Financial Performance Management: Tesco and Marks & Spencer Analysis

VerifiedAdded on 2022/12/16

|16

|4265

|3

Report

AI Summary

This report provides a comprehensive analysis of the financial performance of Tesco and Marks & Spencer. It begins with an introduction to financial performance management and then delves into a detailed ratio analysis of the two companies, comparing their liquidity, profitability, efficiency, and investment ratios for the years 2018 and 2019. The report critically evaluates the Kaplan and Norton's Balance Scorecard, discussing its perspectives and critical success factors within the context of the two companies. Furthermore, the report assesses the benefits and challenges of integrated reporting for the selected organizations, concluding with an overall evaluation of the companies' effectiveness. The report utilizes financial data to illustrate key points and provides insightful commentary on the financial health and strategic management of Tesco and Marks & Spencer.

Financial performance

management

management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

MAIN BODY...................................................................................................................................3

Financial performance using the ratio analysis of two companies.............................................3

Critically determine the Balance scorecard.................................................................................8

Evaluating the benefits and challenges of the Integrated reporting..........................................10

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION ..........................................................................................................................3

MAIN BODY...................................................................................................................................3

Financial performance using the ratio analysis of two companies.............................................3

Critically determine the Balance scorecard.................................................................................8

Evaluating the benefits and challenges of the Integrated reporting..........................................10

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

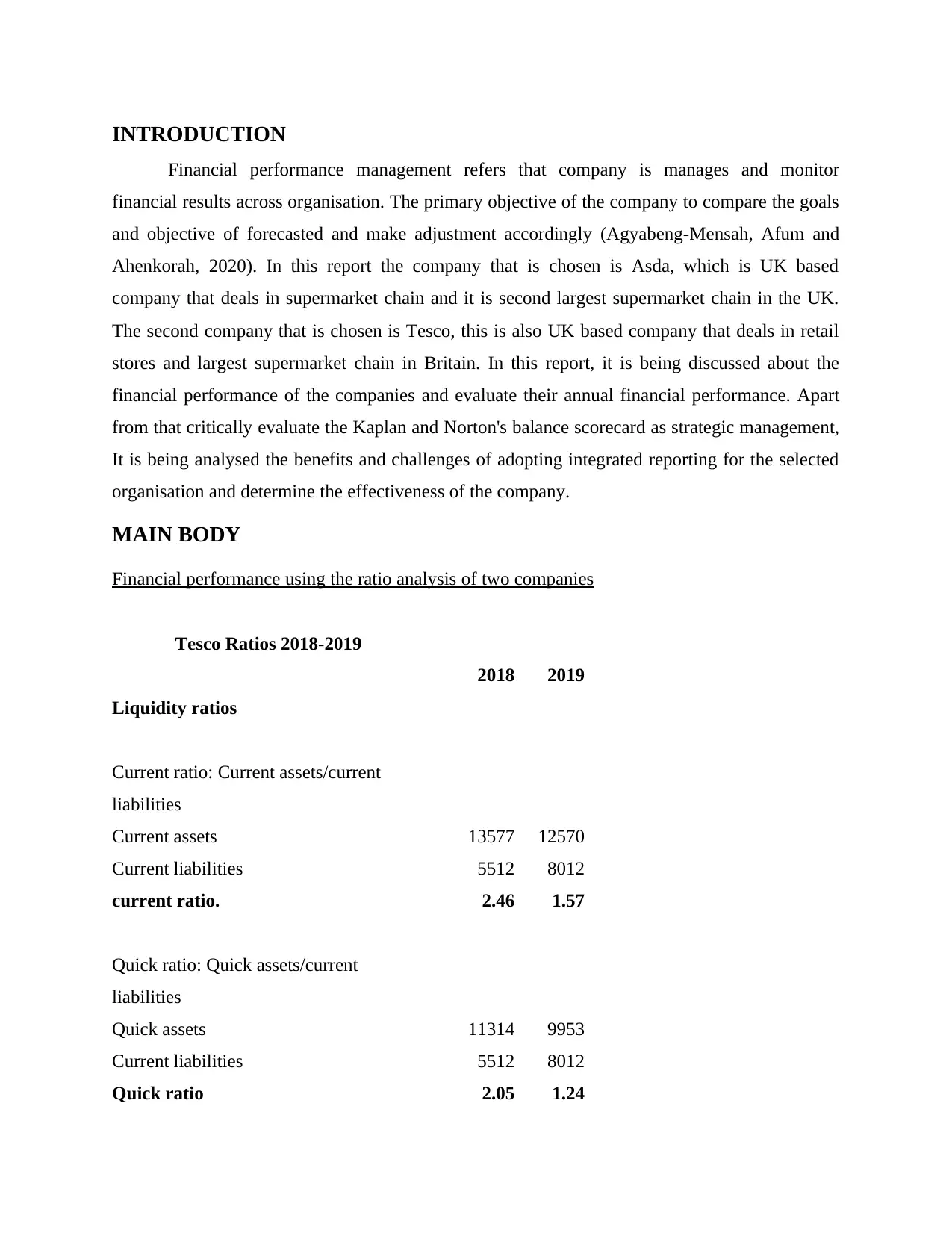

INTRODUCTION

Financial performance management refers that company is manages and monitor

financial results across organisation. The primary objective of the company to compare the goals

and objective of forecasted and make adjustment accordingly (Agyabeng-Mensah, Afum and

Ahenkorah, 2020). In this report the company that is chosen is Asda, which is UK based

company that deals in supermarket chain and it is second largest supermarket chain in the UK.

