Detailed Analysis of Financial Performance Management Report

VerifiedAdded on 2022/12/27

|17

|4707

|46

Report

AI Summary

This report provides a detailed analysis of financial performance, encompassing various aspects of financial management. It begins with an introduction to finance and its importance for businesses, followed by an in-depth exploration of ratio analysis, including liquidity, solvency, profitability, efficiency, and market ratios. The report then delves into the concept of Return on Capital Employed (ROCE) and its formula, providing examples and analysis of British American Tobacco and Philip Morris International. The importance of operating margin and its comparison with net profit margin are discussed, highlighting its significance in assessing a company's ability to generate profits. Furthermore, the report covers the benefits of budgeting and its role in financial planning and control, along with an overview of different profit margins and their levels. The report also covers the benefits of budgeting and its role in financial planning and control.

Managing

Finance

Performance

Finance

Performance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

PART 2............................................................................................................................................6

PART 3............................................................................................................................................9

PART 4..........................................................................................................................................12

CONCLUSION..............................................................................................................................13

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

PART 2............................................................................................................................................6

PART 3............................................................................................................................................9

PART 4..........................................................................................................................................12

CONCLUSION..............................................................................................................................13

INTRODUCTION

Finance is the necessary element for the company’s. This helps companies for running

activities as it manages funds for the company. This will help it’s for managing activities as these

are needs for funds & finance helps for it. The company which has funds for their needs which

helps company for better performance which helps for higher profitability for the businesses. It

includes managing funds through assessing the financial performance which it needs for long

term decisions. Companies are use financial statements which are balance sheet, income

statement etc. These helps company for knowing which resource gives it higher profitability for

its activities. For example, the company purchases assets for running its activities it helps it for

managing funds. Finance is the term for activities which are for management, creation, study for

money & investment. It is for how company managing the needs for funds. It is process for

raising funds for the company’s. Company’s use various financial methods for it which are

financial statements which helps for knowing financial position for helps for ratio analysis.

Companies for investing for the projects it uses investment appraisal techniques which helps it’s

for knowing which project gives it higher profits which helps company for better performance

which helps for higher profitability for the businesses.

PART 1

Ratio analysis: Ratio analysis is a continuous process of gaining a company's understanding,

efficiency, and profitability by studying its financial statements such as balance and revenue

statements. Ratio analysis helps companies for knowing its financial position for the businesses.

Investors and analysts use Ratio analysis to measure the health of companies by examining past

and current financial statements. Comparative data can show how a company is performing over

time and can be used to measure potential performance in the future. This data can also compare

the company's financial position with sector estimates while measuring how a company interacts

with others in the same sector.

Investors can easily use ratio ratings, and all the calculations needed to calculate the ratios are

found in the company's financial statements.

1

Finance is the necessary element for the company’s. This helps companies for running

activities as it manages funds for the company. This will help it’s for managing activities as these

are needs for funds & finance helps for it. The company which has funds for their needs which

helps company for better performance which helps for higher profitability for the businesses. It

includes managing funds through assessing the financial performance which it needs for long

term decisions. Companies are use financial statements which are balance sheet, income

statement etc. These helps company for knowing which resource gives it higher profitability for

its activities. For example, the company purchases assets for running its activities it helps it for

managing funds. Finance is the term for activities which are for management, creation, study for

money & investment. It is for how company managing the needs for funds. It is process for

raising funds for the company’s. Company’s use various financial methods for it which are

financial statements which helps for knowing financial position for helps for ratio analysis.

Companies for investing for the projects it uses investment appraisal techniques which helps it’s

for knowing which project gives it higher profits which helps company for better performance

which helps for higher profitability for the businesses.

PART 1

Ratio analysis: Ratio analysis is a continuous process of gaining a company's understanding,

efficiency, and profitability by studying its financial statements such as balance and revenue

statements. Ratio analysis helps companies for knowing its financial position for the businesses.

Investors and analysts use Ratio analysis to measure the health of companies by examining past

and current financial statements. Comparative data can show how a company is performing over

time and can be used to measure potential performance in the future. This data can also compare

the company's financial position with sector estimates while measuring how a company interacts

with others in the same sector.

