Financial Performance Analysis: Costing, Budgeting, and Variances

VerifiedAdded on 2022/12/28

|10

|2241

|99

Report

AI Summary

This report provides a comprehensive analysis of financial performance, encompassing various costing methods, budgeting techniques, and variance analysis. It begins by calculating costs using absorption costing and then compares it with activity-based costing, highlighting the advantages of the latter. The report then delves into sensitivity analysis to address uncertainties and their impact on financial outcomes. Further, the report calculates and interprets material variances, discussing the problems associated with the current variance reporting system for assessing production manager performance. Finally, it critically evaluates zero-based budgeting and incremental budgeting, comparing their benefits and drawbacks to provide a balanced understanding of these budgeting techniques, supported by relevant references.

Financial performance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENT

Question 1........................................................................................................................................3

A) Calculation of cost ............................................................................................................3

B) Using activity-based costing..............................................................................................4

C) Better technique.................................................................................................................5

D) Sensitivity analysis meeting uncertainties.........................................................................5

Question 2........................................................................................................................................5

A) Calculate of Variances for last month...............................................................................5

Material usage variance.........................................................................................................5

Material mix variance.............................................................................................................6

Total material yield variance .................................................................................................6

B) Various problem with current system of calculating and reporting variances for assessing

the performance of production manager ................................................................................6

Question 3........................................................................................................................................7

Critically evaluation of both Zero based budgeting and incremental budgeting..................7

REFERENCES..............................................................................................................................10

Question 1........................................................................................................................................3

A) Calculation of cost ............................................................................................................3

B) Using activity-based costing..............................................................................................4

C) Better technique.................................................................................................................5

D) Sensitivity analysis meeting uncertainties.........................................................................5

Question 2........................................................................................................................................5

A) Calculate of Variances for last month...............................................................................5

Material usage variance.........................................................................................................5

Material mix variance.............................................................................................................6

Total material yield variance .................................................................................................6

B) Various problem with current system of calculating and reporting variances for assessing

the performance of production manager ................................................................................6

Question 3........................................................................................................................................7

Critically evaluation of both Zero based budgeting and incremental budgeting..................7

REFERENCES..............................................................................................................................10

