Financial Accounting Report: Performance Analysis and Comparison

VerifiedAdded on 2022/12/29

|15

|2530

|1

Report

AI Summary

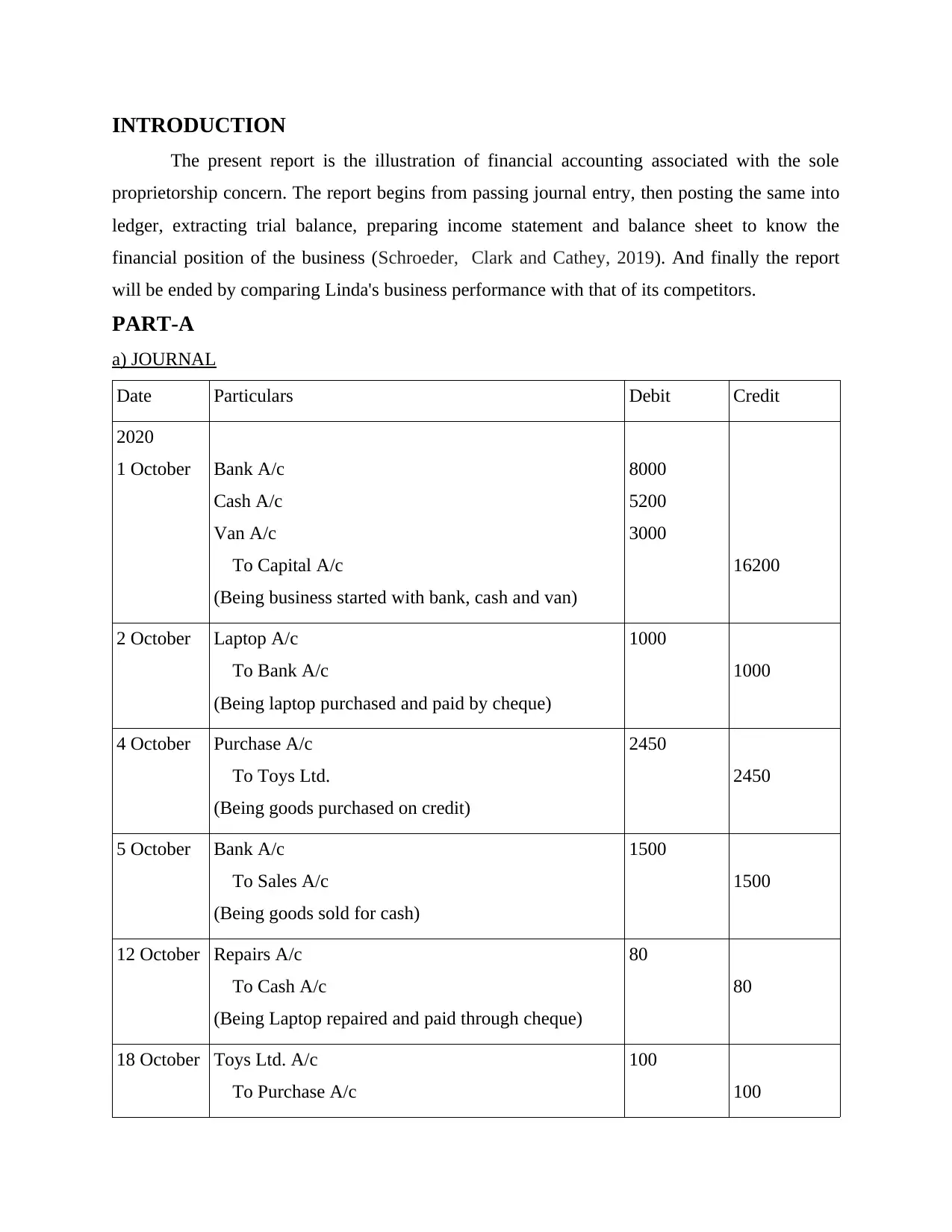

