Financial Performance Analysis: Accounting and Finance Report

VerifiedAdded on 2022/12/23

|12

|1682

|23

Report

AI Summary

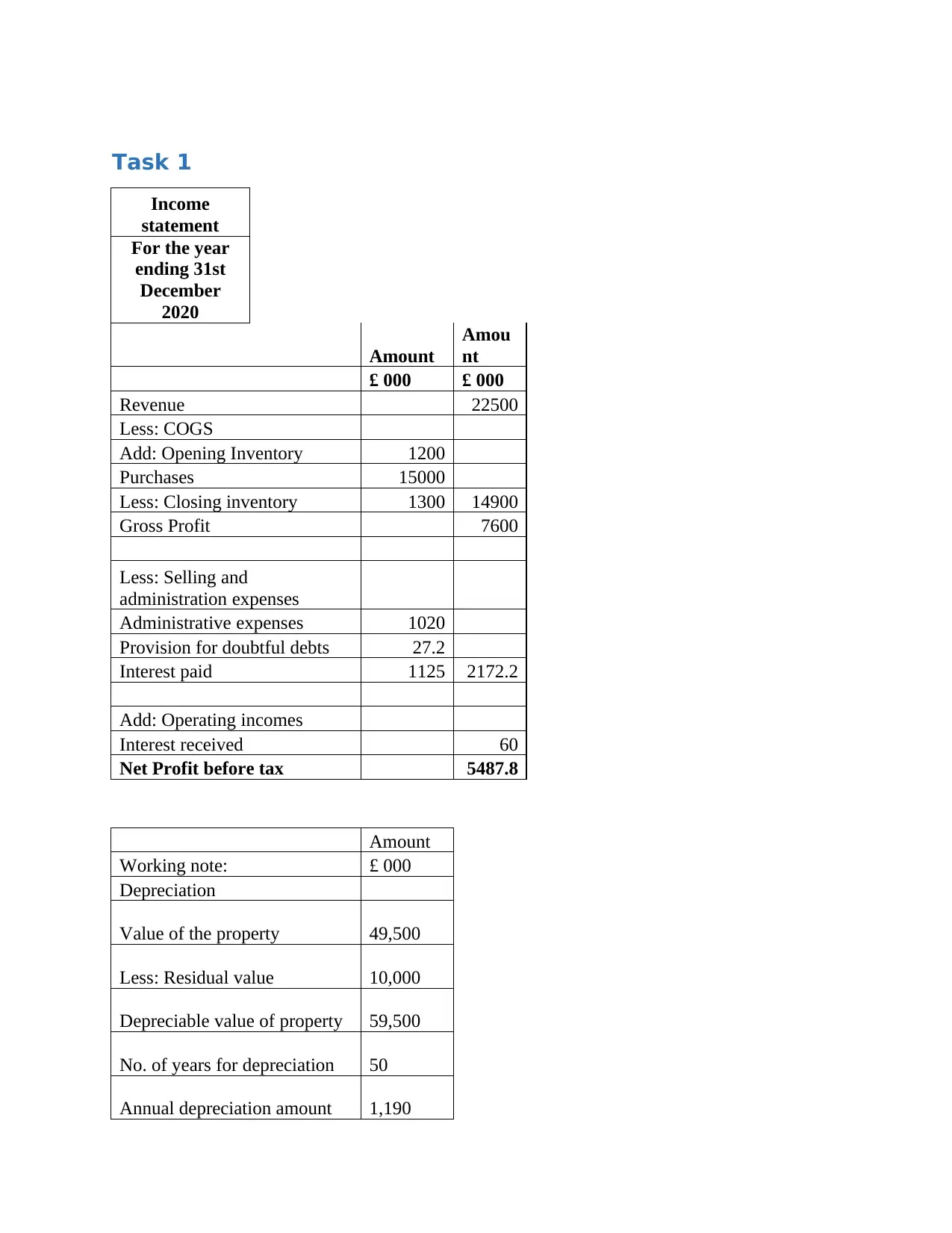