The second company that is chosen is Tesco, this is also UK based company that deals in retail

stores and largest supermarket chain in Britain. In this report, it is being discussed about the

financial performance of the companies and evaluate their annual financial performance. Apart

from that critically evaluate the Kaplan and Norton's balance scorecard as strategic management,

It is being analysed the benefits and challenges of adopting integrated reporting for the selected

organisation and determine the effectiveness of the company.

MAIN BODY

Financial performance using the ratio analysis of two companies

Tesco Ratios 2018-2019

2018 2019

Liquidity ratios

Current ratio: Current assets/current

liabilities

Current assets 13577 12570

Current liabilities 5512 8012

current ratio. 2.46 1.57

Quick ratio: Quick assets/current

liabilities

Quick assets 11314 9953

Current liabilities 5512 8012

Quick ratio 2.05 1.24

Financial performance management refers that company is manages and monitor

financial results across organisation. The primary objective of the company to compare the goals

and objective of forecasted and make adjustment accordingly (Agyabeng-Mensah, Afum and

Ahenkorah, 2020). In this report the company that is chosen is Asda, which is UK based

company that deals in supermarket chain and it is second largest supermarket chain in the UK.

The second company that is chosen is Tesco, this is also UK based company that deals in retail

stores and largest supermarket chain in Britain. In this report, it is being discussed about the

financial performance of the companies and evaluate their annual financial performance. Apart

from that critically evaluate the Kaplan and Norton's balance scorecard as strategic management,

It is being analysed the benefits and challenges of adopting integrated reporting for the selected

organisation and determine the effectiveness of the company.

MAIN BODY

Financial performance using the ratio analysis of two companies

Tesco Ratios 2018-2019

2018 2019

Liquidity ratios

Current ratio: Current assets/current

liabilities

Current assets 13577 12570

Current liabilities 5512 8012

current ratio. 2.46 1.57

Quick ratio: Quick assets/current

liabilities

Quick assets 11314 9953

Current liabilities 5512 8012

Quick ratio 2.05 1.24

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

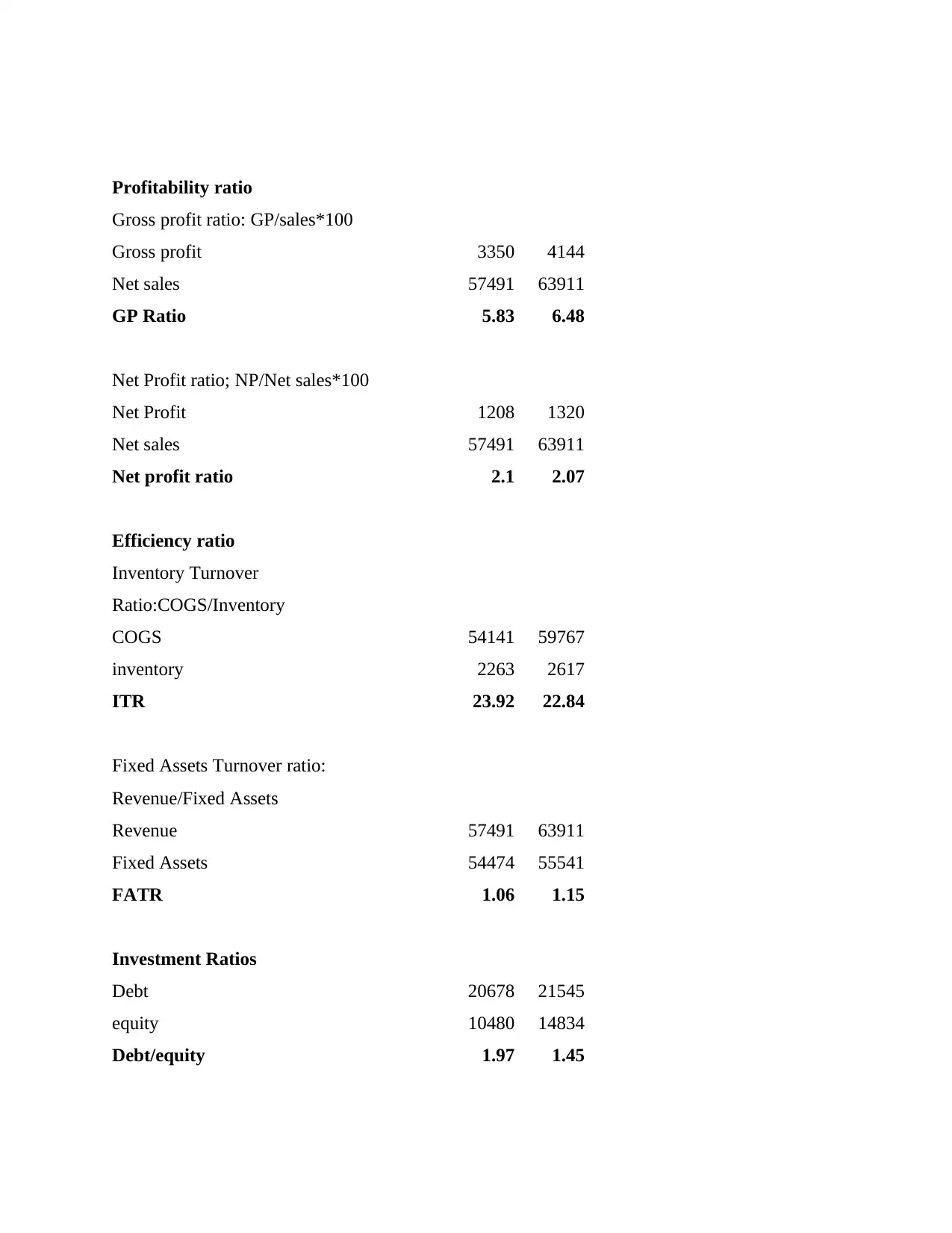

Profitability ratio

Gross profit ratio: GP/sales*100

Gross profit 3350 4144

Net sales 57491 63911

GP Ratio 5.83 6.48

Net Profit ratio; NP/Net sales*100

Net Profit 1208 1320

Net sales 57491 63911

Net profit ratio 2.1 2.07

Efficiency ratio

Inventory Turnover

Ratio:COGS/Inventory

COGS 54141 59767

inventory 2263 2617

ITR 23.92 22.84

Fixed Assets Turnover ratio:

