Financial Analysis of Crown Resorts Limited: Accounting for Business

VerifiedAdded on 2021/06/15

|14

|2445

|24

Report

AI Summary

This report assesses the financial performance of Crown Resorts Limited, an Australian public listed entity in the integrated resorts sector, by analyzing its financial statements. The report focuses on key financial ratios, including quick ratio, gross profit margin, return on equity, debt-to-equity ratio, and days inventory, to evaluate Crown Resorts' financial health. A comparative analysis is also conducted with Tatts Group Limited, a major competitor, using gross margin, quick ratio, and debt-to-equity ratio. The analysis reveals that Crown Resorts Limited demonstrates a stronger financial position and performance compared to Tatts Group Limited in the Australian market, based on the selected financial ratios. The report highlights the significance of these ratios in understanding the company's liquidity, profitability, solvency, and efficiency, providing valuable insights into its financial standing and competitive advantage.

Running head: ACCOUNTING FOR BUSINESS

Accounting for Business

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Accounting for Business

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING FOR BUSINESS

Executive Summary:

The current report aims to assess the financial performance of an Australian public

listed entity based on its financial statements for the past years. For meeting the purpose of

this report, Crown Resorts Limited is selected as the entity operating in the integrated resorts

sector and it is listed in ASX under the code CNW. For extending the scope of this particular

report, comparison is made with one of the major competitors of Crown Resorts, which is

Tatts Group Limited with the ASX code of TTW. By taking into account the financial ratios,

the financial performance and position of Crown Resorts Limited is much better in contrast to

Tatts Group Limited in the Australian market.

Executive Summary:

The current report aims to assess the financial performance of an Australian public

listed entity based on its financial statements for the past years. For meeting the purpose of

this report, Crown Resorts Limited is selected as the entity operating in the integrated resorts

sector and it is listed in ASX under the code CNW. For extending the scope of this particular

report, comparison is made with one of the major competitors of Crown Resorts, which is

Tatts Group Limited with the ASX code of TTW. By taking into account the financial ratios,

the financial performance and position of Crown Resorts Limited is much better in contrast to

Tatts Group Limited in the Australian market.

2ACCOUNTING FOR BUSINESS

Table of Contents

1.0 Introduction:.........................................................................................................................3

1.1 Purpose:............................................................................................................................3

1.2 Scope:...............................................................................................................................3

1.3 Limitations:......................................................................................................................3

2.0 Company overview of Crown Resorts Limited:..................................................................3

3.0 Ratio analysis:......................................................................................................................4

3.1 Quick ratio:.......................................................................................................................4

3.2 Gross profit margin:.........................................................................................................5

3.3 Return on equity:..............................................................................................................6

3.4 Debt to equity ratio:.........................................................................................................7

3.5 Days inventory:................................................................................................................8

4.0 Analysis and comparison of Crown Resorts Limited with Tatts Group Limited:...............9

References:...............................................................................................................................13

Table of Contents

1.0 Introduction:.........................................................................................................................3

1.1 Purpose:............................................................................................................................3

1.2 Scope:...............................................................................................................................3

1.3 Limitations:......................................................................................................................3

2.0 Company overview of Crown Resorts Limited:..................................................................3

3.0 Ratio analysis:......................................................................................................................4

3.1 Quick ratio:.......................................................................................................................4

3.2 Gross profit margin:.........................................................................................................5

3.3 Return on equity:..............................................................................................................6

3.4 Debt to equity ratio:.........................................................................................................7

3.5 Days inventory:................................................................................................................8

4.0 Analysis and comparison of Crown Resorts Limited with Tatts Group Limited:...............9

References:...............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING FOR BUSINESS

1.0 Introduction:

1.1 Purpose:

The current report aims to assess the financial performance of an Australian public

listed entity based on its financial statements for the past years. For meeting the purpose of

this report, Crown Resorts Limited is selected as the entity operating in the integrated resorts

sector and it is listed in ASX under the code CNW. The financial analysis is carried out by

taking into consideration five different financial ratios to understand the current standing of

the organisation in the Australian market.

1.2 Scope:

For extending the scope of this particular report, comparison is made with one of the

major competitors of Crown Resorts, which is Tatts Group Limited with the ASX code of

TTW. In addition, three different methods of comparison are used to determine the

organisation that is enjoying competitive advantage over the other one.

1.3 Limitations:

It has already identified that comparative analysis of the financial statements of the

two selected organisations would be made with the help of five financial ratios. However, it

is to be borne in mind that financial ratios only have the ability to depict the previous trends.

In other words, the future progress of an entity could not be predicted with the help of

financial ratios, since they do not take into consideration the effects of inflationary pressures

on the economy, changes in industrial trends along with consumer preferences. Moreover, the

ratios of only the past two years would be evaluated. If the timeframe would be five years,

more accurate overview of the financial position of both the organisations could be evaluated

in a better way.

2.0 Company overview of Crown Resorts Limited:

Crown Resorts Limited is one of the biggest gaming and entertainment groups having

market capitalisation of nearly $8.7 billion in April 2018 (Crownresorts.com.au 2018). It is

involved in fully operating and owning two leading entertainment and gaming complexes of

Australia, which are Crown Perth and Crown Melbourne. In addition, it has strong portfolio

of future projects along with complementary investments that are anchored on the part of

Crown Sydney. In addition, it provides grants to community welfare, arts, healthcare,

1.0 Introduction:

1.1 Purpose:

The current report aims to assess the financial performance of an Australian public

listed entity based on its financial statements for the past years. For meeting the purpose of

this report, Crown Resorts Limited is selected as the entity operating in the integrated resorts

sector and it is listed in ASX under the code CNW. The financial analysis is carried out by

taking into consideration five different financial ratios to understand the current standing of

the organisation in the Australian market.

1.2 Scope:

For extending the scope of this particular report, comparison is made with one of the

major competitors of Crown Resorts, which is Tatts Group Limited with the ASX code of

TTW. In addition, three different methods of comparison are used to determine the

organisation that is enjoying competitive advantage over the other one.

1.3 Limitations:

It has already identified that comparative analysis of the financial statements of the

two selected organisations would be made with the help of five financial ratios. However, it

is to be borne in mind that financial ratios only have the ability to depict the previous trends.

