Financial Ratio Analysis: Burberry Group Plc vs. Tiffany & Co Report

VerifiedAdded on 2020/05/11

|43

|8665

|433

Report

AI Summary

This report provides a detailed financial analysis comparing Burberry Group Plc and Tiffany & Co, focusing on their performance in 2015 and 2016. It begins with introductions to both companies, outlining their core businesses and market positions. The core of the report lies in the analysis of key financial ratios, including operating profit margin, return on capital employed, gearing ratio, interest coverage ratio, return on assets, and price-to-equity ratio. The report calculates and compares these ratios for both companies across the specified years, providing insights into their profitability, efficiency, and financial health. Interpretations of these ratios are provided, considering macroeconomic and business factors that may have influenced the results, such as economic conditions, consumer confidence, and market strategies. The report also includes an analysis of the sources of funding for Burberry Plc. The report concludes with a discussion of the relevance of management accounting within the context of these companies. Financial statements and ratio calculations are included in the appendix to support the analysis.

Running head: FINANCE AND ACCOUNTING

Finance and Accounting

University Name

Student Name

Authors’ Note

Finance and Accounting

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2FINANCE AND ACCOUNTING

Table of Contents

Finance and Accounting.............................................................................................................1

Solution to Task 1:.....................................................................................................................4

Introduction of Competitor Company: Tiffany & Co................................................................5

Analysis of key financial ratio of two firms during the period 2015 and 2016.........................6

Interpretations taking into account macro business and macroeconomic factors....................16

Solution to Task 2:...................................................................................................................21

Analysis of the sources of funding...........................................................................................21

Analysis of current state of financing in the selected company Burberry Plc.........................23

Solution to Task 3:...................................................................................................................29

Analytical and generic discussion of the relevance of management accounting.....................29

References................................................................................................................................34

Appendix:.................................................................................................................................38

Financial Statements of the selected firm Burberry Plc...........................................................38

Financial Statements of the competitor firm Tiffany & Co.....................................................41

Ratio Calculations....................................................................................................................44

I. Operating Profit Margin Ratio..........................................................................................44

II. Return on Capital Employed Ratio...............................................................................44

III. Gearing Ratio................................................................................................................44

IV. Interest Coverage Ratio.................................................................................................44

V. Return on Assets Ratio..................................................................................................45

VI. Price to Equity Ratio.....................................................................................................45

Table of Contents

Finance and Accounting.............................................................................................................1

Solution to Task 1:.....................................................................................................................4

Introduction of Competitor Company: Tiffany & Co................................................................5

Analysis of key financial ratio of two firms during the period 2015 and 2016.........................6

Interpretations taking into account macro business and macroeconomic factors....................16

Solution to Task 2:...................................................................................................................21

Analysis of the sources of funding...........................................................................................21

Analysis of current state of financing in the selected company Burberry Plc.........................23

Solution to Task 3:...................................................................................................................29

Analytical and generic discussion of the relevance of management accounting.....................29

References................................................................................................................................34

Appendix:.................................................................................................................................38

Financial Statements of the selected firm Burberry Plc...........................................................38

Financial Statements of the competitor firm Tiffany & Co.....................................................41

Ratio Calculations....................................................................................................................44

I. Operating Profit Margin Ratio..........................................................................................44

II. Return on Capital Employed Ratio...............................................................................44

III. Gearing Ratio................................................................................................................44

IV. Interest Coverage Ratio.................................................................................................44

V. Return on Assets Ratio..................................................................................................45

VI. Price to Equity Ratio.....................................................................................................45

3FINANCE AND ACCOUNTING

Solution to Task 1:

Introduction of selected company: Burberry Group Plc

Burberry Group Plc, is in essence a publicly traded luxury fashion business headquartered in

London, England. In essence, its chief fashion house concentrates on and allocates trench

coats, diverse ready-to-wear outer dress, fashionable accessories, fine scent, sunglasses, as

well as cosmetics (Burberryplc.com 2017).

Burberry Plc essentially established during the year 1856 mainly concentrated on the process

of development of primarily outdoor attire. In essence, the fashion house has necessarily

progressed to specifically high fashion market development as well as creation of innovative

fabric known as Gabardine that is entirely breathable as well as waterproof. There are

necessarily 45 degree selected pattern based scarves, different fashion accessories as well as

trench coats. Primarily, the first shop was introduced in the Haymarket situated in London

during the year 1891. As such, Burberry was necessarily a self-governing family controlled

corporation till 1955 that is at the time when the firm was reincorporated. The exclusive

check pattern can be considered as the most extensively copied trademarks. In essence,

Burberry Plc can be regarded as a popular one for mainly trench coats. In addition to this,

Burberry Plc has diverse branded stores as well as franchises throughout the globe and

markets by means of concessions in different third party stores. Essentially, the coats were

necessarily worn in different trenches during the period of First World War by British army.

As per reports, during the period 2015, the company Burberry is rated at the 73rd in

particularly Interbrand’s Best Global assessment and that is ahead of specifically Ralph

Lauren as well as Hugo Boss. The company necessarily has over and above 500 stores in

more than 50 nations.

Solution to Task 1:

Introduction of selected company: Burberry Group Plc

Burberry Group Plc, is in essence a publicly traded luxury fashion business headquartered in

London, England. In essence, its chief fashion house concentrates on and allocates trench

coats, diverse ready-to-wear outer dress, fashionable accessories, fine scent, sunglasses, as

well as cosmetics (Burberryplc.com 2017).

Burberry Plc essentially established during the year 1856 mainly concentrated on the process

of development of primarily outdoor attire. In essence, the fashion house has necessarily

progressed to specifically high fashion market development as well as creation of innovative

fabric known as Gabardine that is entirely breathable as well as waterproof. There are

necessarily 45 degree selected pattern based scarves, different fashion accessories as well as

trench coats. Primarily, the first shop was introduced in the Haymarket situated in London

during the year 1891. As such, Burberry was necessarily a self-governing family controlled

corporation till 1955 that is at the time when the firm was reincorporated. The exclusive

check pattern can be considered as the most extensively copied trademarks. In essence,

Burberry Plc can be regarded as a popular one for mainly trench coats. In addition to this,

Burberry Plc has diverse branded stores as well as franchises throughout the globe and

markets by means of concessions in different third party stores. Essentially, the coats were

necessarily worn in different trenches during the period of First World War by British army.

