Financial Performance Management and Variance Analysis Report

VerifiedAdded on 2022/12/28

|13

|2674

|79

Report

AI Summary

This report undertakes a detailed analysis of financial performance management, encompassing cost calculations, variance analysis, and budgeting techniques. The report begins by calculating cost per unit using both labor hours and activity-based costing approaches, followed by a comparative analysis of the results. Sensitivity analysis is applied to aid managers in dealing with uncertainties. The report then delves into variance calculations, including material usage, mix, and yield variances, while also addressing problems associated with the current system of calculating and reporting variances. Finally, it provides a critical discussion of zero-based budgeting (ZBB) and incremental budgeting (IB) to determine their effectiveness in planning, coordination, and control. The report concludes by assessing the suitability of these methods for financial planning.

Financial Performance

Management

Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

(a) Calculate cost per unit on basis of labour hours....................................................................1

(b) Calculate cost per unit on basis of activity based costing approach......................................2

(c) Analysis results on basis of labour hours and activity based costing approach....................4

(d) Sensitivity analysis help managers to cope with uncertainties..............................................5

QUESTION 2...................................................................................................................................6

(a) Calculation of variances........................................................................................................6

(b) Problems with current system of calculating and reporting variances..................................7

QUESTION 3...................................................................................................................................8

Critically discussed neither ZBB nor the IB provides the perfect toll for planning coordination

and control...................................................................................................................................8

CONCLUSION ...............................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

(a) Calculate cost per unit on basis of labour hours....................................................................1

(b) Calculate cost per unit on basis of activity based costing approach......................................2

(c) Analysis results on basis of labour hours and activity based costing approach....................4

(d) Sensitivity analysis help managers to cope with uncertainties..............................................5

QUESTION 2...................................................................................................................................6

(a) Calculation of variances........................................................................................................6

(b) Problems with current system of calculating and reporting variances..................................7

QUESTION 3...................................................................................................................................8

Critically discussed neither ZBB nor the IB provides the perfect toll for planning coordination

and control...................................................................................................................................8

CONCLUSION ...............................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION

Financial performance management is a continuous cycle of business and essential at

every step for growth & success. It is a subjective measurement that conduct by the every

organisation to effective run their business activities in proper manner. The management use this

term to measure overall efficiency and financial health in specified period of time. There are

various ways to analysis the financial performance and should be taken in aggregated. Moreover

analyst and investors wish to look deeper into financial reports and declining debt (Ye, Xiao and

Zhou, 2019). This report based on the calculation of cost as per the method of activity based

costing and absorption costing. In this report consist of apply sensitivity analysis to support

managers and calculate different material variances. Along with analysis the problems with

current system and variances for analysing the performance. At the end of the report, critically

discuss about the ZBB and incremental budgeting for perfect planning.