In other words, the future progress of an entity could not be predicted with the help of

financial ratios, since they do not take into consideration the effects of inflationary pressures

on the economy, changes in industrial trends along with consumer preferences. Moreover, the

ratios of only the past two years would be evaluated. If the timeframe would be five years,

more accurate overview of the financial position of both the organisations could be evaluated

in a better way.

2.0 Company overview of Crown Resorts Limited:

Crown Resorts Limited is one of the biggest gaming and entertainment groups having

market capitalisation of nearly $8.7 billion in April 2018 (Crownresorts.com.au 2018). It is

involved in fully operating and owning two leading entertainment and gaming complexes of

Australia, which are Crown Perth and Crown Melbourne. In addition, it has strong portfolio

of future projects along with complementary investments that are anchored on the part of

Crown Sydney. In addition, it provides grants to community welfare, arts, healthcare,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING FOR BUSINESS

education and environment by contributing above $100 million over ten years to aid in

community projects in Australia.

3.0 Ratio analysis:

The following ratios are considered in the context of Crown Resorts Limited to

measure its financial condition in the past two years:

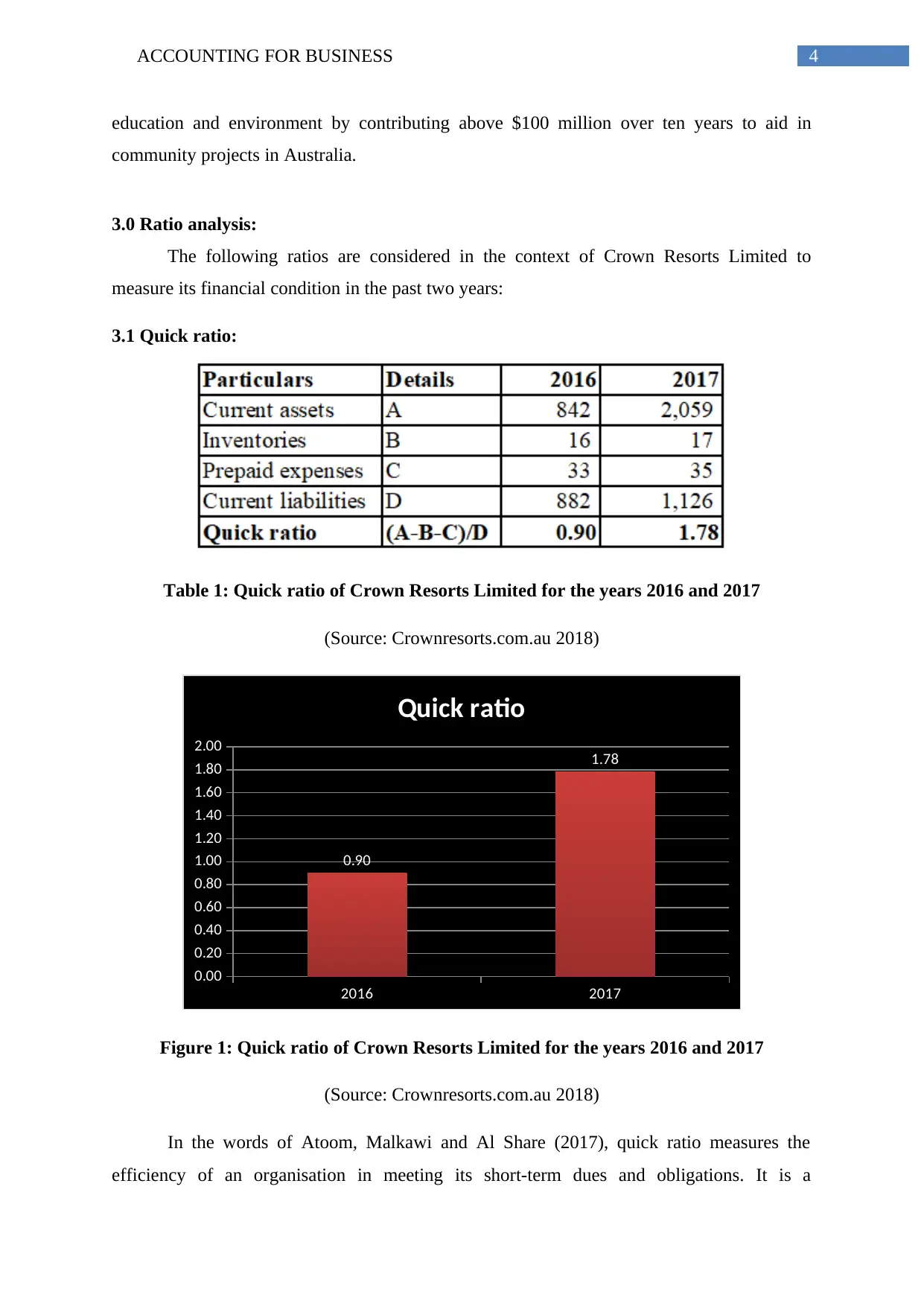

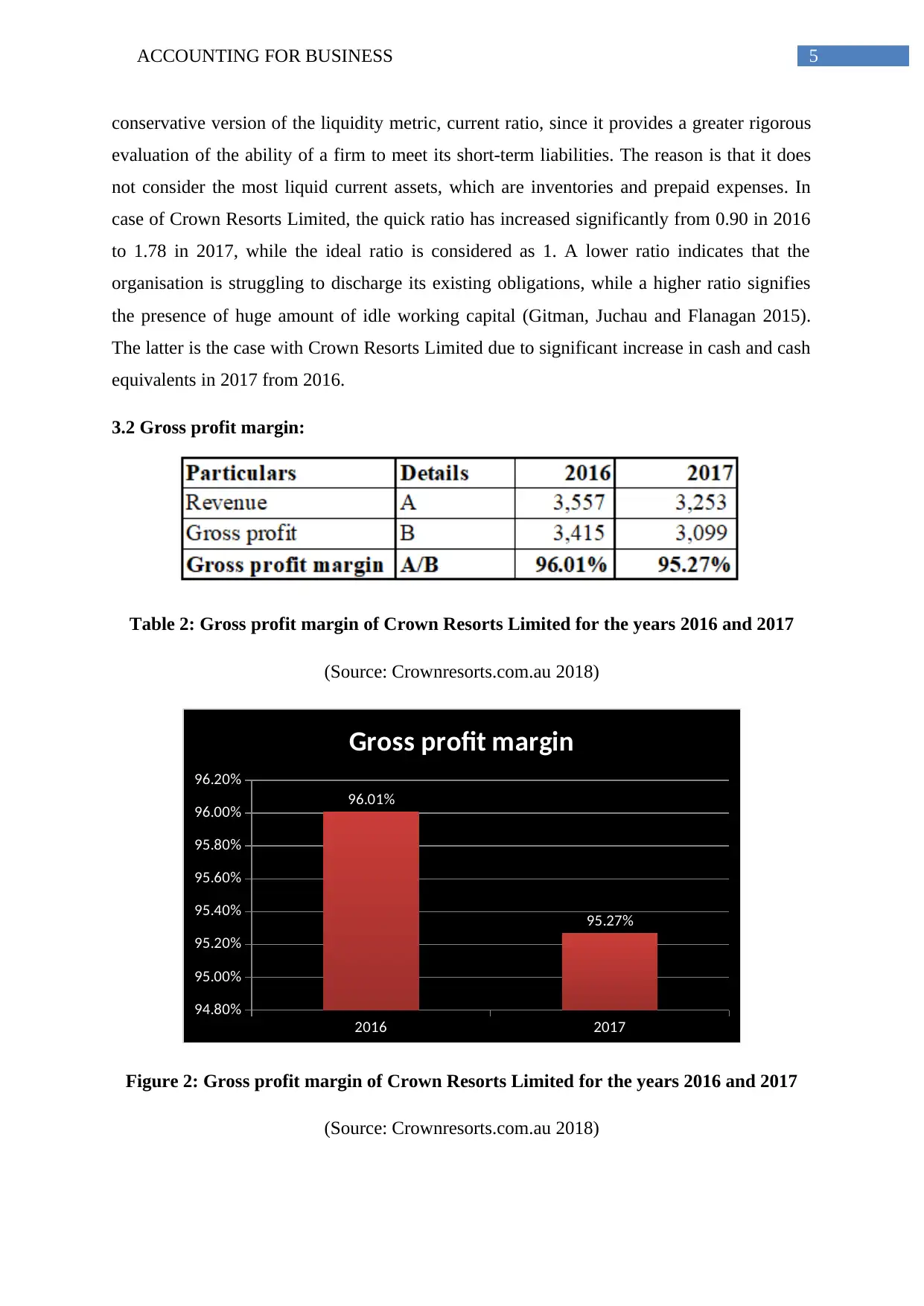

3.1 Quick ratio:

Table 1: Quick ratio of Crown Resorts Limited for the years 2016 and 2017

(Source: Crownresorts.com.au 2018)

2016 2017

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

0.90

1.78

Quick ratio

Figure 1: Quick ratio of Crown Resorts Limited for the years 2016 and 2017