As per reports, during the period 2015, the company Burberry is rated at the 73rd in

particularly Interbrand’s Best Global assessment and that is ahead of specifically Ralph

Lauren as well as Hugo Boss. The company necessarily has over and above 500 stores in

more than 50 nations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4FINANCE AND ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5FINANCE AND ACCOUNTING

Introduction of Competitor Company: Tiffany & Co

Tiffany & Co also referred to as Tiffany is a well-known retailer of jewellery and speciality

retailer, which has its headquarters situated in the New York City. Tiffany necessarily

markets jewellery, crystal, watches, leather goods, sterling silver and water bottles.

Fundamentally, Tiffany is well-known for luxury goods and is specifically known for

diamond and different sterling silver jewellery (Tiffany.com 2017).

Tiffany & Co is essentially a holding corporation that functions by means of different

subsidiary corporations (jointly known as company). The main principal subsidiary of

Tiffany is necessarily Tiffany and Company is necessarily a jeweller as well as field retailer,

whose product offerings comprise of extensive adoption of jewellery (that is approximately

92% of the global net sales in the year 2016). In addition to this, the product offerings of the

company also include timepieces, china, fragrances, accessories, crystal, sterling silverware

as well as stationary. By means of Tiffany and Company as well as other subsidiaries, the

entire corporation is involved in the design of the product, manufacturing as well as retailing

actions.

The corporation’s important growth tactics include selective expansion of distribution

channels in significant markets all around the globe without disturbing the TIFFANY & CO’s

long-term value of trademark. Furthermore, the strategy of the company is also to enhance

the overall sales figure of the firm in subsisting stores by generating novel products.

Moreover, the strategy is also to augment the overall control over firm’s supply of the

product and attain superior margins of profit by means of direct sourcing of diamond as well

as manufacturing of internal jewelry. Additionally the management of the firm is also to

augment awareness among the customer by means of marketing as well as public associations

Introduction of Competitor Company: Tiffany & Co

Tiffany & Co also referred to as Tiffany is a well-known retailer of jewellery and speciality

retailer, which has its headquarters situated in the New York City. Tiffany necessarily

markets jewellery, crystal, watches, leather goods, sterling silver and water bottles.

Fundamentally, Tiffany is well-known for luxury goods and is specifically known for

diamond and different sterling silver jewellery (Tiffany.com 2017).

Tiffany & Co is essentially a holding corporation that functions by means of different

subsidiary corporations (jointly known as company). The main principal subsidiary of

Tiffany is necessarily Tiffany and Company is necessarily a jeweller as well as field retailer,

whose product offerings comprise of extensive adoption of jewellery (that is approximately

92% of the global net sales in the year 2016). In addition to this, the product offerings of the

company also include timepieces, china, fragrances, accessories, crystal, sterling silverware

as well as stationary. By means of Tiffany and Company as well as other subsidiaries, the

entire corporation is involved in the design of the product, manufacturing as well as retailing

actions.

The corporation’s important growth tactics include selective expansion of distribution

channels in significant markets all around the globe without disturbing the TIFFANY & CO’s

long-term value of trademark. Furthermore, the strategy of the company is also to enhance

the overall sales figure of the firm in subsisting stores by generating novel products.

Moreover, the strategy is also to augment the overall control over firm’s supply of the

product and attain superior margins of profit by means of direct sourcing of diamond as well

as manufacturing of internal jewelry. Additionally the management of the firm is also to

augment awareness among the customer by means of marketing as well as public associations

6FINANCE AND ACCOUNTING

programs. In addition to this, the company is to offer customer service that makes certain a

finer shopping experience.