Revenue/Fixed Assets

Revenue 57491 63911

Fixed Assets 54474 55541

FATR 1.06 1.15

Investment Ratios

Debt 20678 21545

equity 10480 14834

Debt/equity 1.97 1.45

Gross profit ratio: GP/sales*100

Gross profit 3350 4144

Net sales 57491 63911

GP Ratio 5.83 6.48

Net Profit ratio; NP/Net sales*100

Net Profit 1208 1320

Net sales 57491 63911

Net profit ratio 2.1 2.07

Efficiency ratio

Inventory Turnover

Ratio:COGS/Inventory

COGS 54141 59767

inventory 2263 2617

ITR 23.92 22.84

Fixed Assets Turnover ratio:

Revenue/Fixed Assets

Revenue 57491 63911

Fixed Assets 54474 55541

FATR 1.06 1.15

Investment Ratios

Debt 20678 21545

equity 10480 14834

Debt/equity 1.97 1.45

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

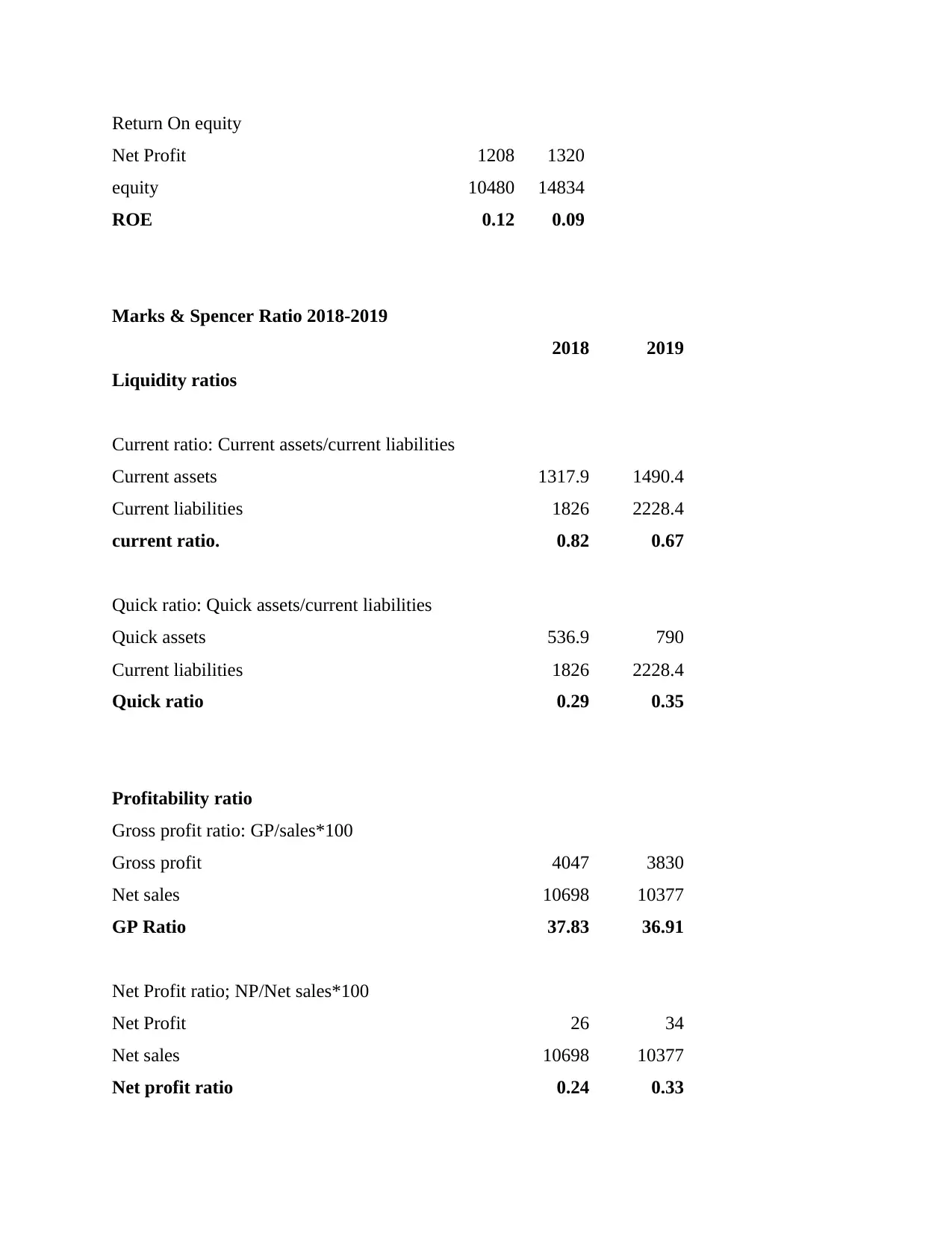

Return On equity

Net Profit 1208 1320

equity 10480 14834

ROE 0.12 0.09

Marks & Spencer Ratio 2018-2019

2018 2019

Liquidity ratios

Current ratio: Current assets/current liabilities

Current assets 1317.9 1490.4

Current liabilities 1826 2228.4

current ratio. 0.82 0.67

Quick ratio: Quick assets/current liabilities

Quick assets 536.9 790

Current liabilities 1826 2228.4

Quick ratio 0.29 0.35

Profitability ratio

Gross profit ratio: GP/sales*100

Gross profit 4047 3830

Net sales 10698 10377

GP Ratio 37.83 36.91

Net Profit ratio; NP/Net sales*100

Net Profit 26 34

Net sales 10698 10377

Net profit ratio 0.24 0.33

Net Profit 1208 1320

equity 10480 14834

ROE 0.12 0.09

Marks & Spencer Ratio 2018-2019

2018 2019