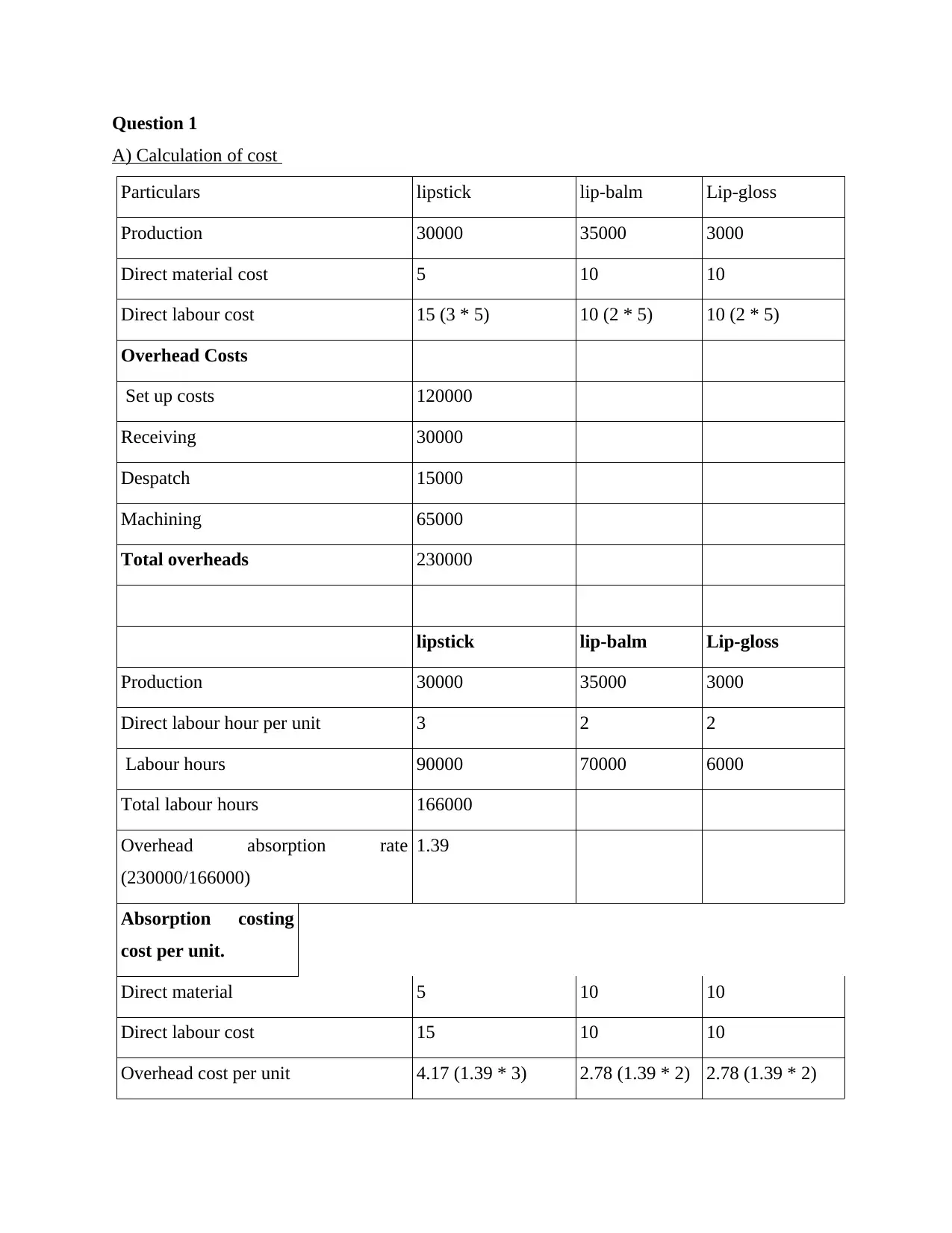

Question 1

A) Calculation of cost

Particulars lipstick lip-balm Lip-gloss

Production 30000 35000 3000

Direct material cost 5 10 10

Direct labour cost 15 (3 * 5) 10 (2 * 5) 10 (2 * 5)

Overhead Costs

Set up costs 120000

Receiving 30000

Despatch 15000

Machining 65000

Total overheads 230000

lipstick lip-balm Lip-gloss

Production 30000 35000 3000

Direct labour hour per unit 3 2 2

Labour hours 90000 70000 6000

Total labour hours 166000

Overhead absorption rate

(230000/166000)

1.39

Absorption costing

cost per unit.

Direct material 5 10 10

Direct labour cost 15 10 10

Overhead cost per unit 4.17 (1.39 * 3) 2.78 (1.39 * 2) 2.78 (1.39 * 2)

A) Calculation of cost

Particulars lipstick lip-balm Lip-gloss

Production 30000 35000 3000

Direct material cost 5 10 10

Direct labour cost 15 (3 * 5) 10 (2 * 5) 10 (2 * 5)

Overhead Costs

Set up costs 120000

Receiving 30000

Despatch 15000

Machining 65000

Total overheads 230000

lipstick lip-balm Lip-gloss

Production 30000 35000 3000

Direct labour hour per unit 3 2 2

Labour hours 90000 70000 6000

Total labour hours 166000

Overhead absorption rate

(230000/166000)

1.39

Absorption costing

cost per unit.

Direct material 5 10 10

Direct labour cost 15 10 10

Overhead cost per unit 4.17 (1.39 * 3) 2.78 (1.39 * 2) 2.78 (1.39 * 2)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total cost per unit 24.17 22.78 22.78

Profit per unit

= Sales price per unit – Cost per unit

Lipstick:

22 – 24.17

= -2.17

Lip balm:

26 – 22.78

= 3.22

Lip gloss:

24 – 22.78

= 1.22

B) Using activity-based costing

Particulars Basis of apportionment lipstick Lip balm Lip gloss

Set up cost No of set up (10 : 14 : 1) 48000 67200 4800

Receiving cost No. of deliveries received

(10 : 10 : 2)

13500 13500 3000

Despatching cost No. of order despatched

(20 : 20 : 10)

6000 6000 3000

Machining cost Machine hours

(4 * 30000 : 4 * 35000 : 4 *

3000)

28600 33150 3250

Total overhead per product 96100 119850 14050

Production units 30000 35000 3000

Profit per unit

= Sales price per unit – Cost per unit

Lipstick:

22 – 24.17

= -2.17

Lip balm:

26 – 22.78

= 3.22

Lip gloss:

24 – 22.78

= 1.22

B) Using activity-based costing

Particulars Basis of apportionment lipstick Lip balm Lip gloss

Set up cost No of set up (10 : 14 : 1) 48000 67200 4800

Receiving cost No. of deliveries received

(10 : 10 : 2)

13500 13500 3000

Despatching cost No. of order despatched

(20 : 20 : 10)

6000 6000 3000

Machining cost Machine hours

(4 * 30000 : 4 * 35000 : 4 *

3000)

28600 33150 3250

Total overhead per product 96100 119850 14050

Production units 30000 35000 3000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