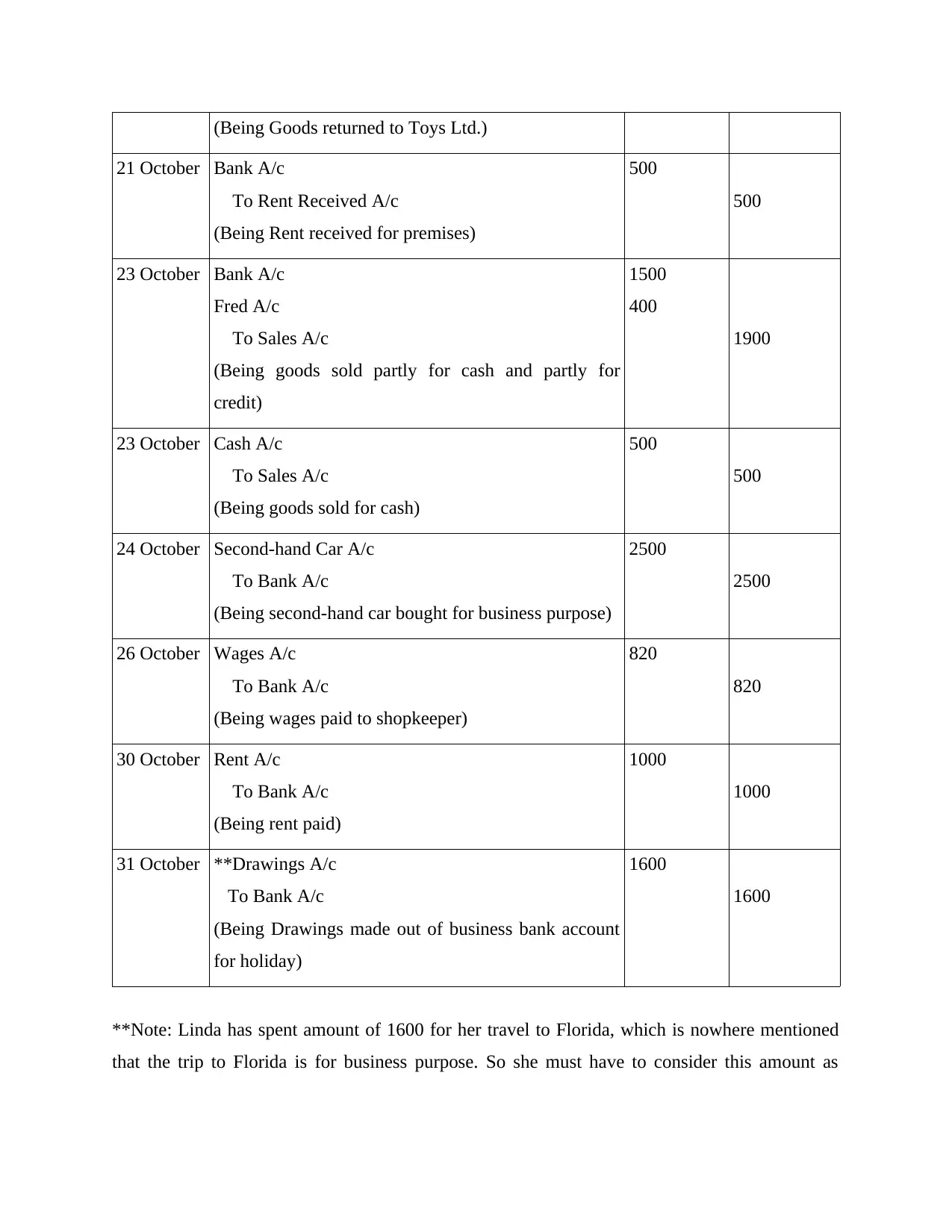

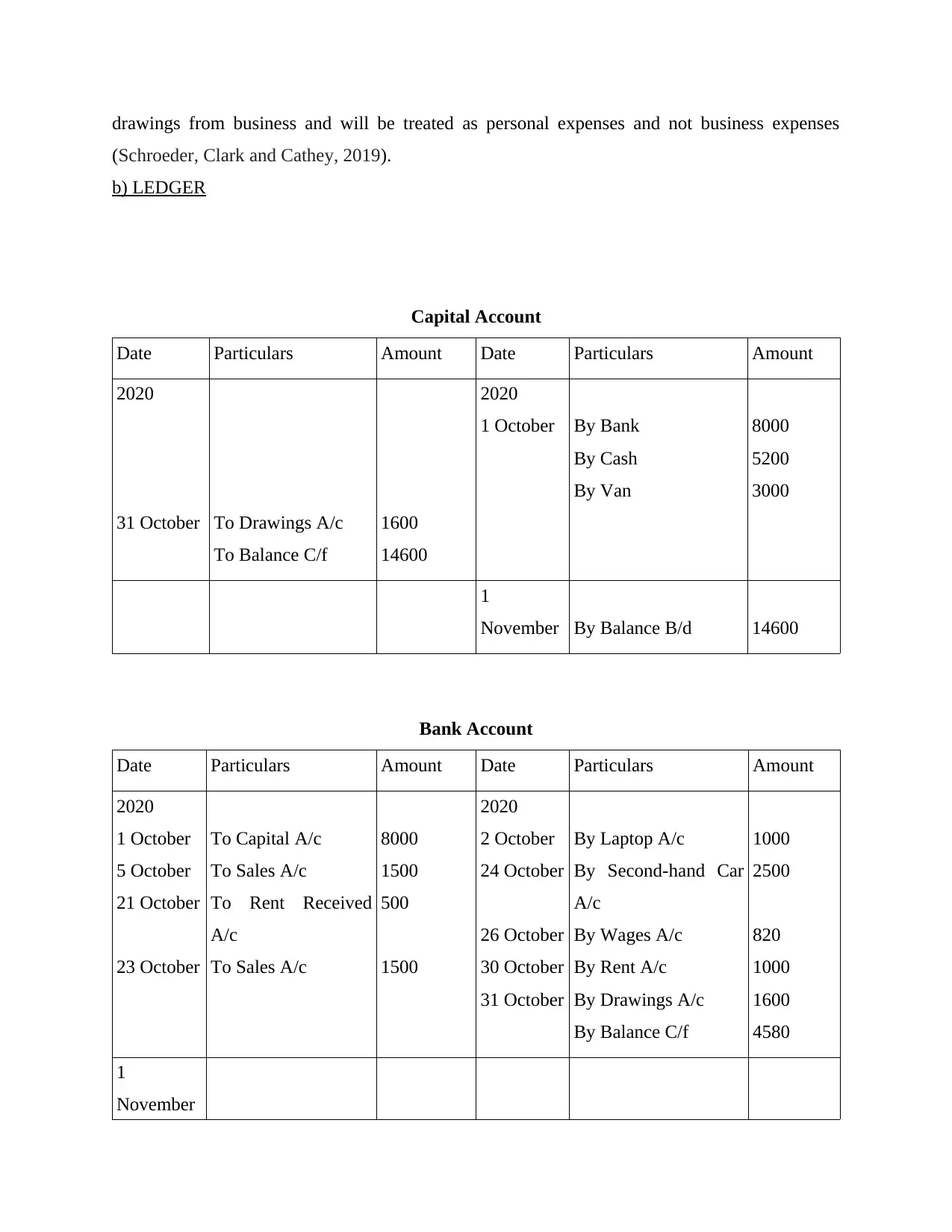

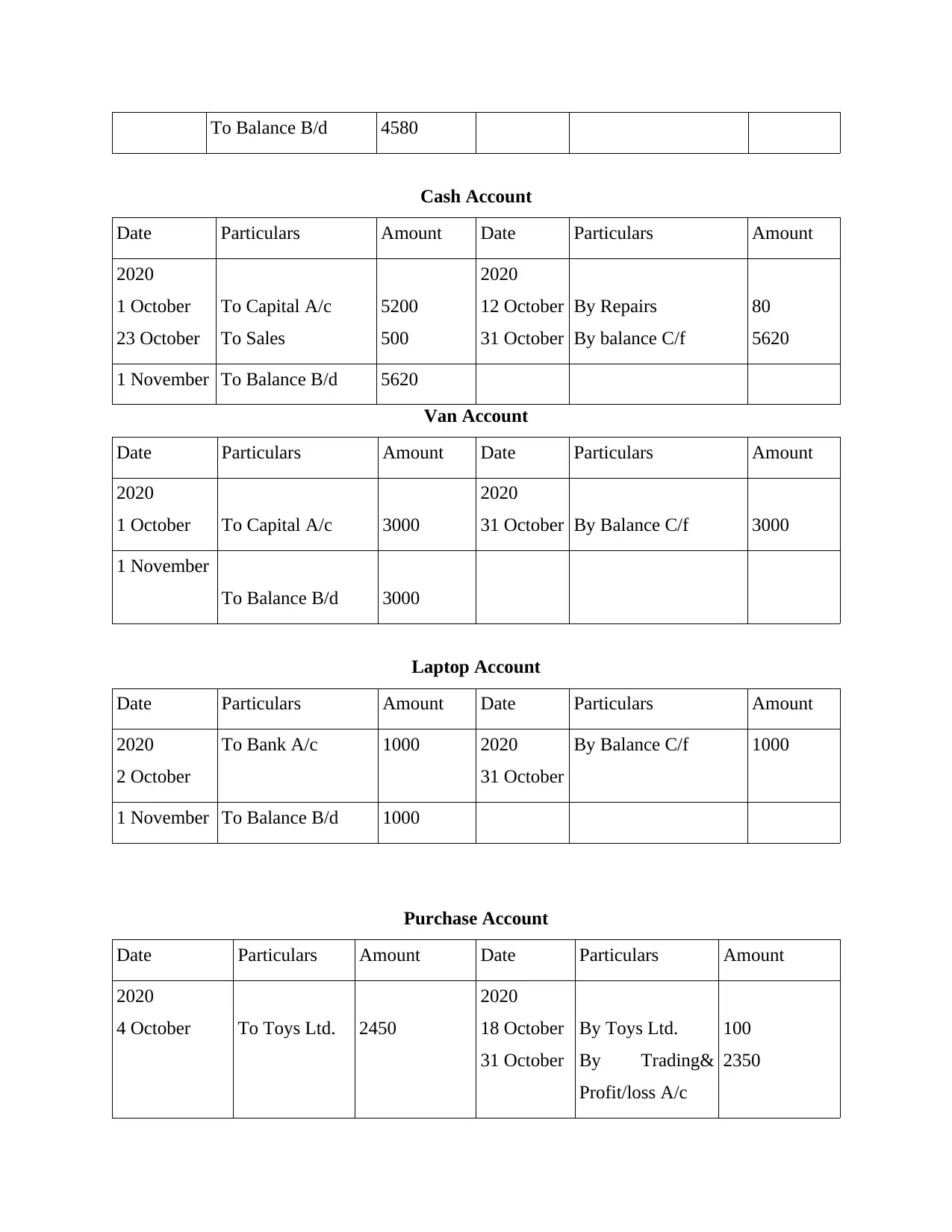

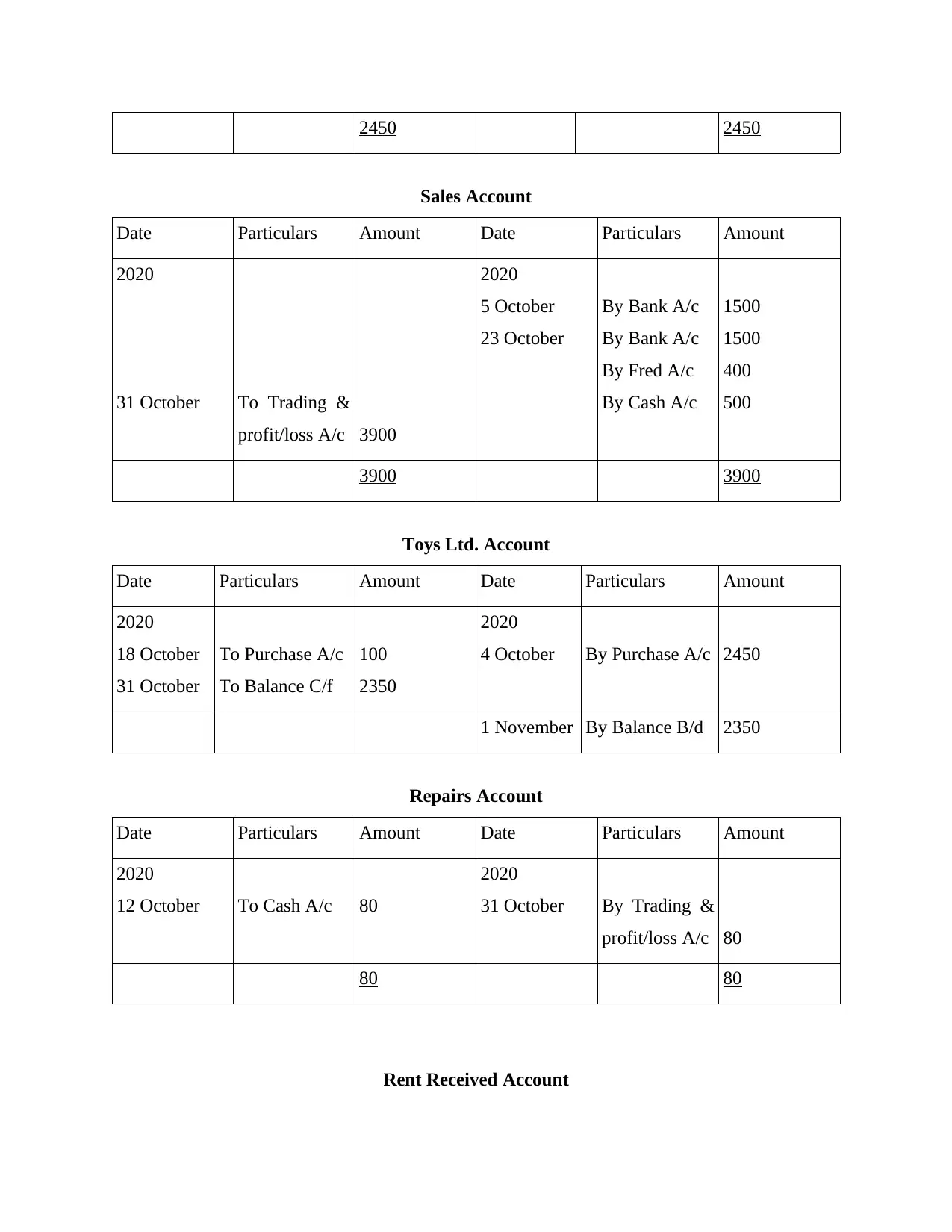

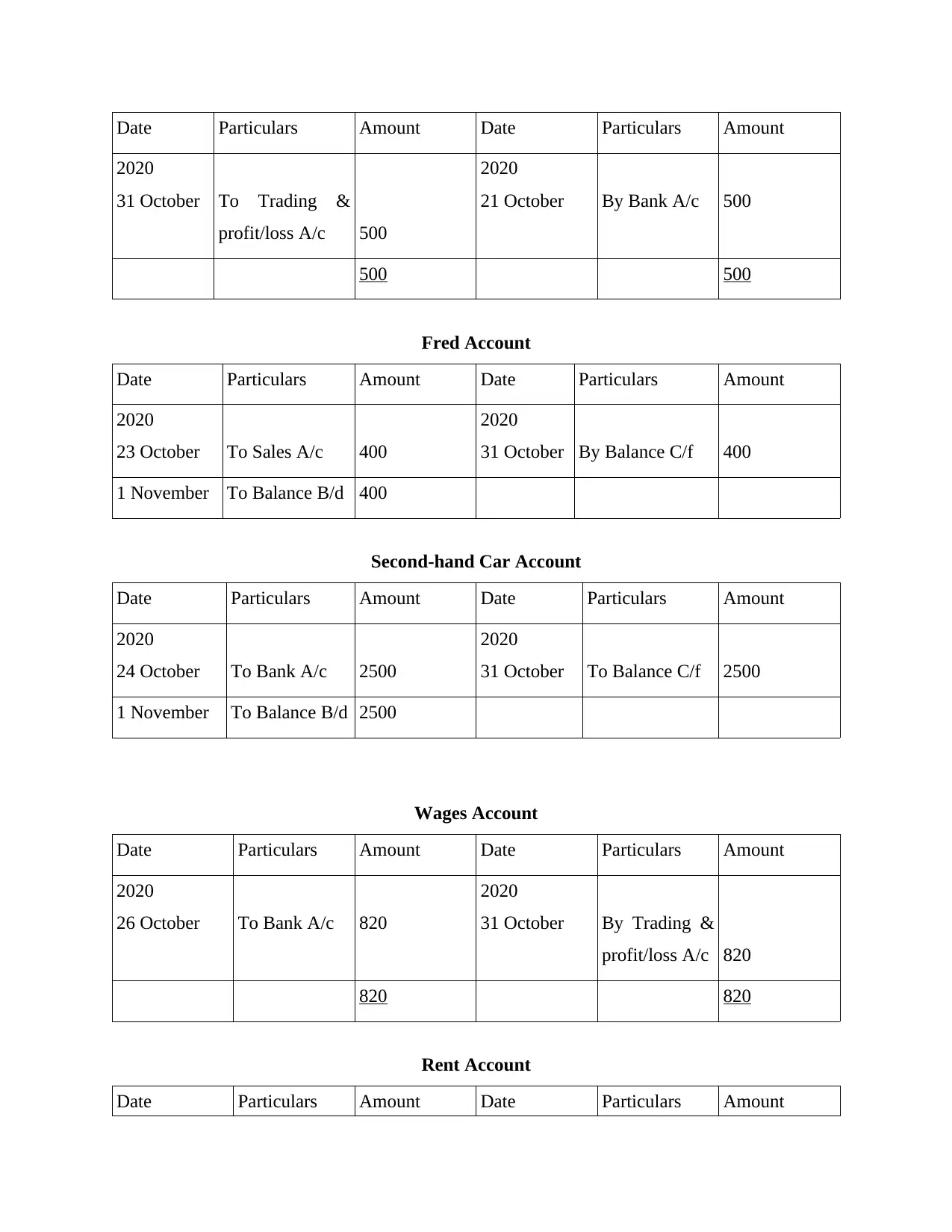