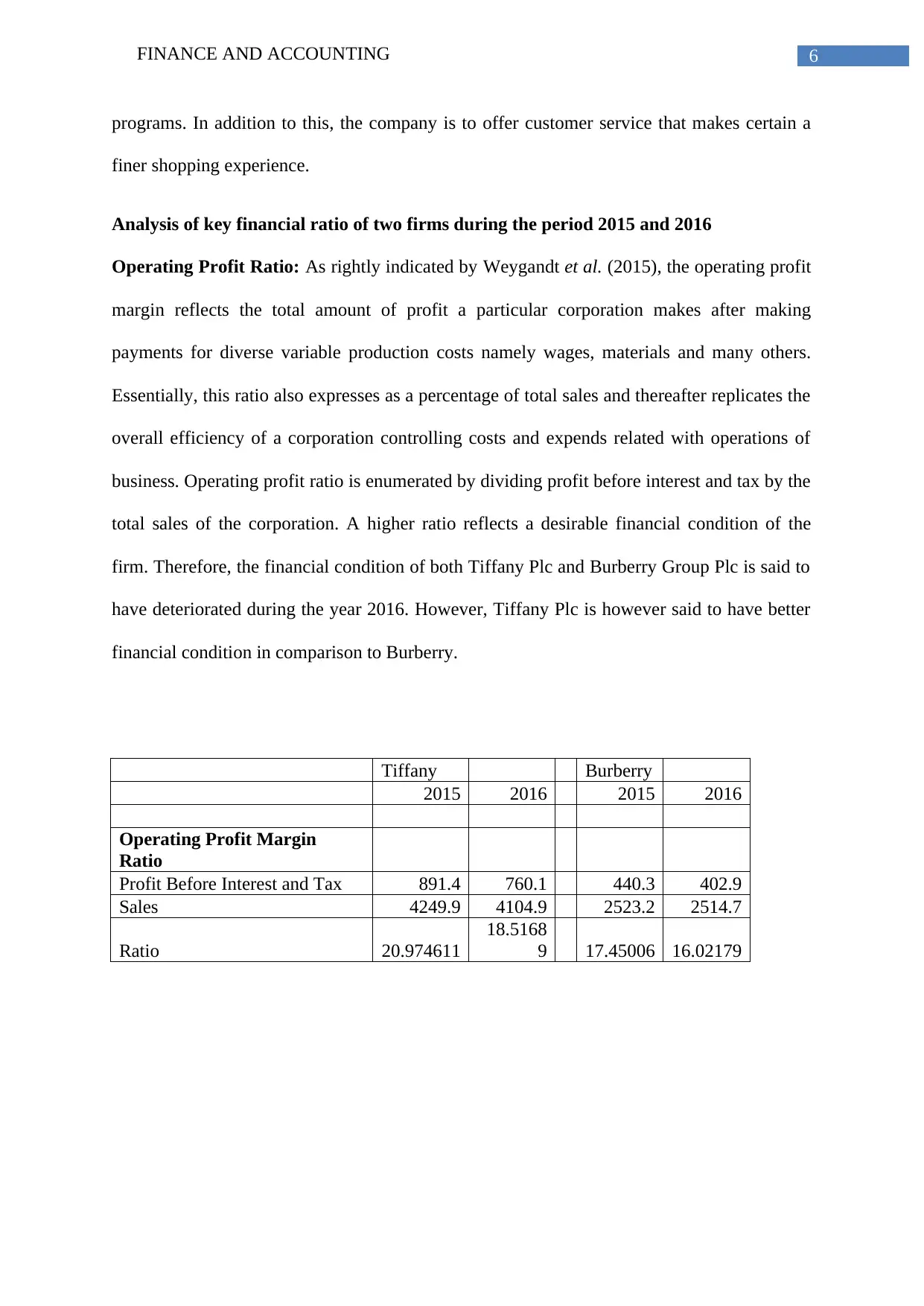

Analysis of key financial ratio of two firms during the period 2015 and 2016

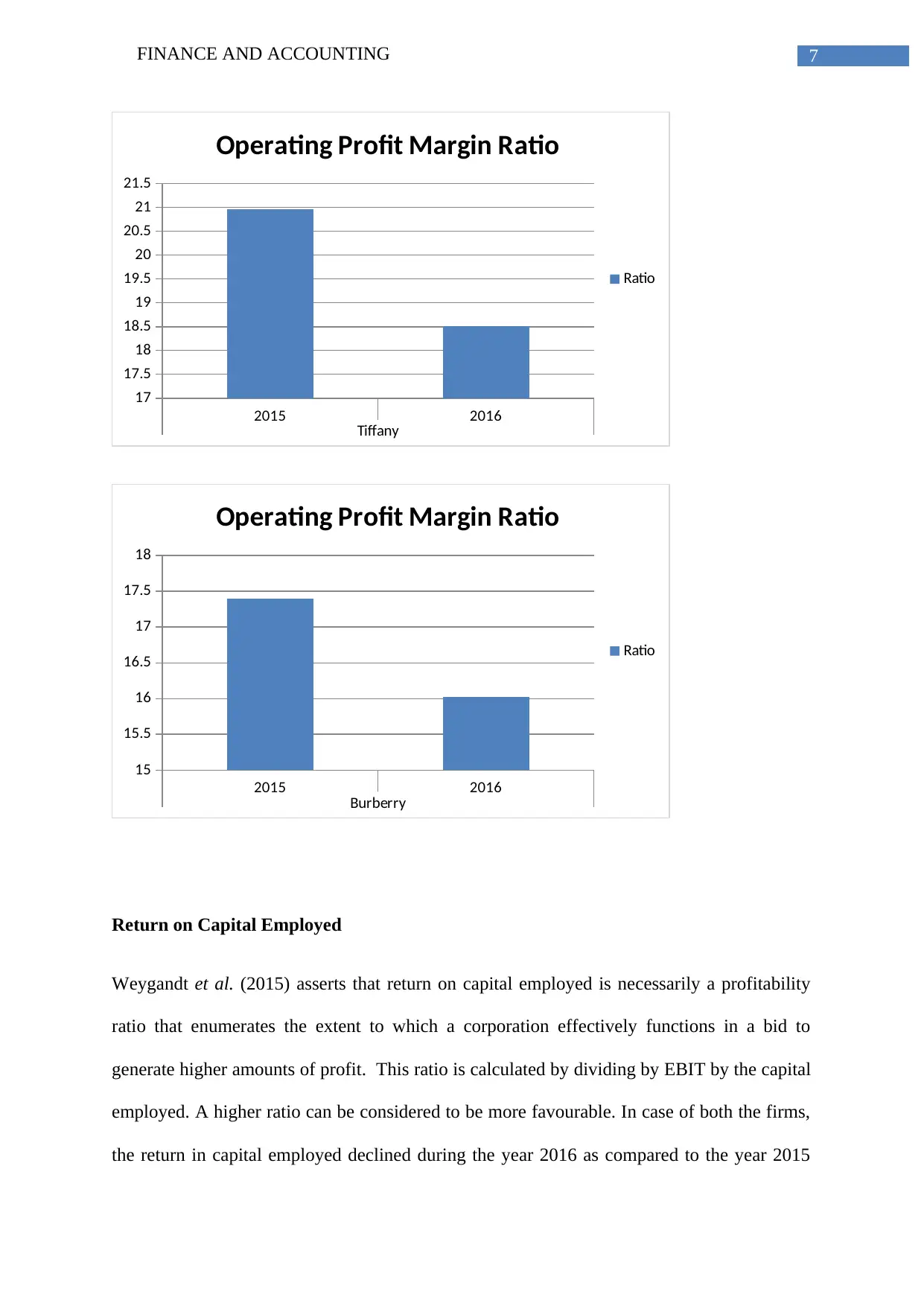

Operating Profit Ratio: As rightly indicated by Weygandt et al. (2015), the operating profit

margin reflects the total amount of profit a particular corporation makes after making

payments for diverse variable production costs namely wages, materials and many others.

