Financial Management and Control: Performance Analysis Report

VerifiedAdded on 2020/02/03

|21

|5368

|111

Report

AI Summary

This report delves into the critical domains of financial management and project evaluation, crucial for firm performance and strategic decision-making. Part A focuses on a detailed ratio analysis, evaluating the financial performance of a firm, and identifying its strengths and weaknesses through various profitability, liquidity, gearing, asset utilization, and investor ratios. The analysis provides interpretations and highlights the implications of each ratio, comparing performance across two years. Part B explores investment appraisal methods, evaluating project cash flows and interpreting the results, alongside a discussion of the benefits and limitations of these methods. The report concludes with an overview of potential sources of finance in the context of project finance.

FINANCIAL MANAGEMENT AND

CONTROL

CONTROL

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

Part A...............................................................................................................................................3

1 Ratio analysis............................................................................................................................3

2 Limitation of ratio analysis.....................................................................................................13

Part B.............................................................................................................................................14

1 Investment appraisal method and interpretation of results.....................................................14

2 Benefits and limitations of the project evaluation methods....................................................18

3 Sources of finance...................................................................................................................19

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................21

INTRODUCTION...........................................................................................................................3

Part A...............................................................................................................................................3

1 Ratio analysis............................................................................................................................3

2 Limitation of ratio analysis.....................................................................................................13

Part B.............................................................................................................................................14

1 Investment appraisal method and interpretation of results.....................................................14

2 Benefits and limitations of the project evaluation methods....................................................18

3 Sources of finance...................................................................................................................19

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................21

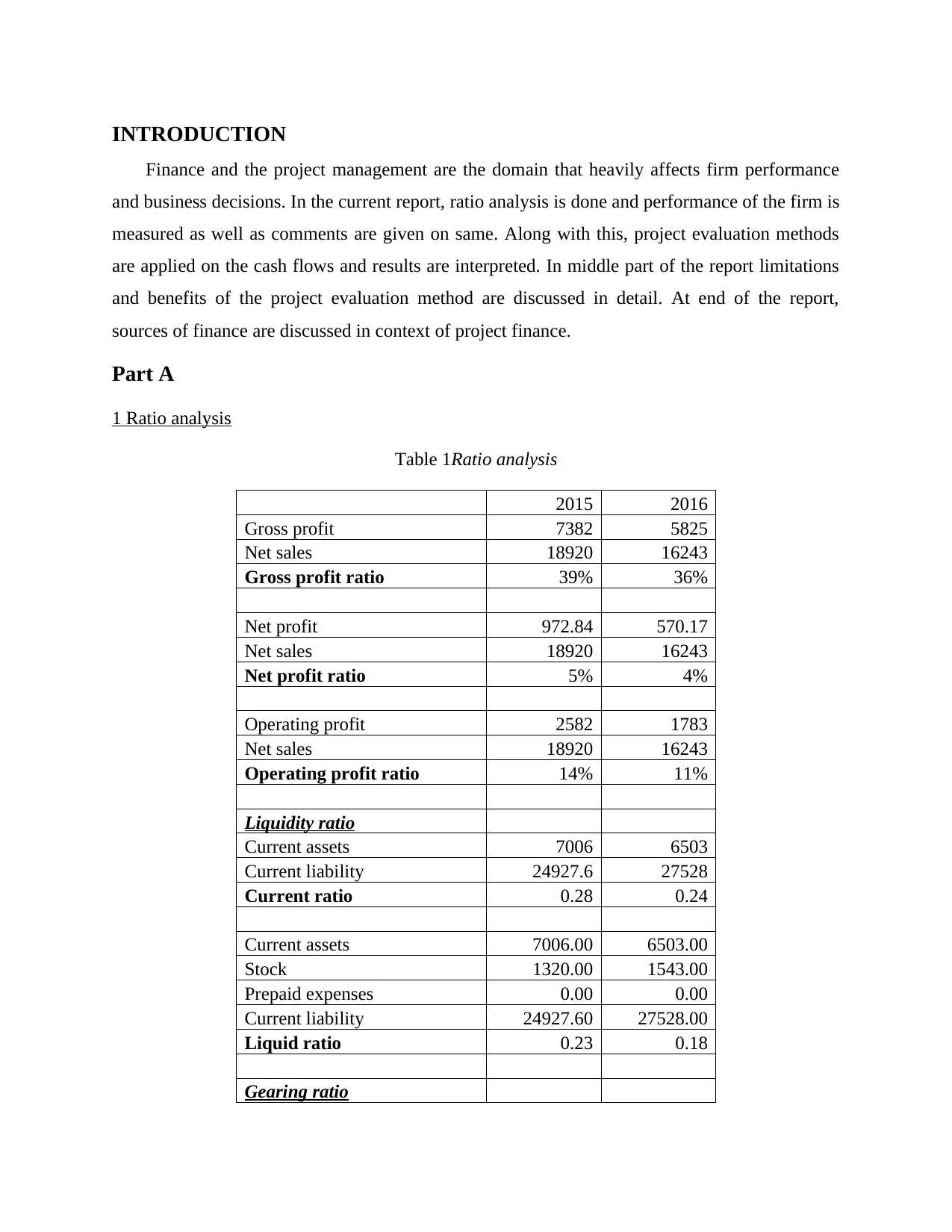

INTRODUCTION

Finance and the project management are the domain that heavily affects firm performance

and business decisions. In the current report, ratio analysis is done and performance of the firm is

measured as well as comments are given on same. Along with this, project evaluation methods

are applied on the cash flows and results are interpreted. In middle part of the report limitations

and benefits of the project evaluation method are discussed in detail. At end of the report,

sources of finance are discussed in context of project finance.

Part A

1 Ratio analysis

Table 1Ratio analysis

2015 2016

Gross profit 7382 5825

Net sales 18920 16243

Gross profit ratio 39% 36%

Net profit 972.84 570.17

Net sales 18920 16243

Net profit ratio 5% 4%

Operating profit 2582 1783

Net sales 18920 16243

Operating profit ratio 14% 11%

Liquidity ratio

Current assets 7006 6503

Current liability 24927.6 27528

Current ratio 0.28 0.24

Current assets 7006.00 6503.00

Stock 1320.00 1543.00

Prepaid expenses 0.00 0.00

Current liability 24927.60 27528.00

Liquid ratio 0.23 0.18

Gearing ratio

Finance and the project management are the domain that heavily affects firm performance

and business decisions. In the current report, ratio analysis is done and performance of the firm is

measured as well as comments are given on same. Along with this, project evaluation methods

are applied on the cash flows and results are interpreted. In middle part of the report limitations

and benefits of the project evaluation method are discussed in detail. At end of the report,

sources of finance are discussed in context of project finance.