(Source: Crownresorts.com.au 2018)

In the words of Atoom, Malkawi and Al Share (2017), quick ratio measures the

efficiency of an organisation in meeting its short-term dues and obligations. It is a

education and environment by contributing above $100 million over ten years to aid in

community projects in Australia.

3.0 Ratio analysis:

The following ratios are considered in the context of Crown Resorts Limited to

measure its financial condition in the past two years:

3.1 Quick ratio:

Table 1: Quick ratio of Crown Resorts Limited for the years 2016 and 2017

(Source: Crownresorts.com.au 2018)

2016 2017

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

0.90

1.78

Quick ratio

Figure 1: Quick ratio of Crown Resorts Limited for the years 2016 and 2017

(Source: Crownresorts.com.au 2018)

In the words of Atoom, Malkawi and Al Share (2017), quick ratio measures the

efficiency of an organisation in meeting its short-term dues and obligations. It is a

5ACCOUNTING FOR BUSINESS

conservative version of the liquidity metric, current ratio, since it provides a greater rigorous

evaluation of the ability of a firm to meet its short-term liabilities. The reason is that it does

not consider the most liquid current assets, which are inventories and prepaid expenses. In

case of Crown Resorts Limited, the quick ratio has increased significantly from 0.90 in 2016

to 1.78 in 2017, while the ideal ratio is considered as 1. A lower ratio indicates that the

organisation is struggling to discharge its existing obligations, while a higher ratio signifies

the presence of huge amount of idle working capital (Gitman, Juchau and Flanagan 2015).

The latter is the case with Crown Resorts Limited due to significant increase in cash and cash

equivalents in 2017 from 2016.