Liquidity ratios

Current ratio: Current assets/current liabilities

Current assets 1317.9 1490.4

Current liabilities 1826 2228.4

current ratio. 0.82 0.67

Quick ratio: Quick assets/current liabilities

Quick assets 536.9 790

Current liabilities 1826 2228.4

Quick ratio 0.29 0.35

Profitability ratio

Gross profit ratio: GP/sales*100

Gross profit 4047 3830

Net sales 10698 10377

GP Ratio 37.83 36.91

Net Profit ratio; NP/Net sales*100

Net Profit 26 34

Net sales 10698 10377

Net profit ratio 0.24 0.33

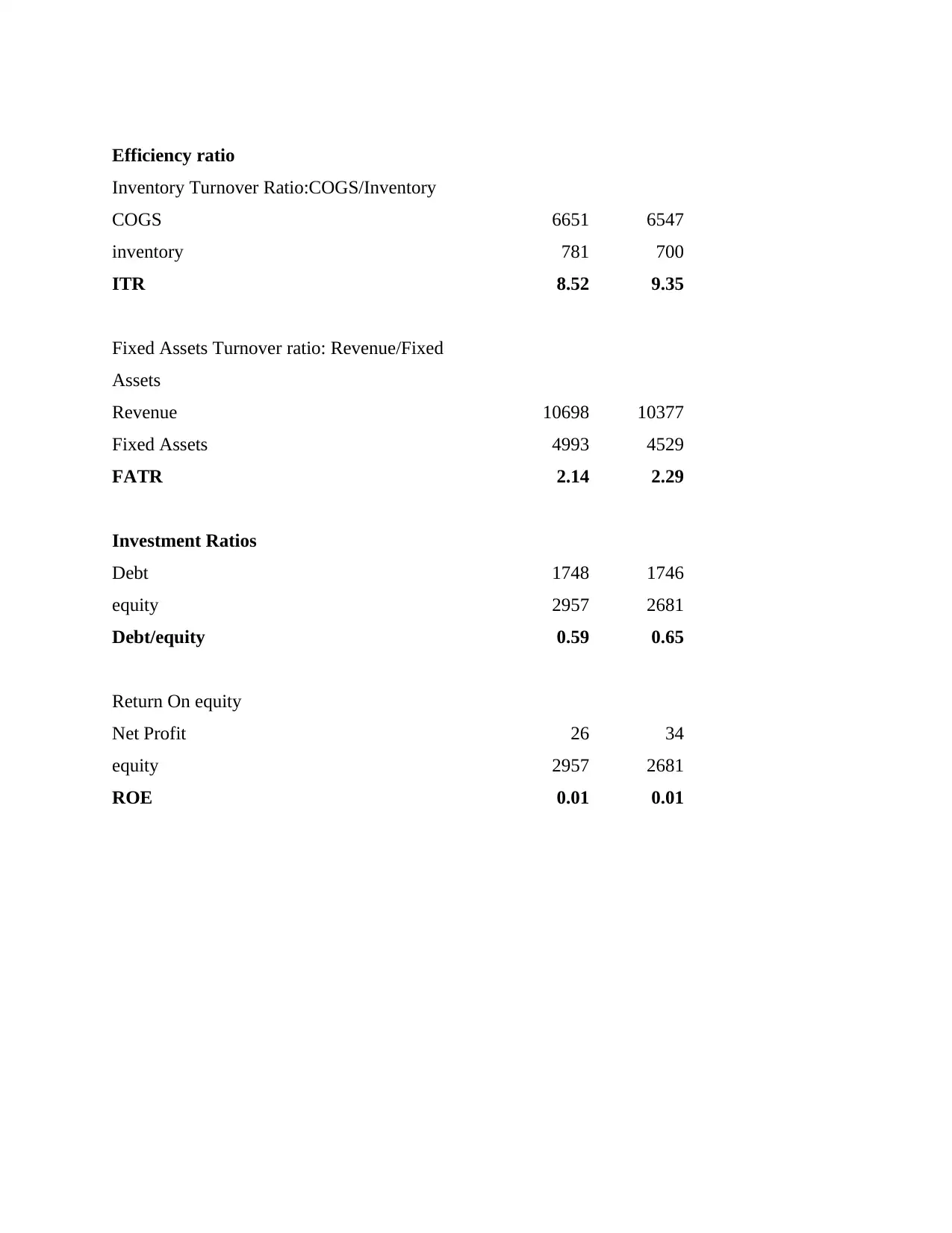

Efficiency ratio

Inventory Turnover Ratio:COGS/Inventory

COGS 6651 6547

inventory 781 700

ITR 8.52 9.35

Fixed Assets Turnover ratio: Revenue/Fixed

Assets

Revenue 10698 10377

Fixed Assets 4993 4529

FATR 2.14 2.29

Investment Ratios

Debt 1748 1746

equity 2957 2681

Debt/equity 0.59 0.65

Return On equity

Net Profit 26 34

equity 2957 2681

ROE 0.01 0.01

Inventory Turnover Ratio:COGS/Inventory

COGS 6651 6547

inventory 781 700

ITR 8.52 9.35

Fixed Assets Turnover ratio: Revenue/Fixed

Assets

Revenue 10698 10377

Fixed Assets 4993 4529

FATR 2.14 2.29

Investment Ratios

Debt 1748 1746

equity 2957 2681

Debt/equity 0.59 0.65

Return On equity

Net Profit 26 34

equity 2957 2681

ROE 0.01 0.01

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Analysis of Ratio -

Liquidity Ratios -

Current Ratio-

Current ratio is a liquidity ratio that measures company's ability to meet its short term

obligations within one year. Ideal current ratio is 2:1.