Essentially, this ratio also expresses as a percentage of total sales and thereafter replicates the

overall efficiency of a corporation controlling costs and expends related with operations of

business. Operating profit ratio is enumerated by dividing profit before interest and tax by the

total sales of the corporation. A higher ratio reflects a desirable financial condition of the

firm. Therefore, the financial condition of both Tiffany Plc and Burberry Group Plc is said to

have deteriorated during the year 2016. However, Tiffany Plc is however said to have better

financial condition in comparison to Burberry.

Tiffany Burberry

2015 2016 2015 2016

Operating Profit Margin

Ratio

Profit Before Interest and Tax 891.4 760.1 440.3 402.9

Sales 4249.9 4104.9 2523.2 2514.7

Ratio 20.974611

18.5168

9 17.45006 16.02179

programs. In addition to this, the company is to offer customer service that makes certain a

finer shopping experience.

Analysis of key financial ratio of two firms during the period 2015 and 2016

Operating Profit Ratio: As rightly indicated by Weygandt et al. (2015), the operating profit

margin reflects the total amount of profit a particular corporation makes after making

payments for diverse variable production costs namely wages, materials and many others.

Essentially, this ratio also expresses as a percentage of total sales and thereafter replicates the

overall efficiency of a corporation controlling costs and expends related with operations of

business. Operating profit ratio is enumerated by dividing profit before interest and tax by the

total sales of the corporation. A higher ratio reflects a desirable financial condition of the

firm. Therefore, the financial condition of both Tiffany Plc and Burberry Group Plc is said to

have deteriorated during the year 2016. However, Tiffany Plc is however said to have better

financial condition in comparison to Burberry.

Tiffany Burberry

2015 2016 2015 2016

Operating Profit Margin

Ratio

Profit Before Interest and Tax 891.4 760.1 440.3 402.9

Sales 4249.9 4104.9 2523.2 2514.7

Ratio 20.974611

18.5168

9 17.45006 16.02179

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7FINANCE AND ACCOUNTING

2015 2016

Tiffany

17

17.5

18

18.5

19

19.5

20

20.5

21

21.5

Operating Profit Margin Ratio

Ratio

2015 2016

Burberry

15

15.5

16

16.5

17

17.5

18

Operating Profit Margin Ratio

Ratio

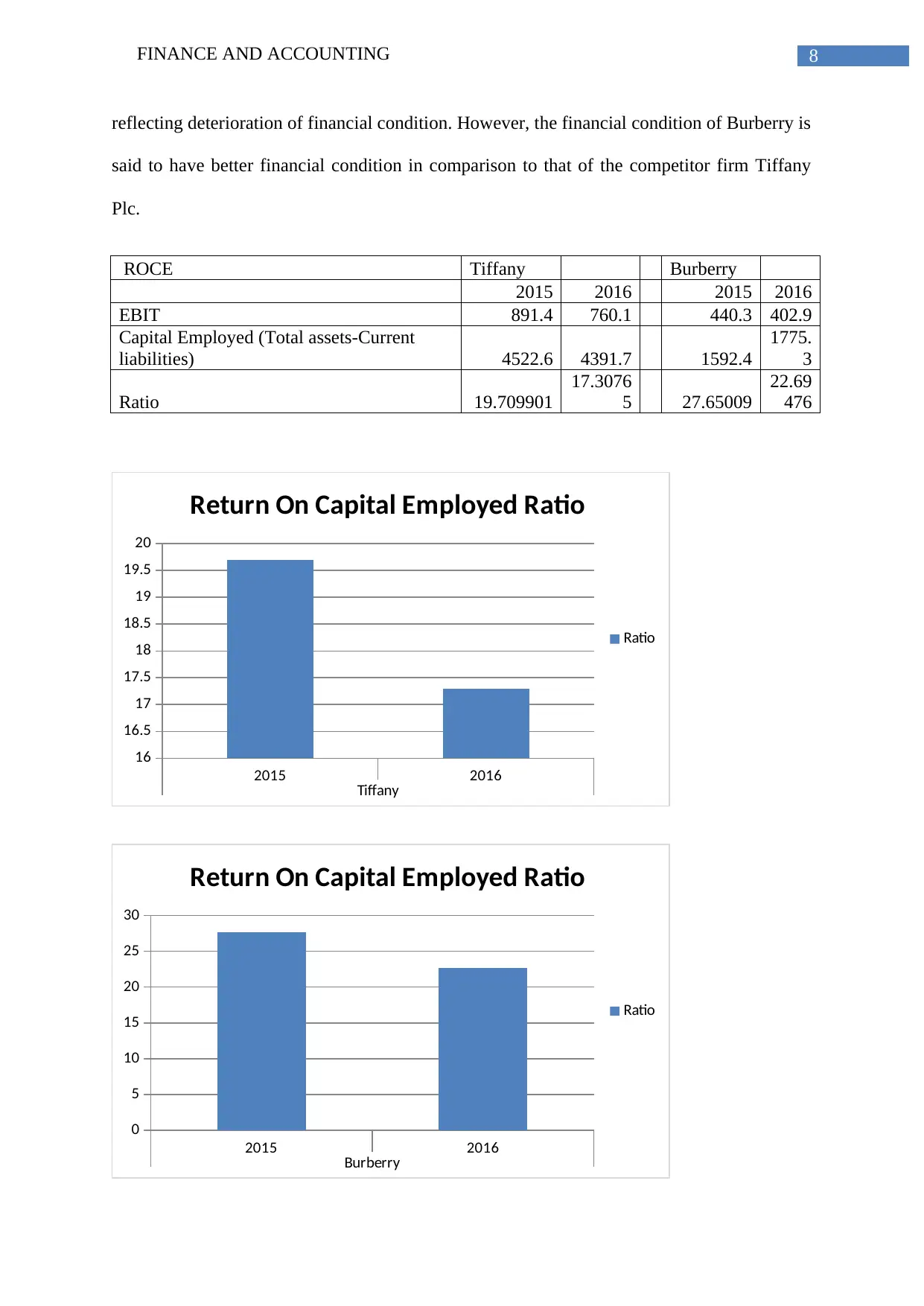

Return on Capital Employed

Weygandt et al. (2015) asserts that return on capital employed is necessarily a profitability

ratio that enumerates the extent to which a corporation effectively functions in a bid to

generate higher amounts of profit. This ratio is calculated by dividing by EBIT by the capital

employed. A higher ratio can be considered to be more favourable. In case of both the firms,

the return in capital employed declined during the year 2016 as compared to the year 2015