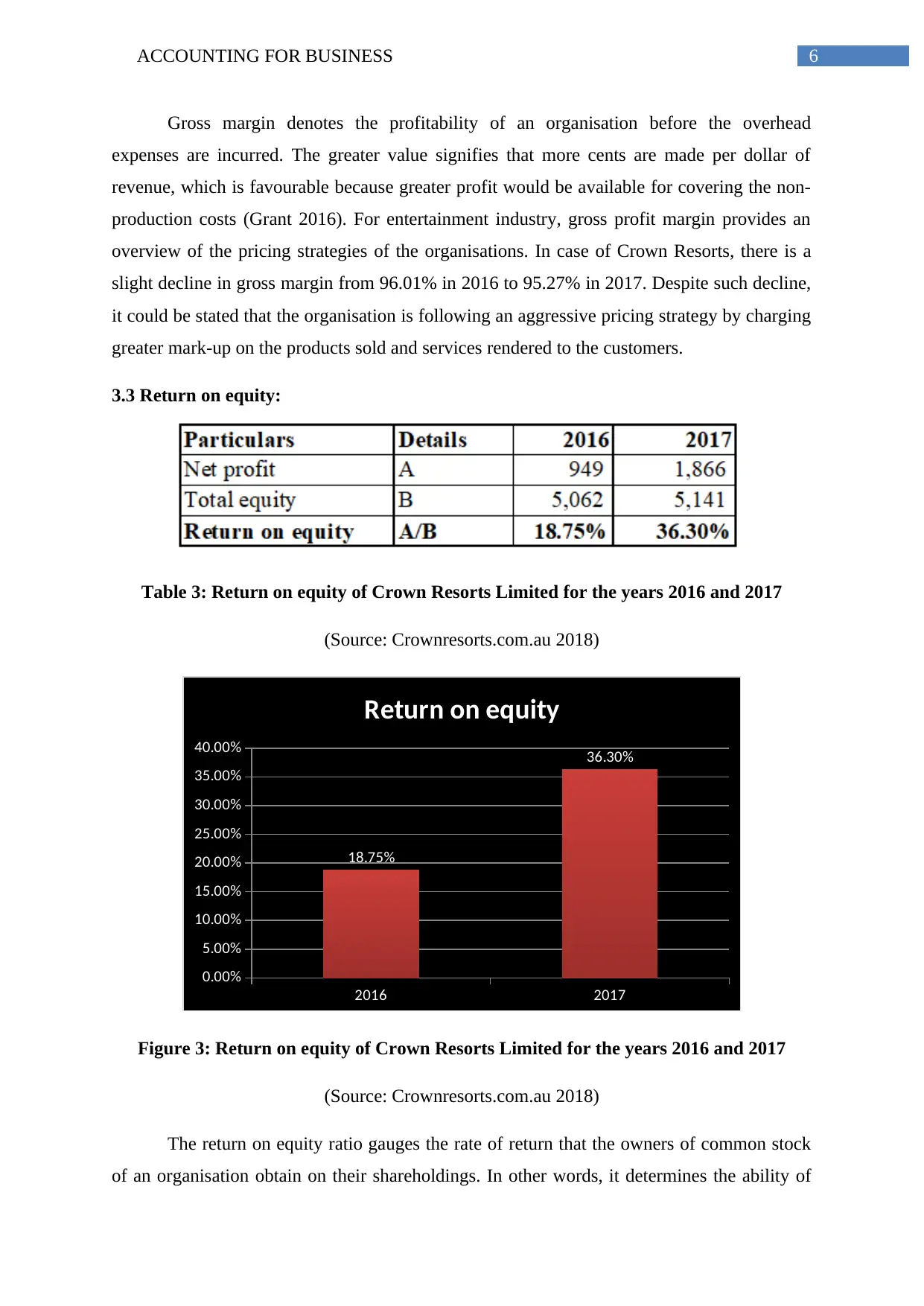

3.2 Gross profit margin:

Table 2: Gross profit margin of Crown Resorts Limited for the years 2016 and 2017

(Source: Crownresorts.com.au 2018)

2016 2017

94.80%

95.00%

95.20%

95.40%

95.60%

95.80%

96.00%

96.20%

96.01%

95.27%

Gross profit margin

Figure 2: Gross profit margin of Crown Resorts Limited for the years 2016 and 2017

(Source: Crownresorts.com.au 2018)

conservative version of the liquidity metric, current ratio, since it provides a greater rigorous

evaluation of the ability of a firm to meet its short-term liabilities. The reason is that it does

not consider the most liquid current assets, which are inventories and prepaid expenses. In

case of Crown Resorts Limited, the quick ratio has increased significantly from 0.90 in 2016

to 1.78 in 2017, while the ideal ratio is considered as 1. A lower ratio indicates that the

organisation is struggling to discharge its existing obligations, while a higher ratio signifies

the presence of huge amount of idle working capital (Gitman, Juchau and Flanagan 2015).

The latter is the case with Crown Resorts Limited due to significant increase in cash and cash

equivalents in 2017 from 2016.

3.2 Gross profit margin:

Table 2: Gross profit margin of Crown Resorts Limited for the years 2016 and 2017

(Source: Crownresorts.com.au 2018)

2016 2017

94.80%

95.00%

95.20%

95.40%

95.60%

95.80%

96.00%

96.20%

96.01%

95.27%

Gross profit margin

Figure 2: Gross profit margin of Crown Resorts Limited for the years 2016 and 2017

(Source: Crownresorts.com.au 2018)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING FOR BUSINESS

Gross margin denotes the profitability of an organisation before the overhead

expenses are incurred. The greater value signifies that more cents are made per dollar of

revenue, which is favourable because greater profit would be available for covering the non-

production costs (Grant 2016). For entertainment industry, gross profit margin provides an

overview of the pricing strategies of the organisations. In case of Crown Resorts, there is a

slight decline in gross margin from 96.01% in 2016 to 95.27% in 2017. Despite such decline,

it could be stated that the organisation is following an aggressive pricing strategy by charging

greater mark-up on the products sold and services rendered to the customers.