Current Ratio can be calculated as – Current assets/current liabilities

After analysing current ratio of Tesco we found that current ratio in 2018 was 2.46. It means

company can meet its short term obligations easily where as current ratio in 2019 was 1.57 that is

less compared to 2018. It means company will be facing problems in meeting its short term

obligations. Similarly, for Marks & Spencer Current ratio was higher in 2018 than 2019

(Albuhisi and Abdallah, 2018).

Quick Ratio-

Quick ratio can be calculated as- Current assets – Inventory/Current Liabilities

Quick Ratio measures company's ability to meet its short term obligations with its most liquid

assets. It is also known as an “Acid Test”. Ideal quick ratio is 1:1. As mentioned in above table

tesco's Quick ratio in 2018 is higher compared to 2019 it means company had more liquid assets

in 2018 compared to 2019. Similarly for marks and spencer quick ratio in 2018 was higher than

2019.

Profitability Ratios -

Gross profit -

Gross Profit can be calculated as – Gross Profit/Revenue*100

When a company makes profit after deducting cost associated in making that product and selling

the same. Gross Profit of 65% is considered as healthy ratio.

Now coming to analysis, In the above table gross profit of tesco in 2018 and 2019 was 5.83 and

6.48, respectively which is very low. It means cost associated in making its product is very high.

For Marks and spencer, Gross profit in the year 2018 was 37.82 and in 2019 it was 36.90 which

is quite better than tesco. It mean company has control over cost associated in making its

products compared to Tesco (Chen, 2018).

Net Profit -

Net profit can be calculate as – Net profit/Net sales *100

Liquidity Ratios -

Current Ratio-

Current ratio is a liquidity ratio that measures company's ability to meet its short term

obligations within one year. Ideal current ratio is 2:1.

Current Ratio can be calculated as – Current assets/current liabilities

After analysing current ratio of Tesco we found that current ratio in 2018 was 2.46. It means

company can meet its short term obligations easily where as current ratio in 2019 was 1.57 that is

less compared to 2018. It means company will be facing problems in meeting its short term

obligations. Similarly, for Marks & Spencer Current ratio was higher in 2018 than 2019

(Albuhisi and Abdallah, 2018).

Quick Ratio-

Quick ratio can be calculated as- Current assets – Inventory/Current Liabilities

Quick Ratio measures company's ability to meet its short term obligations with its most liquid

assets. It is also known as an “Acid Test”. Ideal quick ratio is 1:1. As mentioned in above table

tesco's Quick ratio in 2018 is higher compared to 2019 it means company had more liquid assets

in 2018 compared to 2019. Similarly for marks and spencer quick ratio in 2018 was higher than

2019.

Profitability Ratios -

Gross profit -

Gross Profit can be calculated as – Gross Profit/Revenue*100

When a company makes profit after deducting cost associated in making that product and selling

the same. Gross Profit of 65% is considered as healthy ratio.

Now coming to analysis, In the above table gross profit of tesco in 2018 and 2019 was 5.83 and

6.48, respectively which is very low. It means cost associated in making its product is very high.

For Marks and spencer, Gross profit in the year 2018 was 37.82 and in 2019 it was 36.90 which

is quite better than tesco. It mean company has control over cost associated in making its

products compared to Tesco (Chen, 2018).

Net Profit -

Net profit can be calculate as – Net profit/Net sales *100

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

When all the business expenses are subtracted from the revenue then remaining amount of

money is known as net profit. 10% of net profit is considered as average profit. 20% is

considered as high net profit and 5% profit is considered as low net profit. Net profit of Tesco in

2018 and 2019 is 2.10 and 2.06 respectively which is very low and for marks and spencer net

profit is only 0.24 and 0.32 in 2018 and 2019 respectively, which is also very less. It means

companies are not performing better as they have more expenses than revenue. So companies

should control expenses in order to increase net profit.

Efficiency Ratios -

Inventory Turnover Ratio -

Inventory turnover ratio can be calculated as – Cost of goods sold/Inventory

It measures that number of times inventory is sold or consumed in given time of period. Ideal

inventory turnover ratio is between 5 to 10. From the above table we can see that inventory

turnover ratio of tesco in 2018 and 2019 is very higher than ideal ratio, Whereas for marks and

spencer inventory turnover ratio in 2018 is 8.51 and in 2019 it's 9.35. and it is quite good because

it ranges between 5 to 10 (Cui and et.al., 2019).

Fixed Asset Turnover Ratio -

Fixed asset turnover ratio can be calculated as- Revenue/ Fixed assets

Fixed asset turnover ratio indicates that how well company uses its fixed assets to generate

sales. Higher fixed asset turnover ratio indicates that companies are using its fixed assets

effectively. Fixed asset turnover ratio of tesco in 2018 is 1.05 and in 2019 it is 1.51 and for

marks and spencer this ratio in 2018 is 2.14 and in 2019 it is 2.29. it means companies are using

its fixed assets properly in order to generate sales.