2015 2016

Tiffany

17

17.5

18

18.5

19

19.5

20

20.5

21

21.5

Operating Profit Margin Ratio

Ratio

2015 2016

Burberry

15

15.5

16

16.5

17

17.5

18

Operating Profit Margin Ratio

Ratio

Return on Capital Employed

Weygandt et al. (2015) asserts that return on capital employed is necessarily a profitability

ratio that enumerates the extent to which a corporation effectively functions in a bid to

generate higher amounts of profit. This ratio is calculated by dividing by EBIT by the capital

employed. A higher ratio can be considered to be more favourable. In case of both the firms,

the return in capital employed declined during the year 2016 as compared to the year 2015

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8FINANCE AND ACCOUNTING

reflecting deterioration of financial condition. However, the financial condition of Burberry is

said to have better financial condition in comparison to that of the competitor firm Tiffany

Plc.

ROCE Tiffany Burberry

2015 2016 2015 2016

EBIT 891.4 760.1 440.3 402.9

Capital Employed (Total assets-Current

liabilities) 4522.6 4391.7 1592.4

1775.

3

Ratio 19.709901

17.3076

5 27.65009

22.69

476

2015 2016

Tiffany

16

16.5

17

17.5

18

18.5

19

19.5

20

Return On Capital Employed Ratio

Ratio

2015 2016

Burberry

0

5

10

15

20

25

30

Return On Capital Employed Ratio

Ratio

reflecting deterioration of financial condition. However, the financial condition of Burberry is

said to have better financial condition in comparison to that of the competitor firm Tiffany

Plc.

ROCE Tiffany Burberry

2015 2016 2015 2016

EBIT 891.4 760.1 440.3 402.9

Capital Employed (Total assets-Current

liabilities) 4522.6 4391.7 1592.4

1775.

3

Ratio 19.709901

17.3076

5 27.65009

22.69

476

2015 2016

Tiffany

16

16.5

17

17.5

18

18.5

19

19.5

20

Return On Capital Employed Ratio

Ratio

2015 2016

Burberry

0

5

10

15

20

25

30

Return On Capital Employed Ratio

Ratio

9FINANCE AND ACCOUNTING

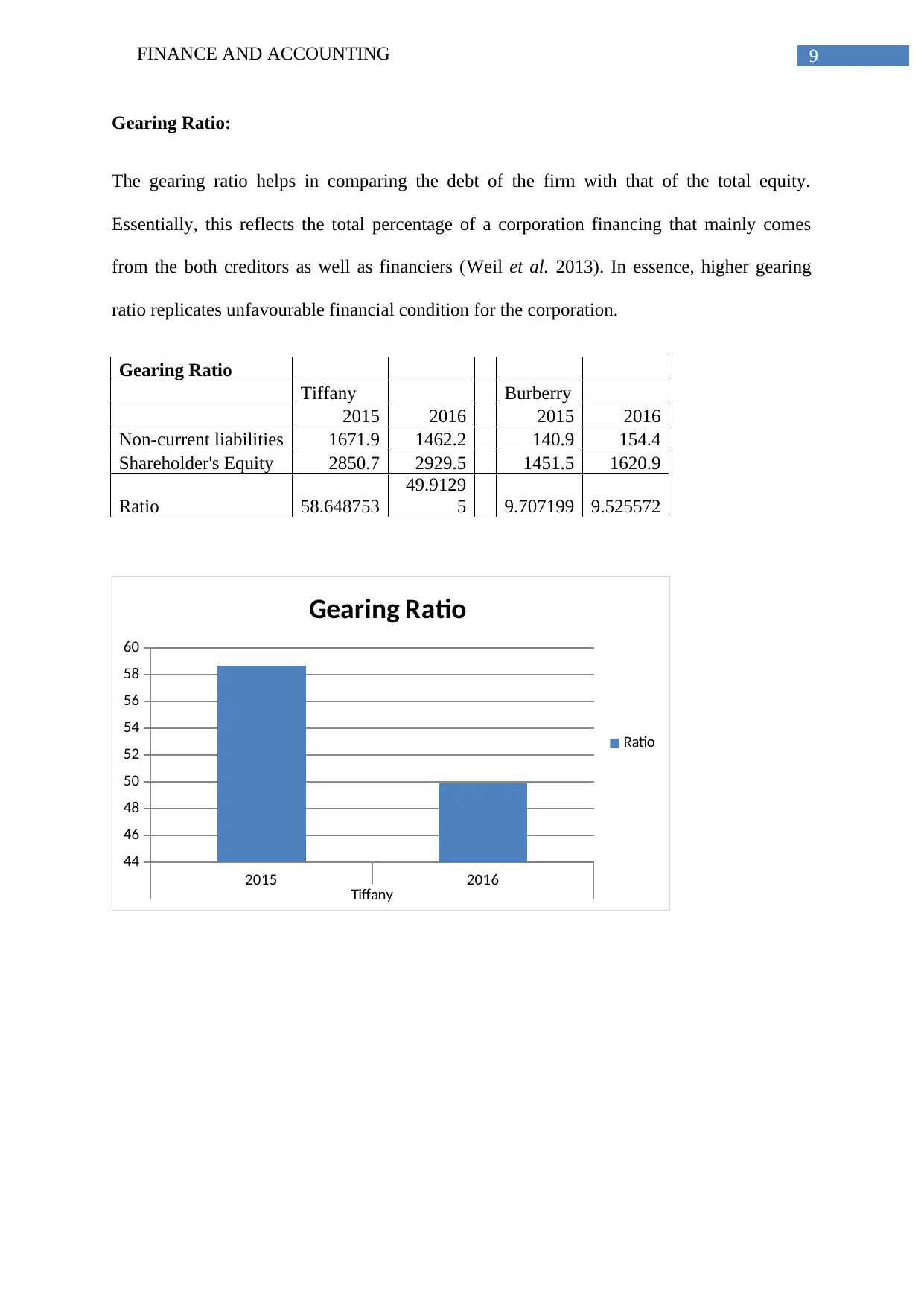

Gearing Ratio:

The gearing ratio helps in comparing the debt of the firm with that of the total equity.