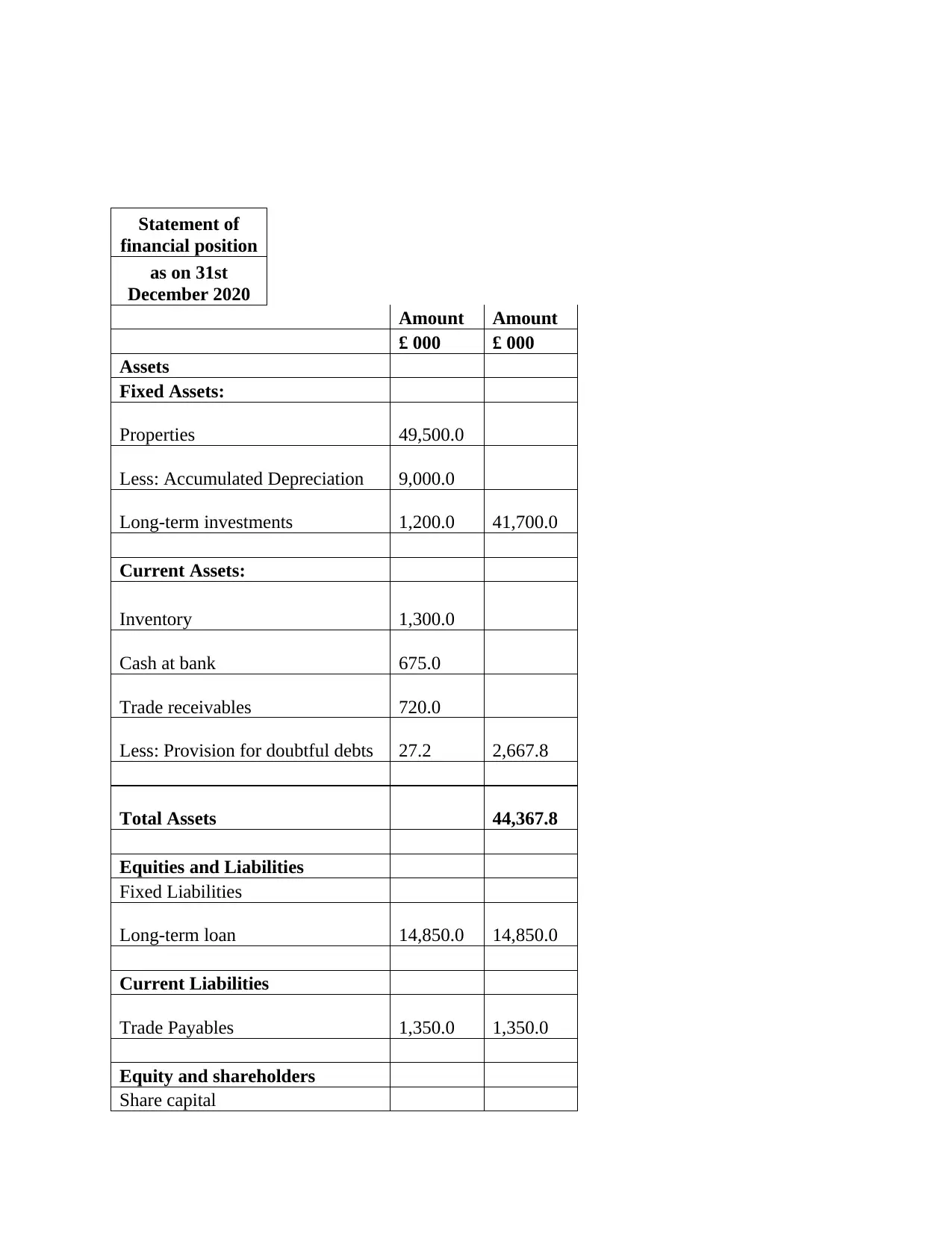

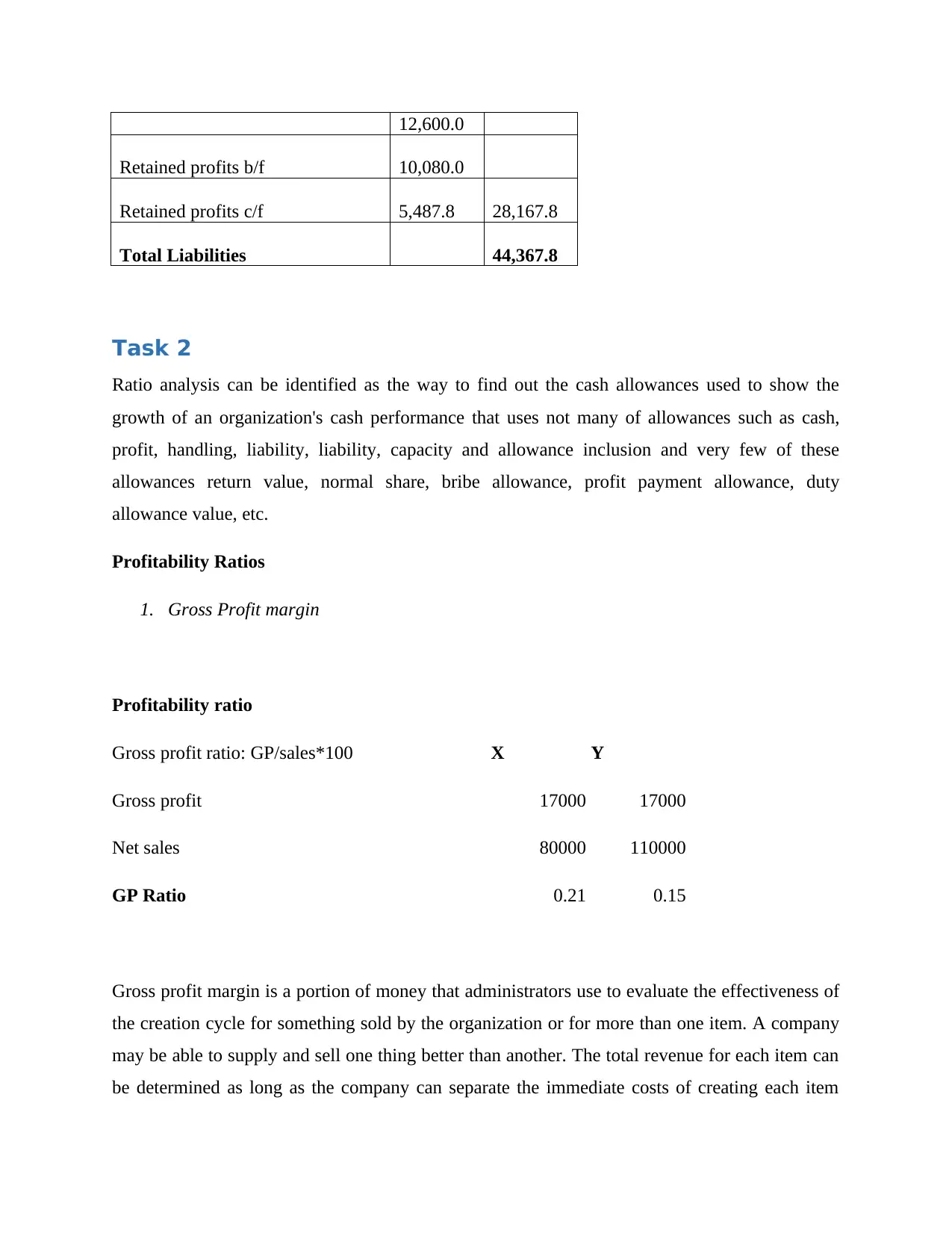

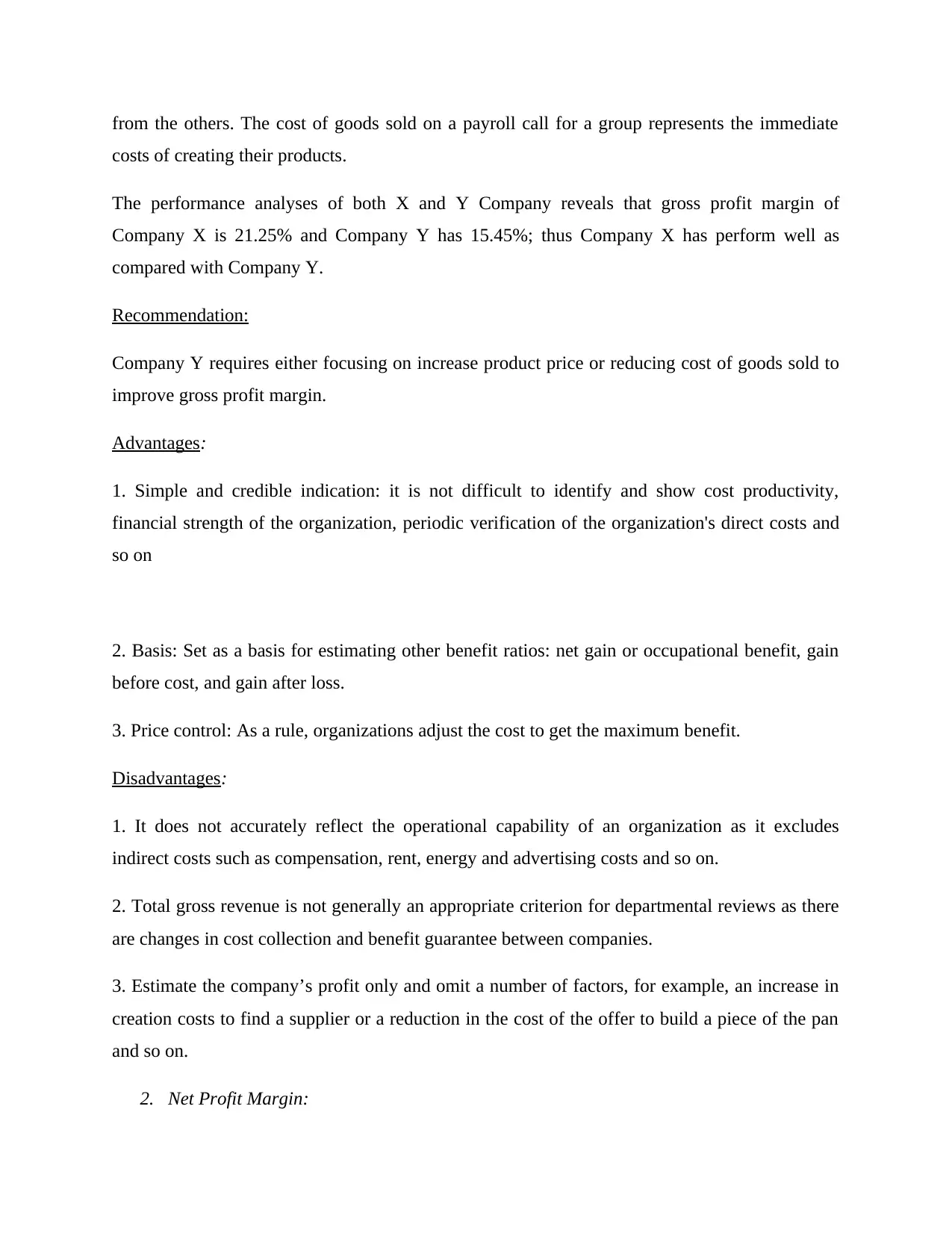

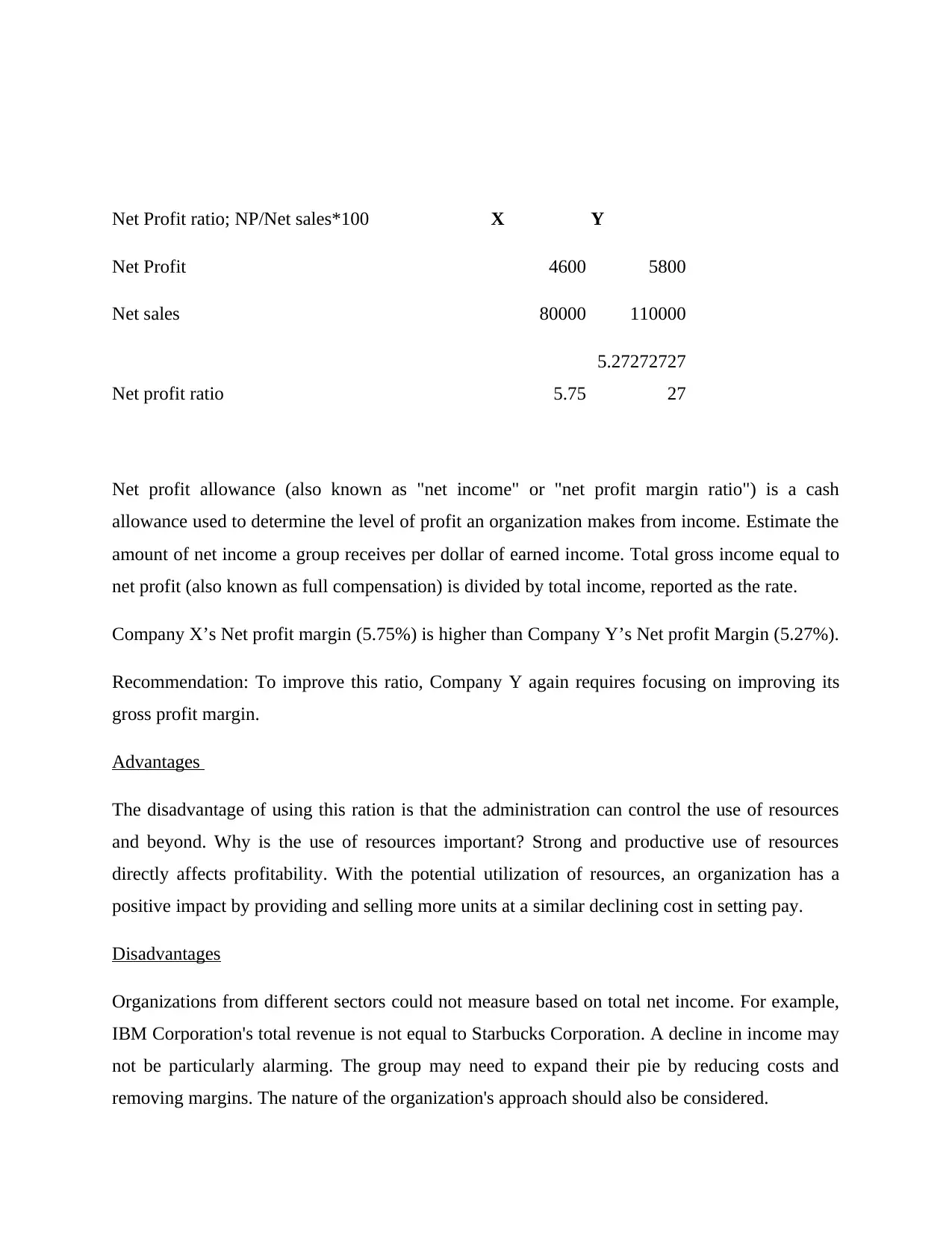