Part A

1 Ratio analysis

Table 1Ratio analysis

2015 2016

Gross profit 7382 5825

Net sales 18920 16243

Gross profit ratio 39% 36%

Net profit 972.84 570.17

Net sales 18920 16243

Net profit ratio 5% 4%

Operating profit 2582 1783

Net sales 18920 16243

Operating profit ratio 14% 11%

Liquidity ratio

Current assets 7006 6503

Current liability 24927.6 27528

Current ratio 0.28 0.24

Current assets 7006.00 6503.00

Stock 1320.00 1543.00

Prepaid expenses 0.00 0.00

Current liability 24927.60 27528.00

Liquid ratio 0.23 0.18

Gearing ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

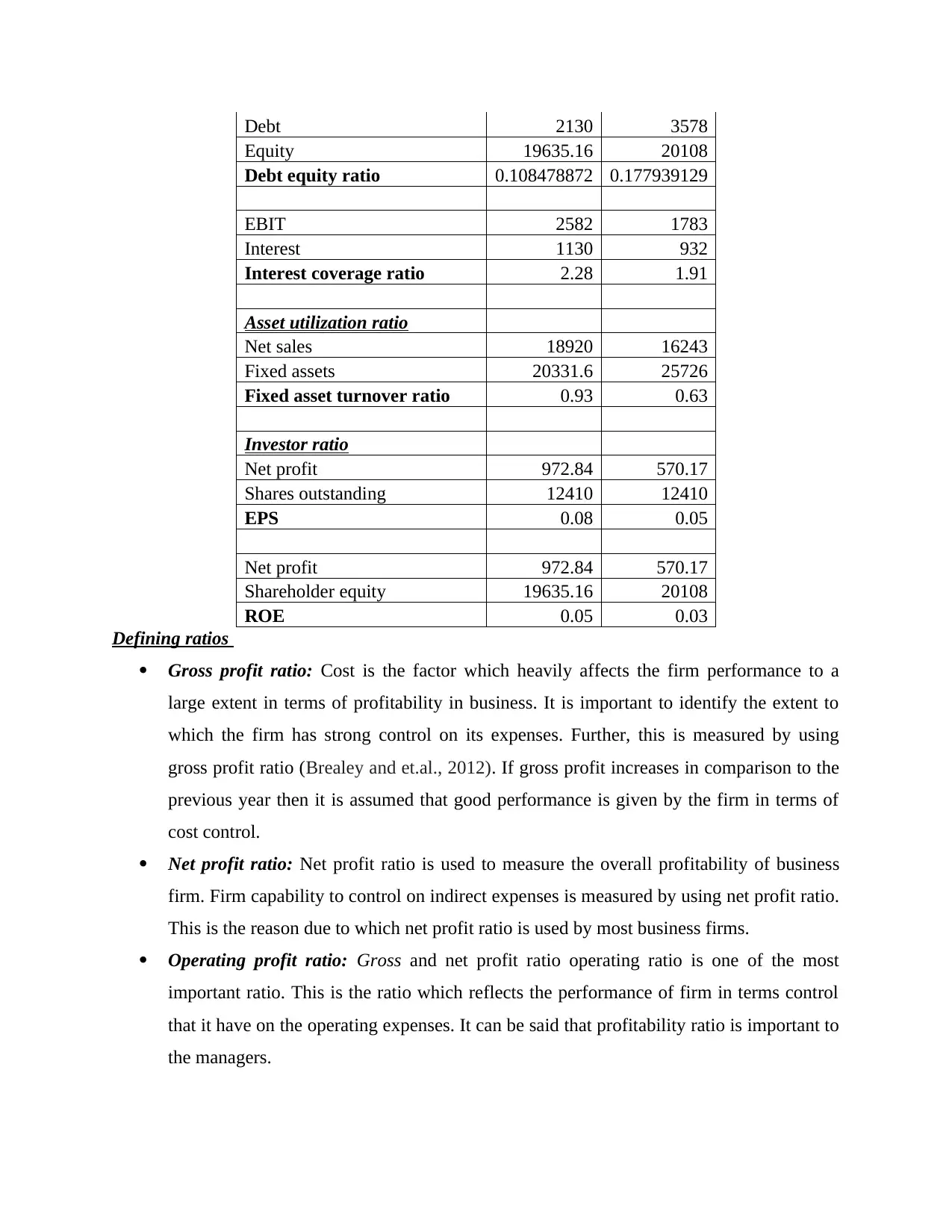

Debt 2130 3578

Equity 19635.16 20108

Debt equity ratio 0.108478872 0.177939129

EBIT 2582 1783

Interest 1130 932

Interest coverage ratio 2.28 1.91

Asset utilization ratio

Net sales 18920 16243

Fixed assets 20331.6 25726

Fixed asset turnover ratio 0.93 0.63

Investor ratio

Net profit 972.84 570.17

Shares outstanding 12410 12410

EPS 0.08 0.05

Net profit 972.84 570.17

Shareholder equity 19635.16 20108

ROE 0.05 0.03

Defining ratios

Gross profit ratio: Cost is the factor which heavily affects the firm performance to a

large extent in terms of profitability in business. It is important to identify the extent to

which the firm has strong control on its expenses. Further, this is measured by using

gross profit ratio (Brealey and et.al., 2012). If gross profit increases in comparison to the

previous year then it is assumed that good performance is given by the firm in terms of

cost control.

Net profit ratio: Net profit ratio is used to measure the overall profitability of business

firm. Firm capability to control on indirect expenses is measured by using net profit ratio.

This is the reason due to which net profit ratio is used by most business firms.

Operating profit ratio: Gross and net profit ratio operating ratio is one of the most

important ratio. This is the ratio which reflects the performance of firm in terms control

that it have on the operating expenses. It can be said that profitability ratio is important to

the managers.

Equity 19635.16 20108

Debt equity ratio 0.108478872 0.177939129

EBIT 2582 1783

Interest 1130 932

Interest coverage ratio 2.28 1.91

Asset utilization ratio

Net sales 18920 16243

Fixed assets 20331.6 25726

Fixed asset turnover ratio 0.93 0.63

Investor ratio

Net profit 972.84 570.17

Shares outstanding 12410 12410

EPS 0.08 0.05

Net profit 972.84 570.17

Shareholder equity 19635.16 20108

ROE 0.05 0.03

Defining ratios

Gross profit ratio: Cost is the factor which heavily affects the firm performance to a

large extent in terms of profitability in business. It is important to identify the extent to

which the firm has strong control on its expenses. Further, this is measured by using

gross profit ratio (Brealey and et.al., 2012). If gross profit increases in comparison to the

previous year then it is assumed that good performance is given by the firm in terms of

cost control.

Net profit ratio: Net profit ratio is used to measure the overall profitability of business

firm. Firm capability to control on indirect expenses is measured by using net profit ratio.

This is the reason due to which net profit ratio is used by most business firms.