QUESTION 1

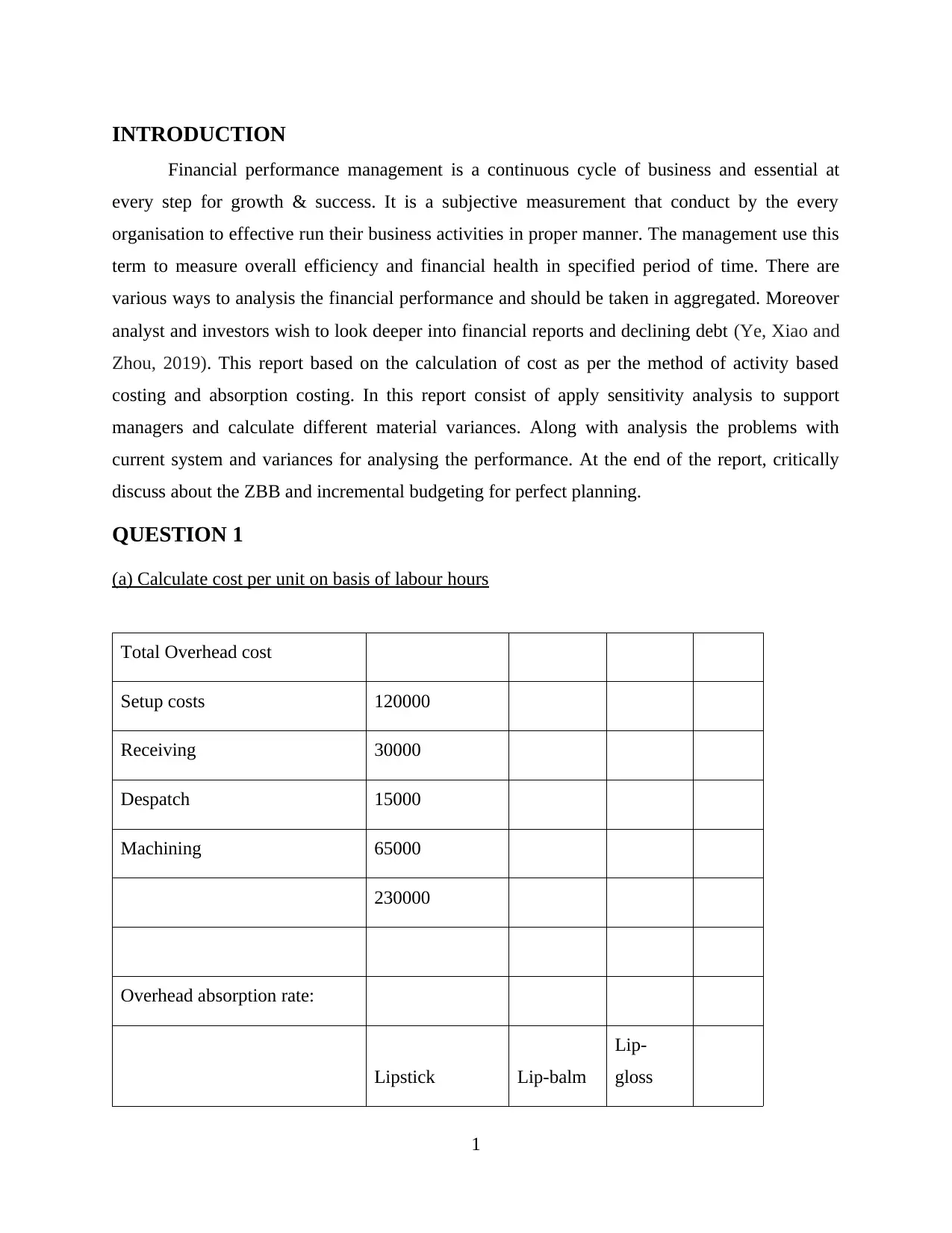

(a) Calculate cost per unit on basis of labour hours

Total Overhead cost

Setup costs 120000

Receiving 30000

Despatch 15000

Machining 65000

230000

Overhead absorption rate:

Lipstick Lip-balm

Lip-

gloss

1

Financial performance management is a continuous cycle of business and essential at

every step for growth & success. It is a subjective measurement that conduct by the every

organisation to effective run their business activities in proper manner. The management use this

term to measure overall efficiency and financial health in specified period of time. There are

various ways to analysis the financial performance and should be taken in aggregated. Moreover

analyst and investors wish to look deeper into financial reports and declining debt (Ye, Xiao and

Zhou, 2019). This report based on the calculation of cost as per the method of activity based

costing and absorption costing. In this report consist of apply sensitivity analysis to support

managers and calculate different material variances. Along with analysis the problems with

current system and variances for analysing the performance. At the end of the report, critically

discuss about the ZBB and incremental budgeting for perfect planning.

QUESTION 1

(a) Calculate cost per unit on basis of labour hours

Total Overhead cost

Setup costs 120000

Receiving 30000

Despatch 15000

Machining 65000

230000

Overhead absorption rate:

Lipstick Lip-balm

Lip-

gloss

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

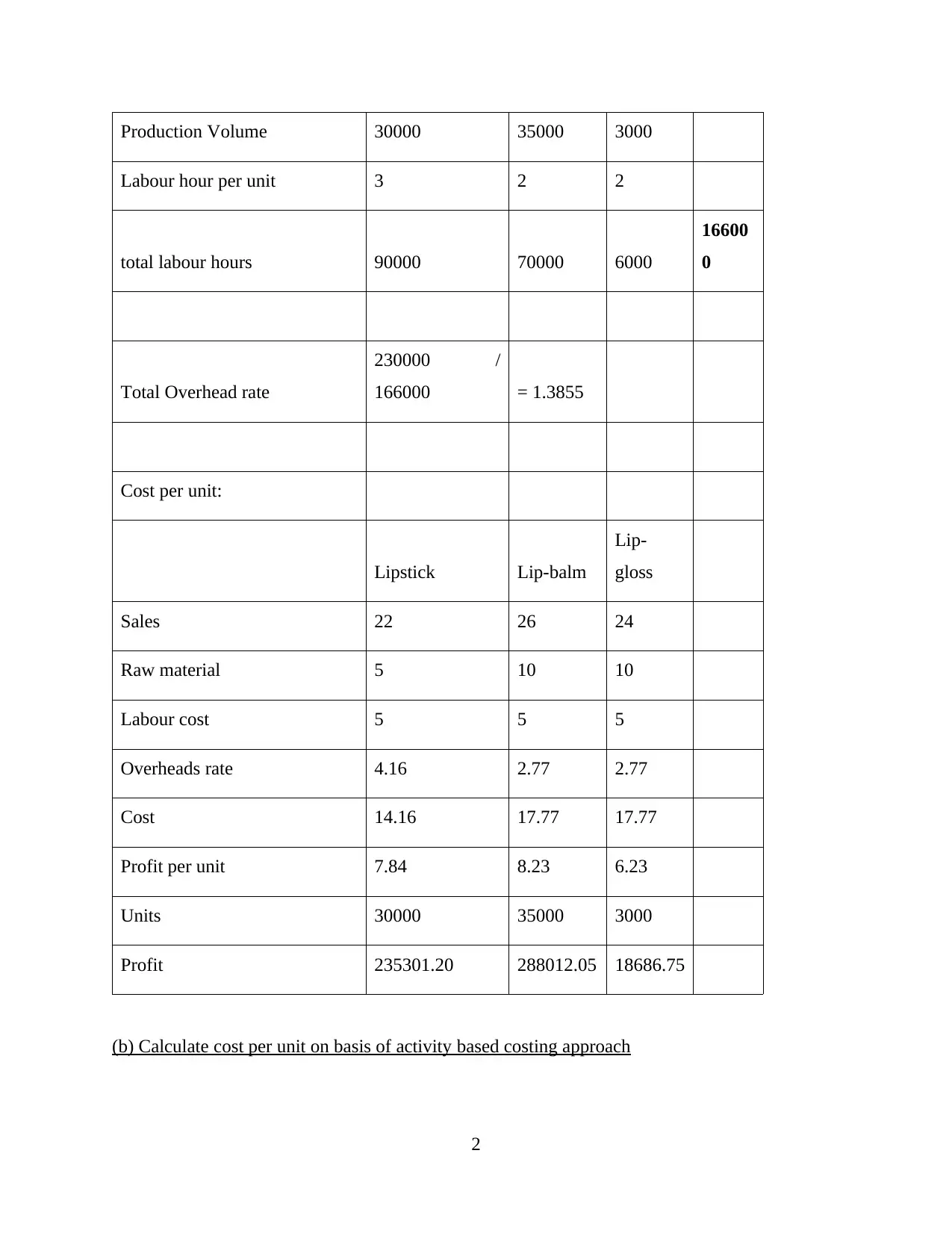

Production Volume 30000 35000 3000

Labour hour per unit 3 2 2

total labour hours 90000 70000 6000

16600

0

Total Overhead rate

230000 /

166000 = 1.3855

Cost per unit:

Lipstick Lip-balm

Lip-

gloss

Sales 22 26 24

Raw material 5 10 10

Labour cost 5 5 5

Overheads rate 4.16 2.77 2.77

Cost 14.16 17.77 17.77

Profit per unit 7.84 8.23 6.23

Units 30000 35000 3000

Profit 235301.20 288012.05 18686.75

(b) Calculate cost per unit on basis of activity based costing approach

2

Labour hour per unit 3 2 2

total labour hours 90000 70000 6000

16600

0

Total Overhead rate

230000 /

166000 = 1.3855

Cost per unit:

Lipstick Lip-balm

Lip-

gloss

Sales 22 26 24

Raw material 5 10 10

Labour cost 5 5 5

Overheads rate 4.16 2.77 2.77

Cost 14.16 17.77 17.77

Profit per unit 7.84 8.23 6.23

Units 30000 35000 3000

Profit 235301.20 288012.05 18686.75

(b) Calculate cost per unit on basis of activity based costing approach

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

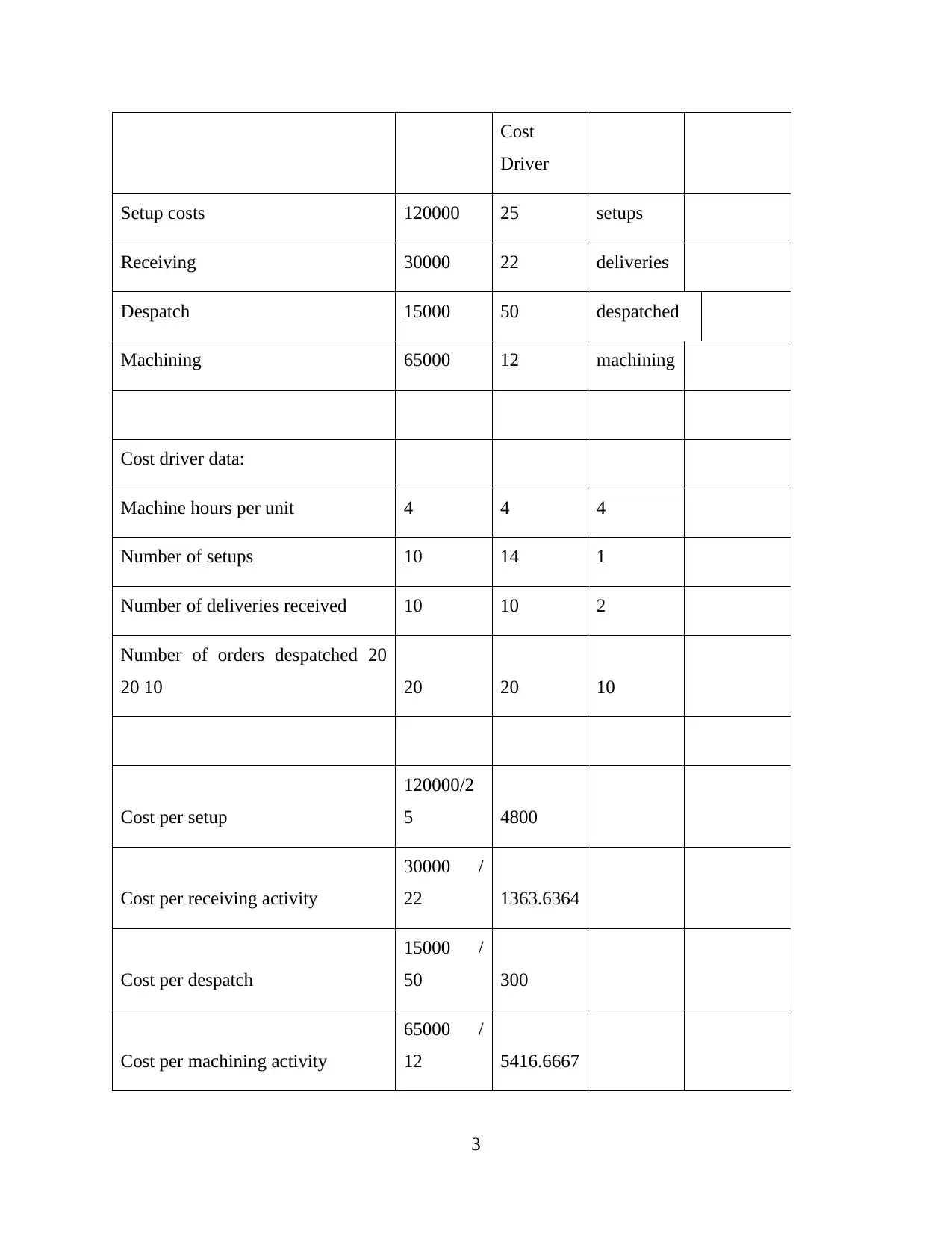

Cost

Driver

Setup costs 120000 25 setups

Receiving 30000 22 deliveries

Despatch 15000 50 despatched

Machining 65000 12 machining

Cost driver data:

Machine hours per unit 4 4 4

Number of setups 10 14 1

Number of deliveries received 10 10 2

Number of orders despatched 20

20 10 20 20 10

Cost per setup

120000/2

5 4800

Cost per receiving activity

30000 /

22 1363.6364

Cost per despatch

15000 /

50 300

Cost per machining activity

65000 /

12 5416.6667

3

Driver

Setup costs 120000 25 setups

Receiving 30000 22 deliveries

Despatch 15000 50 despatched

Machining 65000 12 machining

Cost driver data:

Machine hours per unit 4 4 4

Number of setups 10 14 1

Number of deliveries received 10 10 2

Number of orders despatched 20

20 10 20 20 10

Cost per setup

120000/2

5 4800

Cost per receiving activity

30000 /

22 1363.6364

Cost per despatch

15000 /

50 300

Cost per machining activity

65000 /

12 5416.6667

3

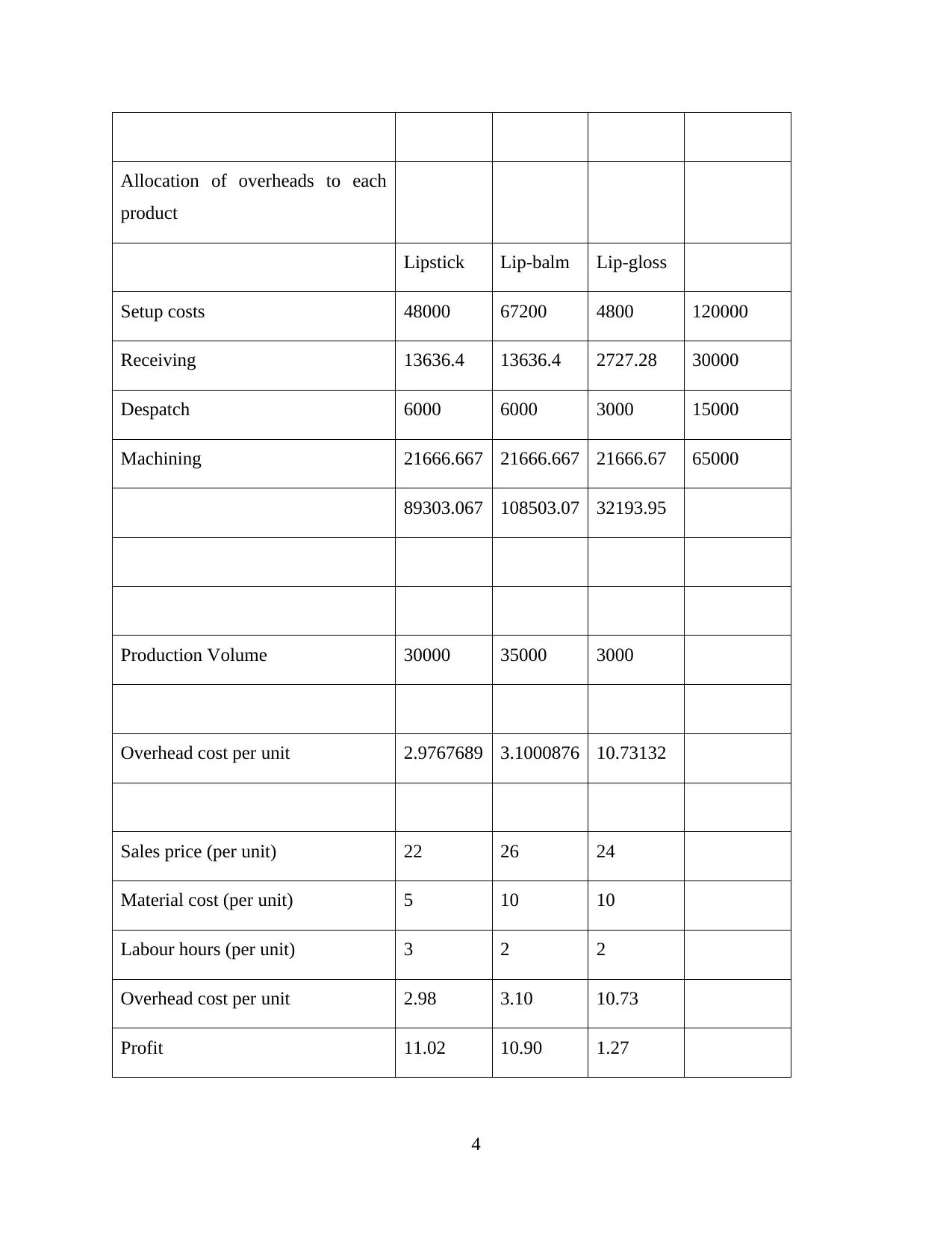

Allocation of overheads to each

product

Lipstick Lip-balm Lip-gloss

Setup costs 48000 67200 4800 120000

Receiving 13636.4 13636.4 2727.28 30000

Despatch 6000 6000 3000 15000

Machining 21666.667 21666.667 21666.67 65000

89303.067 108503.07 32193.95

Production Volume 30000 35000 3000

Overhead cost per unit 2.9767689 3.1000876 10.73132

Sales price (per unit) 22 26 24

Material cost (per unit) 5 10 10

Labour hours (per unit) 3 2 2

Overhead cost per unit 2.98 3.10 10.73

Profit 11.02 10.90 1.27

4

product

Lipstick Lip-balm Lip-gloss

Setup costs 48000 67200 4800 120000

Receiving 13636.4 13636.4 2727.28 30000

Despatch 6000 6000 3000 15000

Machining 21666.667 21666.667 21666.67 65000

89303.067 108503.07 32193.95

Production Volume 30000 35000 3000

Overhead cost per unit 2.9767689 3.1000876 10.73132

Sales price (per unit) 22 26 24

Material cost (per unit) 5 10 10

Labour hours (per unit) 3 2 2

Overhead cost per unit 2.98 3.10 10.73

Profit 11.02 10.90 1.27

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(c) Analysis results on basis of labour hours and activity based costing approach

As per the above calculation it has been analysis that for cost per unit apply two methods

labour hours and activity based costing approach. After the calculation get different results from

both approach as per the labour per hour get results 7.84, 8.23 and 6.23 respectively. On the

other side by application of activity approach get outcomes 11.02, 10.90 and 1.27 respectively.

According to calculation is is analysed that two approaches contain various accumulation

of products and quantities. There is identifying the value of absorption of three products is

235301, 288012 and 18686. On the other side the cost per unit gain for ABC is 11.02, 10.90 and

1.27 respectively.

When apply absorption cost so for the calculation consist of different product expenditure

such as fixed overhead cost, utility costs and warehouse losses in factory. There are consisting of

different cost such as direct materials, labours and overhead expenditure like wages of the site

manager and corporate taxes. These items supports to analysis of actual profitability and less

from the amount of sales. In this method require to allocation of fixed production overhead as

expenditure of item and help in product selection decision making. Moreover, Absorption

costing provides a weak valuation of actual cost of manufacturing each product (Zhou, Mavondo

and Saunders, 2019).

Activity based technique use for accurate distribution of overhead costs by attributing

them of operations. All the cost allocation based on the operations with particular objectivity.

The concept would be based on the reduce overhead cost in adverse manner. ABC functions well

in typical situations where lot of devices and items are not easy to figure out. Such as there is no

simplified value of setting where manufacturing cycles are cut down. There are many

applications for the information that based on the ABC approach. On the other side, the detail

would only be approachable when develop a method in regard of particular collection of details

and it will help in decision making procedure. When an entity can use standardized ABC

structure after that taking decision so it is finding that there is not required of sufficient data. At

the end the structure is based on the procedure and collect cost benefit study based on the choices

and endorse with the cost of system and provide benefit information for optimal results.

Moreover, overall analysis presents that activity based method use for the critical evaluation

(Van Vu and et.al, 2018).

5

As per the above calculation it has been analysis that for cost per unit apply two methods

labour hours and activity based costing approach. After the calculation get different results from

both approach as per the labour per hour get results 7.84, 8.23 and 6.23 respectively. On the

other side by application of activity approach get outcomes 11.02, 10.90 and 1.27 respectively.

According to calculation is is analysed that two approaches contain various accumulation

of products and quantities. There is identifying the value of absorption of three products is

235301, 288012 and 18686. On the other side the cost per unit gain for ABC is 11.02, 10.90 and

1.27 respectively.

When apply absorption cost so for the calculation consist of different product expenditure

such as fixed overhead cost, utility costs and warehouse losses in factory. There are consisting of

different cost such as direct materials, labours and overhead expenditure like wages of the site

manager and corporate taxes. These items supports to analysis of actual profitability and less

from the amount of sales. In this method require to allocation of fixed production overhead as

expenditure of item and help in product selection decision making. Moreover, Absorption

costing provides a weak valuation of actual cost of manufacturing each product (Zhou, Mavondo

and Saunders, 2019).

Activity based technique use for accurate distribution of overhead costs by attributing

them of operations. All the cost allocation based on the operations with particular objectivity.

The concept would be based on the reduce overhead cost in adverse manner. ABC functions well

in typical situations where lot of devices and items are not easy to figure out. Such as there is no

simplified value of setting where manufacturing cycles are cut down. There are many

applications for the information that based on the ABC approach. On the other side, the detail

would only be approachable when develop a method in regard of particular collection of details

and it will help in decision making procedure. When an entity can use standardized ABC

structure after that taking decision so it is finding that there is not required of sufficient data. At

the end the structure is based on the procedure and collect cost benefit study based on the choices

and endorse with the cost of system and provide benefit information for optimal results.