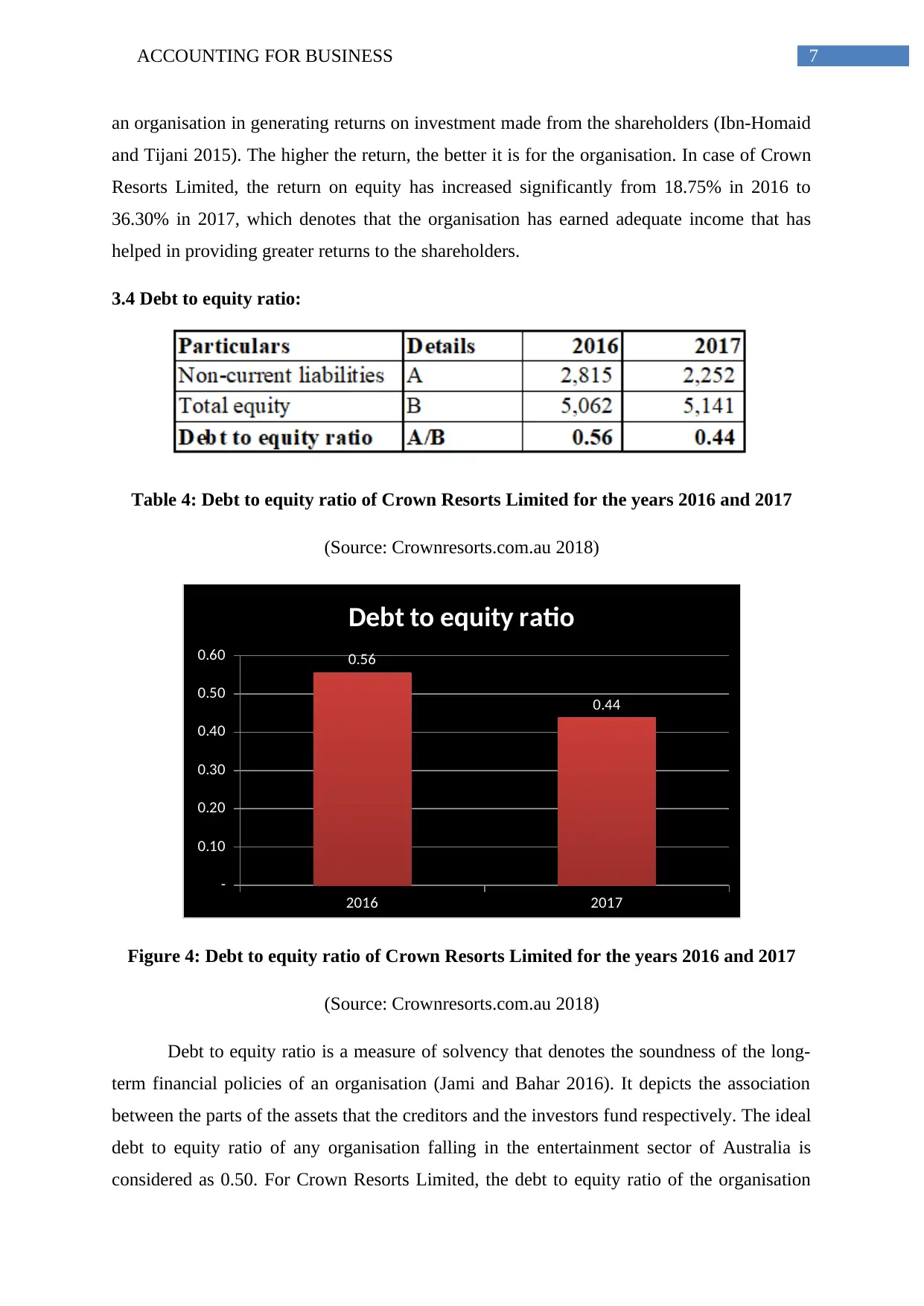

3.3 Return on equity:

Table 3: Return on equity of Crown Resorts Limited for the years 2016 and 2017

(Source: Crownresorts.com.au 2018)

2016 2017

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

18.75%

36.30%

Return on equity

Figure 3: Return on equity of Crown Resorts Limited for the years 2016 and 2017

(Source: Crownresorts.com.au 2018)

The return on equity ratio gauges the rate of return that the owners of common stock

of an organisation obtain on their shareholdings. In other words, it determines the ability of

Gross margin denotes the profitability of an organisation before the overhead

expenses are incurred. The greater value signifies that more cents are made per dollar of

revenue, which is favourable because greater profit would be available for covering the non-

production costs (Grant 2016). For entertainment industry, gross profit margin provides an

overview of the pricing strategies of the organisations. In case of Crown Resorts, there is a

slight decline in gross margin from 96.01% in 2016 to 95.27% in 2017. Despite such decline,

it could be stated that the organisation is following an aggressive pricing strategy by charging

greater mark-up on the products sold and services rendered to the customers.

3.3 Return on equity:

Table 3: Return on equity of Crown Resorts Limited for the years 2016 and 2017

(Source: Crownresorts.com.au 2018)

2016 2017

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

18.75%

36.30%

Return on equity

Figure 3: Return on equity of Crown Resorts Limited for the years 2016 and 2017

(Source: Crownresorts.com.au 2018)

The return on equity ratio gauges the rate of return that the owners of common stock

of an organisation obtain on their shareholdings. In other words, it determines the ability of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING FOR BUSINESS

an organisation in generating returns on investment made from the shareholders (Ibn-Homaid

and Tijani 2015). The higher the return, the better it is for the organisation. In case of Crown

Resorts Limited, the return on equity has increased significantly from 18.75% in 2016 to

36.30% in 2017, which denotes that the organisation has earned adequate income that has

helped in providing greater returns to the shareholders.

3.4 Debt to equity ratio:

Table 4: Debt to equity ratio of Crown Resorts Limited for the years 2016 and 2017

(Source: Crownresorts.com.au 2018)

2016 2017

-

0.10

0.20

0.30

0.40

0.50

0.60 0.56

0.44

Debt to equity ratio

Figure 4: Debt to equity ratio of Crown Resorts Limited for the years 2016 and 2017

(Source: Crownresorts.com.au 2018)

Debt to equity ratio is a measure of solvency that denotes the soundness of the long-

term financial policies of an organisation (Jami and Bahar 2016). It depicts the association

between the parts of the assets that the creditors and the investors fund respectively. The ideal

debt to equity ratio of any organisation falling in the entertainment sector of Australia is

considered as 0.50. For Crown Resorts Limited, the debt to equity ratio of the organisation

an organisation in generating returns on investment made from the shareholders (Ibn-Homaid

and Tijani 2015). The higher the return, the better it is for the organisation. In case of Crown

Resorts Limited, the return on equity has increased significantly from 18.75% in 2016 to

36.30% in 2017, which denotes that the organisation has earned adequate income that has

helped in providing greater returns to the shareholders.

3.4 Debt to equity ratio:

Table 4: Debt to equity ratio of Crown Resorts Limited for the years 2016 and 2017

(Source: Crownresorts.com.au 2018)

2016 2017

-

0.10

0.20

0.30

0.40

0.50

0.60 0.56

0.44

Debt to equity ratio

Figure 4: Debt to equity ratio of Crown Resorts Limited for the years 2016 and 2017

(Source: Crownresorts.com.au 2018)

Debt to equity ratio is a measure of solvency that denotes the soundness of the long-

term financial policies of an organisation (Jami and Bahar 2016). It depicts the association

between the parts of the assets that the creditors and the investors fund respectively. The ideal

debt to equity ratio of any organisation falling in the entertainment sector of Australia is

considered as 0.50. For Crown Resorts Limited, the debt to equity ratio of the organisation

8ACCOUNTING FOR BUSINESS

has fallen from 0.56 in 2016 to 0.44 in 2017. This signifies that the organisation obtains funds

by issuing equity shares in the market, which has helped in minimising long-term debt

burden. Hence, in terms of solvency, Crown Resorts Limited is in a favourable position in the

Australian market.

3.5 Days inventory:

Table 5: Days inventory of Crown Resorts Limited for the years 2016 and 2017

(Source: Crownresorts.com.au 2018)

2016 2017

38.60

38.80

39.00

39.20

39.40

39.60

39.80

40.00 39.84

39.11

Days inventory

Figure 5: Days inventory of Crown Resorts Limited for the years 2016 and 2017

(Source: Crownresorts.com.au 2018)

Days’ inventory is the amount of time that an organisation takes to release its

inventory. In other words, it helps in providing the investors with an idea of the time that an

organisation takes for converting its inventory into sales (Titman, Keown and Martin 2017).