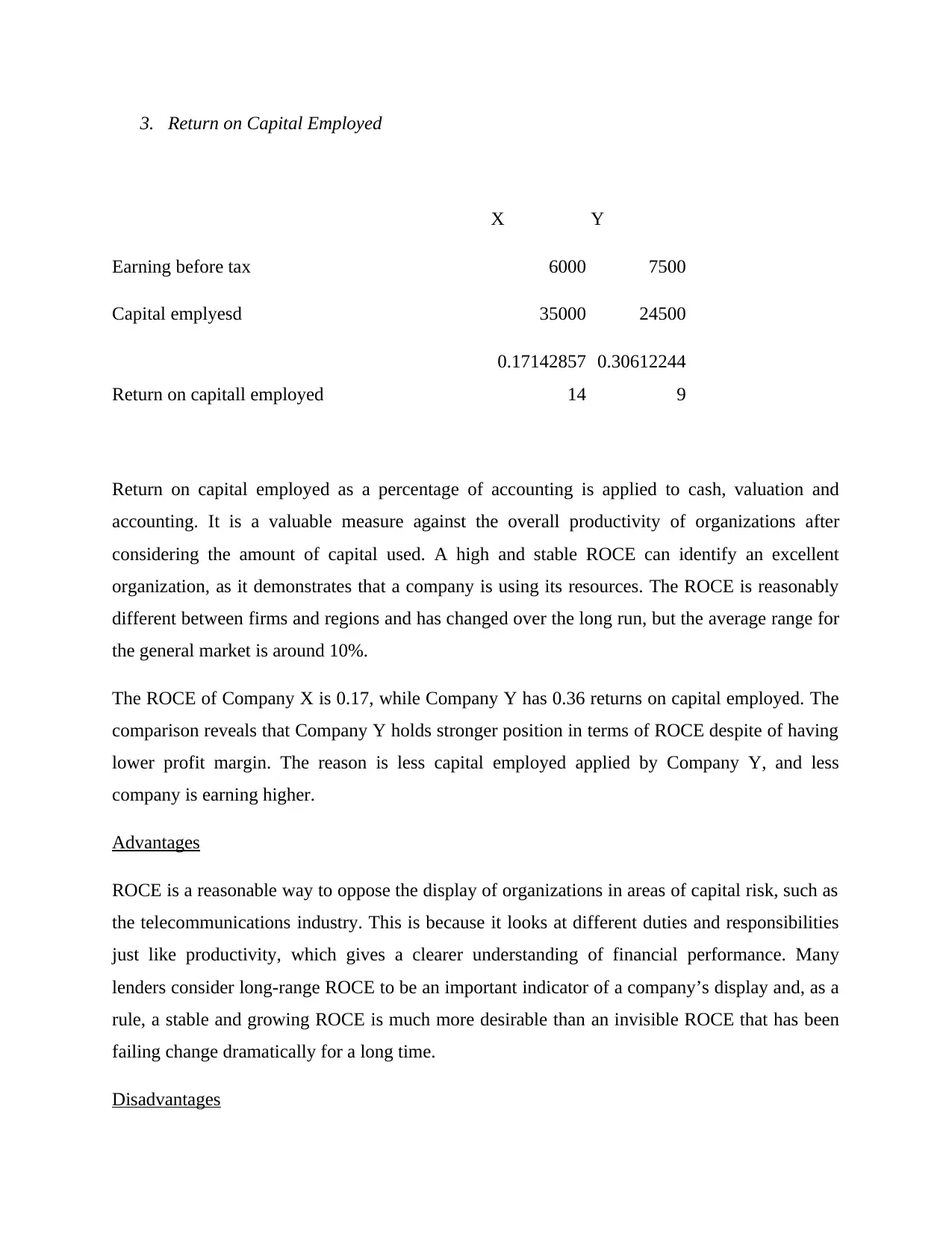

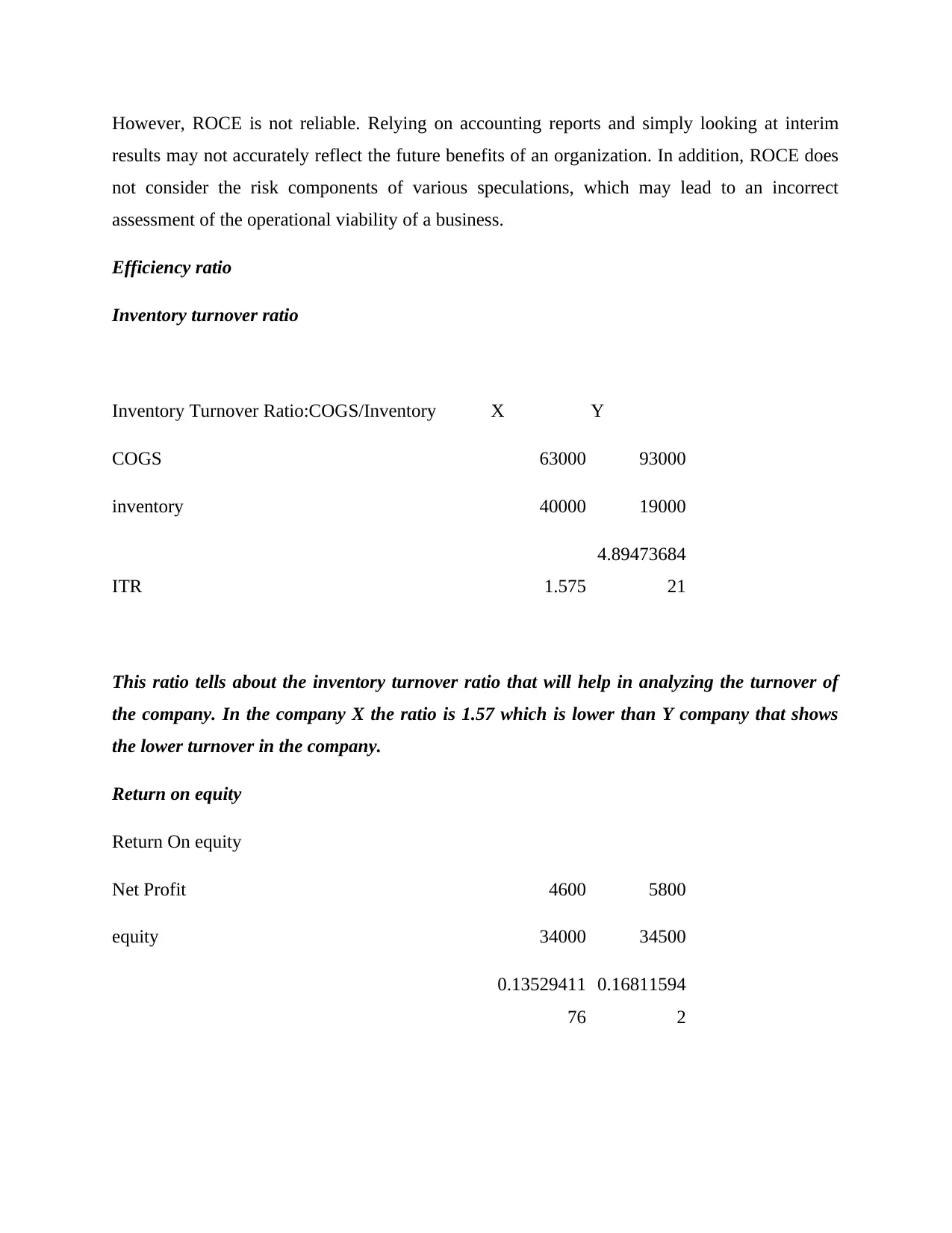

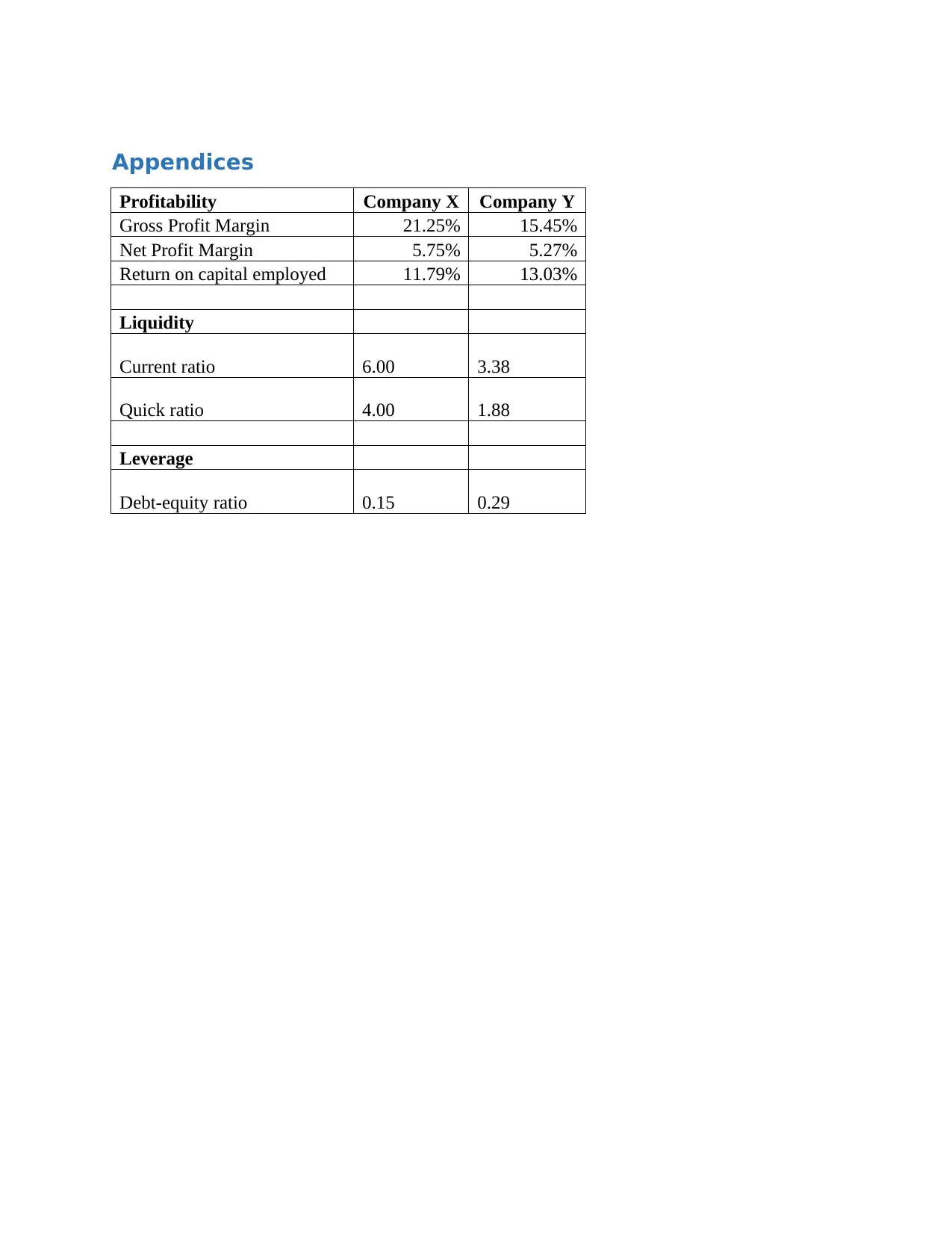

This report provides a comprehensive analysis of financial statements and ratio analysis. It begins with an income statement and a statement of financial position, followed by an in-depth examination of various financial ratios. The report covers profitability ratios such as gross profit margin and net profit margin, efficiency ratios including inventory turnover, and return on capital employed (ROCE). The analysis compares the financial performance of two companies (X and Y), highlighting their strengths and weaknesses based on the calculated ratios. The report also includes recommendations for improvement and discusses the advantages and disadvantages of using different financial ratios. The appendices provide a summary of key ratios for both companies, facilitating a clear comparison of their financial performance.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.