Essentially, this reflects the total percentage of a corporation financing that mainly comes

from the both creditors as well as financiers (Weil et al. 2013). In essence, higher gearing

ratio replicates unfavourable financial condition for the corporation.

Gearing Ratio

Tiffany Burberry

2015 2016 2015 2016

Non-current liabilities 1671.9 1462.2 140.9 154.4

Shareholder's Equity 2850.7 2929.5 1451.5 1620.9

Ratio 58.648753

49.9129

5 9.707199 9.525572

2015 2016

Tiffany

44

46

48

50

52

54

56

58

60

Gearing Ratio

Ratio

Gearing Ratio:

The gearing ratio helps in comparing the debt of the firm with that of the total equity.

Essentially, this reflects the total percentage of a corporation financing that mainly comes

from the both creditors as well as financiers (Weil et al. 2013). In essence, higher gearing

ratio replicates unfavourable financial condition for the corporation.

Gearing Ratio

Tiffany Burberry

2015 2016 2015 2016

Non-current liabilities 1671.9 1462.2 140.9 154.4

Shareholder's Equity 2850.7 2929.5 1451.5 1620.9

Ratio 58.648753

49.9129

5 9.707199 9.525572

2015 2016

Tiffany

44

46

48

50

52

54

56

58

60

Gearing Ratio

Ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10FINANCE AND ACCOUNTING

2015 2016

Burberry

9.4

9.45

9.5

9.55

9.6

9.65

9.7

9.75

Gearing Ratio

Ratio

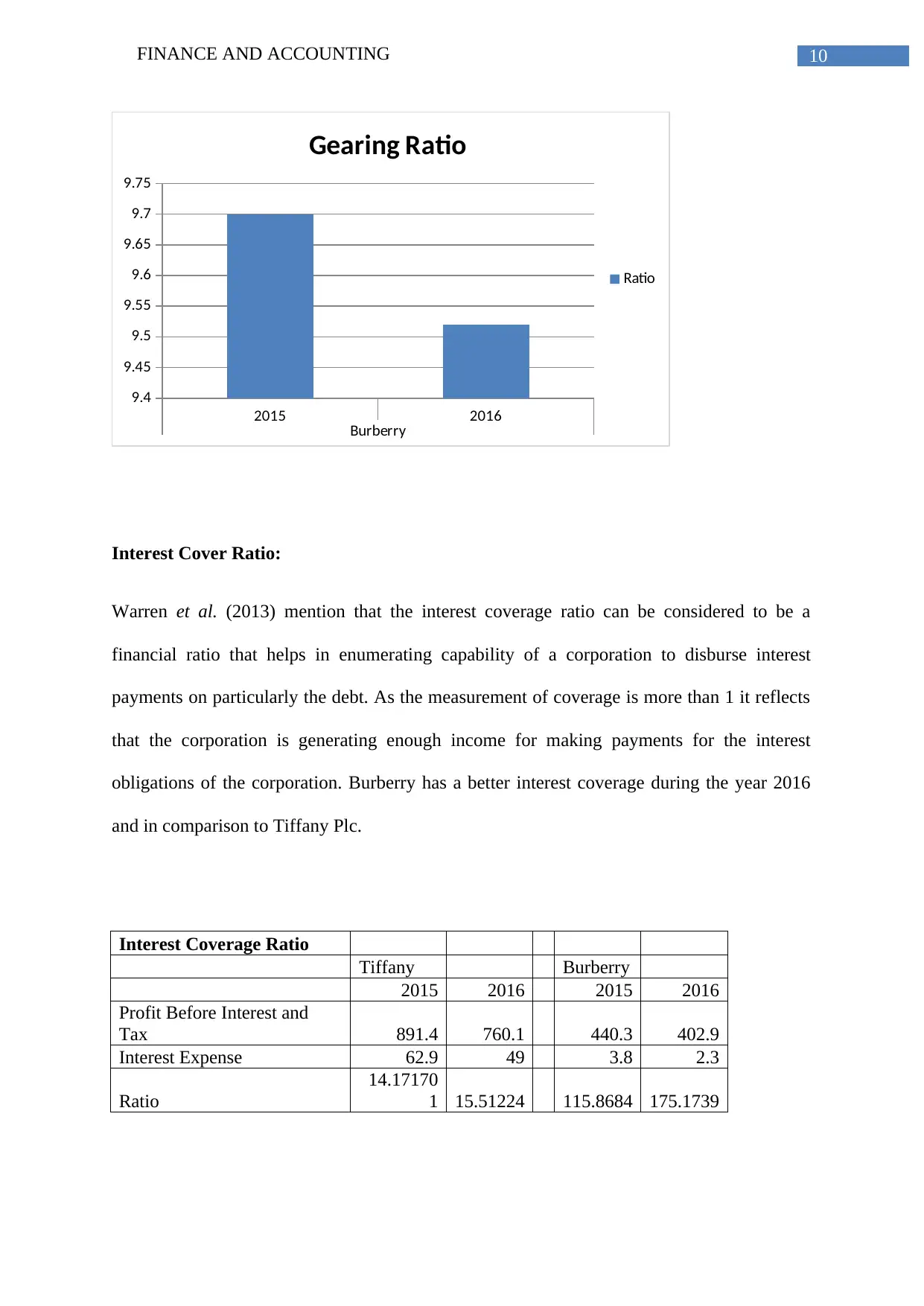