Investment Ratios-

Debt to Equity Ratio-

Debt to equity can be calculated as - Total Debt/Total equity

Debt to equity ratio compares company's total liabilities to shareholder's equity. It can also be

used to evaluate how much leverage company is using. Ideal debt to equity ratio is around 1 to

1.5. For Tesco Debt to equity ratio in 2018 is 1.97 and in 2019 it's 1.45 and it lies between ideal

money is known as net profit. 10% of net profit is considered as average profit. 20% is

considered as high net profit and 5% profit is considered as low net profit. Net profit of Tesco in

2018 and 2019 is 2.10 and 2.06 respectively which is very low and for marks and spencer net

profit is only 0.24 and 0.32 in 2018 and 2019 respectively, which is also very less. It means

companies are not performing better as they have more expenses than revenue. So companies

should control expenses in order to increase net profit.

Efficiency Ratios -

Inventory Turnover Ratio -

Inventory turnover ratio can be calculated as – Cost of goods sold/Inventory

It measures that number of times inventory is sold or consumed in given time of period. Ideal

inventory turnover ratio is between 5 to 10. From the above table we can see that inventory

turnover ratio of tesco in 2018 and 2019 is very higher than ideal ratio, Whereas for marks and

spencer inventory turnover ratio in 2018 is 8.51 and in 2019 it's 9.35. and it is quite good because

it ranges between 5 to 10 (Cui and et.al., 2019).

Fixed Asset Turnover Ratio -

Fixed asset turnover ratio can be calculated as- Revenue/ Fixed assets

Fixed asset turnover ratio indicates that how well company uses its fixed assets to generate

sales. Higher fixed asset turnover ratio indicates that companies are using its fixed assets

effectively. Fixed asset turnover ratio of tesco in 2018 is 1.05 and in 2019 it is 1.51 and for

marks and spencer this ratio in 2018 is 2.14 and in 2019 it is 2.29. it means companies are using

its fixed assets properly in order to generate sales.

Investment Ratios-

Debt to Equity Ratio-

Debt to equity can be calculated as - Total Debt/Total equity

Debt to equity ratio compares company's total liabilities to shareholder's equity. It can also be

used to evaluate how much leverage company is using. Ideal debt to equity ratio is around 1 to

1.5. For Tesco Debt to equity ratio in 2018 is 1.97 and in 2019 it's 1.45 and it lies between ideal

ratio means company is using its assets properly but for marks and spencer 0.59 and 0.65 which

is quite low it means company is not using its assets properly (Franco and et.al., 2020).

Return On Equity-

ROE can be calculated as – Net Income/shareholder's equity

It measures how efficiently company is handling the money that shareholders have contributed

into it. Higher the ROE , higher the company's management is at generating income. In the above

mentioned table, Tseco and marks and spencer are not giving high ROE hence, companies are

not handling shareholders money properly.

Critically determine the Balance scorecard

Balance scorecard- This concern is frameworks in which it helps in implementing the

management strategy of the company. Through this company able to boost the performance of

the employees to perform well in the exams and that will be useful in improving the benefits of

the company in proper manner. This tool is useful in providing the help in maintaining the

efficiency in much better manner as it helps in fulfilling the short- term and long term objective

of the company. This model is basically lustful in improving the efficiency of the company in

better manner and reduces the inefficiency in the company. This model is develop by the Kaplan

and Norton in the year of 1992 and that become the famous frameworks that is useful in

achieving the overall performance of the company and useful in attainment of goals and

objectives. In the context of Tesco and Marks and Spencer, it is important system which required

to be implementation within the process and system and therefore it will help in ensuring the

strategic implementation that could be use in efficient manner to operate the organisation. Hence

the use of this system will be essential for both the company that could use to measure the

performance of objectives and goals of the company (Hutahayan, 2020). Following are the

multiple perspective that used to analyse the balance scorecard in following manner-

Financial- This is higher level of financial perspective that required to be consider by the

company and will be useful in managing the position of funds in better manner. This will

help in managing the funds in the right manner. This help in attainment of overall goals

and objectives of the company. In the context of Tesco, this perspective plays the

important role in financing the companies in much better manner.

Customer- This helps in viewing the organisation from the perspective of customer of

the organisation and useful in framing the goals and objective of the company. Customer,

is quite low it means company is not using its assets properly (Franco and et.al., 2020).

Return On Equity-

ROE can be calculated as – Net Income/shareholder's equity

It measures how efficiently company is handling the money that shareholders have contributed

into it. Higher the ROE , higher the company's management is at generating income. In the above

mentioned table, Tseco and marks and spencer are not giving high ROE hence, companies are

not handling shareholders money properly.

Critically determine the Balance scorecard

Balance scorecard- This concern is frameworks in which it helps in implementing the

management strategy of the company. Through this company able to boost the performance of

the employees to perform well in the exams and that will be useful in improving the benefits of

the company in proper manner. This tool is useful in providing the help in maintaining the

efficiency in much better manner as it helps in fulfilling the short- term and long term objective

of the company. This model is basically lustful in improving the efficiency of the company in

better manner and reduces the inefficiency in the company. This model is develop by the Kaplan

and Norton in the year of 1992 and that become the famous frameworks that is useful in

achieving the overall performance of the company and useful in attainment of goals and

objectives. In the context of Tesco and Marks and Spencer, it is important system which required

to be implementation within the process and system and therefore it will help in ensuring the

strategic implementation that could be use in efficient manner to operate the organisation. Hence

the use of this system will be essential for both the company that could use to measure the

performance of objectives and goals of the company (Hutahayan, 2020). Following are the

multiple perspective that used to analyse the balance scorecard in following manner-

Financial- This is higher level of financial perspective that required to be consider by the

company and will be useful in managing the position of funds in better manner. This will

help in managing the funds in the right manner. This help in attainment of overall goals

and objectives of the company. In the context of Tesco, this perspective plays the

important role in financing the companies in much better manner.