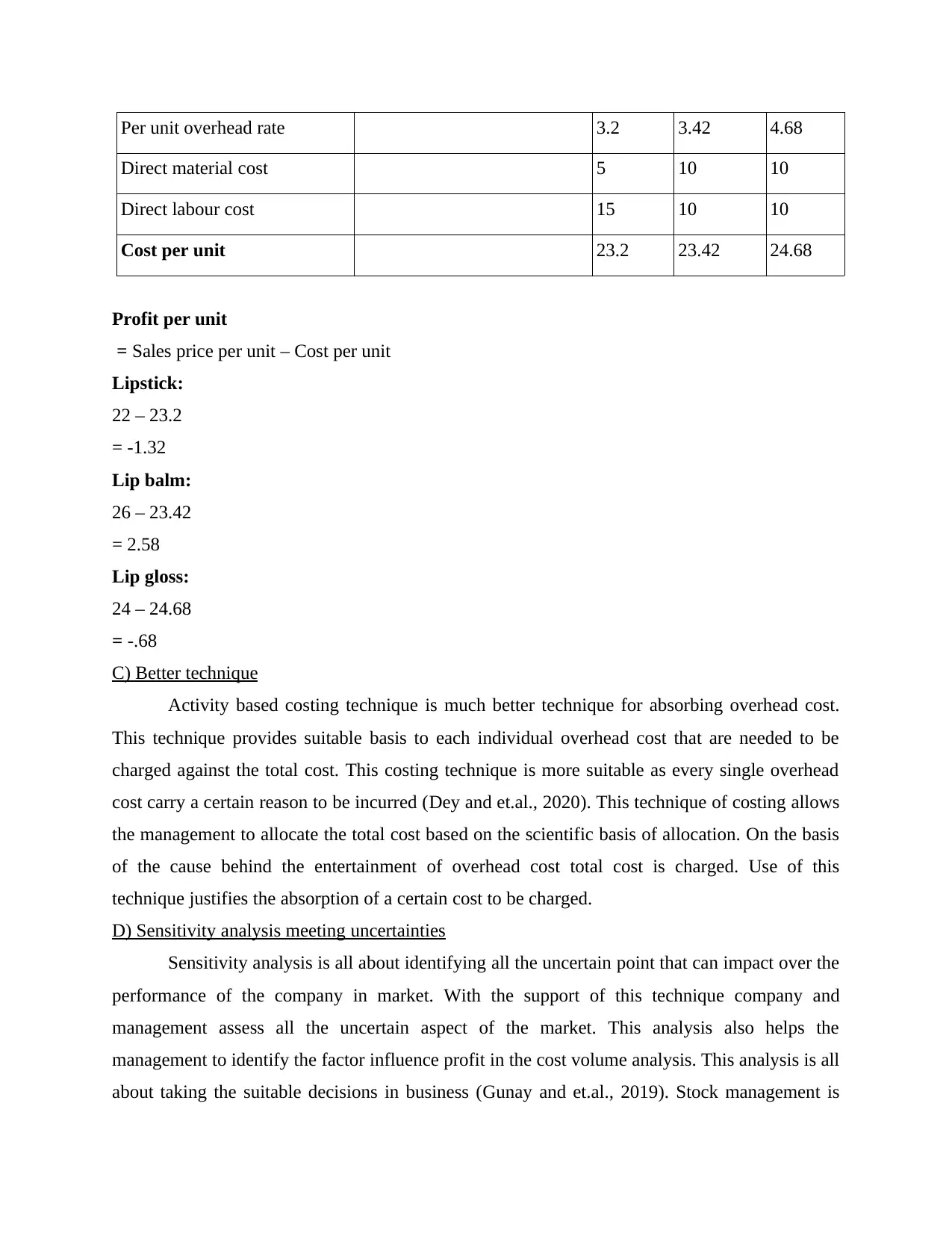

Per unit overhead rate 3.2 3.42 4.68

Direct material cost 5 10 10

Direct labour cost 15 10 10

Cost per unit 23.2 23.42 24.68

Profit per unit

= Sales price per unit – Cost per unit

Lipstick:

22 – 23.2

= -1.32

Lip balm:

26 – 23.42

= 2.58

Lip gloss:

24 – 24.68

= -.68

C) Better technique

Activity based costing technique is much better technique for absorbing overhead cost.

This technique provides suitable basis to each individual overhead cost that are needed to be

charged against the total cost. This costing technique is more suitable as every single overhead

cost carry a certain reason to be incurred (Dey and et.al., 2020). This technique of costing allows

the management to allocate the total cost based on the scientific basis of allocation. On the basis

of the cause behind the entertainment of overhead cost total cost is charged. Use of this

technique justifies the absorption of a certain cost to be charged.

D) Sensitivity analysis meeting uncertainties

Sensitivity analysis is all about identifying all the uncertain point that can impact over the

performance of the company in market. With the support of this technique company and

management assess all the uncertain aspect of the market. This analysis also helps the

management to identify the factor influence profit in the cost volume analysis. This analysis is all

about taking the suitable decisions in business (Gunay and et.al., 2019). Stock management is

Direct material cost 5 10 10

Direct labour cost 15 10 10

Cost per unit 23.2 23.42 24.68

Profit per unit

= Sales price per unit – Cost per unit

Lipstick:

22 – 23.2

= -1.32

Lip balm:

26 – 23.42

= 2.58

Lip gloss:

24 – 24.68

= -.68

C) Better technique

Activity based costing technique is much better technique for absorbing overhead cost.

This technique provides suitable basis to each individual overhead cost that are needed to be

charged against the total cost. This costing technique is more suitable as every single overhead

cost carry a certain reason to be incurred (Dey and et.al., 2020). This technique of costing allows

the management to allocate the total cost based on the scientific basis of allocation. On the basis

of the cause behind the entertainment of overhead cost total cost is charged. Use of this

technique justifies the absorption of a certain cost to be charged.