Investors can easily use ratio ratings, and all the calculations needed to calculate the ratios are

found in the company's financial statements.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Estimates of comparison points for companies. They check stocks within the industry. Similarly,

they rate the company today compared to its historical numbers. In many cases, it is important to

understand the dynamics of dynamic driving as executives are more flexible at times, changing

their strategy to make stocks and companies more attractive. Generally, ratios are not used

separately but are combined with other ratios.

1. Liquidity ratio: Liquidity ratios measure the company's ability to pay off its short-term

liabilities as appropriate, using the company's current or immediate assets. Liquidity ratios

include current rate, acceleration rate, and operating cost. It helps company for paying its

short term debts which it needs for current assets. It helps company for knowing how much

assets company needs for the paying its debts which helps for managing financial

performance which helps for the better performance which helps for the higher profitability

for the businesses.

2. Solvency Ratios: It also called financial growth rates, solvency rates compare a company's

debt levels with its assets, equity, and cash flows, to assess whether a company can continue to

move long-term, by paying off its long-term debt and interest on its debt. Examples of solvency

ratios include: debt equity ratios, debt ratios, and interest rate estimates.

3. Profitability ratios: These estimates reflect how a company can generate profits in its

operations. Profit margins, asset returns, equity returns, reimbursements, and total cash

equivalents are all examples of profit estimates.

4. Efficiency Ratios: It also called performance measures, performance measurements assess

how well a company uses its assets and liabilities to generate sales and increase profits.

Significant performance measurements include: profit margin, revenue, and sales dates in the

asset.

5. Integrating ratios: Measurement ratios measure a company's ability to make interest

payments and other obligations related to its liabilities. Examples include interest rate and credit

service rating.

2

they rate the company today compared to its historical numbers. In many cases, it is important to

understand the dynamics of dynamic driving as executives are more flexible at times, changing

their strategy to make stocks and companies more attractive. Generally, ratios are not used

separately but are combined with other ratios.

1. Liquidity ratio: Liquidity ratios measure the company's ability to pay off its short-term

liabilities as appropriate, using the company's current or immediate assets. Liquidity ratios

include current rate, acceleration rate, and operating cost. It helps company for paying its

short term debts which it needs for current assets. It helps company for knowing how much

assets company needs for the paying its debts which helps for managing financial

performance which helps for the better performance which helps for the higher profitability

for the businesses.

2. Solvency Ratios: It also called financial growth rates, solvency rates compare a company's

debt levels with its assets, equity, and cash flows, to assess whether a company can continue to

move long-term, by paying off its long-term debt and interest on its debt. Examples of solvency

ratios include: debt equity ratios, debt ratios, and interest rate estimates.

3. Profitability ratios: These estimates reflect how a company can generate profits in its

operations. Profit margins, asset returns, equity returns, reimbursements, and total cash

equivalents are all examples of profit estimates.

4. Efficiency Ratios: It also called performance measures, performance measurements assess

how well a company uses its assets and liabilities to generate sales and increase profits.

Significant performance measurements include: profit margin, revenue, and sales dates in the

asset.

5. Integrating ratios: Measurement ratios measure a company's ability to make interest

payments and other obligations related to its liabilities. Examples include interest rate and credit

service rating.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

6. Market ratios: These ratios are most commonly used in basic analysis. It includes dividend

production, P / E rate, per share per share (EPS), and dividend payment rate. Investors use these

metrics to predict future gains and performance.

These ratios help company for knowing its financial position for knowing its liquidity, turnover,

profits which helps for better performance which helps for higher profitability for the businesses.

Reimbursement (ROCE) is a good start for a company. ROCE is a financial measure that

indicates that a company is doing a good job of generating profits in its capital. Companies have

a variety of financial resources that they use to build and grow their businesses. The capital

creates wealth through investment and can include things like corporate security, manufacturing

equipment, land, software, patents and brand names.

How a company chooses to distribute its key assets can directly affect its performance. In many

cases, it could mean the difference between a company that makes a good return or the loss of

money. ROCE is an important tool for measuring this.