Moreover, overall analysis presents that activity based method use for the critical evaluation

(Van Vu and et.al, 2018).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(d) Sensitivity analysis help managers to cope with uncertainties

Sensitivity analysis is a model of outcomes to shift input details and forecast of potential

cash flows that mainly depend on the future activities, revenues, behaviours, payments. The flow

in particular calculations will impact on the importance on the predication. Some input data can

be deducted on the basis of research and conduct more data collection as well as analysis. Before

spending amount and time to collect extra data for the development and estimate system

performance for the reduction in the uncertainty and it is related with the outcomes when all data

and model uncertainties could be deducted if not necessitate. This analysis define about the

different independent variables that impact on single factor activities. For the analysis require a

prepare a strategy that use for target parameters are impacted on the outer expression

modification known as input consideration (Jaskyte, 2020).

The particular model is categorised into mathematical model and a manner of analysing

results that depend on the parameters number. This analytical method analysis on basis of

various variables that impact on the outcomes through developing a series of variables. The

observer investigate about the major modification and output signal impact on the objective.

Sensitivity can be analysed the values of shares of public organisations and consist of

market profits, portfolio figures, number of competing competitors on the sector and various

variables impacts on the equity prices. There are study about the assets values can be refined by

selecting different assumptions and adding more multiple parameters. The evaluation helps to

management to determine the different elements that will impact on the outcomes as reduction in

cost of investment. As a result it will impact on the net profitability and analysis to put up with

risks carry out in new business entity after conducting sensitivity analysis. It is a way of analysis

circumstances that different from the centre anticipate. It is intended to observing of degree of

risks of the activity that enable to analysis the results that based on the consistency of inputs

(Wang, Akbar and Akbar, 2020).

QUESTION 2

(a) Calculation of variances

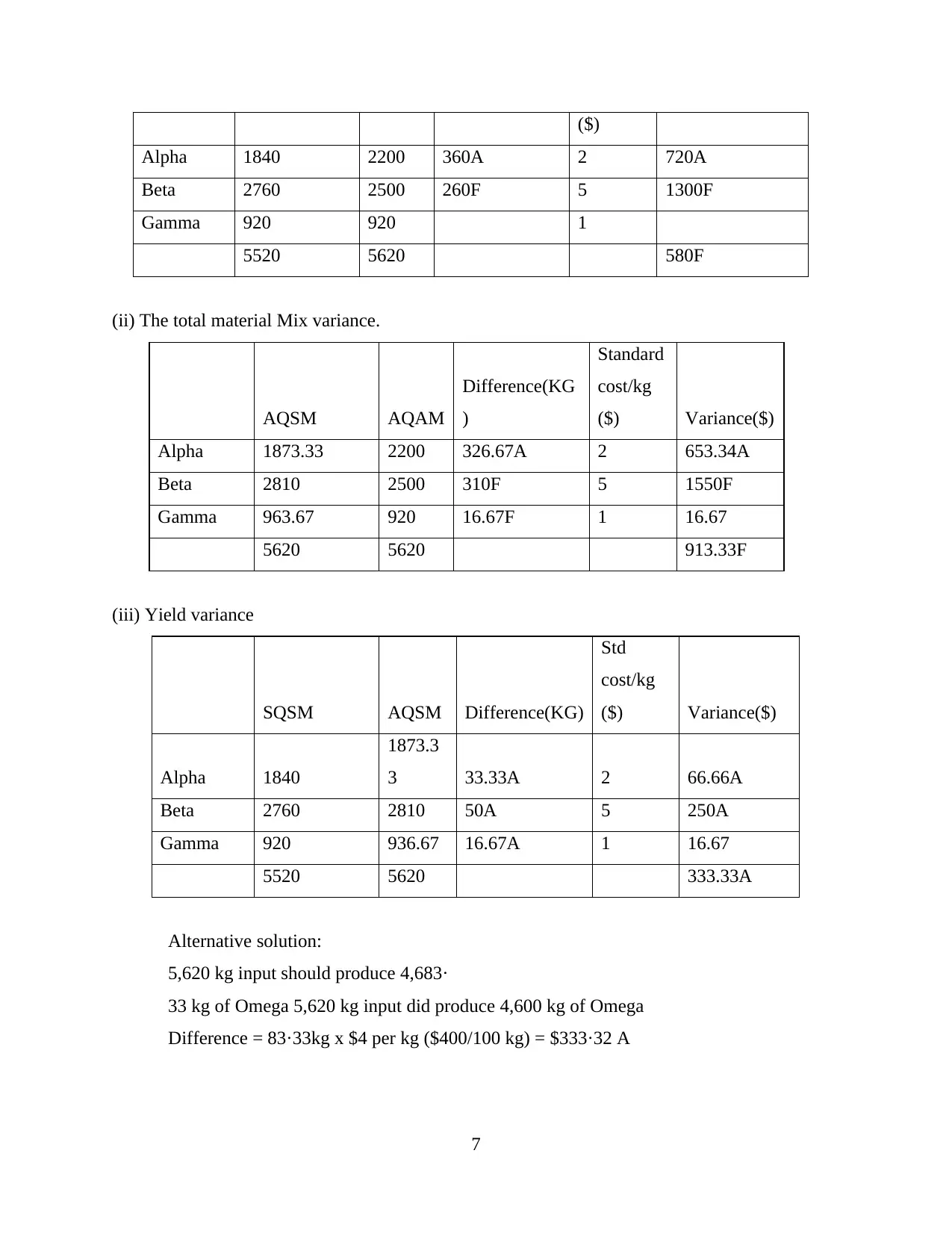

(i) the material usage variance for each ingredient and in total

Should use

(KG)