Operating profit ratio: Gross and net profit ratio operating ratio is one of the most

important ratio. This is the ratio which reflects the performance of firm in terms control

that it have on the operating expenses. It can be said that profitability ratio is important to

the managers.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Current ratio: Liquidity position matter a lot for the organization because it indicates that

whether firm will be able to meet its short term finance needs sufficiently. Proportion of

current assets to current liability is compared in the current ratio to access the firm

performance and availability of cash which will be used to meet the short term

obligations.

Liquid ratio: There is a high degree of similarity between current and liquid ratio

(Gitman and Zutter, 2012). In the liquid ratio, stock and prepaid expenses are subtracted

from the current assets to identify the more accurate liquidity position of the business

firm.

Debt equity ratio: Capital structure of Zurich Plc is measured by using the debt equity

ratio (Debt to equity ratio, 2017). In the mentioned ratio, debt is compared with equity to

identify whether the capital structure is balanced or not.

Interest coverage ratio: Interest coverage ratio reflects the extent to which by using

profit interest can be covered. In other words, it can be said that number of times interest

can be paid by using profit is revealed by the interest coverage ratio.

Fixed asset turnover ratio: Fixed asset turnover ratio is used to measure the efficiency

with which firm is using its asset to generate sales in its business (Embrechts,

Klüppelberg and Mikosch, 2013). This ratio reflects the extent to which resources are

efficiently used by the firm in its business.

EPS: Earning per share is one of the most important ratio which reflect the portion of

earning that comes on each share that investor possessed in current time period. If EPS is

increasing then it is assumed that the firm performance has been improved.

Return on equity: Return on equity refers to the return that is earned on per unit of equity

that same hold for the specific time period. Elevation in value of return on equity reflects

that the firm is giving good amount of return to the investor for the risk they have taken

for investing in the business firm.

To,

Board of Directors,

Zurich Plc.

Date: 20th March 2017

Profitability ratios:

whether firm will be able to meet its short term finance needs sufficiently. Proportion of

current assets to current liability is compared in the current ratio to access the firm

performance and availability of cash which will be used to meet the short term

obligations.

Liquid ratio: There is a high degree of similarity between current and liquid ratio

(Gitman and Zutter, 2012). In the liquid ratio, stock and prepaid expenses are subtracted

from the current assets to identify the more accurate liquidity position of the business

firm.

Debt equity ratio: Capital structure of Zurich Plc is measured by using the debt equity

ratio (Debt to equity ratio, 2017). In the mentioned ratio, debt is compared with equity to

identify whether the capital structure is balanced or not.

Interest coverage ratio: Interest coverage ratio reflects the extent to which by using

profit interest can be covered. In other words, it can be said that number of times interest

can be paid by using profit is revealed by the interest coverage ratio.

Fixed asset turnover ratio: Fixed asset turnover ratio is used to measure the efficiency

with which firm is using its asset to generate sales in its business (Embrechts,

Klüppelberg and Mikosch, 2013). This ratio reflects the extent to which resources are

efficiently used by the firm in its business.

EPS: Earning per share is one of the most important ratio which reflect the portion of

earning that comes on each share that investor possessed in current time period. If EPS is

increasing then it is assumed that the firm performance has been improved.

Return on equity: Return on equity refers to the return that is earned on per unit of equity

that same hold for the specific time period. Elevation in value of return on equity reflects

that the firm is giving good amount of return to the investor for the risk they have taken

for investing in the business firm.

To,

Board of Directors,

Zurich Plc.

Date: 20th March 2017

Profitability ratios:

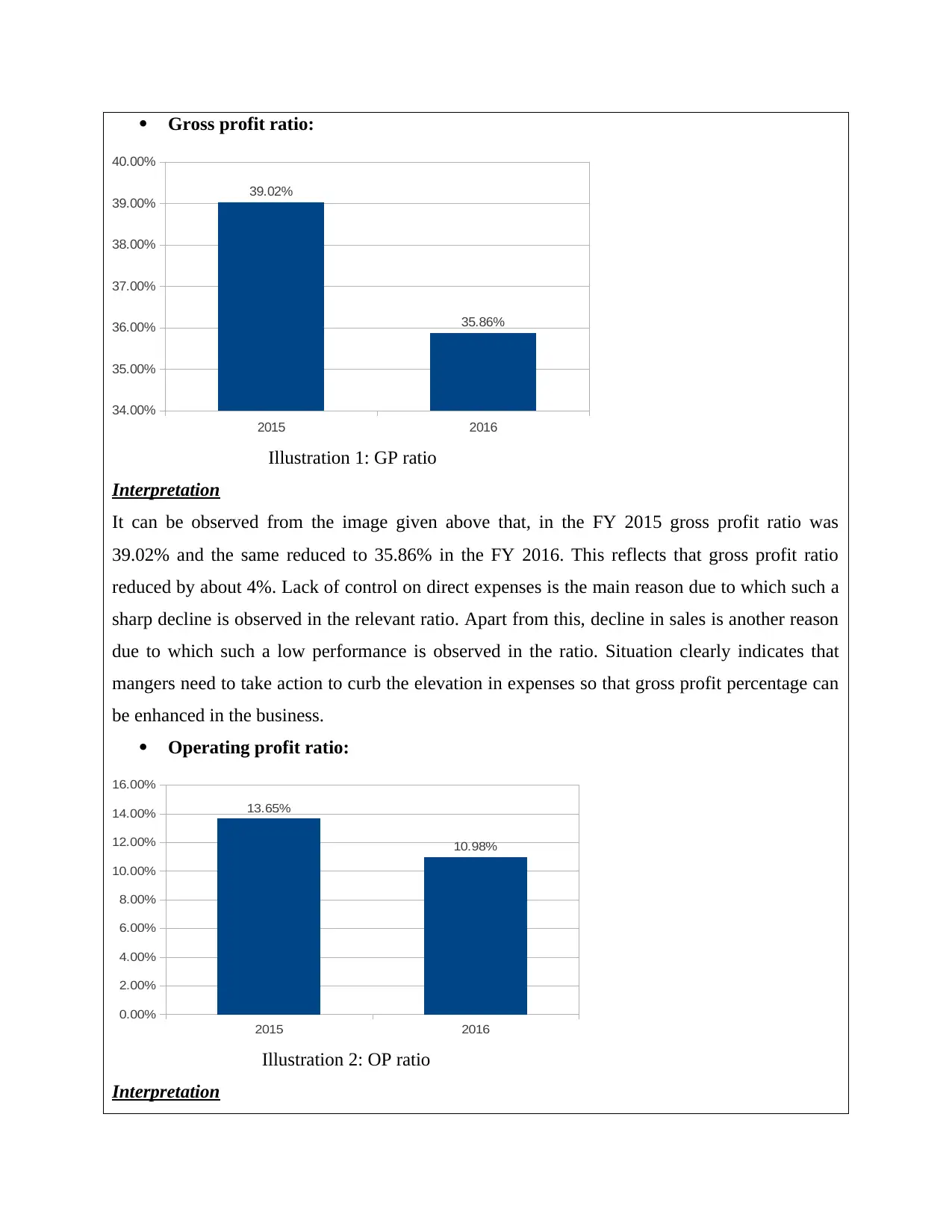

Gross profit ratio:

2015 2016

34.00%

35.00%

36.00%

37.00%

38.00%

39.00%

40.00%

39.02%

35.86%

Illustration 1: GP ratio

Interpretation

It can be observed from the image given above that, in the FY 2015 gross profit ratio was

39.02% and the same reduced to 35.86% in the FY 2016. This reflects that gross profit ratio

reduced by about 4%. Lack of control on direct expenses is the main reason due to which such a

sharp decline is observed in the relevant ratio. Apart from this, decline in sales is another reason

due to which such a low performance is observed in the ratio. Situation clearly indicates that

mangers need to take action to curb the elevation in expenses so that gross profit percentage can

be enhanced in the business.