D) Sensitivity analysis meeting uncertainties

Sensitivity analysis is all about identifying all the uncertain point that can impact over the

performance of the company in market. With the support of this technique company and

management assess all the uncertain aspect of the market. This analysis also helps the

management to identify the factor influence profit in the cost volume analysis. This analysis is all

about taking the suitable decisions in business (Gunay and et.al., 2019). Stock management is

always a critical topic and this favor the management to make suitable decision to take the best

level of decision. This analysis helps the organization to know about all different uncertainties in

the market. There are many direct and indirect factor affect the cost volume of business entity.

This entire analysis guide company to know all the indirect element influence overall profit

volume of the product to be delivered in front of potential customers in market.

Question 2

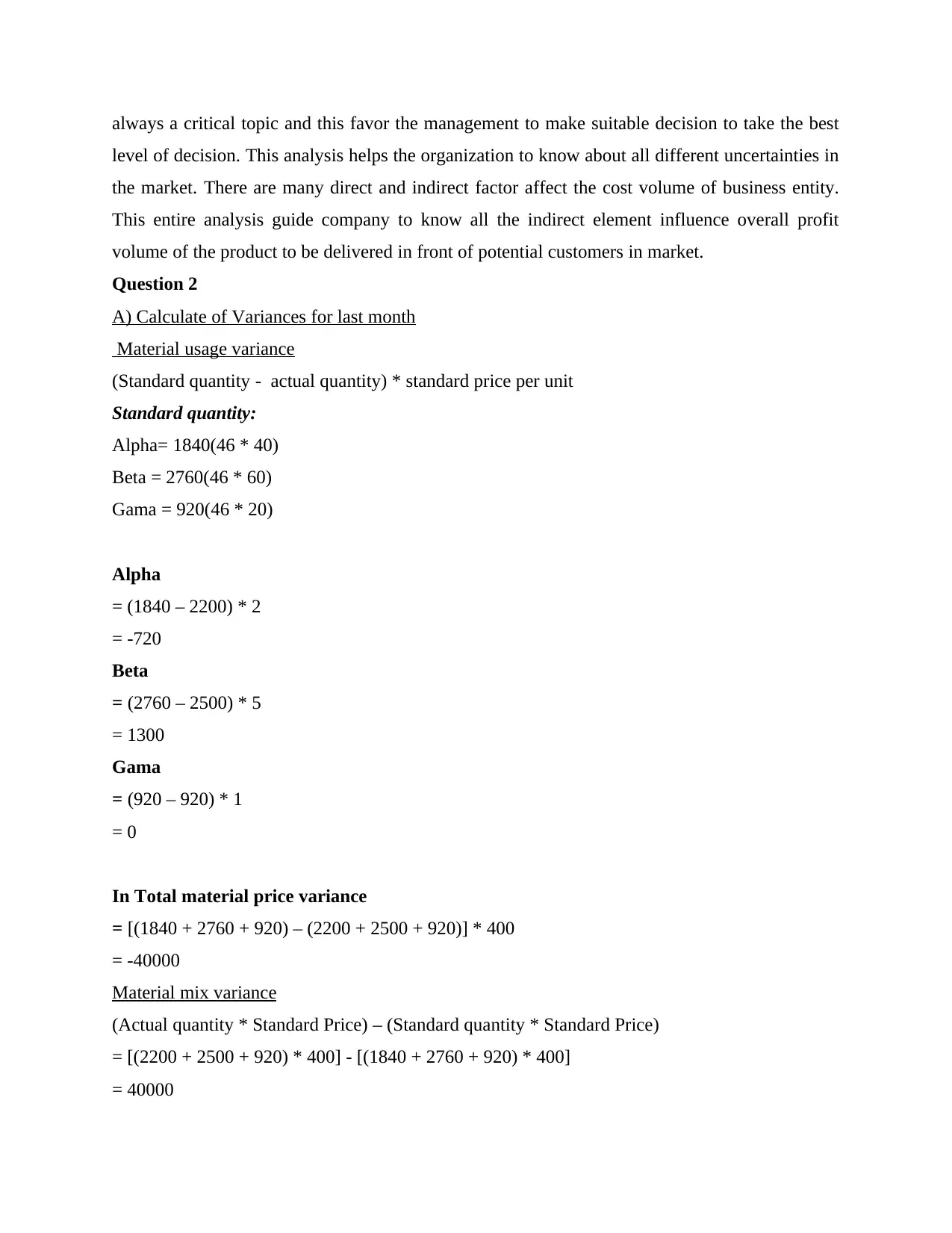

A) Calculate of Variances for last month

Material usage variance

(Standard quantity - actual quantity) * standard price per unit

Standard quantity:

Alpha= 1840(46 * 40)

Beta = 2760(46 * 60)

Gama = 920(46 * 20)

Alpha

= (1840 – 2200) * 2

= -720

Beta

= (2760 – 2500) * 5

= 1300

Gama

= (920 – 920) * 1

= 0

In Total material price variance

= [(1840 + 2760 + 920) – (2200 + 2500 + 920)] * 400

= -40000

Material mix variance

(Actual quantity * Standard Price) – (Standard quantity * Standard Price)

= [(2200 + 2500 + 920) * 400] - [(1840 + 2760 + 920) * 400]

= 40000

level of decision. This analysis helps the organization to know about all different uncertainties in

the market. There are many direct and indirect factor affect the cost volume of business entity.