While companies use ROCE as a useful metric to measure their performance, they are not the

only ones who can benefit from it. Analysts, shareholders, and prospective investors all use

ROCE as a reliable measure of business performance when analysing an investment company.

ROCE is especially useful when comparing businesses in the same industry. It is better used in

conjunction with other methods than in isolation.

ROCE is one of the many profit scales used to evaluate a company's performance. It is designed

to show the company how well it is using its revenue by looking at the total profit generated in

each dollar. In addition to ROCE, companies may also review other significant return rates when

analysing their performance, such as asset return (ROA), equity return (ROE), and return on

invested capital (ROIC).

3

production, P / E rate, per share per share (EPS), and dividend payment rate. Investors use these

metrics to predict future gains and performance.

These ratios help company for knowing its financial position for knowing its liquidity, turnover,

profits which helps for better performance which helps for higher profitability for the businesses.

Reimbursement (ROCE) is a good start for a company. ROCE is a financial measure that

indicates that a company is doing a good job of generating profits in its capital. Companies have

a variety of financial resources that they use to build and grow their businesses. The capital

creates wealth through investment and can include things like corporate security, manufacturing

equipment, land, software, patents and brand names.

How a company chooses to distribute its key assets can directly affect its performance. In many

cases, it could mean the difference between a company that makes a good return or the loss of

money. ROCE is an important tool for measuring this.

While companies use ROCE as a useful metric to measure their performance, they are not the

only ones who can benefit from it. Analysts, shareholders, and prospective investors all use

ROCE as a reliable measure of business performance when analysing an investment company.

ROCE is especially useful when comparing businesses in the same industry. It is better used in

conjunction with other methods than in isolation.

ROCE is one of the many profit scales used to evaluate a company's performance. It is designed

to show the company how well it is using its revenue by looking at the total profit generated in

each dollar. In addition to ROCE, companies may also review other significant return rates when

analysing their performance, such as asset return (ROA), equity return (ROE), and return on

invested capital (ROIC).