Operating profit ratio:

2015 2016

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

13.65%

10.98%

Illustration 2: OP ratio

Interpretation

2015 2016

34.00%

35.00%

36.00%

37.00%

38.00%

39.00%

40.00%

39.02%

35.86%

Illustration 1: GP ratio

Interpretation

It can be observed from the image given above that, in the FY 2015 gross profit ratio was

39.02% and the same reduced to 35.86% in the FY 2016. This reflects that gross profit ratio

reduced by about 4%. Lack of control on direct expenses is the main reason due to which such a

sharp decline is observed in the relevant ratio. Apart from this, decline in sales is another reason

due to which such a low performance is observed in the ratio. Situation clearly indicates that

mangers need to take action to curb the elevation in expenses so that gross profit percentage can

be enhanced in the business.

Operating profit ratio:

2015 2016

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

13.65%

10.98%

Illustration 2: OP ratio

Interpretation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Operating profit ratio has declined slightly by 2% in the current financial year. Operating profit

and sales valued reduced at the sharp rate and fast elevation in operating expenses led to decline

in ratio value by 2%. This reflects that there is a strong need to maintain control on sales and

administrative and other operating expenses in the business. By doing so, the operating profit can

be increased in the business and performance can be improved. Reduction in the operating profit

will lead to improvement in value of net profit in the business. Thus, it can be said that there is a

wide impact of value of the operating profit on the firm performance.

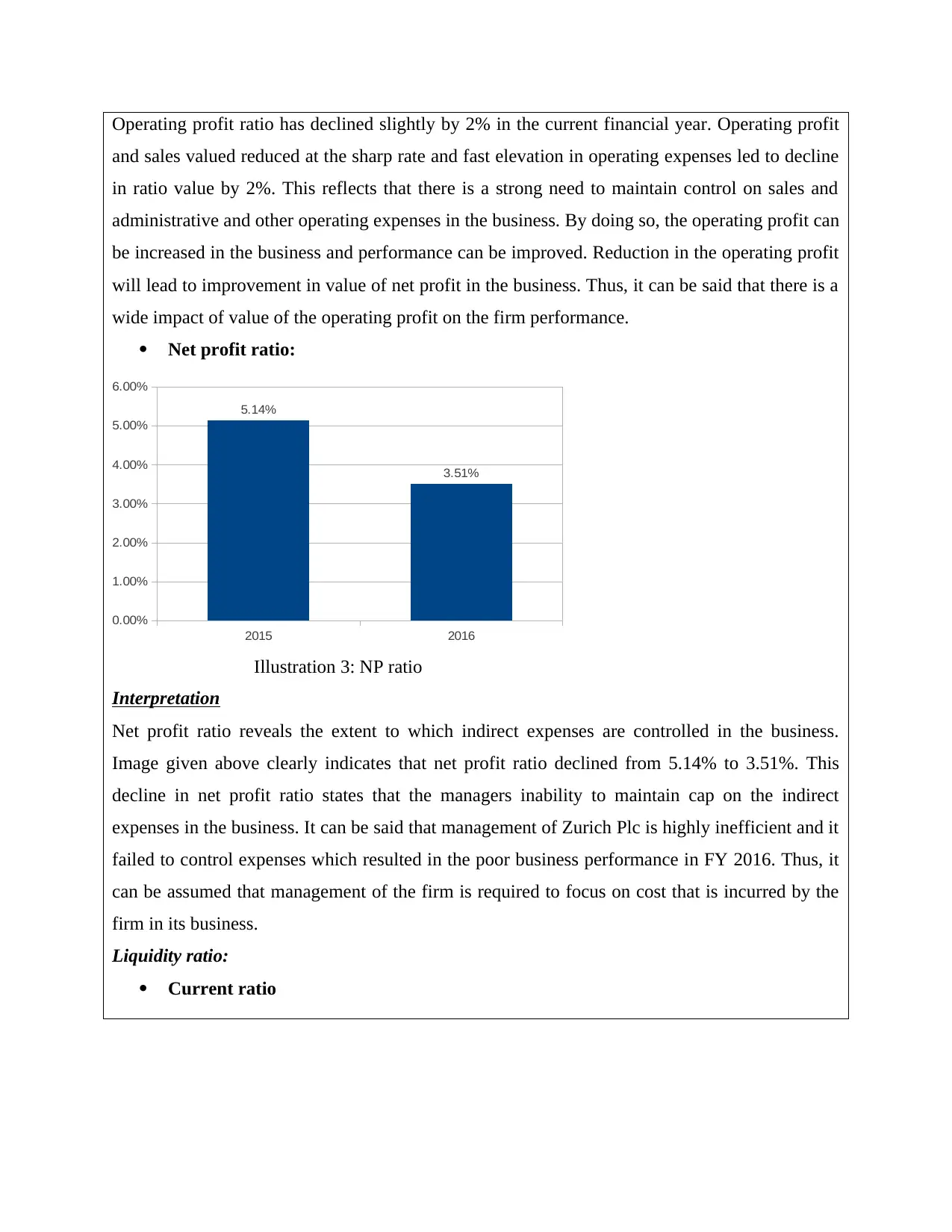

Net profit ratio:

2015 2016

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

5.14%

3.51%

Illustration 3: NP ratio

Interpretation

Net profit ratio reveals the extent to which indirect expenses are controlled in the business.

Image given above clearly indicates that net profit ratio declined from 5.14% to 3.51%. This

decline in net profit ratio states that the managers inability to maintain cap on the indirect

expenses in the business. It can be said that management of Zurich Plc is highly inefficient and it

failed to control expenses which resulted in the poor business performance in FY 2016. Thus, it

can be assumed that management of the firm is required to focus on cost that is incurred by the

firm in its business.

