Detailed Analysis of Financial Statements and Performance Report

VerifiedAdded on 2022/12/30

|9

|1514

|34

Report

AI Summary

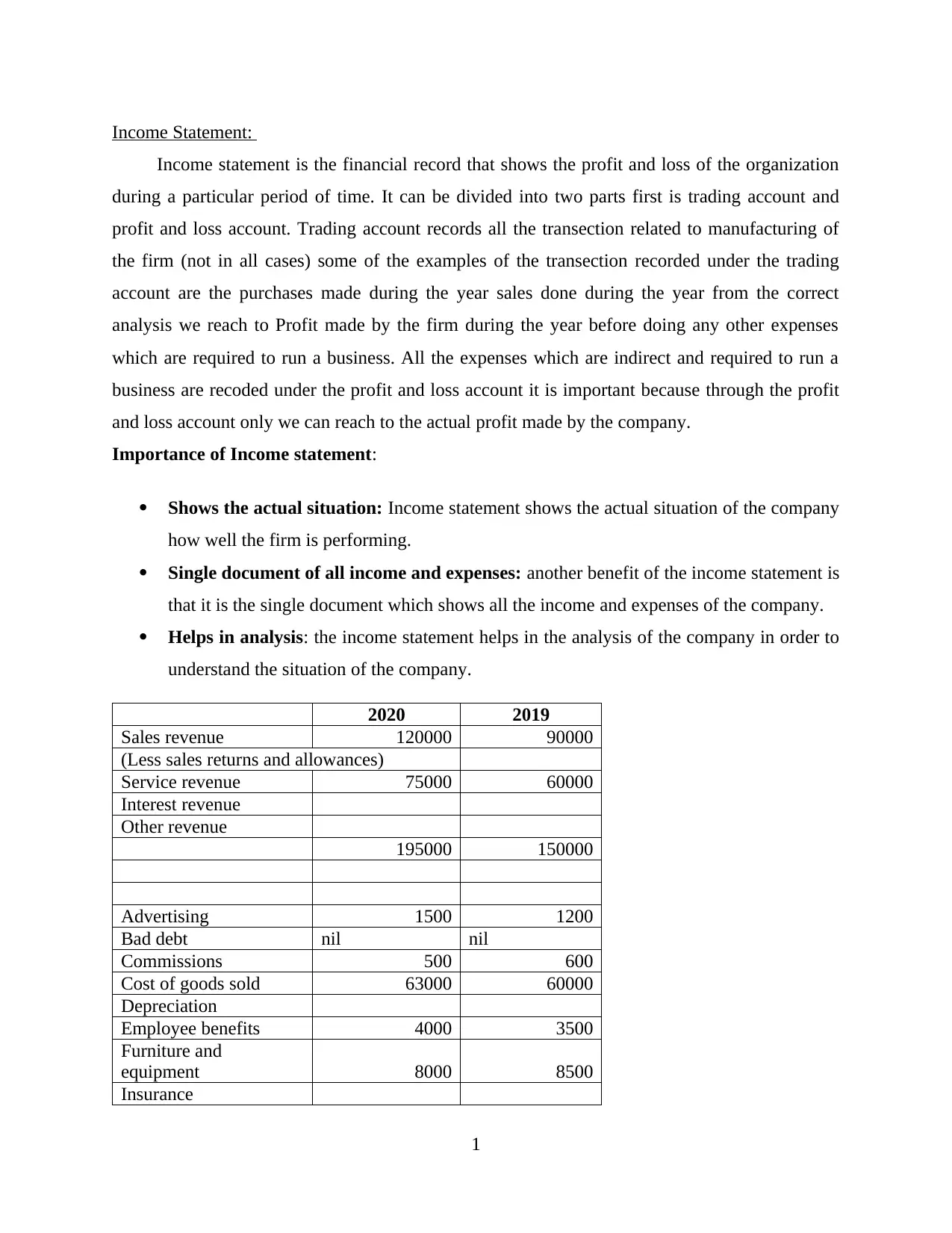

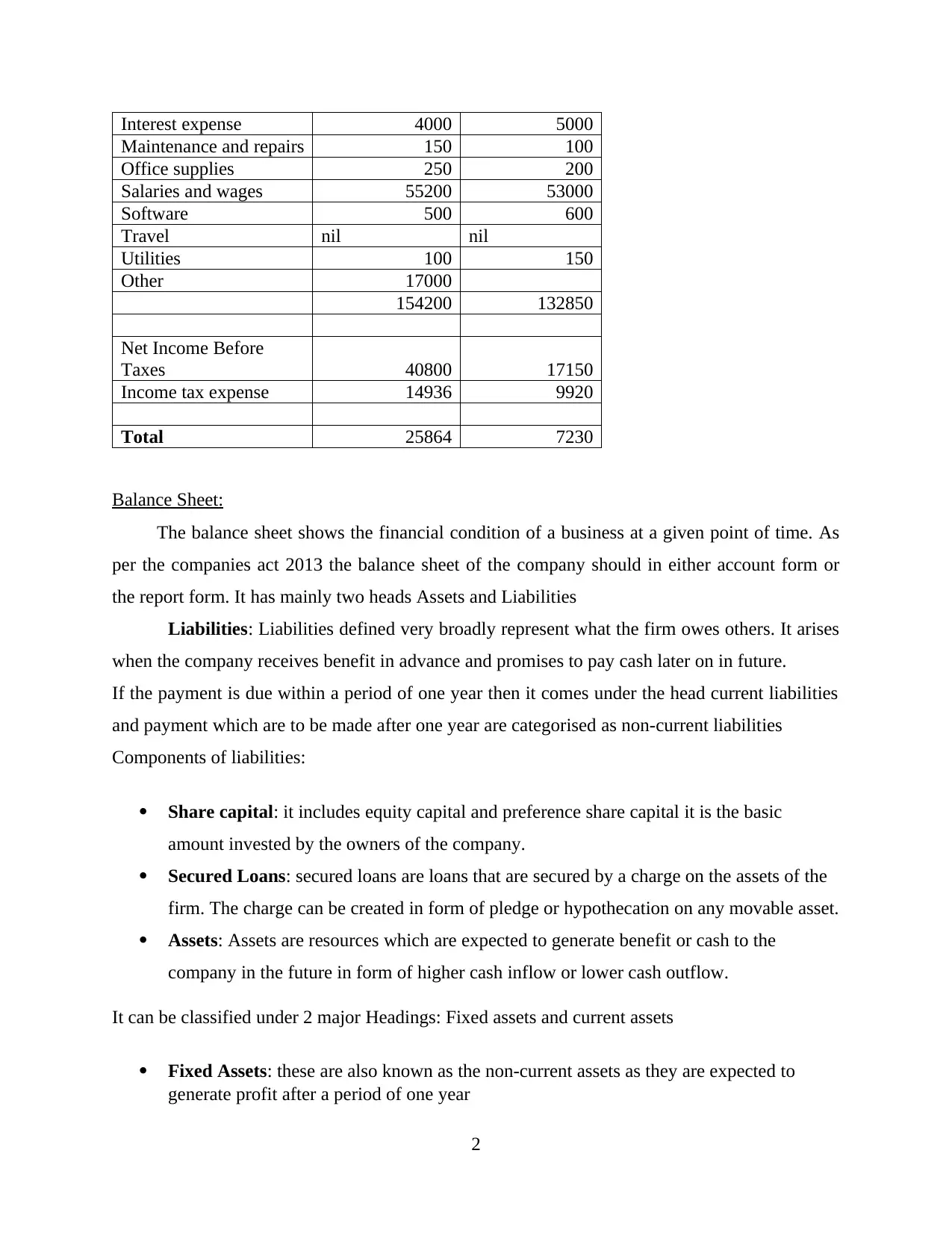

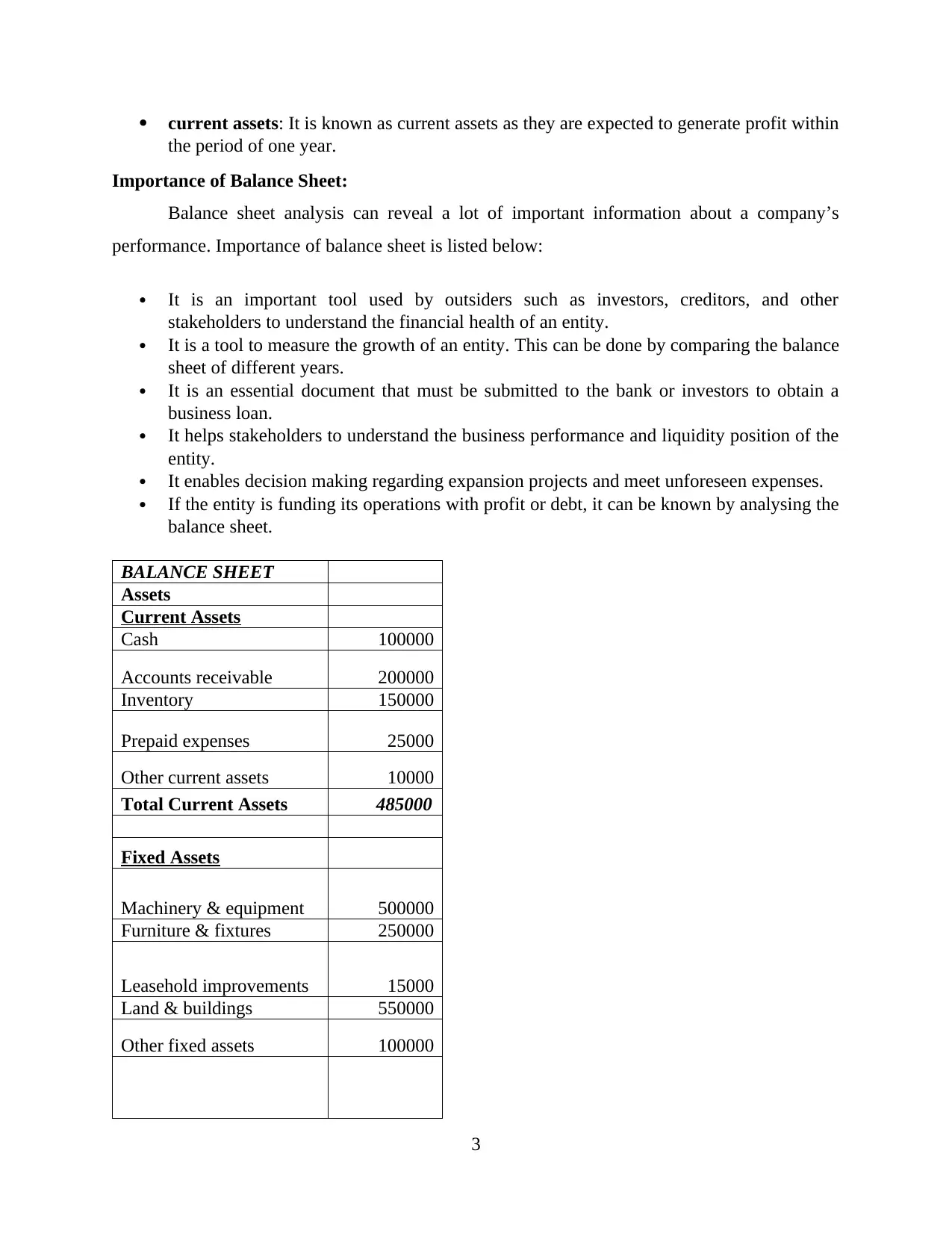

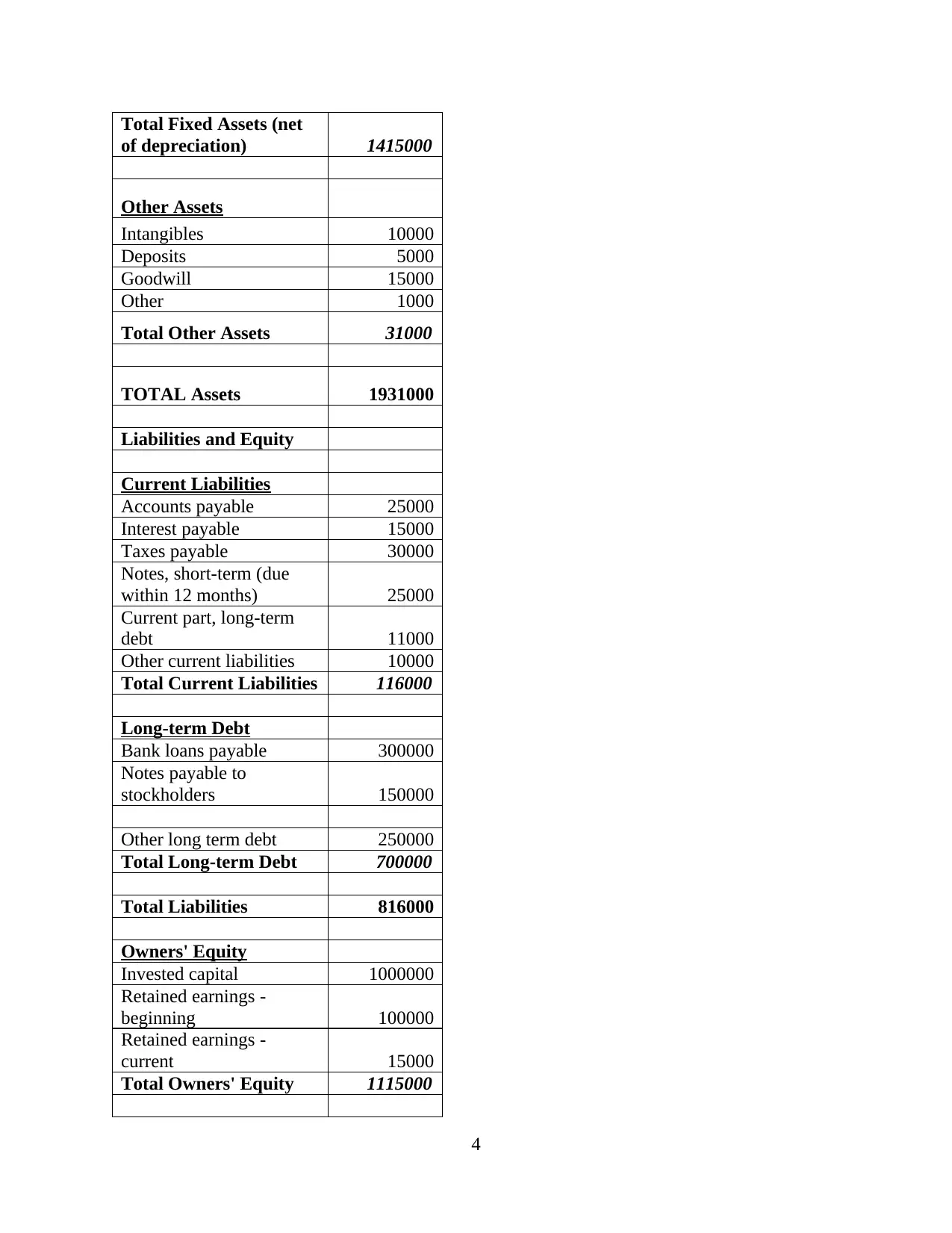