3

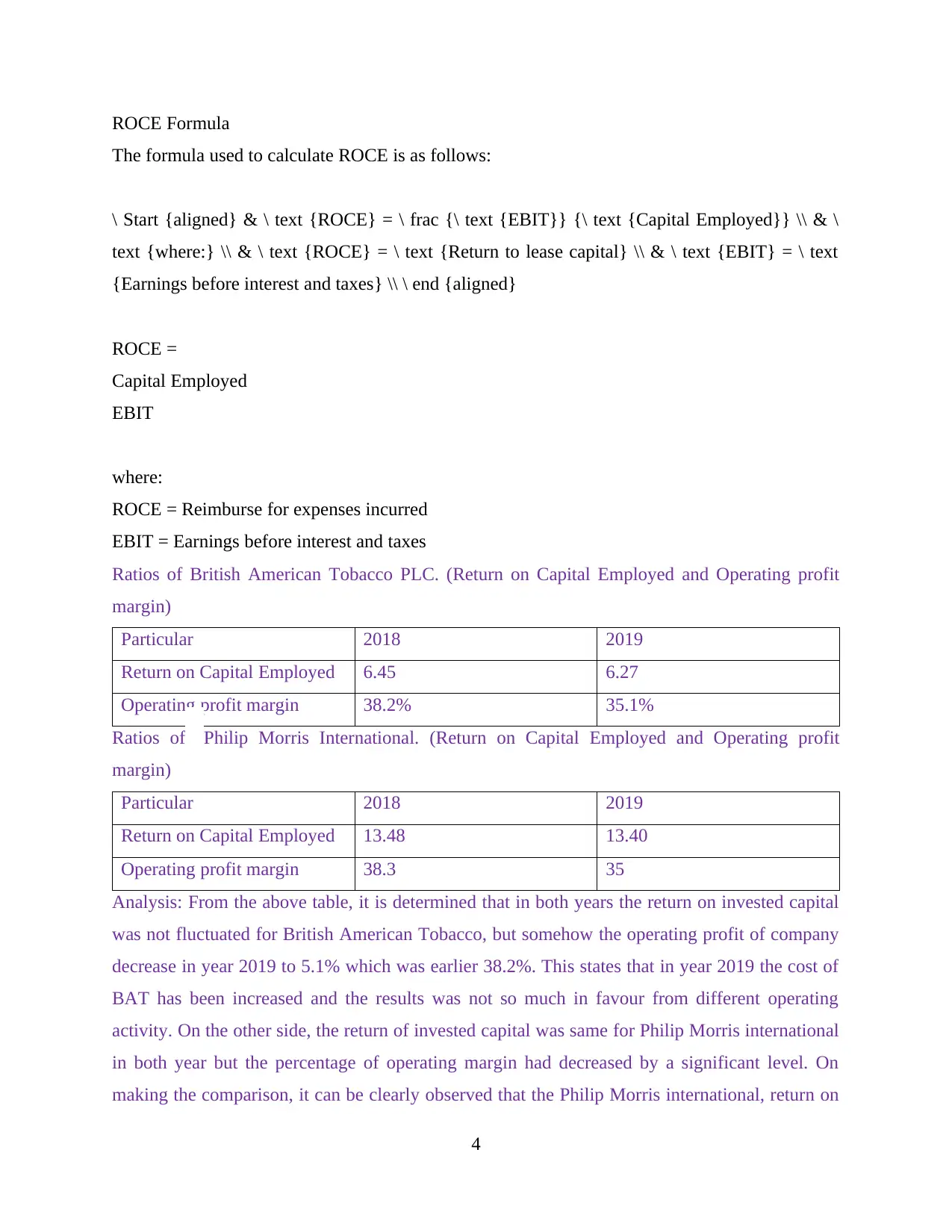

ROCE Formula

The formula used to calculate ROCE is as follows:

\ Start {aligned} & \ text {ROCE} = \ frac {\ text {EBIT}} {\ text {Capital Employed}} \\ & \

text {where:} \\ & \ text {ROCE} = \ text {Return to lease capital} \\ & \ text {EBIT} = \ text

{Earnings before interest and taxes} \\ \ end {aligned}

ROCE =

Capital Employed

EBIT

where:

ROCE = Reimburse for expenses incurred

EBIT = Earnings before interest and taxes

Ratios of British American Tobacco PLC. (Return on Capital Employed and Operating profit

margin)

Particular 2018 2019

Return on Capital Employed 6.45 6.27

Operating profit margin 38.2% 35.1%

Ratios of Philip Morris International. (Return on Capital Employed and Operating profit

margin)

Particular 2018 2019

Return on Capital Employed 13.48 13.40

Operating profit margin 38.3 35

Analysis: From the above table, it is determined that in both years the return on invested capital

was not fluctuated for British American Tobacco, but somehow the operating profit of company

decrease in year 2019 to 5.1% which was earlier 38.2%. This states that in year 2019 the cost of

BAT has been increased and the results was not so much in favour from different operating

activity. On the other side, the return of invested capital was same for Philip Morris international

in both year but the percentage of operating margin had decreased by a significant level. On

making the comparison, it can be clearly observed that the Philip Morris international, return on

4

The formula used to calculate ROCE is as follows:

\ Start {aligned} & \ text {ROCE} = \ frac {\ text {EBIT}} {\ text {Capital Employed}} \\ & \

text {where:} \\ & \ text {ROCE} = \ text {Return to lease capital} \\ & \ text {EBIT} = \ text

{Earnings before interest and taxes} \\ \ end {aligned}

ROCE =

Capital Employed

EBIT

where:

ROCE = Reimburse for expenses incurred

EBIT = Earnings before interest and taxes

Ratios of British American Tobacco PLC. (Return on Capital Employed and Operating profit

margin)

Particular 2018 2019

Return on Capital Employed 6.45 6.27

Operating profit margin 38.2% 35.1%

Ratios of Philip Morris International. (Return on Capital Employed and Operating profit

margin)

Particular 2018 2019

Return on Capital Employed 13.48 13.40

Operating profit margin 38.3 35

Analysis: From the above table, it is determined that in both years the return on invested capital

was not fluctuated for British American Tobacco, but somehow the operating profit of company

decrease in year 2019 to 5.1% which was earlier 38.2%. This states that in year 2019 the cost of

BAT has been increased and the results was not so much in favour from different operating

activity. On the other side, the return of invested capital was same for Philip Morris international

in both year but the percentage of operating margin had decreased by a significant level. On

making the comparison, it can be clearly observed that the Philip Morris international, return on

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

capital invested in different operation and investments are higher than British American

Tobacco. Although the operating profit margin remains same for both firms as they are operating

in same industry, thus most of their operating activities are similar.