Customer- This helps in viewing the organisation from the perspective of customer of

the organisation and useful in framing the goals and objective of the company. Customer,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

stakeholder play important role in the success of the company and will help in developing

the efficient structure of the company. This become essential role in developing and

application of all needs and requirement of the customer demand. To become the leader

in the market, it is necessary to satisfy their needs and all expectation from the company.

Internal process- This is wide range that measure the internal process of the company to

undertake in the improvement in the internal process that has to be measure the

operational efficiency and effectiveness. In the context of Tesco, the internal process is

core business process that decide the operational strategical effectiveness of the company.

So, balance score card useful in maintaining the performance metrics of the company

(Karami, Samimi and Ja'fari, 2020).

Organisational capacity- This is wide range of measure that undertaken in order to

ensure the substantial growth in the company and will be helpful in managing the

capacity of the company. This also leads to increase the overall efficiency in proper

manner to improve the organisational performance. In the context of Company A which

is Tesco, the measuring of organisational performance is very effective in terms of

measuring the improvement in the company so that it able to give maximum profit in its

business to achieve the goals.

Following are the Critical success factor for the organisation are as follows-

Identifying the CSFs helps in track and measure the performance of the progress towards

achieving the strategic goals. In the context of Tesco, following are the activities that need to be

carefully and constantly give attention from the management to adequately perform the function

in the firm.

Strategic focus- This is one of the critical success factor that need to be consider by the

company in order to facilitates in the company. This factor is very useful in terms of

giving successful process of the company and need to be focus. It include the Leadership,

management and planning in the management and will help in maintaining the

effectiveness. This ensure that it will help in achieving the goals and objectives to make

the organisation more effective.

People- This is also critical success of factor that will help in managing the proper

relationship with the loyal and potential staff personnel. This also useful in development

of effectiveness in employee performance as they has to be trained enough to perform

the efficient structure of the company. This become essential role in developing and

application of all needs and requirement of the customer demand. To become the leader

in the market, it is necessary to satisfy their needs and all expectation from the company.

Internal process- This is wide range that measure the internal process of the company to

undertake in the improvement in the internal process that has to be measure the

operational efficiency and effectiveness. In the context of Tesco, the internal process is

core business process that decide the operational strategical effectiveness of the company.

So, balance score card useful in maintaining the performance metrics of the company

(Karami, Samimi and Ja'fari, 2020).

Organisational capacity- This is wide range of measure that undertaken in order to

ensure the substantial growth in the company and will be helpful in managing the

capacity of the company. This also leads to increase the overall efficiency in proper

manner to improve the organisational performance. In the context of Company A which

is Tesco, the measuring of organisational performance is very effective in terms of

measuring the improvement in the company so that it able to give maximum profit in its

business to achieve the goals.

Following are the Critical success factor for the organisation are as follows-

Identifying the CSFs helps in track and measure the performance of the progress towards

achieving the strategic goals. In the context of Tesco, following are the activities that need to be

carefully and constantly give attention from the management to adequately perform the function

in the firm.

Strategic focus- This is one of the critical success factor that need to be consider by the

company in order to facilitates in the company. This factor is very useful in terms of

giving successful process of the company and need to be focus. It include the Leadership,

management and planning in the management and will help in maintaining the

effectiveness. This ensure that it will help in achieving the goals and objectives to make

the organisation more effective.

People- This is also critical success of factor that will help in managing the proper

relationship with the loyal and potential staff personnel. This also useful in development

of effectiveness in employee performance as they has to be trained enough to perform

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

any kind of task and it will increase the overall performance of the employees and

company as well. This gives the major goals and objective to achieve the main mission of

the company. This helps in improving the efficiency of the company and will help in

maintaining the efficiency of the company. In the context of Tesco, this factor plays

important role in achieving the goals and objective of the company as they are playing

essential part in fulfilling the main objectives (Le and et.al., 2018).

Operations- This is also could be consider as the critical success factor of the company

as this involve the process and work of the company. This helps in developing the

effectiveness of the company through controlling and regulating the internal process of

the organisation. This increases the overall efficiency and effectiveness of the company

as this concentrate on the improvement of all operational effectiveness.

Finances- This refers to the important role in the company in order to enhance the

financial stability and performance of the company as this help in analysing the best way

to improving the effectiveness. In the context of Tesco, the need to increase the

productivity of the company it important to identify the following perspective in the

company to understand the requirement of finance function as it facilitates in analysing

the project which are profitable for the investment purpose that will be useful for the firm

(Miroshnychenko, Barontini and Testa, 2017).

Marketing – This also play essential role in managing the overall activities and function

that used to attract the customer to make the better use of their products. This include the

customer relations, sales and promotional activities that were basically responsible for the

success of the company. This factor is playing essential role in sales and profitability in

the organisation and will be useful in maintaining the effectiveness of the company. In

the context of Tesco, the need of monitoring this factor helps in improving the efficiency

and effectiveness of the organisation.