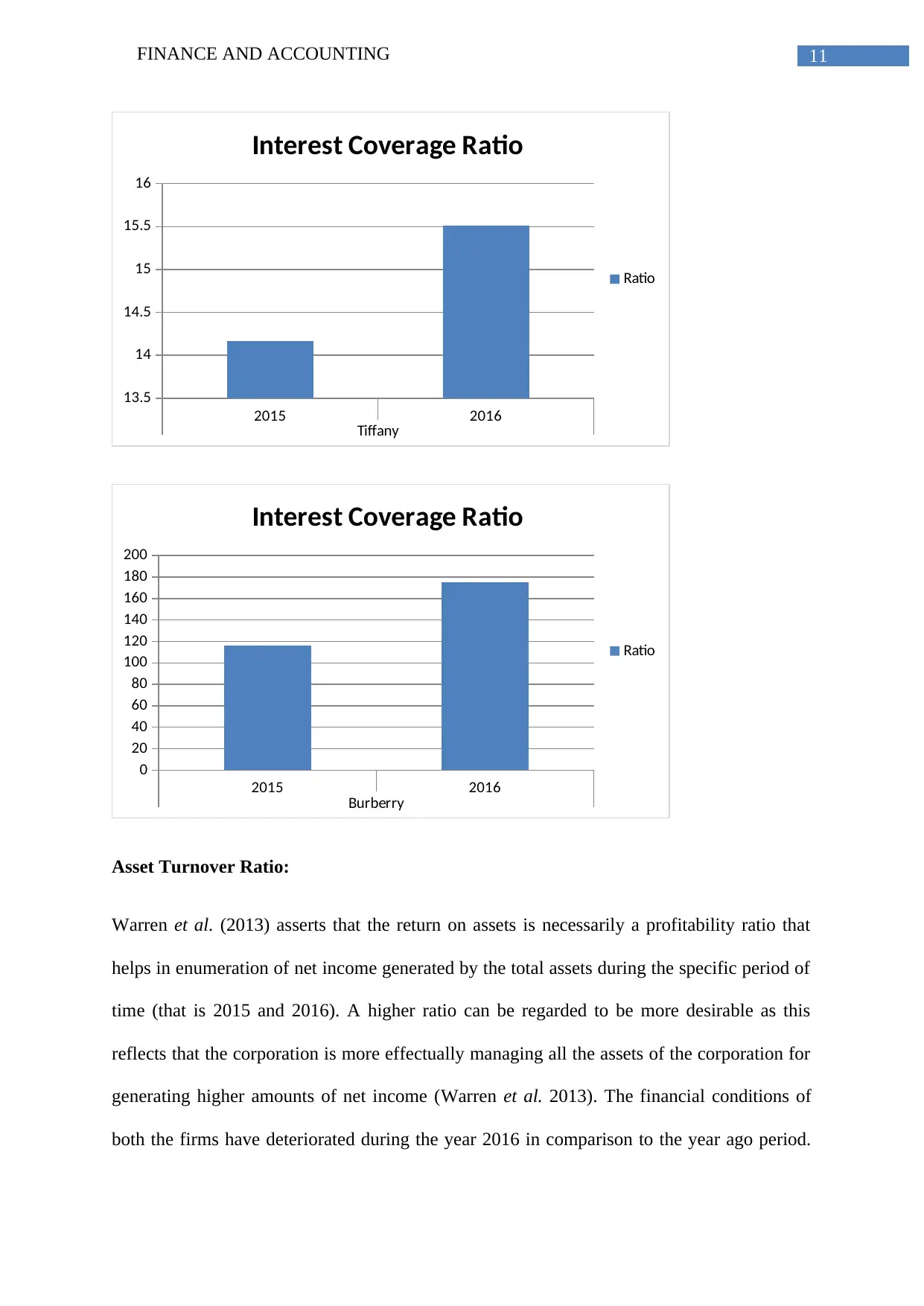

Interest Cover Ratio:

Warren et al. (2013) mention that the interest coverage ratio can be considered to be a

financial ratio that helps in enumerating capability of a corporation to disburse interest

payments on particularly the debt. As the measurement of coverage is more than 1 it reflects

that the corporation is generating enough income for making payments for the interest

obligations of the corporation. Burberry has a better interest coverage during the year 2016

and in comparison to Tiffany Plc.

Interest Coverage Ratio

Tiffany Burberry

2015 2016 2015 2016

Profit Before Interest and

Tax 891.4 760.1 440.3 402.9

Interest Expense 62.9 49 3.8 2.3

Ratio

14.17170

1 15.51224 115.8684 175.1739

2015 2016

Burberry

9.4

9.45

9.5

9.55

9.6

9.65

9.7

9.75

Gearing Ratio

Ratio

Interest Cover Ratio:

Warren et al. (2013) mention that the interest coverage ratio can be considered to be a

financial ratio that helps in enumerating capability of a corporation to disburse interest

payments on particularly the debt. As the measurement of coverage is more than 1 it reflects

that the corporation is generating enough income for making payments for the interest

obligations of the corporation. Burberry has a better interest coverage during the year 2016

and in comparison to Tiffany Plc.