You can get a company income before interest and taxes (EBIT) on its income statement. Some

analysts use the full advantage over EBIT to perform calculations. You can calculate the amount

spent from the company's balance.

ROCE is a useful measure of financial efficiency because it measures profit after investing in the

amount of money used to create that level of profitability. Comparing the ROCE with the basic

financial calculation may show the importance of looking at the ROCE.

Operating Margin differs from Net Profit Margin as a measure of a company's ability to be

profitable. The difference is that the first one is based solely on its performance without the

expense of interest rates and taxes.

An example of how this profit metric can be used is the condition of the acquirer that considers

the purchase made. When the acquirer analyses the targeted company, they will be looking at

potential improvements they can make to the operation. An effective profit line provides insight

into how a targeted company operates compared to its peers, in particular, how a company

effectively manages its costs to maximize profits. Leaving interest and taxes are helpful because

a mixed purchase can put a company in a completely new debt, which will make the cost of

historical interest less significant.

The company's operating profit margin shows how well it is managed because operating costs

such as salaries, rent, and equipment leasing are variable costs, rather than fixed costs. The

company may have little control over the direct production costs such as the cost of materials

needed to produce the company's products. However, company executives have a greater

understanding of areas such as how much they prefer to spend on office hiring, services and

operations. Therefore, a company's effective profit margin is often seen as a high indicator of the

strength of a company's management team, compared to a full or complete line of profits.

Profit limit is one of the most widely used profit margins for measuring the level at which a

company or business is making money. It represents what percentage of sales have become

5

Tobacco. Although the operating profit margin remains same for both firms as they are operating

in same industry, thus most of their operating activities are similar.

You can get a company income before interest and taxes (EBIT) on its income statement. Some

analysts use the full advantage over EBIT to perform calculations. You can calculate the amount

spent from the company's balance.

ROCE is a useful measure of financial efficiency because it measures profit after investing in the

amount of money used to create that level of profitability. Comparing the ROCE with the basic

financial calculation may show the importance of looking at the ROCE.

Operating Margin differs from Net Profit Margin as a measure of a company's ability to be

profitable. The difference is that the first one is based solely on its performance without the

expense of interest rates and taxes.

An example of how this profit metric can be used is the condition of the acquirer that considers

the purchase made. When the acquirer analyses the targeted company, they will be looking at

potential improvements they can make to the operation. An effective profit line provides insight

into how a targeted company operates compared to its peers, in particular, how a company

effectively manages its costs to maximize profits. Leaving interest and taxes are helpful because

a mixed purchase can put a company in a completely new debt, which will make the cost of

historical interest less significant.

The company's operating profit margin shows how well it is managed because operating costs

such as salaries, rent, and equipment leasing are variable costs, rather than fixed costs. The

company may have little control over the direct production costs such as the cost of materials

needed to produce the company's products. However, company executives have a greater

understanding of areas such as how much they prefer to spend on office hiring, services and

operations. Therefore, a company's effective profit margin is often seen as a high indicator of the

strength of a company's management team, compared to a full or complete line of profits.

Profit limit is one of the most widely used profit margins for measuring the level at which a

company or business is making money. It represents what percentage of sales have become

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

profitable. Simply put, a percentage figure indicates how many cents a profit a business has

generated per dollar of sales. For example, if an entity reports that it has earned a 35% profit

margin in the last quarter, it means that it has an income of $ 0.35 per dollar of sales made.

There are many types of profit margins. In day-to-day operations, however, it usually refers to

the full profit line, the company's lower line after all other expenses, including tax and one

exception, deducted from revenue.

Businesses and individuals around the world engage in economic activities for profit. However,

whole numbers - such as total sales worth $ X million, $ 1 billion in business costs, or $ Z salary

- fail to provide a clear and realistic picture of the business's profitability and performance.

