Introduction to Accounting and Finance: Performance Analysis Report

VerifiedAdded on 2022/12/19

|23

|4739

|88

Report

AI Summary

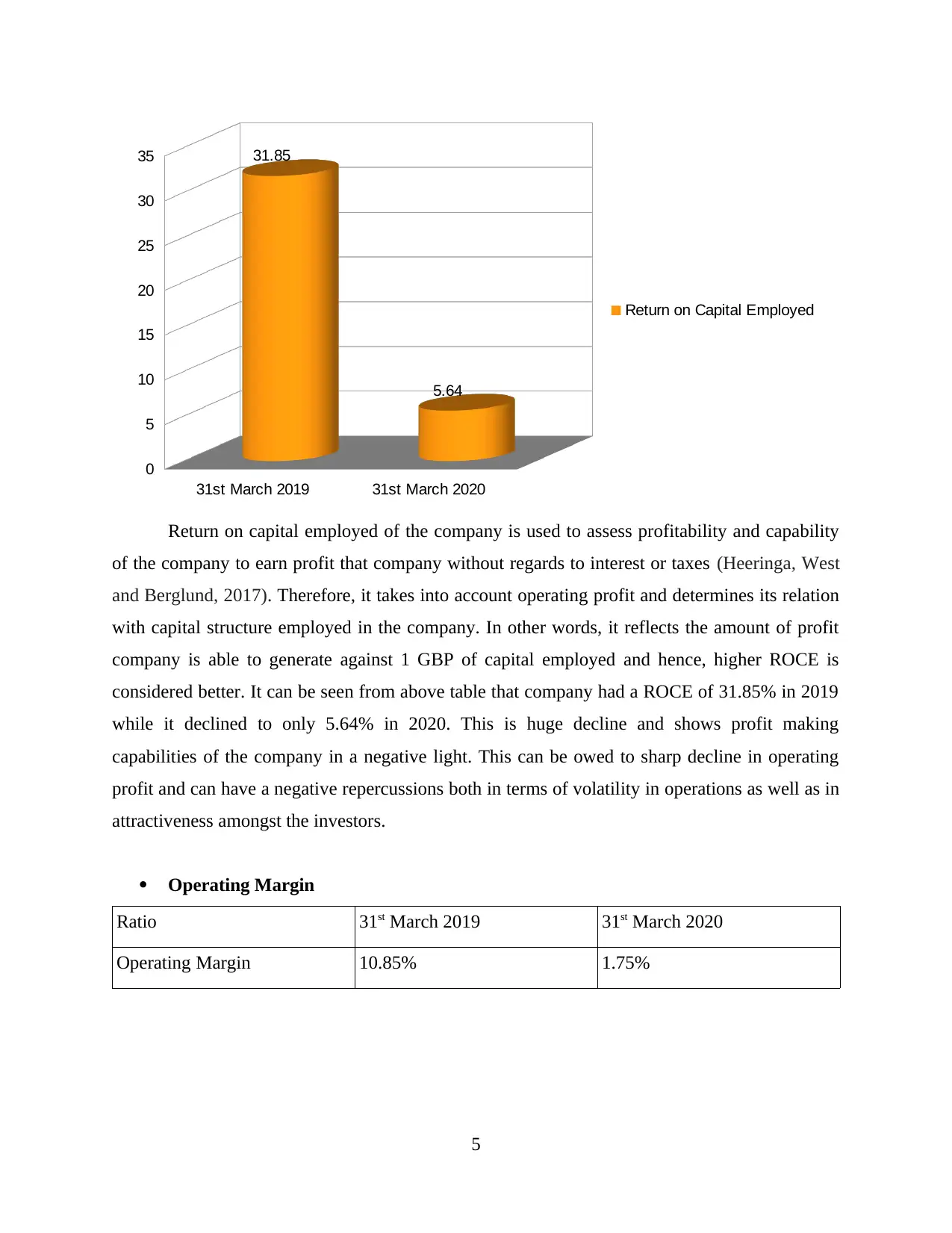

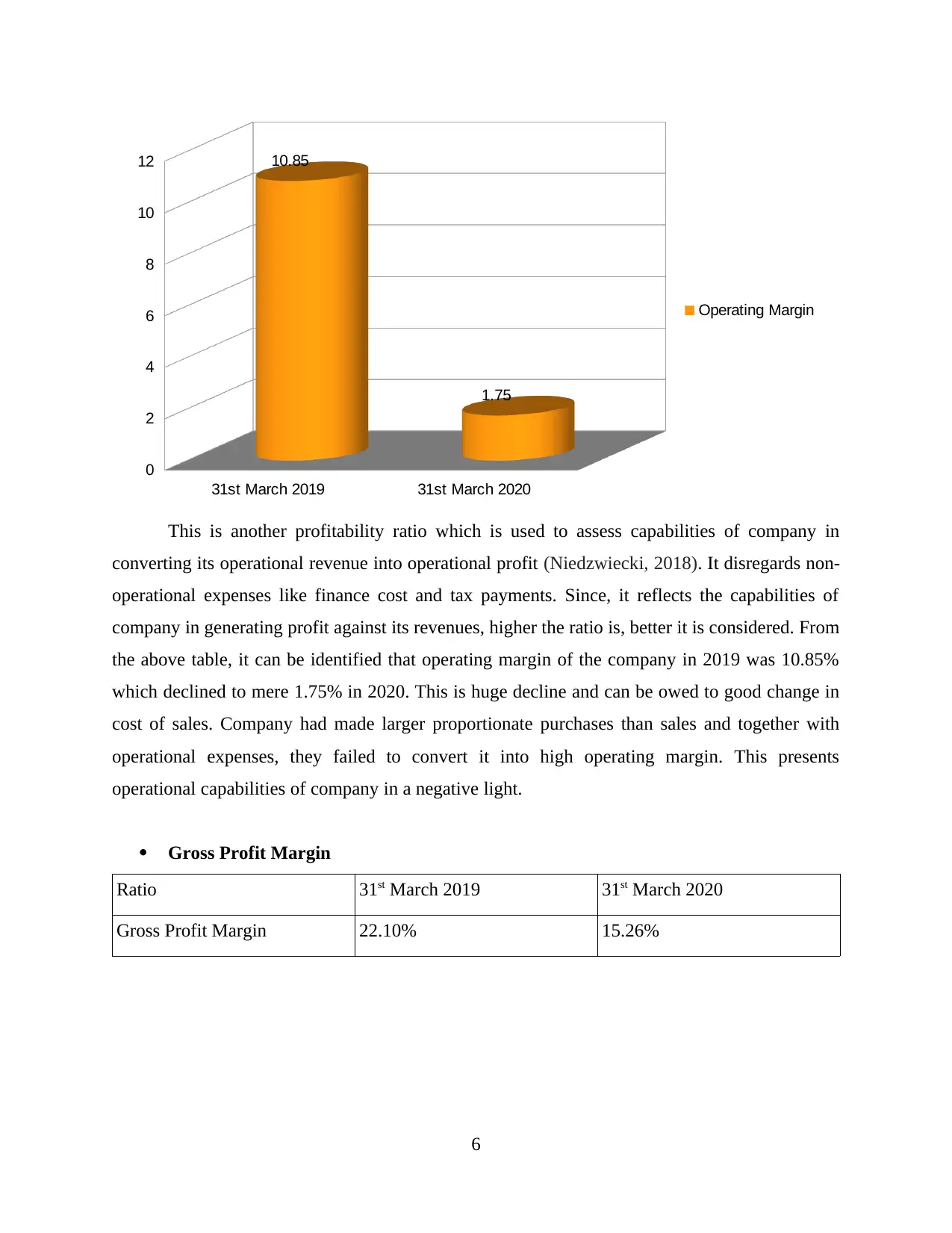

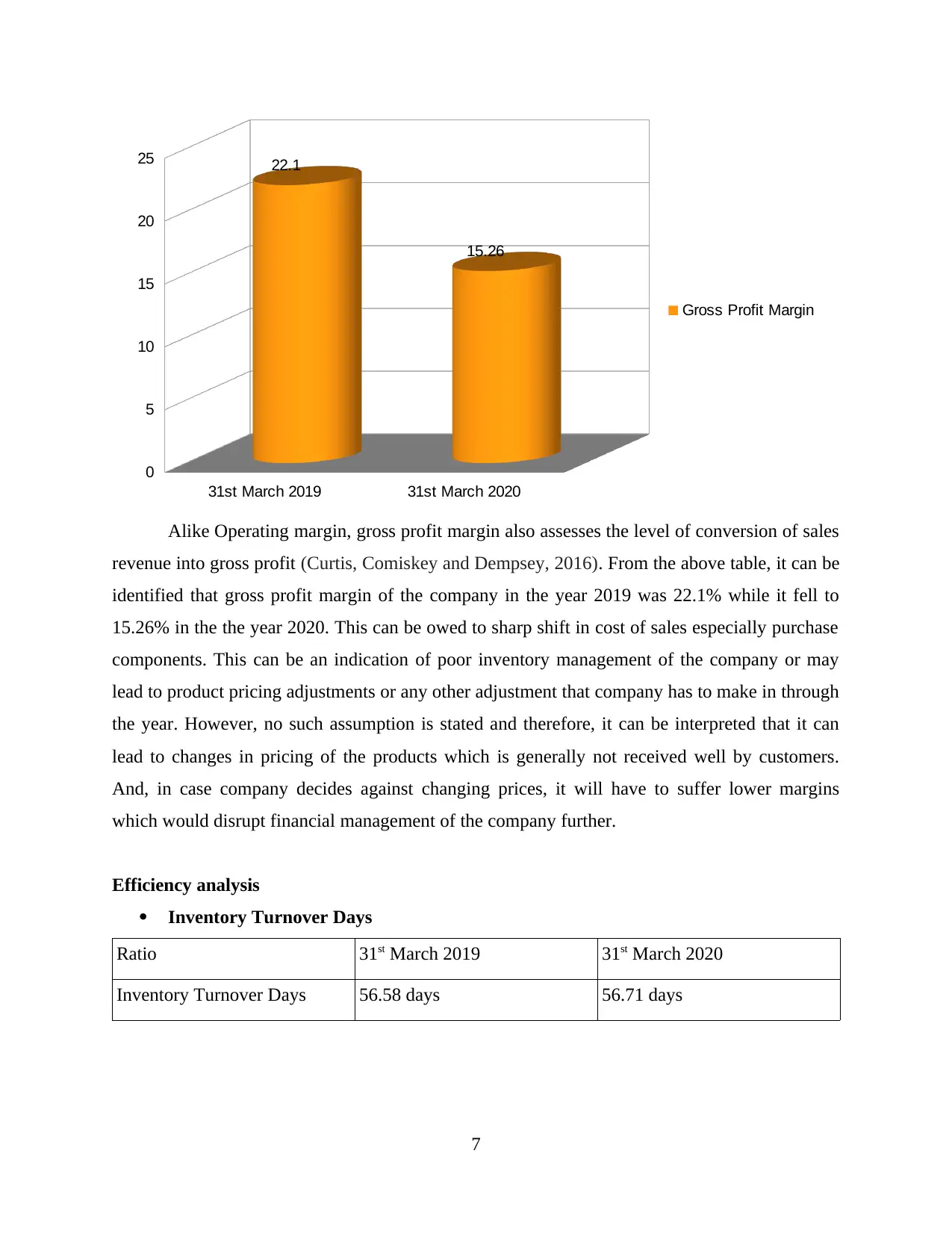

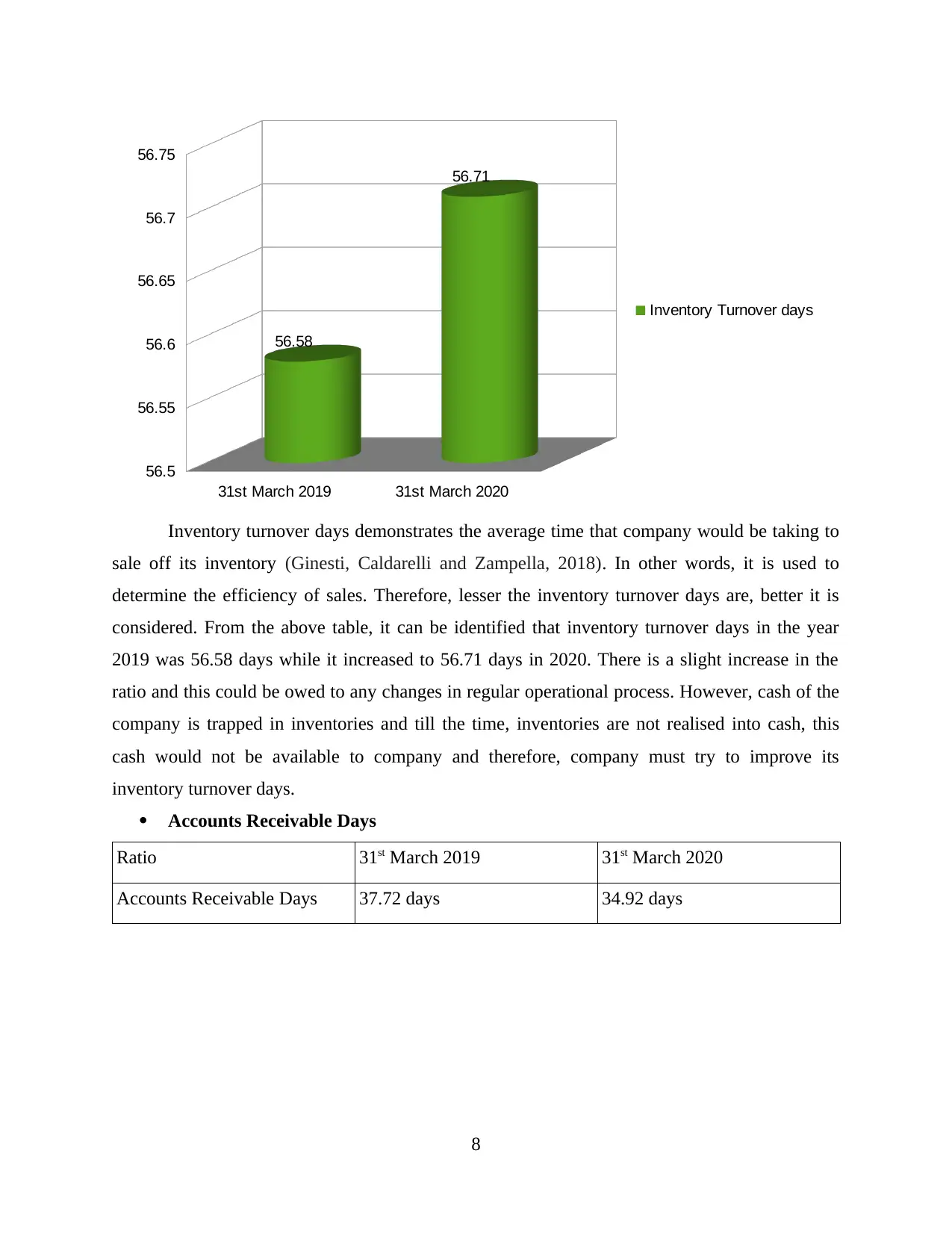

This report provides a comprehensive analysis of financial performance using ratio analysis, focusing on the financial statements of Gray Plc. It examines profitability, efficiency, liquidity, and investment abilities through various ratios, including ROCE, operating margin, gross profit margin, inventory turnover, accounts receivable and payable days, current and acid-test ratios, earnings per share, and price-earnings ratio. The report also includes a section on budgetary control systems, identifying their objectives and exploring the concept of participative budgeting in relation to these objectives for Great Manor Plc. The analysis covers the years 2019 and 2020, offering insights into the financial health and operational efficiency of the companies, and assessing the impact of changes in financial metrics. The report concludes by summarizing the key findings and implications of the financial analysis and budgetary control systems.

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.