The lower the number of days, the faster is the release of inventory for the organisation. In

has fallen from 0.56 in 2016 to 0.44 in 2017. This signifies that the organisation obtains funds

by issuing equity shares in the market, which has helped in minimising long-term debt

burden. Hence, in terms of solvency, Crown Resorts Limited is in a favourable position in the

Australian market.

3.5 Days inventory:

Table 5: Days inventory of Crown Resorts Limited for the years 2016 and 2017

(Source: Crownresorts.com.au 2018)

2016 2017

38.60

38.80

39.00

39.20

39.40

39.60

39.80

40.00 39.84

39.11

Days inventory

Figure 5: Days inventory of Crown Resorts Limited for the years 2016 and 2017

(Source: Crownresorts.com.au 2018)

Days’ inventory is the amount of time that an organisation takes to release its

inventory. In other words, it helps in providing the investors with an idea of the time that an

organisation takes for converting its inventory into sales (Titman, Keown and Martin 2017).

The lower the number of days, the faster is the release of inventory for the organisation. In

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING FOR BUSINESS

case of Crown Resorts Limited, it has fallen from 39.84 days in 2016 to 39.11 days in 2017,

which signifies that the inventories are released at a faster rate due to rising demand in the

market. Thus, from the efficiency point of view, it could be stated that Crown Resorts has

improved its position in the Australian market compared to 2016.

4.0 Analysis and comparison of Crown Resorts Limited with Tatts Group Limited:

For evaluating the financial position and performance of Crown Resorts Limited more

effectively, it is compared with its key competitor, Tatts Group Limited. It provides gambling

services through lotteries, wavering and gaming having operational footprint throughout

Australia and New Zealand, except Western Australia (Tatts Group 2018). The evaluation is

made by considering three ratios, which include gross margin, quick ratio and debt to equity

ratio.

Gross margin:

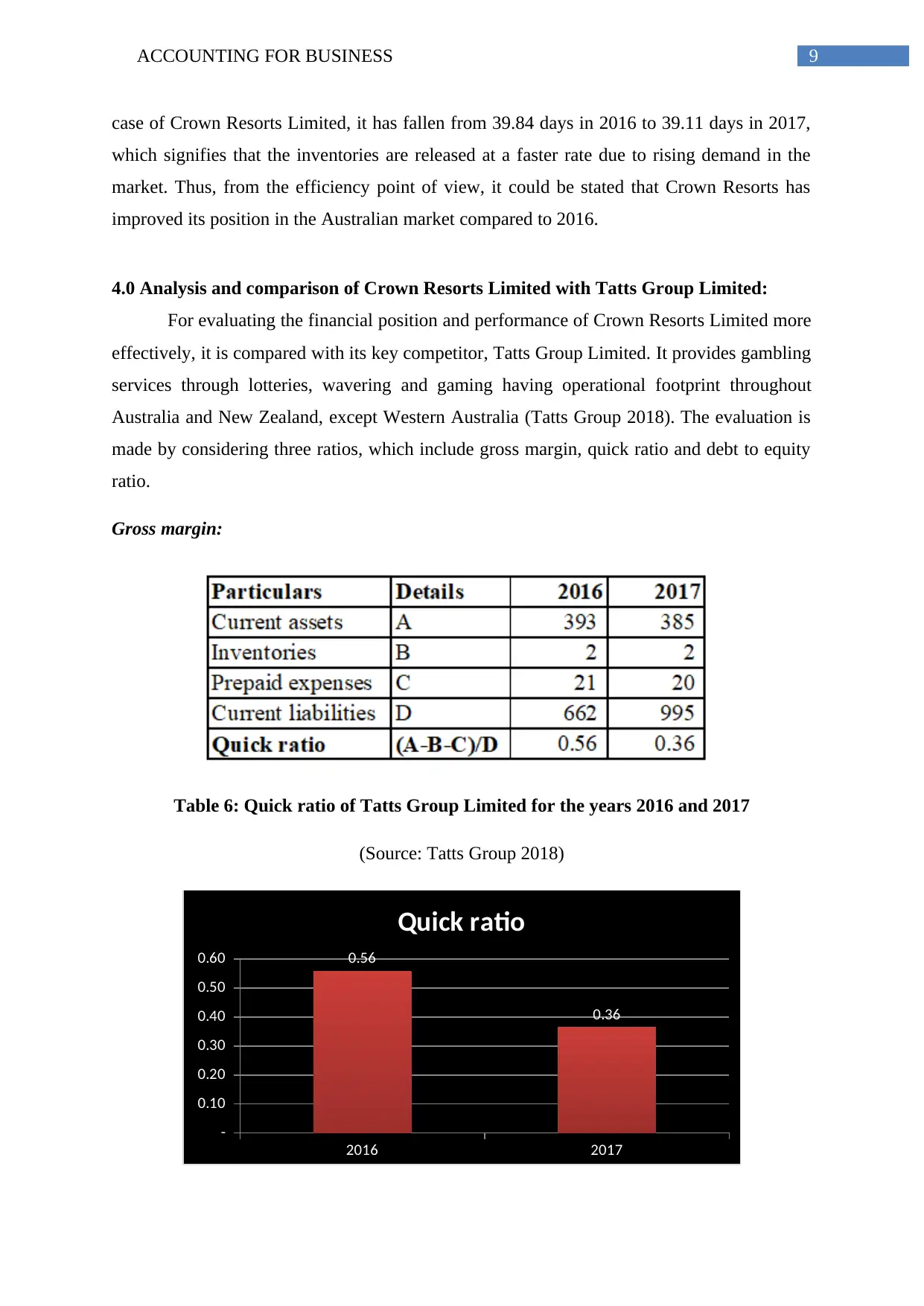

Table 6: Quick ratio of Tatts Group Limited for the years 2016 and 2017

(Source: Tatts Group 2018)

2016 2017

-

0.10

0.20

0.30

0.40

0.50

0.60 0.56

0.36

Quick ratio

case of Crown Resorts Limited, it has fallen from 39.84 days in 2016 to 39.11 days in 2017,

which signifies that the inventories are released at a faster rate due to rising demand in the

market. Thus, from the efficiency point of view, it could be stated that Crown Resorts has

improved its position in the Australian market compared to 2016.