Various accounting methods are used to calculate the profit (or loss) of a business, making it

easier to evaluate the performance of a business at different times or to compare it with

competitors. These measures are called profit margins.

While affiliated businesses, such as local stores, may calculate profit margins on their preferred

frequency (such as weekly or every two weeks), large businesses including listed companies are

required to report within a reporting period (such as quarterly or annual). Businesses that may be

working on a loan may need to calculate and report it to the lender (such as a bank) on a monthly

basis as part of the normal process.

There are four levels of profit or profit margins: total profit, employment benefit, pre-tax benefit,

and total profit. This is reflected in the company's revenue statement in the following order: The

company takes the sales revenue, and pays the direct cost of the service product. The rest is a

huge limit. It then pays for indirect costs such as company headquarters, advertising, and R&D.

Thereafter it pays interest on the debt and adds or removes any unusual charges or entities

unrelated to the company's principal business by the pre-tax limit remaining. It then pays taxes,

leaving the net limit, also known as revenue, which is the most important factor.

6

generated per dollar of sales. For example, if an entity reports that it has earned a 35% profit

margin in the last quarter, it means that it has an income of $ 0.35 per dollar of sales made.

There are many types of profit margins. In day-to-day operations, however, it usually refers to

the full profit line, the company's lower line after all other expenses, including tax and one

exception, deducted from revenue.

Businesses and individuals around the world engage in economic activities for profit. However,

whole numbers - such as total sales worth $ X million, $ 1 billion in business costs, or $ Z salary

- fail to provide a clear and realistic picture of the business's profitability and performance.

Various accounting methods are used to calculate the profit (or loss) of a business, making it

easier to evaluate the performance of a business at different times or to compare it with

competitors. These measures are called profit margins.

While affiliated businesses, such as local stores, may calculate profit margins on their preferred

frequency (such as weekly or every two weeks), large businesses including listed companies are

required to report within a reporting period (such as quarterly or annual). Businesses that may be

working on a loan may need to calculate and report it to the lender (such as a bank) on a monthly

basis as part of the normal process.

There are four levels of profit or profit margins: total profit, employment benefit, pre-tax benefit,

and total profit. This is reflected in the company's revenue statement in the following order: The

company takes the sales revenue, and pays the direct cost of the service product. The rest is a

huge limit. It then pays for indirect costs such as company headquarters, advertising, and R&D.

Thereafter it pays interest on the debt and adds or removes any unusual charges or entities

unrelated to the company's principal business by the pre-tax limit remaining. It then pays taxes,

leaving the net limit, also known as revenue, which is the most important factor.

6

PART 2

Benefits of Budgeting:

Creating a budget assists managers at all levels in carrying out planned tasks.

(a) Performance levels:

Budgets provide performance standards for various periods and sub-periods, actual performance

can be compared to standards at regular intervals and the opposite adjustments can be made.

(b) Budgets facilitate planning:

Budgets specify the time and amount to be spent by the heads of the various departments and,

therefore, serve as the basis for making accurate and specific plans. Budgets are based on defined

activities that are suitable for testing and change (flexible). Therefore, objectives are achieved

within the defined objectives and thus utilize the use of resources.

It also encourages devolution as budgets limit the work that needs to be done by senior and low-

level managers. Higher level managers can focus on strategic thinking by transferring standard

tasks to lower levels.

(c) Baseline:

When managers at various levels are involved in budgeting, it oversees the various activities of

the organization. Managers of different departments at different levels cooperate and coordinate

their activities in order to make the best use of organizational resources.

Budget control coordinates the activities of the various units to bring it closer to the full goals.

For example, the sales budget should be aligned with the procurement budget which should be in

line with the labor budget. This requires the smooth flow of information between the various

departments that assist in achieving integration.

(d) Motivation and job satisfaction:

Active management participates in the preparation of budgets. This increases their motivation,

job satisfaction and job efficiency.

(e) Facilitator:

7

Benefits of Budgeting:

Creating a budget assists managers at all levels in carrying out planned tasks.

(a) Performance levels:

Budgets provide performance standards for various periods and sub-periods, actual performance

can be compared to standards at regular intervals and the opposite adjustments can be made.