This entire analysis guide company to know all the indirect element influence overall profit

volume of the product to be delivered in front of potential customers in market.

Question 2

A) Calculate of Variances for last month

Material usage variance

(Standard quantity - actual quantity) * standard price per unit

Standard quantity:

Alpha= 1840(46 * 40)

Beta = 2760(46 * 60)

Gama = 920(46 * 20)

Alpha

= (1840 – 2200) * 2

= -720

Beta

= (2760 – 2500) * 5

= 1300

Gama

= (920 – 920) * 1

= 0

In Total material price variance

= [(1840 + 2760 + 920) – (2200 + 2500 + 920)] * 400

= -40000

Material mix variance

(Actual quantity * Standard Price) – (Standard quantity * Standard Price)

= [(2200 + 2500 + 920) * 400] - [(1840 + 2760 + 920) * 400]

= 40000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

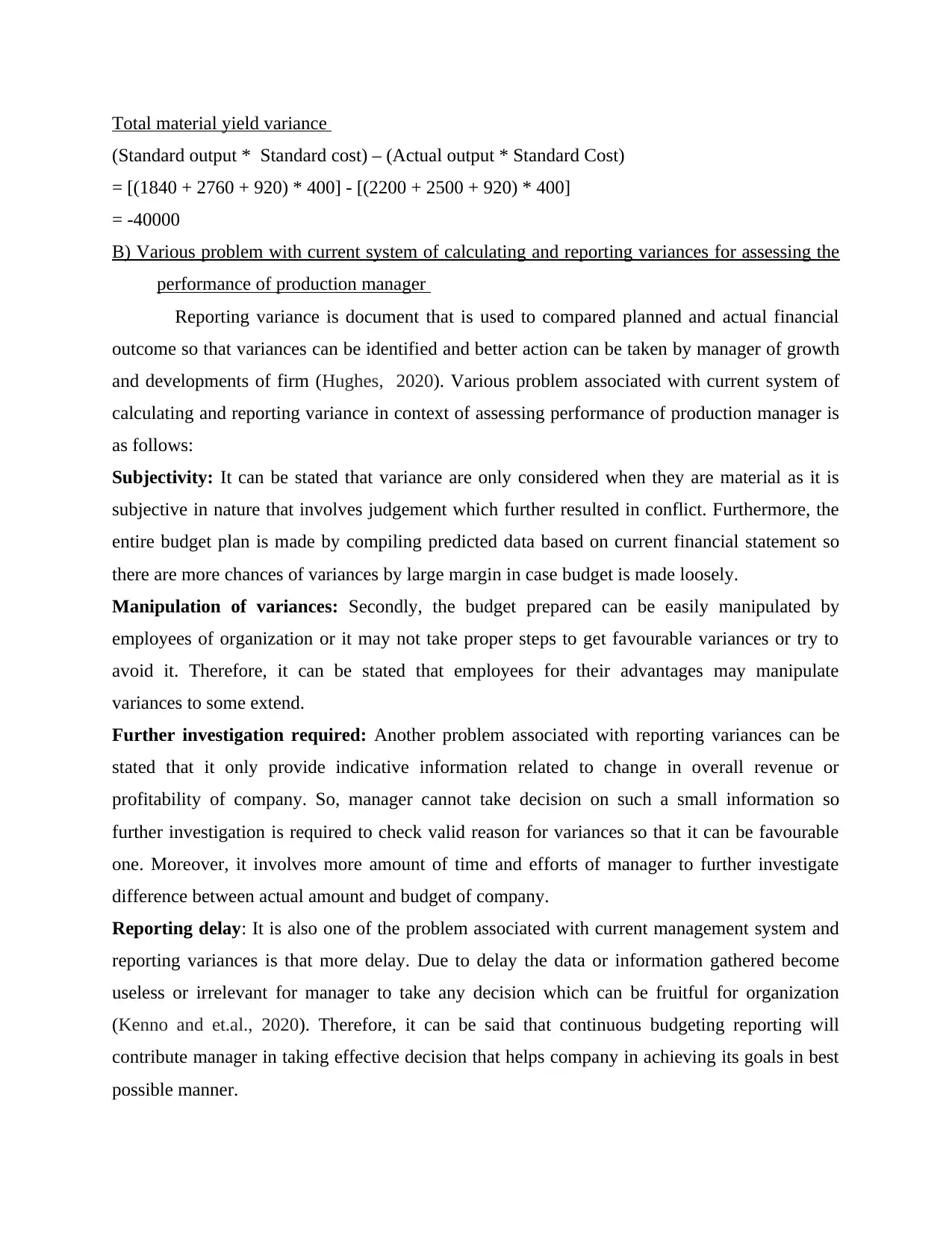

Total material yield variance

(Standard output * Standard cost) – (Actual output * Standard Cost)

= [(1840 + 2760 + 920) * 400] - [(2200 + 2500 + 920) * 400]

= -40000

B) Various problem with current system of calculating and reporting variances for assessing the

performance of production manager

Reporting variance is document that is used to compared planned and actual financial

outcome so that variances can be identified and better action can be taken by manager of growth

and developments of firm (Hughes, 2020). Various problem associated with current system of

calculating and reporting variance in context of assessing performance of production manager is

as follows:

Subjectivity: It can be stated that variance are only considered when they are material as it is

subjective in nature that involves judgement which further resulted in conflict. Furthermore, the

entire budget plan is made by compiling predicted data based on current financial statement so

there are more chances of variances by large margin in case budget is made loosely.