4.0 Analysis and comparison of Crown Resorts Limited with Tatts Group Limited:

For evaluating the financial position and performance of Crown Resorts Limited more

effectively, it is compared with its key competitor, Tatts Group Limited. It provides gambling

services through lotteries, wavering and gaming having operational footprint throughout

Australia and New Zealand, except Western Australia (Tatts Group 2018). The evaluation is

made by considering three ratios, which include gross margin, quick ratio and debt to equity

ratio.

Gross margin:

Table 6: Quick ratio of Tatts Group Limited for the years 2016 and 2017

(Source: Tatts Group 2018)

2016 2017

-

0.10

0.20

0.30

0.40

0.50

0.60 0.56

0.36

Quick ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING FOR BUSINESS

Figure 6: Quick ratio of Tatts Group Limited for the years 2016 and 2017

(Source: Tatts Group 2018)

According to the above figure, it is inherent that there is significant decline in quick

ratio over the years and it is well below the ideal standard and that of its competitor, Crown

Resorts Limited. This denotes that Tatts Group is struggling to meet its existing dues with the

available short-term asset base. Hence, it could be stated that in terms of liquidity, the

position of Crown Resorts is much better compared to Tatts Group.

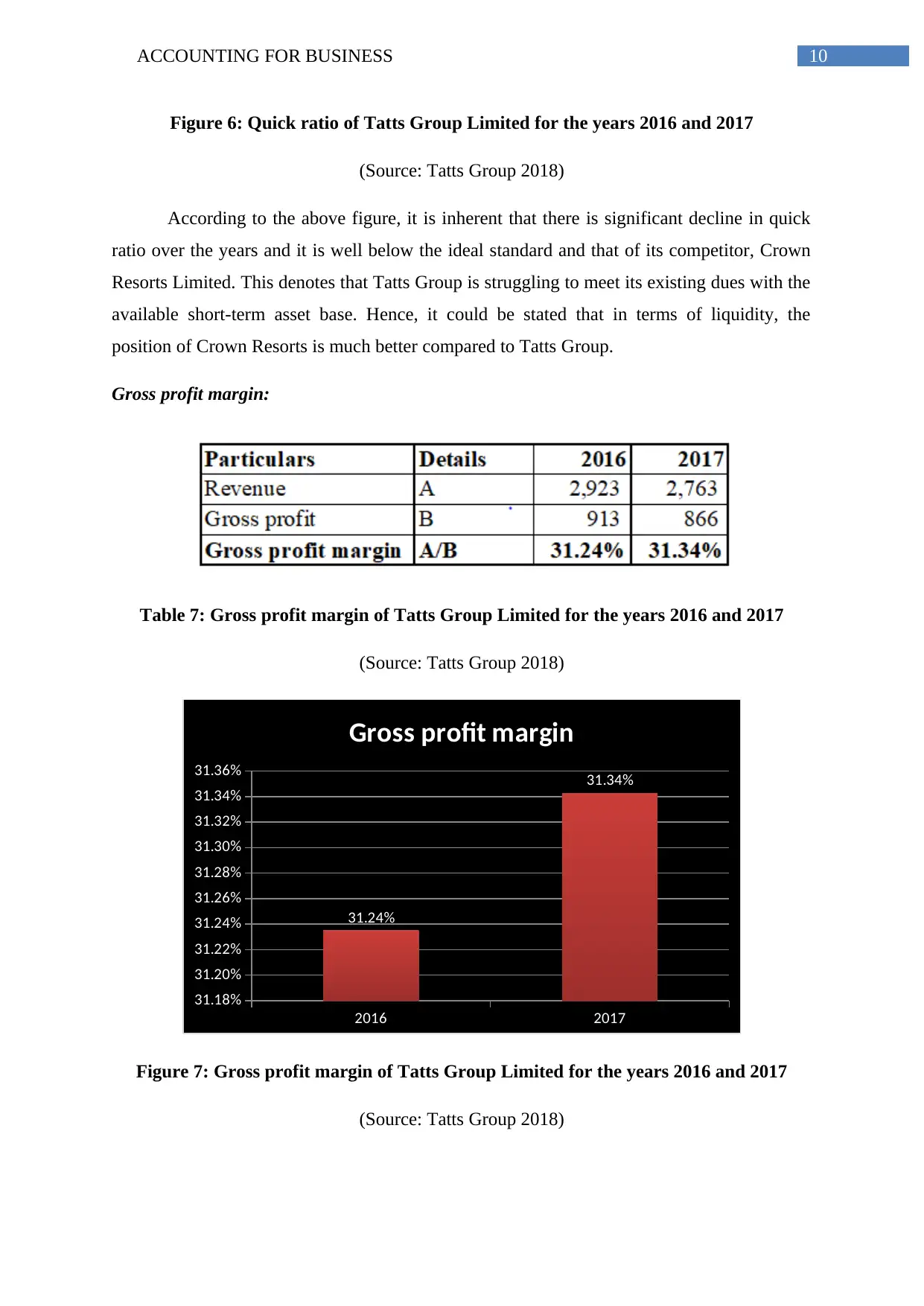

Gross profit margin:

Table 7: Gross profit margin of Tatts Group Limited for the years 2016 and 2017

(Source: Tatts Group 2018)

2016 2017

31.18%

31.20%

31.22%

31.24%

31.26%

31.28%

31.30%

31.32%

31.34%

31.36%

31.24%

31.34%

Gross profit margin

Figure 7: Gross profit margin of Tatts Group Limited for the years 2016 and 2017

(Source: Tatts Group 2018)

Figure 6: Quick ratio of Tatts Group Limited for the years 2016 and 2017

(Source: Tatts Group 2018)

According to the above figure, it is inherent that there is significant decline in quick

ratio over the years and it is well below the ideal standard and that of its competitor, Crown

Resorts Limited. This denotes that Tatts Group is struggling to meet its existing dues with the

available short-term asset base. Hence, it could be stated that in terms of liquidity, the

position of Crown Resorts is much better compared to Tatts Group.