(b) Budgets facilitate planning:

Budgets specify the time and amount to be spent by the heads of the various departments and,

therefore, serve as the basis for making accurate and specific plans. Budgets are based on defined

activities that are suitable for testing and change (flexible). Therefore, objectives are achieved

within the defined objectives and thus utilize the use of resources.

It also encourages devolution as budgets limit the work that needs to be done by senior and low-

level managers. Higher level managers can focus on strategic thinking by transferring standard

tasks to lower levels.

(c) Baseline:

When managers at various levels are involved in budgeting, it oversees the various activities of

the organization. Managers of different departments at different levels cooperate and coordinate

their activities in order to make the best use of organizational resources.

Budget control coordinates the activities of the various units to bring it closer to the full goals.

For example, the sales budget should be aligned with the procurement budget which should be in

line with the labor budget. This requires the smooth flow of information between the various

departments that assist in achieving integration.

(d) Motivation and job satisfaction:

Active management participates in the preparation of budgets. This increases their motivation,

job satisfaction and job efficiency.

(e) Facilitator:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Budgets help to show the future impact on a company's performance. Environmental changes can

be incorporated into organizational policies and procedures.

(f) Facilitating communication:

Budgets provide for horizontal and direct communication in an organization. Plans and

objectives are communicated to the line function and at all levels in the various departments to

assess the impact of departmental actions on organizational performance.

(g) Facilitating the empowerment:

Budgets specify who should spend, when and where and budget areas that can generate

additional revenue. Financial speculation enables senior management to delegate to subordinates

to perform budgeted tasks within budget limits.

Budget Limits:

Budgets are subject to the following limitations:

(a) Overspending:

Sometimes the budget ends. People believe that if they do not spend their money on time, their

future allotment will be reduced. This can lead to the use of areas where it is not required.

In some cases, budget amounts remain unused and, therefore, are used during the expiry of

budget periods to maintain future allocations. This leads to overspending and negatively affects

the effectiveness of the purpose and objectives.

(b) Consistency:

Budgets specify the amount to be spent on various items. If managers do not have the ability to

change the amount allocated to a variety of items depending on the situation, there will be

overuse in some areas and less consumption in others. Managers who restrict their freedom of

use may shift their focus from organizational goals to budgeted activities. This can produce firms

that lead to losses rather than profits.

(c) Guessing for the future:

8

be incorporated into organizational policies and procedures.

(f) Facilitating communication:

Budgets provide for horizontal and direct communication in an organization. Plans and

objectives are communicated to the line function and at all levels in the various departments to

assess the impact of departmental actions on organizational performance.

(g) Facilitating the empowerment:

Budgets specify who should spend, when and where and budget areas that can generate

additional revenue. Financial speculation enables senior management to delegate to subordinates

to perform budgeted tasks within budget limits.

Budget Limits:

Budgets are subject to the following limitations:

(a) Overspending:

Sometimes the budget ends. People believe that if they do not spend their money on time, their

future allotment will be reduced. This can lead to the use of areas where it is not required.

In some cases, budget amounts remain unused and, therefore, are used during the expiry of

budget periods to maintain future allocations. This leads to overspending and negatively affects

the effectiveness of the purpose and objectives.

(b) Consistency:

Budgets specify the amount to be spent on various items. If managers do not have the ability to

change the amount allocated to a variety of items depending on the situation, there will be

overuse in some areas and less consumption in others. Managers who restrict their freedom of

use may shift their focus from organizational goals to budgeted activities. This can produce firms

that lead to losses rather than profits.

(c) Guessing for the future:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Since budgets are based on future forecasts, if events do not turn out as intended, budget

allocations will need to be redistributed. Therefore, uncertainty in the future could affect the

reliability of budgets. However, this does not undermine the value of budgets. Scientific

forecasts can help to make more accurate and reliable forecasts and, thus, increase budget

efficiency.

(d) New barrier to change:

When funds are allocated to different operating budgets, access to additional funding and

resources to take advantage of the environmental opportunity may not be possible and the budget

may, in turn, affect opportunities for innovation and change.