Manipulation of variances: Secondly, the budget prepared can be easily manipulated by

employees of organization or it may not take proper steps to get favourable variances or try to

avoid it. Therefore, it can be stated that employees for their advantages may manipulate

variances to some extend.

Further investigation required: Another problem associated with reporting variances can be

stated that it only provide indicative information related to change in overall revenue or

profitability of company. So, manager cannot take decision on such a small information so

further investigation is required to check valid reason for variances so that it can be favourable

one. Moreover, it involves more amount of time and efforts of manager to further investigate

difference between actual amount and budget of company.

Reporting delay: It is also one of the problem associated with current management system and

reporting variances is that more delay. Due to delay the data or information gathered become

useless or irrelevant for manager to take any decision which can be fruitful for organization

(Kenno and et.al., 2020). Therefore, it can be said that continuous budgeting reporting will

contribute manager in taking effective decision that helps company in achieving its goals in best

possible manner.

(Standard output * Standard cost) – (Actual output * Standard Cost)

= [(1840 + 2760 + 920) * 400] - [(2200 + 2500 + 920) * 400]

= -40000

B) Various problem with current system of calculating and reporting variances for assessing the

performance of production manager

Reporting variance is document that is used to compared planned and actual financial

outcome so that variances can be identified and better action can be taken by manager of growth

and developments of firm (Hughes, 2020). Various problem associated with current system of

calculating and reporting variance in context of assessing performance of production manager is

as follows:

Subjectivity: It can be stated that variance are only considered when they are material as it is

subjective in nature that involves judgement which further resulted in conflict. Furthermore, the

entire budget plan is made by compiling predicted data based on current financial statement so

there are more chances of variances by large margin in case budget is made loosely.

Manipulation of variances: Secondly, the budget prepared can be easily manipulated by

employees of organization or it may not take proper steps to get favourable variances or try to

avoid it. Therefore, it can be stated that employees for their advantages may manipulate

variances to some extend.

Further investigation required: Another problem associated with reporting variances can be

stated that it only provide indicative information related to change in overall revenue or

profitability of company. So, manager cannot take decision on such a small information so

further investigation is required to check valid reason for variances so that it can be favourable

one. Moreover, it involves more amount of time and efforts of manager to further investigate

difference between actual amount and budget of company.

Reporting delay: It is also one of the problem associated with current management system and

reporting variances is that more delay. Due to delay the data or information gathered become

useless or irrelevant for manager to take any decision which can be fruitful for organization

(Kenno and et.al., 2020). Therefore, it can be said that continuous budgeting reporting will

contribute manager in taking effective decision that helps company in achieving its goals in best

possible manner.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Technological industry: Moreover, it can be stated that reporting variances is not suitable for

dynamic industry like technology. Likewise in case production process of organization require

continuous revision so that company can easily adapt to external changes in order to grow and

sustain for longer time frame. Thus, company must have more amount of finance or capital as it

will needs more resources and time.

Question 3

Critically evaluation of both Zero based budgeting and incremental budgeting

Zero based budgeting and incremental budgeting are two different budget techniques that

are completely different form each other. Budgeting is an important process of management

control system that helps in effectively planning, coordination and control of organization

function so that maximum benefits can be enjoyed (Kenno and et.al., 2020). There are two

common method that are used for preparation of budget that is zero based and incremental

approach and thereby degree of success varies. The Optimum solution for perfect planning lies

between them both which can be illustrated as follows:

Incremental budgeting: It is one of the traditional budgeting method in which actual

performance or current period budget is taken as a base and incremental amount is added to new

budget. There are various adjustment that are added to the amount like as increase in overall cost,

sales price or inflation within country. So, it can be illustrated that starting point of the budget is

current year budget or actual performance. There are various benefits and drawbacks of

incremental budgeting that can be explained as follows:

The biggest benefits of using incremental budgeting is that its is highly easy and quick

way to prepare budget as it can be allocated to various member or staff. Moreover, it

leads to saving in cost as less time needs to be invested for its preparation.

Furthermore, due to consistent approached used by firm it contributes in reducing

conflict between department managers thus helps in gaining maximum outcome.

On contrasty note there are some of the drawbacks of making use of incremental

budgeting which can be interpreted as follows:

First and foremost drawback of making use of incremental budgeting is that it assume

that all cost and current activities still needed thereby they are not much examined in

detailed. At the same time it looks backward rather than forwards that create problem

for business as there are several changes in external environment.

dynamic industry like technology. Likewise in case production process of organization require

continuous revision so that company can easily adapt to external changes in order to grow and

sustain for longer time frame. Thus, company must have more amount of finance or capital as it

will needs more resources and time.