Evaluating the benefits and challenges of the Integrated reporting

Integrated reporting refers to the corporate communication that is process for refers to the

communication about the creation. This is concise information about the how business strategy,

governance, performance lead for the short, long term goals. This is the representation of

financial and non-financial performance of the company in single report. This is more beneficial

in the context of non-financial data such as how company is performing the environmental,

company as well. This gives the major goals and objective to achieve the main mission of

the company. This helps in improving the efficiency of the company and will help in

maintaining the efficiency of the company. In the context of Tesco, this factor plays

important role in achieving the goals and objective of the company as they are playing

essential part in fulfilling the main objectives (Le and et.al., 2018).

Operations- This is also could be consider as the critical success factor of the company

as this involve the process and work of the company. This helps in developing the

effectiveness of the company through controlling and regulating the internal process of

the organisation. This increases the overall efficiency and effectiveness of the company

as this concentrate on the improvement of all operational effectiveness.

Finances- This refers to the important role in the company in order to enhance the

financial stability and performance of the company as this help in analysing the best way

to improving the effectiveness. In the context of Tesco, the need to increase the

productivity of the company it important to identify the following perspective in the

company to understand the requirement of finance function as it facilitates in analysing

the project which are profitable for the investment purpose that will be useful for the firm

(Miroshnychenko, Barontini and Testa, 2017).

Marketing – This also play essential role in managing the overall activities and function

that used to attract the customer to make the better use of their products. This include the

customer relations, sales and promotional activities that were basically responsible for the

success of the company. This factor is playing essential role in sales and profitability in

the organisation and will be useful in maintaining the effectiveness of the company. In

the context of Tesco, the need of monitoring this factor helps in improving the efficiency

and effectiveness of the organisation.

Evaluating the benefits and challenges of the Integrated reporting

Integrated reporting refers to the corporate communication that is process for refers to the

communication about the creation. This is concise information about the how business strategy,

governance, performance lead for the short, long term goals. This is the representation of

financial and non-financial performance of the company in single report. This is more beneficial

in the context of non-financial data such as how company is performing the environmental,

social and governance parameters. This is helps to the shareholder and different stakeholders in

terms of analysing the core business efficiency and effectiveness. This is important in the veiw of

determining the sustainability and overall performance of the organisation. It aims to develop the

reporting development to provide more holistic form of reporting to create the value for the

company (Ricci and Civitillo, 2018). As this consider many other factors also other than the

financial aspects of the company. This is backed by IIRC, powerful global coalition of

regulators, investor, companies, standard setters to share the better communication about the

evolution of corporate reporting. In the context of Tesco, this is not just corporate report, it relies

that proposition that companies should be given in proper manner to understand the issue in

many ways. This also helps in traditional approach of the thinking in much better manner and

will be useful in managing the effective way to consider the efficiency. This also helps in

fulfilling the efficiency in greater context. This is useful in many ways and will be helpful in

managing the single task in efficient manner. Some of the following benefits are as follows-

This helps in demonstrating the company in serious form and incorporating sustainability

into it core business. In the context of Tesco, this is useful in increasing the overall

profitability of the company (Xie and Wang, 2017).

This also helps in communicating the impact of company's operations on the

environment and community that helps in mitigating the effects and the commitment of

the organisation. This tells the basic form of understanding the need of the organisation

and useful in delivering the better results, In the context of Tesco, this helps in forming

the major form of efficiency to handle various other benefits and will give the

appropriate manner of results.

Integrated reporting also helps in analysing the informed decision making to improve

overall performance and it also improve the competitive edge of the company in longer

terms to lower the cost of capital. In the context of Tesco, this assist in reducing the cost

of capital and increasing the profitability in longer period and also helps in analysing the

risk and opportunities to improve the sales and correctly identify the ESG. This gives the

better way to improve the effectiveness (Sardo and Serrasqueiro, 2018).

This also increases the brand value and customer loyalty to interpret better image of the

organisation as this helps in improving the effectiveness in order achieve the goals and

objectives. In the context of Tesco, this helps in improving the effectiveness for

terms of analysing the core business efficiency and effectiveness. This is important in the veiw of

determining the sustainability and overall performance of the organisation. It aims to develop the

reporting development to provide more holistic form of reporting to create the value for the

company (Ricci and Civitillo, 2018). As this consider many other factors also other than the

financial aspects of the company. This is backed by IIRC, powerful global coalition of

regulators, investor, companies, standard setters to share the better communication about the

evolution of corporate reporting. In the context of Tesco, this is not just corporate report, it relies

that proposition that companies should be given in proper manner to understand the issue in

many ways. This also helps in traditional approach of the thinking in much better manner and

will be useful in managing the effective way to consider the efficiency. This also helps in

fulfilling the efficiency in greater context. This is useful in many ways and will be helpful in

managing the single task in efficient manner. Some of the following benefits are as follows-

This helps in demonstrating the company in serious form and incorporating sustainability

into it core business. In the context of Tesco, this is useful in increasing the overall

profitability of the company (Xie and Wang, 2017).

This also helps in communicating the impact of company's operations on the

environment and community that helps in mitigating the effects and the commitment of

the organisation. This tells the basic form of understanding the need of the organisation

and useful in delivering the better results, In the context of Tesco, this helps in forming

the major form of efficiency to handle various other benefits and will give the

appropriate manner of results.

Integrated reporting also helps in analysing the informed decision making to improve

overall performance and it also improve the competitive edge of the company in longer

terms to lower the cost of capital. In the context of Tesco, this assist in reducing the cost

of capital and increasing the profitability in longer period and also helps in analysing the

risk and opportunities to improve the sales and correctly identify the ESG. This gives the

better way to improve the effectiveness (Sardo and Serrasqueiro, 2018).

This also increases the brand value and customer loyalty to interpret better image of the

organisation as this helps in improving the effectiveness in order achieve the goals and

objectives. In the context of Tesco, this helps in improving the effectiveness for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.