(e) With emphasis on budgeted objectives:

By staying within the bounds of budgeted goals, management can ignore the organisation's goals

and achieve the budgeted goals of the organization.

(f) Based on past results:

While budgets highlight future speculation, the past provides an important basis for budget

preparation. Events that were not important in the past may not be part of future budgets if they

are to be significant in the future. This problem can also be overcome by creating sub-budgets

where key activities are reviewed throughout the budget period that forms part of the budget.

PART 3

Benefits:

1. Best Strategic Planning

Balanced Scorecard provides a powerful framework for building and communicating strategies.

The business model is seen in the Strategy Map which helps managers to consider the

relationship of cause and effect between the various strategic objectives. The process of building

a Strategic Map ensures that agreement is reached for strategic objectives. It means that the

9

allocations will need to be redistributed. Therefore, uncertainty in the future could affect the

reliability of budgets. However, this does not undermine the value of budgets. Scientific

forecasts can help to make more accurate and reliable forecasts and, thus, increase budget

efficiency.

(d) New barrier to change:

When funds are allocated to different operating budgets, access to additional funding and

resources to take advantage of the environmental opportunity may not be possible and the budget

may, in turn, affect opportunities for innovation and change.

(e) With emphasis on budgeted objectives:

By staying within the bounds of budgeted goals, management can ignore the organisation's goals

and achieve the budgeted goals of the organization.

(f) Based on past results:

While budgets highlight future speculation, the past provides an important basis for budget

preparation. Events that were not important in the past may not be part of future budgets if they

are to be significant in the future. This problem can also be overcome by creating sub-budgets

where key activities are reviewed throughout the budget period that forms part of the budget.

PART 3

Benefits:

1. Best Strategic Planning

Balanced Scorecard provides a powerful framework for building and communicating strategies.

The business model is seen in the Strategy Map which helps managers to consider the

relationship of cause and effect between the various strategic objectives. The process of building

a Strategic Map ensures that agreement is reached for strategic objectives. It means that the

9

performance results and key owners or future operational drivers are identified to create a

complete picture of the plan.

2. Communication and Performance Strategic Development

Having a one-page plan image allows companies to easily communicate strategies internally and

externally. We have long known that a picture costs a thousand words. This 'on-page strategy'

helps to understand the strategy and helps to involve external staff and stakeholders in the

delivery and review of the strategy. One thing to keep in mind is that it is difficult for people to

help create a strategy that they do not fully understand.

3. Better Alignment of Designs and Steps

The Balanced Scorecard helps organizations map their projects and programs into a variety of

strategic objectives, ensuring that projects and programs are firmly focused on achieving more

strategic goals.

4. Better Management Information

The Balanced Scorecard approach helps organizations design key performance indicators for

their various strategic objectives. This ensures that companies measure what is really important.

Research shows that companies with a BSC approach tend to report high quality management

information and make better decisions.

5. Improved Performance Reporting

The Balanced Scorecard can be used to guide the design of performance reports and dashboards.

This ensures that management reporting focuses on the most important strategic issues and helps

companies monitor the implementation of their plan.

6. Better organizational coordination

10

complete picture of the plan.

2. Communication and Performance Strategic Development

Having a one-page plan image allows companies to easily communicate strategies internally and

externally. We have long known that a picture costs a thousand words. This 'on-page strategy'

helps to understand the strategy and helps to involve external staff and stakeholders in the

delivery and review of the strategy. One thing to keep in mind is that it is difficult for people to

help create a strategy that they do not fully understand.

3. Better Alignment of Designs and Steps

The Balanced Scorecard helps organizations map their projects and programs into a variety of

strategic objectives, ensuring that projects and programs are firmly focused on achieving more

strategic goals.

4. Better Management Information

The Balanced Scorecard approach helps organizations design key performance indicators for

their various strategic objectives. This ensures that companies measure what is really important.

Research shows that companies with a BSC approach tend to report high quality management

information and make better decisions.

5. Improved Performance Reporting

The Balanced Scorecard can be used to guide the design of performance reports and dashboards.

This ensures that management reporting focuses on the most important strategic issues and helps

companies monitor the implementation of their plan.

6. Better organizational coordination

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.