Question 3

Critically evaluation of both Zero based budgeting and incremental budgeting

Zero based budgeting and incremental budgeting are two different budget techniques that

are completely different form each other. Budgeting is an important process of management

control system that helps in effectively planning, coordination and control of organization

function so that maximum benefits can be enjoyed (Kenno and et.al., 2020). There are two

common method that are used for preparation of budget that is zero based and incremental

approach and thereby degree of success varies. The Optimum solution for perfect planning lies

between them both which can be illustrated as follows:

Incremental budgeting: It is one of the traditional budgeting method in which actual

performance or current period budget is taken as a base and incremental amount is added to new

budget. There are various adjustment that are added to the amount like as increase in overall cost,

sales price or inflation within country. So, it can be illustrated that starting point of the budget is

current year budget or actual performance. There are various benefits and drawbacks of

incremental budgeting that can be explained as follows:

The biggest benefits of using incremental budgeting is that its is highly easy and quick

way to prepare budget as it can be allocated to various member or staff. Moreover, it

leads to saving in cost as less time needs to be invested for its preparation.

Furthermore, due to consistent approached used by firm it contributes in reducing

conflict between department managers thus helps in gaining maximum outcome.

On contrasty note there are some of the drawbacks of making use of incremental

budgeting which can be interpreted as follows:

First and foremost drawback of making use of incremental budgeting is that it assume

that all cost and current activities still needed thereby they are not much examined in

detailed. At the same time it looks backward rather than forwards that create problem

for business as there are several changes in external environment.

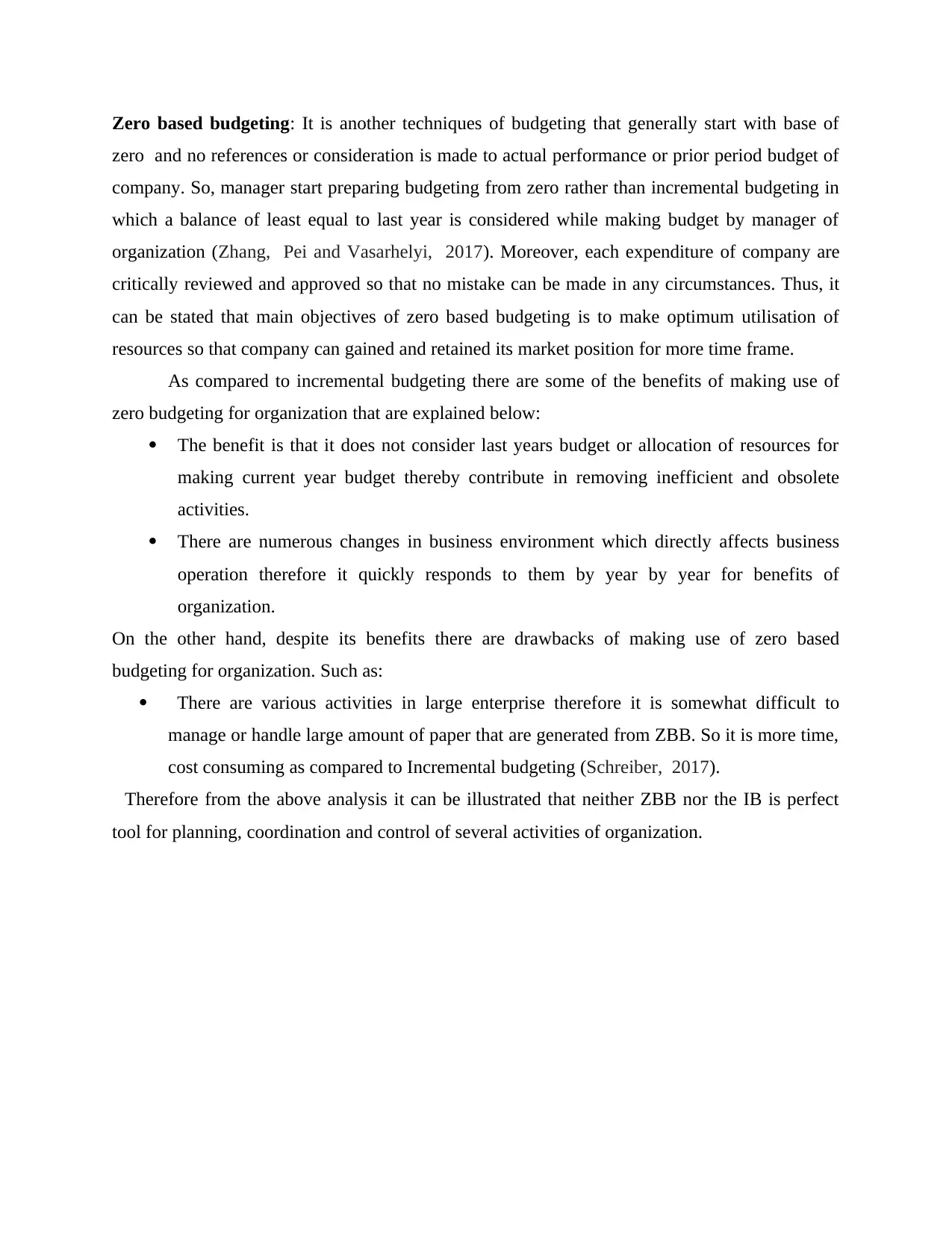

Zero based budgeting: It is another techniques of budgeting that generally start with base of

zero and no references or consideration is made to actual performance or prior period budget of

company. So, manager start preparing budgeting from zero rather than incremental budgeting in

which a balance of least equal to last year is considered while making budget by manager of

organization (Zhang, Pei and Vasarhelyi, 2017). Moreover, each expenditure of company are

critically reviewed and approved so that no mistake can be made in any circumstances. Thus, it

can be stated that main objectives of zero based budgeting is to make optimum utilisation of

resources so that company can gained and retained its market position for more time frame.