Interest Coverage Ratio

Tiffany Burberry

2015 2016 2015 2016

Profit Before Interest and

Tax 891.4 760.1 440.3 402.9

Interest Expense 62.9 49 3.8 2.3

Ratio

14.17170

1 15.51224 115.8684 175.1739

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11FINANCE AND ACCOUNTING

2015 2016

Tiffany

13.5

14

14.5

15

15.5

16

Interest Coverage Ratio

Ratio

2015 2016

Burberry

0

20

40

60

80

100

120

140

160

180

200

Interest Coverage Ratio

Ratio

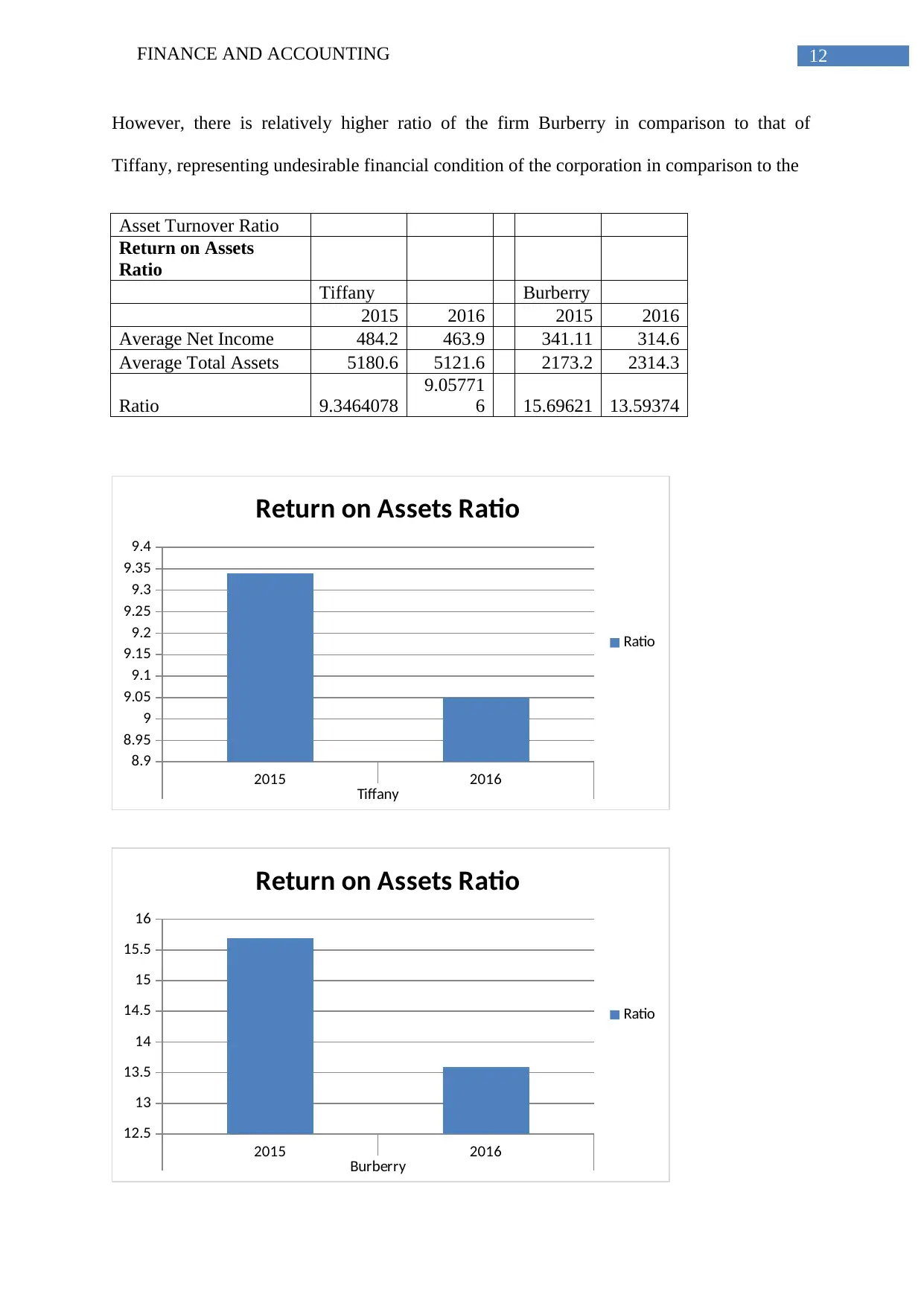

Asset Turnover Ratio:

Warren et al. (2013) asserts that the return on assets is necessarily a profitability ratio that

helps in enumeration of net income generated by the total assets during the specific period of

time (that is 2015 and 2016). A higher ratio can be regarded to be more desirable as this

reflects that the corporation is more effectually managing all the assets of the corporation for

generating higher amounts of net income (Warren et al. 2013). The financial conditions of

both the firms have deteriorated during the year 2016 in comparison to the year ago period.

2015 2016

Tiffany

13.5

14

14.5

15

15.5

16

Interest Coverage Ratio

Ratio

2015 2016

Burberry

0

20

40

60

80

100

120

140

160

180

200

Interest Coverage Ratio

Ratio

Asset Turnover Ratio:

Warren et al. (2013) asserts that the return on assets is necessarily a profitability ratio that

helps in enumeration of net income generated by the total assets during the specific period of

time (that is 2015 and 2016). A higher ratio can be regarded to be more desirable as this

reflects that the corporation is more effectually managing all the assets of the corporation for

generating higher amounts of net income (Warren et al. 2013). The financial conditions of

both the firms have deteriorated during the year 2016 in comparison to the year ago period.

12FINANCE AND ACCOUNTING

However, there is relatively higher ratio of the firm Burberry in comparison to that of

Tiffany, representing undesirable financial condition of the corporation in comparison to the

Asset Turnover Ratio

Return on Assets

Ratio

Tiffany Burberry

2015 2016 2015 2016

Average Net Income 484.2 463.9 341.11 314.6

Average Total Assets 5180.6 5121.6 2173.2 2314.3

Ratio 9.3464078

9.05771

6 15.69621 13.59374

2015 2016

Tiffany

8.9

8.95

9

9.05

9.1

9.15

9.2

9.25

9.3

9.35

9.4

Return on Assets Ratio

Ratio

2015 2016

Burberry

12.5

13

13.5

14

14.5

15

15.5

16

Return on Assets Ratio

Ratio

However, there is relatively higher ratio of the firm Burberry in comparison to that of

Tiffany, representing undesirable financial condition of the corporation in comparison to the

Asset Turnover Ratio

Return on Assets

Ratio

Tiffany Burberry

2015 2016 2015 2016

Average Net Income 484.2 463.9 341.11 314.6

Average Total Assets 5180.6 5121.6 2173.2 2314.3

Ratio 9.3464078

9.05771

6 15.69621 13.59374

2015 2016

Tiffany

8.9

8.95

9

9.05

9.1

9.15

9.2

9.25

9.3

9.35

9.4

Return on Assets Ratio

Ratio

2015 2016

Burberry

12.5

13

13.5

14

14.5

15

15.5

16

Return on Assets Ratio

Ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 43

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.