the

market price is $20, then the P/E ratio will be = $ 20/ $ 2 = 10.

However, as the Damac Properties was listed during the last quarter of 2015, the

market price of its share for 2014 and 2015 cannot be obtained. Therefore, the P/E ratio

cannot be calculated and compared.

2015 2014 2015 2014

DAMAC Al-Mazaya

0.00

0.10

0.20

0.30

0.40

0.50

0.60

Asset turnover ratio

Asset turnover ratio

From the above graph it can be analysed that the though the ratio for DAMAC

properties in 2015 has been reduced as compared to 2014, it is far better as compared to the

ratio of Al-Mazaya for both the years. Whereas the ratios for DAMAC properties are 0.56

and 0.40 respectively for 2014 and 2015, the same for Al-Mazaya are 0.04 and 0.21

respectively (Jordan 2014). However, the turnover ratio of Al-Mazaya for 2015 is improved

considerably as compared to that of 2014.

P/E ratio

PE ratio is used widely for the selection of stock. Thus ratio is computed through

dividing the market price of the share by the earning per share. It reveals the sum of money

the company is ready to pay for each dollar. To be more specific, P/E ratio is that price which

the investor pays for $1 for the earning of the company. For instance, if the EPS is $2 and the

market price is $20, then the P/E ratio will be = $ 20/ $ 2 = 10.

However, as the Damac Properties was listed during the last quarter of 2015, the

market price of its share for 2014 and 2015 cannot be obtained. Therefore, the P/E ratio

cannot be calculated and compared.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 42

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.