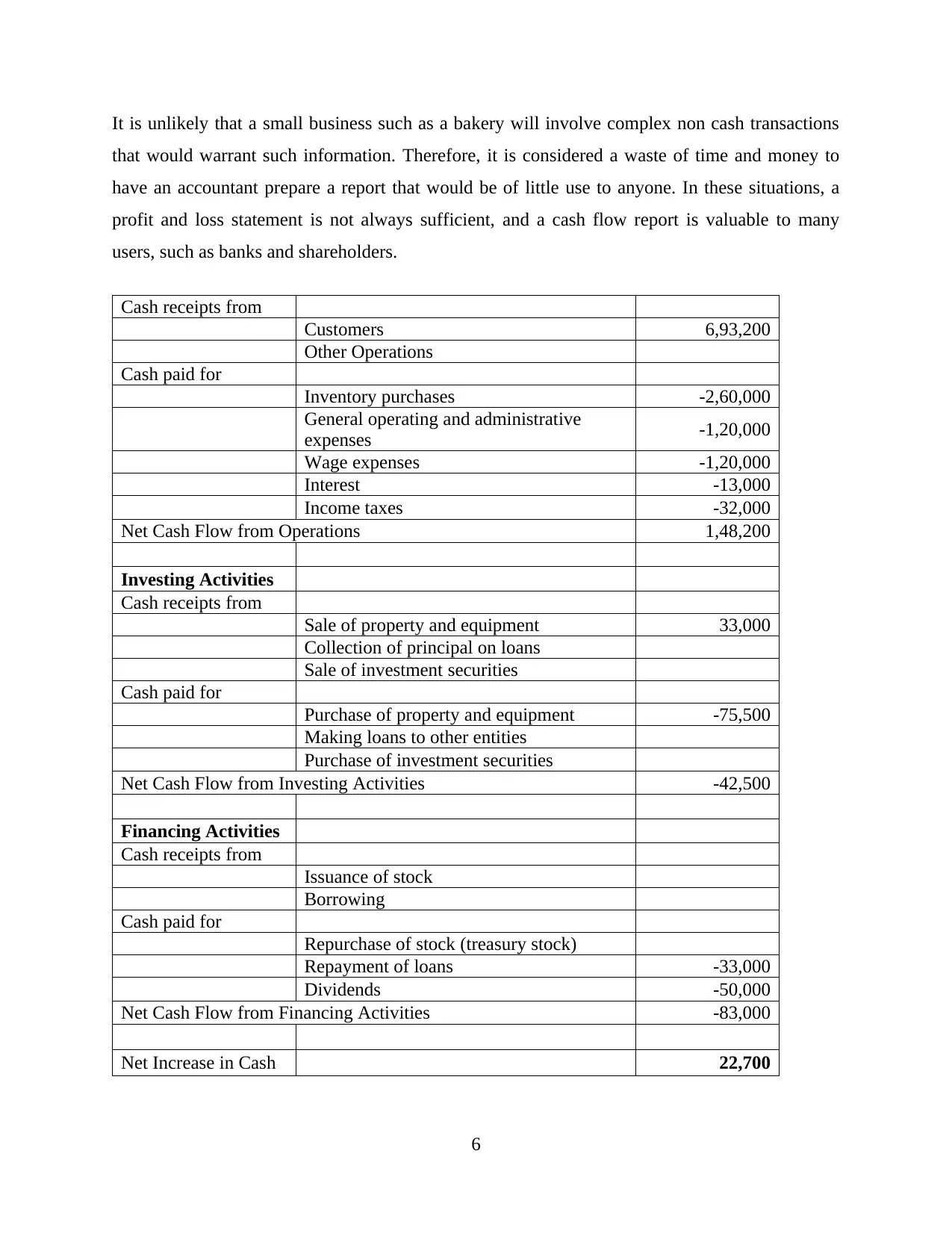

This report provides a detailed analysis of financial statements, including an income statement, balance sheet, and cash flow statement. The income statement presents the company's financial performance over a specific period, detailing revenue, expenses, and net income. The balance sheet offers a snapshot of the company's financial position at a given point in time, outlining assets, liabilities, and equity. The cash flow statement explains how the company obtains and spends cash through operating, investing, and financing activities. The report emphasizes the importance of each statement in understanding a company's financial health and performance, offering insights into profitability, liquidity, and overall financial stability. The financial statements are presented for the year 2020 and 2019 with different components like revenue, cost of goods sold, assets, liabilities, and equity with their respective values. The importance and components of each statement are also discussed.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.