Liquidity ratio:

Current ratio

and sales valued reduced at the sharp rate and fast elevation in operating expenses led to decline

in ratio value by 2%. This reflects that there is a strong need to maintain control on sales and

administrative and other operating expenses in the business. By doing so, the operating profit can

be increased in the business and performance can be improved. Reduction in the operating profit

will lead to improvement in value of net profit in the business. Thus, it can be said that there is a

wide impact of value of the operating profit on the firm performance.

Net profit ratio:

2015 2016

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

5.14%

3.51%

Illustration 3: NP ratio

Interpretation

Net profit ratio reveals the extent to which indirect expenses are controlled in the business.

Image given above clearly indicates that net profit ratio declined from 5.14% to 3.51%. This

decline in net profit ratio states that the managers inability to maintain cap on the indirect

expenses in the business. It can be said that management of Zurich Plc is highly inefficient and it

failed to control expenses which resulted in the poor business performance in FY 2016. Thus, it

can be assumed that management of the firm is required to focus on cost that is incurred by the

firm in its business.

Liquidity ratio:

Current ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2015 2016

0.21

0.22

0.23

0.24

0.25

0.26

0.27

0.28

0.29

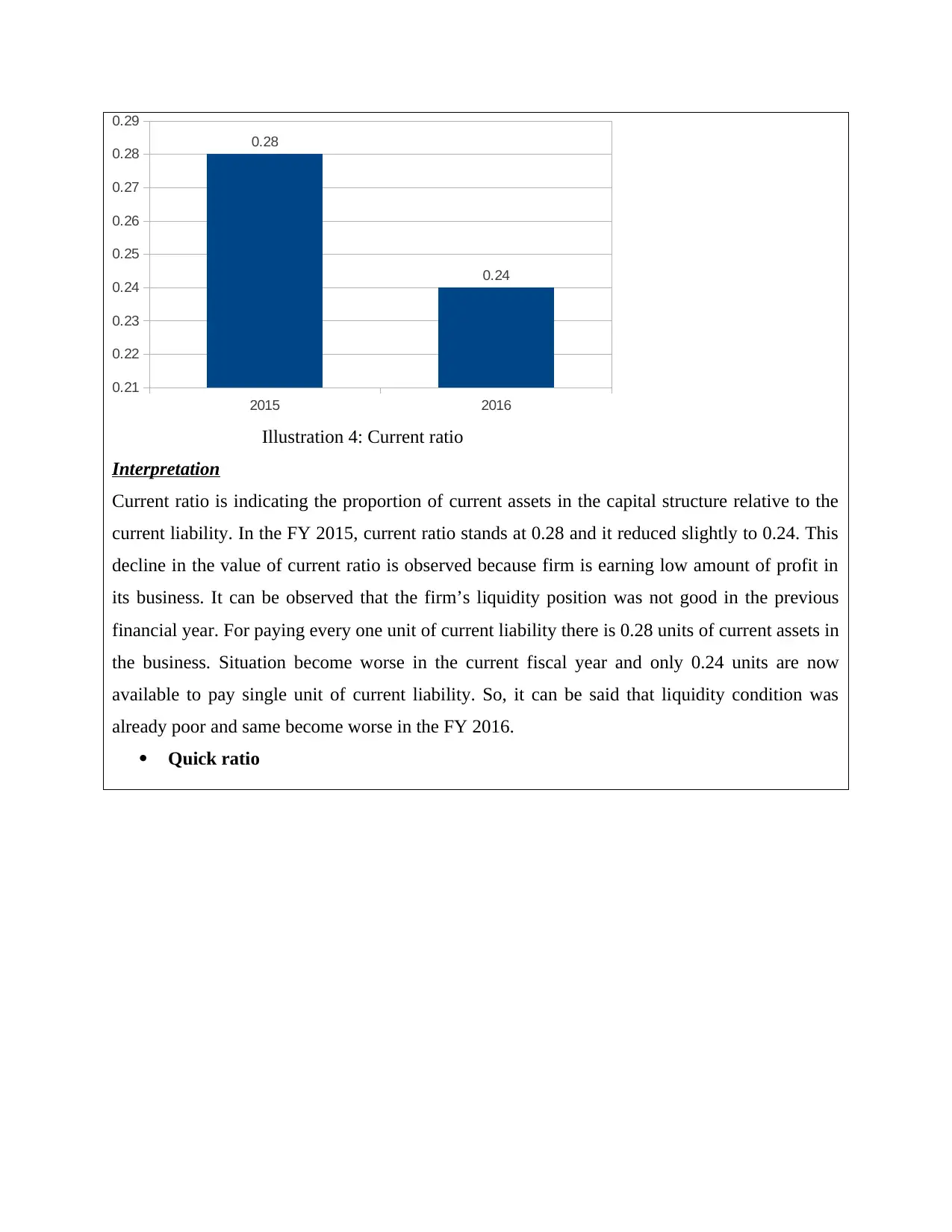

0.28

0.24

Illustration 4: Current ratio

Interpretation

Current ratio is indicating the proportion of current assets in the capital structure relative to the

current liability. In the FY 2015, current ratio stands at 0.28 and it reduced slightly to 0.24. This

decline in the value of current ratio is observed because firm is earning low amount of profit in

its business. It can be observed that the firm’s liquidity position was not good in the previous

financial year. For paying every one unit of current liability there is 0.28 units of current assets in

the business. Situation become worse in the current fiscal year and only 0.24 units are now

available to pay single unit of current liability. So, it can be said that liquidity condition was

already poor and same become worse in the FY 2016.

Quick ratio

0.21

0.22

0.23

0.24

0.25

0.26

0.27

0.28

0.29

0.28

0.24

Illustration 4: Current ratio

Interpretation

Current ratio is indicating the proportion of current assets in the capital structure relative to the

current liability. In the FY 2015, current ratio stands at 0.28 and it reduced slightly to 0.24. This

decline in the value of current ratio is observed because firm is earning low amount of profit in

its business. It can be observed that the firm’s liquidity position was not good in the previous

financial year. For paying every one unit of current liability there is 0.28 units of current assets in

the business. Situation become worse in the current fiscal year and only 0.24 units are now

available to pay single unit of current liability. So, it can be said that liquidity condition was

already poor and same become worse in the FY 2016.