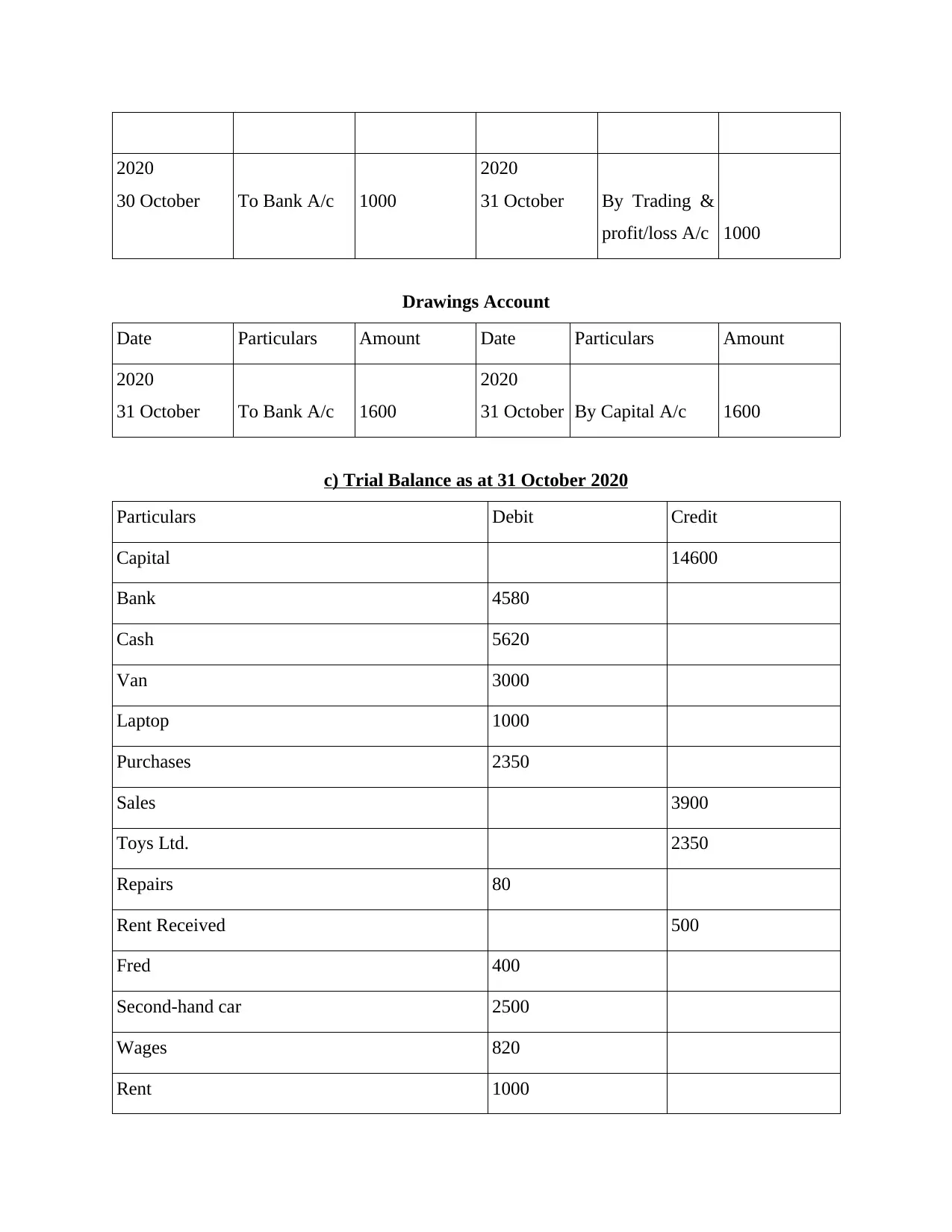

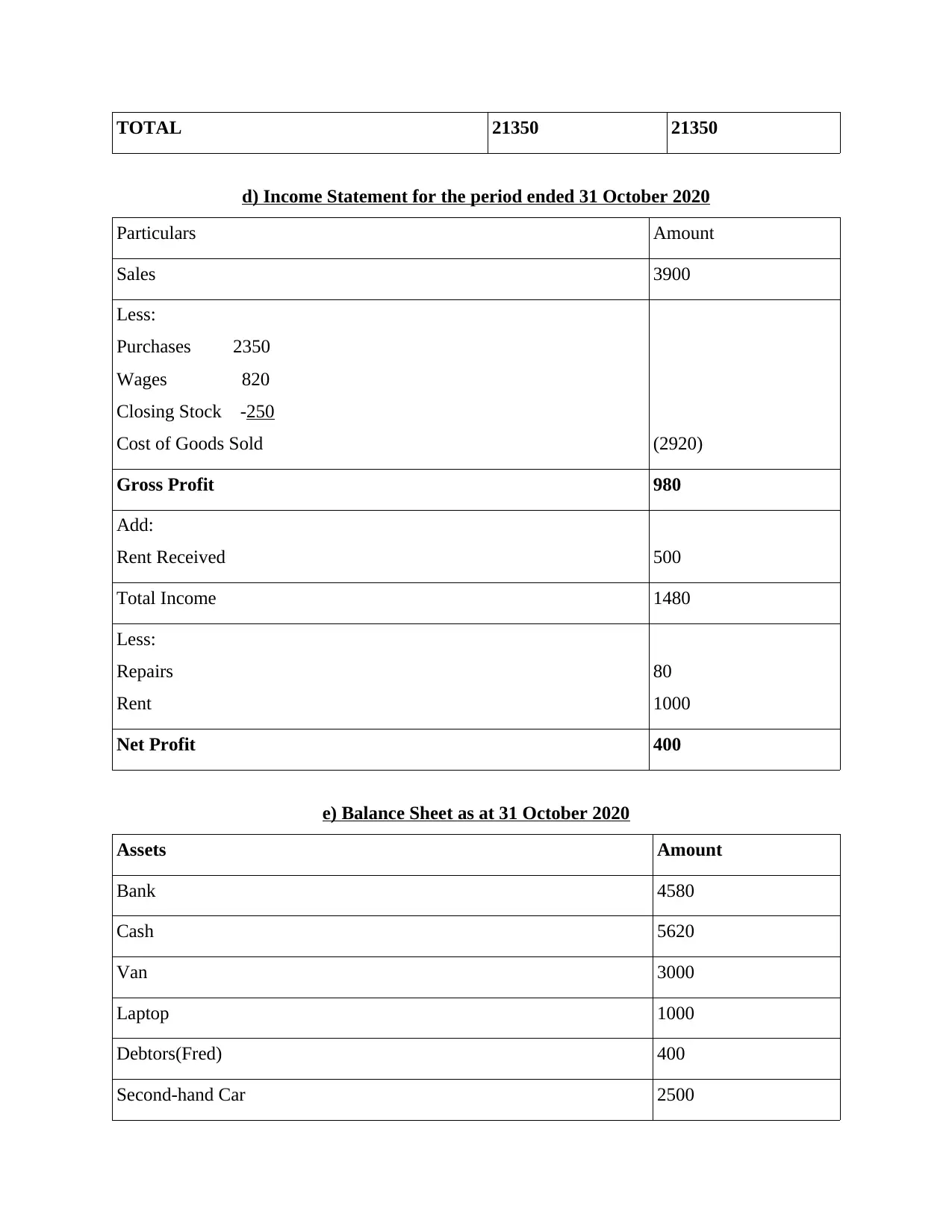

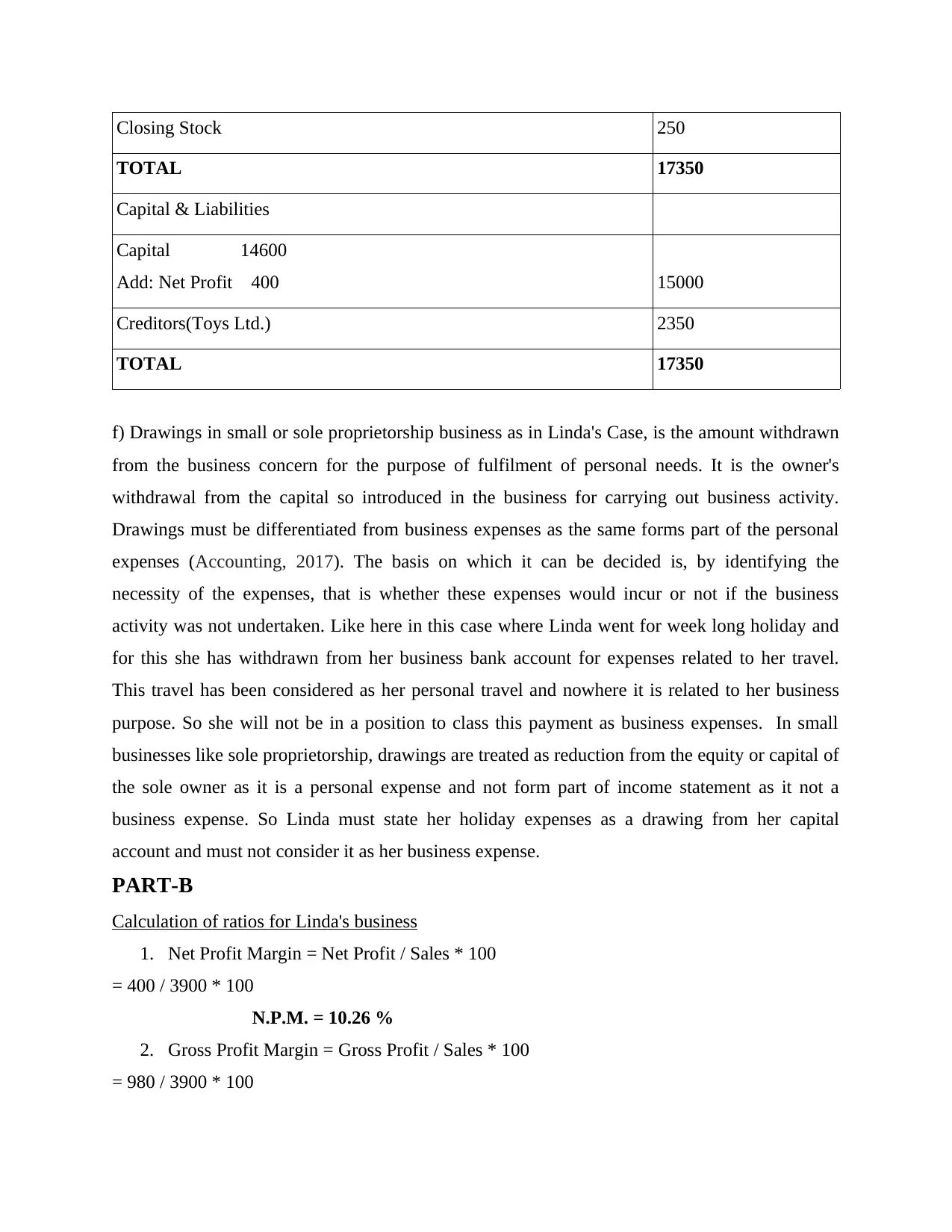

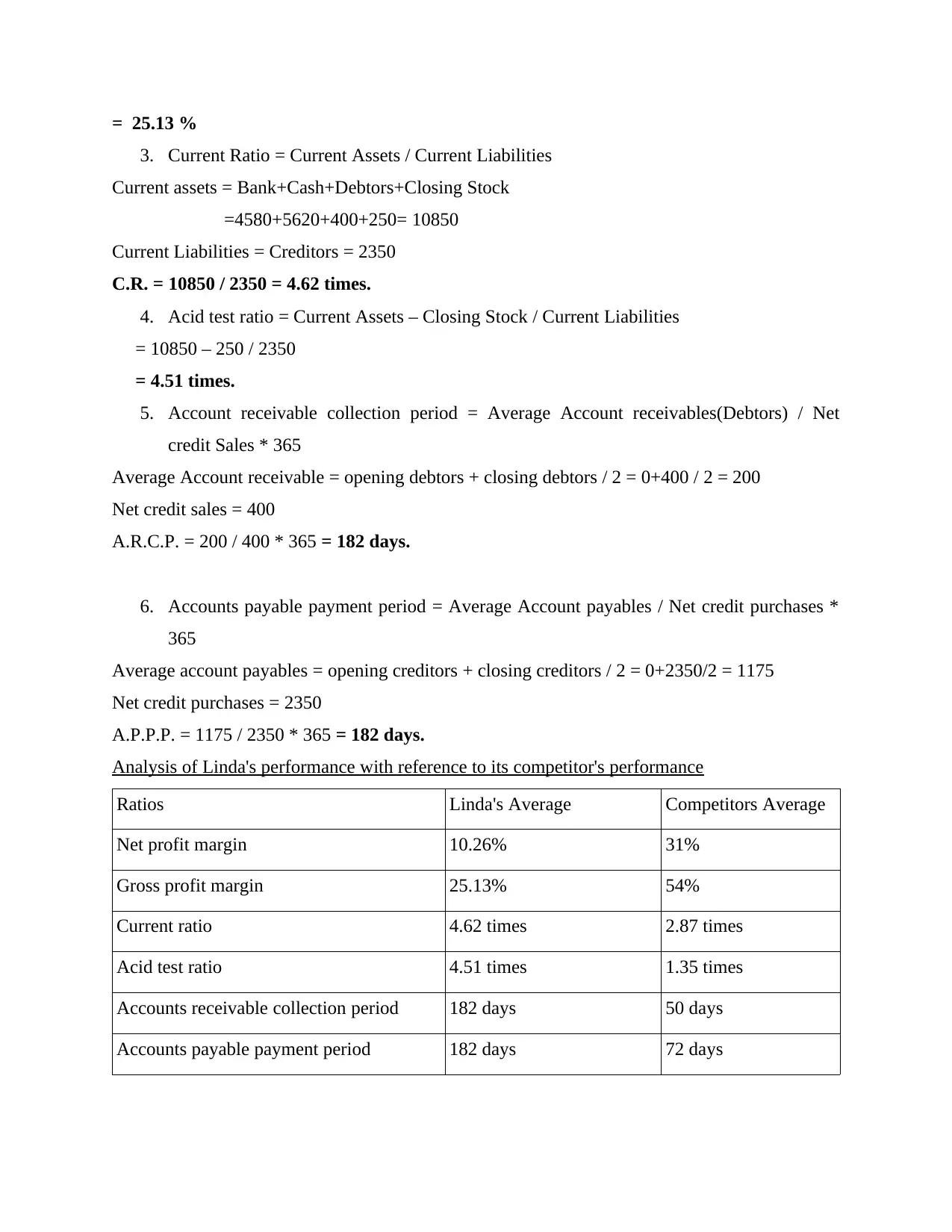

This report presents a comprehensive analysis of financial accounting principles applied to a sole proprietorship, specifically Linda's business. The report begins with the foundational steps of financial accounting, including the creation of journal entries and their subsequent posting to the ledger. It then proceeds to the extraction of a trial balance, followed by the preparation of an income statement and balance sheet to assess the financial position of the business. The report further delves into Part-B, which involves a detailed calculation of various financial ratios, such as net profit margin, gross profit margin, current ratio, and acid test ratio. These ratios are then used to analyze Linda's business performance and compare it with that of its competitors, providing insights into the business's strengths and weaknesses. The report concludes with a summary of findings and references to the sources used.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.