Gross profit margin:

Table 7: Gross profit margin of Tatts Group Limited for the years 2016 and 2017

(Source: Tatts Group 2018)

2016 2017

31.18%

31.20%

31.22%

31.24%

31.26%

31.28%

31.30%

31.32%

31.34%

31.36%

31.24%

31.34%

Gross profit margin

Figure 7: Gross profit margin of Tatts Group Limited for the years 2016 and 2017

(Source: Tatts Group 2018)

11ACCOUNTING FOR BUSINESS

Based on the above table, it could be cited that the gross profit margin of the

organisation has increased from 31.24% in 2016 to 31.34% in 2017; however, it is much

lower compared to Crown Resorts Limited due to lower pricing structure (Vogel 2014).

Hence, from the profitability viewpoint, Crown Resorts Limited is enjoying competitive edge

over Tatts Group Limited in the Australian market.

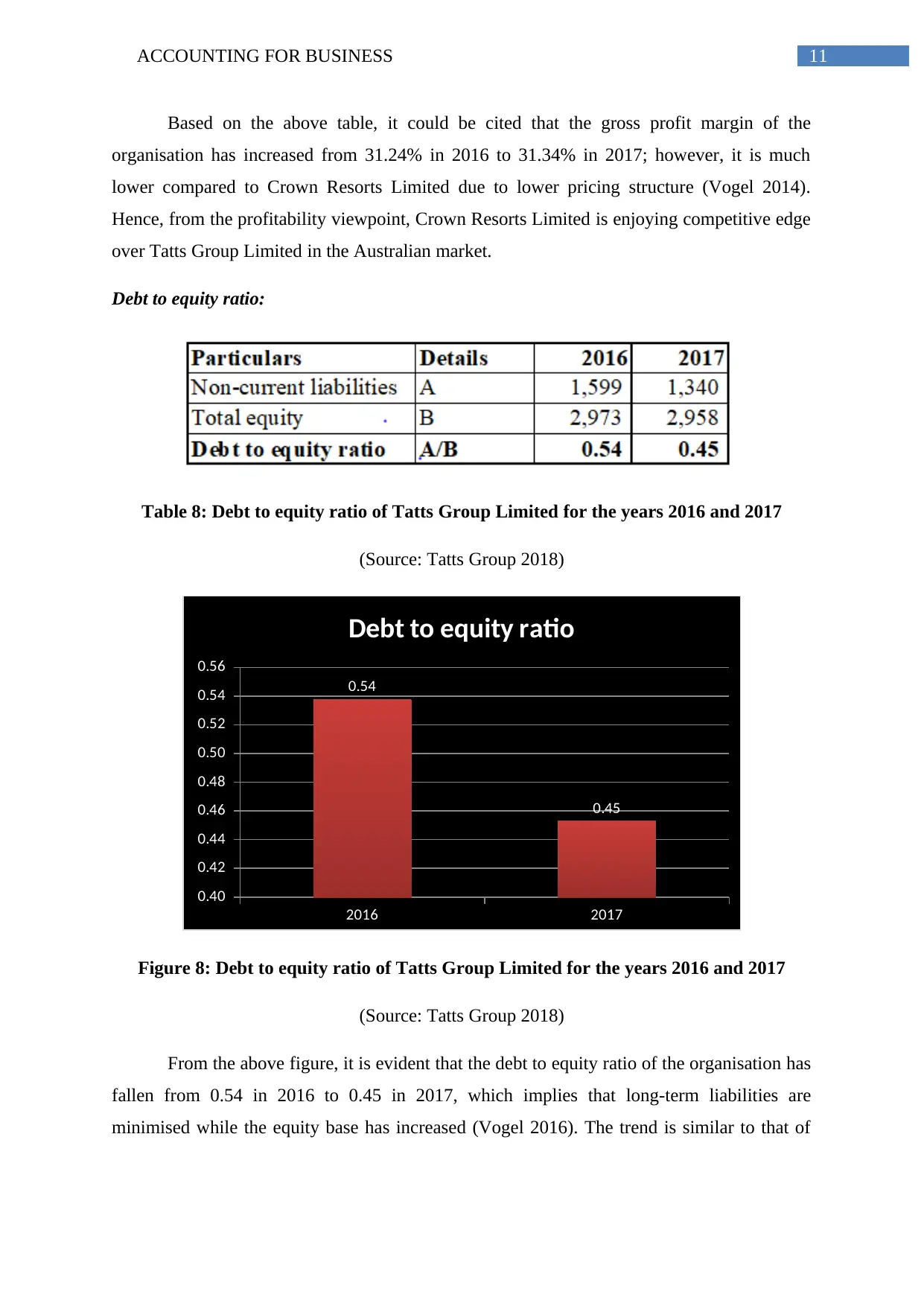

Debt to equity ratio:

Table 8: Debt to equity ratio of Tatts Group Limited for the years 2016 and 2017

(Source: Tatts Group 2018)

2016 2017

0.40

0.42

0.44

0.46

0.48

0.50

0.52

0.54

0.56

0.54

0.45

Debt to equity ratio

Figure 8: Debt to equity ratio of Tatts Group Limited for the years 2016 and 2017

(Source: Tatts Group 2018)

From the above figure, it is evident that the debt to equity ratio of the organisation has

fallen from 0.54 in 2016 to 0.45 in 2017, which implies that long-term liabilities are

minimised while the equity base has increased (Vogel 2016). The trend is similar to that of

Based on the above table, it could be cited that the gross profit margin of the

organisation has increased from 31.24% in 2016 to 31.34% in 2017; however, it is much

lower compared to Crown Resorts Limited due to lower pricing structure (Vogel 2014).

Hence, from the profitability viewpoint, Crown Resorts Limited is enjoying competitive edge

over Tatts Group Limited in the Australian market.

Debt to equity ratio:

Table 8: Debt to equity ratio of Tatts Group Limited for the years 2016 and 2017

(Source: Tatts Group 2018)

2016 2017

0.40

0.42

0.44

0.46

0.48

0.50

0.52

0.54

0.56

0.54

0.45

Debt to equity ratio

Figure 8: Debt to equity ratio of Tatts Group Limited for the years 2016 and 2017

(Source: Tatts Group 2018)

From the above figure, it is evident that the debt to equity ratio of the organisation has

fallen from 0.54 in 2016 to 0.45 in 2017, which implies that long-term liabilities are

minimised while the equity base has increased (Vogel 2016). The trend is similar to that of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.