Quick ratio

2015 2016

0

0.05

0.1

0.15

0.2

0.25 0.23

0.18

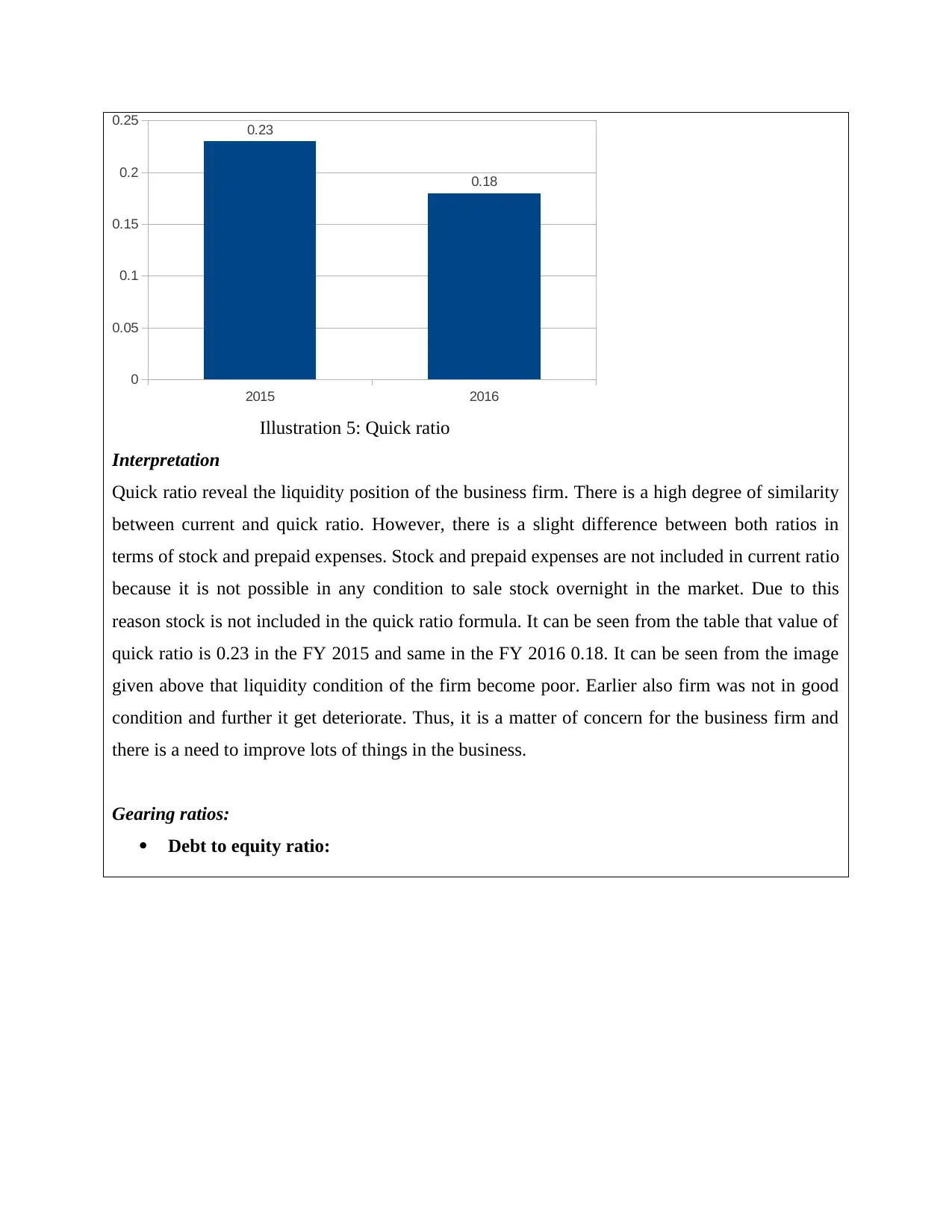

Illustration 5: Quick ratio

Interpretation

Quick ratio reveal the liquidity position of the business firm. There is a high degree of similarity

between current and quick ratio. However, there is a slight difference between both ratios in

terms of stock and prepaid expenses. Stock and prepaid expenses are not included in current ratio

because it is not possible in any condition to sale stock overnight in the market. Due to this

reason stock is not included in the quick ratio formula. It can be seen from the table that value of

quick ratio is 0.23 in the FY 2015 and same in the FY 2016 0.18. It can be seen from the image

given above that liquidity condition of the firm become poor. Earlier also firm was not in good

condition and further it get deteriorate. Thus, it is a matter of concern for the business firm and

there is a need to improve lots of things in the business.

Gearing ratios:

Debt to equity ratio:

0

0.05

0.1

0.15

0.2

0.25 0.23

0.18

Illustration 5: Quick ratio

Interpretation

Quick ratio reveal the liquidity position of the business firm. There is a high degree of similarity

between current and quick ratio. However, there is a slight difference between both ratios in

terms of stock and prepaid expenses. Stock and prepaid expenses are not included in current ratio

because it is not possible in any condition to sale stock overnight in the market. Due to this

reason stock is not included in the quick ratio formula. It can be seen from the table that value of

quick ratio is 0.23 in the FY 2015 and same in the FY 2016 0.18. It can be seen from the image

given above that liquidity condition of the firm become poor. Earlier also firm was not in good

condition and further it get deteriorate. Thus, it is a matter of concern for the business firm and

there is a need to improve lots of things in the business.

Gearing ratios:

Debt to equity ratio:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2015 2016