As compared to incremental budgeting there are some of the benefits of making use of

zero budgeting for organization that are explained below:

The benefit is that it does not consider last years budget or allocation of resources for

making current year budget thereby contribute in removing inefficient and obsolete

activities.

There are numerous changes in business environment which directly affects business

operation therefore it quickly responds to them by year by year for benefits of

organization.

On the other hand, despite its benefits there are drawbacks of making use of zero based

budgeting for organization. Such as:

There are various activities in large enterprise therefore it is somewhat difficult to

manage or handle large amount of paper that are generated from ZBB. So it is more time,

cost consuming as compared to Incremental budgeting (Schreiber, 2017).

Therefore from the above analysis it can be illustrated that neither ZBB nor the IB is perfect

tool for planning, coordination and control of several activities of organization.

zero and no references or consideration is made to actual performance or prior period budget of

company. So, manager start preparing budgeting from zero rather than incremental budgeting in

which a balance of least equal to last year is considered while making budget by manager of

organization (Zhang, Pei and Vasarhelyi, 2017). Moreover, each expenditure of company are

critically reviewed and approved so that no mistake can be made in any circumstances. Thus, it

can be stated that main objectives of zero based budgeting is to make optimum utilisation of

resources so that company can gained and retained its market position for more time frame.

As compared to incremental budgeting there are some of the benefits of making use of

zero budgeting for organization that are explained below:

The benefit is that it does not consider last years budget or allocation of resources for

making current year budget thereby contribute in removing inefficient and obsolete

activities.

There are numerous changes in business environment which directly affects business

operation therefore it quickly responds to them by year by year for benefits of

organization.

On the other hand, despite its benefits there are drawbacks of making use of zero based

budgeting for organization. Such as:

There are various activities in large enterprise therefore it is somewhat difficult to

manage or handle large amount of paper that are generated from ZBB. So it is more time,

cost consuming as compared to Incremental budgeting (Schreiber, 2017).

Therefore from the above analysis it can be illustrated that neither ZBB nor the IB is perfect

tool for planning, coordination and control of several activities of organization.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Dey, T. D. and et.al., 2020. Persuasive Metamorphosis of Manufacturing Overhead at The

Golden Doors of Disparaging Uttermost Cost of Goods. The International Journal of

Technology Information and Computer (TIJOTIC). 1(1). pp.8-15.

Gunay, H. B. and et.al., 2019. Sensitivity analysis and optimization of building

operations. Energy and Buildings. 199. pp.164-175.

Hughes, P., 2020. Discover the power of zero-based budgeting. Farmer’s Weekly, 2020(20032),

pp.30-30.

Kenno, S and et.al., 2020. Budgeting, strategic planning and institutional diversity in higher

education. Studies in Higher Education, pp.1-15.

Pavlik, A., 2020. Familiarize yourself with budgeting best practices to boost your department's

success. Student Affairs Today, 22(12). pp.6-7.

Schreiber, J. B., 2017. Latent class analysis: an example for reporting results. Research in Social

and Administrative Pharmacy, 13(6). pp.1196-1201

Zhang, L., Pei, D. and Vasarhelyi, M. A., 2017. Toward a new business reporting

model. Journal of Emerging Technologies in Accounting, 14(2). pp.1-15.

Books and Journals

Dey, T. D. and et.al., 2020. Persuasive Metamorphosis of Manufacturing Overhead at The

Golden Doors of Disparaging Uttermost Cost of Goods. The International Journal of

Technology Information and Computer (TIJOTIC). 1(1). pp.8-15.

Gunay, H. B. and et.al., 2019. Sensitivity analysis and optimization of building

operations. Energy and Buildings. 199. pp.164-175.

Hughes, P., 2020. Discover the power of zero-based budgeting. Farmer’s Weekly, 2020(20032),

pp.30-30.

Kenno, S and et.al., 2020. Budgeting, strategic planning and institutional diversity in higher

education. Studies in Higher Education, pp.1-15.

Pavlik, A., 2020. Familiarize yourself with budgeting best practices to boost your department's

success. Student Affairs Today, 22(12). pp.6-7.

Schreiber, J. B., 2017. Latent class analysis: an example for reporting results. Research in Social

and Administrative Pharmacy, 13(6). pp.1196-1201

Zhang, L., Pei, D. and Vasarhelyi, M. A., 2017. Toward a new business reporting

model. Journal of Emerging Technologies in Accounting, 14(2). pp.1-15.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.