Did use

(KG)

Difference(KG

)

Standard

cost/kg

Variance($)

6

Sensitivity analysis is a model of outcomes to shift input details and forecast of potential

cash flows that mainly depend on the future activities, revenues, behaviours, payments. The flow

in particular calculations will impact on the importance on the predication. Some input data can

be deducted on the basis of research and conduct more data collection as well as analysis. Before

spending amount and time to collect extra data for the development and estimate system

performance for the reduction in the uncertainty and it is related with the outcomes when all data

and model uncertainties could be deducted if not necessitate. This analysis define about the

different independent variables that impact on single factor activities. For the analysis require a

prepare a strategy that use for target parameters are impacted on the outer expression

modification known as input consideration (Jaskyte, 2020).

The particular model is categorised into mathematical model and a manner of analysing

results that depend on the parameters number. This analytical method analysis on basis of

various variables that impact on the outcomes through developing a series of variables. The

observer investigate about the major modification and output signal impact on the objective.

Sensitivity can be analysed the values of shares of public organisations and consist of

market profits, portfolio figures, number of competing competitors on the sector and various

variables impacts on the equity prices. There are study about the assets values can be refined by

selecting different assumptions and adding more multiple parameters. The evaluation helps to

management to determine the different elements that will impact on the outcomes as reduction in

cost of investment. As a result it will impact on the net profitability and analysis to put up with

risks carry out in new business entity after conducting sensitivity analysis. It is a way of analysis

circumstances that different from the centre anticipate. It is intended to observing of degree of

risks of the activity that enable to analysis the results that based on the consistency of inputs

(Wang, Akbar and Akbar, 2020).

QUESTION 2

(a) Calculation of variances

(i) the material usage variance for each ingredient and in total

Should use

(KG)

Did use

(KG)

Difference(KG

)

Standard

cost/kg

Variance($)

6

($)

Alpha 1840 2200 360A 2 720A

Beta 2760 2500 260F 5 1300F

Gamma 920 920 1

5520 5620 580F

(ii) The total material Mix variance.

AQSM AQAM

Difference(KG

)

Standard

cost/kg

($) Variance($)

Alpha 1873.33 2200 326.67A 2 653.34A

Beta 2810 2500 310F 5 1550F

Gamma 963.67 920 16.67F 1 16.67

5620 5620 913.33F

(iii) Yield variance

SQSM AQSM Difference(KG)

Std

cost/kg

($) Variance($)

Alpha 1840

1873.3

3 33.33A 2 66.66A

Beta 2760 2810 50A 5 250A

Gamma 920 936.67 16.67A 1 16.67

5520 5620 333.33A

Alternative solution:

5,620 kg input should produce 4,683·

33 kg of Omega 5,620 kg input did produce 4,600 kg of Omega

Difference = 83·33kg x $4 per kg ($400/100 kg) = $333·32 A

7

Alpha 1840 2200 360A 2 720A

Beta 2760 2500 260F 5 1300F

Gamma 920 920 1

5520 5620 580F

(ii) The total material Mix variance.

AQSM AQAM

Difference(KG

)

Standard

cost/kg

($) Variance($)

Alpha 1873.33 2200 326.67A 2 653.34A

Beta 2810 2500 310F 5 1550F

Gamma 963.67 920 16.67F 1 16.67

5620 5620 913.33F

(iii) Yield variance

SQSM AQSM Difference(KG)

Std

cost/kg

($) Variance($)

Alpha 1840

1873.3

3 33.33A 2 66.66A

Beta 2760 2810 50A 5 250A

Gamma 920 936.67 16.67A 1 16.67

5520 5620 333.33A

Alternative solution:

5,620 kg input should produce 4,683·

33 kg of Omega 5,620 kg input did produce 4,600 kg of Omega

Difference = 83·33kg x $4 per kg ($400/100 kg) = $333·32 A

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(b) Problems with current system of calculating and reporting variances

As per the analysis it is defined that raw material variances outsider range of

manufacturing and for this mainly responsible purchase manager. Along with production

manager of the organisation is not consideration in regard of the daily blend. For the

administration is is require to analysis different variances but can not observing. It is required for

the planning variations as they can not analysis. Price levels and efficiency of three items is

being variable and the use of prices as per the necessities for mixing yield.

For the improvements in quality and prices of materials based on basic mixture and

substance has not increased in 5 years. It is becoming the reason of undertake control activity

that based on the different variances and set outdated standards. Since kappa company does not

currently have any reviews and comments due to less true images and become the reason of

success of manufacturing manager. Although Kappa co doesn't put and impact on different

variations to capable for the observing cost and becoming complacent (Mishra and Mohanty,

2018).