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

0.2

0.11

0.18

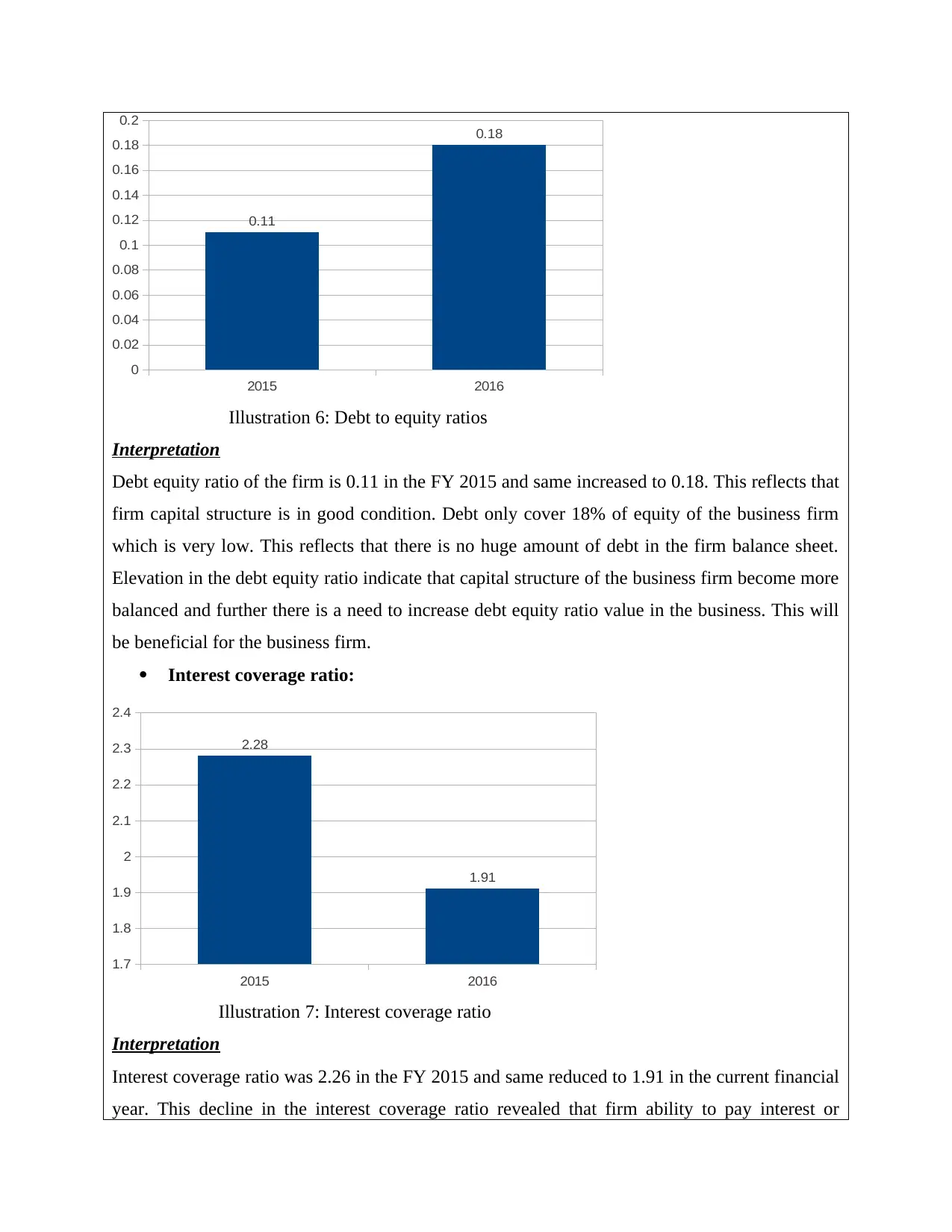

Illustration 6: Debt to equity ratios

Interpretation

Debt equity ratio of the firm is 0.11 in the FY 2015 and same increased to 0.18. This reflects that

firm capital structure is in good condition. Debt only cover 18% of equity of the business firm

which is very low. This reflects that there is no huge amount of debt in the firm balance sheet.

Elevation in the debt equity ratio indicate that capital structure of the business firm become more

balanced and further there is a need to increase debt equity ratio value in the business. This will

be beneficial for the business firm.

Interest coverage ratio:

2015 2016

1.7

1.8

1.9

2

2.1

2.2

2.3

2.4

2.28

1.91

Illustration 7: Interest coverage ratio

Interpretation

Interest coverage ratio was 2.26 in the FY 2015 and same reduced to 1.91 in the current financial

year. This decline in the interest coverage ratio revealed that firm ability to pay interest or

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

0.2

0.11

0.18

Illustration 6: Debt to equity ratios

Interpretation

Debt equity ratio of the firm is 0.11 in the FY 2015 and same increased to 0.18. This reflects that

firm capital structure is in good condition. Debt only cover 18% of equity of the business firm

which is very low. This reflects that there is no huge amount of debt in the firm balance sheet.

Elevation in the debt equity ratio indicate that capital structure of the business firm become more

balanced and further there is a need to increase debt equity ratio value in the business. This will

be beneficial for the business firm.

Interest coverage ratio:

2015 2016

1.7

1.8

1.9

2

2.1

2.2

2.3

2.4

2.28

1.91

Illustration 7: Interest coverage ratio

Interpretation

Interest coverage ratio was 2.26 in the FY 2015 and same reduced to 1.91 in the current financial

year. This decline in the interest coverage ratio revealed that firm ability to pay interest or

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

finance cost out of profit get reduced. This is the negative sign for the business firm. Its liquidity

position is also not good and on this basis it can be said that firm needs to improve its

performance. There must be improvement in the interest coverage ratio of the business firm.

Higher will be the profit and if there will be control on the expenses then in that case interest

coverage ratio will be improved.

Asset utilization ratios:

Fixed assets turnover ratio:

2015 2016

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1 0.93

0.63

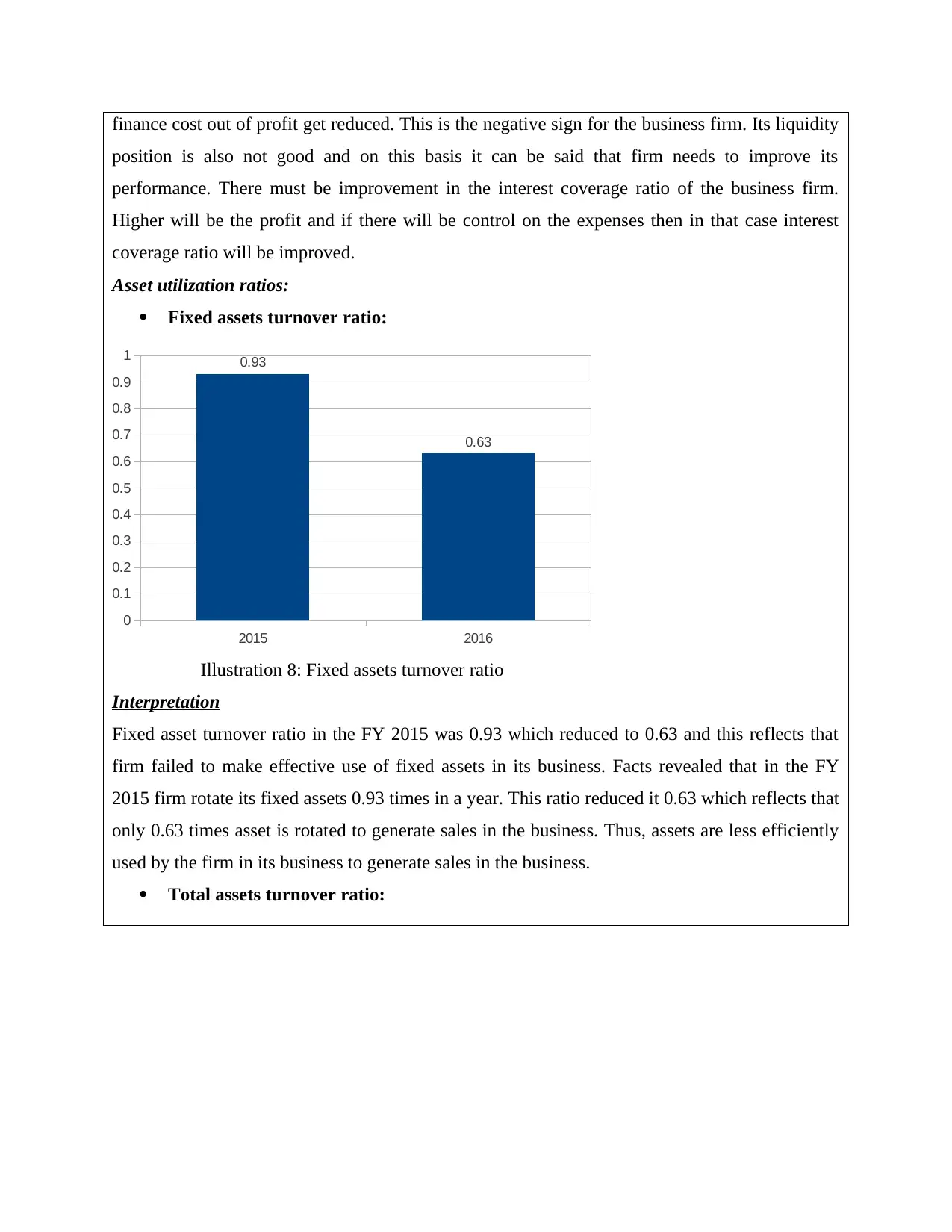

Illustration 8: Fixed assets turnover ratio

Interpretation

Fixed asset turnover ratio in the FY 2015 was 0.93 which reduced to 0.63 and this reflects that

firm failed to make effective use of fixed assets in its business. Facts revealed that in the FY

2015 firm rotate its fixed assets 0.93 times in a year. This ratio reduced it 0.63 which reflects that

only 0.63 times asset is rotated to generate sales in the business. Thus, assets are less efficiently

used by the firm in its business to generate sales in the business.

Total assets turnover ratio:

position is also not good and on this basis it can be said that firm needs to improve its

performance. There must be improvement in the interest coverage ratio of the business firm.

Higher will be the profit and if there will be control on the expenses then in that case interest

coverage ratio will be improved.

Asset utilization ratios:

Fixed assets turnover ratio:

2015 2016

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1 0.93

0.63

Illustration 8: Fixed assets turnover ratio

Interpretation

Fixed asset turnover ratio in the FY 2015 was 0.93 which reduced to 0.63 and this reflects that

firm failed to make effective use of fixed assets in its business. Facts revealed that in the FY

2015 firm rotate its fixed assets 0.93 times in a year. This ratio reduced it 0.63 which reflects that

only 0.63 times asset is rotated to generate sales in the business. Thus, assets are less efficiently

used by the firm in its business to generate sales in the business.

Total assets turnover ratio:

2015 2016

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

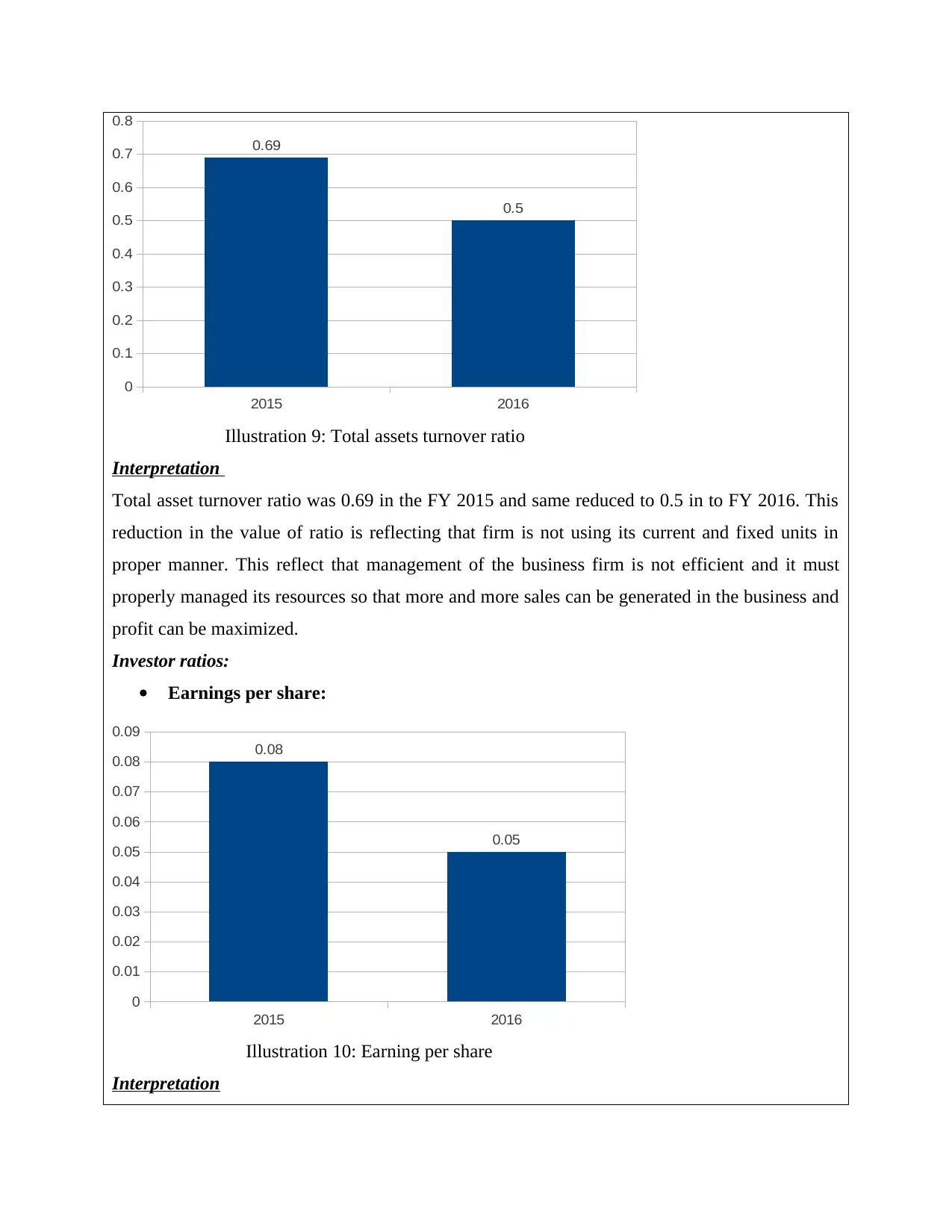

0.69

0.5

Illustration 9: Total assets turnover ratio

Interpretation

Total asset turnover ratio was 0.69 in the FY 2015 and same reduced to 0.5 in to FY 2016. This

reduction in the value of ratio is reflecting that firm is not using its current and fixed units in

proper manner. This reflect that management of the business firm is not efficient and it must

properly managed its resources so that more and more sales can be generated in the business and

profit can be maximized.

Investor ratios:

Earnings per share:

2015 2016

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

0.09

0.08

0.05

Illustration 10: Earning per share

Interpretation

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.69

0.5

Illustration 9: Total assets turnover ratio

Interpretation

Total asset turnover ratio was 0.69 in the FY 2015 and same reduced to 0.5 in to FY 2016. This

reduction in the value of ratio is reflecting that firm is not using its current and fixed units in

proper manner. This reflect that management of the business firm is not efficient and it must

properly managed its resources so that more and more sales can be generated in the business and

profit can be maximized.

Investor ratios:

Earnings per share:

2015 2016

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

0.09

0.08

0.05

Illustration 10: Earning per share

Interpretation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.