It is indicating that overall utilisation of variances stated that favourable variances are

$580 that presents effective efficiency of the business. Along with presents variation in more

depth means mixture and yielding measurement can be found as per the motivation of the shirt in

mix. There is presenting clear relation in between material mixture variation as well as yield

variation.

QUESTION 3

Critically discussed neither ZBB nor the IB provides the perfect toll for planning coordination

and control

Zero-based budgeting is a budget which starts from zero and this is not related to past

budget. The purpose of this budgeting is to calculate the actual expenses to be incurred in the

period. It helps the company to look on the present number not on the past number. It involves

the employees to make decision and improve the collaboration and communication in the

organisation. It helps the company to save money and generate profit for the period by evaluating

the unneeded expenses in the business which can be terminated.

On the other side, Incremental budgeting is the budget which is prepared from the current

budget as a base and add the increment amount in the new budget period. In this budget,

8

As per the analysis it is defined that raw material variances outsider range of

manufacturing and for this mainly responsible purchase manager. Along with production

manager of the organisation is not consideration in regard of the daily blend. For the

administration is is require to analysis different variances but can not observing. It is required for

the planning variations as they can not analysis. Price levels and efficiency of three items is

being variable and the use of prices as per the necessities for mixing yield.

For the improvements in quality and prices of materials based on basic mixture and

substance has not increased in 5 years. It is becoming the reason of undertake control activity

that based on the different variances and set outdated standards. Since kappa company does not

currently have any reviews and comments due to less true images and become the reason of

success of manufacturing manager. Although Kappa co doesn't put and impact on different

variations to capable for the observing cost and becoming complacent (Mishra and Mohanty,

2018).

It is indicating that overall utilisation of variances stated that favourable variances are

$580 that presents effective efficiency of the business. Along with presents variation in more

depth means mixture and yielding measurement can be found as per the motivation of the shirt in

mix. There is presenting clear relation in between material mixture variation as well as yield

variation.

QUESTION 3

Critically discussed neither ZBB nor the IB provides the perfect toll for planning coordination

and control

Zero-based budgeting is a budget which starts from zero and this is not related to past

budget. The purpose of this budgeting is to calculate the actual expenses to be incurred in the

period. It helps the company to look on the present number not on the past number. It involves

the employees to make decision and improve the collaboration and communication in the

organisation. It helps the company to save money and generate profit for the period by evaluating

the unneeded expenses in the business which can be terminated.

On the other side, Incremental budgeting is the budget which is prepared from the current

budget as a base and add the increment amount in the new budget period. In this budget,

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

companies can terminate competitors or create the value of equal opportunities among the units

and same amount to enhance from the past year (Cherian and et.al, 2019).

Zero based budgeting do not consider the past year budget, it starts from zero and funds

assigned to each units are justified related to the expenses of that period whereas incremental

budgeting is prepared for the current year from taking the base of the previous year budget.

Zero-based budgeting prepared by assigning the highest funds to those business activities which

benefit the company. Zero-based budgeting is time consuming because this budget is starts from

zero and takes time to prepare the budget from current activities. Incremental budgeting takes

less time to prepare because current budget is computed from previous budget.

Zero based budgeting requires knowledge and skills to prepare the budget and in

incremental it is easy to prepare because it does not require training for preparing budget. Zero

based budgeting takes incurred cost to formulate the budget because it is prepared from starting

and incremental does not require any cost to formulate the budget. Zero based budgeting

decrease the possibility of threat and misconception in the activities because it evaluates the

budget from the base and in incremental does not apply much attention to the process in an

activity because it add or subtract from the past budget (Gao, Yang and Hafsi, 2019).

CONCLUSION

As per the above report it has been concluded that financial management performance is

a way in which manage and analysis the financial outcomes across an entity. The main reason of

the management to compare real values for budgets and estimate and make adjustments

accordingly. In this report analysis of material variances and labour variances on the basis of

different approach after that get different results effectively.

9

and same amount to enhance from the past year (Cherian and et.al, 2019).

Zero based budgeting do not consider the past year budget, it starts from zero and funds

assigned to each units are justified related to the expenses of that period whereas incremental

budgeting is prepared for the current year from taking the base of the previous year budget.

Zero-based budgeting prepared by assigning the highest funds to those business activities which

benefit the company. Zero-based budgeting is time consuming because this budget is starts from

zero and takes time to prepare the budget from current activities. Incremental budgeting takes

less time to prepare because current budget is computed from previous budget.

Zero based budgeting requires knowledge and skills to prepare the budget and in

incremental it is easy to prepare because it does not require training for preparing budget. Zero

based budgeting takes incurred cost to formulate the budget because it is prepared from starting

and incremental does not require any cost to formulate the budget. Zero based budgeting

decrease the possibility of threat and misconception in the activities because it evaluates the

budget from the base and in incremental does not apply much attention to the process in an

activity because it add or subtract from the past budget (Gao, Yang and Hafsi, 2019).

CONCLUSION

As per the above report it has been concluded that financial management performance is

a way in which manage and analysis the financial outcomes across an entity. The main reason of

the management to compare real values for budgets and estimate and make adjustments

accordingly. In this report analysis of material variances and labour variances on the basis of

different approach after that get different results effectively.

9

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.